annual report project on muthoot finance ltd

DESCRIPTION

Report for the year 2013-14TRANSCRIPT

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

ABSTRACT

The project – REVIEWING PUBLISHED CORPORATE ANNUAL REPORT OF

MUTHOOT FINANCE.

An Annual Report is a comprehensive report on a company's activities throughout the

preceding year. Annual reports are intended to give information about the company's

activities and financial performance. Most jurisdictions require companies to prepare and

disclose annual reports, and many require the annual report to be filed at the company's

registry.

The responsibility of Muthoot Finance is to conduct the audit in accordance with the

Standards on Auditing issued by the Institute of Chartered Accountants of India.

The first step of this project is to understand how company prepare all the essential report

whole year and then submit annual report. To take an in depth knowledge of Financial

Report, Accounting Policies, Annual Reports and different forms of reporting.

The second step of this project is to understand and review the Annual Report made by

company which notify the Financial Report, Accounting Policies and reports of all the

transaction took place in the whole year. The details provided in the report are of use to

investors and other interested person to understand the company's financial position and

future direction.

The final step of this project is to suggest measures to make this whole process more

effective, less time consuming and error proof.

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

EXECUTIVE SUMMARY

Muthoot Finance was founded by M George Muthoot in 1939.Muthoot Finance to enter

capital market through IPO route - Economic Times. The company has been licensed by

Reserve Bank of India under Section 45 I (a) of the RBI Act, 1934 to function as a Non-

banking financial company (NBFC) without accepting public deposits and is specifically

exempted from the provisions of the Money Lenders Act in Karnataka and other states. The

company's gold loan business constitutes more than 99 percent of its total income.

Muthoot Finance was originally incorporated as a private limited company on March 14,

1997 with the name “The Muthoot Finance Private Limited” under the Companies Act.

Subsequently, by fresh certificate of incorporation dated May 16, 2007, its name was

changed to “Muthoot Finance Private Limited”. The company was converted into a public

limited company on November 18, 2008 with the name “Muthoot Finance Limited” and

received a fresh certificate of incorporation consequent upon change in status on December

02, 2008 from the RoC.

Muthoot Finance Ltd. is an Indian financial corporation. It is known as the largest gold

financing company in the world. In addition to financing gold transactions, the company

offers foreign exchange services, money transfers, wealth management services, travel and

tourism services, and sells gold coins at Muthoot Finance Branches. The company's

headquarters are located in Kerala, India, and operates over 4,400 branches throughout the

country. Outside India, Muthoot Finance is established in the UK, US, and United Arab

Emirates. While the company falls under the brand umbrella of the Muthoot Group, its stocks

are listed on BSE and NSE. The target market of Muthoot Finance includes small

businesses, vendors, farmers, traders, SME business owners, and salaried individuals.

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

OBJECTIVE OF STUDY

An annual report is a comprehensive report on a company's activities and financial

performance throughout the preceding year.

Thus the detailed study on Annual Report is being carried out with the following objectives:

1. To understand how to read, analyze, and create financial statements to get a full and

accurate understanding how much money there is, how much debt is owed, the

income coming in each month, and the expenses going out the door.

2. To know how well the company is doing. Is company earnings higher, lower or the

same as the year before? How are sales doing? These numbers should be presented

clearly in the financial section of the annual report.

3. To find out whether the company is making more money than it is spending. How

does the balance sheet look? Are assets higher or lower than the year before? Is debt

growing, shrinking, or about the same as the year before?

4. To get an idea of management’s strategic plan for the coming year. How

will management build on the company’s success? This plan is usually covered in the

beginning of the annual report — frequently in the letter from the chairman of the

board.

5. To find out where the company has been, where it is now, and where it’s going.

LIMITATIONS OF THE STUDY

Despite of all the efforts to make the analysis more comprehensive and scientific, a study

of present kind is bound to have certain limitations. Attempts have been made to provide

more comprehensive conceptual analysis.

1. The study is only limited to the information published and available by the

company.

2. The study is limited to the financial area of Annual Report.

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

SCOPE OF THE STUDYThe study is limited based on data published by the company’s financial statements.

The data has been collected for the financial year 2013-14 and has been analysed using pictorial diagrams like graph, bar and columns charts etc.

The data has been collected from secondary sources.

RESEARCH METHODOLOGY

In order to fulfil the objectives of the study the data can be collected from two sources of data

–

Primary Data Secondary Data

SOURCES OF DATA :

Primary Data

The primary data of the topic is collected by personal interaction with the officials of the

finance and accounting department .For this project secondary data was used for collecting

data.

Secondary data

For gathering secondary data various other sources were used, which are –

1. Different accounting records of the company.

2. Magazines and journals

3. Annual Reports

4. Company website

5. Internet and web searching

6. Company databases

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

CONTENTS

SR.NO PARTICULARS PAGE NO.

CHAPTER - IINTRODUCTION OF PUBLISHED CORPORATE ANNUAL REPORT

1 - 12

CHAPTER – II MUTHOOT FINANCE LTD 13 - 14

Introduction of Muthoot Finance Ltd 13

CHAPTER - IIIFinancial Statements of Muthoot Finance Ltd for the year ended March, 2014

15 - 18

Balance Sheet 15

Profit and Loss Statement 16

Cash Flow Statement 17

CHAPTER - IV DATA ANALYSIS AND INTERPRETATION 19 - 32

Management Discussion and Analysis 19

Notes to Accounts 27

Interpretation to Financial Statements 30

CHAPTER - V CONCLUSION 33

BIBLIOGROPHY 34

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

CHAPTER - I

INTRODUCTION

Today reporting by companies has to assume a high level of importance. Formerly annual

reports used to be less revealing and reporting was not timely and we not catering to

requirement of various shareholder. More was concealed than what was revealed. But today

thanks to investor awareness global standards used the effective functioning of regulatory

bodies corporate reporting has become more revealing.

ESSENTIALS OF FINANCIAL REPORTS

1) Relevance

Means selecting the information most likely to aid users in their economic decisions.

2) Understandibility

which implies not only that the selected information must be intelligible but also that

the users can understand it.

3) Verifiability

which implies that the accounting results may be corn borated by independent

measurers using the same measurement methods.

4) Neutrality

which implies that the accounting information is directed towards the common needs

of users rather than the particulars needs of specific users.

5) Timeliness

which implies an early communication of information to avoid delays in economic

decision-making.

6) Comparability

which implies that differences should not be the result of different financial accounting

treatments.

7) Completeness

Which implies that all the information that ‘reasonably’ fulfils the requirements of other

qualitative objectives should be reported.

1

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

DEVELOPMENTS OF FINANCIAL REPORTING OBJECTIVE

. These objectives may be summarized as follows:

1. The particular objectives of financial statements are to present fairly, and in conformity

with generally accepted accounting principles, financial position, results of operations,

and other changes in financial position.

2. To provide reliable information about economic resources and obligations a business

enterprise in order-

(i) Evaluate its strengths and weakness.

(ii) Show its financing and investment.

(iii) Evaluate its ability to meet its commitments and

(iv)Show its resources base for growth.

3. To provide reliable information about changes in net resources resulting from a

business enterprise’s profit- directed activities in order

(i) Show investors expected dividend return

(ii) Show operation’s ability to pay creditors and suppliers, provide jobs for employees

pay taxes, and generate funds for expansion.

(iii) Provide management with information for planning and control and

(iv)Show its long-term profitability.

4. To provide financial information useful for estimating the earning potential of the firm.

5. To serve users who have limited authority.

6. To provide other needed information about changes in economic resources and

obligations.

7. To disclose other information relevant to statement user’s needs.

8. To provide a statement of earnings for predicting future performance.

9. To provide information required for decision making

10.To educate public about the company`s mission and goals.

2

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

ANNUAL REPORT

There are different ways of corporate reporting of which the most important is the published

Annual Report sent to the shareholders. An annual report is a comprehensive report on

company's activities throughout the preceding year. Annual reports are intended to

give shareholders and other interested people information about the company's activities

and financial performance. Annual Report is a mandatory part of reporting. Most jurisdictions

require companies to prepare and disclose annual reports, and many require the annual

report to be filed at the company's registry.

IMPORTANCE OF ANNUAL REPORT

i. It gives an opportunity to take a step back and look at the overall practical and

financial health of your business.

ii. You can know how well the company is doing.

iii. You can find out whether the company is making more money than it is spending

iv. You can get an idea of management`s strategic plan for the coming year.

Annual Report is statutory financial statements include profit & loss and balance

sheet in vertical form. It is accompanied by various schedules and notes to the accounts.

Other information deemed relevant to stakeholders may be included, such as a report on

operations for manufacturing firms or corporate social responsibility reports for companies

with environmentally or socially sensitive operations. The details provided in the report are of

use to investors to understand the company's financial position and future direction. The

financial statements are usually compiled in compliance with IFRS and/or the

domestic GAAP, as well as domestic legislation.

The information largely reflects the financial effects of transactions and events that have

already happened. Financial reporting is expected to provide information about an

enterprise’s financial performance during a period and about how management of an

enterprise has discharged its stewardship responsibility to owners. Management is also

interested in the information contained in the financial information that helps it carry out its

planning, decision-making and control responsibilities. Management has the ability to

determine the form and content of such additional information order to meet its own needs.

Published financial statements are based on the information used by management about the

financial position, performance and changes in financial position of the enterprise.

3

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

CONTENTS OF ANNUAL REPORT

1. STATUTORY :

a. Profit & Loss A/c

b. Balance Sheet

c. Director`s Report

d. Auditor`s Report

e. Notes to Accounts

2. ACCOUNTING STANDARDS :

f. Disclosure of accounting policies (AS 1)

g. Cash flow statement (AS 3)

h. Consolidated financial statements (AS 21)

i. Segment reporting (AS 17)

j. Related party Disclosures (AS 18)

3. LISTING REQUIREMENTS :

k. Cash flow statement

l. Management Discussion and Analysis

m. Report on corporate Governance

4. EXTENDED REPORTING :

n. Chairman`s speech

o. Financial highlights

p. Ten year`s summary

q. Value Added statement

r. Shareholder`s Information

s. Segment Reporting

t. Human Resource Accounting

u. Inflation Adjusted Accounts

v. Social Reporting

w. Important Ratios

x. Economic Value Added

y. Shareholder`s reference

z. Risk Management

4

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Annual Report and Accounts - Contents

Contents: non-audited information

Narrative items

– Chairmen’s statement

– Directors’ report

– Operating and financial review

– Review of operations

– Statement of corporate governance

– Auditors report

– Statement of directors’ responsibilities for the financial statements

– Shareholder information

• Non-narrative

– Highlights

– Historical summary

– Shareholder analysis

Balance sheet

• A balance sheet is a statement of the resources owned and controlled by a business at a

single point in time.

• It gives a snapshot of assets, liabilities and capital at a point in time.

• It provides information about the company’s funds and how they are used in the business.

Profit and loss account

• The Profit and Loss Account is a statement which shows total business revenue less

expenses.

• The P&L account quantifies and explains the gains or losses of the company over the

period of time bounded by two balance sheets

• It provides a summary of the year’s trading activities:

– Revenue from sales (turnover)

– Business costs

– Profit or (loss)

– How the profit was used.

5

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Cash flow statement

• This is a statement which shows the flow of cash into and out of the business.

• It is not the same as a profit and loss account.

• The cash flow statement only records movements of cash and, for example, does not

include credit sales or purchases until such time as cash actually flows.

• This statement became mandatory because of some high profile business failures of the

1980s/90s - these were companies that, in terms of the P&L, were profitable but were short

of cash to pay their debts.

• The cash flow statement should not be confused with a cash flow forecast. The former is

historical whereas the latter is a forecast about the future.

Statement of total recognised gains and losses

• The STRGL is a financial statement which attempts to highlight all shareholder gains and

losses and not just those from trading.

• It is a summary of all the profits and losses made during the year.

• It is necessary because not all gains and losses are shown on the P and L account.

• Example: upward revaluation of a fixed asset is not classed as revenue from trading

operations and so it will not shown up on the P and L Account. It does show up as an

addition to revaluation reserves on the balance sheet.

Certification of the annual report

A company’s annual report must be provided with a certification that it is a true copy of the

original document. Read more on the page Certification of annual reports, see the menu.

Notes to the accounts

• Provides a more detailed analysis of some of the entries in the accounts

• Disclosure of accounting policies used (e.g. depreciation) and any changes to these

policies.

• An explanation for any deviation from accounting standards.

• Sources of turnover from different geographical areas.

• Details of fixed assets, investments, share capital, debentures and reserves.

•Directors emoluments (how much the Directors earned)

• Earnings per share.

6

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Accounting policies

• Companies must describe the accounting policies they use in preparing financial

statements.

• Companies have a choice of accounting policies in many areas such as foreign currencies,

goodwill, pensions, sales and stocks.

• As different accounting policies will result in different figures it is necessary to state the

policy that was used so that readers of the accounts can make an informed judgement about

performance.

• It is also important to state the effect of any changes in accounting policies – restating prior

year numbers where this is materially significant.

Chairpersons statement

• An overview of the trading year.

• A personalise overview of the company’s performance over the past year.

• Usually covers strategy, financial performance and future prospects.

Directors’ Report

• Its principal objective is to supplement the financial information with other information

consider necessary for a full appreciation of the companies activities. It includes:

• A description of the principal activities of the company.

• A fair review of the current and future prospects of the business.

• Information on the sale, purchase or valuation of assets.

• Recommended dividends.

• Employee statistics.

• Names of directors and their interests.

• Details of political or charitable donations.

Operating and financial review

• This is a statement in the annual report which provides a formalised, structured explanation

of financial performance.

• The operating review covers items such as operating results, profit and dividend.

• The financial review discusses items such as capital structure and treasury policy.

Operating and financial review

7

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Operating review

• New product development

• Details of shareholders returns

• Risks and uncertainties

• Future investment

• Sensitivity of financial results to specific accounting policies.

Financial review

• Current cash position.

• Sources of finding.

• Treasury policy.

• Capital structure.

• Confirmation of the business as a going concern.

• Factors outside the balance sheet impacting on the value of the business.

• Taxation.

Other features

• Highlights

– An “at a glance” summary of selected figures and ratios.

• Historical summary

– Five years of selected data from the balance sheet and profit and loss account

– Tables and graphs to illustrate trend and comparison of turnover, profit, dividend and

earnings per share.

• Shareholder analysis

– Detailed analysis of the shareholders, for example by size of shareholding.

Auditors report

• Auditors are independent accountants who are registered to carry out this work.

• They also have to certify that the accounts are drawn up in accordance with the

requirements of the Companies Act.

• Auditors must make a brief report to confirm that the accounts give a true and fair view of

the firm’s financial position.

8

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Shareholder`s fund and policy holder`s fund

•Shareholder`s fund are usually the shares in the company, any share issue premium,

retained profits and possibly other reserved that have been accumulated.

•Policy holder`s fund represents customer deposit plus interest credited at current rates.

CAG Report

CAG Report shows all receipts and expenditure of the government of India and the state

government.

Report of board of directors to member

Board of directors issue a report quarterly, half yearly and annually giving details about the

companies, policies, programs and formulating strategies about the company to members

Annual general meeting

Gathering of the directors and stockholders of every incorporated firm required.

Management report

Management report is the statement made by management and it is used to compare the

actual results achieved with the budgeted forecast levels. This report helps the management

to see where they went wrong and they apply measures to improve it.

Segment reporting schedule

In an annual report the purpose of business segment reporting is to provide an accurate

picture of a public company`s performance to its shareholder`s. For upper management,

business segment reporting is used to evaluate each segment`s income, expenses, assets,

liabilities and so on in order to assess profitability and riskiness.

9

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

NOTES TO ACCOUNTS

Financial Statements are prepared as per historical cost convention on accrual basis of

accounting. These statements comply with the companies Act 1956 and the Accounting

Standards issued by the ICAI. The significant Accounting Policies are about the following:

1. Fixed assets depreciation and amortisation

2. Investments

3. Inventories

4. Provision for doubtful debts/advances

5. Foreign currency transactions

6. Revenue Recognition

7. Retirement benefits

8. R & D

9. Excise / Custom duty

10. Income tax

11.Borrowing cost

12.Provision for current and Deferred Tax

13.Premium on Redemption of Debentures.

NOTES TO ACCOUNTS

Annual Report of every company must contain notes to accounts due to the following

1. Financial statements are prepared in vertical format in abridged form.

2. Notes to Accounts give the contents of every item in the financial statements.

3. Notes to Accounts explain the policies of the company.

4. Notes to Accounts bring out the effect of change in method of accounting on profits of

the company.

5. Details of the changes in policies are disclosed through notes.

6. The reader can interpret the financial statements with the help of Notes to Accounts.

7. Notes to Accounts explain about the compliance of SEBI Guidelines, RBI Guidelines,

Accounting Standards etc.

8. Notes to Accounts throw light on the methods/procedure of accounting followed by the

organisation.

10

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Significant Accounting Policies in Financial Statements

Significant Accounting Policies are specific accounting principles and methods a

company employs and considers to be the most appropriate to use in current circumstances

in order to fairly present its financial statements. The disclosure of Accounting Policies helps

users of financial statements (e.g., investors, creditors, vendors) to understand how

particular accounting principles were used in preparing the company’s financial statements.

Description of significant accounting policies also helps in comparing financial statements of

different companies.

Disclosure of significant accounting policies should be done in the following situations:

A selection of existing acceptable alternatives.

Principles and methods that are specific in a particular industry in which the company operates.

Unusual or innovative application of GAAP.

Some areas for which significant accounting policies can be disclosed in financial statements are presented below:

Basis of consolidation Accounts receivables and determination of allowance for bad debts Advertising costs Cash and cash equivalents Changes in accounting policies Deferred income taxes Derivatives and hedging activities Fair value elections, methods, assumptions, inputs used Fiscal year (52-53 week year) Foreign currency translation Goodwill Impairment of long-lived assets, goodwill, other intangibles, investments, etc. Intangible assets Interest capitalization Internal-use software Inventories and their pricing (FIFO, LIFO, Weighted-average, etc.) Nature of operations Operating cycle Pension and other postretirement or postemployment plans Property and equipment and related depreciation and amortization Reclassifications Research and development costs and their basis of amortization Revenue recognition Stock-based compensation

11

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Shipping and handling costs Start-up costs Use of estimates Warranties

Companies normally present significant accounting policies in a separate note to financial

statements or in a separate summary of significant accounting policies preceding the notes

to financial statements.

RATIO TO ANALYSE FINANCIAL STATEMENT

Annual reports contain information about financial highlights and the key indicators. The key

ratios are given for the last 10 years. These ratios help to interpret financial position of the

company. The analyst should draw conclusion about the following from the reported ratios:

1. Liquidity Position With the help of ratio conclusions can be drawn about liquidity position of a company.

Liquidity is the ability of a company to meet its current obligations when they become

due. A firm is said to have food liquidity position when it has sufficient liquid assets to

meet the current obligations.

2. Long term Solvency

Ratio analysis is useful for assessing the long term financial position of a company.

The position can judged from capital structure ratio, debt equity ratio and proprietary

ratio.

3. Operating efficiency

Operating efficiency of the management is judged from operating ratio, net operating

profit ratio, inventory turnover, debt collection etc.

4. Overall Profitability

It is the ability of the company to generate adequate income so that the shareholders

can be rewarded adequately. This is judged from return on investment, return on

equity capital, E.P.S etc.

5. Utilisation of resources

The management efficiency in utilization of resources can be judged from assets

turnover ratios, return on investment etc.

12

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

CHAPTER - II

MUTHOOT FINANCE LIMITED

Muthoot Finance was founded by M George Muthoot in 1939.Muthoot Finance to enter

capital market through IPO route - Economic Times. The company has been licensed by

Reserve Bank of India under Section 45 I (a) of the RBI Act, 1934 to function as a Non-

banking financial company (NBFC) without accepting public deposits and is specifically

exempted from the provisions of the Money Lenders Act in Karnataka and other states. The

company's gold loan business constitutes more than 99 percent of its total income. Its retail

loan assets stand at Rs. 23,763 Crs. the total number of shares of Muthoot Finance held by

Individuals/Hindu Undivided Family stood at 80.12 percent and the public shareholdings from

Mutual Funds/UTI totalled 3.52 percent.

Muthoot finance is a flagship company of the Muthoot Group based in Southern India.

Company was formed with a vision of “creating an organization capable of serving the

versatile need of the growing Indian financial market” the focus of the company is on

creating liquidity with an asset class, namely gold that has the largest consumer market.

Muthoot Finance Ltd (MFL), incorporated in 1997, is the Kerala based largest gold financing

company in India in terms of loan portfolio. The company offers gold loan to individuals like

small businessmen, vendors, traders, and salaried individuals who cannot access formal

credit for reasons like lack of credit history, documentation, accessibility. They have

deployed 25000 people in over 4400 branches spread over 21 states and 4 union Territories.

Muthoot finance is a major market player dedicated to make a positive impact on countless

people ranging from farmers to salaried employees seeking financial aid. The target market

of Muthoot Finance includes small businesses, vendors, farmers, traders, SME business

owners, and salaried individuals.

Muthoot finance India Ltd has 4,270 branches across 26 states and Union Territories,

75% Promoter shareholding in the company

5 lakhs + Debenture holders in the company

5 Millions + Customers

75 years unblemished track records

13

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

PRODUCT AND SERVICES OF THE MUTHOOT FINANCE

1. GOLD LOAN

India`s largest gold loan service provider, safeguard the deposit of gold is primary

concern. Gold loan range starts from Rs.1500 to Rs. 1 Crore.

2. GOLD COIN

Muthoot finance help to invest in the most powerful asset, which is gold it is also a

leading Silver and Gold Coins provider in India.

3. M POWER CARD

Ticket to heavy discounts, rebates and interesting services that add value to

members. M Power Card is a CRM Service provided by Muthoot Finance.

4. MONEY TRANSFER

Mothoot Money Transfer makes it possible to Receive and Send money within a blink

of an eye.

5. FOREIGN TRANSFER

Muthoot Exchange brings you hassle-free currency exchange services that are

provided at competitive rates.

6. TRAVELSMART

Muthoot finance provides flexible and customized travel insurance and foreign

exchange alongside travel packages and tour arrangements.

7. WEALTH MANAGEMENT SERVICE

Wealth Management is classified into 4 step process comprising risk evaluation, client

evaluation, value analysis and consultancy.

8. ATM

Muthoot finance aims to expand the number of ATMs reach to Tier III to Tier VI cities

as well, as part of financial inclusion.

In 2013 it obtains RBI License to start operating 9,000 White Label ATMs.

14

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

CHAPTER – III

FINANCIAL STATEMENTS OF MUTHOOT FINANCE LTD FOR THE

YEAR ENDED MARCH 2014

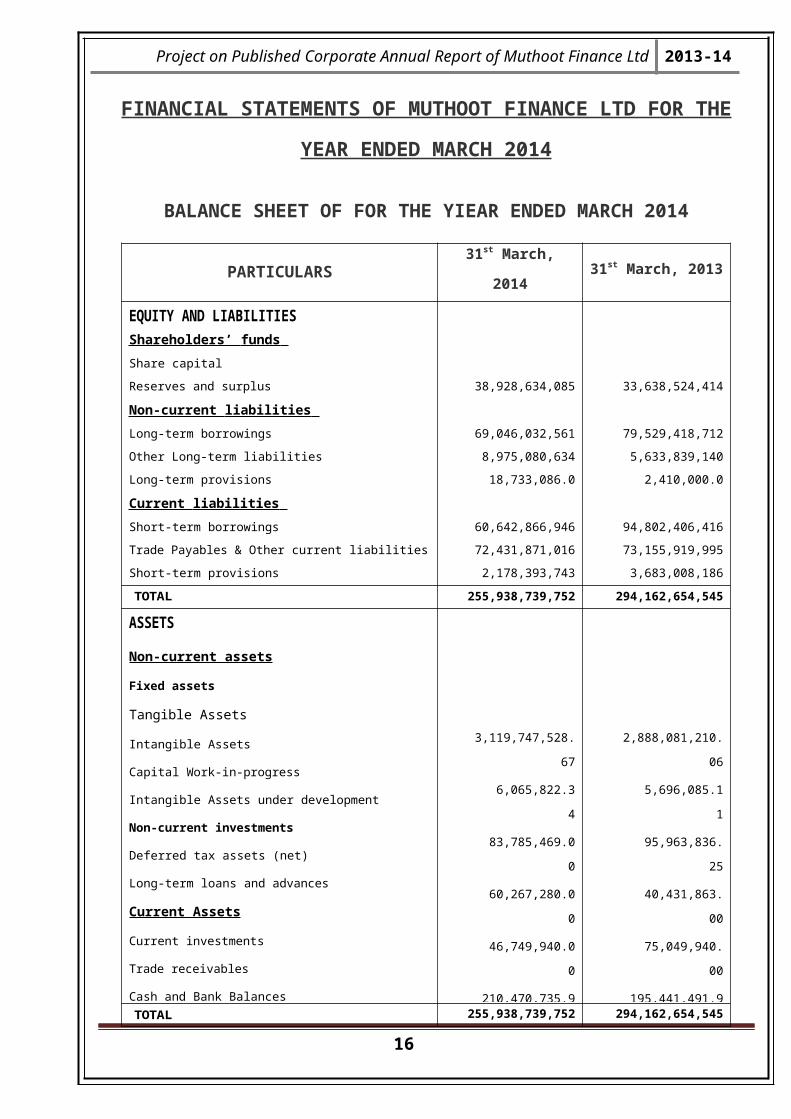

BALANCE SHEET OF FOR THE YIEAR ENDED MARCH 2014

15

PARTICULARS 31st March, 2014 31st March, 2013

EQUITY AND LIABILITIES

3,717,127,680.00 3,717,127,680.00

Shareholders’ funds

Share capital

Reserves and surplus 38,928,634,085.04 33,638,524,414.26

Non-current liabilities

Long-term borrowings 69,046,032,561.10 79,529,418,712.87

Other Long-term liabilities 8,975,080,634.76 5,633,839,140.60

Long-term provisions 18,733,086.00 2,410,000.00

Current liabilities

Short-term borrowings 60,642,866,946.00 94,802,406,416.23

Trade Payables & Other current liabilities 72,431,871,016.08 73,155,919,995.26

Short-term provisions 2,178,393,743.91 3,683,008,186.58

TOTAL 255,938,739,752.89 294,162,654,545.80

ASSETS

Non-current assets

Fixed assets

Tangible Assets

Intangible Assets

Capital Work-in-progress

Intangible Assets under development

Non-current investments

Deferred tax assets (net)

Long-term loans and advances

Current Assets

Current investments

Trade receivables

Cash and Bank Balances

Short-term loans and advances

Other current assets

3,119,747,528.67

6,065,822.34

83,785,469.00

60,267,280.00

46,749,940.00

210,470,735.90

1,019,451,594.24

307,000,000.00

11,639,680,421.27

20,489,267,554.30

218,944,896,078.16

11,357,329.01

2,888,081,210.06

5,696,085.11

95,963,836.25

40,431,863.00

75,049,940.00

195,441,491.90

1,045,225,440.06

750,000,000.00

11,481,770,359.45

13,419,987,682.79

264,131,088,154.70

33,918,482.48

TOTAL 255,938,739,752.89 294,162,654,545.80

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

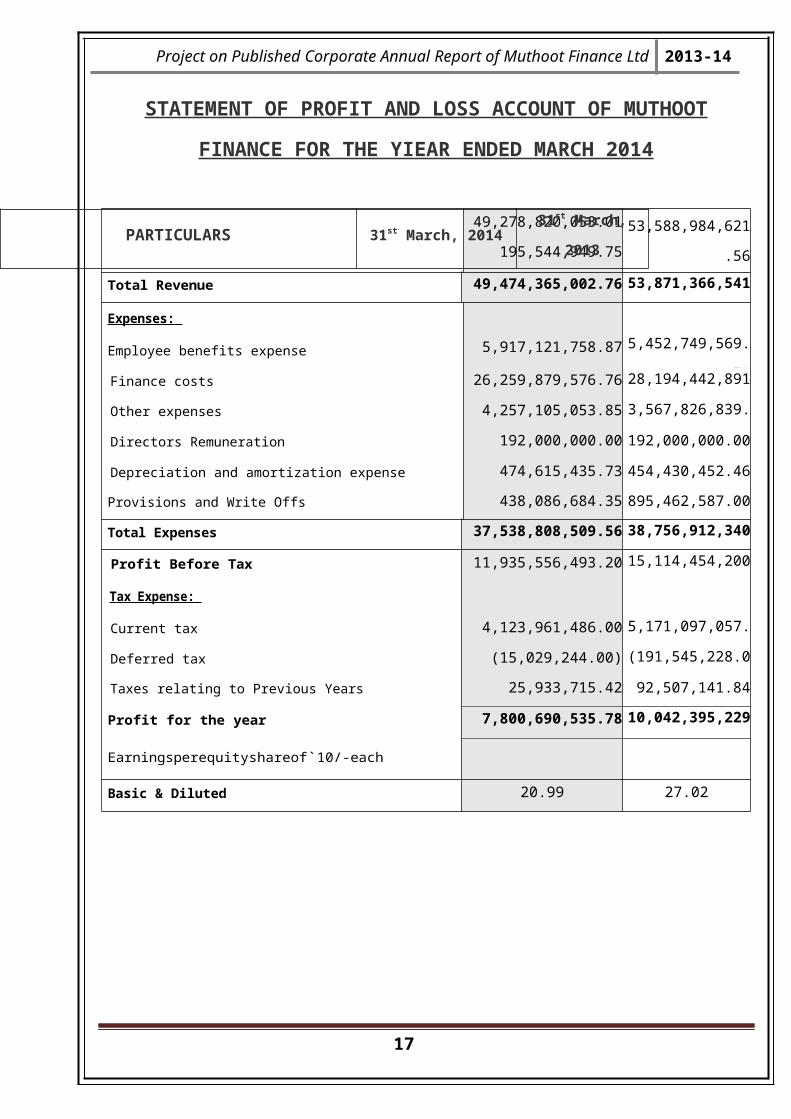

STATEMENT OF PROFIT AND LOSS ACCOUNT OF MUTHOOT

FINANCE FOR THE YIEAR ENDED MARCH 2014

Revenue from Operations

49,278,820,053.01

195,544,949.75

53,588,984,621.56

282,381,919.53

Total Revenue 49,474,365,002.76 53,871,366,541.09

Expenses:

5,917,121,758.87 5,452,749,569.71Employee benefits expense

Finance costs 26,259,879,576.76 28,194,442,891.99

Other expenses 4,257,105,053.85 3,567,826,839.56

Directors Remuneration 192,000,000.00 192,000,000.00

Depreciation and amortization expense 474,615,435.73 454,430,452.46

Provisions and Write Offs 438,086,684.35 895,462,587.00

Total Expenses 37,538,808,509.56 38,756,912,340.72

Profit Before Tax 11,935,556,493.20 15,114,454,200.37

T a x E xpense:

Current tax 4,123,961,486.00 5,171,097,057.00

Deferred tax (15,029,244.00) (191,545,228.00)

Taxes relating to Previous Years 25,933,715.42 92,507,141.84

Profit for the year 7,800,690,535.78 10,042,395,229.53

Earningsperequityshareof`10/-each

Basic & Diluted 20.99 27.02

CASH FLOW STATEMENT FOR THE YIEAR ENDED MARCH 2014

16

PARTICULARS 31st March, 2014 31st March, 2013

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

A Cash Flow From Operating ActivitiesNet Profit Before Taxation 11,935,556,493.20 15,114,454,200.37

Adjustments for:

213,948,607.00 765,190,034.00Add: Provision for Non- Performing Assets and

Standard assetsAdd: Finance Cost 26,259,879,576.76 28,194,442,891.99

Add: Loss on Sale of Fixed Assets 80,760.00 213,367.00

Add: Depreciation and amortization 474,615,435.73 454,430,452.46

Add: Provision for Gratuity 18,733,086.00 2,410,000.00

Add :Expenses on ESOP 98,731,243.00 -

Less: Interest received on Bank Deposits (70,993,542.80) (195,639,653.95)

Less: Income from Investments (85,776,381.95) (85,698,393.58)

Less: Profit on sale of Investments (37,950,000.00) -

Operating profit before working capital changes 38,806,825,276.94 44,249,802,898.29

Adjustments for:

45,211,965,922.36 (50,477,390,792.72)(Increase) / Decrease in Loans and Advances

(Increase) / Decrease in Trade receivables (157,910,061.82) (4,141,538,546.09)

(Increase) / Decrease in other receivables - 521,805.60

Increase / (Decrease) in Current liabilities 153,937,363.67 -23,712,913.76

Increase / (Decrease) in Other Liabilities (1,852,892.26) 5,486,267.30

Cash generated from operations 84,012,965,608.89 (10,386,831,281.38)

Finance cost paid (22,391,757,790.41) (23,828,995,205.26)

Direct tax paid (4,359,281,173.09) (5,308,549,132.10)

Net cash from operating activities 57,261,926,645.39 (39,524,375,618.74)

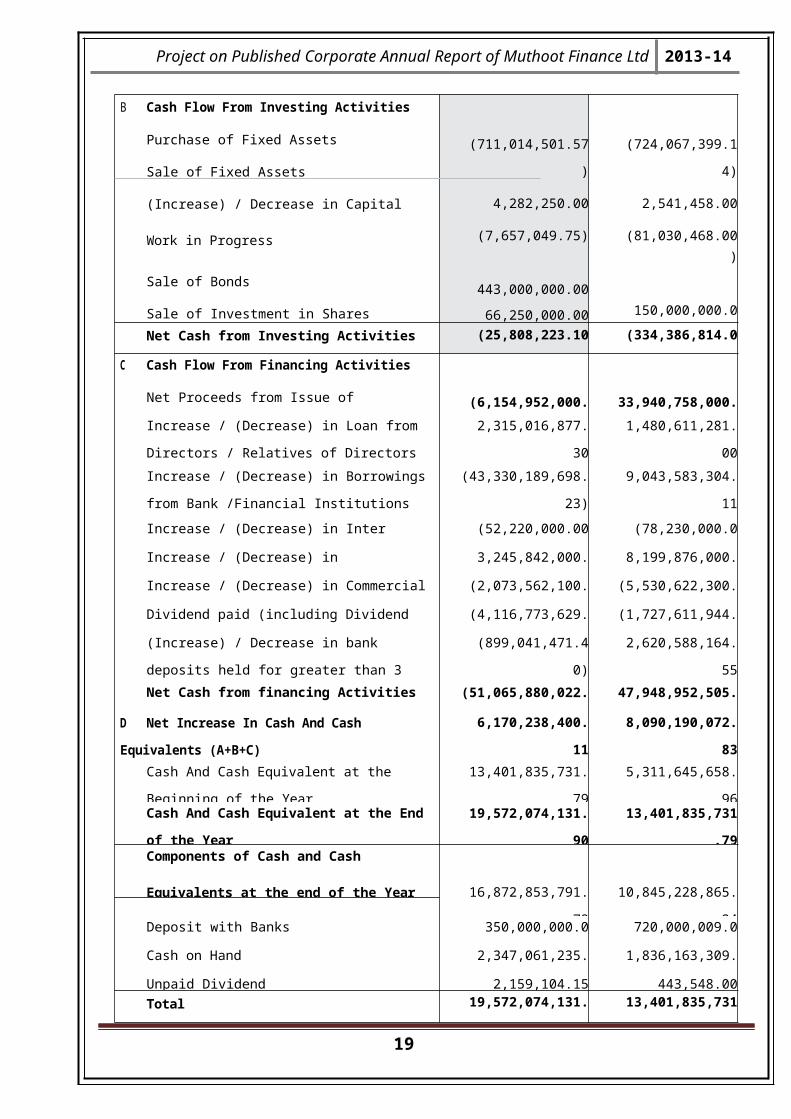

B Cash Flow From Investing Activities

Purchase of Fixed Assets

Sale of Fixed Assets

(Increase) / Decrease in Capital Work in Progress

Sale of Bonds

Sale of Investment in Shares

Interest

Income

(711,014,501.57)

4,282,250.00

(7,657,049.75)

443,000,000.00

66,250,000.00

81,966,908.60

97,364,169.62

(724,067,399.14)

2,541,458.00

(81,030,468.00)

150,000,000.00

---

252,089,352.15

66,080,242.90

Net Cash from Investing Activities (25,808,223.10) (334,386,814.09)

17

PARTICULARS 31st March, 2014 31st March, 2013

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

C Cash Flow From Financing Activities

(6,154,952,000.00) 33,940,758,000.00Net Proceeds from Issue of Debentures

Increase / (Decrease) in Loan from Directors /

Relatives of Directors

2,315,016,877.30 1,480,611,281.00

Increase / (Decrease) in Borrowings from Bank

/Financial Institutions

(43,330,189,698.23) 9,043,583,304.11

Increase / (Decrease) in Inter Corporate Loan (52,220,000.00) (78,230,000.00)

Increase / (Decrease) in Subordinated debt 3,245,842,000.00 8,199,876,000.00

Increase / (Decrease) in Commercial Papers (2,073,562,100.00) (5,530,622,300.00)

Dividend paid (including Dividend distribution tax) (4,116,773,629.85) (1,727,611,944.00)

(Increase) / Decrease in bank deposits held for

greater than 3 months

(899,041,471.40) 2,620,588,164.55

Net Cash from financing Activities (51,065,880,022.18) 47,948,952,505.66

D Net Increase In Cash And Cash Equivalents

(A+B+C)

6,170,238,400.11 8,090,190,072.83

Cash And Cash Equivalent at the Beginning of

the Year

13,401,835,731.79 5,311,645,658.96

Cash And Cash Equivalent at the End of the

Year

19,572,074,131.90 13,401,835,731.79

Components of Cash and Cash Equivalents at

the end of the Year 16,872,853,791.79 10,845,228,865.24

Deposit with Banks 350,000,000.00 720,000,009.00

Cash on Hand 2,347,061,235.96 1,836,163,309.55

Unpaid Dividend 2,159,104.15 443,548.00

Total 19,572,074,131.90 13,401,835,731.79

CHAPTER – IV

DATA ANALYSIS AND INTERPRETATIONS

MANAGEMENT DISCUSSION AND ANALYSIS

18

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

2011-12 2012-13 2013-140

1

2

3

4

5

6

7

8

6.7

4.5 4.7

GDP at factor cost

GDP GROWTH

The Indian Economy witnessed yet another year of sub 5 % GDP growth. FY 13 saw the

worst GDP growth rate in the decade. The last time the economic growth rate had pierced

the 5% mark. It is widely believed that economic growth will accelerate in 2014-15 as the

reform process continues and starts yielding results. The pick-up will depend on resolution of

several existing issues mainly implementation of stalled projects, ease of land acquisition,

approvals from state governments, mine sector reforms, capital infusion to banks etc. There

could be a minor improvement in growth rate in the second half of the current fiscal due to

improvement in manufacturing and investments to around 5% and depending on the level of

reforms, the growth may rise to 6% over medium term.

Role of NBFCs

NBFCs being financial intermediaries are engaged in the activity of bringing the saving and

the investing community together. In this role they are perceived to be playing a

complimentary role to banks rather than competitors. NBFCs have carved niche business

areas for them within the financial

sector space and are also popular for providing customised products. In short, NBFCs bring

the much needed diversity to the financial sector thus diversifying the risks, increasing

liquidity in the markets thereby promoting financial stability and bringing efficiency to the

financial sector.

Regulations

Reserve Bank Of India has over the last 50 years streamlined the NBFC regulations,

addressed the risks posed by them to financial stability, depositors’ and customers’ interests,

19

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

regulatory arbitrage and helped the sector grow in a healthy and efficient manner. Some of

the regulatory measures

include identifying systemically important non-deposit taking NBFCs as those with asset size

of Rs.100 Crores and above and bringing them under stricter prudential norms (CRAR and

exposure norms), issuing guidelines on Fair Practices Code, aligning the guidelines on

restructuring and

securitisation with that of banks, permitting NBFCs-ND-SI to issue perpetual debt

instruments etc. It is an acknowledged fact that NBFC’s in India are playing a crucial role in

meeting the ‘Financial Inclusion’ objectives and needs of our country.

Gold Loan Sector

The country’s Organised Gold Loan market has witnessed a significant expansion in the last

one decade. The large domestic household gold holding of the country enabled the creation

of this market. The magnitude of this holding could be more than 18000 tonnes. Most of the

gold is held by people in rural areas and in many cases this is the only asset they have in

their possession. While richer sections diversify their portfolio according to risk-return

equation, the poor rely more on gold as well as silver commodities. The jewellery bought in

times of prosperity has been sold for cash in periods of distress or need. Due to the

increased holding of gold as an asset among large section of people as also the non-

transparent practices of lending against gold in the Unorganised sector, entities like

‘Muthoot Finance’ started providing loans against the collateral of used gold jewellery many

years back and over a period transformed itself as NBFCs with core focus on gold loans.

Factors influencing expansion of gold loan sector

The gold loan industry is driven by multiple factors. Since the loan is granted against gold

jewellery, the quantum of gold jewellery available with the customers is of utmost

importance. The needs of the borrower coinciding with various purposes like cropping

season, business season, academic year, festivals, Medical purposes etc, are critical in

determining the demand for gold loans. Further, easy

availability of loans on flexible terms and changing attitude of customers to avail loans and

relative constriction by banks for giving personal loans enabled the popularisation of the

product. To tap the opportunity, aggressive network expansion by NBFCs on a pan India

basis, enabled the product to reach the masses and thereby widening the customer base.

Further, aggressive marketing campaigns by the NBFCs increased awareness among the

people and renunciation of stigma

20

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

attached to pledging of gold jewellery. NBFCs, since having core focus, invested in

infrastructure thereby building service quality. Customers found comfort and confidence in

their transparent practices and started shifting their loyalties from the unorganised sector to

the organised sector.

LEVEL PLAYING FIELD

The regulatory Loan to Value cap of 60% on gold price for NBFCs denied the sector a level

playing field with banks. The increased focus of banks on retail lending consequent to lack of

adequate opportunities for safe corporate lending created disequilibrium in gold loan

business. In January

2014, RBI relaxed the LTV norms for NBFCs by increasing the cap to 75% from 60%.

Subsequently, RBI made the LTV cap applicable for banks also. This measure will pave way

for a stability in the business of gold loans by NBFCs going forward and healthy

development of the sector.

OUTLOOK

Credit extended by the gold loan NBFCs witnessed a CAGR of 86.7% during the period

March 2009 to March 2013. In absolute terms, NBFC gold loans increased from just Rs.39

billion as on 31st March, 2009 to Rs.475 billion as on 31st March, 2013. Monetising idle gold

is crucial for creation of productive resources for India. NBFCs can continue to play a major

role in this process.

NBFCs-MONETISING IDLE GOLD

Core focus - The primary focus of the gold loan NBFCs is to provide gold loans.

Branch network - Branches play a significant role in building an institutions brand image. A

wide network of branches enables NBFCs to be closer to the customer

Faster turnaround time - Superior service creates loyalty and deeper customer

relationships. achieved without any compromise on documentation discipline and KYC

compliance requirements.

Transparent and Standard Operating Practices - NBFCs offer a transparent transaction

capturing all the terms clearly in the loan document and operate with standard operating

procedures

Flexible Repayment Option - Customers get a trouble free loan period where he is not

troubled for any payment of equated monthly instalment rather would be allowed to make

payment of interest and principal on closure of the loan.

21

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Resources availability - NBFCs have access to organised credit and hence do not face any

constraint.

Value to the Customer - Customers stay with a service provider if they pay a price they

deem fair for quality of the products they receive.

Low-cost structure - The Company has built network with a minimum investment

corresponding to the potential of business in which it is going to operate.

RISK MANAGEMENT

The objective of risk management systems is to measure and monitor the various risks the

Company is subject to and to implement policies and procedures to address these. The

Company continues to improve its operating processes and risk management systems that

will further enhance its ability to manage these risks.

INTERNAL SYSTEMS AND THEIR ADEQUACY

Muthoot Finance has an adequate internal control system in place to safeguard assets and

protect against losses from any unauthorised use or disposition. The Company’s internal

controls are supplemented by an extensive programme of internal audits, review by the

management, and documented policies, guidelines and procedures.

CAUTIONARY STATEMENTS

Statements in this Management Discussion and Analysis describing the Company’s

objectives, projections, estimates and expectations may be ‘forward looking statements’

within the meaning of applicable laws and regulations. This report should be read in

conjunction with the financial statements included herein and the notes thereto.

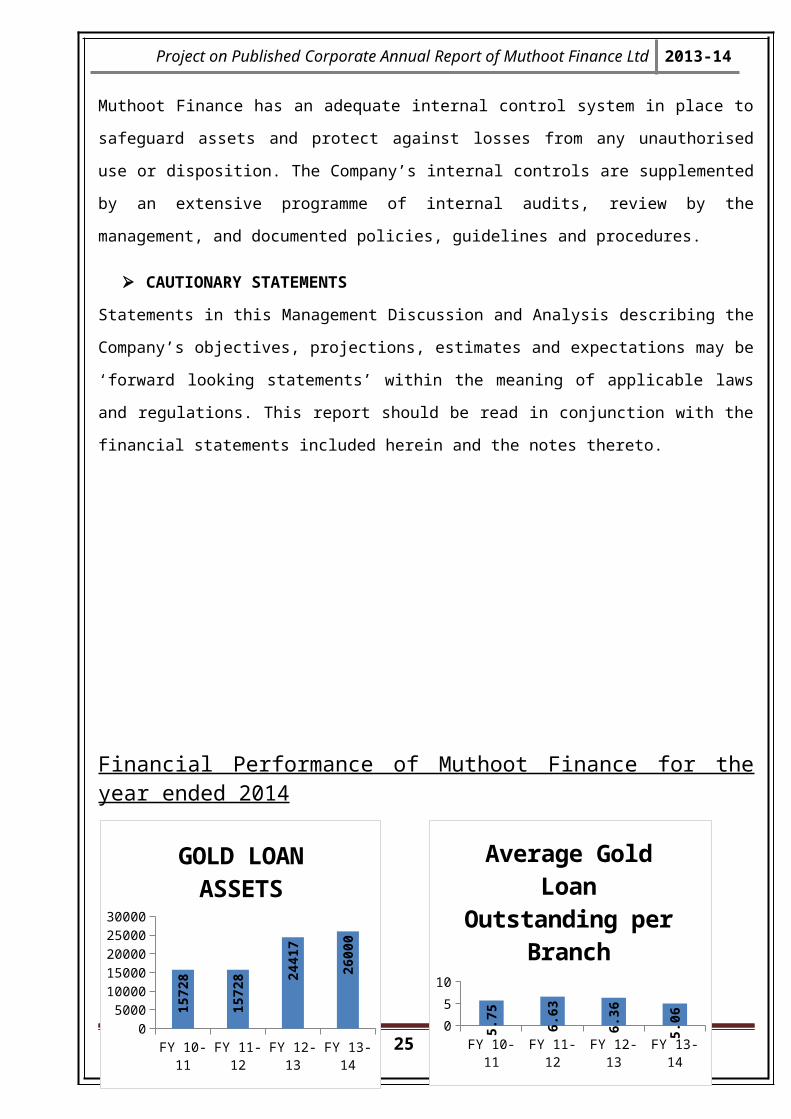

Financial Performance of Muthoot Finance for the year ended 2014

22

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

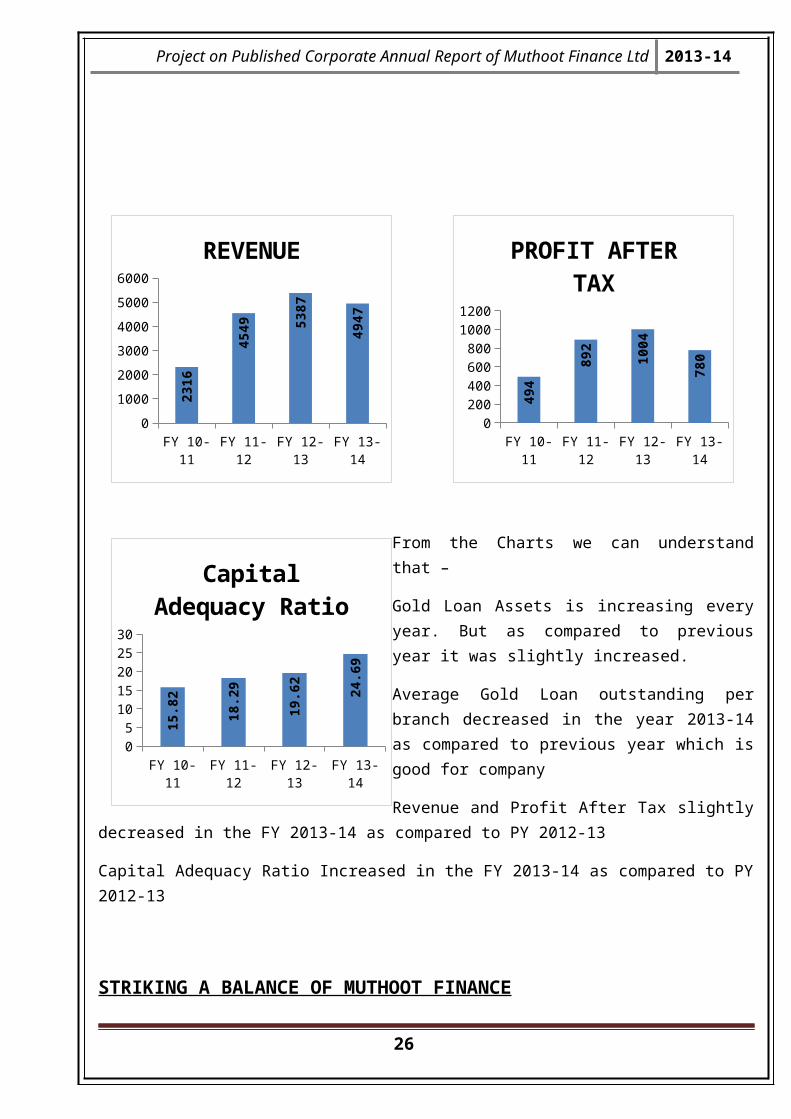

From the Charts we can understand that –

Gold Loan Assets is increasing every year. But as compared to previous year it was slightly increased.

Average Gold Loan outstanding per branch decreased in the year 2013-14 as compared to previous year which is good for company

Revenue and Profit After Tax slightly decreased in the FY 2013-14 as compared to PY 2012-13

Capital Adequacy Ratio Increased in the FY 2013-14 as compared to PY 2012-13

STRIKING A BALANCE OF MUTHOOT FINANCE

23

FY 10-11 FY 11-12 FY 12-13 FY 13-140

5000

10000

15000

20000

25000

30000

1572

8

1572

8

2441

7

2600

0

GOLD LOAN ASSETS

FY 10-11 FY 11-12 FY 12-13 FY 13-140

1000

2000

3000

4000

5000

6000

2316

4549

5387

4947

REVENUE

FY 10-11 FY 11-12 FY 12-13 FY 13-140

5

10

15

20

25

30

15.8

2

18.2

9

19.6

2 24.6

9

Capital Adequacy Ra-tio

FY 10-11 FY 11-12 FY 12-13 FY 13-140

200

400

600

800

1000

1200

494

892 10

04

780

PROFIT AFTER TAX

FY 10-11 FY 11-12 FY 12-13 FY 13-1401234567

5.75 6.

63

6.36

5.06

Average Gold Loan Outstanding per

Branch

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

During FY 2013-14, the gold loan industry was severely impacted by a set of three distinct

factors. First, it was regulatory action, designed to infuse greater credibility and governance

in the sector in the long run. Second, it was the fall in the price of gold, unleashing a fresh

wave of speculations on the business model, leading to an uncertain environment. Third, it

was the overall downturn in the core economic sectors, which led to Regulatory action first

reduced the maximum loan-to-value allowed on gold loans by NBFCs to 60% of gold price,

Subsequently, however, this cap was revised upwards to 75% for NBFCs and

simultaneously made this cap applicable for banks, which paved the way for a level playing

field. The fall in gold prices triggered a wave of speculation on business model leading to

suspicion in the minds of various stakeholders inspite of clarifications on the risk

management practices of the company. Therefore, striking a balance between adhering

to evolving regulation and changing as well as growing customer expectations

remains a key focus area.

Striking a balance between Regulatory landscape and commitments

The regulatory clarity came following a period of uncertainty, which engulfed the gold

loan industry, with intermediate rules making banks capable of lending at a higher

LTV than NBFCs. In addition, the disbursement of loans of Rs.1 lakh and above

compulsorily by cheque also affected the interest of customers as a normal cheque

collection usually takes about three days even now. Though it’s easier to obtain PAN

card now-a-days, insistence of PAN card for loans of Rs.5 lakhs and above was

another regulatory norm, which a gold loan customer was required to comply with.

As the largest industry player in the gold loan business, They focused on gold loan

financing with widening reach, customised products and services, and above all

deepening relationships and trust of a growing fraternity of customers, investors and

other stakeholders. They stand by their customers when it matters most, bringing

millions of people within the ambit of organised financing.

Striking a balance between raising capital and cost of capital

Muthoot finance have relied on the proceeds of non-convertible debentures placed

through their branches under private placement mode subscribed primarily by retail

investors with an average ticket size of around Rs.1.5 lakhs. This constituted about

49% of total funding source at the beginning of FY 2013-14. They believe that

mobilisation through this mode was possible on account of for industry leadership,

24

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

goodwill, trust, reputation, track record, performance, stability in our business and

strong quality asset portfolio.

To tame spiralling inflation, RBI consistently increased the benchmark policy repo rate

from 7.25% to 8% by the end of FY 2013-14 and correspondingly the bank rate from

8.25% to 9.0%. This resulted in the banking sector increasing the base rate of lending

to a certain extent. In addition, the regulatory stress and baseless speculation about

the business model kept the expectations of lenders on lending rates high. The

situation has eased a little following the RBI’s relaxation of LTV cap from 60% to 75%

Striking a balance between Mitigating Risk and Maximising Return.

They provide one of the fastest loan approval and collateral appraisal processes

backed by strong systems and policies that give us a two-fold advantage. One, it

strengthens the trust of the customers. Second, their strong systems and processes

help them to keep the bad debts write-off levels at the minimum. In addition, the gold

jewellery, which acts as a collateral for loans, can be easily liquidated at auctions,

ensuring maximum realisation of loan amounts in case of any defaults

While their assets under management declined considerably during FY 2013-14, they

remained profitable, despite hardships. Their profitability during tough times

demonstrates the strength of business model consequent to which the capital

leverage declined to 4.53 times from 6.52 times in previous year. As reserves

strengthened to Rs.3, 893 Crores, They decided to give back a higher amount to

stakeholders, resulting in a higher dividend payout of 29% as against 17% last year.

Such a measure will reinforce stakeholder trust in their operations and the long term

commitment to create value.

Striking a balance between Diverse Offerings and Fostering Relationships

During FY 2013-14, they disbursed Rs.4596 Crores comprising 21 lakhs transactions.

They have also forayed into the ATM network with the launch of White Label ATM,

empowering rural customers with ATM services. The ATM launch reiterates to

commitment towards making finance easily available in the rural hinterland. We

developed an in-house Core Banking Solution, It enabled to provide ‘anytime &

anywhere’ services to customers and enhanced convenience.

At Muthoot, they have been committed to continuously strengthen brand and enrich

products and services. Being consumer focused, they strive to reach and connect with

consumers through several brand initiatives. Apart from the conventional outdoor

25

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

branding routes (buses, bus depots, local trains, boats in high-traffic areas), we have

also aggressively scaled up contemporary branding measures (principal sponsors of

Delhi. Daredevils in 2011, 2012 and 2013 and online media, among others). These

measures have not only widened their reach, but also strengthened relationships with

customers.

Striking a balance between Employee Engagement and Employee Motivation

Muthoot empower and engage 25,012-people strong team to achieve the

organisational goals and, in turn, drive their career progression. They routinely

conduct several sales orientation and marketing programmes for their people, so that

they can go to the market and educate potential customers about the benefits of gold

financing.

During the year under review, they announced our maiden Employee Stock Option

Plan (ESOP) for all our permanent employees. The options were granted to

employees through three stock option schemes. The management decided to reward

employees for their loyalty and performance and the initiative helped enhance their

sense of ownership. They continue to train their national team at higher levels with

their established Regional Learning Centres across India with 7 days of average

training per employee. They focus on developing the qualities, such as soft-skills,

leadership, personality development, marketing and customer service, among others.

These factors enhance the service quotient of our team, motivating and inspiring

people to lead from the front.

Striking a balance between Commerce and Conscience

Muthoot have created sustainable value by driving financial inclusion for a significant

consumer base. They have the relevant infrastructure and the technological expertise

to process large number of transactions on a daily basis across pan-India branch

network. In addition, they are expanding and deepening their reach to India’s remote

corners with the help of a motivated workforce.

They are committed to empower the ambitions of a large cross-section of people, who

in turn help shape the nation’s future course as citizens. As a conscientious corporate,

they partner with several organisations to contribute in areas like education, health,

environment and safety. They are stepping up investments in the social sector to help

improve the quality of life

NOTES TO ACCOUNTS FOR THE YEAR ENDED 31 st March 2014

26

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

(Amounts in the financial statements are stated in Rupees, except for share data and as otherwise stated.)

1. Accounting Concepts

The financial statements are prepared on historical cost convention complying with the

relevant provisions of the Companies Act, 1956 and the Accounting Standards issued by the

Institute of Chartered Accountants of India, as applicable. The Company follows prudential

norms for income recognition; asset classification and provisioning as prescribed by Reserve

Bank of India vide Non-Banking Financial Companies Prudential Norms (Reserve Bank)

Directions, 2007. The estimates and assumptions used in these financial statements are

based upon the management evaluation of the relevant facts and circumstances as of the

date of the financial statements. Management believes that these estimates and

assumptions used are prudent and reasonable.

2. Revenue Recognition

Revenues are recognised and expenses are accounted on accrual basis with necessary

provisions for all known liabilities and losses. Revenue is recognised to the extent it is

realisable wherever there is uncertainty in the ultimate collection. Income from Non-

Performing Assets is recognised only when it is realised. Income and expense under

bilateral assignment of receivables accrue over the life of the related receivables assigned.

Interest income and expenses on bilateral assignment of receivables are accounted on gross

basis. Interest income on deposits is recognised on time proportionate basis.

3. Fixed Assets

Fixed assets are stated at historical cost less accumulated depreciation. Cost comprises the

purchase price and any attributable cost of bringing the asset to its working condition for its

intended use. Depreciation is charged at the rates specified in Schedule XIV of the

Companies Act, 1956.

4. Intangible Assets

Intangible Assets are amortised over their expected useful life. It is stated at cost, net of

amortisation. Computer Software is amortised over a period of five years on straight line

method.

5. Cash And Cash Equivalents

Cash and cash equivalents comprise of cash at bank, cash in hand, bank deposits having a

maturity of less than 3 months and unpaid dividend.

27

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

6. Provisions, Contingent Liabilities & Contingent Assets

Provisions are recognised only when the Company has present, legal, or constructive

obligations as a result of past events, for which it is probable that an outflow of economic

benefit will be required to settle the transaction and a reliable estimate can be made for the

amount of the obligation.Contingent liability is disclosed for (i) possible obligations which will

be confirmed only by future events not wholly within the control of the Company or (ii)

present obligations arising from past events where it is not probable that an outflow of

resources will be required to settle the obligation or a reliable estimate of the amount of the

obligation cannot be made. Contingent assets are not recognised in the financial

statements since this may result in the recognition of income that may never be realised.

7. General Reserve

Appropriate transfer to General Reserves in accordance with Companies (Transfer of Profits

to Reserves) Rules, 1975, has been made in the financial statements.

8. Debenture Redemption Reserve

During the year, the company has transferred an amount of Rs.6,637,035,559.00

(Previous Year Rs. 967,249,498.00) to the Debenture Redemption Reserve. No

appropriation was made from this Reserve during the year.

9. Statutory Reserve

Statutory Reserve represents the Reserve Fund created under Section 45 IC of the Reserve

Bank of India Act, 1934. An amount of Rs.1,560,138,107.00 representing 20% of Net Profit is

transferred to the Fund for the year ( Previous Year: Rs.2,008,479,046.00).

10.Secured Redeemable Non-Convertible Debentures

The Company had privately placed Secured Redeemable Non-Convertible Debentures for a

maturity period of 60-120 months with an outstanding amount of Rs.81,579,609,000.00

(Previous Year: Rs.94,596,214,000.00)

11.Secured Non Convertible Debentures – Public Issue

The outstanding amount of Secured Rated Non-Convertible Listed Debentures raised

through Public Issue stood at Rs.23,734,590,000.00 (Previous Year: Rs.16,872,937,000.00)

12.Subordinated Debt

Subordinated Debt is subordinated to the claims of other creditors and qualifies as Tier II

capital under the Non-Banking Financial (Non-Deposit Accepting or Holding) Companies

Prudential Norms (Reserve Bank) Directions, 2007. The outstanding amount of privately

placed subordinated debt stood at Rs.25,366,628,000.00 (Previous year:

Rs.23,000,972,000.00)

28

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

13.Long Term Loans and Advances

Security Deposit includes Rs.1,822,500.00 (Previous Year: Rs.1,822,500.00) being rent

deposit due from promoter Directors and Rs.1,470,000.00 (Previous Year: Rs.1,470,000.00)

being rent deposits due from firms in which promoter Directors are partners

14.Current Investments (Valued at lower of cost and fair value) – Quoted

Current investments refers to investment in 307 bonds of 10.05% Unsecured, Redeemable,

Non-Convertible, Upper Tier II Subordinated Bonds issued by Yes Bank Limited

Rs.307,000,000.00 listed in BSE (Previous Year: Rs.750,000,000.00)

15.Employee Benefits

Defined Contribution Plan - During the year, the Company has recognised the contribution

to Provident Fund, in the Statement of Profit and Loss.

Defined Benefit Plan - Gratuity Plan - The deficit in funding of gratuity Rs.18,733,086.00

has been accounted as Long term provisions.Estimated employer contribution for 2014-15 -

Rs.90,000,000.00

16.Dividends proposed to be distributed to equity shareholders

The Board has recommended a final dividend for the year 2013-14 of Re.1/- (10%) per

equity share of Rs.10/- each , subject to the approval of shareholders in the ensuing Annual

General Meeting. The Company has during the year paid interim dividends aggregating to

Rs.5/- (50%) per equity share of Rs.10/- each (Previous Year: Nil). The total dividend for the

year 2013-14 is Rs.6/- (60%) per equity

Share of Rs.10/- each (Previous Year Rs.4.5/- (45%) per equity share of Rs.10/- each).

17.Earnings Per Share

As per Accounting Standard 20, Earning Per Share is calculated by dividing the net profit or

loss for the year attributable to equity shareholders by the Weighted average number of

equity shares outstanding during the year.

18.Dividend remitted in foreign currency

The company has also remitted Rs.264,441,172.50 in Indian currency to 908 non resident

shareholders holding 58,764,705 shares of Rs.10/- each as final dividend for the F Y 2012-

13 and the company has remitted Rs.174,697,074.00 in Indian currency to 980 non resident

shareholders holding 58,232,358 shares of Rs.10/- each as First Interim Dividend for the F Y

2013-14 and Rs.101,637,018.00 in Indian currency to 915 shareholders holding 50,818,509

shares of Rs.10/- each as Second Interim Dividend for the F Y 2013-14 (Previous year : The

Company has remitted Rs.150,220,372.00 in Indian currency to 1060 non-resident

shareholders holding 37,555,093 Shares of Rs.10/- each).

29

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

INTERPRETATIONS ON FINANCIAL STATEMENTS

INTERPRETATION ON BALANCE SHEET OF MUTHOOT FINANCE LTD FOR THE

YEAR ENDING 31 st MARCH 2014

Shares and Premium

On 29th April, 2014, your Company allotted 2, 53, 51,062 shares of Rs.10 each for

cash at a premium of Rs.155 per equity share aggregating to Rs.41, 829.25 Lakhs.

Economic Scenario

India’s economic growth rate in the current financial year remained weak at 4.7 %

Dividend

Based on Company’s performance, directors had recommend for approval of the

shareholders a dividend of 10% for Equity Shares of face value of Rs.10 each (Rs.1/-

per share) of the Company for the financial year 2013-14 which is payable on

obtaining the approval of the shareholders of the Company on the 17th Annual

General Meeting.

Gross retail loan assets under management

The Company’s Gross Retail Loan Assets under Management decreased from Rs.26,

386 Crores in FY 2012-13 to Rs.21, 861 Crores in FY 2013-14. Regulatory headwinds

in the form of lower LTV of 60% throughout the year impacted disbursements and

resulted in decline in loan portfolio. LTV has, since January 2014, increased to 75%

for NBFCs and later made the same applicable for banks. This relaxation can

positively impact the business going forward.

Average gold loan outstanding per branch

The Company’s average gold loan outstanding per Branch witnessed a decline from

Rs.6.36 Crores in FY 2012-13 to Rs.5.06 Crores in FY 2013-14 on account of decline

in gold loan portfolio.

Subordinated Debts

Subordinated Debts represents long term source of funds for the Company and the

amount outstanding as on 31st March, 2014 was Rs.2635 Crores. Commercial Banks

continued their support to the Company during Financial Year. As of 31st March 2014,

borrowings from banks were Rs.5803 Crores as against Rs.10136 Crores in the

previous year. The reduction in borrowings were on account of the decline in gold

loan portfolio of Rs.4383 Crores during the year.

Capital Adequacy

30

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Your Company’s Capital Adequacy Ratio as of 31st March, 2014 stood at 24.69% of

the aggregate risk weighted assets on balance sheet

Public Deposits

The Company has not accepted any public deposits and as such, no amount on

account of principal or interest on public deposits was outstanding as on the date of

Balance Sheet.

Unsecured loans

The company has taken unsecured loans during the year was Rs.48,661.03 Lakhs

and the year-end balance of such loan is Rs.44,617.78 Lakhs. In our opinion, in

respect of loan taken, the repayment of principal amount and interest was regular.

Current Assets

Current Assets have increased as compare to previous year that means the firms

liquidity position is very good and he is able to meet its current obligations.

INTERPRETATION ON PROFIT AND LOSS ACCOUNT OF MUTHOOT FINANCE LTD

FOR THE YEAR ENDING 31 st MARCH 2014

Revenues

The Company’s revenues declined by 8% from Rs.5,387 Crores in FY 2012-13 to

Rs.4947 Crores in FY 2013-14. This was on account of reduction in gold loan portfolio

during the year.

Profit before Tax

The Company’s Profit before Tax declined by 21%, from Rs.1,511 Crores in FY 2012-

13 to Rs.1193 Crores in FY 2013-14.

Profit after Tax

Muthoot Finance’s Profit after Tax declined by 22% at Rs.780 Crores in FY 2013-14

from Rs.1,004 Crores in FY 2012-13.

Capital Adequacy Ratio

The Company’s Capital Adequacy Ratio increased from 19.62% in FY 2012-13 to

24.69% in FY 2013-14 with Tier I capital of 18.01%, on account of ploughing back of

profit for the year net of dividend payment.

Earnings per share (EPS)

Earnings per share declined to Rs.20.99 in 2013-14 from Rs. 27.02 in 2012-13 on

account of lower profits generated during the year.

Comparision of Profit and Loss as compare to previous year –

31

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

Total income declined by 8% to Rs.4947 Crores as compared to previous year 2012-

13

Profit Before Tax declined by 21% to Rs.1194 Crores as compare to previous year

2012-13

Profit After Tax declined by 22% to Rs.780 Crores as compare to previous year 12-13

The Return on Average Retail Loans declined to 3.22% in the year 2013-14 as

compared to 4.05% in fiscal 2012-13.

On account of the above, the Net Interest Margin declined to 9.42% in the year 2013-

14 as against 10.28% in fiscal 2012-13.

The Company remitted to exchequer Rs.458 Crores in the year 2013-14

Observed from the above Profit & Loss A/C Statement of Muthoot Finance Ltd it can

say that the firm has limited earnings in the year 2014.

INTERPRETATION ON CASH FLOW STATEMENT OF MUTHOOT FINANCE LTD FOR

THE YEAR ENDING 31 st MARCH 2014

Observed from the above table that cash flow statement of Muthoot Finance Limited.

In the year 2013-14 variable net profit after tax, depreciation and others have

decreased.

Operating profit before and after working capital changes has decreased for the

financial year 2014.

Cash generated from operations have increased due to huge decrease in trade

receivables

Net Cash from operating activities have increased due to a huge decrease in trade

receivables and other receivables and even due to decrease in loans and advances

and liabilities. Thus this increased Net cash from operating activities.

Due to increase in sale of Bonds and sale of investment in shares and decrease in

capital work in progress there was a huge decrease in Net Cash from investing

Activities.

Due to fund borrowings form financial institute/banks there was a huge increase in

Net cash from financing activities.

Cash and Cash Equivalent increased during the year 2013-14 as compared to

previous year 2012-13 this shows that the liquidity fund is very much good in the year

2014 and company can utilise it in a way that it gain a huge profit in upcoming years.

32

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

CHAPTER - V

CONCLUSION

An Annual Report is a document published on a yearly basis to provide stockholders, the

public and the government with financial data, a summary of ownership, and the accounting

practices used to prepare the report. Annual reports measure a corporation`s financial

health. They focus on past and present financial performance, and make predictions about

future prospects. The annual report is a report issued to a company's shareholders,

creditors, and regulatory organizations following the end of its fiscal year. An annual report

includes a balance sheet reflecting changes in the corporation`s financial worth, an income

cash flow statement, and other relevant documentation. In addition they make public details

about products and services, domestic and foreign markets and the backgrounds of directors

and executive officer. It also contain management comments, an audit report, and various

supporting schedules that may be required by regulatory organizations.

An annual report is an audited corporate document that details the business activity and

financial status of a publicly-held company over the previous year. The annual

report provides a variety of important financial data. The SEC requires all publicly traded

companies to file reports on an annual and quarterly basis, and the reports provide in-depth

information on a company's products, market segments, competitors, customers,

management and legal proceedings.

In this annual report project I have analysed annual report of Muthoot Finance Ltd.

I have studied balance sheet, income statement and cash flow statement of Muthoot Finance

for the year ending 31st March 2014 and understood company`s financial positions in current

year comparing to previous years and gave interpretations of it. Muthoot Finance is the

fastest growing company largest loan, which offers a variety of gold trade, personal loans,

housing, education, investments, etc., low interest rates on the site, only 1% of the Muthoot

Finance Web site to keep people from all over India in place of promise and improvement

but still the main lending. Muthoot Finance delivered a stable performance and recorded

revenues to the tune of Rs.4947 Crores. Significant shareholder value was created with our

basic earnings per share at Rs.20.99 for FY 2013-14. Our book value per share increased to

Rs.114.73.

Annual report project helps us in analysing the financial position of the company practically

and to judge accordingly company`s position in the market.

33

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14

BIBLOGRAPHY

17 th Annual Reports of Muthoot Finance Ltd of 2014

www.muthootfinance.com

Advance Accounting Finance Book of M.com Part 1 Semester 1 written by L.N

Chopde, D.H Choudhari, Dhiren Kanabar and Sandeep Chopde.

and published by Sheth Publications

http://en.wikipedia.org/wiki/Annual_report

http://en.wikipedia.org/wiki/Muthoot_Finance_Ltd

http://www.muthootfinance.com/about-us/

http://www.muthootfinance.com/fair-practices-code/

34

Project on Published Corporate Annual Report of Muthoot Finance Ltd 2013-14