annual shareholders meeting 13 september 2007

DESCRIPTION

Annual Shareholders Meeting 13 September 2007. Chairman’s Review Rob Challinor. Overview of Investing Activities. Listed 26 October 2006 - $100m subscribed - $ 97m after issue costs To 30 June 2007: Total surplus of $21.3 million after tax - PowerPoint PPT PresentationTRANSCRIPT

Annual Shareholders

Meeting

13 September 2007

Chairman’s Review

Rob Challinor

Overview of Investing Activities• Listed 26 October 2006 - $100m subscribed - $ 97m after issue

costs

• To 30 June 2007:

– Total surplus of $21.3 million after tax

– Total net assets $120m

– Net Asset Value up 23% to $1.20 compared with 10% benchmark

– Market value of shares up 13% and warrants up 32%

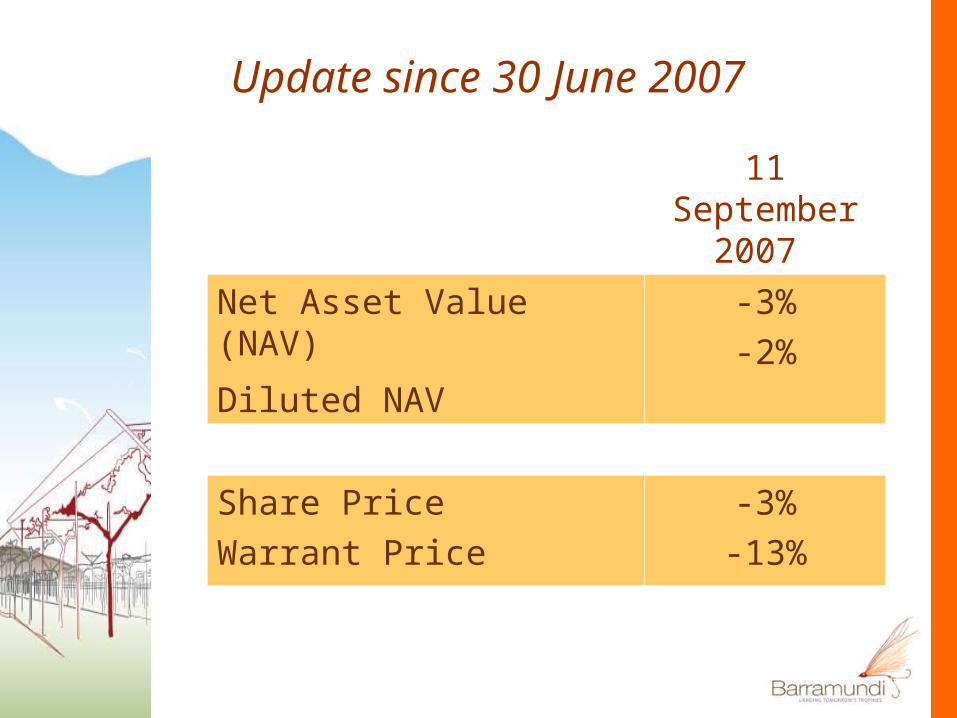

Update since 30 June 2007

11 September

2007

Net Asset Value (NAV)

Diluted NAV

-3%-2%

Share PriceWarrant Price

-3%-13%

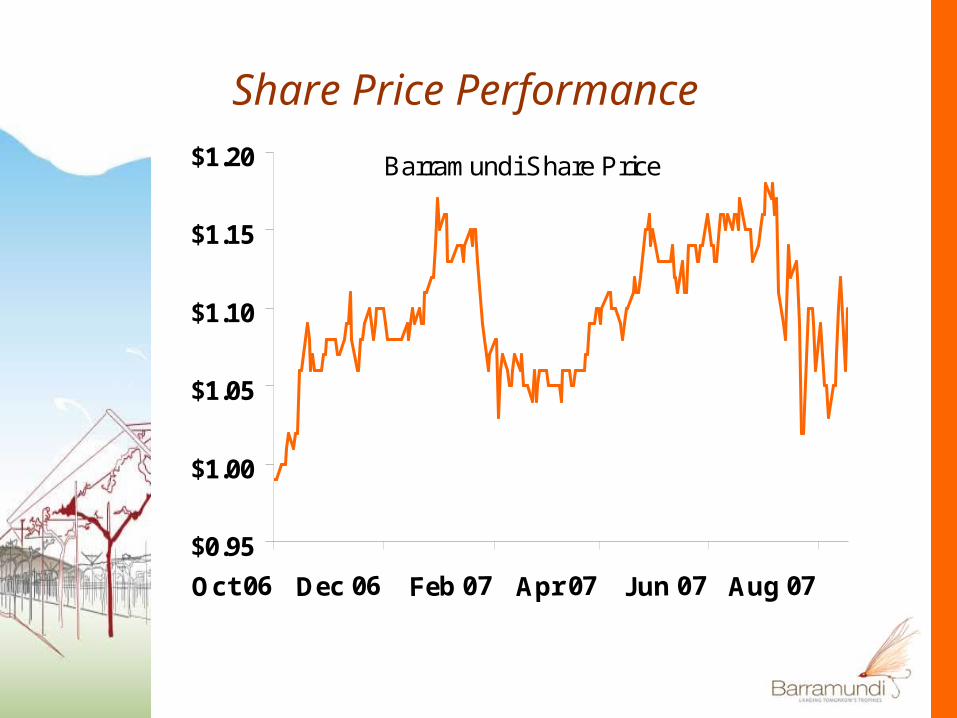

Share Price Performance

Barramundi Share Price

$0.95

$1.00

$1.05

$1.10

$1.15

$1.20

Oct 06 Dec 06 Feb 07 Apr 07 Jun 07 Aug 07

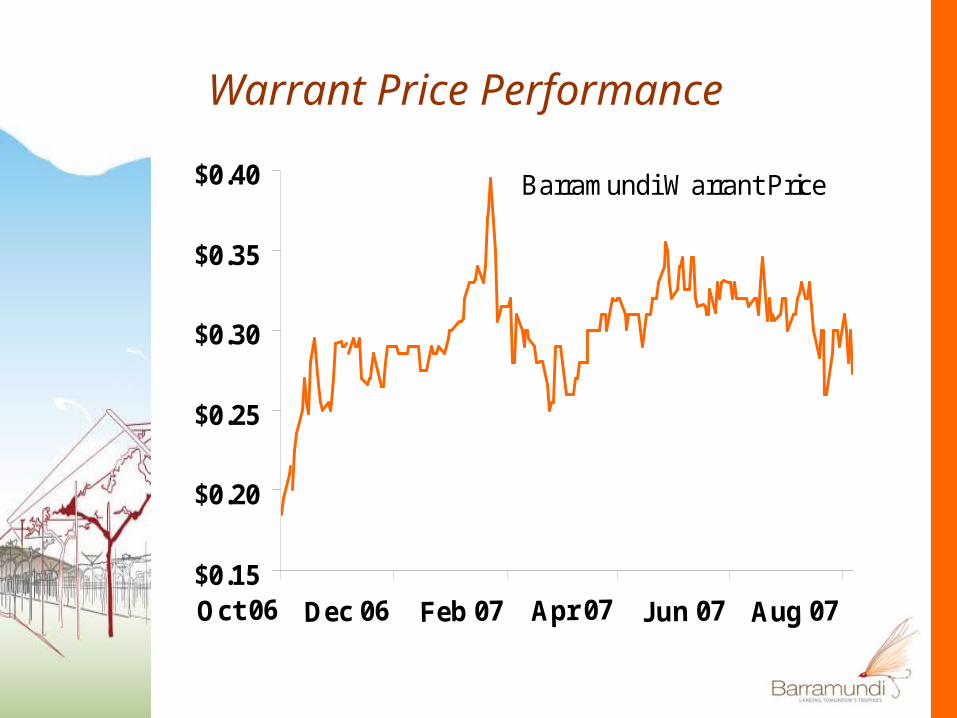

Warrant Price Performance

Barramundi Warrant Price

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

Share Price Premium/(Discount) to Diluted NAV

-10%

-5%

0%

5%

10%

15%

20%

Oct06

Dec06

Feb07

Apr07

Jun07

Aug07

NAV $m

No. Shares (m)

NAV per share

NAV 30 June 2007 120 100 $1.20

Warrants exercisable: 26 Oct 07 to 25 Oct 09

50 50 -

Diluted NAV 170 150 $1.1

3

Share Price 30 June 2007

$1.1

3

Discount to Diluted NAV

nil

Diluted Net Asset Value Calculation

– PIE Regime means not necessary to separate long and short term investments

– Short form amalgamation effected 31 August 2007

– Assets and liabilities of Barra Holdings and Barra Nursery transferred to Barramundi Limited

– Barra Holdings and Barra Nursery no longer exist

Amalgamation under Companies Act 1993

Manager’s ReportCarmel Fisher

Fisher FundsSeptember 2007

Agenda

• Review of June 2007 year – major contributors

• Review since balance date• Exam results – the fiscal year

2007 results season• Outlook

The Year to June 2007Highlights

• Built Barramundi portfolio – 16 of Australia’s best growth companies

• Enjoyed strong share price performance from a number of portfolio companies

• Placements and capital raisings allowed discounted volume access to several stocks

Lowlights

• Strong kiwi dollar took lustre off early returns

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

% c

ontr

ibut

ion

to p

erfo

rman

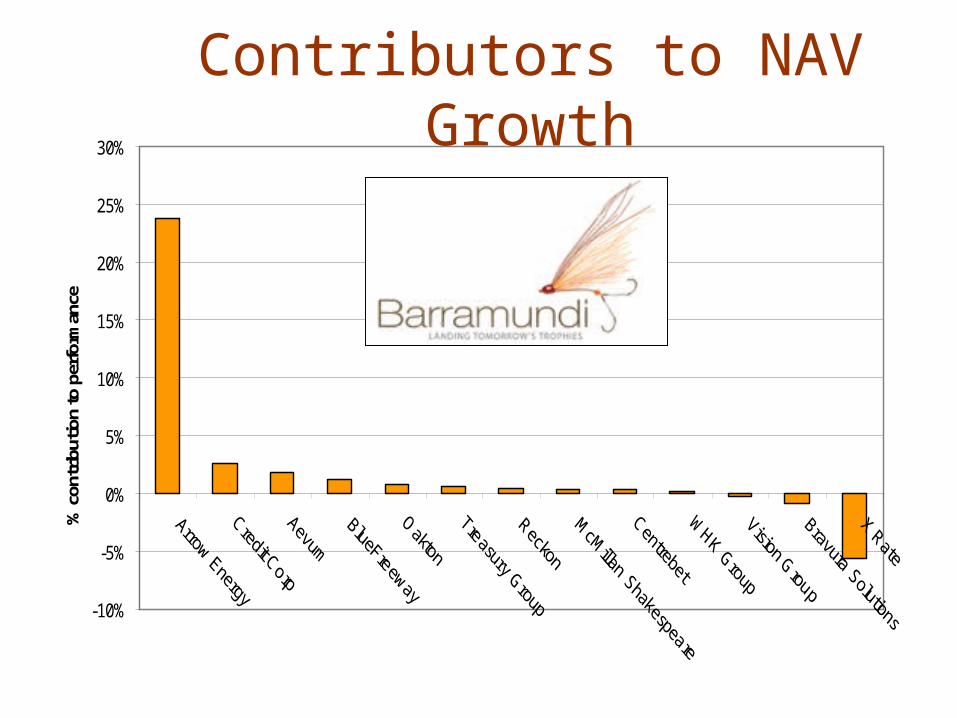

ceContributors to NAV

Growth

-50%

0%

50%

100%

150%

200%

250%

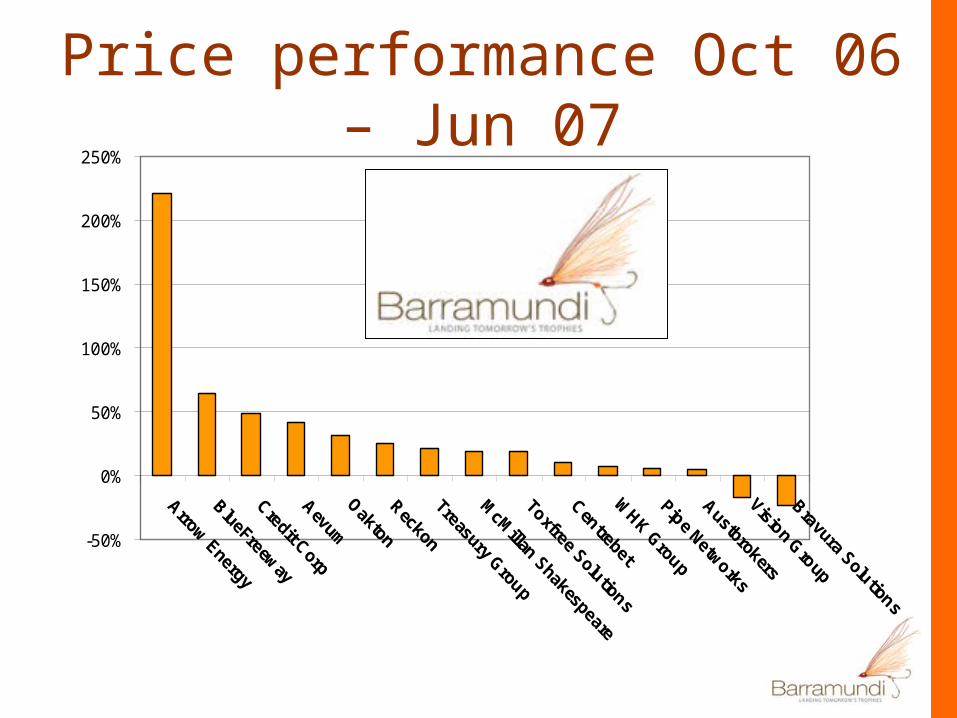

Price performance Oct 06 – Jun 07

-50%

-25%

0%

25%

50%

75%

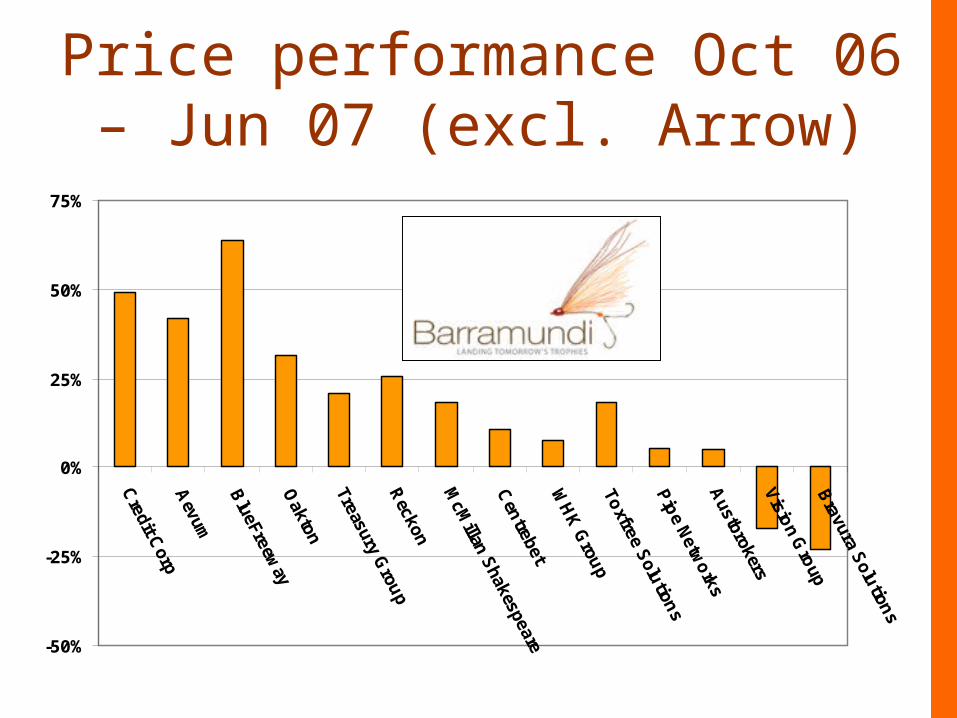

Price performance Oct 06 – Jun 07 (excl. Arrow)

-50%

0%

50%

100%

150%

200%

250%

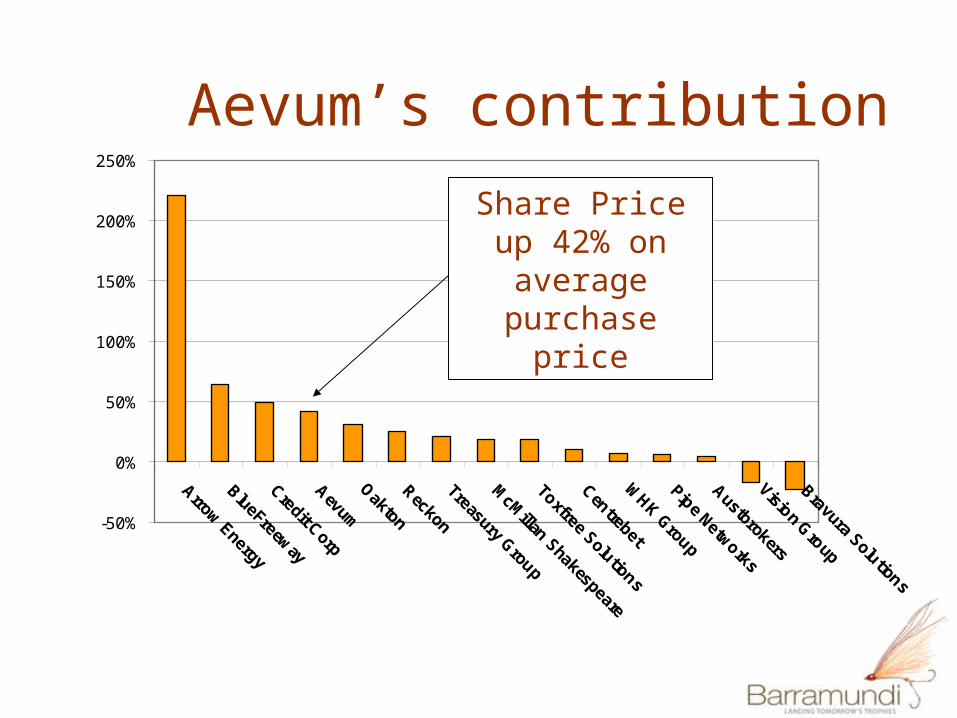

Arrow Energy

BlueFreeway

Credit Corp

Aevum

Oakton

Reckon

Treasury Group

McM

illan Shakespeare

Toxfree Solutions

Centrebet

WHK Group

Pipe Networks

Austbrokers

Vision Group

Bravura Solutions

Arrow Energy’s contribution

Share Price up 221% on average

purchase price

Arrow Energy

A leading global coal seam methane player

-50%

0%

50%

100%

150%

200%

250%

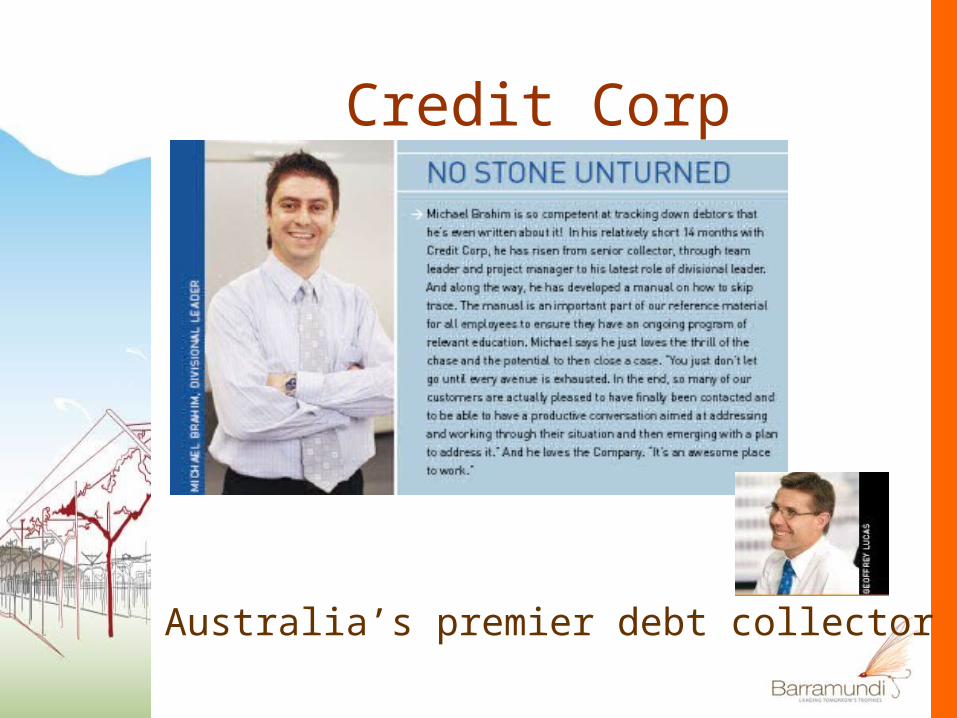

Credit Corp’s contribution

Share Price up 49% on average

purchase price

Credit Corp

Australia’s premier debt collector

-50%

0%

50%

100%

150%

200%

250%

Arrow Energy

BlueFreeway

Credit Corp

Aevum

Oakton

Reckon

Treasury Group

McM

illan Shakespeare

Toxfree Solutions

Centrebet

WHK Group

Pipe Networks

Austbrokers

Vision Group

Bravura Solutions

Aevum’s contribution

Share Price up 42% on average

purchase price

Aevum

Retirement living – great locations

Golden Ponds – Forster – Northern NSW Coast

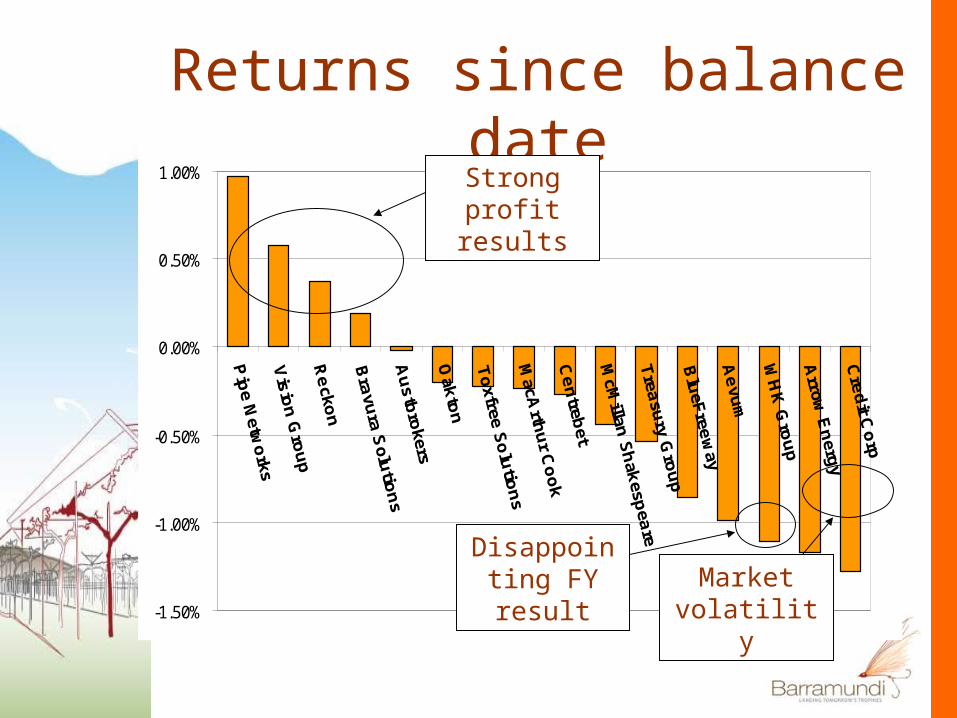

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

Returns since balance dateStrong profit

results

Market volatility

Disappointing FY result

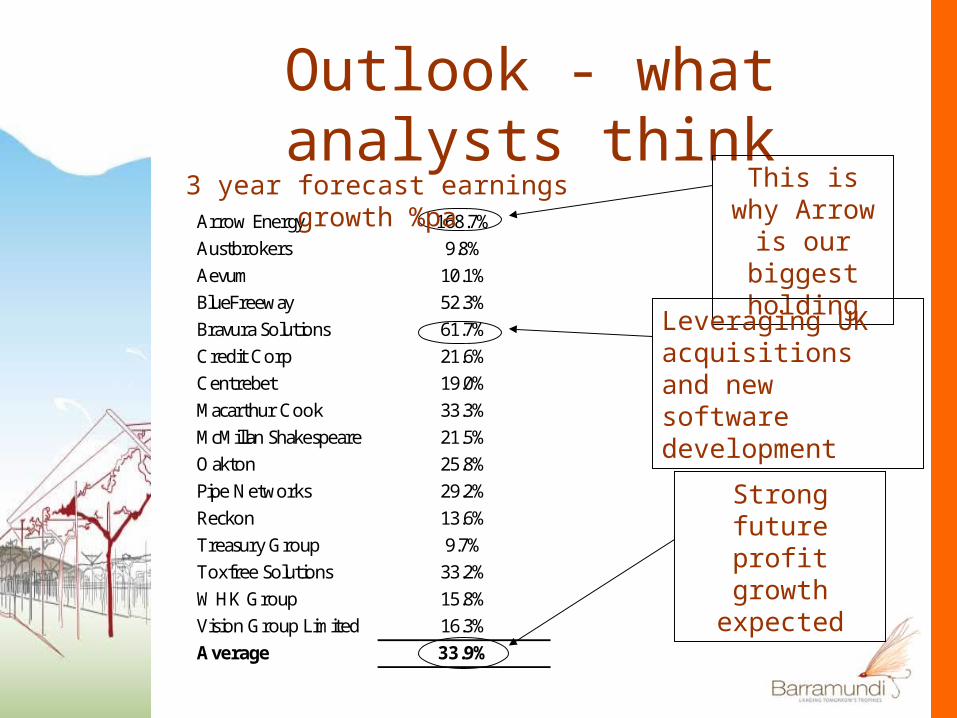

2007 results – earnings growth

Arrow Energy na

Austbrokers 22.1%

Aevum 42.0%

BlueFreeway na

Bravura Solutions 32.0%

Credit Corp 26.0%

Centrebet 214.4%

Macarthur Cook 36.9%

McMillan Shakespeare 16.8%

Oakton 38.6%

Pipe Networks 47.0%

Reckon 18.8%

Treasury Group 16.8%

Toxfree Solutions 35.0%

WHK Group 9.7%

Vision Group Limited 11.8%

Average 40.5%

First full year of profits

Disappointing – margin

pressure in accounting business

6th consecutive year of 25%+ EPS growth

Arrow Energy 168.7%

Austbrokers 9.8%

Aevum 10.1%

BlueFreeway 52.3%

Bravura Solutions 61.7%

Credit Corp 21.6%

Centrebet 19.0%

Macarthur Cook 33.3%

McMillan Shakespeare 21.5%

Oakton 25.8%

Pipe Networks 29.2%

Reckon 13.6%

Treasury Group 9.7%

Toxfree Solutions 33.2%

WHK Group 15.8%

Vision Group Limited 16.3%

Average 33.9%

Outlook - what analysts think

This is why Arrow is our

biggest holding

Strong future profit growth

expected

Leveraging UK acquisitions and new software development

3 year forecast earnings growth %pa

Our thoughts• We firmly believe we own some of

Australia’s best listed growth stocks• We are confident that the executives

of our companies will make the right “macro” decisions

• We believe it important to focus on our companies’ achievements rather than on the mood of the market

• Our best “value-add” is our extensive company visit schedule and networks

Our thoughts• The two main components of our

investments success are the stock selection and portfolio composition

• The PIE regime will be beneficial as we can more actively manage portfolio composition

• Our stock selection processes have not and will not change

• We continue to see plenty of interesting opportunities

Questions

• What is it?– Legislation, commencing 1 October

2007, changes the way managed funds (including Listed Investment Companies) are taxed

– Removes tax disadvantages to those investing in managed funds and leaves the investor in the same (or better) position whether they invest in equities directly or via a managed fund

Portfolio Investment Entity Regime

• Key Benefits to Barramundi:– Barramundi no longer taxed on capital gains

on sale of investments held on revenue account (previously held by Barra Nursery Limited)

– Distributions to shareholders will be excluded from their income tax returns

– As a PIE, there will no longer be a restriction on the distribution of capital gains to shareholders

– The ability to simplify the legal and reporting structure of the Group (through amalgamation) which will result in lower costs

Portfolio Investment Entity Regime

– Certain Australian equities will attract tax on a flat 5% of opening market values (primarily those stocks not listed on the ASX/S&P All Ordinaries Index – top 500 listed stocks)

– Dividends and any capital gains on these stocks will no longer be taxable

– Where gains on these stocks are > 5%, the fixed tax payable will represent a tax saving

– Where gains are <5%, the fixed tax payable will represent additional tax

– At 31 August 2007 Barramundi had 16% of the portfolio invested in ‘caught’ Australian equities

Foreign Investment Fund Regime