annuity dr. vijay kumar [email protected]

TRANSCRIPT

• In our day to day life we observe a lot of money

transactions. In many money transactions payment

is made in single transaction or in equal installments

over a certain period of time.

• The amounts of these installations are determined in

such a way that they compensate for their waiting

time.

• In other cases, in order to meet future planned

expenses, a regular saving may be done, i.e., at

regular time intervals a certain amount may be kept

aside, on which the person gains interest. In such

cases the concept of annuity is used.

• A sequence of equal payments made/received at

equal intervals of time is called annuity.

• The amount of regular payment of an annuity is

called periodic payments.

• The time interval between two successive payments

is called is called payment interval or period.

Payment periods may be annual, half yearly,

quarterly, monthly or any fixed duration of time.

• The time for which the payment of an annuity is

made is called term of annuity, i.e., it is the time

interval between the first payment and the last

payment.

• The sum of all payments made and interest earned

on them at the end of the term of annuities is called

future value of an annuity, i.e., it is the total

worth of all the payments at the end of the term of

an annuity.

• The present and or capital value of an annuity is

the sum of the present values of all the payments of

the annuity at the beginning of the annuity, i.e. it is

the amount of money that must be invested in the

beginning of the annuity of purchase the payments

due in future. (payments means yearly payments)

Types of Annuity

An annuity payable for a fixed number of years is

called annuity certain.

Installments of payment for a plot of land, bank

security deposits, purchase of domestic durables

are examples of annuities certain. Here the

buyer/person knows the specified dates on which

installments are to be made.

Annuity Contingent:- An annuity payable at regular

interval of time till the happening of a specific

event or the date of which can not be foretold.

Types of Annuity…

For example, the premiums on a life insurance policy,

or a fixed sum paid to an unmarried girl at regular

intervals of time till her marriage takes place.

Perpetual Annuity or Perpetuity:- An annuity payable forever. In it, beginning date is known but the terminal date is unknown, i.e., an annuity whose payments continues forever is called perpetuity. For example – the endowment funds of trust, where the interest earned is used for welfare activities only. The principal remains the same and activity continuous forever.

1. All the above types of annuities are based on the number of their periods.

2. An annuity in which payments of installments are

made at the end of each period is called ordinary

annuity or annuity immediate, e.g. repayment of

housing loan, car loan etc.

3. An annuity in which payments of installments are

made in the beginning of each period is called annuity

due. In annuity due every payment is an investment

and earns interest. Next payment will earn interest for

one period less and so on, the last payment will earn

interest of one period, e.g. saving schemes, life

insurance, life insurance payments etc.

4. An annuity which is payable after the lapse of a

number of periods is called deferred annuity. In it ,

the term begins after certain time period termed as

deferment period, e.g., pension plan of L.I.C. Many

financial organizations give loan amount immediately

and regular installments may start after specified time

period.

Formulae

1. Amount of Immediate Annuity or ordinary

annuity.

Let a be the ordinary annuity, i % = the rate of interest per period.

The total annuity (A) for n period at i% rate of interest

is:

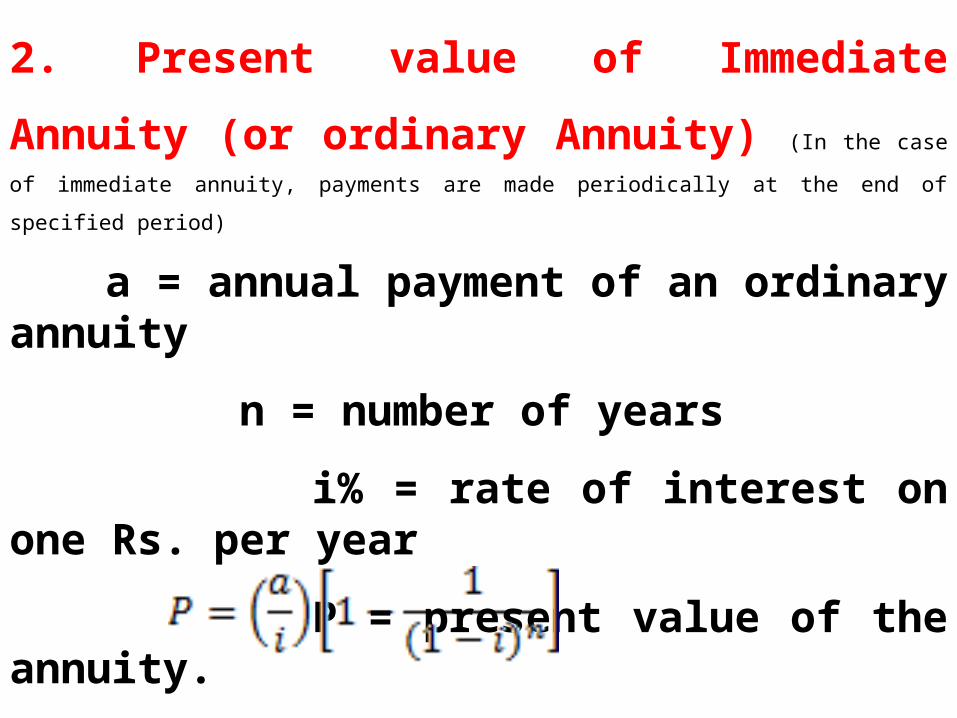

2. Present value of Immediate Annuity (or ordinary

Annuity) (In the case of immediate annuity, payments are made periodically at the end of specified

period)

a = annual payment of an ordinary annuity

n = number of years

i% = rate of interest on one Rs. per year

P = present value of the annuity.

Formulae…

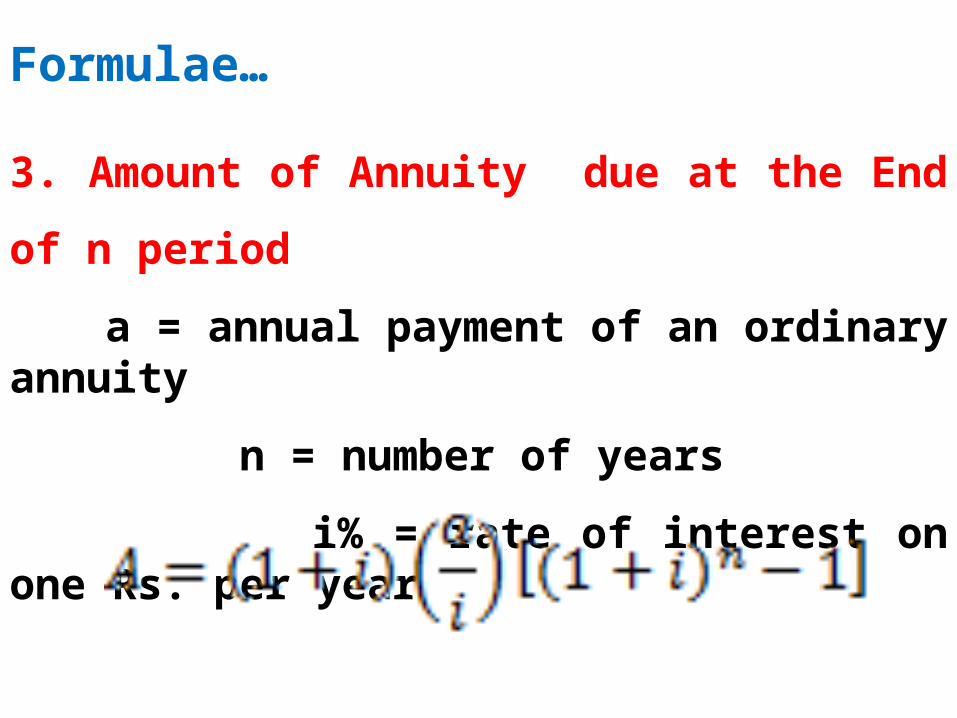

3. Amount of Annuity due at the End of n period

a = annual payment of an ordinary annuity

n = number of years

i% = rate of interest on one Rs. per year

Formulae…

4. Present value of Annuity due

a = annual payment of an ordinary annuity

n = number of years

i% = rate of interest on one Rs. per year

Formulae…

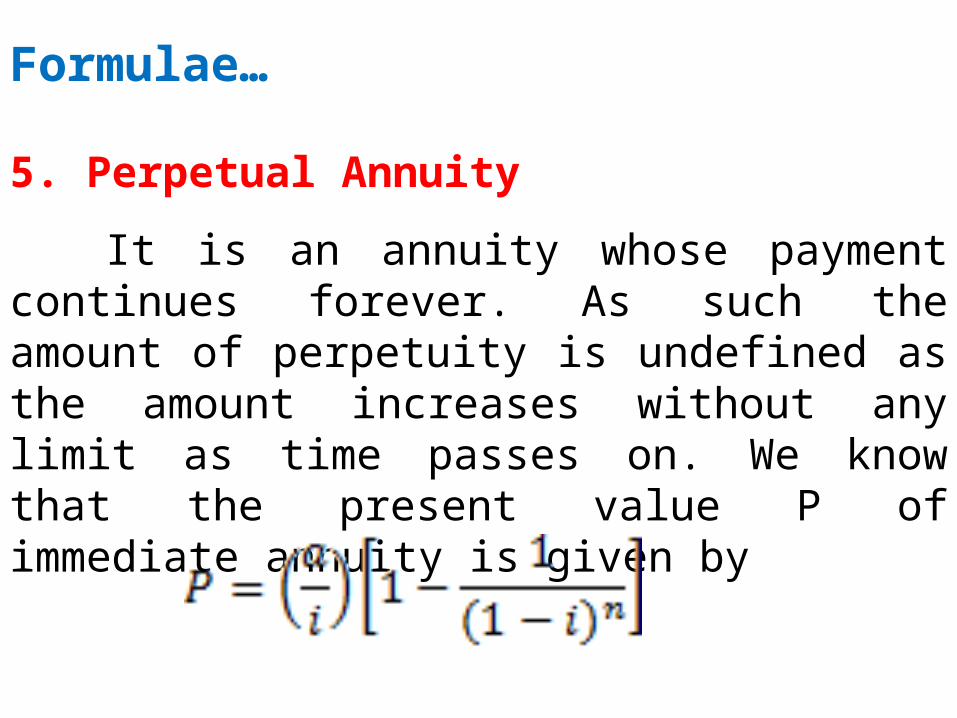

5. Perpetual Annuity

It is an annuity whose payment continues forever. As such the amount of perpetuity is undefined as the amount increases without any limit as time passes on. We know that the present value P of immediate annuity is given by

Formulae…

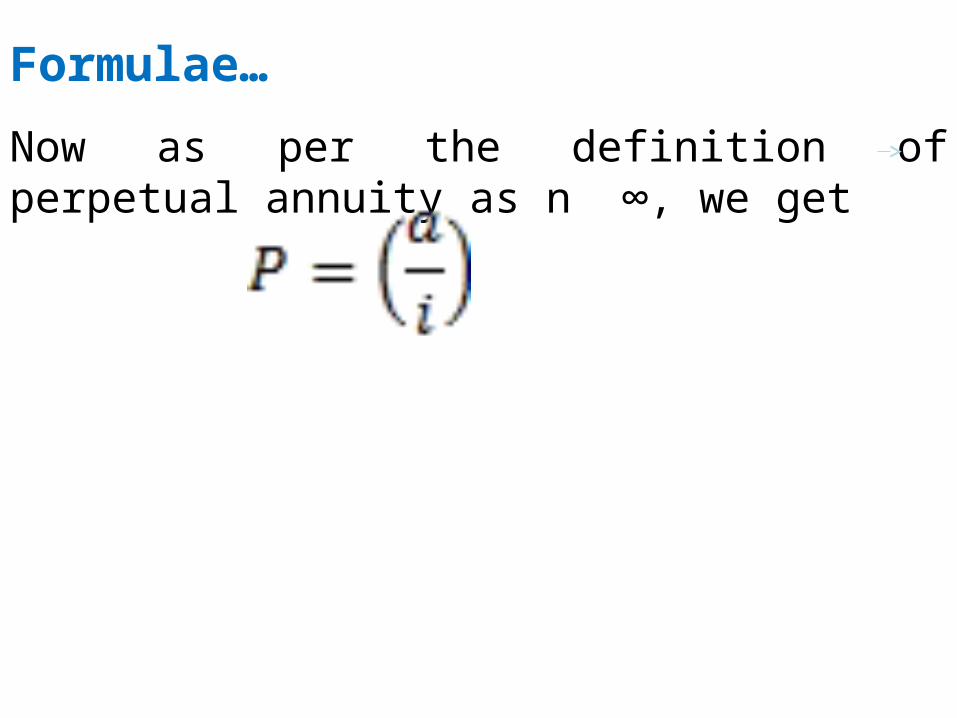

Now as per the definition of perpetual annuity as n ∞, we get

Amortization

A loan is said to be amortized if it can be removed by a

sequence of equal payments made over equal periods of

time, which consists of the interest on the loan outstanding at

the beginning of the payment period and part payments of

the loan. With each payment the principal amount

outstanding decreases and hence interest part on each

payment decreases while the loan repayment of principal

increases.

Amortization…

When a loan is amortized, the principal outstanding is

the present value of remaining payments. Based on this,

the following formulae are obtained that describe the

amortization of an interest bearing loan of Rs. A at a

rate of i per units per period, by n equal payments of

Rs. a each when the payment is made at the end of each

period.

Amortization…

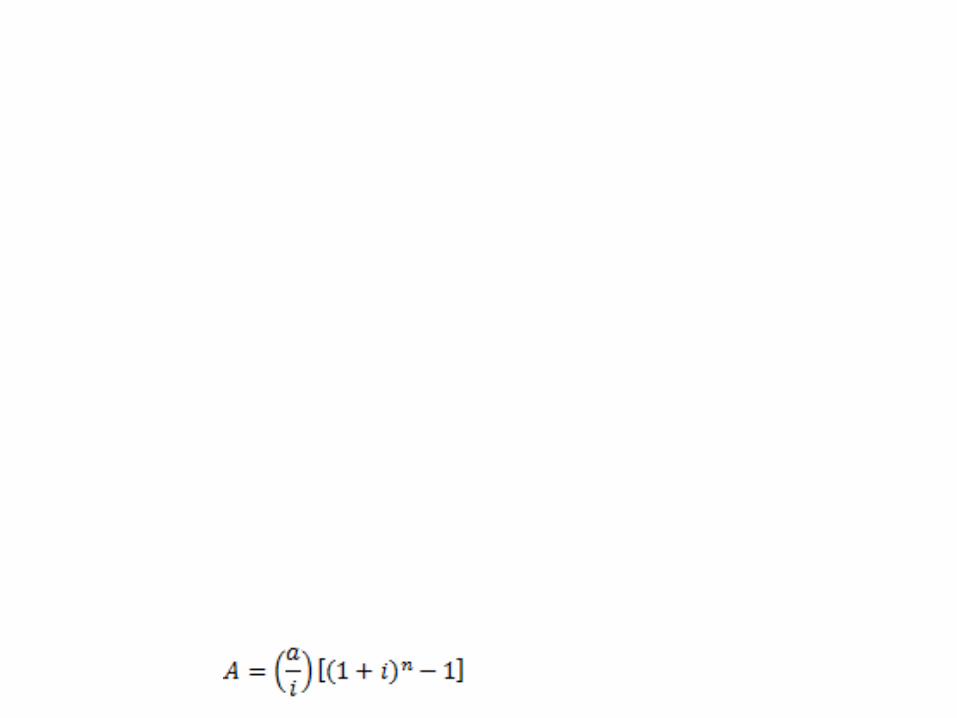

1.Amount of each periodic payment =

2.Principal outstanding of pth period =

3.Interest contained in the pth payment=

4.Principal contained in pth payment=

5.Total interest paid = (na-A)

Sinking Fund

It is the fund created by a company or person to meet

predetermined debts or certain liabilities out of their

profit at the end of every accounting year at

compound rate of interest. This fund is also known as

sinking fund.

If a is the periodic deposits or payments, at the rate of

iper units per year than after n years the sinking fund

Sinking Fund…

A is

Derivation of Formulae…

the end of first period. Therefore it earns interest for

(n-1) periods, second installment earns interest for (n-

2) periods and so on. The last installment earns for (n-

n) period, i.e. earns no interest.

The amount of first annuity for (n-1) period at i % rate

per period =