annual report - start

TRANSCRIPT

2015Annual Report

BANKGIROT 105 19 Stockholm. VISITORS Palmfeltsvägen 5. SWITCHBOARD +46 8 725 60 00. WEBSITE bankgirot.se/enHEAD OFFICE Stockholm. CIN 556047-3521 VAT NO. SE556047352101

20

23

24

26

27

28

36

12

11

PAYMENT MODELS

DEPOSIT INSURANCE

02

03

04

07

08

15

18

19

IMPORTANT EVENTS 2015

FOREWORD FROM THE CHAIR OF THE BOARD

FOREWORD FROM THE CEO

BANKGIROT'S OFFERING

EARLY ACTOR

CUSTOMER SERVICE

BOARD OF DIRECTORS

MANAGEMENT TEAM

DIRECTORS' REPORT

INCOME STATEMENT

BALANCE SHEET

EQUITY

CASH FLOW STATEMENT

NOTES TO THE ACCOUNTS

AUDITORS' REPORT

WRITERS Karl Bruze, Susanna Kull, Intellecta Corporate PHOTOGRAPHERS Christoffer Edling, Robert EldrimGRAPHIC PRODUCTION AND PRINTING INEKO

Ineko, Stockholm 2016/260659, Environmentally-labelled printed matter 341142

15

1819

07

04

08

12

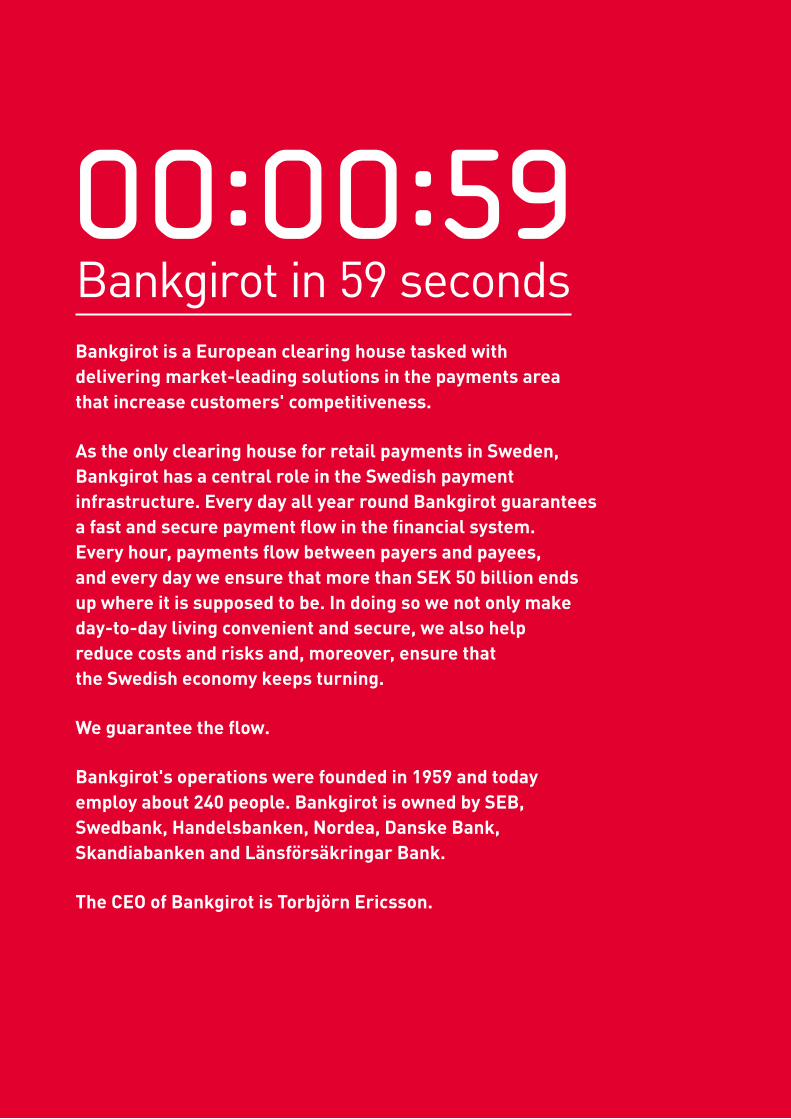

Bankgirot in 59 seconds00:00:59Bankgirot is a European clearing house tasked with delivering market-leading solutions in the payments area that increase customers' competitiveness.

As the only clearing house for retail payments in Sweden, Bankgirot has a central role in the Swedish payment infrastructure. Every day all year round Bankgirot guarantees a fast and secure payment flow in the financial system. Every hour, payments flow between payers and payees, and every day we ensure that more than SEK 50 billion ends up where it is supposed to be. In doing so we not only make day-to-day living convenient and secure, we also help reduce costs and risks and, moreover, ensure that the Swedish economy keeps turning.

We guarantee the flow.

Bankgirot's operations were founded in 1959 and today employ about 240 people. Bankgirot is owned by SEB, Swedbank, Handelsbanken, Nordea, Danske Bank, Skandiabanken and Länsförsäkringar Bank.

The CEO of Bankgirot is Torbjörn Ericsson.

2 IMPORTANT EVENTS 2015

AVAILABILITY IN the Clearing and Settlement Service was 99.95 percent on an annual basis.

SETTLEMENT IN REAL TIME remained stable with availability at 99.91 percent.

A TOTAL OF almost 950 million payments were processed in the Bankgiro System, an increase of 4.9 percent compared to 2014.

SWISH, WHICH BANKGIROT develops and manages on behalf of Getswish AB, processed more than SEK 50 billion. The most Swish payments in a single day were recorded on 23 December, with almost 500,000 transactions.

4 MILLION USERS – the number of active Swish users at the end of 2015. The verb to swish (swisha in Swedish) was included in the 2015 list of new Swedish words issued by the Language Council of Sweden, and is also seen in its swedicised form svischa.

THE AUTUMN SAW final testing of a new custom version of Swish for e-commerce, which was launched on 18 January 2016.

CUSTOMER SATISFACTION as regards Bankgirot's products and services remained very high. A full 91 percent stated that they are satisfied with our quality and our services.

IN AUGUST, Torbjörn Ericsson took office as CEO of Bankgirot. He succeeds Birgitta Simonsson, who retired.

Important Events 2015

On 28 December 2015 Bankgirot settled interbank payments totalling more than SEK 128 billion. On an average bank day the total is about SEK 50 billion.1

SEK 717 million in 2012SEK 713 million in 2013SEK 725 million in 2014SEK 789 million in 2015

The company's profit for 2015 was SEK 65.8 million.

1 This includes all of Bankgirot's settlements at the Riksbank. Bankgiro System, Payments in Real Time, Dataclearing (interbank account transfers), Bankgirot's Cash Management, settlement of VISA and MasterCard transactions and ATM transactions.

SEK 128,000,000,000 Bankgirot's sales

Average value in SEK per bank dayIn 2015 payments totalling an average of almost SEK 40 billion were processed each bank day.

Number of Bankgiro payments per bank dayIn 2015 Bankgirot handled 3.8 million Bankgiro payments per bank day (based on 251 bank days).

0

200

400

600

800

1,000Value, SEK billions Number, millions

0

2,000

4,000

6,000

8,000

10,000

12,000

20152014201320122011

Processed amount and number of payments in the Bankgiro System

3

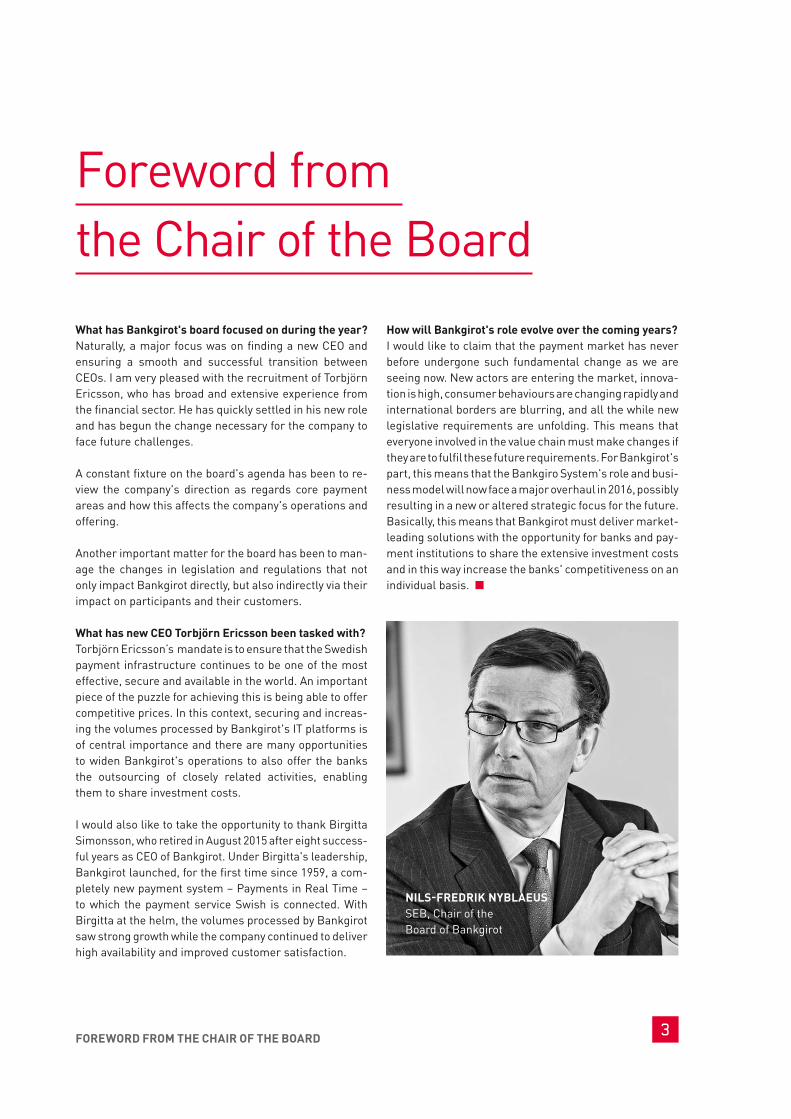

What has Bankgirot's board focused on during the year?Naturally, a major focus was on finding a new CEO and ensuring a smooth and successful transition between CEOs. I am very pleased with the recruitment of Torbjörn Ericsson, who has broad and extensive experience from the financial sector. He has quickly settled in his new role and has begun the change necessary for the company to face future challenges.

A constant fixture on the board's agenda has been to re-view the company's direction as regards core payment areas and how this affects the company's operations and offering.

Another important matter for the board has been to man-age the changes in legislation and regulations that not only impact Bankgirot directly, but also indirectly via their impact on participants and their customers.

What has new CEO Torbjörn Ericsson been tasked with?Torbjörn Ericsson’s mandate is to ensure that the Swedish payment infrastructure continues to be one of the most effective, secure and available in the world. An important piece of the puzzle for achieving this is being able to offer competitive prices. In this context, securing and increas-ing the volumes processed by Bankgirot's IT platforms is of central importance and there are many opportunities to widen Bankgirot's operations to also offer the banks the outsourcing of closely related activities, enabling them to share investment costs.

I would also like to take the opportunity to thank Birgitta Simonsson, who retired in August 2015 after eight success-ful years as CEO of Bankgirot. Under Birgitta's leadership, Bankgirot launched, for the first time since 1959, a com-pletely new payment system – Payments in Real Time – to which the payment service Swish is connected. With Birgitta at the helm, the volumes processed by Bankgirot saw strong growth while the company continued to deliver high availability and improved customer satisfaction.

How will Bankgirot's role evolve over the coming years?I would like to claim that the payment market has never before undergone such fundamental change as we are seeing now. New actors are entering the market, innova-tion is high, consumer behaviours are changing rapidly and international borders are blurring, and all the while new legislative requirements are unfolding. This means that everyone involved in the value chain must make changes if they are to fulfil these future requirements. For Bankgirot's part, this means that the Bankgiro System's role and busi-ness model will now face a major overhaul in 2016, possibly resulting in a new or altered strategic focus for the future. Basically, this means that Bankgirot must deliver market- leading solutions with the opportunity for banks and pay-ment institutions to share the extensive investment costs and in this way increase the banks' competitiveness on an individual basis. n

FOREWORD FROM THE CHAIR OF THE BOARD

Foreword from the Chair of the Board

NILS-FREDRIK NYBLAEUSSEB, Chair of the Board of Bankgirot

4 FOREWORD FROM THE CEO

Could you share with us a few impressions from your initial time as CEO of Bankgirot?After an intensive first six months, I can conclude that I have taken command of an impressively well-run compa-ny. Every day I can see how methodical the entire operation is, down to the smallest detail. This is particularly appar-ent in the well-oiled organisation, which makes it easy to quickly gather forces to handle peak loads or deviations. The employees' combination of solid expertise, dedication and willingness to always go that extra mile has greatly impressed me. And the results can be seen in the recur-ring high and uniform quality of our deliveries.

2015 was an eventful year – how would you like to summarise the past year from an internal viewpoint? We have successfully managed the growth in volume in our real time system while maintaining availability and qual-ity, with our clearing and settlement service attaining top results. Our real time system also handled the enormous flow of new Swish users, which was mostly concentrated in the last six months of the year, and which means that

the service now has more than four million active users. Of course, volume growth is a pleasing develop ment and something we expected, but it is difficult to predict when it will take place. As long as volumes continue to grow, efforts will continue to refine every part of the ecosystem in which the Payments in Real Time platform takes centre stage.

And from an external viewpoint?Looking outwards, we can see that the payment market is undergoing considerable change with the launch of new payment services and a declining use of cash. Tradition-al actors in the payment market are being challenged by new, non-financial actors, all with their sights set on es-sentially the same volumes and fulfilling the same cus-tomer needs. Our customers, the banks, remain focused on optimisation and reduced costs, and efforts to comply with new and coming regulations consume extensive re-sources. On top of this we have the standardisation of the payment market, which is starting to manifest itself more clearly, and this places demands on the clearing houses' ability to offer modular systems that allow a more selec-tive choice of services and products than before.

If we consider MasterPass and, not least, Payments in Real Time with Swish as the first payment flow – both good examples of joint work by the banks to create innovative solutions that clearly reflect market trends and needs – then I believe that the way forward is to cooperate and do more together. This provides leeway for all involved to also concentrate on their core operations.

2015 was characterised by the continued stable delivery of Bankgirot's services and products with retained quality, availability, good growth and volume development. This provides us with a solid foundation for the continuing work to develop the future pay-ment infrastructure and innovative products and services that fulfil customer needs.

Well prepared for a future at the cutting edge of technology

5FOREWORD FROM THE CEO

TORBJÖRN ERICSSONChief Executive Officer

Well prepared for a future at the cutting edge of technology

6

So what are Bankgirot's priorities for the near future to face challenges and leverage opportunities? From our standpoint, we need to adapt to changes in the world around us and increased competition while retain-ing our focus on customer benefits and the insight that our journey of change must continue and be intensified. One priority for 2016 is to increase the volumes in all products and services, which requires proactivity to secure our daily deliveries by means of planning, performance, expertise and readiness. We are keeping a firm grasp on Bankgirot's ability to deliver quality and security. Our customers must be able to rely on our deliveries being made on time and to the right account – every hour, every day, all year round.

That we are moving towards some form of standardisation is irrefutable. While waiting for a decision on how the future payment infrastructure will be realised, we must still act. We must support the banks by consolidating and stream-lining the existing payment structure so as to standard-ise payments, making them easy and effective regardless of country and channel. We must also carefully examine the extent to which we can help optimise the banks’ payment systems, platforms and payment processes.

This requires the continual refinement of our offering and complete adaptation to real time systems, as well as the continued development of market-specific and innovative products, with reduced time to market. We must also ex-amine international opportunities where we can assume a clearer position, while also allowing for the effects of new competitors.

Yet another aspect that I would like to highlight is the work we have done to clarify what Bankgirot is and what we can do for our customers. The combination of being a clearing house and a regulated FinTech company, together with our long history and position at the very cutting edge of technology, makes us quite unique. We should be proud of being regulated, since this gives Bankgirot a unique market position in that everything we do must be char-acterised by rigorous security, availability and quality. In the digitised society this makes us the leading supplier of secure payment solutions and related infrastructures. In other words, Bankgirot guarantees the flow!

Stockholm, March 2016 n

FOREWORD FROM THE CEO

7

CLEARING AND SETTLEMENTClearing and Settlement is the core of Bankgirot's ope-rations and through this service Bankgirot contributes to guaranteeing security and keeping down costs in the financial system. This operation is licensed by the Swed-ish Financial Supervisory Authority and supervised by Sweden's central bank, the Riksbank.

PAYMENTSPayments in the Bankgiro System and associated ser-vices comprise Bankgirot's historical origin. At the end of 2015, 21 banks were affiliated. With the Payments in Real Time payment system Bankgirot even enables interbank transfers in real time. The first service to make use of the Payments in Real Time platform is the mobile payment solution Swish, which can now be joined by new innovative payment flows.

DIGITAL SERVICESBankgirot offers services to banks and the banks' joint companies based on shared IT solutions and related pe-ripheral services. The offering includes operation, ad-ministration and development in the areas of electronic identification and signatures and mobile payments. Ad-ditionally, we also offer services for electronic invoicing and information management that enable the digitisation of day-to-day finances.

ADVICE AND SERVICECustomer Service offers tailored services for Bankgirot's products. n

Bankgirot's offering

8 EARLY ACTOR

Early actor with a cutting-edge position in technology

JOSEFINE RUSSOHead of Digital Information

JENNY WINTHERHead of Products and Services

9EARLY ACTOR

"Today, Bankgirot serves increasingly as a discussion partner and enabler for the banks' technically innovative solutions. Even if cost efficiency is a central issue in our dialogues with the banks, our owners, there is also a strong focus on the areas where Bankgirot is working to develop new solutions. The owners have expectations for the continued development of payments, with an emphasis on security and new flows for Payments in Real Time. An important aid in this work is a mutual understanding of the importance of operational reliability and expertise in payment infrastructure, which is becoming increasingly important due to the rapid growth in transactions," explains Jenny Winther, Head of Products and Services at Bankgirot.

BANKGIROT INSTILS CONFIDENCE As a platform for the banks' shared solutions, infrastruc-ture and cooperation, Bankgirot also has a positive in-fluence on society in general. Confidence in the payment system always working facilitates business agreements and contributes to favourable conditions for economic welfare. Jenny emphasises, however, that most people take the infrastructure provided by Bankgirot for granted:

"When we talk about what Bankgirot does and our central role in the Swedish financial system, many people are surprised. But it is also our central role in retail payments, under the supervision of the Swedish Financial Supervisory Authority and the oversight of the Riksbank, that makes us the natural choice when rapid progress in digital development demands a guarantor for security, availability and authenticity. And this is a need that will only increase as more new types of actors establish operations in the payment market," says Jenny.

Payment infrastructure is very much about creating uni-formity. This also means that new major products are seldom seen.

"Development most often entails basic functions and products being refined, as well as adapted to new circumstances and changing demand," Jenny continues.

GUARANTEES SECURE FLOWSJosefine Russo, Head of Digital Information at Bankgirot, offers an example of how Bankgirot's high level expertise in security and electronic identification is in demand and put to good use: "One concrete example of how Bankgirot creates value and benefits customers and society is the launch of MasterPass, MasterCard's digital wallet. The banks did not consider the original security solution sufficiently secure compared to what we are used to. So Bankgirot was engaged by the banks to develop a function that enables BankID to be used as the identification solution. Pilot tests were conducted in 2015 and this functionality will be commissioned in the spring of 2016," Josefine explains.

PAYMENTS IN REAL TIME CREATES NEW DEMANDBoth Josefine and Jenny underline that Bankgirot's Pay-ments in Real Time is an important milestone in technolo-gy development.

Since 1959, Bankgirot has provided the under-lying financial infrastructure for processing payments and payment information. Every day all year round Bankgirot generates a fast and secure flow of transactions, which also makes us the central hub of the Swedish financial system. In recent years, Stockholm has garnered attention as one of the foremost global FinTech clusters – a development that has involved Bankgirot.

1959 Bankgirocentralen begins operations, which are initially paper-based.

1965 The first computers are installed at Bankgirot.

1969 Autogiro direct debit service introduced for consumer payments.

1970 OCR technology established, enabling the electronic recognition of payment slips.

1996 Internet-based payment services introduced.

2003 Electronic ID service introduced.2012 A new payment system is launched that

enables payments in real time.

Bankgirot’s technical history

10 EARLY ACTOR

"With the launch of Payments in Real Time in 2012, Bankgirot also unveiled the world's first payment system with the ability to handle multiple payment flows in real time. The launch was a success and the payment system has continued to attract extensive international interest," Jenny reports.

Payments in Real Time is also an enabler for the mobile payment service Swish, which was developed parallel to Payments in Real Time. Behind the service is the banks' joint company Getswish AB. The Swish success story has entailed increased expectations for services available in real time, which provides the banks with favourable op-portunities to develop and offer additional payment ser-vices that meet customer demand and create increased customer benefits.

BANKGIROT PART OF STOCKHOLM FINTECHThe extensive breadth and knowledge in the field of IT development that is predominantly found in Stockholm makes Bankgirot's home town the European city – next to London – with by far the largest investments in the cross-over between finance and technology this past ten years.

"Sweden's population has long been to the fore when it comes to using the internet, online banking and smartphones," Josefine explains.

In a study of the FinTech sector in Stockholm that was published in 20151, the 1959 founding of Bankgirot com-prises the starting point for development on the over-

arching timeline. In recent years, FinTech investments in Stockholm have been overwhelmingly biased towards the payments area. Josefine points out that this underlines Bankgirot's continued central position and importance in the development of Stockholm's FinTech sector:

"The infrastructure that Bankgirot provides – with generic services that are available to all actors – also enables completely new innovative actors to establish operations," says Josefine. n

1 Report from the Stockholm School of Economics: Stockholm FinTech – An overview of the FinTech sector in the greater Stockholm Region.

Stockholm attracted 18 percent of investments in the European FinTech sector in 2014, corresponding to 32 per of the total investments in Sweden. Among the FinTech companies in Stockholm that attracted the largest invest-ments in 2014 we find the payment solutions Klarna and iZettle. At least 4,600 people were working in the FinTech sector in Stockholm that same year. A few of the explanations usually put forward for Stockholm's FinTech success are extensive and early personal computer use, the Swedish corporate management style and a natural global focus due to the limited size of the domestic market.

Stockholm FinTech

XXXXX 11

Cooperation for improved deposit insurance

The Swedish National Debt Office is the underwriting au-thority tasked with handling deposit insurance. Deposit insurance is intended to contribute to financial stability by creating peace of mind for savers and reducing the chances of mass withdrawals in conjunction with finan-cial turbulence. Complying with the requirements of the new legislation for faster payment demands a new, more automated solution. The service that Bankgirot and the Swedish National Debt Office have developed – Digital Account Registration – is an industry-wide solution based on existing infrastructure for electronic identification and retail payments.

Once the new deposit insurance regulations come into effect, the new Digital Account Registration service will enable depositors to register an account via the Swedish National Debt Office website or any bank connected to

the service. Secure identification will be achieved using BankID, after which deposit insurance settlements will reach the recipient's account within seven working days. The current payment procedure, using money orders and cheques, will be retained for depositors who do not reg-ister an account.

"This is an important support system for handling deposit insurance and we are very pleased to have developed an effective solution together with Bankgirot. This is a consid erable project that needed to be implemented in a short space of time and must be ready for use at all times. That a depositor can register an account into which compensation can be paid puts Sweden well ahead in this area," says Helena Persson, Deposit Guarantee Manager at the Swedish National Debt Office. n

As a consequence of a revised EU Directive, the payment of compensation from deposit insurance is to be made within seven working days as of July 2016, as compared to twenty working days previously. The Swedish National Debt Office (Riksgälden) has worked together with Bankgirot to enable faster payment.

XXXX12

PER ZETTERBERGProduct Manager Interbank Payments

NIKLAS HELLGRENProduct Manager Swish

13PAYMENT MODELS

A brief review of current payment models

Parallel to the Riksbank launching new banknotes and coins in 2016, Apple and Google are both due to roll out their mobile payment solutions internationally. The list of digital payment services is extremely long, and while some can now be considered well established others pale in comparison: Swish, Klarna, PayPal, WyWallet, iZettle, Dibs, Qliro, Google Wallet, Bitcoin, SEQR, Apple Pay, Payair, Betalo, Linkpay, MasterPass and V.me.

Card payments maintain their firm grasp on the number one spot as the most popular payment method by far. Even invoicing is holding on relatively well, while cash is declin-ing in stature. Mobile payments are on the increase – in terms of both users and the number of transactions – even if their use is currently limited. There are, however, signs that mobile payments are the most common form of pay-ment between friends in Sweden. The explanation is, quite simply, Swish, which Bankgirot develops and operates on behalf of Getswish AB.

PAYMENTS IN REAL TIME ARE THE FUTUREAvailability is the most appreciated aspect of the mobile payment market. When it comes to availability, the real time component – which those who use Swish have al-ready begun to take for granted – is central to the dramatic impact on society. Payments in real time have been en-abled by the globally unique Payments in Real Time plat-

form that was launched by Bankgirot in December 2012, as Per Zetterberg, Product Manager Interbank Payments at Bankgirot, explains:

"This platform enables the instant transfer of money between sender and recipient. Bankgirot owns the Payments in Real Time system and we consider it our first building block for a modern infrastructure that will enable instant payments. Other European countries still lack an equivalent service," says Per.

NUMBER OF TRANSACTIONS QUADRUPLEDIn 2015 the number of transactions via Payments in Real Time almost quadrupled. So far, however, it is only Swish that makes use of the platform.

"Interest from the banks for Payments in Real Time remains great. Particularly in the new types of flows that the platform enables, alongside the existing Swish service, which mostly encompasses payments between consumers or from consumers to businesses. The growth in volume has consistently exceeded all expectations. In the future, Payments in Real Time will also be offered for use with, for example, payments between businesses and other alternative flows," Per explains.

Niklas Hellgren, Product Manager Swish at Bankgirot, emphasises that Bankgirot is very proud about being entrusted to operate and manage Swish, which like Pay-ments in Real Time is characterised by great stability.

SWISH OFFERS SEVERAL ADVANTAGES"Interest from other countries has been great. I believe the reason for this is that the solution is unique: a realtime, accounttoaccount solution that provides such extensive coverage of the Swedish market. Via the participating banks, Swish enables access to perhaps 97–98 percent of the market's payment customers, despite the fact that not all banks are affiliated," Niklas explains.

As payment habits change and the use of cash declines, increasingly more new actors pop up in the payment market offering in-novative digital payment services. Regard-less of how the Swedish payment market is shaped in ten years' time, in all likelihood, it will be based on Bankgirot's underlying infrastructure with its world-leading solutions for payments in real time.

14

Real-time transfers mean that no one has to worry about drawing the shortest straw. People's growing experience of payments in real time also creates completely new op-portunities in the payment market.

"We find that Swish enables new types of payment scenarios since you avoid the need to handle cash when making payments," Niklas continues.

OVER FOUR MILLION PEOPLE USE SWISHThe total number of people who have downloaded the Swish app passed four million in 2015. The critical mass defining success has now been well and truly passed.

"The service is spread by word of mouth and drives itself by satisfied customers spreading the message to others. In the Swedish language, the name first became a concept and then developed from a noun to a verb on the list of new words issued by the Language Council of Sweden," says Niklas.

"If someone doesn't have Swish, it's a bit like they're living in the stone age. People expect their friends to have Swish," Per interjects.

In many ways, mobile phones have replaced wallets and payment cards. Consequently, one important new pay-ment model for direct purchases is Swish Commerce, which will provide an effective and secure e-commerce experience without the need for a payment card.

SWISH COMMERCE IS A HIGHLY ANTICIPATED SERVICEOn 18 January, Swish was launched in a new, specially adapted version for e-commerce, making it easy to shop – and pay – online. The solution provides online retail-ers with the opportunity to offer their customers this new payment method in both apps and traditional web shops. All transactions take place in real time, just like when consumers use Swish to transfer money to each other.

"Swish has a large and expanding customer base with more than four million users who find it an easy and convenient way to pay. That is why we think that this solution can bring increased sales to online retailers," says Niklas.

Demand for Swish among online retailers has been great and many already use the service together with their own technical solutions. The new customised and standard-ised interface makes it easier for online retailers to get started with Swish and to offer this payment method to their customers.

"As a simple payment method Swish will contribute to growth in ecommerce, but it's the retailers themselves who exhibit creativity and show the way forwards. Increasingly more people consider mobile phones a tool for optimising the purchase process and incorporate them to create a better shopping experience for their customers," Niklas concludes. n

PAYMENT MODELS

15CUSTOMER SERVICE

Customer service that embodies the brand

KATHARINA HJORTH MALIN WESTMAN DAVID SELANDER

Accessible and knowledgeable customer service is essential to instilling confidence and gaining customer loyalty. Bankgirot clearly succeeds at this since year after year the company is rewarded with extremely favourable customer ratings. What is the secret?

KATHARINA An acute awareness of the fact that how we deal with customers reflects upon our brand. And this is a responsibility that we take very seriously, with the aim of delivering customer benefits in every customer relation. Accordingly, based on our service policy we work contin-ually to develop customer relations, working with not

From year to year, customer satis-fac tion with Bankgirot's products and services remains above 90 percent. A figure that few companies even approach. Solid expertise, a focus on customer benefits and continual improvement work – that is Bankgirot's recipe for success.

DAVID SELANDER Support Manager Swish Commerce

Type of customer: Online retailer IT departments,

PSPs (Payment Service Provider)

A frequent question: Problems connecting to the test server

– what are we doing wrong?

KATHARINA HJORTHSupport Manager and Technical Customer Advisor for einvoice

Type of customer: The 21 banks and their corporate customers

A frequent question: Registered for e-invoice but not receiving

any invoices – what's happened?

MALIN WESTMANGroup Manager Customer Service

Type of customer: The 21 banks and their corporate customers

A frequent question: Could you help explain the payment

information I've received?

17CUSTOMER SERVICE

only what we say, but also how we say it. The most impor-tant prerequisite for success is, of course, our employees. The excellent service they provide, and their willingness to help out and build strong customer relations, is why we enjoy the position we have today.

DAVID We also work continually to ensure the quality of our answers, by directly after each contact asking the customer to rate our performance. We even take the op-portunity to ask questions about how they experience availability, service, proactivity and case resolution. In light of the fact that due to bank confidentiality we can-not answer certain questions, our customer ratings are especially pleasing. I believe that one reason for this is that we always try to help our customers by guiding them to where they can get answers in those cases where we cannot help them.

How do you view customer benefits and how does the concept influence your day-to-day work?

KATHARINA For me, delivering customer benefits means facilitating the customer's workaday week by solving their problems, answering their questions and delivering add-ed value. This also entails having an ear for the challeng-es faced by customers, enabling preventative measures to avoid future problems. An important rule of thumb is to unburden the customer by assuming responsibility for solving the problem.

Customer service employees have broad knowledge of all products and services, and are also a central source of valuable information about customers' challenges, questions and opinions. How is all this expertise utilised by the rest of the organisation?

MALIN Very well, I think. The excellent support system that we now have, and which is central to our work, has been successively developed in joint efforts. We have creat ed a structure that supports ongoing improvement work by forwarding input on customer enquiries and challenges to the right people within the organisation. In return, we receive feedback about what is being done about our suggestions and opinions, which often benefit product and service development. In other words, there is a continual internal exchange of knowledge and infor-mation which provides a basis for both support system improvements and product development. In the long run, the internal dialogue not only helps us deliver customer benefits, but even provides an excellent way to increase internal understanding of our different roles.

DAVID Customer service is also an attractive recruitment base for the rest of operations. I myself am an example of that, moving from general customer service to the bank team to my current role within Swish Commerce. The op-portunity to continually develop and find new roles within the organisation is, I believe, a strong contributory factor to why so many people remain within the company for so long.

MALIN I can add that already when recruiting someone to customer service we look at their potential to deve-lop within the company and many current employees at Bankgirot have also followed a career path that began here. Naturally, studies in economics and finance are a plus for applicants, but to an increasingly greater extent so are IT skills.

Finally, any advice on how to create a good customer service department? KATHARINA Continual training and coaching in how to handle customers, both in writing and verbally. This in-cludes what we say, how we express ourselves and how we lead the conversation. And recruiting the right people. Together these two key components lay the foundation for good customer service.

DAVID I would also like to emphasise the somewhat soft-er values. Such as part of the secret is the work environ-ment and corporate culture. It may sound like a cliché, but if I enjoy working with my colleagues, and if the atmos-phere is pleasant and well balanced, then this is reflected in our dealings with customers. Satisfied employees quite simply ensure satisfied customers! n

18 BOARD OF DIRECTORS

BOARD OF DIRECTORS

JOHAN LÖFGRENDanske Bank

ANDERS FAGERDAHLHandelsbanken

LEIF KARLSSONSwedbank

ERIK ZINGMARKNordea

OLLE NYLUNDBankgirot, Employee Representative

NILS-FREDRIK NYBLAEUSSEB, Chair

MARIA JERHAMRE ENGSTRÖMLänsförsäkringar Bank

19

MANAGEMENT TEAM

ULF SANDEGRENCFO

TORBJÖRN ERICSSONCEO

LORRAINE NIELSENHead of Payments

MADELEINE WIDAEUSCIO/Head of IT

HÅKAN YGBERGDigital Services Director

ELISABETH FALLBERGHR Director

20 DIRECTORS' REPORT

ANNUAL REPORT 2015 BGC HOLDING ABThe Board of Directors and Chief Executive Officer of BGC Holding AB hereby submit the annual report and consolidated accounts for the 2015 financial year.

DIRECTORS' REPORT

BGC HOLDING ABBGC Holding AB is the parent company of the following wholly-owned companies:• Bankgirocentralen BGC AB (Bankgirot)• Bankgirot Business Transactions Sweden AB

Business activities consist of directly or indirectly owning and managing:• companies that conduct clearing operations and closely related activities• companies with connections to such financial activities

BGC Holding AB does not conduct any operating activities. Such activ-ities are performed within the subsidiary Bankgirocentralen BGC AB.

The ownership structure of BGC Holding AB is as follows: Skandina-viska Enskilda Banken, 33.1 percent, Swedbank, 29.2 percent, Svenska Handelsbanken, 25.4 percent, and Nordea, 10 percent. The remaining 2.3 percent is owned by Danske Bank, Skandiabanken and Länsförsäk-ringar Bank.

BANKGIROCENTRALEN BGC AB (BANKGIROT)OperationsBankgirocentralen BGC AB is a wholly-owned subsidiary of BGC Holding AB.

The company conducts clearing operations as defined in Chapter 19 and Chapter 1, Section 5, Paragraphs 6a and 6c of the Swedish Securi-ties Market Act (2007:528) and activities closely related to them, as well as other operations as defined in Chapter 20, Section 7, Paragraph 3 of the same act on the condition that the Swedish Financial Supervisory Authority permits such operations. In Bankgirot's case, this comprises electronic invoicing (Bg E-invoice), scanning operations (Bg Scanning Solution), certificates for secure identification (Bg PKI Services) and secure verification and identification of electronic signatures (Bg eID Gateway).

In August, Torbjörn Ericsson took office as the new CEO of Bankgiro-centralen BGC AB. Torbjörn has extensive experience from the financial sector, most recently as COO of the Large Companies and Institutions business area at Swedbank, prior to this holding positions at SEB Mer-chant Banking and Alfred Berg. Torbjörn has also been chair of the boards of the Swedish Securities Dealers Association and SwedSec.

Market and customersBankgirot is the central actor in Sweden in the processing of payments and payment information between banks and bank customers. Bank-girot comprises an important component of the financial infrastructure by offering products and services for clearing payments, credit trans-fers, giro transfers, electronic invoicing and security on the Internet in Sweden. The payment infrastructure enables households, businesses and authorities to make and receive payments in a secure and effec-

tive manner. The Bankgiro System is the only giro system in Sweden that can handle all types of payment regardless of the banks involved. Bankgirot is also the only actor in Sweden licensed by the Swedish Financial Supervisory Authority to conduct clearing operations on retail payments. With its unique position, Bankgirot endeavours to provide secure products and the related infrastructures to banks and payment institutions with operations in Sweden in order to increase their com-petitiveness and to help ensure financial stability. By offering Internet security solutions Bankgirot also helps create security in new innovative solutions that benefit consumers and businesses alike.

Clearing and Settlement Clearing and Settlement is the core of Bankgirot's operations and through this service Bankgirot contributes to keeping down costs in the financial system. This operation is licensed by the Swedish Financial Supervisory Authority and supervised by Sweden's central bank, the Riksbank.

In 2015 Bankgirot once again achieved very good results as regards the quality and availability of Bankgirot's Clearing and Settlement Service. The service is used by the Bankgiro System and its Bankgiro products, as well as by third-party payment products. Bankgirot's Clearing and Settlement Service conducts clearing and creates settle-ment instructions that are sent to the Riksbank's RIX system, which handles settlement in Swedish kronor. For payments in euro Bankgirot sends payment instructions to the remitting bank, which is responsible for settlement taking place in the European Central Bank's settlement system TARGET2. All retail payments in SEK in Sweden between banks, with the exception of payments settled directly in RIX, use Bankgirot's Clearing and Settlement Service.

PaymentsIn terms of volume, Bankgirot's largest service in the payments area is giro transfers, that is, payments in the Bankgiro System. In 2015 pay-ments in the Bankgiro System increased by 4.9 percent compared with 2014, which means that almost 940 billion payments were processed by the Bankgiro System throughout the year.

During the year Bankgirot, together with all participants in and cus-tomers of the Bankgiro System, continued to broaden and elaborate the strategic efforts of the past few years focused on the payment in-frastructure of the future to ensure that we can continue to deliver effective payment solutions with high quality and security in the years to come. Together with the banks, Bankgirot has focused on establishing a common objective and timetable for a future payment infrastructure for Sweden based on European standards. The objective is to make payments easy and effective for banks and their customers regardless of country and channel.

Swish m-/e-com, a mobile payment solution for online and mobile purchases, was launched in 2015. This means that Swish is now one of the payment alternatives alongside card and invoice payments for online and mobile purchases. Swish m-/e-com is a complement to the existing services Swish C2B (mobile payments in real time from con-sumers to businesses) and Swish P2P (mobile payments in real time from consumers to consumers). Consequently, Swish m-/e-com is the third flow to be commissioned on Bankgirot's Payments in Real Time platform. When this payment system was originally launched three

Directors’ Report

21DIRECTORS' REPORT

years ago, it was the first of its kind in the world and now offers multiple payment flows that enable the optimisation of existing and the creation of new payment solutions. Since its launch, Payments in Real Time has received a number of national and international awards and prizes.

The services Swish P2P, Swish C2B and Swish m-/e-com are owned by the company Getswish AB, which in turn is owned by the six largest commercial banks in Sweden. Bankgirot is responsible for the develop-ment, administration and operation of the Swish services. In 2015 the number of active users of Swish P2P exceeded 3.8 million at year-end, which is a major achievement. Nine banks are connected to Swish P2P, six banks are connected to Swish C2B and, by the end of 2015, four banks had connected to Swish m-/e-com.

Electronic invoicing and electronic identification Bankgirot has continued to experience good volume growth in electronic invoicing with the number of transactions increasing by 19 percent. Availability and quality have also remained very high and during the year 250 new companies joined the e-invoicing service. Furthermore, together with the banks Bankgirot continued efforts in function develop-ment and cost efficiency, which resulted in agreement on a long-term objective for the service.

The increased market offering and the use of e-services offered by authorities, banks and other companies have created increased demand for electronic identification services. This contributed to Bankgirot during the year seeing very positive development in Bg PKI Services, the infra-structure for secure electronic communication and identification. Paral-lel to this, demand for gateways for electronic identification, eID Gateway, has fallen due to BankID becoming the dominant solution in recent years. Based on the prevailing market development and Bankgirot's strategic direction, a decision has been made to gradually phase out the service Bg eID Gateway for businesses.

In 2015 Bankgirot also evaluated the company's scanning solution, which together with a desire to streamline the company's offering based on core operations has led Bankgirot to decide to terminate the Bg Scanning Solution service. This will be achieved by selling Bankgirot's customer base to the company's two subcontractors, which provide end customers with the actual service.

Services and availabilityBankgirot's service delivery in 2015 proved stable and achieved the agreed service levels within both the banks' shared Basic Delivery and Bank-specific Delivery without any major deviations. The volume man-aged within Basic Delivery was a little lower than expected. The drop is due to completed optimisation work and continued improvements in Bankgirot's product and service portfolio, which have reduced the number of cases submitted to customer service.

The outcome of the customer surveys conducted throughout the year show increased customer satisfaction, within both Basic Delivery (outcome 86 percent) and Bank-specific Delivery (outcome 89 percent). Consequently, quality has improved since 2014 as regards both compe-tence and service, although the greatest improvement has been seen in proactivity. During the year Bankgirot's customer service worked ac-tively to improve proactivity with individual coaching and performance reviews, which saw improvement in the area.

In efforts to involve employees and increase participation in the development of operations, Bankgirot's customer service has imple-mented a structured method for working with continual improvement. Involvement has been high and throughout the year several hundred improvement suggestions were submitted, with a third being imple-mented so far.

At the beginning of February 2015 Bankgirot launched its new web-site. The aim of the new website is to offer better support for visitors as regards their questions and queries for Bankgirot. Another ambition is to make it easier for visitors to find the information they seek. To-gether with Bankgirot's extranet, the new website creates an effective way to communicate and improve cooperation with both customers and suppliers.

QualityQuality and security are two of Bankgirot's cornerstones. Bankgirot's customers should be able to rely on our systems functioning every hour, every day – and now even every night – all year round. As in previous years Bankgirot exhibited very high quality in all delivered services in all product and service areas. Bankgirot meets tough market demands thanks to active and continuous quality assurance work.

CPMI/IOSCO In its supervision and oversight of the companies that comprise the financial infrastructure, which include Bankgirot, the Swedish Finan-cial Supervisory Authority and the Riksbank use the security and ef-ficiency recommendations found in new international standards as a complement to their own policies. This means that the authorities apply Principles for Financial Market Infrastructures as issued by the Committee on Payment and Market Infrastructures (CPMI) and the International Organization of Securities Commissions (IOSCO). Bank-girot's self-assessment is published on the company's website and the assessment was conducted in accordance with sixteen principles. Bankgirot's compliance with the principles has been assessed such that eleven principles have received the highest rating (Observed) and five principles have received the second highest rating (Broadly Observed). One of the principles for which Bankgirot achieved the highest rating (Observed) is Principle 15, which includes a requirement for "liquid net assets funded by equity". One of the criteria for achieving the highest rating is that Bankgirot's equity and liquid net assets total an amount that guarantees stable continuing operations, secures the capacity to continue developing operations and secures the capacity to withstand serious internal and/or external disruptions.

Sales and profitBankgirot's sales in 2015 totalled SEK 789 million, an increase of SEK 64 million or just under nine percent, while the number of giro transactions increased by almost five percent. The company's profit after financial items for 2015 was SEK 65.8 million (17.2).

22 DIRECTORS' REPORT

Objectives for 2016 Continued growth and volume development One of Bankgirot's most prioritised objectives for 2016, as in previous years, is to increase the volumes of all products and services. Bankgirot works continually to together with the banks canvas the market in order to increase volumes in both the Bankgiro System and Bg E-invoice. A strong driving force to increase volumes is that it enables reduced prices. Moreover, it creates the opportunity to, together with internal optimisation, continually refine and adapt products and services to meet market needs while maintaining high quality. Bankgirot also supports the banks in order to help them more easily sell Bankgirot's services. How the above will be achieved in 2016 has been agreed in consulta-tion with Bankgirot's customers in joint customer forums as well as in individual customer meetings. Bankgirot's close collaboration and planning with its customers aim to ensure that the activities which cre-ate the greatest overall customer benefit are prioritised.

Focus on refining existing functionality and creating increased competi-tiveness for the banks Within the payments area, during the year Bankgirot will focus on imple-menting the banks' agreed development plan, which encompasses the refinement of existing products in the Bankgiro System. Strategically, work will continue to lay the foundation for the future payment infra-structure. This work is conducted in close concert with all banks par-ticipating in the Bankgiro System with the objective of making payments easy and effective, for both the banks and their customers, regardless of country and channel.

Focus on customer relations Our annual customer survey was conducted in September and October. A high response rate of 59 percent, or a total of 636 responses, ensures that the results are statistically significant. More than nine out of ten customers are "very satisfied" or "quite satisfied" overall with Bankgirot as a supplier. Only one percent have responded with the alternative "dissatisfied", which means that general customer satisfaction with Bankgirot totals 91 percent. In preparation for 2016, Bankgirot will use the 2015 customer survey results in its improvement work and continue to develop operations in accordance with the banks' wishes.

Greater efficiency and high delivery quality Bankgirot continues its ongoing improvement work, which has been under way for several years and entails further rationalisation of opera-tions to retain the highest possible delivery quality, to increase delivery capacity and to stabilise customer service. Bankgirot's principal focus remains to deliver each day's transactions on time and to the right accounts

Information about risks and uncertainties The payment market is increasingly driven by common regulations and standards. In order for Bankgirot to retain its market position exist-ing products must be adapted and new products and services must be launched in conjunction with the adaptation of the Swedish payment market to ongoing European and international standardisation. As a result of impending legislative changes, the current payment market

will also be opened to more actors. This development will provide third- party suppliers with direct access to the payer's payment account held at the payment service provider. The implication for Bankgirot is that we must take into consideration an altered commercial scenario in which customer groups are expected to become increasingly fragmented as regards investment cycle, geographic market and focus.

BANKGIROT BUSINESS TRANSACTIONS SWEDEN ABThe company does not conduct any business activities.

CONSOLIDATED PROFITS AND FINANCIAL POSITION

2015 2014 2013 2012 2011

Operating revenue, SEK millions 788.9 725.3 712.9 716.8 758.7

Profit after financial items, SEK millions 65.7 16.5 7.3 16.5 53.4

Total assets, SEK millions 427.5 374.3 356.0 377.4 375.6

Investments, SEK millions * 6.4 12.9 21.4 56.7 26.7

Average no. employees 230 226 223 216 214

* Comprises property, plant and equipment and intangible fixed assets. See Notes 6–9.

PROPOSED APPROPRIATION OF PROFITS

The following earnings are at the disposal of the Annual General Meet-ing of Shareholders:

Retained earnings 15,774,133.10

Profit for the year 10,820.00

SEK 15,784,953.10

The Board of Directors proposes that the earnings be appropriated as follows:

Dividend to shareholders: SEK 0 per share 0.00

Carried forward 15,784,953.10

SEK 15,784,953.10

23

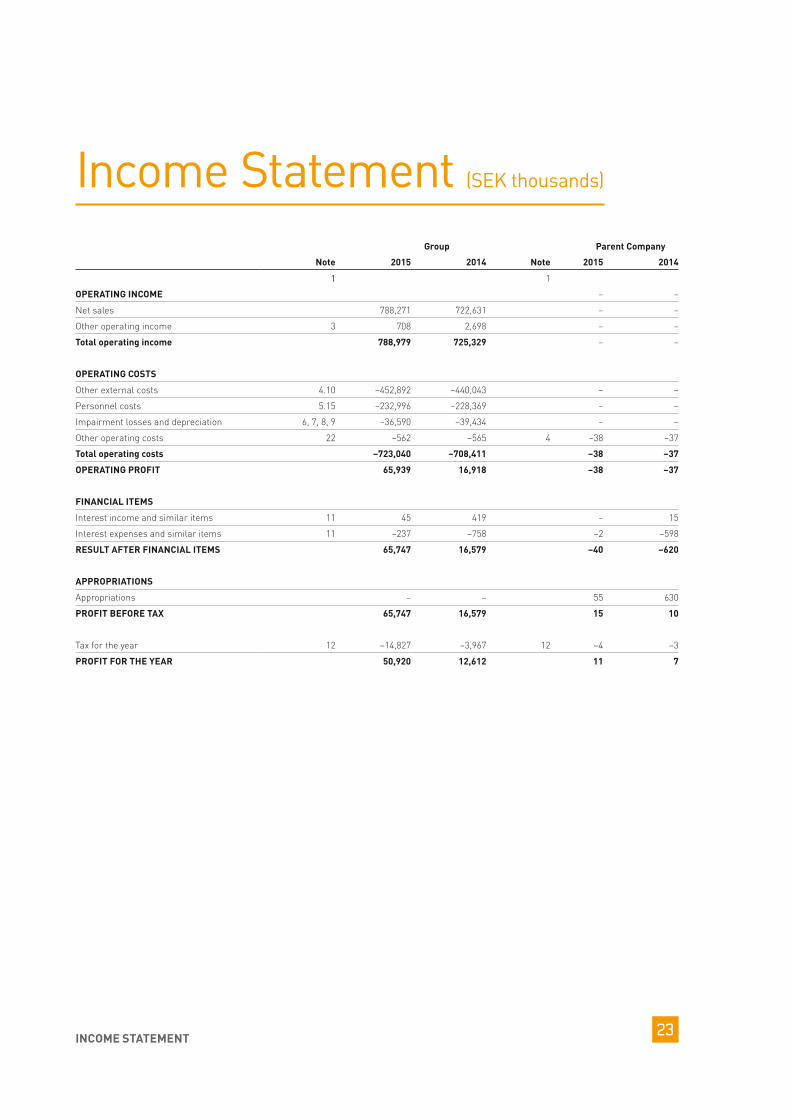

Income Statement (SEK thousands)

INCOME STATEMENT

Group Parent Company

Note 2015 2014 Note 2015 2014

1 1

OPERATING INCOME – –

Net sales 788,271 722,631 – –

Other operating income 3 708 2,698 – –

Total operating income 788,979 725,329 – –

OPERATING COSTS

Other external costs 4.10 –452,892 –440,043 – –

Personnel costs 5.15 –232,996 –228,369 – –

Impairment losses and depreciation 6, 7, 8, 9 –36,590 –39,434 – –

Other operating costs 22 –562 –565 4 –38 –37

Total operating costs –723,040 –708,411 –38 –37

OPERATING PROFIT 65,939 16,918 –38 –37

FINANCIAL ITEMS

Interest income and similar items 11 45 419 – 15

Interest expenses and similar items 11 –237 –758 –2 –598

RESULT AFTER FINANCIAL ITEMS 65,747 16,579 –40 –620

APPROPRIATIONS

Appropriations – – 55 630

PROFIT BEFORE TAX 65,747 16,579 15 10

Tax for the year 12 –14,827 –3,967 12 –4 –3

PROFIT FOR THE YEAR 50,920 12,612 11 7

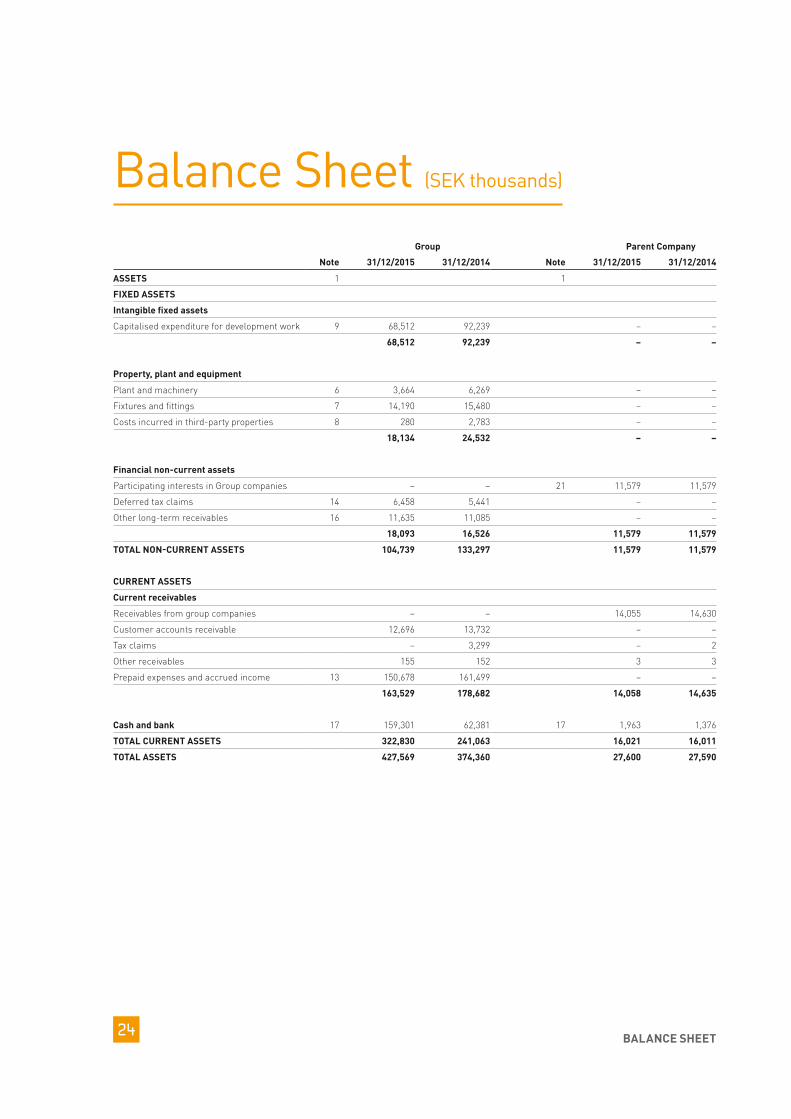

24 BALANCE SHEET

Group Parent Company

Note 31/12/2015 31/12/2014 Note 31/12/2015 31/12/2014

ASSETS 1 1

FIXED ASSETS

Intangible fixed assets

Capitalised expenditure for development work 9 68,512 92,239 – –

68,512 92,239 – –

Property, plant and equipment

Plant and machinery 6 3,664 6,269 – –

Fixtures and fittings 7 14,190 15,480 – –

Costs incurred in third-party properties 8 280 2,783 – –

18,134 24,532 – –

Financial non-current assets

Participating interests in Group companies – – 21 11,579 11,579

Deferred tax claims 14 6,458 5,441 – –

Other long-term receivables 16 11,635 11,085 – –

18,093 16,526 11,579 11,579

TOTAL NON-CURRENT ASSETS 104,739 133,297 11,579 11,579

CURRENT ASSETS

Current receivables

Receivables from group companies – – 14,055 14,630

Customer accounts receivable 12,696 13,732 – –

Tax claims – 3,299 – 2

Other receivables 155 152 3 3

Prepaid expenses and accrued income 13 150,678 161,499 – –

163,529 178,682 14,058 14,635

Cash and bank 17 159,301 62,381 17 1,963 1,376

TOTAL CURRENT ASSETS 322,830 241,063 16,021 16,011

TOTAL ASSETS 427,569 374,360 27,600 27,590

Balance Sheet (SEK thousands)

25BALANCE SHEET

Group Parent Company

Note 31/12/2015 31/12/2014 Note 31/12/2015 31/12/2014

EQUITY AND LIABILITIES 1

EQUITY 2

Share capital 100 100 100 100

Restricted reserves 70,548 70,548 – –

Non-restricted reserves 193,799 181,186 15,774 15,767

Contribution issue – – 11,679 11,679

Profit for the year 50,920 12,612 11 7

TOTAL EQUITY 315,367 264,446 27,564 27,553

Provisions

Provisions for pensions 5.15 11,635 11,085 – –

Provisions for deferred tax 14 1,060 1,060 – –

Total provisions 12,695 12,145 – –

Current liabilities

Supplier accounts payable 47,099 46,777 – –

Tax liabilities 4,830 – – –

Other liabilities 4,116 4,223 – –

Accrued expenses and deferred income 18 43,462 46,769 36 37

Total current liabilities 99,507 97,769 36 37

TOTAL EQUITY AND LIABILITIES 427,569 374,360 27,600 27,590

PLEDGED ASSETS 19 None None

Endowment insurance policies 11,635 11,085

CONTINGENT LIABILITIES 20 – – 20 – –

26

Equity Statement (SEK thousands)

EQUITY

Changes in equity Share capital Restricted reserves Non-restricted

reserves Total equity

GROUP

Equity at 31 December 2013 100 78,825 172,910 251,835

Transfer from non-restricted to restricted equity *) – –8,277 8,277 –

Profit for the year – – 12,612 12,612

Equity at 31 December 2014 100 70,548 193,799 264,447

Profit for the year – – 50,920 50,920

Equity at 31 December 2015 100 70,548 244,719 315,367

The share capital is composed of 100,000 shares with a par value of SEK 1 each.*) Equity's share of tax allocation reserve attributable to dissolution of tax allocation reserve for 2009.

PARENT COMPANY

Equity at 31 December 2013 100 11,679 15,767 27,546

Profit for the year – – 7 7

Equity at 31 December 2014 100 11,679 15,774 27,553

Profit for the year – – 11 11

Equity at 31 December 2015 100 11,679 15,785 27,564

The share capital is composed of 100,000 shares with a par value of SEK 1 each.

27

Cash Flow Statement (SEK thousands)

CASH FLOW STATEMENT

Group Parent Company

Note 2015 2014 Note 2015 2014

Current operations

Profit after financial items 65,747 16,579 –40 –620

Adjustment for non-cash items etc.

Impairment losses/depreciation 6, 7, 8, 9 36,590 39,434 – –

Capital gain upon sale/disposal of non-current assets – –82 – –

102,337 55,931 –40 –620

Paid income tax –7,715 –7,586 –3 –1

Cash flow from current operations before changes in working capital 94,622 48,345 –43 –621

Cash flow from changes in working capital

Decrease (+) / increase (–) in operating receivables 11,855 –6,621 630 67

Decrease (–) / increase (+) in operating liabilities –3,092 7,572 – –

CASH FLOW FROM CURRENT OPERATIONS 103,385 49,296 587 –554

Investment operations

Acquisition of intangible fixed assets 9 – –2,579 – –

Acquisition of property, plant and equipment 6, 7, 8 –6,465 –10,334 – –

Sale of property, plant and equipment – 84 – –

CASH FLOW FROM INVESTMENT OPERATIONS –6,465 –12,829 – –

CASH FLOW FOR THE YEAR 96,920 36,467 587 –554

LIQUID FUNDS AT BEGINNING OF THE YEAR 62,381 25,914 1,376 1,930

LIQUID FUNDS AT END OF THE YEAR 159,301 62,381 1,963 1,376

Interest received amounted to SEK 45 thousand (419) and interest paid amounted to SEK 3 thousand (530) (Group).Interest received amounted to SEK 0 thousand (15) and interest paid amounted to SEK 0 thousand (516) (Parent Company).

28 NOTES TO THE ACCOUNTS

NOTE 1 Accounting principlesThe annual report for BGC Holding AB has been prepared in accordance with the Swedish Annual Accounts Act and even in accordance with the Swedish Accounting Standards Board's general guidelines BFNAR 2012:1 Annual Accounts and Consolidated Accounts (K3).

BGC Holding AB pursues operations as a limited liability company and is domiciled in Stockholm, Sweden. The head office is located at Palmfeltsvägen 5, 105 19 Stockholm.

The accounting principles are unchanged compared to previous years. The Parent Company applies the same accounting principles as the Group. Non-current assets, long-term liabilities and provisions consist in all essentials entirely of amounts that are expected to be recovered or paid more than twelve months after the balance sheet date. Current assets and liabilities consist in all essentials entirely of amounts that are expected to be recovered or paid within twelve months of the balance sheet date.

Assets, provisions and liabilities have been valued at cost unless stated otherwise below.

Intangible fixed assetsIntangible fixed assets are only recognised when the asset is identifi-able, there is control over the asset and it is expected to be of future benefit. Development expenditure is only recognised as an asset on the condition that, in addition to the above-mentioned general require-ments being satisfied, the aim and assumption is for the asset to be used in the business, or sold, and that the value can be calculated in a reliable manner.

DepreciationDepreciation is applied linearly over the asset's estimated useful life.Depreciation is recognised as a cost in the income statement. The fol-lowing depreciation period is applied:

Intangible fixed assets are depreciated over the duration of the agreement or over 5 years.

For a more detailed description of capitalised expenditure, please refer to Note 9.

Property, plant and equipmentProperty, plant and equipment are recognised as assets in the balance sheet when, on the basis of the information available, it is likely that the future financial benefit that is linked to the holding will accrue to the company and the cost of the asset can be calculated in a reliable manner. Property, plant and equipment are reported at cost less depreciation and impairment losses.

Subsequent expenditureSubsequent expenditure that fulfils the asset criterion is included in the asset's carrying amount. Expenses for ongoing maintenance and repairs are recognised as costs when incurred.

DepreciationDepreciation according to plan is based on the original cost. Deprecia-tion is applied linearly over the asset's estimated useful life. Deprecia-tion is recognised as a cost in the income statement.

The following depreciation periods are applied:

Plant and machinery 5 years

Fixtures and fittings 3 to 5 years

Costs incurred in third-party properties are depreciated over the duration of the lease

Impairment losses – property, plant and equipment and intangible fixed assetsThe carrying amounts of the company’s assets are tested for impair-ment on each balance sheet date. If impairment losses have arisen, the asset's recoverable amount is calculated as the higher of the asset's value in use and net realisable value. An impairment loss is recognised if the recoverable amount is less than the carrying amount of an as-set. When assessing value in use, the estimated future cash flows are discounted to their present value using an interest rate that reflects current market assessments of the time value of money and the risks specific to the asset. An asset that is dependent on other assets is not regarded as generating any independent cash flows. Such assets are instead assigned to the smallest cash-generating unit where independ-ent cash flows can be established.

An impairment loss is reversed if there has been a change in the calculations used to determine the recoverable amount. An impairment loss is only reversed to the extent that the asset's carrying amount does not exceed the carrying amount that would have been determined, less depreciation, if no impairment loss had been recognised.

Leasing – lesseeAll leasing agreements have been classified in the consolidated ac-counts as finance or operating lease agreements. Finance leases trans-fer the bulk of the economic risks and rewards of ownership to the les-see. If that is not the case, the lease is classified as an operating lease.

Finance lease agreementsAssets leased under finance lease agreements are recognised as assets in the consolidated balance sheet. The obligation to pay future leasing fees is reported as long-term and current liabilities. The leased assets are systematically depreciated, while the leasing fees are recognised as interest and repayment of debts.

Operating lease agreementsLeasing fees under operating lease agreements, including increased initial leasing fees but excluding expenses for services such as insurance and maintenance, are recognised as costs linearly over the leasing period.

Financial assets and liabilitiesFinancial assets and liabilities are reported in accordance with Chapter 11 (Financial instruments valued at cost) of BFNAR 2012:1.

Recognition and derecognition in the balance sheetFinancial instruments recognised in the balance sheet comprise, among assets, liquid funds, customer accounts receivable and current invest-ments that are interest-bearing instruments. Supplier accounts pay-able are found under liabilities and equity.

Notes to the Accounts (SEK thousands)

29NOTES TO THE ACCOUNTS

A financial asset or financial liability is recognised in the balance sheet when the company becomes a party to the contractual provisions of the instrument. A financial asset is derecognised in the balance sheet when the contractual right to the cash flow from the asset has ceased or been settled. The same applies when the bulk of the risks and benefits associated with the holding are transferred to another party and the company no longer exerts control over the financial asset. A financial liability is derecognised in the balance sheet when the agreed obligation has been fulfilled or ceased.

Liquid fundsLiquid funds comprise cash balances and call deposits with banks. These items are generally valued at the accrued cost.

Financial investmentsCurrent investments have been recognised as current assets and hold-ings in interest-bearing instruments have been recognised at fair value (market value).

Customer accounts receivableCustomer accounts receivable are recognised at the amount expect-ed to be paid after deductions for bad debts assessed on a case-by-case basis. Customer accounts receivable are of short duration, which is why the value is recognised at the nominal amount without discounting.

Supplier accounts payableSupplier accounts payable are of short duration and are valued without discounting at the nominal amount.

Employee benefitsDefined contribution pensionsThe Group's obligation for each period consists of those amounts that the Group is obliged to contribute for the current period. Consequently, no actuarial assumptions are required in order to calculate the obliga-tion or cost, and there are no opportunities for any actuarial gains or losses. The obligation is calculated without discounting, except for in those cases where it does not fall due for payment in its entirety within twelve months following the end of the period during which the employ-ees carry out the related services.

TaxTax on the year's result in the income statement comprises current tax and deferred tax. Current tax is income tax for the current financial year on the taxable profit for the year and the share of the previous year's income tax that has not yet been reported.

Deferred tax liabilities are reported for all taxable temporary dif-ferences. Deferred tax claims are reported for deductible temporary differences and for the opportunity to in the future utilise fiscal net operating losses. The valuation is based on how the carrying amount of the equivalent asset or liability is expected to be recovered or settled. The amounts are based on the tax rates and tax regulations that are in force prior to the balance sheet date. Temporary differences have arisen as a result of provisions for pensions, as well as in relation to plant

and machinery. In the consolidated balance sheet untaxed reserves are divided between deferred tax and equity.

ProvisionsA provision is recognised in the balance sheet when the company has a legal or informal obligation resulting from a previous event and it is likely that an outflow of resources is required to settle the obligation and a reliable estimate of the amount can be made.

RevenueRevenue recognition is carried out in the income statement when it is likely that the future financial benefits will accrue to the company and these benefits can be calculated in a reliable manner. Transac-tion revenue is recognised concurrently with the services being used. Remuneration in the form of interest as a result of others' use of the company's assets is recognised as revenue when it is likely that the financial benefits that are linked with the transaction will accrue to the company and can be calculated in a reliable manner.

Consolidated financial statementsSubsidiariesSubsidiaries are companies in which the Parent Company, either direct-ly or indirectly, has more that 50 percent of the votes or in some other way has a controlling influence over the operational and financial man-agement of the company. Acquisitions of subsidiaries are normally re-ported in accordance with the purchase method. The purchase method means that the acquisition of a subsidiary is regarded as a transaction wherein the parent indirectly acquires the subsidiary's assets and as-sumes its liabilities. The acquired company's earnings and expenditure, identifiable assets and liabilities, and any goodwill or negative goodwill, are included in the consolidated financial statements as of the date of acquisition.

Elimination of transactions between group companiesIntragroup receivables and liabilities and transactions between compa-nies in the Group, as well as the related unrealised gains, are eliminated in their entirety. Unrealised losses are eliminated in the same way as unrealised gains, provided that there is no evidence of impairment.

Group contributionsGroup contributions that have been received/provided are reported as appropriations in the income statement. The received/provided group contribution has affected the company's current tax.

NOTE 2 EquityRestricted reservesValue transfer may not be carried out if after the change in value there is insufficient full coverage for the company's restricted equity.

Legal reserveThe purpose of the legal reserve is to reserve part of retained net profits to cover an accumulated deficit.

30 NOTES TO THE ACCOUNTS

Non-restricted reservesRetained earningsComprise the previous year's accumulated earnings, less any dividend distributed to the shareholders. Together with the year's earnings, constitutes total non-restricted equity, that is, the amount available for distribution to the shareholders.

The Board of Directors proposes that the accumulated earnings be used in part to pay a dividend of SEK 0 to the shareholders.

NOTE 3 Other operating income Group

2015 2014

Other operating income 708 2,698

Total 708 2,698

NOTE 4 KPMG AB Group Parent Company

2015 2014 2015 2014

Auditing assignments 358 375 31 31

Assignments other than auditing assignments 34 – – –

Tax consultation 50 50 5 5

Total 442 425 36 36

NOTE 5 EmployeesAll staff in the Group are employed by the subsidiary Bankgirocentralen BGC AB. The average number of employees by gender is as follows:

Group

2015 2014

Women 126 121

Men 104 105

Company total 230 226

Salaries and remuneration amounted to:

Board of Directors – –

CEO 3,944 3,577

(of which variable remuneration to CEO) (300) (400)

Other employees 128,039 124,754

131,983 128,331

Statutory social costs 41,944 40,157

Pension costs 46,215 45,053

(of which to Board of Directors) (–) (–)

(of which to CEO) (3,389) (1,443)

88,159 85,210

Total salaries, remuneration, social costs 220,142 213,541

Target incentive costs of SEK 3,338 thousand (2,866) are in addition to the salaries, remuneration and social costs in the table above. The CEO's pension costs amount to SEK 3,389 thousand (1,443), of which the special employer's contribution was SEK 662 thousand (282). The costs for both the former and the current CEO are included in these amounts.

SEK 7,181 thousand (6,755) of the salaries and remuneration dis-bursed to other employees in the Group relates to other senior execu-tives besides the CEO.

Agreement has been reached with the Chief Executive Officer re-garding severance pay amounting to 12 months. The CEO's pension commitment comprises a defined contribution pension plan (BTP1) and a direct pension, for which premiums are paid regularly throughout the employment period. The period of notice for the CEO is 12 months.

Agreement has been reached with other senior executives besides the CEO regarding severance pay amounting to a maximum of 12 months' pay. The period of notice for other senior executives is 6 months.

NOTE 6 Plant and machinery Group

2015 2014

Opening accumulated costs 30,650 29,464

Purchases – 1,308

Sales / disposals –129 –122

Closing accumulated costs 30,521 30,650

Opening accumulated depreciation –24,381 –22,153

Sales / disposals 129 122

Impairment losses / depreciation for the year –2,605 –2,350

Closing accumulated depreciation –26,857 –24,381

Closing net book value 3,664 6,269

31NOTES TO THE ACCOUNTS

NOTE 7 Fixtures and fittings Group

2015 2014

Opening accumulated costs 67,047 63,733

Purchases 6,465 8,569

Sales / disposals –504 –5,255

Closing accumulated costs 73,008 67,047

Opening accumulated depreciation –51,567 –50,036

Sales / disposals 504 5,151

Impairment losses / depreciation for the year –7,755 –6,682

Closing accumulated depreciation –58,818 –51,567

Closing net book value 14,190 15,480

NOTE 8 Costs incurred in third-party properties Group

2015 2014

Opening accumulated costs 15,897 15,440

Purchases – 457

Sales / disposals – –

Closing accumulated costs 15,897 15,897

Opening accumulated depreciation –13,114 –10,701

Sales / disposals – –

Impairment losses / depreciation for the year –2,503 –2,413

Closing accumulated depreciation –15,617 –13,114

Closing net book value 280 2,783

NOT 9 Capitalised expenditure for development work Group

2015 2014

Opening accumulated costs 209,658 207,079

Purchases – 2,579

Closing accumulated costs 209,658 209,658

Opening accumulated depreciation –117,419 –89,430

Sales / disposals – –

Impairment losses / depreciation for the year –23,727 –27,989

Closing accumulated depreciation –141,146 –117,419

Closing net book value 68,512 92,239

This asset comprises in part development costs for a platform that was commissioned in 2011 by VocaLink, and which in the accounts is treated as a finance lease, and in part a proprietary real-time platform that was commissioned in 2012.

The development costs for VocaLink are depreciated over the dura-tion of the agreement. The agreement runs until 2019. The development costs for the payments in real time platform have a depreciation period of 5 years, which means the costs will be fully depreciated in 2017.

NOTE 10 Lease agreementsLease agreements where the Group as lessee in all essentials enjoys the economic rewards and bears the economic risks attributable to the leasing asset are classified as finance leases and the asset is rec-ognised as an intangible fixed asset in the consolidated balance sheet. The corresponding obligation to pay future leasing fees is reported as a liability. At the beginning of the lease period the asset and liability are recognised at the lower of the leasing asset's fair value and the present value of the minimum lease fees.

In lease agreements where the economic rewards and risks attrib-utable to the leasing asset in all essentials remain with the lessor, the lease is classified as an operating lease. Payments in accordance with these agreements are charged on a straight-line basis over the terms of the lease.

In the subsidiary, all lease agreements are recognised as rental agreements (operating lease agreements), regardless of whether they are finance or operating leases. The leasing fee is charged on a straight-line basis over the term of the lease.

Finance lease agreementsThe Group's property, plant and equipment include leasing assets that are held in accordance with finance lease agreements according to the following:

Acquisition values

Accumulated impairment losses

/ depreciation

2015 2014 2015 2014

Intangible fixed assets 209,658 209,658 –141,146 –117,419

Operating lease agreementsLeasing expenditure relating to operating lease agreements attribut-able to property, plant and equipment amounted to SEK 5,328 thousand (9,960) for the year.

Remaining operating lease fees are due for payment as follows:

Group Parent Company

2015 2014 2015 2014

Due 2015 – 8,388 – –

Due 2016 2,336 62 – –

Due 2017 119 62 – –

Due 2018 109 – – –

32 NOTES TO THE ACCOUNTS

NOTE 11 Interest income, interest expenses and similar items

Group

2015 2014

Interest income and similar items 45 419

Total 45 419

Interest expenses and similar items –237 –758

Total –237 –758

NOTE 12 Tax for the year Group Parent Company

2015 2014 2015 2014

Current tax for the year –15,844 –6,539 –4 –3

Deferred tax 1,017 2,572 – –

Total –14,827 –3,967 –4 –3

Difference between Group's tax expense and tax expense based on current tax rate

Group Parent Company

2015 2014 2015 2014

Result before tax 65,747 16,579 15 10

Tax according to current tax rate –14,464 –3,647 –3 –2

Business entertainment –217 –172 – –

Association fees –56 –44 – –

Miscellaneous –83 –52 –1 –1

Standard income pension fund –7 –51 – –

Interest income – 1 – –

Interest expenses – –2 – –

Tax for the year according to income statement –14,827 –3,967 –4 –3

NOT 13 Prepaid expenses and accrued income Group

2015 2014

Accrued income 116,544 91,271

Prepaid expenses, lease, rental and licensing agreements 22,345 21,143

Other prepaid expenses 11,789 49,086

Total 150,678 161,499

NOT 14 Deferred tax Group

Deferred tax claims 2015 2014

Opening deferred tax claims 5,441 5,204

Change in deferred tax related to pension provisions 150 132

Change in deferred tax related to fiscal depreciation 867 105

Closing deferred tax claims 6,458 5,441

Deferred tax liability

Opening deferred tax liabilities 1,060 3,395

Change in deferred tax in untaxed reserves – –2,335

Closing deferred tax liabilities 1,060 1,060

NOT 15 Pension provisions Group

2015 2014

Opening balance 11,085 10,603

Liabilities calculated according to local principles 550 482

Total 11,635 11,085

Pension insurance BTP planThe retirement pensions and family pensions for workers in Sweden, the BTP plan, are covered via insurance with SPP (BTP2). The pension plan is a defined benefit plan, which covers several employers. The Group has not had access to information for the 2015 and 2016 financial years that would facilitate the reporting of this plan as a defined benefit plan. The pension plan is therefore reported as a defined contribution plan. SPP's surplus may be distributed to the members of the plan and/or to the plan participants. Since 1 January 2006, SPP has been reorganised into a profit distributing life insurance company and there-fore no longer discloses a collective consolidation ratio. Instead, the insurance capital is disclosed for each employer at agreement level. As of 2013 new employees are instead included in the defined contribution pension plan BTP1.

33NOTES TO THE ACCOUNTS

Liabilities calculated according to local principlesThe net amount is recognised in the following items in the consolidated balance sheet:

Group

2015 2014