annual return - a presentation done to icsi hyderabad chapter by sas partners

TRANSCRIPT

Companies Act 2013

ANNUAL RETURN

Presented by

Soy Joseph, ACS, ACIS (UK), BL, Senior Partner

Key Areas

2

KE

Y A

RE

AS

Applicable Sections & Rules

Comparison between CA 1956 & 2013

Contents of Annual Return

Signing of Annual Return

Certification

Due date for filing with Roc

Non Compliance

Liability on Company Secretaries

MGT – 9 Extract to Board’s Report

Key Definitions

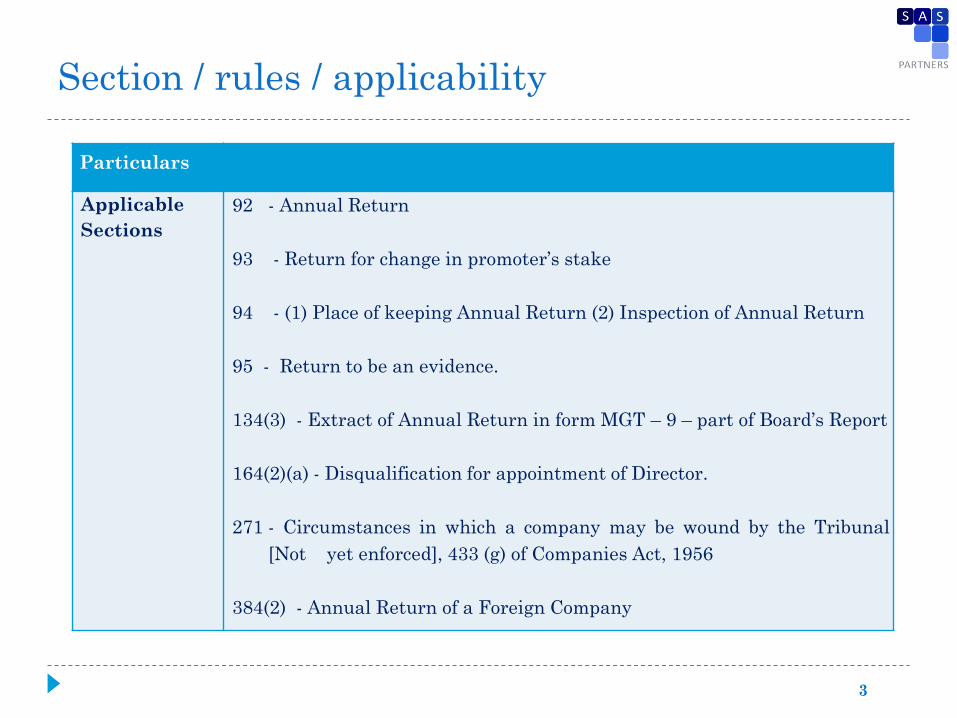

Section / rules / applicability

3

Particulars

Applicable

Sections

92 - Annual Return

93 - Return for change in promoter’s stake

94 - (1) Place of keeping Annual Return (2) Inspection of Annual Return

95 - Return to be an evidence.

134(3) - Extract of Annual Return in form MGT – 9 – part of Board’s Report

164(2)(a) - Disqualification for appointment of Director.

271 - Circumstances in which a company may be wound by the Tribunal

[Not yet enforced], 433 (g) of Companies Act, 1956

384(2) - Annual Return of a Foreign Company

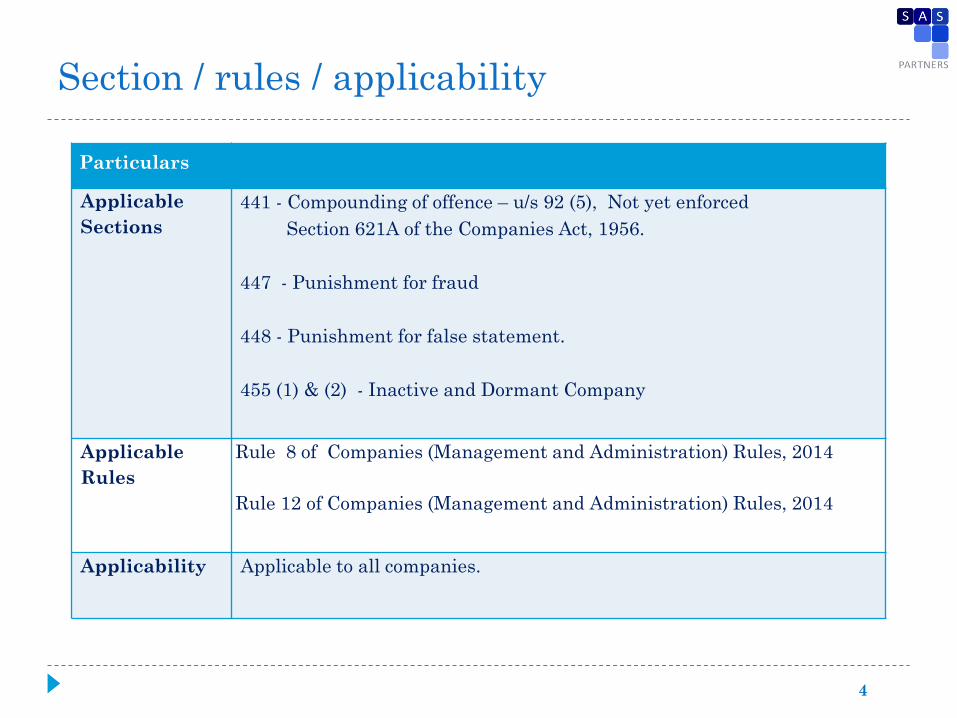

Section / rules / applicability

4

Particulars

Applicable

Sections

441 - Compounding of offence – u/s 92 (5), Not yet enforced

Section 621A of the Companies Act, 1956.

447 - Punishment for fraud

448 - Punishment for false statement.

455 (1) & (2) - Inactive and Dormant Company

Applicable

Rules

Rule 8 of Companies (Management and Administration) Rules, 2014

Rule 12 of Companies (Management and Administration) Rules, 2014

Applicability Applicable to all companies.

5

Companies Act, 1956 Companies Act, 2013

Section 159,160,161,162 & Schedule V deals

with the Annual Return & related provisions

under Companies Act,1956.

Whereas in Companies Act, 2013 all these

sections are combined together and are dealt

with in Section 92.

Annual Return is prepared as at the date of

Annual General Meeting

Annual Return is prepared as on the closing

date of the Financial Year.

Narrow Outlook. Provides information on

General information, shareholding pattern,

details of present and past directors, details

of transfer etc.

Broad and comprehensive document and

covers almost all important aspects such as

General information including nature of

activity, detailed shareholding pattern,

details of directors, indebtedness of the

Company, Details of forms filed,

Penalizations etc.

Annual Return – CA 1956 Vs CA 2013

6

Annual Return – CA 1956 Vs CA 2013

Companies Act, 1956 Companies Act, 2013

Lesser Penalty Penalty has been substantially increased

20B verification by CS/CA/ICWA.

Certification by PCS required only for Listed

Companies

Verification only by CS and Certification by

PCS for Listed Companies, Companies

having Share capital of Rs.10 Crores or

more, or turnover of Rs.50 Crores or more.

Certification by two directors Certification by One Director and a Company

Secretary. In absence of Company Secretary,

PCS shall certify the same.

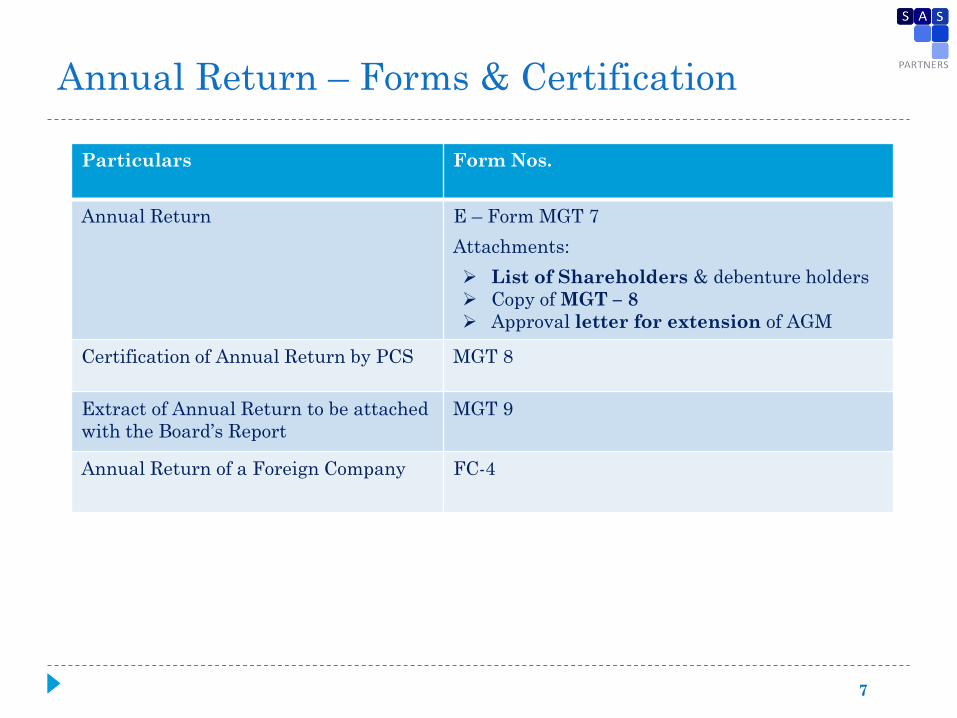

Particulars

Form Nos.

Annual Return E – Form MGT 7

Attachments:

List of Shareholders & debenture holders

Copy of MGT – 8

Approval letter for extension of AGM

Certification of Annual Return by PCS MGT 8

Extract of Annual Return to be attached

with the Board’s Report

MGT 9

Annual Return of a Foreign Company FC-4

Annual Return – Forms & Certification

7

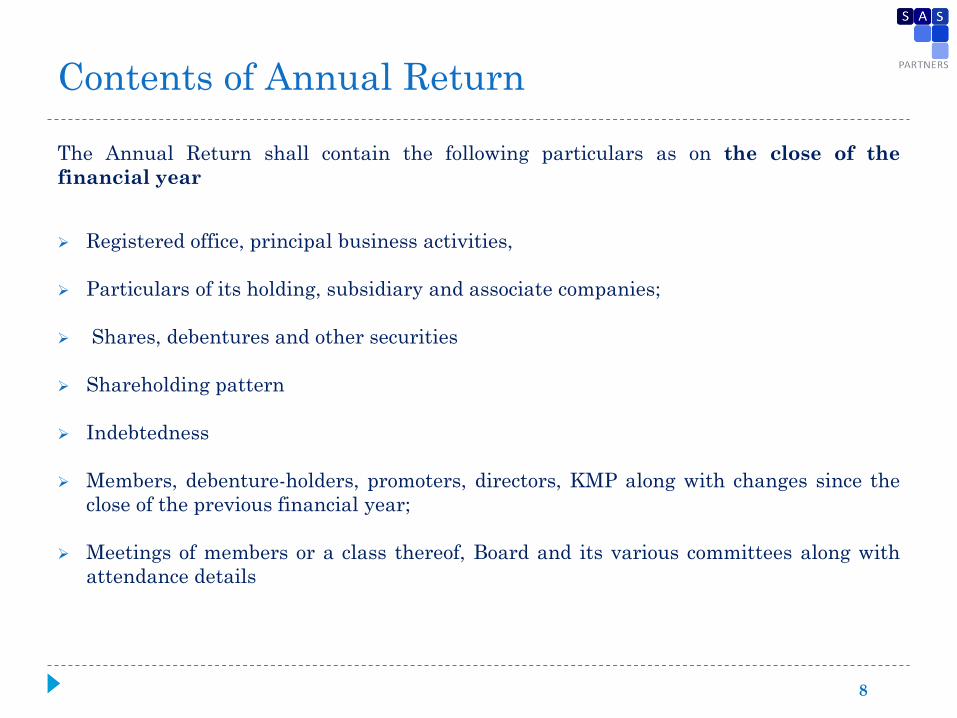

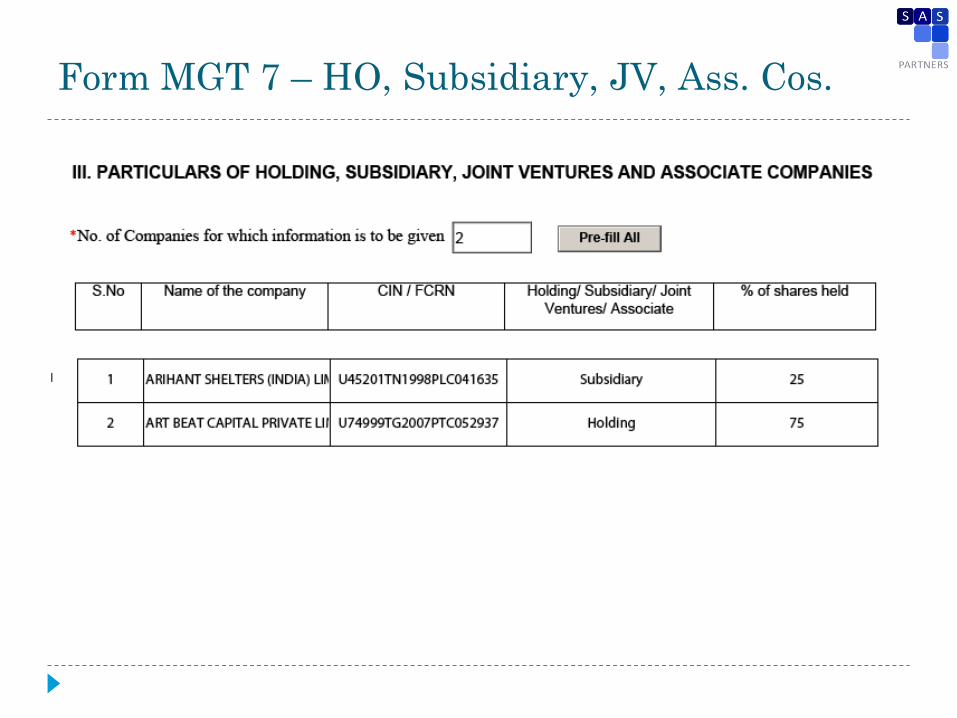

The Annual Return shall contain the following particulars as on the close of the

financial year

Registered office, principal business activities,

Particulars of its holding, subsidiary and associate companies;

Shares, debentures and other securities

Shareholding pattern

Indebtedness

Members, debenture-holders, promoters, directors, KMP along with changes since the

close of the previous financial year;

Meetings of members or a class thereof, Board and its various committees along with

attendance details

Contents of Annual Return

8

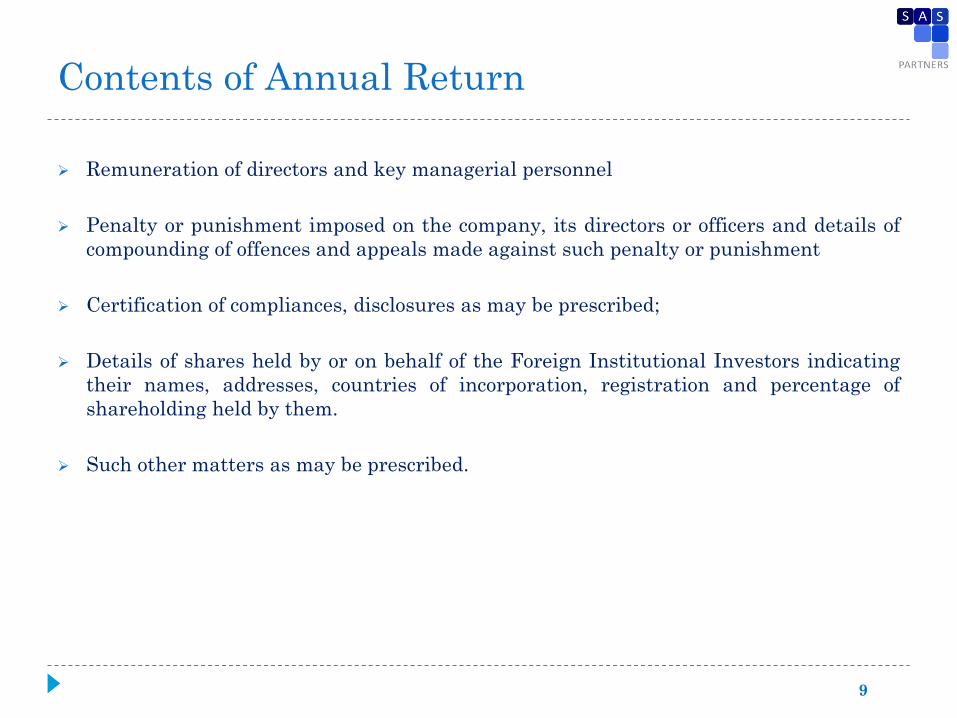

Remuneration of directors and key managerial personnel

Penalty or punishment imposed on the company, its directors or officers and details of

compounding of offences and appeals made against such penalty or punishment

Certification of compliances, disclosures as may be prescribed;

Details of shares held by or on behalf of the Foreign Institutional Investors indicating

their names, addresses, countries of incorporation, registration and percentage of

shareholding held by them.

Such other matters as may be prescribed.

Contents of Annual Return

9

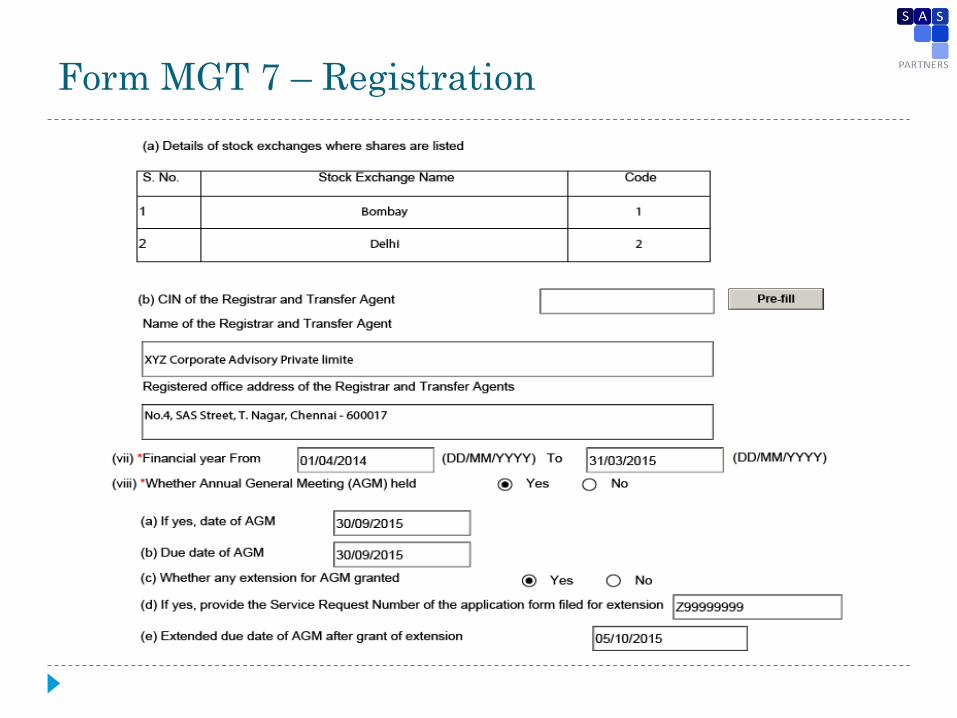

Form MGT 7 – Registration

Form MGT 7 – Registration

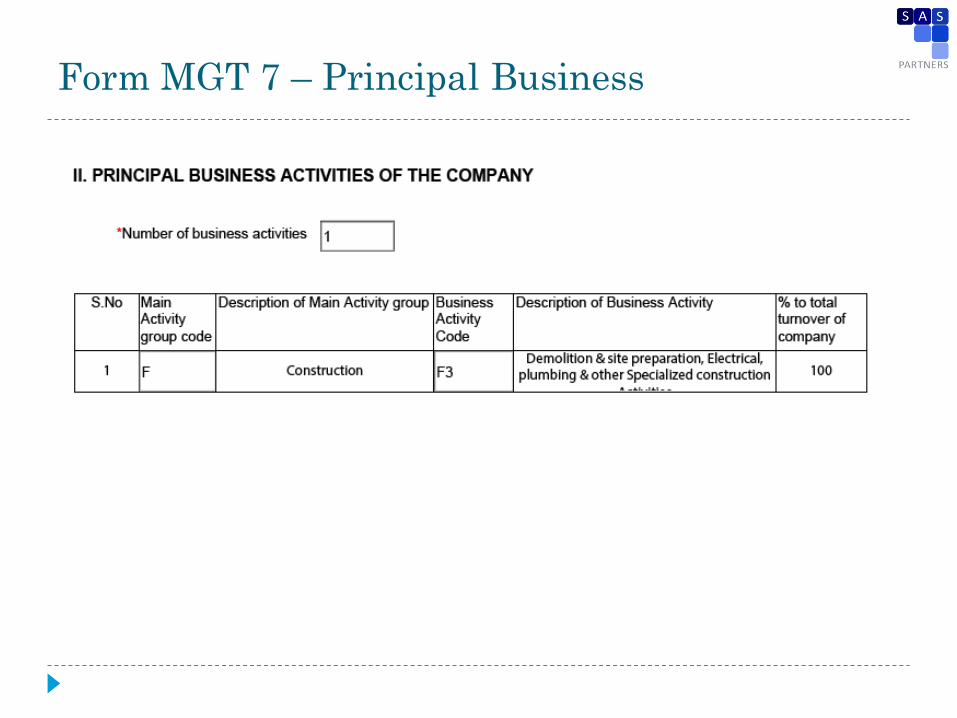

Form MGT 7 – Principal Business

Form MGT 7 – Principal Business TERM DEFINITION

Principal

Business

Activity

As mentioned in MOA of the Company. No activity outside

MOA.

All business contributing 10% or more of the total

turnover of the Company.(as required under MGT- 9)

Reference under

the Act Section 92 : Annual return

Section 185 : Loan to directors

Section 186 : Loan and investments by company

Term ―Ordinary course of Business‖ – though not defined

referred at many places under the Act.

principal business

– RBI

when a company’s financial assets constitute more than 50 per

cent of the total assets and income from financial assets

constitute more than 50 per cent of the gross income. A

company which fulfils both these criteria will be registered as

NBFC by RBI.

- popularly known as 50-50 test

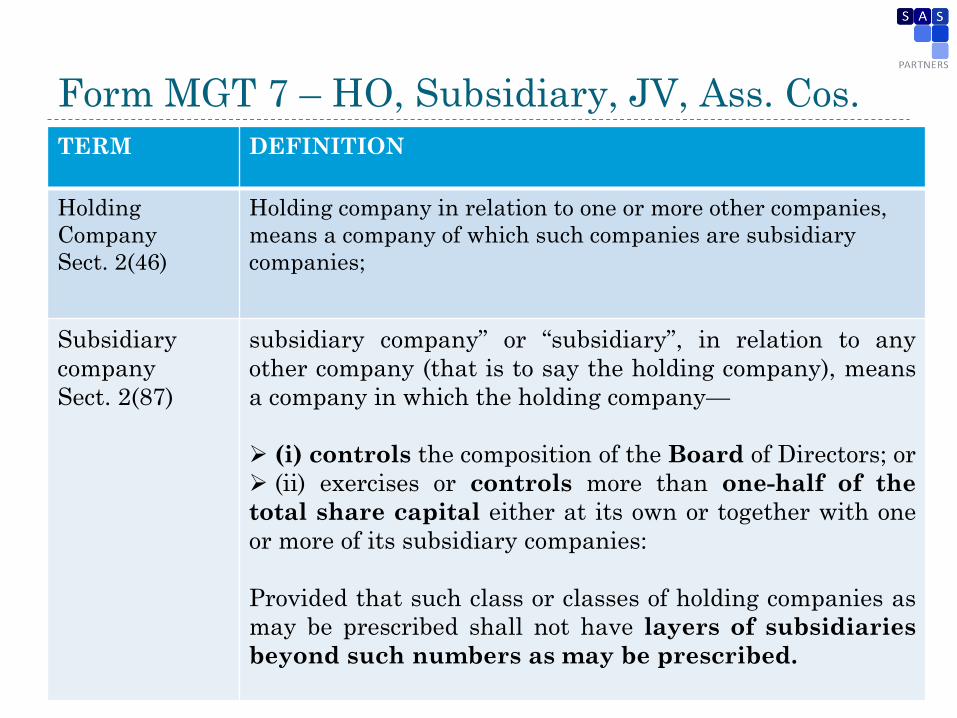

Form MGT 7 – HO, Subsidiary, JV, Ass. Cos.

Form MGT 7 – HO, Subsidiary, JV, Ass. Cos.

TERM DEFINITION

Holding

Company

Sect. 2(46)

Holding company in relation to one or more other companies,

means a company of which such companies are subsidiary

companies;

Subsidiary

company

Sect. 2(87)

subsidiary company‖ or ―subsidiary‖, in relation to any

other company (that is to say the holding company), means

a company in which the holding company—

(i) controls the composition of the Board of Directors; or

(ii) exercises or controls more than one-half of the

total share capital either at its own or together with one

or more of its subsidiary companies:

Provided that such class or classes of holding companies as

may be prescribed shall not have layers of subsidiaries

beyond such numbers as may be prescribed.

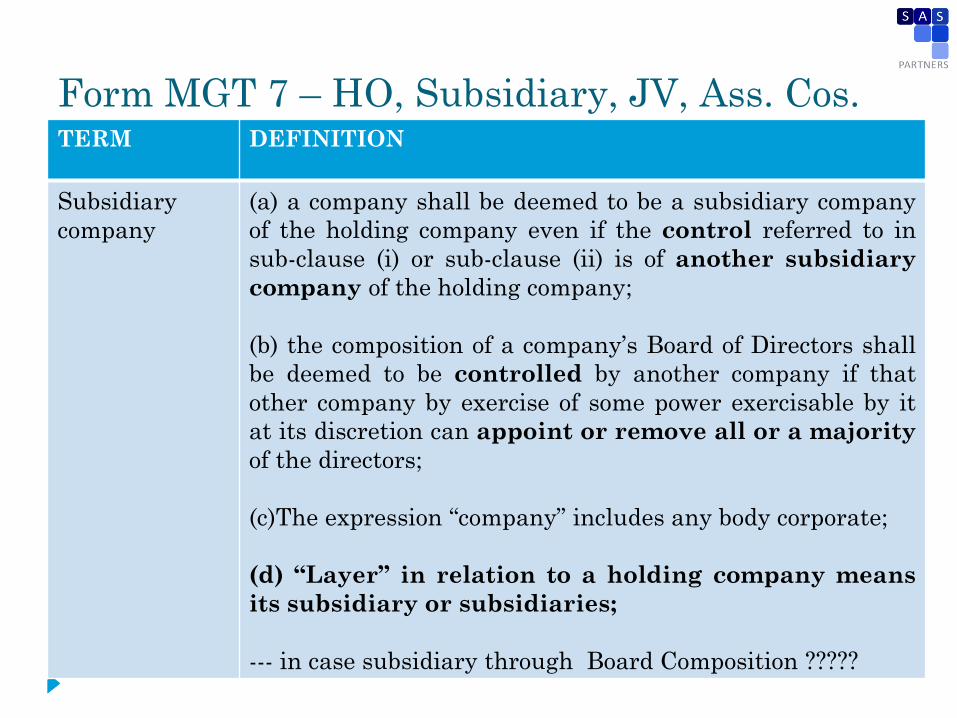

Form MGT 7 – HO, Subsidiary, JV, Ass. Cos. TERM DEFINITION

Subsidiary

company

(a) a company shall be deemed to be a subsidiary company

of the holding company even if the control referred to in

sub-clause (i) or sub-clause (ii) is of another subsidiary

company of the holding company;

(b) the composition of a company’s Board of Directors shall

be deemed to be controlled by another company if that

other company by exercise of some power exercisable by it

at its discretion can appoint or remove all or a majority

of the directors;

(c)The expression ―company‖ includes any body corporate;

(d) “Layer” in relation to a holding company means

its subsidiary or subsidiaries;

--- in case subsidiary through Board Composition ?????

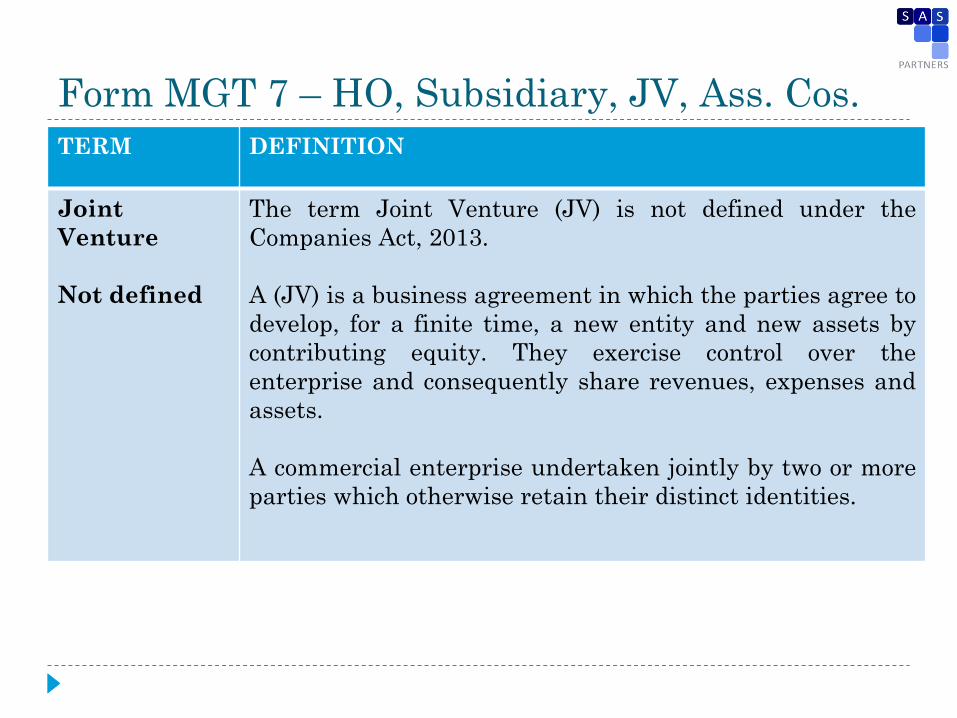

Form MGT 7 – HO, Subsidiary, JV, Ass. Cos.

TERM DEFINITION

Joint

Venture

Not defined

The term Joint Venture (JV) is not defined under the

Companies Act, 2013.

A (JV) is a business agreement in which the parties agree to

develop, for a finite time, a new entity and new assets by

contributing equity. They exercise control over the

enterprise and consequently share revenues, expenses and

assets.

A commercial enterprise undertaken jointly by two or more

parties which otherwise retain their distinct identities.

Form MGT 7 – HO, Subsidiary, JV, Ass. Cos.

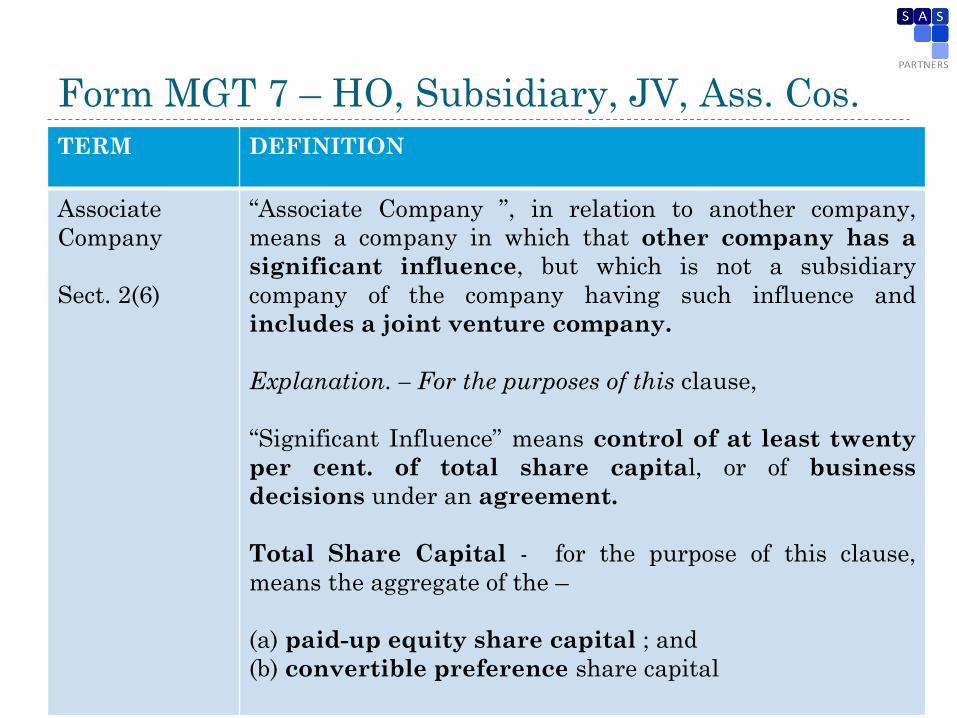

TERM DEFINITION

Associate

Company

Sect. 2(6)

―Associate Company ‖, in relation to another company,

means a company in which that other company has a

significant influence, but which is not a subsidiary

company of the company having such influence and

includes a joint venture company.

Explanation. – For the purposes of this clause,

―Significant Influence‖ means control of at least twenty

per cent. of total share capital, or of business

decisions under an agreement.

Total Share Capital - for the purpose of this clause,

means the aggregate of the –

(a) paid-up equity share capital ; and

(b) convertible preference share capital

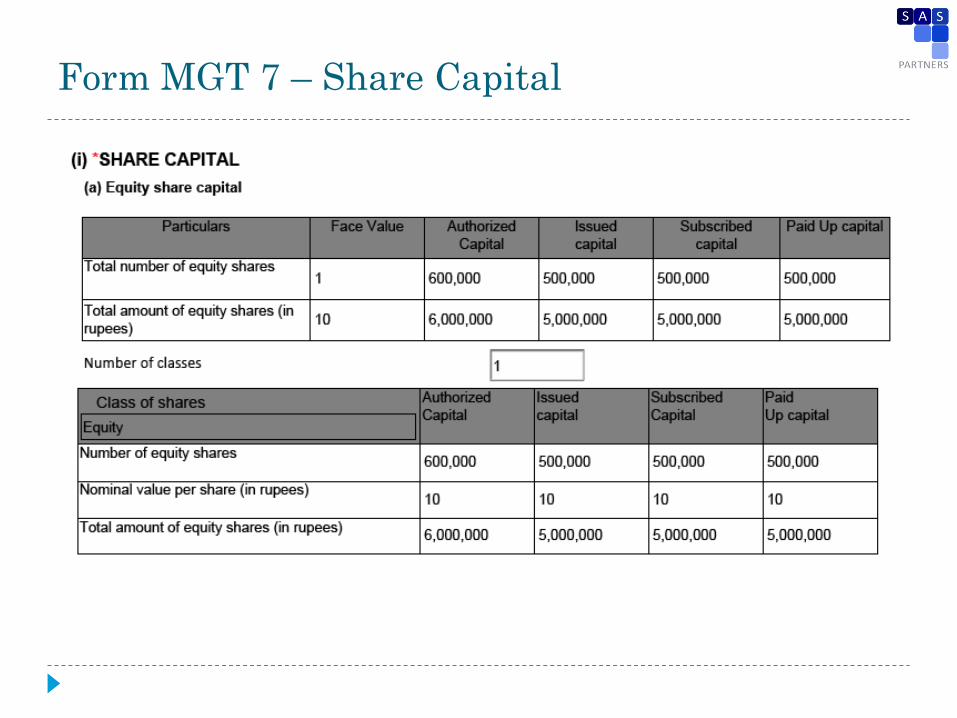

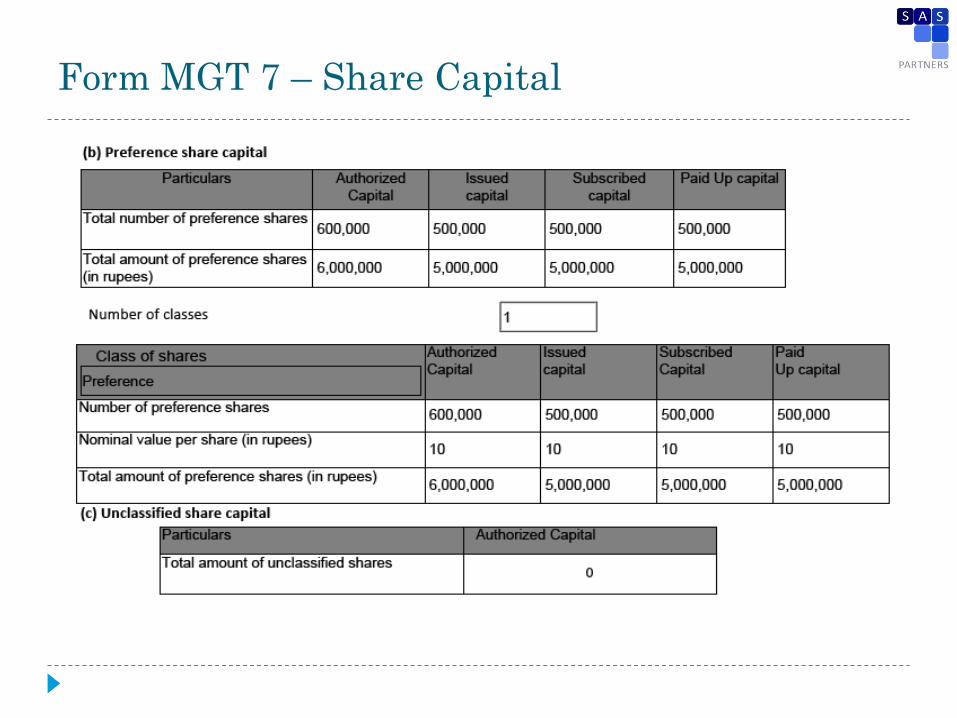

Form MGT 7 – Share Capital

Form MGT 7 – Share Capital

Form MGT 7 – Paid Up Capital

Form MGT 7 – Paid Up Capital

Form MGT 7 – Break up of paid up capital

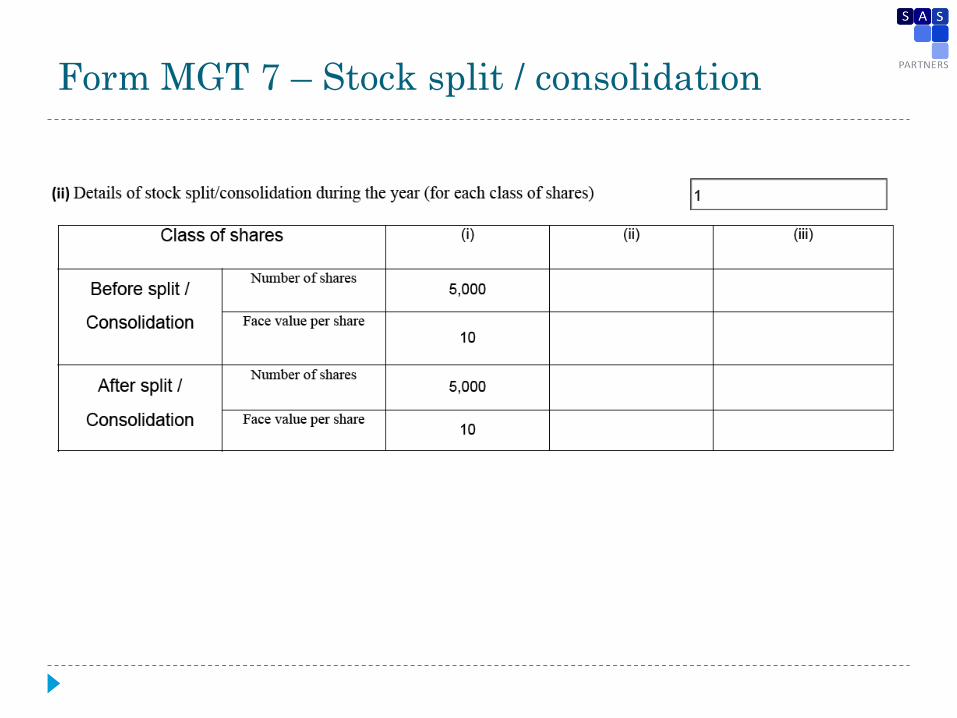

Form MGT 7 – Stock split / consolidation

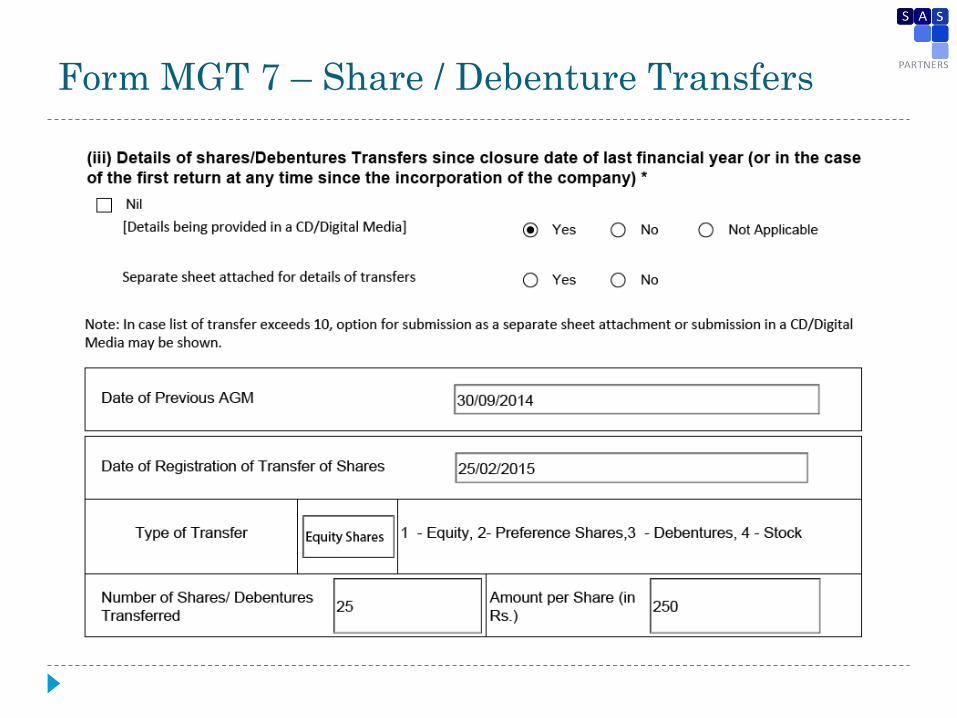

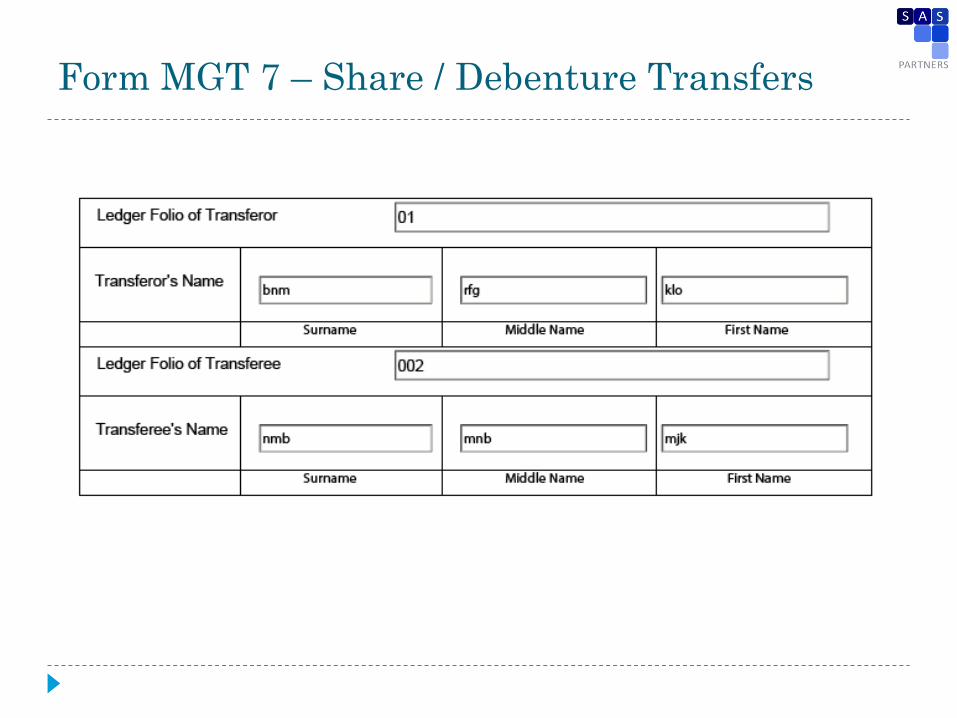

Form MGT 7 – Share / Debenture Transfers

Form MGT 7 – Share / Debenture Transfers

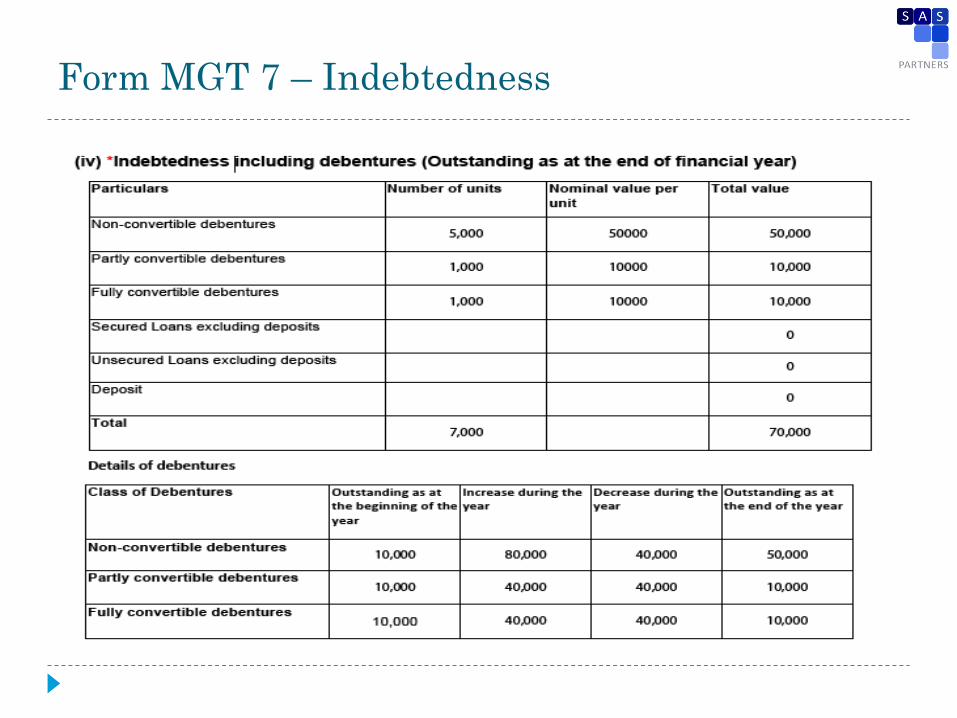

Form MGT 7 – Indebtedness

Form MGT 7 – Indebtedness

Form MGT 7 – Indebtedness TERM DEFINITION

Indebtedness

- Whether indebtedness includes interest ??

- Information on optionally convertible debentures??

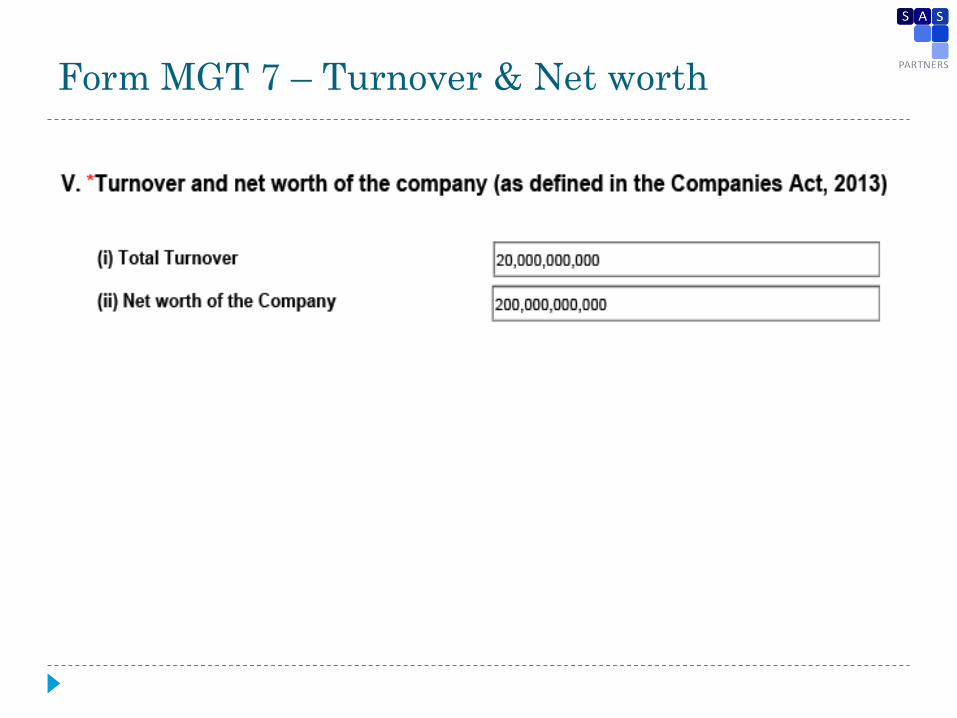

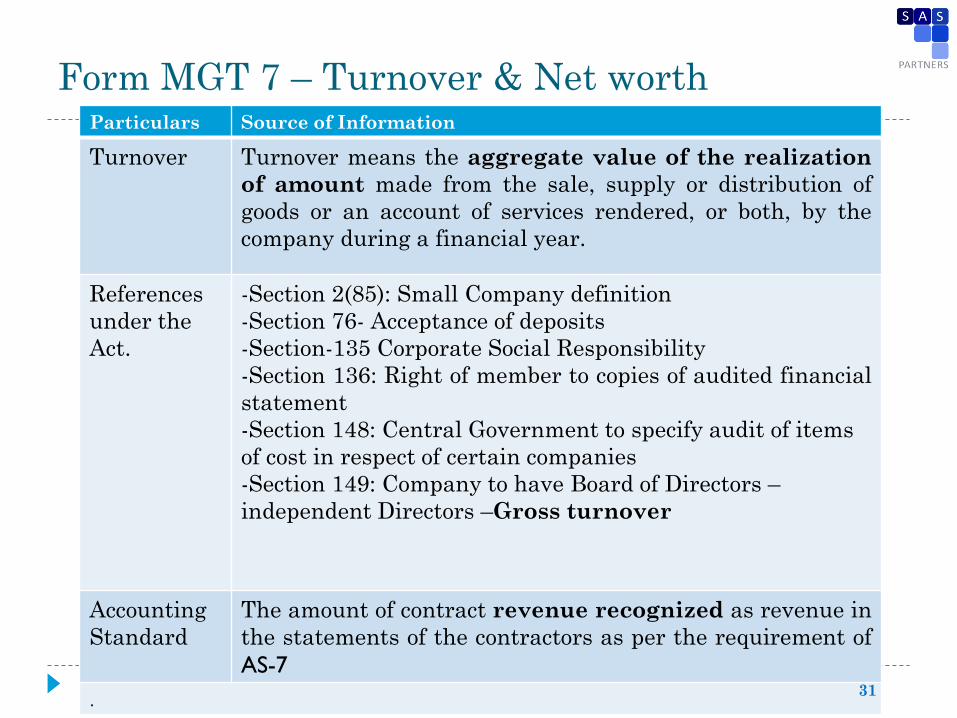

Form MGT 7 – Turnover & Net worth

Form MGT 7 – Turnover & Net worth Particulars Source of Information

Turnover Turnover means the aggregate value of the realization

of amount made from the sale, supply or distribution of

goods or an account of services rendered, or both, by the

company during a financial year.

References

under the

Act.

-Section 2(85): Small Company definition

-Section 76- Acceptance of deposits

-Section-135 Corporate Social Responsibility

-Section 136: Right of member to copies of audited financial

statement

-Section 148: Central Government to specify audit of items

of cost in respect of certain companies

-Section 149: Company to have Board of Directors –

independent Directors –Gross turnover

Accounting

Standard

The amount of contract revenue recognized as revenue in

the statements of the contractors as per the requirement of

AS-7

. 31

Key Definitions – MGT - 7

Term Definition

Net Worth

―Net worth‖ means the aggregate value of paid- share

capital and all reserves created out of the profits and

securities premium account, after deducting the

aggregate value of the accumulated losses, deferred

expenditure and miscellaneous expenditure not

written off, as per the audited balance sheet, but does not

include reserves created out of revaluation of assets, write-

back of depreciation and amalgamation.

32

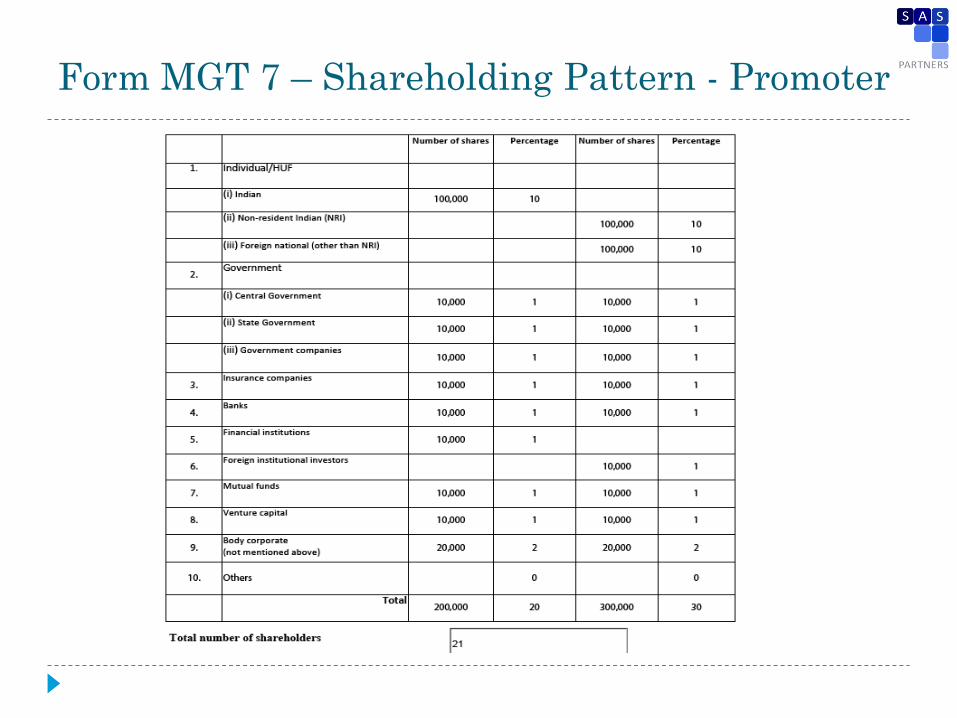

Form MGT 7 – Shareholding Pattern - Promoter

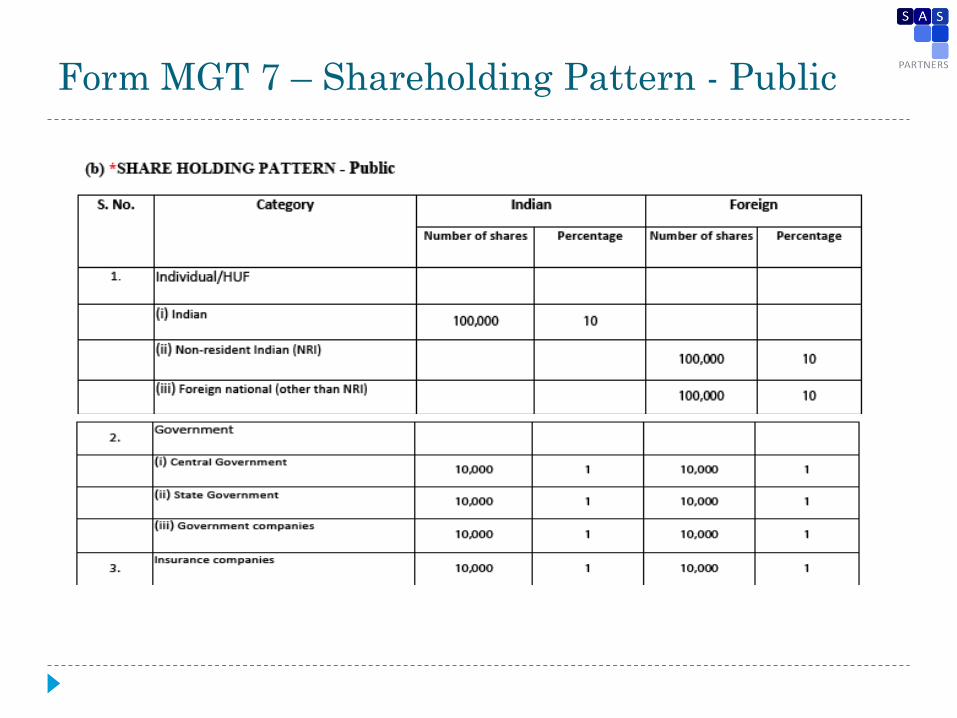

Form MGT 7 – Shareholding Pattern - Public

Form MGT 7 – Shareholding Pattern - Public

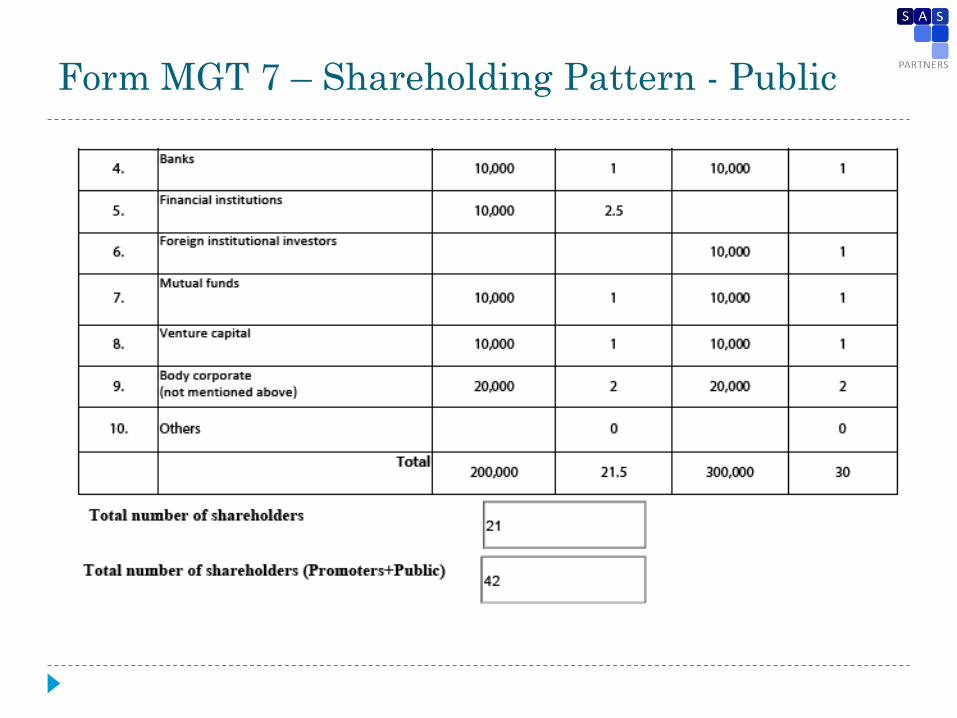

Form MGT 7 – Shareholding Pattern - Public

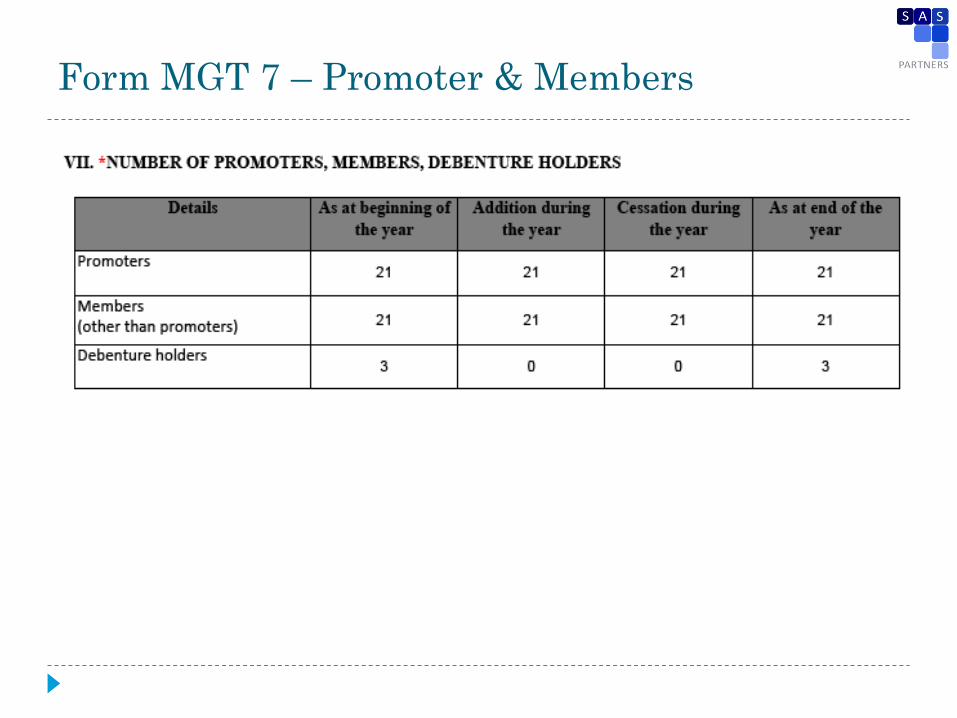

Form MGT 7 – Promoter & Members

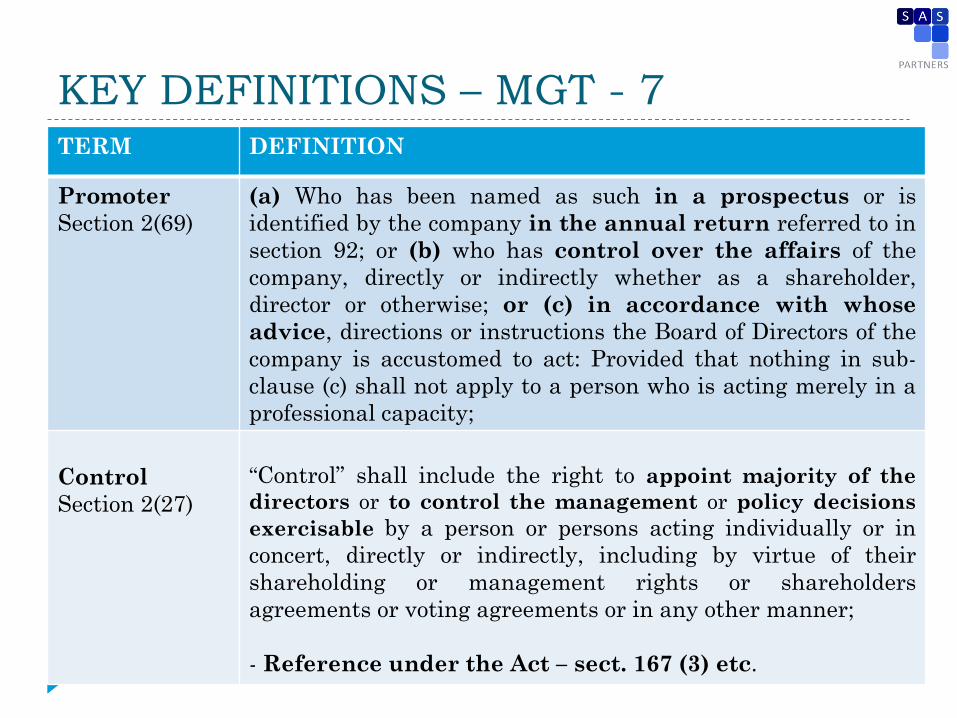

KEY DEFINITIONS – MGT - 7 TERM DEFINITION

Promoter

Section 2(69)

(a) Who has been named as such in a prospectus or is

identified by the company in the annual return referred to in

section 92; or (b) who has control over the affairs of the

company, directly or indirectly whether as a shareholder,

director or otherwise; or (c) in accordance with whose

advice, directions or instructions the Board of Directors of the

company is accustomed to act: Provided that nothing in sub-

clause (c) shall not apply to a person who is acting merely in a

professional capacity;

Control

Section 2(27)

―Control‖ shall include the right to appoint majority of the

directors or to control the management or policy decisions

exercisable by a person or persons acting individually or in

concert, directly or indirectly, including by virtue of their

shareholding or management rights or shareholders

agreements or voting agreements or in any other manner;

- Reference under the Act – sect. 167 (3) etc.

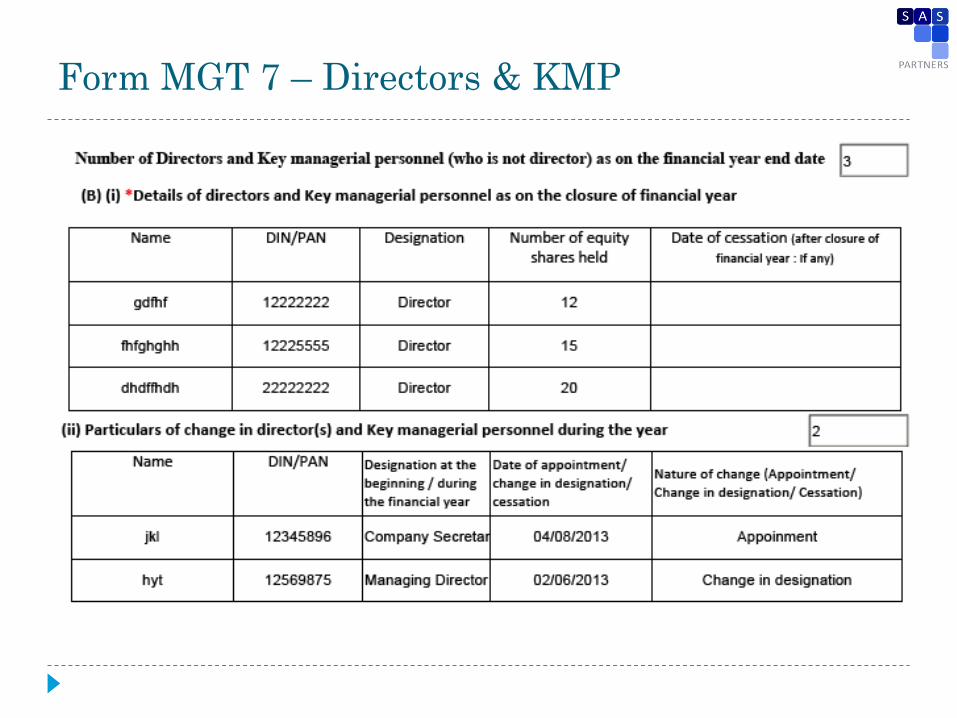

Form MGT 7 – Directors & KMP

Form MGT 7 – Directors & KMP

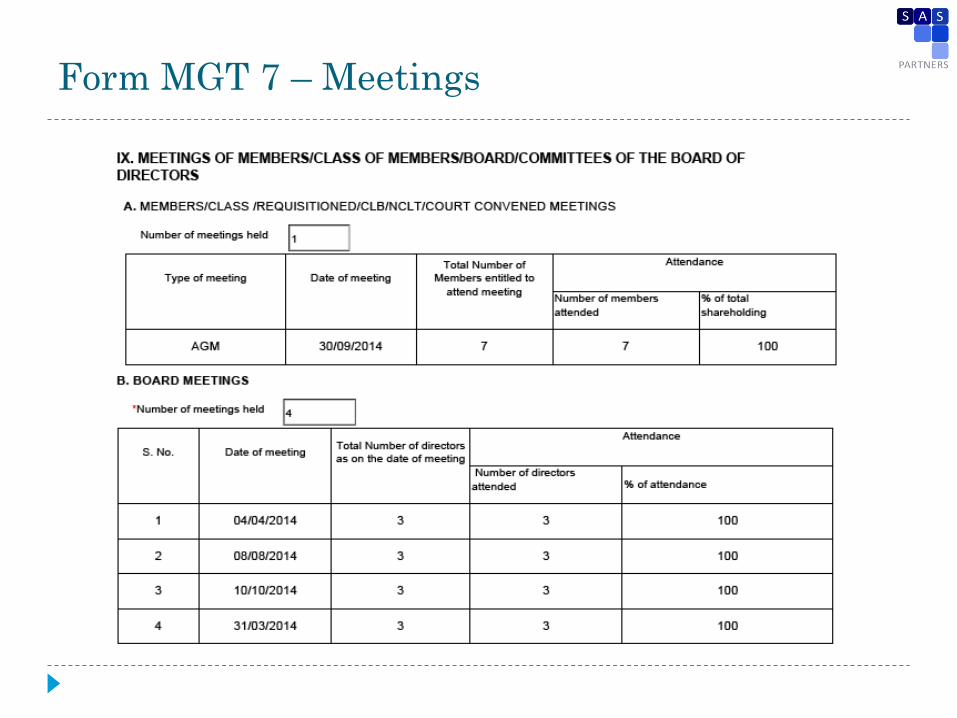

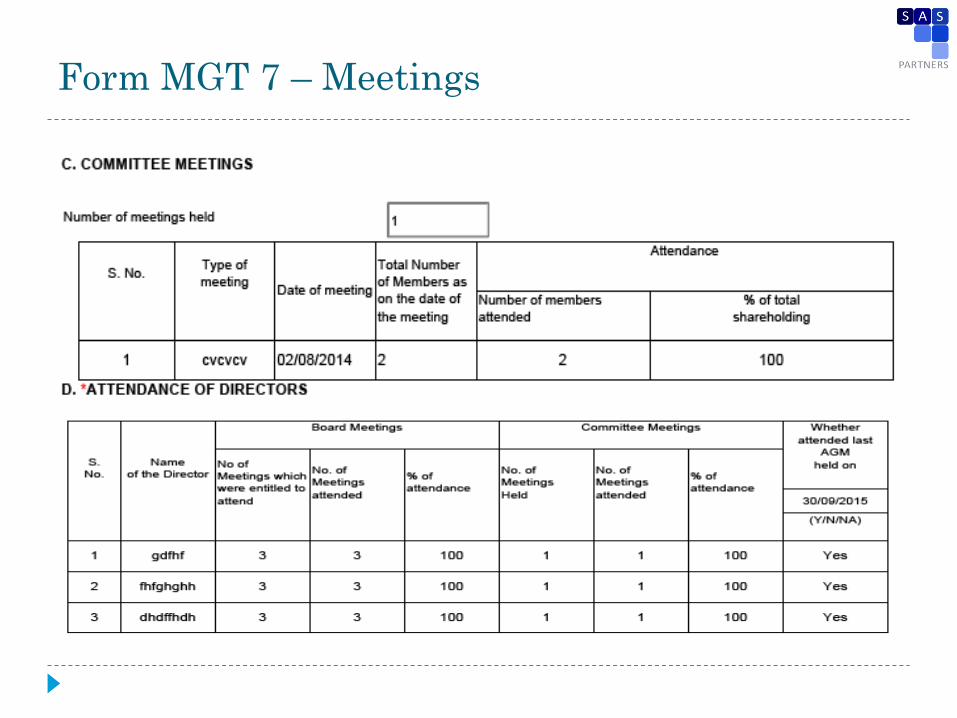

Form MGT 7 – Meetings

Form MGT 7 – Meetings

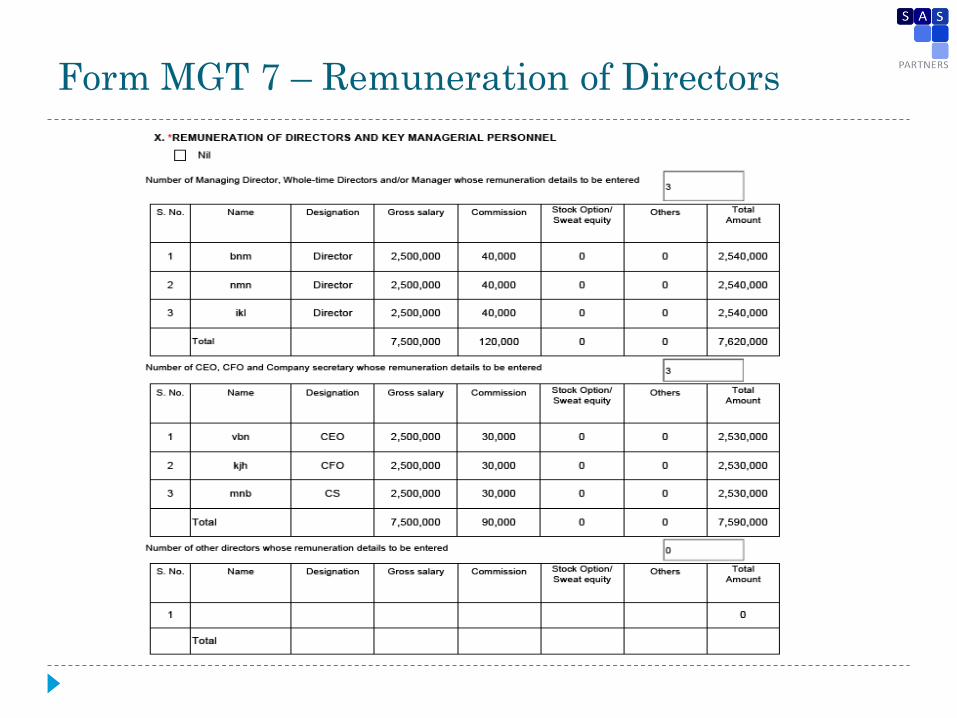

Form MGT 7 – Remuneration of Directors

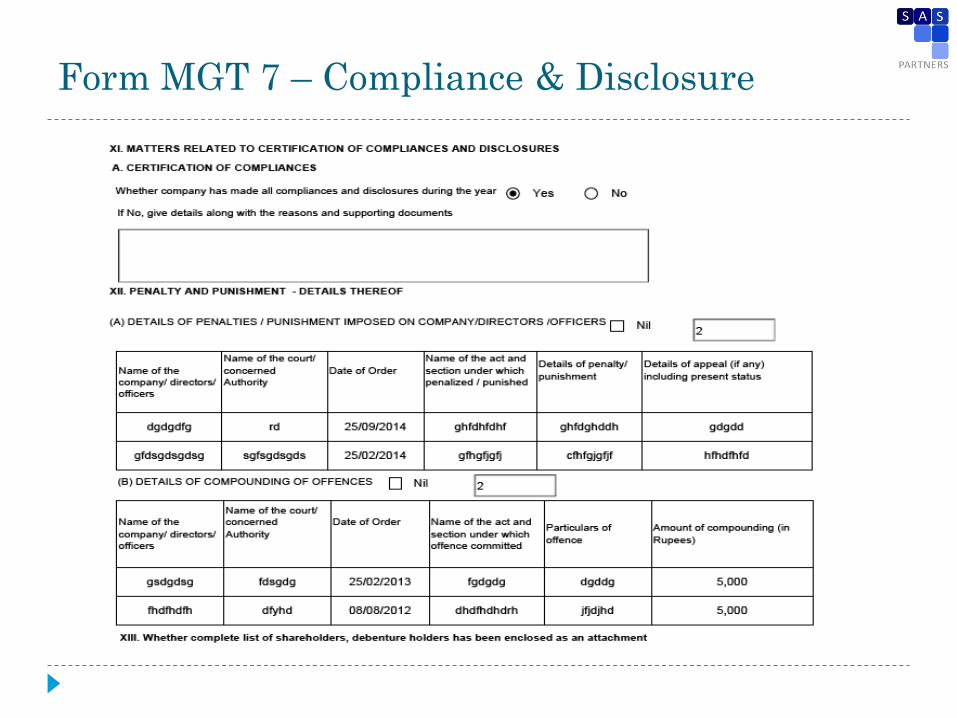

Form MGT 7 – Compliance & Disclosure

Form MGT 7 – Signing

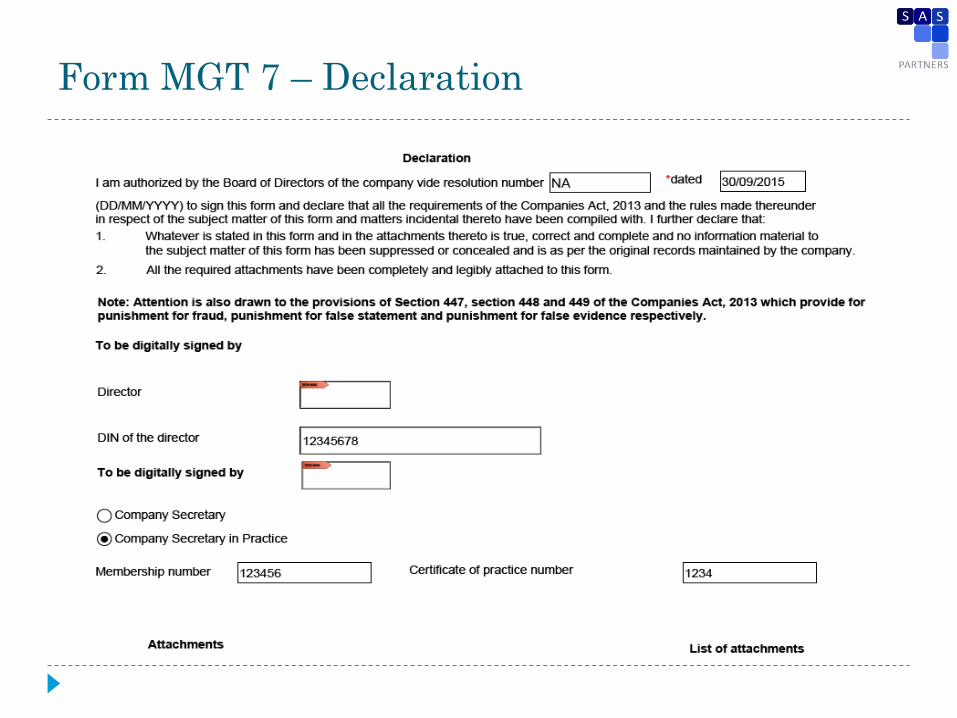

Form MGT 7 – Declaration

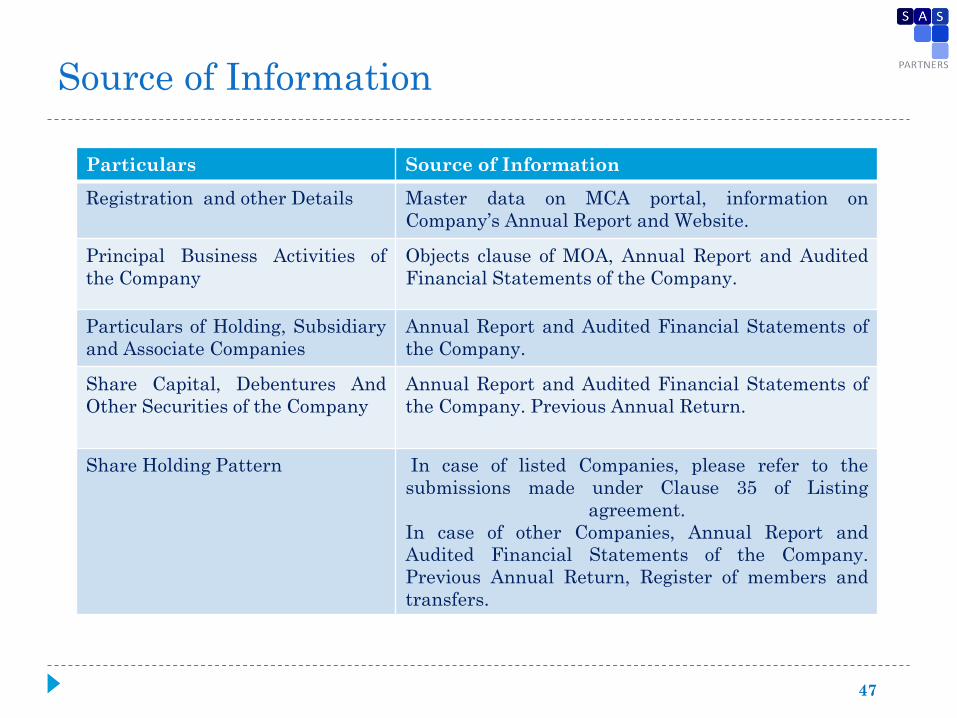

Source of Information

Particulars Source of Information

Registration and other Details Master data on MCA portal, information on

Company’s Annual Report and Website.

Principal Business Activities of

the Company

Objects clause of MOA, Annual Report and Audited

Financial Statements of the Company.

Particulars of Holding, Subsidiary

and Associate Companies

Annual Report and Audited Financial Statements of

the Company.

Share Capital, Debentures And

Other Securities of the Company

Annual Report and Audited Financial Statements of

the Company. Previous Annual Return.

Share Holding Pattern In case of listed Companies, please refer to the

submissions made under Clause 35 of Listing

agreement.

In case of other Companies, Annual Report and

Audited Financial Statements of the Company.

Previous Annual Return, Register of members and

transfers.

47

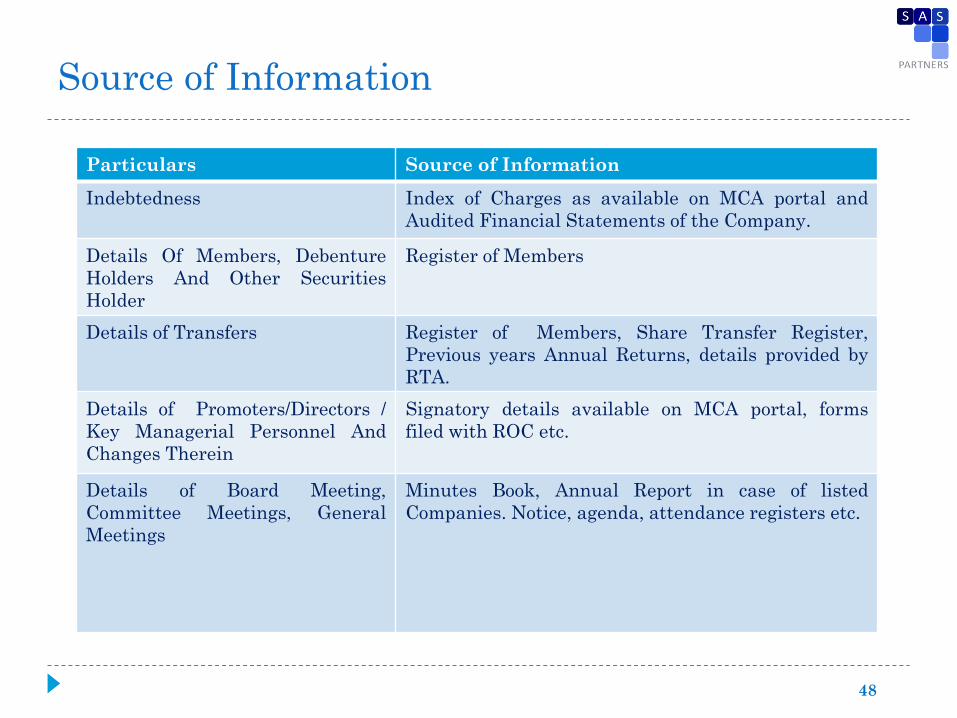

Source of Information

Particulars Source of Information

Indebtedness Index of Charges as available on MCA portal and

Audited Financial Statements of the Company.

Details Of Members, Debenture

Holders And Other Securities

Holder

Register of Members

Details of Transfers Register of Members, Share Transfer Register,

Previous years Annual Returns, details provided by

RTA.

Details of Promoters/Directors /

Key Managerial Personnel And

Changes Therein

Signatory details available on MCA portal, forms

filed with ROC etc.

Details of Board Meeting,

Committee Meetings, General

Meetings

Minutes Book, Annual Report in case of listed

Companies. Notice, agenda, attendance registers etc.

48

Source of Information

Particulars Source of Information

Remuneration of Directors and

KMP

Forms filed with respect to appointment of Directors

and KMP, Audited Financial Statements of the

Company.

Penalties, Punishments,

Compounding of offences

Defaults made by the Company, Verification of Show

cause notices received during the year, Information

available under companies against which prosecution

is initiated on MCA portal, defaulters list provided by

RBI and FIPB, Compounding applications filed by

the Company

Matters related to certification of

compliances and disclosures

ROC file, Document available under Check filing

status/ Public documents on MCA portal, Annual

Report etc, filings with other regulatory authorities

such as RBI and SEBI, Statutory registers,

Disclosures, consents and declarations.

49

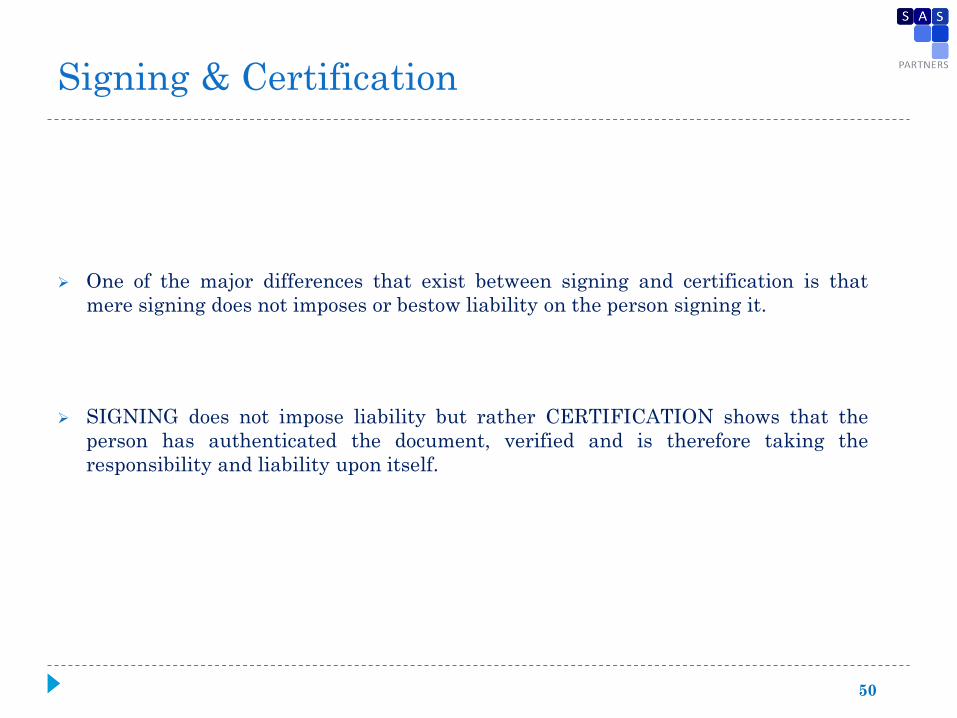

Signing & Certification

One of the major differences that exist between signing and certification is that

mere signing does not imposes or bestow liability on the person signing it.

SIGNING does not impose liability but rather CERTIFICATION shows that the

person has authenticated the document, verified and is therefore taking the

responsibility and liability upon itself.

50

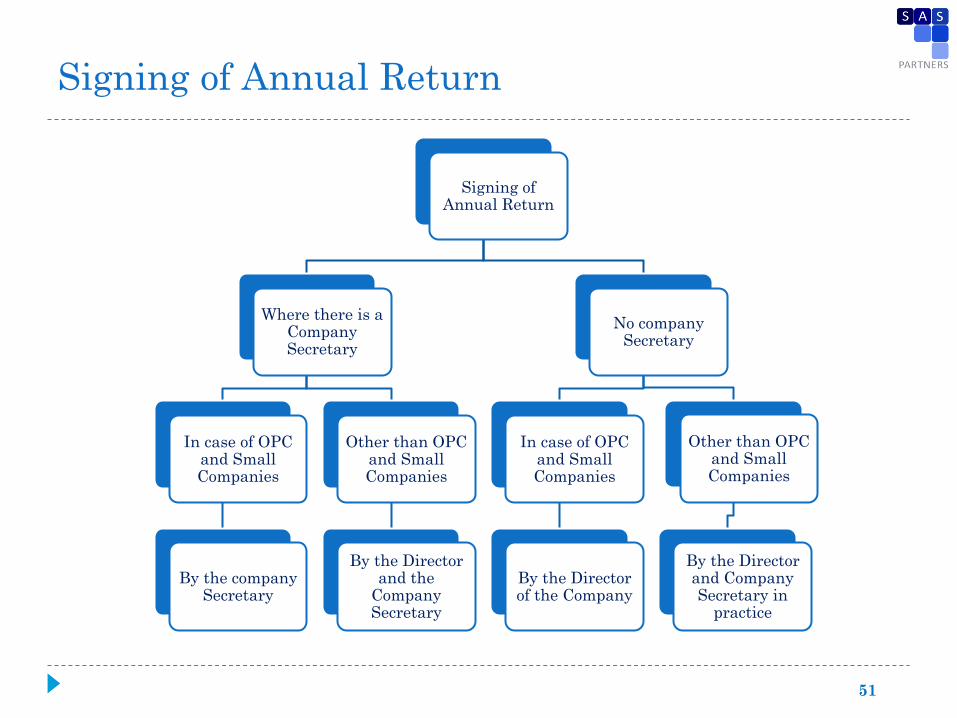

Signing of Annual Return

51

Signing of Annual Return

Where there is a Company Secretary

In case of OPC and Small Companies

By the company Secretary

Other than OPC and Small Companies

By the Director and the

Company Secretary

No company Secretary

In case of OPC and Small Companies

By the Director of the Company

Other than OPC and Small Companies

By the Director and Company Secretary in

practice

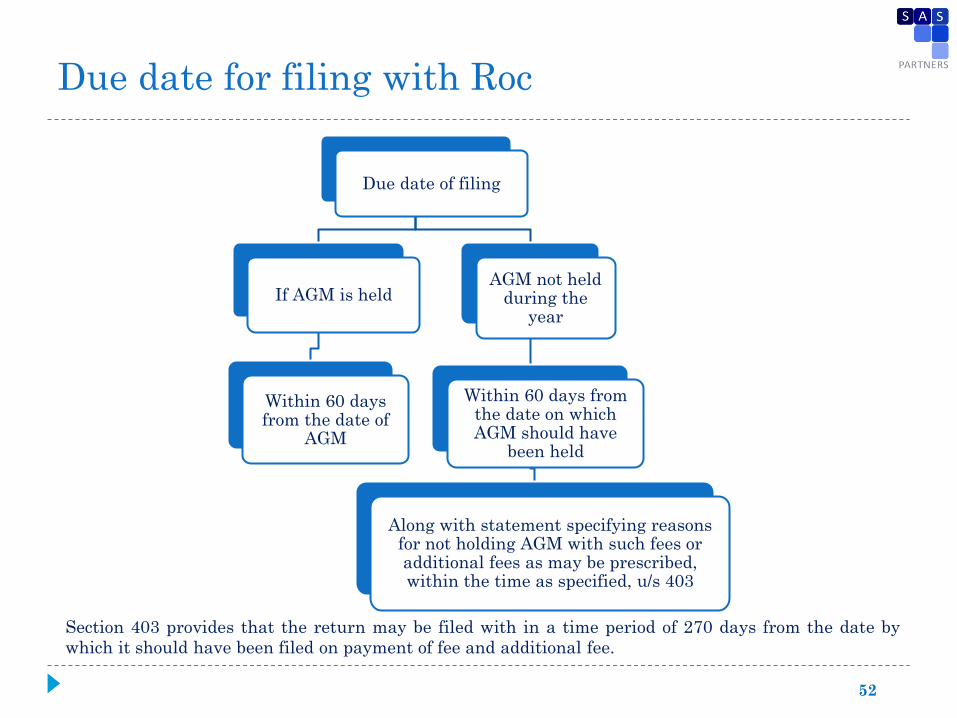

Due date for filing with Roc

52

Due date of filing

If AGM is held

Within 60 days from the date of

AGM

AGM not held during the

year

Within 60 days from the date on which AGM should have

been held

Along with statement specifying reasons for not holding AGM with such fees or additional fees as may be prescribed, within the time as specified, u/s 403

Section 403 provides that the return may be filed with in a time period of 270 days from the date by

which it should have been filed on payment of fee and additional fee.

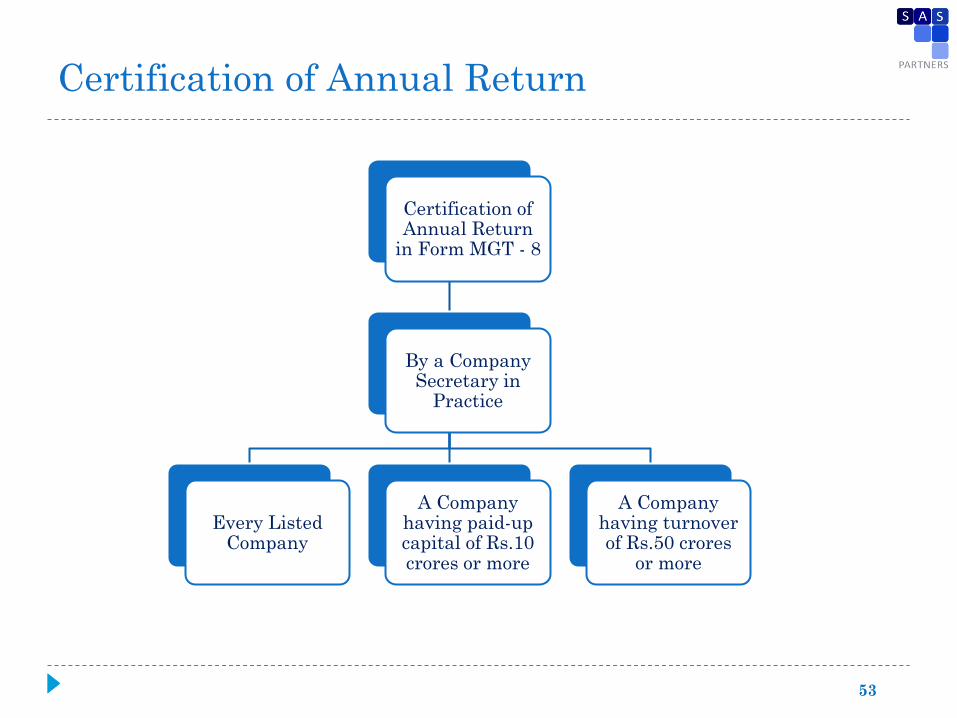

Certification of Annual Return

Certification of Annual Return

in Form MGT - 8

By a Company Secretary in

Practice

Every Listed Company

A Company having paid-up capital of Rs.10 crores or more

A Company having turnover of Rs.50 crores

or more

53

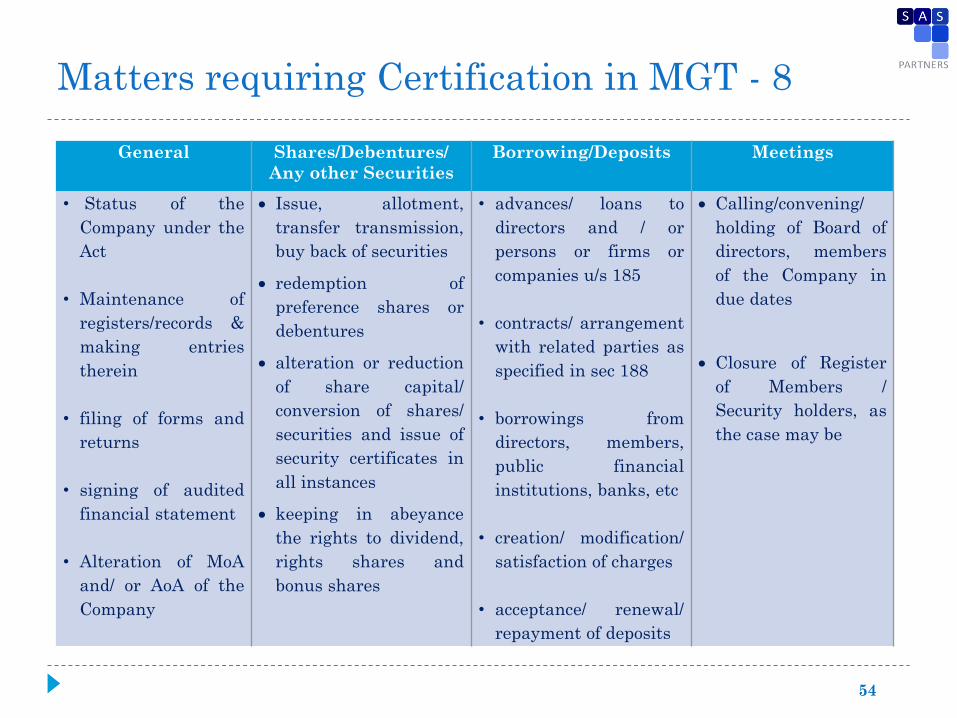

Matters requiring Certification in MGT - 8

54

General Shares/Debentures/

Any other Securities

Borrowing/Deposits Meetings

• Status of the

Company under the

Act

• Maintenance of

registers/records &

making entries

therein

• filing of forms and

returns

• signing of audited

financial statement

• Alteration of MoA

and/ or AoA of the

Company

Issue, allotment,

transfer transmission,

buy back of securities

redemption of

preference shares or

debentures

alteration or reduction

of share capital/

conversion of shares/

securities and issue of

security certificates in

all instances

keeping in abeyance

the rights to dividend,

rights shares and

bonus shares

• advances/ loans to

directors and / or

persons or firms or

companies u/s 185

• contracts/ arrangement

with related parties as

specified in sec 188

• borrowings from

directors, members,

public financial

institutions, banks, etc

• creation/ modification/

satisfaction of charges

• acceptance/ renewal/

repayment of deposits

Calling/convening/

holding of Board of

directors, members

of the Company in

due dates

Closure of Register

of Members /

Security holders, as

the case may be

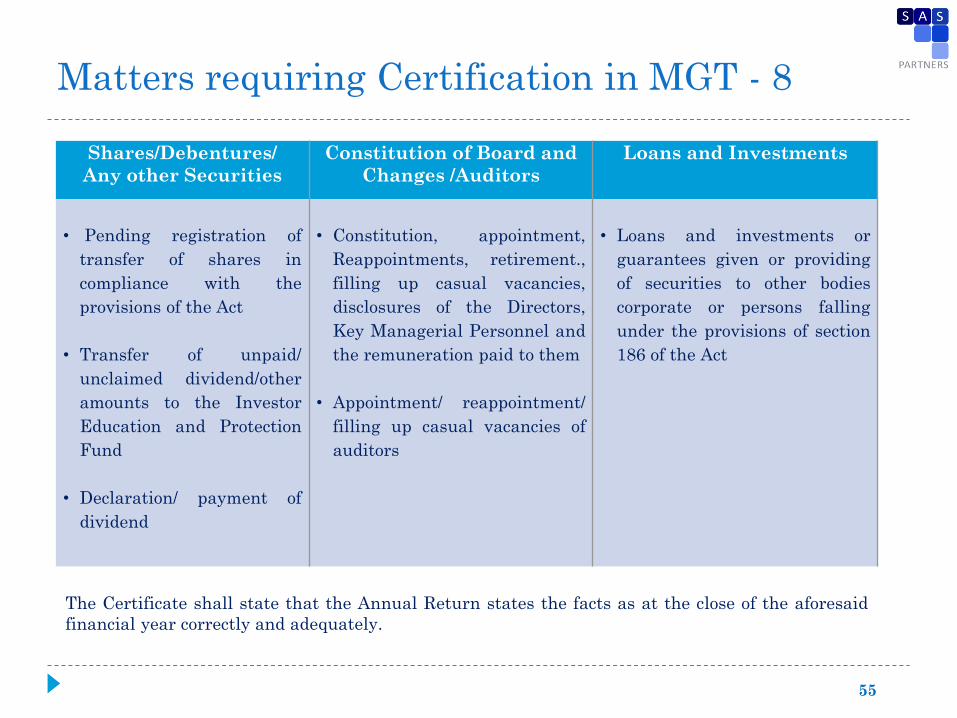

Matters requiring Certification in MGT - 8

55

Shares/Debentures/

Any other Securities

Constitution of Board and

Changes /Auditors

Loans and Investments

• Pending registration of

transfer of shares in

compliance with the

provisions of the Act

• Transfer of unpaid/

unclaimed dividend/other

amounts to the Investor

Education and Protection

Fund

• Declaration/ payment of

dividend

• Constitution, appointment,

Reappointments, retirement.,

filling up casual vacancies,

disclosures of the Directors,

Key Managerial Personnel and

the remuneration paid to them

• Appointment/ reappointment/

filling up casual vacancies of

auditors

• Loans and investments or

guarantees given or providing

of securities to other bodies

corporate or persons falling

under the provisions of section

186 of the Act

The Certificate shall state that the Annual Return states the facts as at the close of the aforesaid

financial year correctly and adequately.

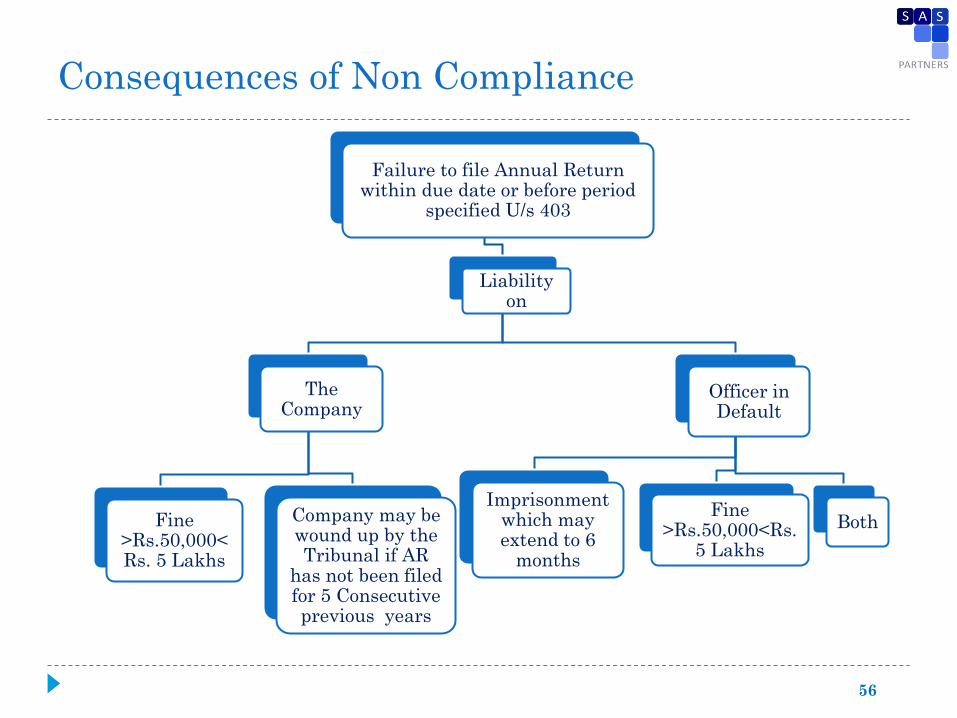

Consequences of Non Compliance

56

Failure to file Annual Return within due date or before period

specified U/s 403

Liability on

The Company

Fine >Rs.50,000<Rs. 5 Lakhs

Company may be wound up by the Tribunal if AR

has not been filed for 5 Consecutive previous years

Officer in Default

Imprisonment which may extend to 6

months

Fine >Rs.50,000<Rs.

5 Lakhs

Both

Disqualification u/s 164 (2) (a):

Every person who is or has been director of that company shall not be eligible for re-appointment

as Director of that company or appointed in any other company for a period of five years from the

date on which the said company fails to do so if the company has not filed its Annual Return for

continuous period of three financial years

Section 455(1) explanation:

If the Company has not filed its Annual Return for last two financial years, it will

be termed as “inactive company”

Section 455(4)

If the Company has not filed its Annual Return for two financial years consecutively, the

Registrar shall issue notice to the Company and enter its name in the Register of Dormant

Companies.

Consequences of Non Compliance

57

Section 433 of CA’ 1956 [Section 271 under CA’ 2013 – not notified]

A company may be wound up by the Tribunal, -

If the company has made a default in filing with the Registrar, annual return for any five

consecutive financial years.

Compounding of offence – Section 621A

Offence in respect of default in filing annual return is compoundable with the

permission of the Special court, in accordance with the procedure laid down in the

Code of Criminal Procedure, 1973 for compounding of offences.

As section 441 has not yet been notified, section 621A of the Companies Act, 1956 will

continue to be in force and under that section, the offence is compoundable by the

Company Law Board or where the maximum amount of fine which may be imposed for such

offence does not exceed fifty thousand rupees, by the Regional Director.

Consequences of Non Compliance

58

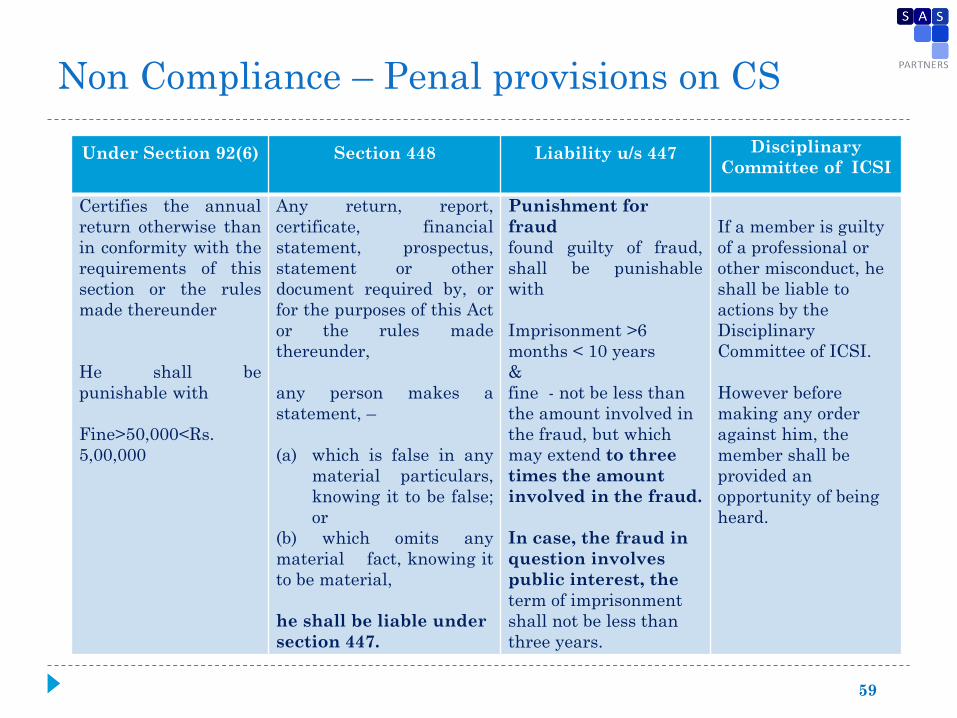

59

Under Section 92(6) Section 448 Liability u/s 447 Disciplinary

Committee of ICSI

Certifies the annual

return otherwise than

in conformity with the

requirements of this

section or the rules

made thereunder

He shall be

punishable with

Fine>50,000<Rs.

5,00,000

Any return, report,

certificate, financial

statement, prospectus,

statement or other

document required by, or

for the purposes of this Act

or the rules made

thereunder,

any person makes a

statement, –

(a) which is false in any

material particulars,

knowing it to be false;

or

(b) which omits any

material fact, knowing it

to be material,

he shall be liable under

section 447.

Punishment for

fraud

found guilty of fraud,

shall be punishable

with

Imprisonment >6

months < 10 years

&

fine - not be less than

the amount involved in

the fraud, but which

may extend to three

times the amount

involved in the fraud.

In case, the fraud in

question involves

public interest, the

term of imprisonment

shall not be less than

three years.

If a member is guilty

of a professional or

other misconduct, he

shall be liable to

actions by the

Disciplinary

Committee of ICSI.

However before

making any order

against him, the

member shall be

provided an

opportunity of being

heard.

Non Compliance – Penal provisions on CS

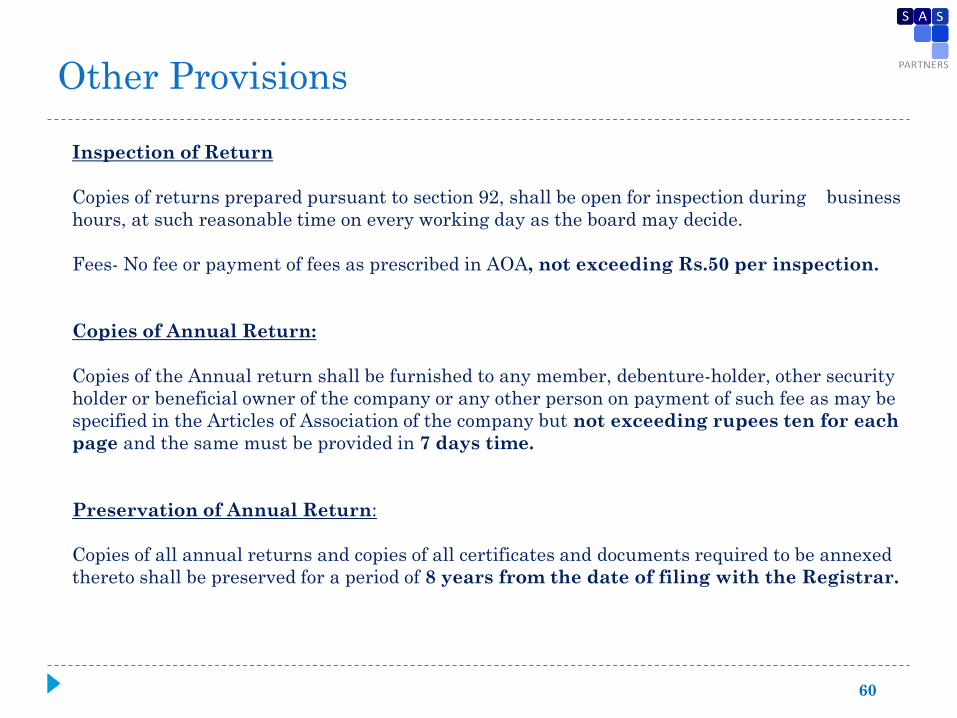

Inspection of Return

Copies of returns prepared pursuant to section 92, shall be open for inspection during business

hours, at such reasonable time on every working day as the board may decide.

Fees- No fee or payment of fees as prescribed in AOA, not exceeding Rs.50 per inspection.

Copies of Annual Return:

Copies of the Annual return shall be furnished to any member, debenture-holder, other security

holder or beneficial owner of the company or any other person on payment of such fee as may be

specified in the Articles of Association of the company but not exceeding rupees ten for each

page and the same must be provided in 7 days time.

Preservation of Annual Return:

Copies of all annual returns and copies of all certificates and documents required to be annexed

thereto shall be preserved for a period of 8 years from the date of filing with the Registrar.

Other Provisions

60

Promoter’s Shareholding (Section 93)

Every listed company is required to file with the Registrar, a return in Form No. MGT-10 with

respect to changes relating to either increase or decrease of two percent or more in the

shareholding position of promoters and top ten shareholders of the company in each case, within

fifteen days of such change.

Place of keeping Annual Return (Section 94(1))

The copies of Annual Return shall be kept at the Registered Office of the company or with the

approval of members by way of a Special Resolution, at any place in India, where more than

1/10 the of the total members reside, provided the copy of such resolution is given to the

Registrar in advance.

Annual Return as evidence (Section 95)

The details contained in the return are admissible as prima-facie evidence in Courts and

other Judicial Authorities.

If a person’s name is shown as member in the Return, then it is conclusive evidence about

the person’s membership in the Company.

If a Company submits a Certified True copy of Return by Roc they are admitted on record,

the Court need not have to prove the truth of contents of the Return.

Other Provisions

61

Section 134 (3) (a)

As per Section 92(3) read with Rule 12 of Companies (Management and Administration) Rules,

2014, every Company is required to attach with its Board’s report, an extract of Annual return

as specified in Form MGT-9.

Contents of MGT – 9

Registration details

Principal business

Particulars of Holding, Subsidiaries and Associate Companies;

Shareholding pattern (Equity break up as % of total equity) Category wis

shareholding

Indebtedness

Remuneration of Directors and KMPs

Details of Punishment/Penalties/Compounding of offences

Extract of Annual Return in Form Mgt – 9

62

Signing of MGT – 9

Signed by the Chairperson of the company, if he is authorized by the Board to do so, or where

he is not so authorized, by at least two directors, one of whom shall be a managing director, or

by the director where there is one director.

Section 134 (8) - Penalty for Non compliance under the provisions of this section

On company shall be punishable

With fine > Rs.50, 000 < Rs. 25 Lakhs

Officer who is in default

Punishable with

Imprisonment for a term which may extend to three years or

Fine > Rs.50, 000 < Rs. 5 Lakhs or

with both.

Extract of Annual Return in Form Mgt – 9

63

Section 384 (2) and Rule 7 of Companies (Registration of Foreign Companies) Rules,

2014.

Every Foreign Company shall

File Annual Return within 60 days from the last day of its financial year.

In Form FC – 4 containing particulars as they stood on the close of the financial year.

Section 2(42) - Foreign company means

Any company or body corporate incorporated outside India which—

a) has a place of business in India whether by itself or through an agent, physically or

through electronic mode; and

b) conducts any business activity in India in any other manner.

Annual Return by a Foreign Company

64

Term Definition

Remuneration ―Remuneration‖ means any money or its equivalent given or passed to

any person for services rendered by him and includes perquisites as

defined under the Income-tax Act, 1961;

Deposits Deposit includes any receipt of money by way of deposit or loan or in any

other form by a company, but does not include such categories of amount

as may be prescribed in consultation with the Reserve Bank of India

Debenture Debenture includes debenture stock, bonds and any other instrument

evidencing a debt, whether constituting a charge on the assets of the

company or not.‖

Key Definitions – MGT - 7

65

the expression ―company‖ includes any

body corporate;

“layer” in relation to a holding company means

its subsidiary or subsidiaries;

Term Definition

Key

Managerial

personnel

―Key managerial personnel‖, in relation to a company, means –

the Chief Executive Officer or the managing director or the manager;

the company secretary

the whole-time director

the Chief Financial Officer; and

such other officer as may be prescribed.

Officer – 2(59) Officer includes any director, manager or KMP or any person in

accordance with whose directions or instructions the Board of directors or

any one or more of the directors is or are accustomed to act.

Charge ―Charge‖ means an interest or lien created on the property or assets of a

company or any of its undertakings or both as security and includes a

mortgage

Key Definitions – MGT - 7

66

Thank you for your kind attention