annual review 2006 - sgkb · the major stock markets were able to build on the previous year’s...

TRANSCRIPT

Annual review 2006

The private bank of Cantonal Bank of St.Gallen

HYPOSWISS Private Bank Ltd. Bahnhofstrasse/Schützengasse 4 | CH-8023 Zurich | Phone +41 (0)44 214 31 11 | Telefax +41 (0)44 211 52 23 | www.hyposwiss.ch

HYPOSWISS Private Bank Ltd. Bahnhofstrasse /Schützengasse 4CH-8023 ZurichPhone +41 (0)44 214 31 11Telefax +41 (0)44 211 52 23

www.hyposwiss.ch

Contents

Editorial 3

Annual review 4

Organs of the bank 5

Organisation 7

Key Data 2006 9

Financial section Summary 11

About the balance sheet 12

About the income statement 14

Personnel 16

Income Statement 2006 17

Balance sheet at 31 December 2006 18

Appropriation of disposable profi t 21

Cashfl ow account 22

Auditors’ report 23

SecurityFaced with the problem of increasing your assets while at the

same time minimising risk? Never tackle tricky passages alone;

always think of your safety – both elementary rules of moun-

taineering. As they are of private banking.

Dear Customer,

Dear Sir,

Dear Madam,

HYPOSWISS can look back on 2006 as a very successful fi nancial

year. All the key datas were up, some of them markedly. Our

operating income rose to CHF 112.6 m (+18 %) and net profi t to

CHF 47.5 m, representing an increase of 68 %. Customer assets

also rose very satisfactorily to a new high of CHF 12.4 billion

(+3.6 billion). These fi gures are on the one hand an expression

of the high regard in which our customers hold HYPOSWISS;

on the other hand, an excellent year on the stock markets with

some record-breaking index levels also had a positive effect on

business growth.

Our investment policy is designed to achieve above-average

yields for our customers. Particular attention should be drawn

to HYPOSWISS’s own funds, which registered excellent value-

growth over the past year, as well as to the gratifying perform-

ance of our asset-management mandates.

Among the most important events of the past year have been

the introduction of a new, modern IT platform and the expan-

sion of our Investment Centre. The dynamic growth of

HYPOSWISS also fi nds expression in the personnel sphere, our

staff having increased by 12 employee units to a new level of

146 persons.

On 1 April 2006 Hansjörg Enderli, a member of the Executive

Board and Head of Service and Logistics, retired from

HYPOSWISS after working for the bank for 32 years. Stefan

Betschart was appointed to succeed him. On 1 October 2006

Hansjürg Christen joined us as Head of Business Management,

fi lling another key post for our projected expansion at home

and abroad. On 1 December 2006 Dr Thomas Stucki entered the

employment of our bank as Chief Investment Offi cer and

member of the Executive Board. Dr Stucki is responsible for

investment policy and manages the Investment Centre.

As part of the traditional HYPOSWISS «Art in the Bank» pro-

gramme, three private views of exhibitions were held. Large

numbers of visitors accepted the invitations of Heidi Thöny,

Elisabeth Heller, Yvonne, Aline, and Fritz J. Dold and drew

inspiration from the art objects on display.

The corporate culture of HYPOSWISS is founded on our aspira-

tion (which is something that we take for granted) to achieve a

sustainable increase in value for our customers, to offer them

personal, discreet service – in fact, to place customer service at

the heart of everything we do.

So we can look forward to the future with a hefty dose of

optimism. In addition, the economic climate remains positive.

The prospects are excellent that HYPOSWISS will be able to

pursue the growth curve that the bank is currently enjoying.

I thank you most warmly for the trust you continue to place in

our institution.

Your

Marcel W. Schmid

Chief Executive Offi cer

Editorial

HYPOSWISS Annual review 2006 3

Annual review

The Executive Board (l. to r.):Stefan Betschart, Dr Thomas Stucki, Marcel W. Schmid (CEO), Martin Forster, Anton Schaad, Urs Eggenberger

As an investment year, 2006 was characterised by favourable

developments on stock markets. With the exception of Japan,

the major stock markets were able to build on the previous

year’s excellent performance - in spite of a clear course correc-

tion in spring 2006. Much of this had to do with persistently

high corporate profi ts and overwhelmingly positive economic

news.

On the interest side, rate increases by the central banks lead

to losses at the short end of the term spectrum. On the other

hand, interest rates in the medium-term and long-term seg-

ments changed only little on balance, which led to an increas-

ing levelling-out of interest curves in the principal countries.

In the USA the structure of the interest curve even took an

inverse turn.

On the foreign-exchange markets, the value of the euro in-

creased sharply against the other major currencies, the US

dollar and the yen, but also against the Swiss franc. The dimin-

ishing interest-rate gap between Europe and the USA was one

important factor in this development.

In 2006 all funds managed by the group’s own Investment

Centre turned in an above-average performance. The Danube

Tiger Fund, investing not only in shares but also in bonds from

central and eastern European countries, and the share funds

of Euroland, Switzerland, and the USA all increased by more

than 20 % each in the year under review. In the context of an

internationally favourable share environment, prudent selection

of securities by fund managers paid off. Compared with the

equivalent competitor products, the said funds were to be found

in the front rank in the year just ended.

In 2006 the Investment Centre launched a total of 70 structured

products, put together almost exclusively on the basis of shares

or raw-material values. On the other hand, the market environ-

ment for structured products on a fi xed-interest basis proved

insuffi ciently attractive for many investors. The upshot was

reduced activity in this sector.

Our portfolio managers once again achieved a very good result

in the area of asset-management mandates, clearely outdoing

the performance of their comparative indices (benchmarks) in

most investment objectives. The positive outcome is due mainly

to an overweighting in favour of share investments and raw

materials. It proved possible in this connnection to achieve a

marked increase not only in the number of mandates but also

in the volume managed.

4 HYPOSWISS Annual review 2006

Organs of the bank

Board of Directors Term of offi ce expires

Dr Urs Rüegsegger, Mörschwil, Chairman 2008

Dr Rico Jenny, Erlenbach, Vice-chairman 2009

Theodor Horat, Obfelden 2007

Executive BoardPresident (CEO)Marcel W. Schmid

MembersStefan Betschart, Managing Director

Martin Forster, Managing Director

Anton Schaad, Managing Director

Dr Thomas Stucki, Managing Director

Urs Eggenberger, Executive Director

AuditorsPricewaterhouseCoopers AG

Members of senior managementManaging DirectorsHans Bucher, Marek Wierzbicki

Executive DirectorsChristoph Angster, Markus Holenstein, Alexander Iten,

Otmar Keller, Dr Milan Kormanak, Caterina Minelle,

Rolf Müller, Patrick Schlessinger, Paul Sonderegger,

Heinz von Dach, René Wyss

DirectorsJürg Althaus, Gabriele Bosshard, Paulo Caminada,

Hansjürg E. Christen, Hans Peter Ehrler, Kurt Frischknecht,

Ernst Gfeller, Wolfgang Haller, Marc Jungi, Karl R. Keller,

Adrian D. Koller, Ueli Lott, Guido Lustenberger, René Merz,

Andreas Moser, Gregor Neidhart, Mauro Pivetta,

Daniel Reichmuth, Alfred Rüttimann, Daniel Schibli,

Roland Schneiter, Alfred Steininger, Giuseppe Stella,

Edna Weiner

HYPOSWISS Annual review 2006 5

The Board of Directors (l. to r.):Theodor Horat,Dr Urs Rüegsegger (Chairman),Dr Rico Jenny (Vice-chairman)

InnovativeTechnical innovations help to cross inhospitable terrain quickly.

It is the same when you are investing assets: being open to the

latest trends brings you more swiftly to your objective.

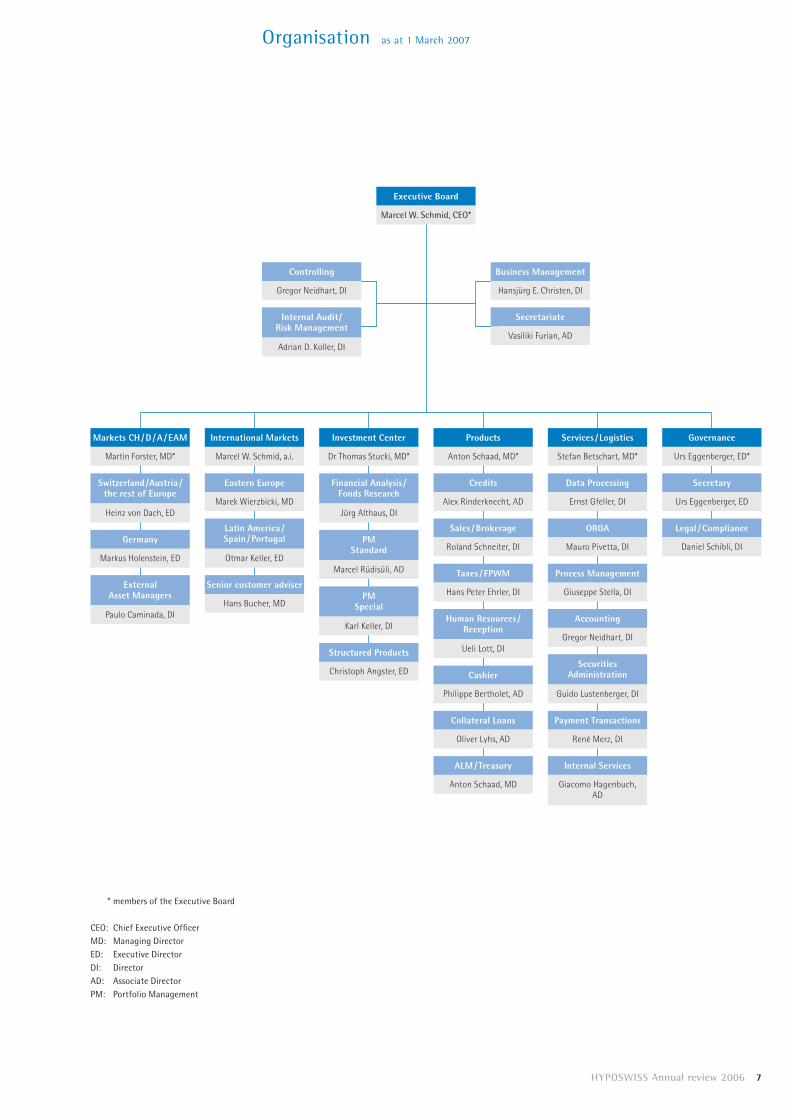

Markets CH / D / A / EAM International Markets Investment Center Products Services / Logistics Governance

Martin Forster, MD* Marcel W. Schmid, a.i. Dr Thomas Stucki, MD* Anton Schaad, MD* Stefan Betschart, MD* Urs Eggenberger, ED*

Switzerland / Austria / the rest of Europe

Eastern Europe Financial Analysis /Fonds Research

Credits Data Processing Secretary

Heinz von Dach, EDMarek Wierzbicki, MD

Jürg Althaus, DIAlex Rinderknecht, AD Ernst Gfeller, DI Urs Eggenberger, ED

GermanyLatin America /Spain / Portugal PM

Standard

Sales / Brokerage ORGA Legal / Compliance

Markus Holenstein, ED Otmar Keller, EDMarcel Rüdisüli, AD

Roland Schneiter, DI Mauro Pivetta, DI Daniel Schibli, DI

External Asset Managers

Senior customer adviserPM

Special

Taxes / FPWM Process Management

Paulo Caminada, DIHans Bucher, MD

Karl Keller, DI

Hans Peter Ehrler, DI Giuseppe Stella, DI

Structured Products

Human Resources / Reception

Accounting

Christoph Angster, ED

Ueli Lott, DIGregor Neidhart, DI

CashierSecurities

Administration

Philippe Bertholet, AD Guido Lustenberger, DI

Collateral Loans Payment Transactions

Oliver Lyhs, AD René Merz, DI

ALM / Treasury Internal Services

Anton Schaad, MD Giacomo Hagenbuch,AD

Executive Board

Marcel W. Schmid, CEO*

Business Management

Hansjürg E. Christen, DI

Secretariate

Vasiliki Furian, AD

Controlling

Gregor Neidhart, DI

Internal Audit / Risk Management

Adrian D. Koller, DI

Organisation as at 1 March 2007

* members of the Executive Board

CEO: Chief Executive Offi cerMD: Managing DirectorED: Executive DirectorDI: DirectorAD: Associate DirectorPM: Portfolio Management

HYPOSWISS Annual review 2006 7

Teamwork The more two people go through together, the better they

understand each other. Personal and demanding subjects also

belong in a truly confi dential dialogue.

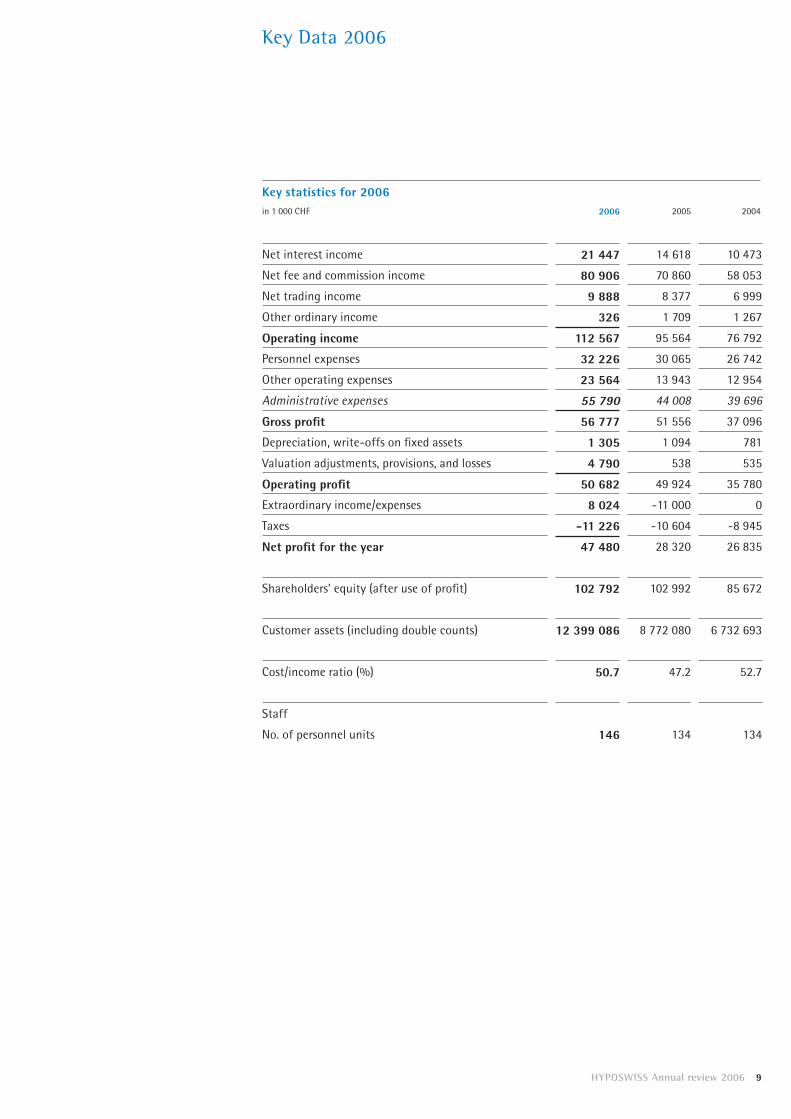

Key statistics for 2006in 1 000 CHF 2006 2005 2004

Net interest income 21 447 14 618 10 473

Net fee and commission income 80 906 70 860 58 053

Net trading income 9 888 8 377 6 999

Other ordinary income 326 1 709 1 267

Operating income 112 567 95 564 76 792

Personnel expenses 32 226 30 065 26 742

Other operating expenses 23 564 13 943 12 954

Administrative expenses 55 790 44 008 39 696

Gross profi t 56 777 51 556 37 096

Depreciation, write-offs on fi xed assets 1 305 1 094 781

Valuation adjustments, provisions, and losses 4 790 538 535

Operating profi t 50 682 49 924 35 780

Extraordinary income/expenses 8 024 -11 000 0

Taxes -11 226 -10 604 -8 945

Net profi t for the year 47 480 28 320 26 835

Shareholders’ equity (after use of profi t) 102 792 102 992 85 672

Customer assets (including double counts) 12 399 086 8 772 080 6 732 693

Cost/income ratio (%) 50.7 47.2 52.7

Staff

No. of personnel units 146 134 134

Key Data 2006

HYPOSWISS Annual review 2006 9

CompetitiveTechnique, strength, equipment, mental attitude. For top

performances such as those produced by four-times world

champion snowboarder Ursula Bruhin, whom HYPOSWISS

has sponsored for years, many things have to slot together.

She must also possess enormous endurance and a fi erce

determination to succeed.

In a highly dynamic environment HYPOSWISS achieved an

outstanding result. For the fi rst time the bank’s operating income

exceeded CHF 100 m; to be precise, it reached CHF 112.6 m.

Administrative expenses rose by 27 % to CHF 55.8 m. A large

part of this cost increase was due to project and migration

costs for the changeover to the Avaloq Banking System. Thanks

to the new operating system, from 2007 onwards IT operating

costs will be very much lower. As a result, gross profi t rose

disproportionately by CHF 5.2 m or 10 %; the previous year’s

CHF 51.6 m became CHF 56.8 m. Leaving the said costs out of

account, a gross profi t of CHF 64.5 m would have resulted,

corresponding to an increase of 25 % over the previous year.

Depreciation and write-offs on fi xed assets were slightly up on

the previous year, as a result of one-off licensing costs for the

new EDP-system being entered on the assets side. During the

course of 2006, mortgage-secured loans were subjected to

thorough scrutiny. It turned out that certain items were critical.

To take account of this circumstance, reserves in the amount

of CHF 3.7 m were formed, a fi gure that corresponds to 0.44 %

of loans granted.

Extraordinary income includes the projected dissolution of

reserves for general banking risks in the amount of the project

and migration costs incurred plus a liquidation profi t.

The net profi t for the year of CHF 47.5 m achieved made it

possible substantially to increase our dividend distribution to

our shareholder from CHF 22.0 m to CHF 40.0 m.

As a result of the investments described, the proportion of

administrative expenses including depreciation and write-offs

on fi xed assets went up from 47 % to 51 % in the year under

review.

The balance-sheet total shown by HYPOSWISS at the end of

the fi nancial year was CHF 1 147.8 m. This corresponds to

an increase of CHF 211.3 m or 23 % compared with the previous

year’s fi gure of CHF 936.4 m. Total shareholders’ equity, after

use of profi t, are shown as CHF 102.8 m, corresponding to a

degree of self-fi nancing of 9 %.

Customer deposits and current assets shown went up markedly

in the course of the fi nancial year from CHF 8.8 billion to

CHF 12.4 billion. That fi gure includes CHF 934.4 m due to the

fi ve HYPOSWISS investment funds. People who have been

customers for many years and new customers entrusted

HYPOSWISS with new money in the amount of CHF 2 691.2 m

for the bank to invest and manage.

Financial section

Summary

HYPOSWISS Annual review 2006 11

Of which loans to customersTotal 840 870 (in 1 000 CHF )

AssetsBalance-sheet total 1 147 753 (in 1 000 CHF )

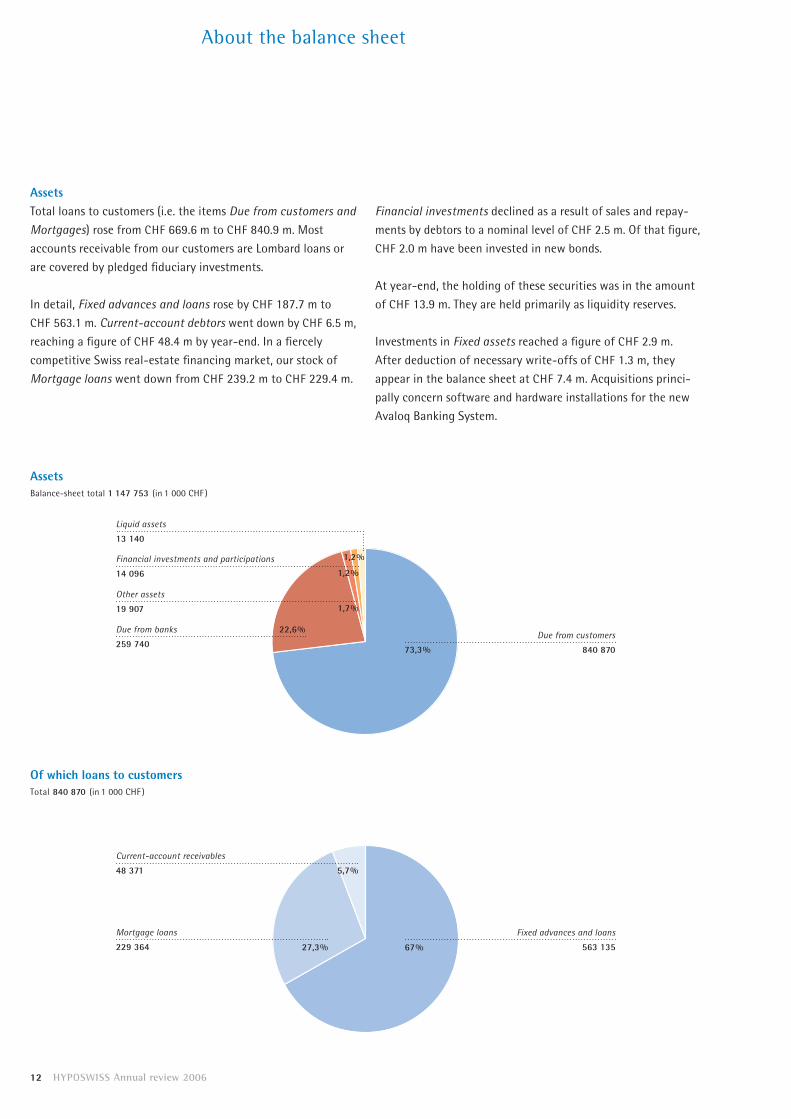

Assets Total loans to customers (i.e. the items Due from customers and Mortgages) rose from CHF 669.6 m to CHF 840.9 m. Most

accounts receivable from our customers are Lombard loans or

are covered by pledged fi duciary investments.

In detail, Fixed advances and loans rose by CHF 187.7 m to

CHF 563.1 m. Current-account debtors went down by CHF 6.5 m,

reaching a fi gure of CHF 48.4 m by year-end. In a fi ercely

competitive Swiss real-estate fi nancing market, our stock of

Mortgage loans went down from CHF 239.2 m to CHF 229.4 m.

Financial investments declined as a result of sales and repay-

ments by debtors to a nominal level of CHF 2.5 m. Of that fi gure,

CHF 2.0 m have been invested in new bonds.

At year-end, the holding of these securities was in the amount

of CHF 13.9 m. They are held primarily as liquidity reserves.

Investments in Fixed assets reached a fi gure of CHF 2.9 m.

After deduction of necessary write-offs of CHF 1.3 m, they

appear in the balance sheet at CHF 7.4 m. Acquisitions princi-

pally concern software and hardware installations for the new

Avaloq Banking System.

About the balance sheet

Due from customers

840 870

Financial investments and participations

14 096 1,2 %

Due from banks

259 740

Mortgage loans

229 364 27,3 %

Current-account receivables

48 371 5,7 %

Fixed advances and loans

563 13567 %

Other assets

19 907 1,7 %

73,3 %

22,6 %

12 HYPOSWISS Annual review 2006

Liquid assets

13 140

1,2 %

Liabilities By the end of the fi nancial year funds entrusted to HYPOSWISS

by customers totalled CHF 573.2 m. This corresponds to an

increase of CHF 112.5 m or 24 %. The biggest item on the balance

sheet is Other amounts due to customers at CHF 550.3 m,

followed by Amounts due to customers in the form of savings and deposits at CHF 19.1 m. Medium-term notes went up to

CHF 3.8 m. Substantially higher long-term interest rates led over

the course of the fi nancial year to our customers once again

investing more heavily in HYPOSWISS time-deposit investments.

These climbed from CHF 17.3 m to CHF 107.2 m.

Because of the sharp rise in loans to customers, Amounts due to banks went up by CHF 101.2 m to CHF 326.2 m. Long-term

mortgage-backed bonds declined by CHF 15.0 m to a fi gure of

CHF 56.0 m.

Share capital stands unchanged at CHF 26.0 m, while open

reserves after use of profi t are shown at CHF 67.5 m.

Demand deposits

443 01277,3 %

Amounts due to customers in the form of savings or deposits

19 087 3.3 %

Time deposits

107 248 18.7 %

Medium-term notes

3 825

0,7 %

Mortgage-backed bonds

56 000

Customer deposits

573 172

LiabilitiesBalance-sheet total 1 147 753 (in 1 000 CHF )

4.9 %

Due to banks

326 240 28.4 %

Other liabilities

97 029

Shareholders’ equity

95 312 8.3 %

49,9 %

Of which customer depositsTotal 573 172 (in 1 000 CHF )

8.5 %

HYPOSWISS Annual review 2006 13

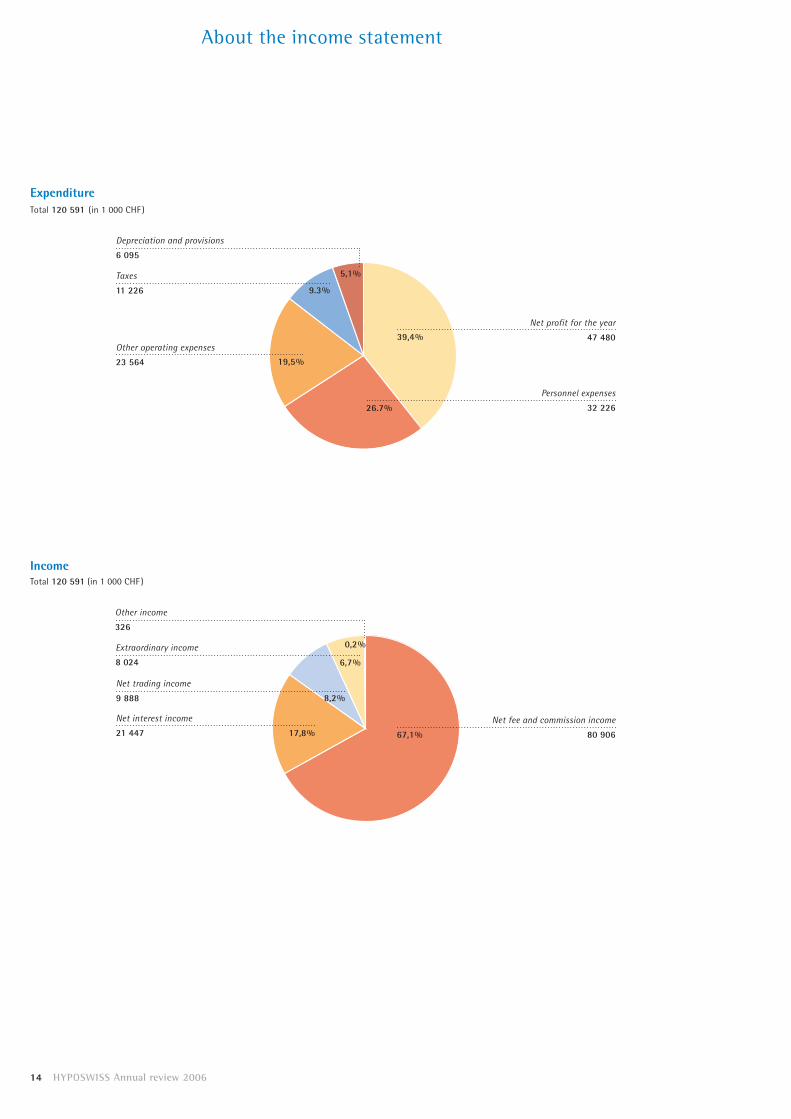

About the income statement

Depreciation and provisions

6 095

5,1 %

Personnel expenses

32 22626.7 %

Net profi t for the year

47 48039,4 %

Net fee and commission income

80 90667,1 %

Extraordinary income

8 024

Other income

326

0,2 %

Net trading income

9 888 8,2 %

6,7 %

Taxes

11 226 9.3 %

ExpenditureTotal 120 591 (in 1 000 CHF )

IncomeTotal 120 591 (in 1 000 CHF )

Other operating expenses

23 564 19,5 %

Net interest income

21 447 17,8 %

14 HYPOSWISS Annual review 2006

We were able, during the year under review, to increase Net interest income by CHF 6.8 m to CHF 21.4 m. This result was

made possible by rising interest rates in the year under review

as well as by an increase in loans to customers.

Continued favourable development of international capital

and money markets affected the fee and commission business

of HYPOSWISS (our core activity) in an extremely satisfactory

way. We were able to boost earnings by a further CHF 10.0 m

compared with the previous year, reaching CHF 80.9 m. Earnings

from the fi ve HYPOSWISS investment funds also grew satis-

factorily.

Net trading income was increased by CHF 1.5 m to CHF 9.9 m.

Contributory causes were customer transactions and (to a lesser

extent) proprietary trading as well.

Administrative expenses increased in the year under review by

CHF 11.8 m, reaching a fi gure of CHF 55.8 m. Greater staff

numbers led to higher salary costs and the concomitant social-

security contributions. Moreover, performance-related bonuses

went up as a result of the positive development of the operat-

ing profi t.

Other operating expenses rose by CHF 9.6 m in the year under

review, reaching CHF 23.6 m. A major part of this cost increase

(namely, CHF 7.7 m) was due to project and migration costs for

the new Avaloq Banking System.

The dissolution of reserves for general banking risks entered

under Extraordinary income was effected in order to offset the

project and migration costs for the Avaloq Banking System.

In the previous year CHF 11.0 m had been added to the reserve

for this purpose. Moreover, this item includes the profi t realised

from liquidation of HYPOSWISS Fund Management Company SA,

Luxembourg.

HYPOSWISS Annual review 2006 15

Personnel

During the course of the year under review the following

promotions were made to senior management level:

To Managing Directors

Hans Bucher, Marek Wierzbicki

To Executive Director

Caterina Minelle

To Directors

Paulo Caminada, Ueli Lott

We attach enormous importance to the ongoing training and

development of our employees. Consequently, much use was

once again made during the year under review of the wide range

of in-service and external training opportunities available.

It was with the greatest sympathy and regret that we took leave,

in the past year, of a long-serving customer adviser and member

of senior management, Kurt W. Buchmann. Mr Buchmann died

in Zurich on 1 June 2006 after a brief but severe illness. We shall

hold him in honoured memory.

Our thanks go to each and every member of our staff for their

great commitment and for special services rendered in connec-

tion with introducing the new IT platform.

Zurich, 25 January 2007

For the Board of Directors: For the Executive Board:

Dr Urs Rüegsegger, Chairman Marcel W. Schmid, CEO

16 HYPOSWISS Annual review 2006

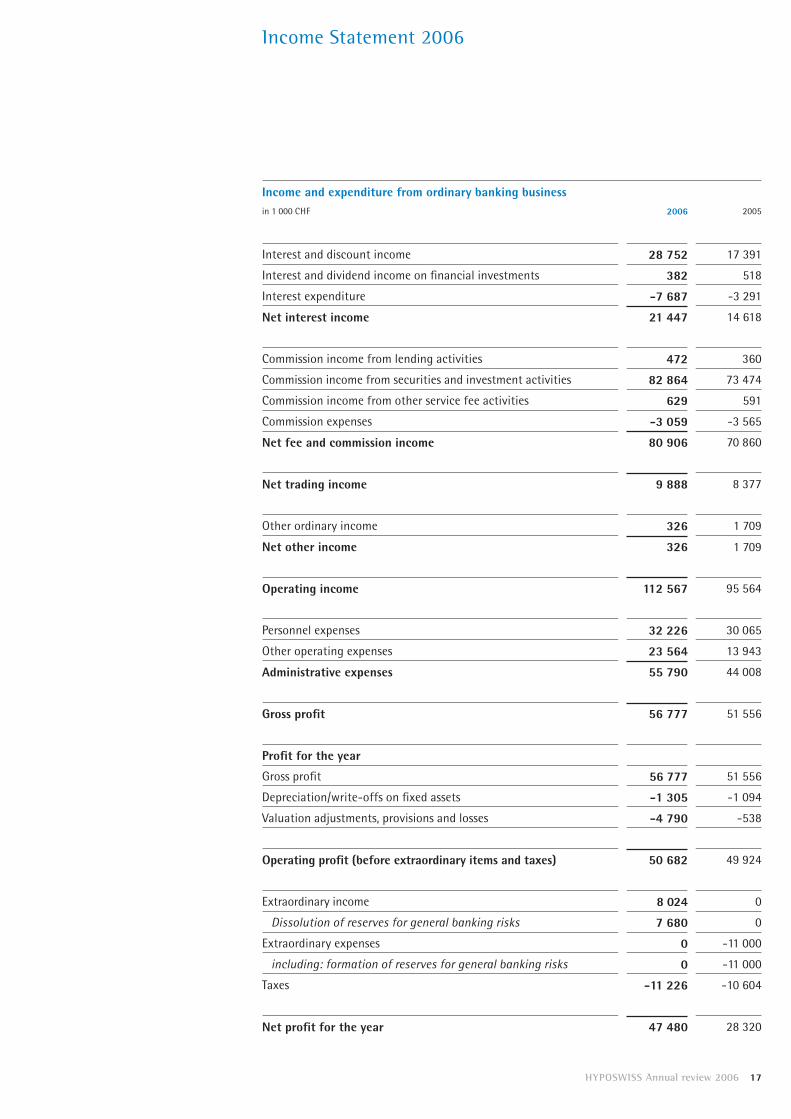

Income and expenditure from ordinary banking businessin 1 000 CHF 2006 2005

Interest and discount income 28 752 17 391

Interest and dividend income on fi nancial investments 382 518

Interest expenditure -7 687 -3 291

Net interest income 21 447 14 618

Commission income from lending activities 472 360

Commission income from securities and investment activities 82 864 73 474

Commission income from other service fee activities 629 591

Commission expenses -3 059 -3 565

Net fee and commission income 80 906 70 860

Net trading income 9 888 8 377

Other ordinary income 326 1 709

Net other income 326 1 709

Operating income 112 567 95 564

Personnel expenses 32 226 30 065

Other operating expenses 23 564 13 943

Administrative expenses 55 790 44 008

Gross profi t 56 777 51 556

Profi t for the year

Gross profi t 56 777 51 556

Depreciation/write-offs on fi xed assets -1 305 -1 094

Valuation adjustments, provisions and losses -4 790 -538

Operating profi t (before extraordinary items and taxes) 50 682 49 924

Extraordinary income 8 024 0

Dissolution of reserves for general banking risks 7 680 0

Extraordinary expenses 0 -11 000

including: formation of reserves for general banking risks 0 -11 000

Taxes -11 226 -10 604

Net profi t for the year 47 480 28 320

Income Statement 2006

HYPOSWISS Annual review 2006 17

Assets in 1 000 CHF 2006 2005

Liquid assets 13 140 13 062

Accounts receivable from money-market securities 0 9 971

Due from banks 259 740 213 600

Due from customers 611 506 430 332

Mortgage loans 229 364 239 227

Financial investments 13 912 14 498

Participation 184 409

Fixed assets 7 364 5 815

Accrued income and prepaid expenses 7 342 3 126

Other assets 5 201 6 382

Total assets 1 147 753 936 422

Total due from group companies and qualifi ed participants

149 129 160 486

Balance sheet at 31 December 2006 before use of profit

18 HYPOSWISS Annual review 2006

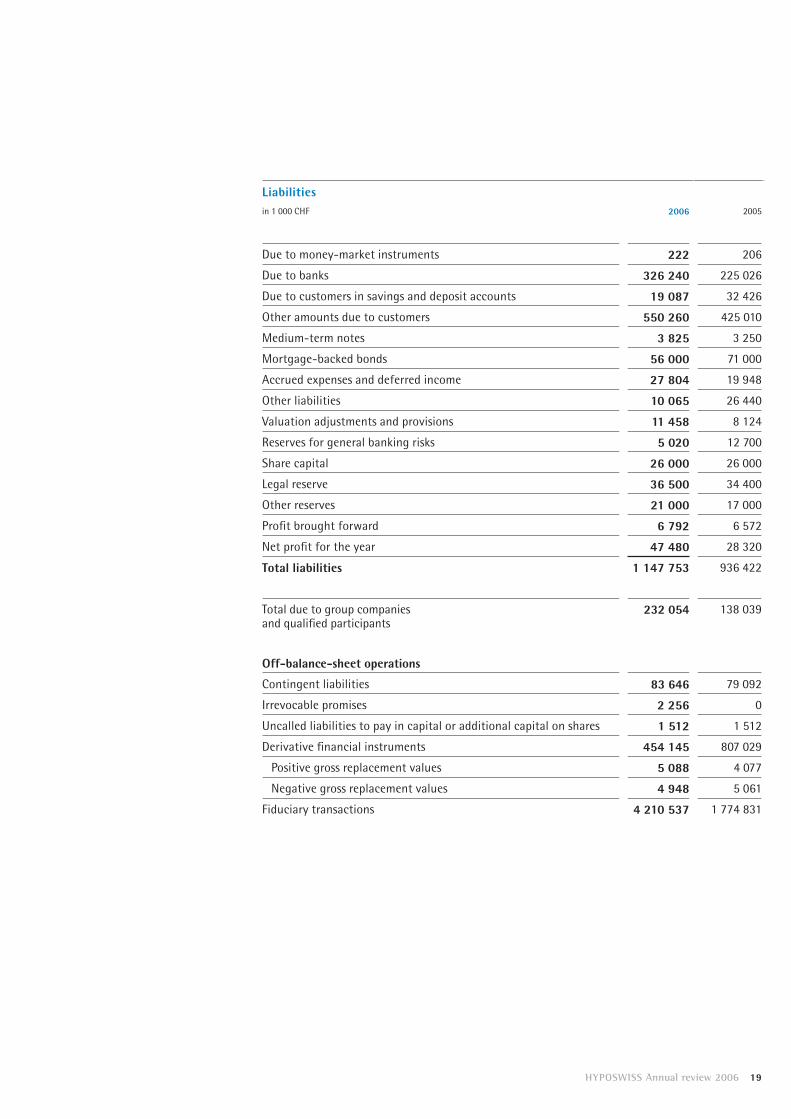

Liabilitiesin 1 000 CHF 2006 2005

Due to money-market instruments 222 206

Due to banks 326 240 225 026

Due to customers in savings and deposit accounts 19 087 32 426

Other amounts due to customers 550 260 425 010

Medium-term notes 3 825 3 250

Mortgage-backed bonds 56 000 71 000

Accrued expenses and deferred income 27 804 19 948

Other liabilities 10 065 26 440

Valuation adjustments and provisions 11 458 8 124

Reserves for general banking risks 5 020 12 700

Share capital 26 000 26 000

Legal reserve 36 500 34 400

Other reserves 21 000 17 000

Profi t brought forward 6 792 6 572

Net profi t for the year 47 480 28 320

Total liabilities 1 147 753 936 422

Total due to group companies and qualifi ed participants

232 054 138 039

Off-balance-sheet operations

Contingent liabilities 83 646 79 092

Irrevocable promises 2 256 0

Uncalled liabilities to pay in capital or additional capital on shares 1 512 1 512

Derivative fi nancial instruments 454 145 807 029

Positive gross replacement values 5 088 4 077

Negative gross replacement values 4 948 5 061

Fiduciary transactions 4 210 537 1 774 831

Jahresrechnung

Bilanz per 31. Dezember 2005 vor Gewinnverwendung

HYPOSWISS Annual review 2006 19

All things SwissLong-term deals thrive on solid foundations. Switzerland is

a byword for stable conditions.

Appropriation of disposable profi t in 1 000 CHF 2006 2005

Net profi t for the year 47 480 28 320

Balance brought forward from previous year 6 792 6 572

At the disposal of the General Meeting (profi t as shownin the balance sheet)

54 272 34 892

The Board of Directors proposes that this amount be distributed as follows:

a) Payment of a dividend 40 000 22 000

b) Allocation to legal reserve 4 000 2 100

c) Allocation to other reserves 6 000 4 000

d) Balance carried forward to new account 4 272 6 792

Total 54 272 34 892

Upon approval of this proposal, total shareholders’ equity will comprise

Share capital 26 000 26 000

Legal reserve 40 500 36 500

Other reserves 27 000 21 000

Reserves for general banking risks 5 020 12 700

Balance carried forward to new account 4 272 6 792

Total 102 792 102 992

Appropriation of disposable profi t

HYPOSWISS Annual review 2006 21

Cashfl ow account

in 1 000 CHF Year under review Previous year

Origin ofresources

Use ofresources

Balance Origin ofresources

Use ofresources

Balance

Profi t for the year 47 480 28 320

Depreciation/write-offs on fi xed assets 1 305 1 094

Valuation adjustments and provisions 3 334 3

Reserves for general banking risks 7 680 11 000

Active deferrals 4 216 977

Passive deferrals 7 856 3 384

Previous year’s dividend 22 000 22 000

Cashfl ow from operating result (internal fi nancing)

59 975 33 896 26 079 43 798 22 980 20 818

Participations 287 62

Fixed assets 2 854 1 350

Cashfl ow from operations in fi xed assets

287 2 916 -2 629 1 350 -1 350

Due to money-market instruments 16 4

Due to banks 101 214 208 080

Receivables from money-market instruments 9 971 9 971

Due from banks 46 140 89 598

Interbank transactions 111 201 46 140 65 061 208 080 99 573 108 507

Medium-term notes 575 1 720

Due to customers in savings and deposit accounts

13 339 7 916

Other amounts due to customers 125 250 61 950

Mortgage loans 9 863 3 305

Due from customers 181 174 217 163

Customer business 135 688 194 513 -58 825 63 670 228 384 -164 714

Financial investments 586 9 218

Mortgage-backed bonds 15 000 2 000

Capital-market business 586 15 000 -14 414 11 218 11 218

Other assets 1 181 15 385

Other liabilities 16 375 10 639

Other balance-sheet items 1 181 16 375 -15 194 26 024 26 024

Cashfl ow from banking business 248 656 272 028 -23 372 308 992 327 957 -18 965

Liquid assets 78 -78 503 -503

Sources of funds 308 918 352 790

Uses of funds 308 918 352 790

22 HYPOSWISS Annual review 2006

Auditors’ report

Report of the statutory auditors to the General Meeting of

HYPOSWISS Private Bank Ltd., Zurich.

As statutory auditors we have examined the bookkeeping and

annual accounts (income statement, balance sheet, cashfl ow

account and appendix) of HYPOSWISS Private Bank Ltd., Zurich,

for the fi nancial year ended 31 December 2006.

Responsibility for the annual accounts lies with the board;

our task consists in examining those accounts and passing judge-

ment thereon. We confi rm that we meet the statutory require-

ments with regard to competence and independence.

Our examination complied with the Swiss standards of auditing

whereby an audit is to be planned and executed in such a way

that major misstatements in the annual accounts are recog-

nised with reasonable certainty. We examined the items of and

information given in the annual accounts, using analyses and

investigations on a random-sample basis. We also assessed the

application of the standard principles of rendering of account,

key decisions regarding valuation, and the presentation of the

annual accounts as a whole. We take the view that our exami-

nation provided an adequate foundation on which to judge.

In our estimation, the bookkeeping and annual accounts,

together with the motion regarding use of the profi t shown in

the balance sheet, are in conformity with Swiss law and with

the articles of association.

We recommend that the present annual accounts be adopted.

Zurich, 8 February 2007

PricewaterhouseCoopers AG

Pascal Portmann Thomas Kleger

Chief auditor

HYPOSWISS Annual review 2006 23

The following auditors’ report refers to the annual report 2006, which can be ordered from HYPOSWISS Private Bank Ltd.

Impressum© 2007 HYPOSWISS Private Bank Ltd.PlanningThe Investor Relations Firm AG, ZurichDesign TGG Hafen Senn Stieger, St.GallenIllustrationsPortraits page 4 and 5, photos T+T Fotografi e, Toni Sutter, Zurichpage 8, photographer Lorenz Andreas Fischerpage 10, photographer WojtechRemaining pictures, Image Point