annual report for amincome - aminvest · pdf fileannual report for 31 march 2017 amincome ....

TRANSCRIPT

Annual Report for

31 March 2017

AmIncome

AmIncome

TRUST DIRECTORY

Manager

AmFunds Management Berhad

9th & 10

th Floor, Bangunan AmBank Group

55 Jalan Raja Chulan

50200 Kuala Lumpur

Board of Directors

Raja Maimunah Raja Abdul Aziz

Mustafa Mohd Nor

Tai Terk Lin

Datin Maznah Mahbob

Sum Leng Kuang

Investment Committee

Sum Leng Kuang

Tai Terk Lin

Mustafa Mohd Nor

Zainal Abidin Mohd Kassim

Datin Maznah Mahbob

Trustee

HSBC (Malaysia) Trustee Berhad

Auditors and Reporting Accountants

Ernst & Young

Taxation Adviser

Deloitte Tax Services Sdn Bhd

AmIncome

CONTENTS

1 Manager’s Report

10 Independent Auditor’s Report to the Unitholders

13 Statement of Financial Position

14 Statement of Comprehensive Income

15 Statement of Changes In Equity

16 Statement of Cash Flows

17 Notes to the Financial Statements

43 Statement by the Manager

44 Trustee’s Report

45 Directory

1

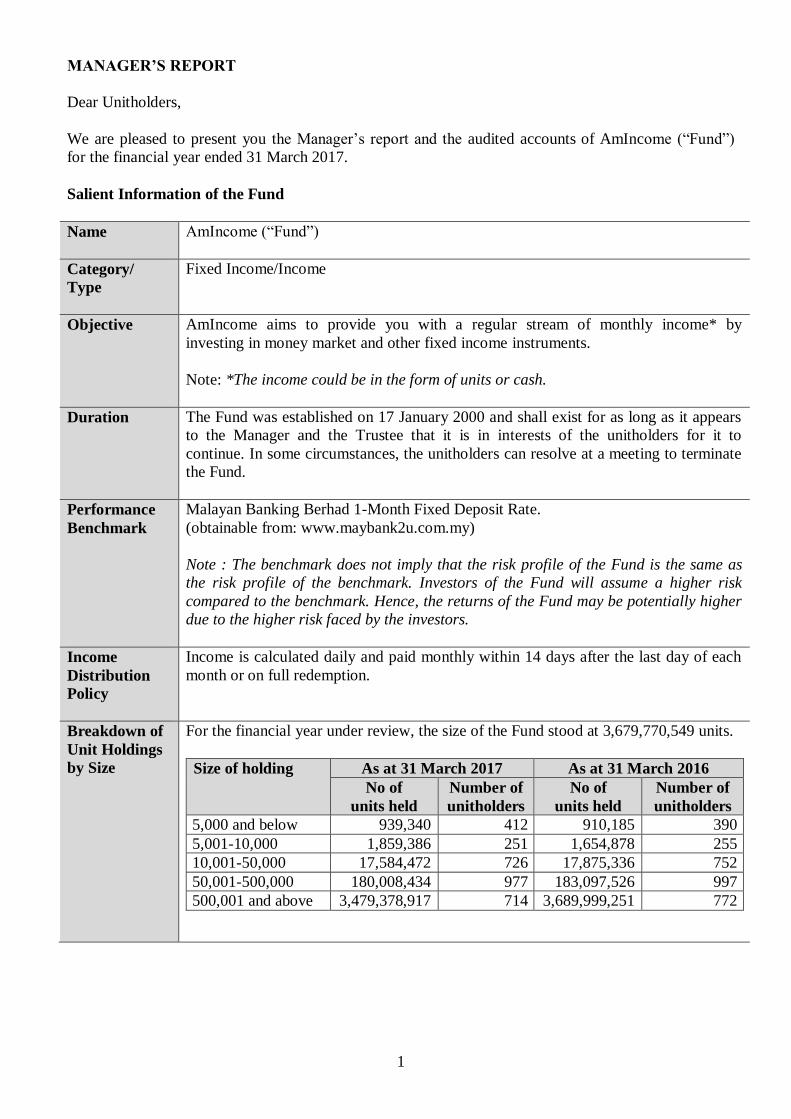

MANAGER’S REPORT

Dear Unitholders,

We are pleased to present you the Manager’s report and the audited accounts of AmIncome (“Fund”)

for the financial year ended 31 March 2017.

Salient Information of the Fund

Name AmIncome (“Fund”)

Category/

Type

Fixed Income/Income

Objective AmIncome aims to provide you with a regular stream of monthly income* by

investing in money market and other fixed income instruments.

Note: *The income could be in the form of units or cash.

Duration The Fund was established on 17 January 2000 and shall exist for as long as it appears

to the Manager and the Trustee that it is in interests of the unitholders for it to

continue. In some circumstances, the unitholders can resolve at a meeting to terminate

the Fund.

Performance

Benchmark

Malayan Banking Berhad 1-Month Fixed Deposit Rate.

(obtainable from: www.maybank2u.com.my)

Note : The benchmark does not imply that the risk profile of the Fund is the same as

the risk profile of the benchmark. Investors of the Fund will assume a higher risk

compared to the benchmark. Hence, the returns of the Fund may be potentially higher

due to the higher risk faced by the investors.

Income

Distribution

Policy

Income is calculated daily and paid monthly within 14 days after the last day of each

month or on full redemption.

Breakdown of

Unit Holdings

by Size

For the financial year under review, the size of the Fund stood at 3,679,770,549 units.

Size of holding As at 31 March 2017 As at 31 March 2016

No of

units held

Number of

unitholders

No of

units held

Number of

unitholders

5,000 and below 939,340 412 910,185 390

5,001-10,000 1,859,386 251 1,654,878 255

10,001-50,000 17,584,472 726 17,875,336 752

50,001-500,000 180,008,434 977 183,097,526 997

500,001 and above 3,479,378,917 714 3,689,999,251 772

2

Fund Performance Data

Portfolio

Composition

Details of portfolio composition of the Fund for the financial years as at 31 March are as

follows:

FY

2017

%

FY

2016

%

FY

2015

%

Corporate bonds 44.90 49.60 54.76

Cagamas bonds - - 0.59

Malaysian Government Securities 0.27 - -

Quasi-Government bonds 0.76 - -

Cash and others 54.07 50.40 44.65

Total 100.00 100.00 100.00

Note: The abovementioned percentages are calculated based on total net asset value.

Performance

Details

Performance details of the Fund for the for the financial years ended 31 March are as

follows:

FY

2017

FY

2016

FY

2015

Net asset value (RM)* 3,731,666,854 3,942,659,183 4,310,599,433

Units in circulation* 3,679,770,549 3,893,537,176 4,266,090,477

Net asset value per unit

(RM)* 1.0000

1.0000

1.0000

Highest net asset value per

unit (RM)* 1.0000 1.0000

1.0000

Lowest net asset value per

unit (RM)* 1.0000 1.0000

1.0000

Benchmark performance (%) 3.00 3.16 3.11

Total return (%)(1)

3.18 3.18 3.02

- Capital growth (%) - - -

- Income distribution (%) 3.18 3.18 3.02

Gross distribution (RM) 119,447,771 129,199,537 134,104,757

Net distribution (RM) 119,447,771 129,199,537 134,104,757

Management expense ratio

(%)(2)

0.85 0.85

0.80

Portfolio turnover ratio

(times)(3)

0.21 0.32

0.34

* Above price and net asset value per unit are shown as ex-distribution.

Note:

(1) Net asset value per unit is aimed to be maintained at RM1.00 as all income earned is

distributed on daily basis.

(2) Total return is the annualised return of the Fund for the respective financial years

computed based on the income return of the Fund net of all fees.

(3) Management expense ratio (“MER”) is calculated based on the total fees and

expenses incurred by the Fund divided by the average fund size calculated on a daily

basis.

(4) Portfolio turnover ratio (“PTR”) is calculated based on the average of the total

3

acquisitions and total disposals of investment securities of the Fund divided by the

average fund size calculated on a daily basis. The PTR decreased by 0.11 times

(34.4%) as compared to 0.32 times for the financial year ended 31 March 2016 mainly

due to decrease in investing activities.

Average Total Return (as at 31 March 2017)

AmIncome(a)

%

MBB(b)

%

One year 3.18 3.00

Three years 3.12 3.09

Five years 2.99 3.05

Ten years 2.92 2.87

Annual Total Return

Financial Years Ended

(31 March)

AmIncome (a)

%

MBB(b)

%

2017 3.18 3.00

2016 3.18 3.16

2015 3.02 3.11

2014 2.75 3.00

2013 2.81 2.99

(a) Source: Novagni Analytics and Advisory Sdn Bhd.

(b) Malayan Banking Berhad 1-month fixed deposit rate (“MBB”)

(Obtainable from: www.maybank2u.com.my).

The Fund performance is calculated based on daily returns of the Fund. Average total

return of the Fund and its benchmark for a period is computed based on the accumulated

returns for that period annualised over one year.

Note: Past performance is not necessarily indicative of future performance and that

unit prices and investment returns may go down, as well as up.

Fund

Performance

For the financial year under review, the Fund registered a return of 3.18% which was

entirely income distribution in nature.

Thus, the Fund’s return of 3.18% has outperformed the benchmark’s return of 3.00% by

0.18%.

As at 31 March 2017, the net asset value (“NAV”) per unit of the Fund is maintained at

RM1.0000, while units in circulation decreased by 5.49% from 3,893,537,176 units to

3,679,770,549 units.

The line chart below shows comparison between the annual performances of AmIncome

and its benchmark, MBB, for financial years ended 31 March.

4

2.81 2.75

3.02

3.18 3.182.99 3.00

3.11

3.163.00

1.00

1.50

2.00

2.50

3.00

3.50

4.00

To

tal R

etu

rn (%

)

Financial Years Ended (31 March)

AmIncome

MBB

Note: Past performance is not necessarily indicative of future performance and that

unit prices and investment returns may go down, as well as up.

Has the Fund

achieved its

objective?

The Fund has achieved its objective to provide investors with a regular stream of monthly

income* by investing in money market and other fixed income instruments.

Note: *The income could be in the form of units or cash.

Strategies

and Policies

Employed

For the financial year under review, the Fund seeks to achieve its objective by invested

primarily in short to medium term fixed income instruments (i.e. debt instruments with

maturity of no longer than five (5) years) with minimum short term local credit rating of

P2 (by RAM) or MARC2 (by MARC) or long-term credit rating of A3 (by RAM) or A-

(by MARC).

With the exception of unforeseeable circumstances (e.g. in the event of a default, the

restructuring or the recovery process may take longer than the maturity of the debt

instrument), the weighted average maturity of the Fund’s investments would not exceed

one year.

Portfolio

Structure

This table below is the asset allocation of the Fund for the financial years under review.

As at

31-3-2017

%

As at

31-3-2016

%

Changes

%

Corporate bonds 44.90 49.60 -4.70

Malaysian Government Securities 0.27 - 0.27

Quasi-Government bonds 0.76 - 0.76

Cash and others 54.07 50.40 3.67

Total 100.00 100.00

5

For the financial year under review, the Fund exposure to corporate bonds stood at

44.90% while the remaining 0.27%, 0.76% and 54.09% of the Fund are made up of

Malaysian Government Securities, Quasi-Government bonds and cash holdings.

Cross Trades

Cross trades are conducted between the Fund and other funds; and private mandates

managed by the Manager amounting to:

Financial Institutions

Transaction Value

(RM)

RHB Investment Bank Berhad 64,366,430.14

Malayan Banking Berhad 5,096,395.72

Hong Leong Bank Investment 13,518,776.44

Total 82,981,602.30

Funds

Transaction Value

(RM)

AmIncome Institutional 3 30,156,986.30

AmBond 13,518,776.44

AmDynamic Bond 9,103,290.41

AmIncome Regular 2 14,924,249.32

AmIslamic Fixed Income Conservative 15,278,299.83

Total 82,981,602.30

Distribution /

Unit splits

The Fund distributes the entire income on a monthly basis. For the financial year under

review, the Fund has distributed income totaling RM119,447,771 and no unit split was

declared.

State of

Affairs

There has been neither significant change to the state of affairs of the Fund nor any

circumstances that materially affect any interests of the unit holders during the financial

year under review.

Rebates

and Soft

Commission

It is our policy to pay all rebates to the Fund. Soft commission received from

brokers/dealers are retained by the Manager only if the goods and services provided are of

demonstrable benefit to unitholders of the Fund.

During the financial year under review, the Manager had received on behalf of the Fund,

soft commissions in the form of fundamental database, financial wire services, technical

analysis software and stock quotation system incidental to investment management of the

Fund. These soft commissions received by the Manager are deem to be beneficial to the

unitholders of the Fund.

Market

Review

In April 2016, Malaysia released its February exports number, which rebounded 6.7%

YoY. The increase was generally driven by electrical and electronics sector as well as

increase in palm oil and palm-based and timber and timber based products. On the

inflation front, CPI for March came in much weaker than expected at 2.6% YoY against

consensus expectations of 3.4%. The drop was due to lower transport cost as RON95

petrol price was reduced by 15 sen to RM1.60 per litre in March 2016 from RM1.75 in

February. Meanwhile, Bank Negara Malaysia (BNM) said that the reduction of the

statutory reserve requirement by 50 basis points on 1 February 2016 has had its desired

impact on the banking system’s interbank rates. The base rate of commercial banks, on

6

average, remained relatively stable at 3.89% in March (February: 3.88%). On the

consumer sentiment front, 1Q16 Consumer Sentiment Index (“CSI”) has rebounded to

72.9 points after plunging for six consecutive quarters. Recall that the index had hit its all-

time lows in the past two quarters, falling to 63.8 in 4Q15. In April, BNM’s international

reserves continue to climb steadily and were last seen at USD97b as at end-March 2016.

More pertinently, foreign holdings in Malaysian bonds of RM226.6 billion as at end

March has broken the previous record set in November 2014. Strengthening crude oil

prices and foreign fund inflows in both the bond as well as equities market has help turned

the Ringgit into Asia’s best-performing currency, confounding some analyst’s

expectation. The Ringgit has surged around 10% as at end April, the most in 43 years.

Finally, polling for Sarawak’s 11th state election has finally been announced to be on 7

May 2016.

In May 2016, Bank Negara Malaysia BNM kept the Overnight Policy Rate and Statutory

Reserve Requirement (“SRR”) ratio unchanged at 3.25% and 3.50% respectively as

widely expected in Datuk Muhammad Ibrahim’s inaugural Monetary Policy Committee

(“MPC”) meeting as BNM Governor. The tone of the MPC statement was largely neutral

with the stance broadly similar to the previous MPC statements. BNM also reiterated its

expectations for the domestic economy to expand by 4.0 – 4.5% in 2016 while inflation is

expected to trend lower for the remaining parts of the year from the average consumer

price index (“CPI”) of 3.4% in the first quarter of 2016 (“1Q16”). This followed the

release of Malaysia’s 1Q16 gross domestic product (“GDP”) data which grew at a slower

pace of 4.2% year-on-year (“YoY”), on the back of weakness in exports and soft private

investment growth while on a quarter to quarter basis, the domestic economy grew 1.0%,

compared to 1.5% previously.

In June 2016, Malaysia reported a positive growth in exports of 1.6% YoY for the month

of April 2016, while imports contracted by 2.3%, thus leaving a positive trade balance of

RM9.1b. Main contributors to exports came from the E&E sector which showed an

encouraging growth of 2.1% versus 0.5% in the preceding month. On the inflation front,

May’s CPI eases marginally to 2.0% YoY matching market expectations. Since the

implementation of GST in April 2015, the initial price shock has faded while the current

record low pump prices continue to keep inflationary pressure in check. Meanwhile,

Malaysia’s unemployment rate continued to inch up in April. At 3.6%, the unemployment

figure is at the highest since 2010. Finally, Malaysia’s Ringgit appreciated versus USD

by 2.9% from RM4.15 to RM4.03 at as end June. The Ringgit has been volatile in June

primarily due to two key events, the FOMC meeting as well as the UK Referendum on

Brexit.

In July 2016, Malaysia reported a negative growth in exports of -0.9% YoY for the month

of May 2016, its first drop in 4 months. This was against market expectation of 2.0%

growth. Nevertheless, Malaysia’s trade surplus continues to be in the positive albeit

narrowing to RM3.26b (April: RM9.06b) which brings cumulative trade surplus to

RM36.3b YTD. To recap, the biggest news of the month came from Bank Negara

Malaysia (“BNM”) which unexpectedly cut the Overnight Policy Rate (“OPR”) by 25bps

to 3.00% at its July 2016 meeting. This was the first monetary policy move since July

2014. BNM’s Governor was also reported as explaining that the cut was a pre-emptive

move in light of the recent UK Referendum on Brexit event as well as weaker global

growth prospects in the near term. On the inflation front, June’s CPI softened again to

1.6% YoY, below consensus expectations. Average inflation for 1H2016 is now around

2.7% which is in line with BNM’s guidance of 2 - 3% for 2016.

In August 2016, Malaysia exports bounced back into gain of 3.4% y-o-y in June after

falling by -0.9% in May and compared with +1.6% in April. Meanwhile, the foreign

7

exchange reserves increased marginally by USD0.1b to USD97.3b as at 29 July 2016. The

current account surplus in the balance of payments narrowed to MYR1.9bn in 2Q 2016,

after recording a surplus of MYR5.0bn in 1Q and compared with a surplus of MYR8.1bn

in 2Q 2015. This was attributed to a smaller surplus in the merchandise trade account and

a larger deficit in the income transfers. Meanwhile, the financial account registered a

higher net inflow of MYR9.5bn in 2Q, compared with an inflow of MYR5.8bn in the

previous quarter. The improvement was mainly due to a rebound in net inflow on other

investments and a larger net inflow of direct investments. On the other hand, the

slowdown in the Malaysian economy continued with real GDP growing at a slower pace

of 4.0% y-o-y in 2Q 2016, from +4.2% in 1Q and +4.5% in 4Q 2016. The overall growth

was dragged lower by a cutback in inventories and subdued exports.

In September 2016, Malaysia’s PMI reading rose to 48.6 in September from 47.4 in

August 2016. This marked the highest reading in eight months. Nevertheless, it was still

the eighteenth consecutive month of contraction as indicated by the sub 50 reading. On

the inflation front, headline inflation reading for August rebounded to 1.5% versus

consensus expectation of 1.3%. Main drivers were non-food items particularly cultural

services which saw inflation surging from 1.0% in July to 6.1% YoY in August. Finally,

the banking sector’s loan growth moderated for the twelfth consecutive month to 4.2%

YoY in August from 5.1% YoY in July. Notably, this is the lowest level in at least 13

years, as lending activities continue to face headwinds from a slowing economy, tepid

deposit growth and rising loan impairments.

In October 2016, Malaysia’s foreign exchange reserves rose by USD0.2bn to USD97.7bn

as at 30 September 2016, from USD97.5bn registered at end-August and compared to

USD95.3bn at end-December 2015. On the inflation front, the headline inflation rate

remained stable in September, as the easing in cost of food and beverages was mitigated

by the smaller magnitude of decline in cost of transport. The core inflation rate inched

lower in September. Growth of the broader money supply, M3, slowed to 2.2% y-o-y in

September, from +2.4% in August, due to a decline in external operations and a slowdown

in demand for funds by the private and public sector. Meanwhile, loan growth was stable

at 4.2% y-o-y in September, unchanged from the previous month but lower compared

with +5.6 in July, as the deceleration in growth of household loans were mitigated by the

marginal increase in business loans.

In November 2016, Malaysia’s foreign exchange reserves rose by USD0.5bn to

USD98.3bn as at 15 November 2016, from USD97.8bn registered at end-October 2016

and compared to USD95.3bn at end-December 2015. CPI for Oct 2016 came in

marginally lower at 1.4% YoY compared to Sep 2016’s reading on 1.5% YoY. 3Q GDP

was 4.3% YoY, higher than consensus expectations of 4.0% YoY (2Q: 4.0%, 1Q: 4.2%).

GDP growth was boosted by higher consumer spending which grew 6.4% YoY, supported

by wage and employment growth. Private investment eased slightly to 4.7% from 5.6% in

2Q, attributed to a decline in spending on machinery and equipment. Government

spending also slowed to 3.1% from 6.5% in 2Q, on the back of lower spending on supply

and services. Bank Negara Malaysia (BNM) left its Overnight Policy Rate(OPR)

unchanged at 3.00%, as expected by the market given the significant degree of financial

market volatility following Donald Trump's presidential victory. Compared to September,

BNM slightly upgraded its view on global growth in 2017, but retained its assessment that

the domestic economy remains on track to expand as projected in 2016 and 2017.

In December 2016, Malaysia’s manufacturing Purchasing Managers’ Index (PMI)

continue to remain below the 50-level mark coming in unchanged at 47.1 in December.

This was the twenty first consecutive months of contraction. On the trade front, exports

were below expectations, recording a contraction of 8.6% YoY in October (September: -

8

3.0%). Consensus expectations were for a contraction of -5.6%. Imports meanwhile also

fell by 6.6% YoY (September: -0.1%) driven by broad-based declines in capital imports (-

2.0%), intermediate imports (-8.9%), and consumption imports (-8.0%). Nevertheless,

trade surplus continues to be positive at RM9.76b (September: RM7.56b). Indicative of

the huge foreign outflows in the month of November, Malaysia’s foreign reserves fell

USD1.4b to USD96.4b. This was the lowest reserve level since March 2016. The current

level of reserves is sufficient to cover 1.2 times of short-term external debt and 8.3 months

of retained imports. During the month, Bank Negara Malaysia (“BNM”) announced

several measures to enhance onshore foreign exchange liquidity effective 5 December

2016. The measures include the liberalization and deregulation of the onshore MYR

hedging market, streamlining treatment for investment in foreign currency assets and

incentives and treatment of export proceeds. These pre-emptive measures were

implemented to stabilise the ringgit and support financial stability amid further broad

strengthening of the USD. Finally, the banking sector’s loan growth showed signs of

bottoming. For the month of November, growth accelerated to 5.3% YoY (October: 4.5%)

and a robust 0.9% MoM, resulting in YTD annualised loan growth improving to 4.7%

(10M2016: 4.0%). The main driver of loan growth was in working capital loans (+1.6%

MoM vs average MoM run rate of +0.3%). In terms of consumer loans, residential

property loan growth remained stable at 9.5% YoY while automobile loans remain mired

in negative territory at -0.8% YoY.

In January 2017, after increasing by USD 0.2b and USD 0.5b in October and November

respectively, Malaysia’s foreign reserves fell by USD3.7b to USD 94.6b in December.

This was the lowest reserve level the start of the year and the decline was spurred by

considerable foreign outflows. The current level of reserves is sufficient to cover 1.2 times

of short-term external debt and 8.3 months of retained imports. In comparison Malaysia’s

foreign reserves stood at USD 95.3bn at end-December 2015. On the trade front exports &

imports rebounded 11.2% YoY. BNM left the policy rate unchanged at 3.00% in its latest

meeting, with a more upbeat statement on the external sector and higher inflation

expectation for 2017. The general expectation is that BNM will leave the rate unchanged

in 2017, against the backdrop of expected Fed rate hike(s) during the year.

In February 2017, Malaysia’s 4Q16 GDP growth was printed at 4.5% vs consensus of

4.4%, in line with BNM’s forecasts of 4.0-4.5%. The growth came on the back of

moderate rebound in exports/imports and resilient domestic demand in the 4 Qtr. 2016

budget deficits met the 3.1% of GDP target allaying concerns on the sovereign’s ratings.

Further, despite the persistent weakness in the MYR, Malaysia external reserves remained

resilient; it stood unchanged from end-January at US$95b in mid-February. The January

CPI print came in much higher than expected today at 3.2%, vs consensus estimate of

2.7%. The upside surprise was driven by 2 factors: 1) domestic fuel price increases, and 2)

food prices due to bad weather and also lagged impact of cooking oil subsidy removals.

In March 2017, Bank Negara Malaysia (“BNM”) released the 2016 Annual Report where

the central bank projected Malaysia’s GDP to grow at 4.3% - 4.8% for 2017. The higher

growth projection is based on a rebound in exports as well as resilient domestic demand.

Inflation, however, is expected to spike upwards to 3% - 4% (2016: 2.1%) due mainly to

cost-driven factors i.e. pass-through impact from an elevated retail oil prices. In the same

report, BNM also projects Malaysia’s current account surplus to remain positive at

RM17.4b (2016: RM25.2b). Meanwhile, as at end 2016, the top five Foreign Direct

Investments (“FDI”) contributor was Singapore (RM115b), Japan (RM70b), China & HK

(RM53b), Netherlands (RM48b) and United States (RM36b). In 2016, out of the

RM207.9b approved investments, the Services sector command 68% while the

Manufacturing sector command a lower share of 28%. The bulk of investments in the

Manufacturing sector came from Petroleum Products, E&E Products, Basic Metal

9

Products and Transport Equipment while the usual Real Estate, Financial Services,

Utilities and Distributive Trade dominate the Services Sector. Finally, the banking

sector’s loan growth for February slipped slightly to 5.3% YoY from 5.6% YoY in the

previous month. The moderation in February’s loan growth was caused by a slower

Household loan growth of +5.1% whilst business loan was unchanged at 5.4%.

Market

Outlook

The US Federal Open Market Committee (“FOMC”) March rate hike was fully expected

by most investors but more importantly, the dovish guidance that accompanied the FOMC

statement was welcomed by all, especially Emerging Markets investors. With the FOMC

decision out of the way, investors’ attention is now tuned to how President Trump and his

team will maneuver all the election promises made last November starting with its China

policy.

Meanwhile, the rise in inflation outlook globally as well as in Malaysia is very much in

focus. Bank Negara Malaysia (“BNM”) has guided for 2017 headline inflation Consumer

Price Index (“CPI”) to fall within 3.0% - 4.0% in its latest Annual Report. We note that

the forecast is significantly higher than the 2.1% recorded for the whole of 2016. What is

more pertinent however is whether the recent surge in Malaysia’s CPI (Feb: 4.5%)

portends a potential change in BNM’s monetary policy given the current negative real rate

environment.

We do not think so, at least not in the next six months. The reason for the surge in the CPI

can be attributed to the lower base in prior year as well as the multiple price hikes in

petrol pump prices via RON95, RON97 and Diesel. In other words, Malaysia’s headline

inflation is largely cost-push and not demand-driven. In fact, core inflation remains below

3.0% (Feb: 2.5%) and BNM has acknowledged as much in its recent Monetary Policy

Index (“MPC”) statement stating that “the cost-driven inflation is not expected to have a

significant impact on the broader price trends given the stable domestic demand

conditions. Core inflation is expected to increase modestly.”

Given the above and based on BNM’s actions in the past, we opine that the current higher

inflation pressures are unlikely to trigger an Overnight Policy Rate (“OPR”) hike, given

lingering growth risks, and the absence of strong demand conditions leading to second-

round effects on domestic inflation.

Kuala Lumpur, Malaysia

AmFunds Management Berhad

8 May 2017

Independent auditors’ report to the unitholders of

AmIncome

Report on the financial statements

Opinion

Basis for opinion

Independence and other ethical responsibilities

Information other than the financial statements and auditors’ report thereon

We have audited the financial statements of AmIncome (“the Fund”), which comprise the statement

of financial position as at 31 March 2017, and the statement of comprehensive income, statement of

changes in equity and statement of cash flows for the year then ended, and notes to the financial

statements, including a summary of significant accounting policies, as set out on pages 13 to 42.

In our opinion, the accompanying financial statements give a true and fair view of the financial

position of the Fund as at 31 March 2017, and of its financial performance and its cash flows for the

year then ended in accordance with Malaysian Financial Reporting Standards and International

Financial Reporting Standards.

We conducted our audit in accordance with approved standards on auditing in Malaysia and

International Standards on Auditing. Our responsibilities under those standards are further described

in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We

believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for

our opinion.

We are independent of the Fund in accordance with the By-Laws (on Professional Ethics, Conduct

and Practice) of the Malaysian Institute of Accountants (“By-Laws”) and the International Ethics

Standards Board for Accountants’ Code of Ethics for Professional Accountants (“IESBA Code”),

and we have fulfilled our other ethical responsibilities in accordance with the By-Laws and the

IESBA Code.

The Manager is responsible for the other information. The other information comprises information

in the Annual Report, but does not include the financial statements of the Fund and our auditors’

report thereon.

Our opinion on the financial statements of the Fund does not cover the other information and we do

not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements of the Fund, our responsibility is to read the

other information and, in doing so, consider whether the other information is materially inconsistent

with the financial statements of the Fund or our knowledge obtained in the audit or otherwise

appears to be materially misstated.

10

Independent auditors’ report to the unitholders of

AmIncome (cont’d.)

Responsibilities of the Manager and the Trustees for the financial statements

Auditor’s responsibilities for the audit of the financial statements

Identify and assess the risks of material misstatement of the financial statements of the Fund,

whether due to fraud or error, design and perform audit procedures responsive to those risks,

and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.

The risk of not detecting a material misstatement resulting from fraud is higher than for one

resulting from error, as fraud may involve collusion, forgery, intentional omissions,

misrepresentations, or the override of internal control.

If based on the work we have performed, we conclude that there is a material misstatement of this

other information, we are required to report that fact. We have nothing to report in this regard.

The Manager is responsible for the preparation of the financial statements of the Fund that give a

true and fair view in accordance with Malaysian Financial Reporting Standards and International

Financial Reporting Standards. The Manager is also responsible for such internal control as the

Manager determines is necessary to enable the preparation of financial statements of the Fund that

are free from material misstatement, whether due to fraud or error.

In preparing the financial statements of the Fund, the Manager is responsible for assessing the

Fund’s ability to continue as a going concern, disclosing, as applicable, matters related to going

concern and using the going concern basis of accounting unless the Manager either intends to

liquidate the Fund or to cease operations, or has no realistic alternative to do so.

The Trustee is responsible for ensuring that the Manager maintains proper accounting and other

records as are necessary to enable true and fair presentation of these financial statements.

Our objectives are to obtain reasonable assurance about whether the financial statements of the Fund,

as a whole are free from material misstatement, whether due to fraud or error, and to issue an

auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is

not a guarantee that an audit conducted in accordance approved standards on auditing in Malaysia

and International Standards on Auditing will always detect a material misstatement when it exists.

Misstatements can arise from fraud or error and are considered material if, individually or in the

aggregate, they could reasonably be expected to influence the economic decisions of users taken on

the basis of these financial statements.

As part of an audit in accordance with the approved standards on auditing in Malaysia and

International Standards on Auditing, we exercise professional judgment and maintain professional

skepticism throughout the planning and performance of the audit. We also:

Obtain an understanding of internal control relevant to the audit in order to design audit

procedures that are appropriate in the circumstances, but not for the purpose of expressing an

opinion on the effectiveness of the Fund’s internal control.

11

Independent auditors’ report to the unitholders of

AmIncome (cont’d.)

Other matters

Ernst & Young Wan Daneena Liza Bt Wan Abdul Rahman

AF: 0039 No. 2978/03/18(J)

Chartered Accountants Chartered Accountant

Kuala Lumpur, Malaysia

8 May 2017

This report is made solely to the unitholders of the Fund, as a body, and for no other purpose. We do

not assume responsibility to any other person for the content of this report.

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting

estimates and related disclosures made by the Manager.

Conclude on the appropriateness of the Manager’s use of the going concern basis of

accounting and, based on the audit evidence obtained, whether a material uncertainty exists

related to events or conditions that may cast significant doubt on the Fund’s ability to

continue as a going concern. If we conclude that a material uncertainty exists, we are required

to draw attention in our auditors’ report to the related disclosures in the financial statements

or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the

audit evidence obtained up to the date of our auditors’ report. However, future events or

conditions may cause the Fund to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the financial statements of the

Fund, including the disclosures, and whether the financial statements of the Fund represent

the underlying transactions and events in a manner that achieves fair presentation.

We communicate with the Manager regarding, among other matters, the planned scope and timing of

the audit and significant audit findings, including any significant deficiencies in internal control that

we identify during our audit.

12

AmIncome

STATEMENT OF FINANCIAL POSITION

AS AT 31 MARCH 2017

2017 2016

Note RM RM

ASSETS

Investments 4 1,714,169,503 1,955,623,906

Deposits with financial institutions 5 2,022,803,222 1,910,736,315

Cash at banks 7,829,193 89,821,466

TOTAL ASSETS 3,744,801,918 3,956,181,687

LIABILITIES

Amount due to Manager 6 2,778,286 2,516,441

Amount due to Trustee 7 162,372 167,763

Distributions payable and to be reinvested 9,979,399 10,660,138

Sundry payables and accrued expenses 215,007 178,162

TOTAL LIABILITIES 13,135,064 13,522,504

EQUITY

Unitholders’ capital 9(a) 3,679,770,549 3,893,537,176

Accumulated losses 9(b) (152) (5,295)

Available-for-sale reserve 9(c) 1,830,452 1,424,586

Capital reserve 11 50,066,005 47,702,716

TOTAL EQUITY 9 3,731,666,854 3,942,659,183

TOTAL EQUITY AND LIABILITIES 3,744,801,918 3,956,181,687

UNITS IN CIRCULATION 9(a) 3,679,770,549 3,893,537,176

NET ASSET VALUE PER UNIT

− EX DISTRIBUTION 100.00 sen 100.00 sen

The accompanying notes form an integral part of the financial statements.

13

AmIncome

STATEMENT OF COMPREHENSIVE INCOME

FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017

2017 2016

Note RM RM

INVESTMENT INCOME

Interest income 154,127,648 166,851,982

Other income 71,983 174,782

Net gain from investments:

− Gain on disposals of available-for-sale investments 388,716 111,086

Gross Income 154,588,347 167,137,850

EXPENDITURE

Manager’s fee 6 (28,936,880) (31,424,275)

Trustee’s fee 7 (1,929,125) (2,094,952)

Auditors’ remuneration (11,000) (12,000)

Tax agent’s fee (4,000) (4,000)

Other expenses 8 (1,891,139) (2,055,271)

Total Expenditure (32,772,144) (35,590,498)

NET INCOME BEFORE TAX 121,816,203 131,547,352

LESS: INCOME TAX 13 - -

NET INCOME AFTER TAX 121,816,203 131,547,352

OTHER COMPREHENSIVE INCOME THAT MAY BE

RECLASSIFIED TO PROFIT OR LOSS IN

SUBSEQUENT PERIODS:

− Fair value revaluation gain 794,582 2,376,322

− Reclassification of gain on financial investments

available-for-sale to profit or loss, net (388,716) (111,086)

TOTAL COMPREHENSIVE INCOME FOR THE

FINANCIAL YEAR 122,222,069 133,812,588

Total comprehensive income comprises the following:

Realised income 121,816,203 131,547,352

Unrealised gain 405,866 2,265,236

122,222,069 133,812,588

Distributions for the financial year:

Gross/net distributions 14 119,447,771 129,199,537

The accompanying notes form an integral part of the financial statements.

14

AmIncome

STATEMENT OF CHANGES IN EQUITY

FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017

Retained Available-

earnings/ for-sale

Unitholders’ (accumulated (deficit)/ Capital Total

capital losses) reserve reserve equity

Note RM RM RM RM RM

At 1 April 2015 4,266,090,477 1,830 (840,650) 45,347,776 4,310,599,433

Total comprehensive income

for the financial year - 131,547,352 2,265,236 - 133,812,588

Transfer to capital

reserve 11 - (2,354,940) - 2,354,940 -

Creation of units 9(a) 6,079,351,082 - - - 6,079,351,082

Reinvestments of

distributions 9(a) 125,624,005 - - - 125,624,005

Cancellation of units 9(a) (6,577,528,388) - - - (6,577,528,388)

Distributions 14 - (129,199,537) - - (129,199,537)

Balance at 31 March 2016 3,893,537,176 (5,295) 1,424,586 47,702,716 3,942,659,183

At 1 April 2016 3,893,537,176 (5,295) 1,424,586 47,702,716 3,942,659,183

Total comprehensive income

for the financial year - 121,816,203 405,866 - 122,222,069

Transfer to capital

reserve 11 - (2,363,289) - 2,363,289 -

Creation of units 9(a) 4,272,531,144 - - - 4,272,531,144

Reinvestments of

distributions 9(a) 117,071,096 - - - 117,071,096

Cancellation of units 9(a) (4,603,368,867) - - - (4,603,368,867)

Distributions 14 - (119,447,771) - - (119,447,771)

Balance at 31 March 2017 3,679,770,549 (152) 1,830,452 50,066,005 3,731,666,854

The accompanying notes form an integral part of the financial statements.

15

AmIncome

STATEMENT OF CASH FLOWS

FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017

2017 2016

RM RM

CASH FLOWS FROM OPERATING AND

INVESTING ACTIVITIES

Proceeds from maturity/sale of investments 891,198,130 3,043,047,673

Interest received 172,651,170 189,964,858

Other income received 71,983 174,782

Manager’s fee paid (28,675,035) (31,687,270)

Trustee’s fee paid (1,934,516) (2,112,485)

Tax agent’s fee paid (4,000) (4,000)

Payments for other expenses (1,865,294) (1,906,672)

Purchase of investments (1,072,910,476) (1,228,314,153)

Net cash (used in)/generated from operating and

investing activities (41,468,038) 1,969,162,733

CASH FLOWS FROM FINANCING

ACTIVITIES

Proceeds from creation of units 4,272,531,144 6,079,351,082

Payment for cancellation of units (4,603,368,867) (6,577,528,388)

Distributions paid (3,057,414) (4,463,701)

Net cash used in financing activities (333,895,137) (502,641,007)

NET (DECREASE)/INCREASE IN CASH AND

CASH EQUIVALENTS (375,363,175) 1,466,521,726

CASH AND CASH EQUIVALENTS AT

BEGINNING OF FINANCIAL YEAR 1,899,699,699 433,177,973

CASH AND CASH EQUIVALENTS AT

END OF FINANCIAL YEAR 1,524,336,524 1,899,699,699

Cash and cash equivalents comprise:

Deposits with financial institutions 1,516,507,331 1,809,878,233

Cash at banks 7,829,193 89,821,466

1,524,336,524 1,899,699,699

The accompanying notes form an integral part of the financial statements.

16

AmIncome

NOTES TO THE FINANCIAL STATEMENTS

1. GENERAL INFORMATION

2. BASIS OF PREPARATION OF FINANCIAL STATEMENTS

Standards effective during the financial year

Standards issued but not yet effective

MFRS 9: Financial Instruments

MFRS 15: Revenue From Contracts With Customers

AmIncome (“the Fund”) was established pursuant to a Deed dated 17 January 2000 as amended by Deeds

Supplemental thereto (“the Deed”), between AmFunds Management Berhad as the Manager, HSBC (Malaysia)

Trustee Berhad as the Trustee and all unitholders.

The Fund was set up with the objective of providing investors with a high stream of income returns. As

provided in the Deed, the “accrual period” or financial year shall end on 31 March and units in the Fund were

first offered for sale on 20 January 2000.

financial periods

The financial statements of the Fund have been prepared under the historical cost convention, unless otherwise

stated in the accounting policies.

The adoption of MFRS which have been effective during the financial year did not have any material financial

impact to the financial statements.

As at the date of authorisation of these financial statements, the following Standards, which are relevant to the

Fund, have been issued by MASB but are not yet effective and have not been adopted by the Fund.

1 January 2018

The financial statements of the Fund have been prepared in accordance with Malaysian Financial Reporting

Standards (“MFRS”) as issued by the Malaysian Accounting Standards Board (“MASB”) and are in

compliance with International Financial Reporting Standards.

beginning on or after

1 January 2018

Effective for

The Fund plans to adopt the above pronouncements when they become effective in the respective financial

periods. These pronouncements are expected to have no significant impact to the financial statements of the

Fund upon their initial application except as described below:

17

MFRS 9 Financial Instruments

3. SIGNIFICANT ACCOUNTING POLICIES

Income recognition

Income tax

Functional and presentation currency

Statement of cash flows

Distribution

Current taxes are recognised in profit or loss except to the extent that the tax relates to items recognised outside

profit or loss, either in other comprehensive income or directly in equity.

Distributions are at the discretion of the Fund. A distribution to the Fund’s unitholders is accounted for as a

deduction from realised reserves. A proposed distribution is recognised as a liability in the period in which it is

approved.

Functional currency is the currency of the primary economic environment in which the Fund operates that most

faithfully represents the economic effects of the underlying transactions. The functional currency of the Fund is

Ringgit Malaysia which reflects the currency in which the Fund competes for funds, issues and redeems units.

The Fund has also adopted Ringgit Malaysia as its presentation currency.

The Fund adopts the direct method in the preparation of the statement of cash flows.

Cash equivalents are short-term, highly liquid investments that are readily convertible to cash with insignificant

risk of changes in value.

Income is recognised to the extent that it is probable that the economic benefits will flow to the Fund and the

income can be reliably measured. Income is measured at the fair value of consideration received or receivable.

Interest income on fixed income securities and short-term deposits are recognised on an accrual basis using the

effective interest method, which includes the accretion of discounts and amortisation of premiums.

Current tax assets and liabilities are measured at the amount expected to be recovered from or paid to the tax

authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively

enacted at the reporting date.

MFRS 9 reflects International Accounting Standards Board’s (“IASB”) work on the replacement of MFRS 139

Financial Instruments: Recognition and Measurement (“MFRS 139”). MFRS 9 will be effective for financial

year beginning on or after 1 January 2018. The Fund is in the process of quantifying the impact of the first

adoption of MFRS 9.

18

Unitholders’ capital

Capital reserve

Financial assets

(i) Available-for-sale investments

(ii) Loans and receivables

The Fund determines the classification of its financial assets at initial recognition, and the categories applicable

to the Fund include available-for-sale investments and loans and receivables.

Capital reserve of the Fund represents non-distributable amount as determined by the Manager that may be

applied to make good any losses incurred by the Fund, in order to maintain the Fund’s prices at RM1.00 per

unit, as approved by the Securities Commission.

Financial assets are recognised in the statement of financial position when, and only when, the Fund becomes a

party to the contractual provisions of the financial instrument.

The unitholders’ capital of the Fund meets the definition of puttable instruments and is classified as equity

instruments under MFRS 132 Financial Instruments: Presentation (“MFRS 132”).

When financial assets are recognised initially, they are measured at fair value, plus, in the case of financial

assets not at fair value through profit or loss, directly attributable transaction costs.

Subsequent to initial recognition, loans and receivables are measured at amortised cost using the effective

interest method. Gains and losses are recognised in profit or loss when the loans and receivables are

derecognised or impaired, and through the amortisation process.

Financial assets with fixed or determinable payments that are not quoted in an active market are classified

as loans and receivables.

Available-for-sale investments are measured at fair value. Any gains or losses from changes in fair value of

the investments are recognised in other comprehensive income, except that impairment losses, foreign

exchange gains and losses on monetary instruments and interest calculated using the effective interest

method are recognised in profit or loss. The cumulative gain or loss previously recognised in other

comprehensive income is reclassified from equity to profit or loss as a reclassification adjustment when the

investment is derecognised.

For investments in fixed income securities, fair value is determined based on the indicative prices from

Bond Pricing Agency Malaysia Sdn Bhd plus accrued interest, which includes the accretion of discount and

amortisation of premium.

19

Impairment of available-for-sale

Impairment of loans and receivables

Financial liabilities

The Fund assesses at each reporting date whether there is any objective evidence that a financial asset is

impaired.

To determine whether there is objective evidence that an impairment loss on financial assets has been incurred,

the Fund considers factors such as the probability of insolvency or significant financial difficulties of the debtor

and default or significant delay in payments.

If any such evidence exists, the amount of impairment loss is measured as the difference between the assets’s

carrying amount and the present value of estimated future cash flows discounted at the financial asset’s original

effective interest rate. The impairment loss is recognised in profit or loss.

The carrying amount of the financial asset is reduced through the use of an allowance account. When loans and

receivables become uncollectible, they are written off against the allowance account.

If in a subsequent period, the amount of the impairment loss decreases and the decrease can be related

objectively to an event occurring after the impairment was recognised, the previously recognised impairment

loss is reversed to the extent that the carrying amount of the asset does not exceed its amortised cost at the

reversal date. The amount of reversal is recognised in profit or loss.

For financial investments AFS, the Fund assesses at each reporting date whether there is objective evidence that

an investment is impaired. The amount of any impairment loss identified is measured as the difference between

the asset’s carrying amount and the present value of estimated future cash flows (excluding future expected

credit losses that have not yet been incurred). The present value of the estimated future cash flows is discounted

at the financial asset’s original effective interest rate. However, the amount recorded for impairment is the

cumulative loss measured as the difference between the amortised cost and the current fair value, less any

impairment loss on that investment previously recognised in profit or loss.

If, in a subsequent year, the fair value of a debt instrument increases and the increase can be objectively related

to an event occurring after the impairment loss was recognised in the profit or loss, the impairment loss is

reversed through the profit or loss.

Financial liabilities are classified according to the substance of the contractual arrangements entered into and

the definitions of a financial liability.

Financial liabilities, within the scope of MFRS 139, are recognised in the statement of financial position when,

and only when, the Fund becomes a party to the contractual provisions of the financial instrument.

The Fund’s financial liabilities are recognised initially at fair value plus directly attributable transaction costs

and subsequently measured at amortised cost using the effective interest method.

20

Classification of realised gains and losses

Significant accounting estimates and judgments

4. INVESTMENTS

2017 2016

Available-for-sale investments RM RM

At nominal value:

Quasi-Government Bonds 28,000,000 -

Corporate bonds 1,634,888,000 1,900,188,000

Malaysian Government Securities 10,000,000 -

1,672,888,000 1,900,188,000

At amortised cost:

Quasi-Government Bonds 28,298,052 -

Corporate bonds 1,673,959,438 1,954,199,320

Malaysian Government Securities 10,081,561 -

1,712,339,051 1,954,199,320

At fair value:

Quasi-Government Bonds 28,324,646 -

Corporate bonds 1,675,701,280 1,955,623,906

Malaysian Government Securities 10,143,577 -

1,714,169,503 1,955,623,906

No major judgments have been made by the Manager in applying the Fund’s accounting policies. There are no

key assumptions concerning the future and other key sources of estimation uncertainty at the reporting date,

that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities

within the next financial year.

The preparation of the Fund’s financial statements requires the Manager to make judgments, estimates and

assumptions that affect the reported amounts of revenues, expenses, assets and liabilities, and the disclosure of

contingent liabilities at the reporting date. However, uncertainty about these assumptions and estimates could

result in outcomes that could require a material adjustment to the carrying amount of the asset or liability in the

future.

Realised gains and losses on disposals of financial instruments are calculated using the weighted average

method. They represent the difference between an instrument’s initial carrying amount and disposal amount.

21

Details of investments as at 31 March 2017 are as follows:

Carrying

value as a

percentage

Maturity Credit Nominal Fair Amortised of net asset

date Issuer rating value value cost value

RM RM RM %

Quasi-Government Bonds

09.06.2017 Pengurusan Air

SPV Berhad NR 10,000,000 10,125,811 10,115,983 0.27

16.06.2017 Pengurusan Air

SPV Berhad NR 15,000,000 15,181,818 15,165,988 0.41

25.08.2017 Malaysia Debt

Ventures Berhad NR 3,000,000 3,017,017 3,016,081 0.08

28,000,000 28,324,646 28,298,052 0.76

Corporate bonds

03.05.2017 ADCB Finance

(Cayman)

Limited AAA 10,000,000 10,173,834 10,173,569 0.27

12.05.2017 Jimah Energy

Ventures

Sdn Bhd AA 25,000,000 25,927,748 25,924,510 0.70

29.05.2017 TNB Northern

Energy

Berhad AAA 5,000,000 5,057,265 5,056,495 0.14

28.06.2017 Mukah Power

Generation

Sdn Bhd AA 1,000,000 1,028,446 1,027,967 0.03

28.06.2017 UMW Holdings

Berhad AA 15,000,000 15,133,071 15,149,322 0.41

30.06.2017 Sports Toto

Malaysia

Sdn Bhd AA 1,900,000 1,937,194 1,935,206 0.05

03.08.2017 Public Bank

Berhad AA 45,000,000 45,355,673 45,340,573 1.22

08.08.2017 Sabah

Development

Bank Berhad AA 20,000,000 20,096,847 20,096,176 0.54

15.08.2017 OCBC Bank

(Malaysia)

Berhad AA 10,000,000 10,049,815 10,037,032 0.27

29.08.2017 Celcom Networks

Sdn Bhd AA 50,000,000 50,017,808 50,080,185 1.34

(Forward)

22

Carrying

value as a

percentage

Maturity Credit Nominal Fair Amortised of net asset

date Issuer rating value value cost value

RM RM RM %

Corporate bonds

06.09.2017 AmBank Islamic

Berhad* AA 13,000,000 13,050,146 13,035,119 0.35

18.09.2017 CIMB Islamic

Bank Berhad AA 20,000,000 20,015,774 20,026,374 0.54

20.09.2017 AmBank Islamic

Berhad* AA 20,000,000 20,051,474 20,039,540 0.54

10.11.2017 Jimah Energy

Ventures

Sdn Bhd AA 9,000,000 9,526,096 9,519,877 0.25

22.11.2017 ADCB Finance

(Cayman)

Limited AAA 131,038,000 134,197,954 134,352,136 3.60

24.11.2017 Manjung Island

Energy Berhad AAA 5,000,000 5,071,669 5,078,471 0.14

30.11.2017 CIMB Bank

Berhad AA 235,000,000 238,341,990 238,445,173 6.39

30.11.2017 RHB Bank Berhad AA 22,000,000 22,376,744 22,366,797 0.60

08.12.2017 Malaysia

Building

Society Berhad AA 35,000,000 35,404,686 35,415,055 0.95

25.01.2018 Putrajaya Holdings

Sdn Bhd AAA 8,000,000 8,153,062 8,144,726 0.22

31.01.2018 Mecuro Properties

Sdn Bhd AAA 10,000,000 10,067,541 10,075,873 0.27

12.03.2018 The Export-Import

Bank of Korea

Berhad AAA 10,000,000 10,070,525 10,058,041 0.27

11.05.2018 Jimah Energy

Ventures

Sdn Bhd AA 43,000,000 46,447,377 46,378,158 1.24

22.06.2018 Sarawak Energy

Berhad AA 15,000,000 15,298,169 15,277,056 0.41

27.07.2018 Besraya (M)

Sdn Bhd AA 7,300,000 7,378,806 7,370,564 0.20

24.08.2018 YTL Power

International

Berhad AA 70,000,000 70,434,201 70,386,261 1.89

25.09.2018 Malayan Banking

Berhad AA 30,000,000 30,637,590 30,682,466 0.82

(Forward)

23

Carrying

value as a

percentage

Maturity Credit Nominal Fair Amortised of net asset

date Issuer rating value value cost value

RM RM RM %

Corporate bonds

05.10.2018 CIMB Bank

Berhad AA 43,000,000 45,606,955 45,553,171 1.22

12.11.2018 Jimah Energy

Ventures

Sdn Bhd AA 12,000,000 13,168,838 13,138,526 0.35

30.11.2018 Hong Leong

Financial

Group Berhad AA 5,000,000 5,073,323 5,067,918 0.14

10.12.2018 Malaysia

Building

Society Berhad AA 60,000,000 60,615,625 60,683,978 1.62

27.12.2018 BGSM

Management

Sdn Bhd AA 7,100,000 7,249,094 7,218,660 0.19

25.02.2019 Media Chinese

International

Limited AA 5,000,000 5,046,599 5,039,644 0.13

29.03.2019 RHB Bank Berhad A 57,800,000 61,404,361 61,241,209 1.64

17.04.2019 OCBC Bank

(Malaysia)

Berhad AA 20,000,000 21,388,973 21,313,065 0.57

15.05.2019 RHB Islamic Bank

Berhad AA 25,000,000 25,655,486 25,605,911 0.69

30.05.2019 Etiqa Takaful

Berhad AA 40,800,000 41,457,612 41,511,975 1.11

05.06.2019 PBFIN Berhad AA 44,200,000 47,821,354 47,560,793 1.28

25.06.2019 YTL Corporation

Berhad AA 5,000,000 5,078,145 5,053,768 0.14

28.06.2019 TF Varlik

Kiralama A.S. AA 18,000,000 18,307,499 18,341,077 0.49

18.07.2019 Sabah

Development

Bank Berhad AA 60,000,000 61,008,600 60,611,013 1.63

08.08.2019 AMMB Holdings

Berhad AA 25,000,000 25,030,024 24,915,125 0.67

09.08.2019 Sarawak Hidro

Sdn Bhd AAA 30,000,000 30,104,770 30,192,345 0.81

16.08.2019 Sabah

Development

Bank Berhad AA 45,000,000 45,207,376 45,262,853 1.21

(Forward)

24

Carrying

value as a

percentage

Maturity Credit Nominal Fair Amortised of net asset

date Issuer rating value value cost value

RM RM RM %

Corporate bonds

21.08.2019 Sabah

Development

Bank Berhad AA 26,200,000 26,317,308 26,350,162 0.70

29.08.2019 Celcom Networks

Sdn Bhd AA 15,000,000 14,779,165 15,039,612 0.40

08.11.2019 GB Services

Berhad AAA 20,000,000 20,746,288 20,780,867 0.56

25.11.2019 Manjung Island

Energy Berhad AAA 10,000,000 10,147,158 10,121,955 0.27

17.12.2019 RHB Bank

Berhad A 27,350,000 29,145,745 29,072,884 0.78

27.12.2019 BGSM

Management

Sdn Bhd AA 57,500,000 61,429,968 60,691,969 1.65

03.04.2020 CIMB Group

Holdings

Berhad AA 5,000,000 5,361,486 5,348,883 0.14

09.04.2020 Danga Capital

Berhad AAA 20,000,000 20,348,658 20,388,658 0.54

29.04.2020 RHB Bank Berhad AA 4,700,000 4,937,306 4,924,460 0.13

06.07.2020 Krung Thai Bank

Public

Company

Limited AA 10,000,000 10,290,867 10,302,453 0.27

03.12.2020 Rantau Abang

Capital Berhad AAA 40,000,000 40,700,457 40,563,414 1.09

21.12.2020 AmBank Islamic

Berhad* AA 20,000,000 20,618,594 20,295,994 0.55

23.06.2021 Sarawak Energy

Berhad AA 5,000,000 5,216,492 5,183,453 0.14

08.10.2021 Kesas Sdn Bhd AA 5,000,000 5,135,649 5,110,921 0.14

1,634,888,000 1,675,701,280 1,673,959,438 44.90

25

Carrying

value as a

percentage

Maturity Credit Nominal Fair Amortised of net asset

date Issuer rating value value cost value

RM RM RM %

Malaysian Government Securities

07.02.2018 Government

of Malaysia NR 10,000,000 10,143,577 10,081,561 0.27

Total investments 1,672,888,000 1,714,169,503 1,712,339,051 45.93

Excess of fair value over cost 1,830,452

* A licensed financial institution related to the Manager.

The weighted average effective yield on unquoted investments are as follows:

2017 2016

% %

Quasi-Government Bonds 3.53 -

Corporate bonds 4.42 4.31

Malaysian Government Securities 3.26 -

Less than 1 year to

1 year 5 years

RM RM

At nominal value:

Quasi-Government Bonds 28,000,000 -

Corporate bonds 700,938,000 933,950,000

Malaysian Government Securities 10,000,000 -

At nominal value:

Corporate bonds 711,900,000 1,188,288,000

Effective yield

2017

2016

Analyses of the remaining maturity of unquoted investments as at 31 March 2017 and 31 March 2016 are as

follows:

26

5. DEPOSITS WITH FINANCIAL INSTITUTIONS

2017 2016

RM RM

At nominal value:

Fixed deposits with a licensed bank 500,000,000 100,000,000

Short-term deposits with licensed banks/Islamic banks/

investment banks (tenure 7 days or less) 414,000,000 370,000,000

Short-term deposits with licensed banks/Islamic banks/

investment banks (more than 7 days) 1,100,000,000 1,436,000,000

2,014,000,000 1,906,000,000

At carrying value:

Fixed deposits with a licensed bank 506,295,891 100,858,082

Short-term deposits with licensed banks/Islamic banks/

investment banks (tenure 7 days or less) 414,057,496 370,046,397

Short-term deposits with licensed banks/Islamic banks/

investment banks (more than 7 days) 1,102,449,835 1,439,831,836

2,022,803,222 1,910,736,315

Details of deposits with financial institutions as at 31 March 2017 are as follows:

Carrying

value as a

percentage

Maturity Nominal Carrying Purchase of net asset

date value value cost value

RM RM RM %

Fixed deposit with a licensed bank

05.04.2017 RHB Bank 50,000,000 50,441,781 50,000,000 1.35

25.04.2017 Hong Leong

Bank Berhad 50,000,000 50,352,603 50,000,000 1.35

26.04.2017 AmBank Berhad* 100,000,000 100,694,521 100,000,000 2.70

12.07.2017 Sumitomo Mitsui

Banking

Corporation

Malaysia Berhad 150,000,000 153,718,356 150,000,000 4.12

26.07.2017 AmBank Berhad* 100,000,000 100,703,425 100,000,000 2.70

450,000,000 455,910,686 450,000,000 12.22

Fixed deposit with a licensed investment bank

17.04.2017

Bank Berhad 50,000,000 50,385,205 50,000,000 1.35

Total fixed deposit 500,000,000 506,295,891 500,000,000 13.57

Affin Hwang Investment

Bank

27

Carrying

value as a

percentage

Maturity Nominal Carrying Purchase of net asset

date value value cost value

RM RM RM %

Short-term deposits with licensed banks (tenure: 7 days or less)

03.04.2017 AmBank Berhad* 84,000,000 84,007,825 84,000,000 2.25

03.04.2017 Malayan Banking

Berhad 100,000,000 100,009,178 100,000,000 2.68

03.04.2017 National Bank Of

Abu Dhabi

Malaysia Berhad 60,000,000 60,011,178 60,000,000 1.61

03.04.2017 Public Bank Berhad 100,000,000 100,009,315 100,000,000 2.68

344,000,000 344,037,496 344,000,000 9.22

Short-term deposit with a licensed investment bank (tenure: 7 days or less)

04.04.2017 Hong Leong Investment

Bank 30,000,000 30,012,000 30,000,000 0.81

06.04.2017 Kaf Investment Bank

Berhad 40,000,000 40,008,000 40,000,000 1.07

70,000,000 70,020,000 70,000,000 1.88

Total short-term deposits

(tenure: 7 days or less) 414,000,000 414,057,496 414,000,000 11.10

Short-term deposits with licensed banks (tenure: more than 7 days)

03.04.2017 United Overseas Bank

(Malaysia) Bhd. 50,000,000 50,143,014 50,000,000 1.34

04.04.2017 Hong Leong Bank

Berhad 50,000,000 50,055,000 50,000,000 1.34

05.04.2017 RHB Bank Berhad 80,000,000 80,134,137 80,000,000 2.15

17.04.2017 United Overseas Bank

(Malaysia) Bhd. 50,000,000 50,208,219 50,000,000 1.35

20.04.2017 United Overseas Bank

(Malaysia) Bhd. 100,000,000 100,416,438 100,000,000 2.69

21.04.2017 United Overseas Bank

(Malaysia) Bhd. 50,000,000 50,203,014 50,000,000 1.34

28.04.2017 AmBank (M)

Berhad* 100,000,000 100,010,137 100,000,000 2.68

31.05.2017 AmBank (M)

Berhad* 100,000,000 100,010,411 100,000,000 2.68

580,000,000 581,180,370 580,000,000 15.57

Bank

28

Carrying

value as a

percentage

Maturity Nominal Carrying Purchase of net asset

date value value cost value

RM RM RM %

Short-term deposits with licensed investment banks (tenure: more than 7 days)

03.04.2017

Bank Berhad 100,000,000 100,177,534 100,000,000 2.69

03.04.2017

Berhad 40,000,000 40,086,795 40,000,000 1.07

06.04.2017

Bank Berhad 50,000,000 50,126,438 50,000,000 1.34

07.04.2017

Berhad 50,000,000 50,015,205 50,000,000 1.34

17.04.2017

Bank Berhad 30,000,000 30,044,384 30,000,000 0.81

24.04.2017

Bank Berhad 50,000,000 50,050,000 50,000,000 1.34

320,000,000 320,500,356 320,000,000 8.59

Short-term deposits with licensed Islamic banks (tenure: more than 7 days)

03.04.2017 Hong Leong Islamic

Bank Berhad 50,000,000 50,088,767 50,000,000 1.34

17.05.2017 Bank Islam Malaysia

Berhad 150,000,000 150,680,342 150,000,000 4.04

200,000,000 200,769,109 200,000,000 5.38

Total short-term deposits

(tenure: more than 7 days) 1,100,000,000 1,102,449,835 1,100,000,000 29.54

Total deposits with financial

institutions 2,014,000,000 2,022,803,222 2,014,000,000 54.21

* A licensed bank related to the Manager.

Public Investment Bank

Affin Hwang Investment

Affin Hwang Investment

Bank

Affin Hwang Investment

KAF Investment Bank

Affin Hwang Investment

The weighted average effective interest rate and average remaining maturity of short-term deposits are as

follows:

29

2017 2016 2017 2016

% % Days Days

Fixed deposits with a licensed bank 3.89 4.35 49 20

Short-term deposits with licensed

banks/ investment banks/ Islamic

banks (tenure: 7 days or less) 3.43 3.48 4 4

Short-term deposits with licensed

banks/ investment banks/ Islamic

banks (tenure: more than 7 days) 3.70 3.97 17 16

6. AMOUNT DUE TO MANAGER

7. AMOUNT DUE TO TRUSTEE

8. OTHER EXPENSES

9. TOTAL EQUITY

Total equity is represented by:

2017 2016

Note RM RM

Unitholders’ capital (a) 3,679,770,549 3,893,537,176

Retained earnings

− Realised loss (b) (152) (5,295)

Available-for-sale reserve (c) 1,830,452 1,424,586

Capital reserve 11 50,066,005 47,702,716

3,731,666,854 3,942,659,183

Weighted average effective

Manager’s fee was charged at a rate of 0.75% (2016: 0.75%) per annum on the net asset value of the Fund,

calculated on a daily basis.

The normal credit period in the previous and current financial years for Manager’s fee payable is one month.

Included in other expenses is Goods and Services Tax incurred by the Fund during the financial year amounting

to RM1,853,641 (2015: RM2,014,409).

Trustee’s fee was charged at a rate of 0.05% (2016: 0.05%) per annum on the net asset value of the Fund,

calculated on a daily basis.

The normal credit period in the previous and current financial years for Trustee’s fee payable is one month.

interest rate

Remaining

maturity

30

(a) UNITHOLDERS’ CAPITAL/UNITS IN CIRCULATION

Number of Number of

units RM units RM

At beginning of the

financial year 3,893,537,176 3,893,537,176 4,266,090,477 4,266,090,477

Creation during the

financial year 4,272,531,144 4,272,531,144 6,079,351,082 6,079,351,082

Distributions reinvested 117,071,096 117,071,096 125,624,005 125,624,005

Cancellation during the

financial year (4,603,368,867) (4,603,368,867) (6,577,528,388) (6,577,528,388)

At end of the financial

year 3,679,770,549 3,679,770,549 3,893,537,176 3,893,537,176

(b) REALISED – DISTRIBUTABLE

2017 2016

RM RM

At beginning of the financial year (5,295) 1,830

Total comprehensive income for the financial year 121,816,203 131,547,352

Transfer to capital reserve (Note 11) (2,363,289) (2,354,940)

Distributions out of realised reserve (Note 14) (119,447,771) (129,199,537)

Net increase/(decrease) in realised reserve for the financial year 5,143 (7,125)

At end of the financial year (152) (5,295)

(c) AVAILABLE-FOR-SALE RESERVE/(DEFICIT)

2017 2016

RM RM

At beginning of the financial year 1,424,586 (840,650)

Fair value revaluation gain 794,582 2,376,322

Reclassification of gain on financial investments

available-for-sale to profit or loss, net (388,716) (111,086)

At end of the financial year 1,830,452 1,424,586

10.NET ASSET VALUE ATTRIBUTABLE TO UNITHOLDERS

In line with the adoption of MFRS 139, unquoted available-for-sale investments have been valued at the

indicative prices at the close of business. However, the valuation, creation and cancellation of units will be

based on RM1.00 per unit as stated in the trust deed.

2017 2016

31

11.CAPITAL RESERVE

2017 2016

RM RM

At beginning of the financial year 47,702,716 45,347,776

Transfer from realised income [Note 9(b)] 2,363,289 2,354,940

At end of the financial year 50,066,005 47,702,716

12.UNITS HELD BY RELATED PARTIES

The related parties of and their relationship with the Fund are as follows:

Related parties Relationship

AmFunds Management Berhad The Manager

AmInvestment Bank Berhad

AMMB Holdings Berhad

Subsidiaries and associates of AMMB Subsidiaries and associate companies of the ultimate

holding

Number of Number of

units RM units RM

Subsidiaries and associates

of AMMB * 536,624,288 536,624,288 472,946,134 472,946,134

*

13.INCOME TAX

2017 2016

RM RM

Net income before tax 121,816,203 131,547,352

(Forward)

Ultimate holding company of the Manager

Holdings company of the Manager

A reconciliation of income tax expense applicable to net income before tax at the statutory income tax rate to

income tax expense at the effective income tax rate of the Fund is as follows:

The parties related to the Manager are the legal and beneficial owners of the units. The Manager did not

hold any units in the Fund as at 31 March 2017 and 31 March 2016.

Pursuant to Schedule 6 of the Income Tax Act, 1967, local interest income derived by the Fund is exempted

from tax.

2017 2016

Income tax payable is calculated on investment income less deduction for permitted expenses as provided for

under Section 63B of the Income Tax Act, 1967.

32

2017 2016

RM RM

Taxation at Malaysian statutory rate of 24% 29,236,000 31,571,400

Tax effects of:

Income not subject to tax (37,084,000) (40,071,100)

Restriction on tax deductible expenses for unit trust fund 6,260,800 6,797,600

Non-permitted expenses for tax purposes 908,900 988,800

Permitted expenses not used and not available for

future financial years 678,300 713,300

Tax expense for the financial year - -

14.DISTRIBUTIONS

2017 2016

RM RM

On redemption of units 1,189,990 857,848

Income entitlement distributed on:

30 April 2016/2015 10,116,511 10,576,521

31 May 2016/2015 10,271,306 10,538,253

30 June 2016/2015 9,842,588 10,084,519

31 July 2016/2015 10,257,374 10,036,755

31 August 2016/2015 10,133,826 10,669,071

30 September 2016/2015 9,801,139 10,344,649

31 October 2016/2015 10,010,891 10,946,304

30 November 2016/2015 9,475,506 11,033,262

31 December 2016/2015 9,639,365 11,924,262

31 January 2017/2016 9,584,177 11,396,833

29 February 2017/28 February 2016 9,145,699 10,131,122

31 March 2017/2016 9,979,399 10,660,138

119,447,771 129,199,537

Distributions to unitholders are from the following sources:

2017 2016

RM RM

Interest income 152,219,915 164,790,035

Less: Expenses (32,772,144) (35,590,498)

Total amount of distributions 119,447,771 129,199,537

Distributions made out of:

Realised reserve [Note 9(b)] 119,447,771 129,199,537

(Forward)

33

2017 2016

RM RM

Comprising:

Distributions reinvested 106,632,889 114,398,748

Distributions to be reinvested 9,845,605 10,438,207

Cash distributions 2,969,277 4,362,582

119,447,771 129,199,537

15.MANAGEMENT EXPENSE RATIO (“MER”)

2017 2016

% p.a. % p.a.

Manager’s fee 0.75 0.75

Trustee’s fee 0.05 0.05

Fund’s other expenses 0.05 0.05

Total MER 0.85 0.85

16.PORTFOLIO TURNOVER RATIO (“PTR”)

17.SEGMENTAL REPORTING

18.TRANSACTIONS WITH THE FINANCIAL INSTITUTIONS

The Fund’s MER is as follows:

The PTR of the Fund, which is the ratio of average total acquisitions and disposals of investments to the

average net asset value of the Fund calculated on a daily basis, is 0.21 times (2016: 0.32 times).

In accordance with the objective of the Fund, substantially all of the Fund’s investments are made in the form

of fixed income securities in Malaysia. The Manager is of the opinion that the risk and rewards from these

investments are not individually or segmentally distinct and hence the Fund does not have a separately

identifiable business or geographical segments.

The gross and net distributions of the Fund are of similar amounts as the Fund is not subject to tax. The above

distributions have no implication on unit prices as the net asset value per unit of the Fund was maintained at

RM1.00 throughout the financial year.

The MER of the Fund is the ratio of the sum of annualised fees and expenses incurred by the Fund to the

average net asset value of the Fund calculated on a daily basis.

Details of transactions with financial institutions for the financial year ended 31 March 2017 are as follows:

34

Financial institutions

RM %

Malayan Banking Berhad 26,209,223,570 28.68

RHB Bank Berhad 17,460,987,000 19.10

CIMB Bank Berhad 14,601,390,117 15.98

Public Bank Berhad 12,088,000,000 13.23

Ambank (M) Berhad* 6,676,145,644 7.30

KAF Investment Bank Berhad 2,710,000,000 2.97

Hong Leong Bank Berhad 2,305,880,975 2.52

Hong Leong Investment Bank Berhad 2,095,924,743 2.29

Kenanga Investment Bank Berhad 1,620,000,000 1.77

Affin Hwang Investment Bank Berhad 1,330,000,000 1.46

Other financial institutions# 4,298,117,769 4.70

Total 91,395,669,818 100.00

*

#

19. FINANCIAL INSTRUMENTS

(a) Classification of financial instruments

Loans and Financial

Available- receivables liabilities at

for-sale at amortised amortised

investments cost cost Total

RM RM RM RM

2017

Assets

Investments 1,714,169,503 - - 1,714,169,503

Deposits with financial

institutions - 2,022,803,222 - 2,022,803,222

(Forward)

The above transactions were in respect of fixed income instruments and money market deposits.

Transactions in these investments do not involve any commission or brokerage.

The significant accounting policies in Note 3 describe how the classes of financial instruments are

measured, and how income and expenses, including fair value gains and losses, are recognised. The

following table analyses the financial assets and liabilities of the Fund in the statement of financial

position by the class of financial instrument to which they are assigned, and therefore by the

measurement basis.

A financial institution related to the Manager. The Manager and the Trustee are of the opinion that the

above transactions have been entered in the normal course of business and have been established under

terms that are no less favourable than those arranged with independent third parties.

Transaction value

Included in the other brokers and financial institutions, there were transactions amounting to

RM50,000,000 with a related party, AmIslamic Bank Berhad. The Manager and the Trustee are of the

opinion that the above transactions have been entered in the normal course of business and have been

established under terms that are no less favourable than those arranged with independent third parties.

35

Loans and Financial

Available- receivables liabilities at

for-sale at amortised amortised

investments cost cost Total

RM RM RM RM

2017AssetsCash at banks - 7,829,193 - 7,829,193

Total financial assets 1,714,169,503 2,030,632,415 - 3,744,801,918

Liabilities

Amount due to Manager - - 2,778,286 2,778,286

Amount due to Trustee - - 162,372 162,372

Distributions to be

reinvested - - 9,979,399 9,979,399

Sundry payables and

accrued expenses - - 215,007 215,007

Total financial liabilities - - 13,135,064 13,135,064

2016

Assets

Investments 1,955,623,906 - - 1,955,623,906

Deposits with financial

institutions - 1,910,736,315 - 1,910,736,315

Cash at banks - 89,821,466 - 89,821,466

Total financial assets 1,955,623,906 2,000,557,781 - 3,956,181,687

Liabilities

Amount due to Manager - - 2,516,441 2,516,441

Amount due to Trustee - - 167,763 167,763

Distributions to be

reinvested - - 10,660,138 10,660,138

Sundry payables and accrued

expenses - - 178,162 178,162

Total financial liabilities - - 13,522,504 13,522,504

Income, expense, gains

and losses

2017 2016

RM RM