annual report 2012 - fic english-email.pdf · fic annual report 2012 ... your company settled...

TRANSCRIPT

Annual Report 2012

FIC Annual Report 2012

His HighnessSheikh Nawaf Al-Ahmad Al-Jaber Al-Sabah

Crown Prince

His Highness Sheikh Sabah Al-Ahmad Al-Jaber Al-Sabah

Amir of the State of Kuwait

FIC Annual Report 2012

9131618273032333435

36-3738-81

CONTENTS

Mission StatementBoard of Directors’ Report Group Strategic Investments Economic ReportReport Of Fatwa And Shari’a Supervisory BoardAuditor’s ReportConsolidated Income StatementConsolidated Statement Of Comprehensive IncomeConsolidated Statement Of Financial PositionConsolidated Statement Of Changes In EquityConsolidated Cash Flow Statement Notes To The Consolidated Financial Statements

6

7

FIC Annual Report 2012

BOARD MEMBERS

Khalid S. Al-SanaousiChairman and Managing Director

Bader Mohammad Al Qattan Vice Chairman

Bader Ali Abdulla BenaianMember

Khalifa Abdulla Al-AjeelMember

Ahmad Abdulgadir Mohammad Member

Abdulmehsen Hamad Al Hamad Member

Marzouk Fajhan Al MutairiMember

8

9

FIC Annual Report 2012

Uphold Stakeholder,s interests by being a Professionally Managed Financial Institution offering Shari

,a Compliant Investment Products and Services for Local and International Clients

MISSION STATEMENT

10

FATWA AND SHARI’A SUPERVISORY BOARD

Sheikh Dr. Ali Mohyiddeen Al-QaradaghiChairman

Sheikh Dr. Essa Zaki ShaqraMember

Sheikh Dr. Abdulaziz Khalefa Al-QassarMember

11

FIC Annual Report 2012

EXECUTIVE MANAGEMENT

Tareq A. Al-AdsaniDeputy C.E.O

Omar Salem Al-MutawaaDeputy C.E.O

Mohamed Ajami AbdulbakiGeneral Legal Consultant

Ahamed Nawal SaheedVice President - Business Development

& Real Estate Investment

Fahad M. Al-Alloush Vice President - Business Development

& Real Estate Investment

Fawaz AL-AyyarVice President - Asset Management

Mohammad G. AL-Ghaith Vice President- Direct Investment

12

13

FIC Annual Report 2012

Board of Directors’ Report

In the Name of Allah the most Merciful

Dear shareholders,As the global and regional markets lean towards a sort of fragile stability, we meet you today to present to you our main achievements of the company during the past year.

The strong financial base and stable performance of the company in the past years as well as its conservative strategies, have contributed significantly to transform the company from cutback of losses, and addressing liquidity constraints to a stage today where we have recorded profits. Your company settled Kuwaiti Dinar 20 million of debts to two local banks and a GCC bank as part of restructuring of debts during 2012 which has brought down the company’s debt to Kuwaiti Dinar 29 million. One of the key strategic activities of the Company is to improve the performance of Subsidiary and Associate Companies towards achieving sustainable profitability. These efforts which included reorganization of companies have resulted in most subsidiaries and associate companies starting to record profitability since recovering from the consequences of the financial crisis.

Arkan Al Kuwait Real Estate Company successfully completed several exits at attractive prices in line with its geographical expansion strategy along with achieving desired growth and profitability which will have positive impacts to shareholders. Burgan Company for Well Drilling, Trading & Maintenance K.S.C.C also continued the expansion of its activities and was awarded several new tenders from oil companies. Burgan Company made good progress in the enhancement of its administrative and technical structure to be in line with its expansion strategy. First Education Company also made further growth in its investments in both universities and schools in several countries in the Arab region. The company is planning to entering into new educational projects in Kuwait and other regional countries. The company also entered into the field of training with a view to achieve further growth in its business lines. First Energy Resources Company witnessed many significant positive developments in relation to its subsidiary company the Kuwait Valves Company, especially after obtaining the approval from governmental oil companies in Kuwait for the supply and maintenance of oil valves. The Company was also awarded several tenders.

14

Your company is continuing to develop asset management activities by selecting investment opportunities of appropriate returns and risk profiles to meet the requirements of investors. The current portfolio of assets under management is approximately Kuwaiti Dinars 150 million.

Your company is pursuing promoting investments in the Sultanate of Oman, where it has a strong presence in the real estate sector through its associate company, Tameer Investment Oman. The company has a range of projects in different real estate sectors such as commercial complexes, industrial warehouses, investment properties, and a project to develop a tourist resort complex in the city of Salalah, as well as the development of a mixed-use complex (residential, commercial and offices) in Muscat, the capital of Oman.

The Company manages several diversified real estate portfolios in the Kingdom of Saudi Arabia in diversified sectors of residential, offices, hospitality and warehousing. The Company has begun sale of units in one of these portfolios; a residential project comprising 80 villas spread over three locations in Riyadh, with a project value of around Kuwaiti Dinar 7.5 million. This project represents the first achievements of the company’s projects in the residential sector in the Kingdom of Saudi Arabia in collaboration with Shomoul Real Estate Company, the developer and marketer of the project units.

The Company also manages a real estate portfolio in the hospitality sector which involves developing a 5 star hotel in Riyadh with a cost around Kuwaiti Dinars 22 million. This hotel is located in one of the prime locations in Riyadh. The construction of this hotel is expected to be completed in the middle of 2015. Further, the Company is targeting to offer additional real estate investment opportunities in the Kingdom of Saudi Arabia and Sultanate of Oman.

During the second quarter of last year, the Company completed all its requirements of the Capital Markets Authority (CMA) within the stipulated period. The Company is in the process of submitting its requirements of the Kuwait Companies Law No. 25 of 2012 which is expected to be completed during the first quarter of 2013.

The Board of Directors was reconstituted after the Annual General Meeting which was held on 8th July 2012 to hold interim elections to elect members to the Board of Directors. The composition of new major shareholders includes leading companies conducting businesses in vital economic sectors in the country. The strong coordination of the major shareholders of the Company with respect to direction of the Company and its business decisions along with their expertise and strong reputation is expected to contribute towards enhancing the performance of the Company in accordance with its ambitious strategy.

As for the strategic steps of the Company for 2013, your company will focus on completing the restructuring of the company’s assets to rebalance sector and geographic concentration and increase the liquidity. The Company will also take steps towards exiting of certain assets, the proceeds of which will be invested in income producing investments, and will increase fund management business line which is expected to be one of the main activities in the future. The Company, God willing, will continue to enhance the performance of subsidiaries and associate companies to become an important source of income. We can not fail to emphasize that the Company is in the process of complying its requirements with respect to the new Kuwait Companies Law No. 25 of 2012 having successfully completed compliance with the rules and instructions of the Capital Markets Authority.

15

FIC Annual Report 2012

With respect to our results for fiscal year ended 31 December 2012 are as follows:

2012 2011 Change rateNet Profit (KD million) 2.9 2 45%Revenue (KD million) 8.2 14.4 -43%Expenses (KD million) 5.1 11.4 -55%Total assets (KD million) 147 165 -11%Return on Assets 2% 1%Return on shareholders, equity 3.15% 2.3%Earning per share (fils) 4.5 3.2Bonus shares - -Cash dividends - -Capital increase - -

Based on these results the Board of Directors has recommended to the General Assembly not to distribute dividends for the fiscal year ended 31 December 2012.

We extend our sincere thanks and gratitude to all governmental authorities for the support extended to the company, and we ask the Allah Almighty to continue the blessings of security and safety to our dear Kuwait under the leadership of His Highness the Emir Sheikh Sabah Al-Ahmad Al-Jaber Al-Sabah and Crown Prince His Highness Sheikh Nawaf Al-Ahmad Al-Jaber Al-Sabah and protect it from any adversity. We also thank the company’s customers and shareholders for their valued trust and confidence placed on us and the members of the Sharia Supervisory Board for their blessed efforts. The Board expresses its sincere appreciation to the employees of your Company in their dedicated work towards achieving the Company’s goals.

May Allah bless your deeds,

Khalid Saud Al-Sanousi Chairman

16

Real Estate Sector

GROUP STRATEGIC INVESTMENTS

Country of Incorporation : Kingdom of BahrainCapital : B.D 6.900.000 million FIC contribution % : 35.29 %Nature of business : Real estate development and investment in Kingdom of Bahrain.

Sahab Al Khaleej Real Estate Co.

Country of Incorporation : Kingdom of Saudi Arabia Capital : SAR 2,000 million FIC contribution % : 9.91 %Nature of business : Real estate development and investment in Kingdom of Saudi Arabia.

Al Muttahed Company

Country of Incorporation : OmanCapital : OR 18،507 million FIC contribution % : 37.40 %Nature of business : Real estate development and investment in Oman.

Taameer Investment Company

Country of Incorporation : Kuwait Capital : KD 22.116 million FIC contribution % : 29.03 %Nature of business : Real estate development and investment in Kuwait and Arabian Gulf region.

Arkan Al-Kuwait Real Estate Company

Financial Sector

Country of Incorporation : Kingdom of Saudi Arabia Capital : SAR 60 million FIC contribution % : 40.00 %Nature of business : Provide of Islamic financial and investment services as well as asset management in the Kingdom of Saudi Arabia.

Adeem Capital

adeemcapital

17

FIC Annual Report 2012

Energy Sector

Asian Petroleum Company

First Education Company

Country of Incorporation : Kuwait Capital : KD 0.2 millionFIC contribution % : 66.6 %Nature of business : Oil field, Services, Supply & Construction.

Country of Incorporation : Kuwait Capital : KD 15 millionFIC contribution % : 17.16 %Nature of business : Investment in the Education sector.

Country of Incorporation : Kuwait Capital : KD 20,962,500 millionFIC contribution % : 20.46 %Nature of business : Drilling & Exploration.

Burgan Well Drilling Company

First Energy Resources CompanyCountry of Incorporation : Kuwait Capital : KD 21.650 million (50% paid up)FIC contribution % : 33.21 %Nature of business : Investment company in the energy, oil and gas sector.

Education Sector

18

THE ECONOMIC REPORT

KuwaitThe year 2012 was one marked by ups and downs for Kuwait, with a record profit highlighting the country’s economic growth, but also exposing its reliance on oil revenues. While the planning of new infrastructure projects and growth in the banking sector showed that the country is recovering well from the effects of the 2009 economic crisis, the political scene was dominated by tensions between the government and opposition.

Kuwait’s GDP is forecast to grow by 6.3% in 2012 (8.2%:2011), building on a strong performance in 2011 which produced growth of 5.7%. At the end of the 2011-12 fiscal years, the country posted a record budget surplus of KD 13.2 billion (29.8% of GDP) as revenue driven by oil sector grew by 41%.Local banks posted strong 2012 returns, with many institutions recovering from negative growth in the second quarter caused by allocating funds for provisioning against potential defaults. A number of banks have signaled their intention to continue approaching lending with caution. However slowdown in project awards has impacted credit growth for Banks as they struggle with high non performing loans ratios and balance sheet restructuring issues.

The Kuwait Stock Exchange ended 2012 with the KSE price Index recording an increase of 2.07% (KSE Weighted Index rose by 2.97%) to close at 5,934, following four consecutive years of losses. Trading activity in the Kuwait Stock Exchange witnessed sharp growth in 2012, with the total volume traded increasing by 120% in 2012, while the turnover rose by 19% to KD 7.3 billion. Financial and Services was the most actively traded index accounting for 35% of the traded turnover and 28% of the volumes.

19

FIC Annual Report 2012

The Real Estate market ended year 2012 with a positive outcome where the market liquidity rose by 15.8% to KD 3.3 billion. Housing activity, both private and investment captured 91% of the real estate market liquidly.

The country is expected to follow the pattern of previous years by ending the 2012-13 fiscal years with a budget surplus. In the medium term Kuwait’s fiscal policy is expected to remain expansionary and the Current expenditure will rise as the government wage bill rises. Real GDP in Kuwait is expected to grow at 2.2% and 3.3% in 2013 and 2014 respectively, supported by stable oil production. Signs of a greater determination by Kuwaiti authorities to implement large infrastructure projects associated with the government’s 4 year development plan should ease the economy’s dependence on growth in the consumer sector. The construction industry in particular should see significant growth on the back of key projects.

These will add to large fiscal and trade surpluses, which will provide a buffer against any fresh turbulence in the global economy. Whilst implementing large projects provide significant challenges moreover, the economy faces broader long term challenges most notably the need to create viable private sector jobs.

The budget is forecast to remain in huge surplus, though could decline to under 20% of GDP over the next two years as oil revenues plateau but spending pushes higher. Meanwhile, strong oil receipts are expected to keep the current account surplus strong in 2013 and 2014 at 35-45% of GDP implying a continued build up in Kuwait’s foreign assets.

GCCThe GCC countries combined GDP is estimated to grow by 5.4% to reach USD 1.48 trillion in 2012 driven by robust oil prices and government deployment of massive fiscal surpluses to develop non-hydrocarbon sectors. The OPEC Crude Basket averaged at around $110 per barrel during 2012, compared to $107 in 2011. With Oil prices remaining above the budget forecasts of all GCC governments and aided by expanded oil production most GCC governments have retained their expansionary fiscal policies, with strong infrastructure spending.

20

Saudi Arabia remains the region’s largest economy with nominal GDP forecasted to reach USD 657 bn, an increase of 6% in 2012 (7.1%: 2011). Much of this expansion is expected to come from strong energy prices, higher-than-expected oil output and increased state spending as part of the government’s long-term capital works programme.

Qatar’s Real GDP is forecasted to grow at 6.3% in 2012 (14.1%: 2011) to USD 184.6 bn. Qatar government’s initiatives to consolidate several years of economic expansion, while channeling a budgetary surplus towards large-scale capital works projects, helped the country achieve its aim of more moderate growth for 2012. The estimates are down significantly on figures from 2011 when Qatar’s economy expanded by 14.1%. Winning the right to host the World Cup helped accelerate Qatar’s long-term infrastructure development programme.

While 2012 may have been marked by an ongoing political stalemate and effects from regional and local unrest, Bahrain managed to overcome negative pressures and produce solid growth for 2012 with a real GDP growth of 2% in 2012 ( 2.1%: 2011). However, the country’s political intractability remains quite salient, as small-scale anti-government demonstrations continue in the midst of a protest ban. Oman recorded a GDP growth of 5% ( 5.4%: 2011) on the back of infrastructure development.

In stark contrast to the emerging markets, which surged in 2012 due to the large influx of liquidity, the GCC equity markets’ performance was lackluster. While the MSCI World and Emerging Market indices increased 13.2% and 15.1%, respectively, Saudi Arabia, the largest market in the GCC, recorded an increase of 6.0% in 2012. Strong corporate earnings catalyzed market growth in Kuwait with the index ended 2012 with a gain of 2.1% as measured by Kuwait Price index. In 2012, Dubai market outperformed other GCC markets and surged by 19.9% followed by the Abu Dhabi market that rose by 9.5%. Investors returned to the Dubai and Abu Dhabi markets in 2012 following a recovery in property prices. All the GCC markets ended the year on a positive note with the exception of Bahrain Bourse losing 6.83%, and Qatar, the only GCC market that gained in 2011, reported a 4.8% decline in 2012. Political unrest in the Middle East continued for a second year and had an adverse impact on the markets in 2012.

Meanwhile, the UAE remains the second largest economy with a nominal GDP forecasted to reach USD 361.9 in 2012, a growth of 4% ( 5.2%: 2011). The UAE economy has benefited from its status as a safe haven’ amidst the political turmoil across the Arab World, which helped to lift the Tourism and Hospitality sector in Dubai. Dubai’s debt problems are no longer a drag on overall sentiment, following several positive developments in terms of restructuring and rescheduling of the overall debt profile. One sector that continues to see a slow recovery is real estate, Abu Dhabi has targeted non-oil growth in line with its bid to diversify the emirate’s economy and reduce dependence on oil revenue. Initiatives include a plan to increase non-oil exports from 1% of GDP, which is the current figure, to 11% by 2030.

21

FIC Annual Report 2012

The year 2012 witnessed several key developments that shaped GCC equity markets’ performance including the implementation of the by laws and regulations of the Capital Markets Law issued by the Capital Markets Authority in Kuwait, the recovery of the real estate sector in Dubai and the announcement from the Saudi Capital Markets Authority that it would allow listing by foreign companies that already have their shares listed on other regulated exchanges.

Demand for Dubai properties and prices have been on a rebound during most of 2012, and the trend is expected to continue through 2013. An improvement in the Dubai economy has given a strong impetus to the Real Estate sector, with prices and sales activity showing a sustained trend of improvement. However, Abu Dhabi remains subdued due to supply overhang and pressure on prices has continued to take their toll. Meanwhile, in Saudi Arabia, the announcement of mortgage framework has failed to enthuse much interest, due to a gap in the supply of low-cost housing.

Despite healthy rates of economic growth, GCC inflation remains low which is expected to average to 2.4% in 2012. A slight pickup in inflation to 3% is seen in 2013.

OutlookGCC economic growth is set to slow to 3.6% in 2013 from 5.4% in 2012 as the three year surge in regional oil production comes to an end. However, the business conditions are expected to remain solid as governments maintain higher levels of investment and social spending. An oil price of $100 per barrel will allow most GCC governments to finance higher spending without draining their financial resources. However, a major global economic downturn could drive oil prices downwards that would put government fiscal balances under pressure. Interest rates are expected to stay at recent record lows and the banking sector profitability should see an improvement so long as the global economy does not deteriorate.

In Saudi Arabia, growth is anticipated to moderate this year with GDP projected to expand by around 4% in 2013 (6%: 2012) as demand for energy eases. Oil production remains near record highs, and government spending continues to expand. While growth may moderate in 2013, a number of sectors, including construction and banking, look set to continue expanding.

22

The Qatar GDP is expected to ease to around 5% in 2013 (6.3%: 2012) and beyond. The IMF also expects the oil and gas sector’s contribution to remain flat, with gas production having now reached the government’s target, economic expansion was set to fall to mid-range single digits, while ongoing high capital spending by the state would maintain growth for the non-energy sector UAE’s economy as a whole could see a growth of a more modest 2.6% in 2013 (4% :2012). Over the next four years, Dubai will have to repay or renegotiate $50bn worth of debt, with $9.4bn-$9.8bn of this expected in 2013. Any delays in servicing this debt could undermine the confidence. Abu Dhabi’s economy is expected to continue expanding into 2013. The Bahrain economy is expected to witness a slowdown in growth to 2.8% (2% 2012) in 2013. Modestly expanding oil production and a recovering services sector will keep real GDP growth at around 3% in the next few years, around half the rate witnessed in the five years prior to the onset of the global recession. Oman GDP is expected to slightly decrease to 3.2% in 2013 (3.9% :2011)

GCC government spending is seen rising by 6-8% over the next two years. A major global economic downturn could see global oil market fundamentals loosen by than anticipated, pushing oil prices below $100 per barrel. This would put government fiscal balances under pressure and cause cuts in spending or delays in project execution wakening economic growth. Banking sector profitability should see an improvement after provisioning affected 2012. Interest rates are expected to stay at recent record lows, in order to manage exchange rate pegs against the US dollar.

GLOBAL ECONOMY AND OUTLOOK

Global financial conditions continued its improvement in the second half of the year of 2012 with a GDP growth of 3.3 % (3.8%: 2011). The main sources of acceleration were emerging market economies, where activity picked up broadly as expected, and the United States, where growth surprised on the upside. Financial conditions stabilized and capital flows to emerging markets remained strong

23

FIC Annual Report 2012In the United States a supportive a financial market environment and the turnaround in the housing market have helped to improve household balance sheets. The GDP is forecast to grow by 2.2% in 2012 (1.8%: 2011). The priority in the United States is to avoid excessive fiscal consolidation in the short term and promptly raise the debt ceiling. The recovery of the housing market plus abundant shale oil will help the manufacturing sector. These two factors will be working to the benefit of the US.

The euro area continues to pose a large downside risk to the global outlook. In particular, risks of prolonged stagnation in the euro area as a whole will rise if the momentum for reform is not maintained. The GDP in 2012 is forecast to contract by 0.4%. The near-term outlook for the euro area is expected to contract by 0.2 percent in 2013. This reflects delays in improved bank liquidity to private sector borrowing conditions, and still-high uncertainty about the ultimate resolution of the crisis despite recent progress. EIU expects five of the Euro 15 in recession in 2013, with Greece, Portugal and Spain needing further bailouts. The UK is, on the other side, stabilizing with labor costs coming down rapidly.

In Japan, the priority is to underpin the renewed emphasis on raising growth and inflation with more ambitious monetary policy easing, and adopting a credible medium-term fiscal consolidation plan. The Japan GDP is forecast to grow by 2.2% in 2012 (-0.8% in 2011). Japan is expected to expand by 1.2 percent in 2013. The recession is expected to be short-lived because the effects of temporary factors, such as the car subsidy and disruptions to trade with China, will subside. The sizeable fiscal stimulus package and further monetary easing will give growth at least a near-term boost, with support from a pickup in external demand and a weaker yen.

Although the steady decline in global exports and imports across the globe is likely to continue through 2013, the growth in emerging market and developing economies is on track to record 5.6 percent in 2013 a slight increase from 5.3% in 2012. Nevertheless, growth is not projected to rebound to the high rates recorded in 2010–11. But weakness in advanced economies will weigh on external demand. Moreover, the space for further policy easing has diminished, while supply bottlenecks and policy uncertainty have hampered growth in economies such as, Brazil, India.

24

China recorded a GDP growth of 7.8% in 2012 a significant decline from 9.2% in 2012. The GDP growth is expected to be around 8% in the next three years. Ensuring sustained rapid growth in China requires continued progress with market-oriented structural reforms and rebalancing of the economy more toward private consumption. In other emerging market and developing economies, requirements differ. In the Middle East and North Africa region, many countries will need to maintain macroeconomic stability under difficult internal and external conditions.

The projections by IMF imply that global growth will strengthen gradually through 2013, averaging 3.5 percent on an annual basis, a moderate uptick from 3.2 percent in 2012. A further strengthening to 4.1 percent is projected for 2014, assuming recovery takes a firm hold in the euro area economy.

25

FIC Annual Report 2012

26

27

FIC Annual Report 2012

REPORT OF FATWA AND SHARI’A BOARD

Praise be to Allah, the Lord of the Universe and Prayers and Peace upon the Messenger of Allah who was sent as Blessing to the world, Mohammad may Prayers and Peace be upon him, his family, his companions and his followers until the Day of Judgment.

We, the Fatwa and Shari’a Board of First Investment Company (“the Company”), state hereby that we have reviewed the principles followed and the contracts pertaining to the transactions and deals made by the Company during the year ended 31st December, 2012, have exercised our control duties as a preview to expressing our opinion on whether the Company has complied with the dictates and principles of Islamic Shari’a Law to specific edicts, decisions and guidelines issued by our board.

It is our view that:1. The contracts, operations and transactions concluded by the Company during the year ended 31st December, 2012, which we have reviewed, were carried out in conformity with the dictates and principles of Islamic Shari’a Law.

2. The distributions of profits and encumbrances of losses against the investment accounts conform with our approved principles which conform with the dictates and principles of the Islamic Shari’a Law.

3. All earnings realized from sources or through ways prohibited by the dictates and principles of the Islamic Shari’a Law have been disbursed in charitable activities.

We hereby take this opportunity to express our appreciation and thanks to the management of the Company for its kind cooperation to our board, as well as the shareholders and other parties dealing with the Company.

We pray to Allah Almighty to bless their efforts and dedication to serve the Islamic economy, and develop our nation in ways that shall yield benefits to all parties involved.

Note: Zakat amount per share is : 1.724 fils, and it is payable on shareholder.

Sheikh Dr. Ali Mohyiddeen Al-QaradaghiChairman

Sheikh Dr. Essa Zaki ShaqraMember

Sheikh Dr. Abdulaziz Khalefa Al-QassarMember

28

First Investment Company K.S.C. (Closed)

and its Subsidiaries

CONSOLIDATED FINANCIAL STATEMENTS31 December 2012

30

31

FIC Annual Report 2012

32

First Investment Company K.S.C. (Closed) and its Subsidiaries

2012 2011 Notes KD KD

INCOMEMurabaha and ijara income 68,431 84,777Rental income 634,399 -Realised gain on financial assets at fair value through statement of income 4 54,009 750,064

Unrealised loss on financial assets at fair value throughstatement of income 4 (125,959) (48,875)Gain on disposal of financial assets available-for-sale 2,821,193 4,211,269Gain on disposal of properties under development 12 153,277 3,055,552Gain on disposal of investment properties 92,113 202,423Gain on revaluation of investment properties 13 137,324 467,458Management fees 988,115 814,775Dividend income 5 110,533 188,723Gain on disposal of associates 11 772,299 2,416,626Share of results of associates 11 896,278 (87,598)Gain on settlement of murabaha payables 17 1,110,365 2,278,000Other income 501,243 40,169

8,213,620 14,373,363EXPENSESReversal (provision) of murabaha and ijara receivables – net 9 453,980 (432,859)Impairment of financial assets available-for-sale 10 (1,439,964) (1,144,319)Provision and write off of other assets 14 (192,161) (1,659,751)Staff costs (2,133,210) (1,796,815)Foreign exchange gain (loss) 949,906 (378,859)Depreciation (136,333) (99,811)Finance costs (1,680,876) (4,833,582)Other expenses (956,633) (1,086,809)

(5,135,291) (11,432,805)

PROFIT BEFORE CONTRIBUTION TO KUWAIT FOUNDATION FOR THE ADVANCEMENT OF SCIENCES (“KFAS”), NATIONAL LABOUR SUPPORT TAX (“NLST”), ZAKAT AND DIRECTORS’ REMUNERATION

3,078,329 2,940,558

Contribution to KFAS (16,799) (12,691)Contribution to NLST (64,600) (56,861)Zakat (24,805) (19,902)Directors’ remuneration (7,000)

PROFIT FOR THE YEAR 2,972,125 2,844,104

Attributable to:Owners of the Parent Company 2,909,976 2,066,288Non-controlling interests 62,149 777,816

2,972,125 2,844,104

BASIC AND DILUTED EARNINGS PER SHARE ATTRIBUTABLE TO THE OWNERS OF THE PARENT COMPANY 6 4.5 fils 3.2 fils

The attached notes 1 to 26 form part of these consolidated financial statements.

CONSOLIDATED STATEMENT OF INCOMEFor the year ended 31 December 2012

33

First Investment Company K.S.C. (Closed) and its Subsidiaries FIC Annual Report 2012

2012 2011Note KD KD

Profit for the year 2,972,125 2,844,104

Other comprehensive income

Financial assets available-for-sale:Unrealised (loss) gain (1,920,672) 1,640,864Transferred to consolidated statement of income on impairment 10 1,439,964 1,144,319

Net unrealised (loss) gain on financial assets available-for-sale (480,708) 2,785,183Share of other comprehensive income of associates 47,351 578,147Exchange differences on translation of foreign operations (406,842) 433,646

Other comprehensive (loss) income for the year (840,199) 3,796,976

Total comprehensive income for the year 2,131,926 6,641,080

Attributable to:

Owners of the Parent Company 1,987,405 6,094,538Non-controlling interests 144,521 546,542

2,131,926 6,641,080

.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME Year ended 31 December 2012

The attached notes 1 to 26 form part of these consolidated financial statements.

2012 2011Notes KD KD

ASSETS Bank balances and cash 7 8,116,741 9,314,660Financial assets at fair value through statement of income 8 1,351,240 1,804,747Murabaha and ijara receivables 9 2,116,007 2,383,916Financial assets available-for-sale 10 32,266,092 65,062,640Investment in associates 11 53,000,509 55,293,202Properties under development 12 17,383,621 17,857,359Investment properties 13 26,816,298 6,383,054Other assets 14 4,372,229 5,521,857Property and equipment 1,198,768 1,193,129

TOTAL ASSETS 146,621,505 164,814,564

EQUITY AND LIABILITIES EquityShare capital 15 65,107,055 65,107,055Share premium 15 18,250,362 18,250,362Treasury share 15 (104,693) -Statutory reserve 16 517,892 216,274Share options reserve 3 3,016,890 3,016,890Treasury shares reserve 15 1,090,539 1,090,539Cumulative changes in fair values 134,667 632,864Foreign currency translation reserve 555,528 979,902Retained earnings 4,458,372 1,850,014

Equity attributable to owners of the Parent Company 93,026,612 91,143,900Non-controlling interests 19,750,500 19,873,439

Total equity 112,777,112 111,017,339

LiabilitiesMurabaha and sukuk payables 17 29,560,317 48,939,220Other liabilities 18 4,284,076 4,858,005

Total liabilities 33,844,393 53,797,225

TOTAL EQUITY AND LIABILITIES 146,621,505 164,814,564

34

First Investment Company K.S.C. (Closed) and its SubsidiariesCONSOLIDATED STATEMENT OF FINANCIAL POSITIONAt 31 December 2012

Khalid S. Al-SanaousiChairman and Managing Director

Badar Mohammed Al-Qatan Vice Chairman

The attached notes 1 to 26 form part of these consolidated financial statements.

35

First Investment Com

pany K.S.C. (Closed) and its SubsidiariesC

ON

SOLIDATED STATEM

ENT O

F CH

ANG

ES IN EQ

UITYFor the year ended 31 D

ecember 2012

The attached notes 1 to 26 form part of these consolidated financial statem

ents.

Attributable to owners of the Parent Company

Non-controllinginterests

Total equity

Sharecapital

Sharepremium

Treasury shareStatutoryreserve

Shareoptions reserve

Treasuryshares reserve

Cumulative changes in fair values

Foreigncurrency

translationreserve

Retained earnings

(accumulated losses)

Sub-totalKD

KD KD

KD KD

KD KD

KDKD

KD KD

KD

As at 1 January 201265,107,055

18,250,362-

216,2743,016,890

1,090,539632,864

979,9021,850,014

91,143,90019,873,439

111,017,339

Profit for the year-

- -

- -

- -

- 2,909,976

2,909,976 62,149

2,972,125Other comprehensive (loss) income for the year

- -

- -

- -

(498,197)(424,374)

- (922,571)

82,372(840,199)

Total comprehensive (loss) income for the year-

- -

- -

- (498,197)

(424,374)2,909,976

1,987,405144,521

2,131,926Purchase treasury share

- -

(104,693)-

- -

- -

- (104,693)

- (104,693)

Transfer to reserve -

- -

301,618-

- -

- (301,618)

- -

- Distribution to non-controlling interests

- -

- -

- -

- -

- -

(267,460)(267,460)

At 31 December 201265,107,055

18,250,362(104,693)

517,8923,016,890

1,090,539134,667

555,5284,458,372

93,026,61219,750,500

112,777,112

As at 1 January 201165,107,055

21,490,583-

7,275,9883,016,890

1,090,539(2,735,106)

319,622(10,516,209)

85,049,3628,931,900

93,981,262

Profit for the year-

- -

- -

- -

- 2,066,288

2,066,288777,816

2,844,104Other comprehensive income (loss) for the year

- -

- -

- -

3,367,970660,280

- 4,028,250

(231,274)3,796,976

Total comprehensive income for the year-

- -

- -

- 3,367,970

660,2802,066,288

6,094,538546,542

6,641,080Write-off of accumulated losses (Note 15)

- (3,240,221)

- (7,275,988)

- -

- -

10,516,209-

- -

Transfer to reserve -

- -

216,274-

- -

- (216,274)

- -

- Arising on business combination

- -

- -

- -

- -

- -

13,965,28813,965,288

Distribution to non-controlling interests-

- -

- -

- -

- -

- (3,570,291)

(3,570,291)

At 31 December 201165,107,055

18,250,362-

216,2743,016,890

1,090,539632,864

979,9021,850,014

91,143,90019,873,439

111,017,339

FIC Annual Report 2012

36

First Investment Company K.S.C. (Closed) and its Subsidiaries

2012 2011 Notes KD KD

OPERATING ACTIVITIESProfit for the year 2,972,125 2,844,104Adjustments for:Depreciation 136,333 99,811Finance costs 1,680,876 4,833,582Murabaha and ijara income (68,431) (84,777)Gain on disposal of financial assets available-for-sale (2,821,193) (4,211,269)Gain on revaluation on investment properties (137,324) (467,458)Gain on disposal of properties under development 12 (153,277) (3,055,552)Gain on disposal of investment properties (92,113) (202,423)Dividend income 5 (110,533) (188,723)Gain on disposal of associates 11 (772,299) (2,416,626)Share of results of associates 11 (896,278) 87,598 Gain on settlement of murabaha and sukuk payables 17 (1,110,365) (2,278,000)( Reversal) provision against murabaha and ijara receivables – net 9 (453,980) 432,859Impairment of financial assets available-for-sale 10 1,439,964 1,144,319Provision and write-off of other assets 14 192,161 1,659,751Foreign exchange (gain) loss (949,906) 378,859

(1,144,240) (1,423,945)Changes in operating assets and liabilities:Financial assets at fair value through statement of income 416,123 (1,100,694)Murabaha and ijara receivables 452,430 2,802,571Other assets 1,194,563 51,542Other liabilities 89,033 536,052

1,007,909 865,526Murabaha and ijara income received 62,911 33,830Finance costs paid (2,337,133) (5,758,082)

Net cash used in operating activities (1,266,313) (4,858,726)

INVESTING ACTIVITIESArising on acquisition of a subsidiary - 1,500,103Dividend income received 5 110,533 188,723Purchase of financial assets available-for-sale - (914,388)Proceeds from disposal of financial assets available-for-sale 970,444 270,611Purchase of investment properties (807,096) -Proceeds from disposal of investment properties 6,117,856 1,856,801Purchase of investment in associates 11 (2,123,062) (5,595)Proceeds from disposal of investment in associates 1,936,000 11,160,567Dividends received from associates 319,992 -

Purchase of properties under development (543,217) (876,239)Proceeds from sale of properties under development 1,213,877 12,235,066Purchase of property and equipment (141,972) (114,525)

Net cash flows from investing activities 7,053,355 25,301,124

CONSOLIDATED STATEMENT OF CASH FLOWSFor the year ended 31 December 2012

The attached notes 1 to 26 form part of these consolidated financial statements.

37

First Investment Company K.S.C. (Closed) and its Subsidiaries FIC Annual Report 2012

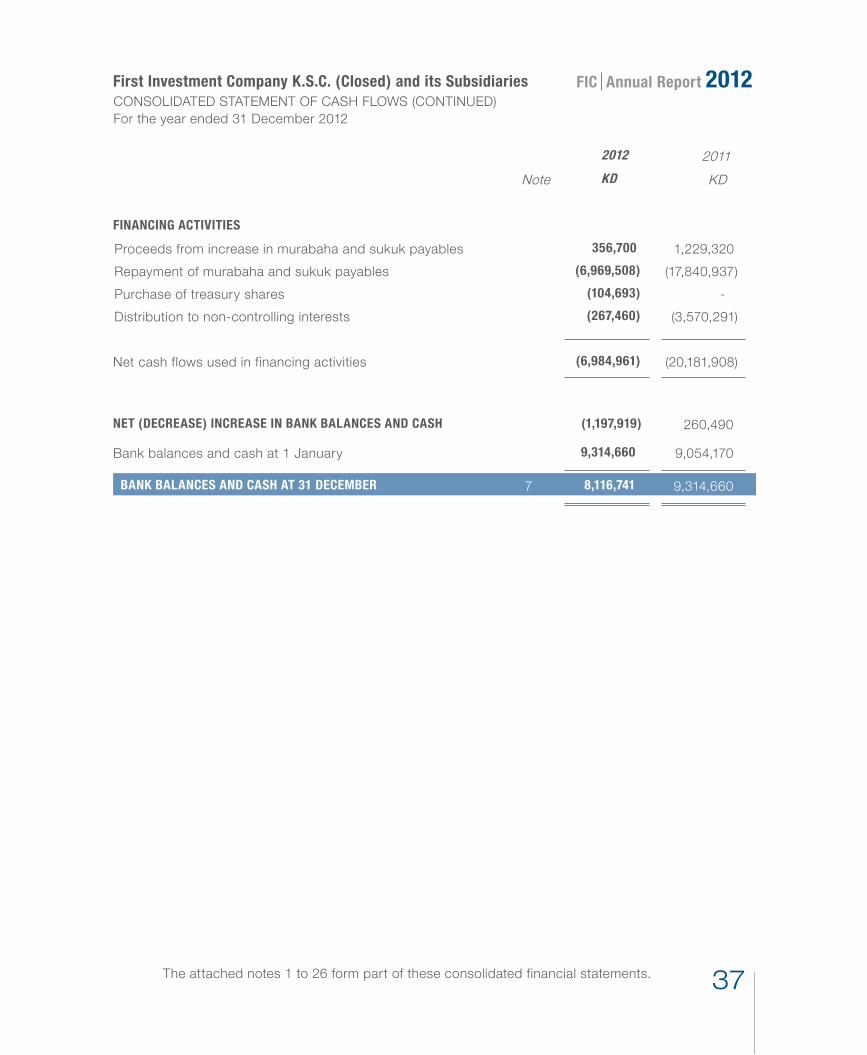

2012 2011 Note KD KD

FINANCING ACTIVITIES

Proceeds from increase in murabaha and sukuk payables 356,700 1,229,320Repayment of murabaha and sukuk payables (6,969,508) (17,840,937)Purchase of treasury shares (104,693) -Distribution to non-controlling interests (267,460) (3,570,291)

Net cash flows used in financing activities (6,984,961) (20,181,908)

NET (DECREASE) INCREASE IN BANK BALANCES AND CASH (1,197,919) 260,490

Bank balances and cash at 1 January 9,314,660 9,054,170

BANK BALANCES AND CASH AT 31 DECEMBER 7 8,116,741 9,314,660

The attached notes 1 to 26 form part of these consolidated financial statements.

CONSOLIDATED STATEMENT OF CASH FLOWS (CONTINUED)For the year ended 31 December 2012

38

First Investment Company K.S.C. (Closed) and its Subsidiaries

1 CORPORATE INFORMATION

The consolidated financial statements of First Investment Company K.S.C. (Closed) (the “Parent Company”) and its subsidiaries (together, the “Group”) for the year ended 31 December 2012 were authorised for issue in accordance with a resolution of the Board of Directors of the Parent Company on 20 March 2013. The shareholders’ General Assembly has the power to amend these consolidated financial statements after issuance.

The Parent Company is a Kuwaiti shareholding company incorporated on 26 July 1997 under the Commercial Companies Law No. 15 of 1960 and amendments thereto and is regulated by the Central Bank of Kuwait (“CBK”) and Capital Market Authority (“CMA”) as an investment company. The Parent Company’s shares are listed on Kuwait Stock Exchange. The Parent Company’s registered office is at Souk Al Safat, Abdullah Mubarak Street, Kuwait City.

The Parent Company is principally engaged in the provision of investment and financial services and all activities are carried out in compliance with the memorandum of association, the article of association and the Islamic Sharia.

2.1 BASIS OF PREPARATION

The consolidated financial statements of the Group have been prepared in accordance with the regulations of the State of Kuwait for financial services institutions regulated by the CBK. These regulations require adoption of all International Financial Reporting Standards (IFRS) except for the IAS 39 requirement for collective provision, which has been replaced by CBK’s requirement for a minimum general provision made on all applicable credit facilities that are not provided specifically.

The consolidated financial statements have been prepared on a historical cost basis, except for the financial assets at fair value through statement of income, financial assets available-for-sale and investment properties that have been measured at fair value.

The consolidated financial statements are presented in Kuwaiti Dinars which is also the functional currency of the Parent Company.

The Companies Law issued on 26 November 2012 by Decree Law no 25 of 2012 (the “Companies Law”), which was published in the Official Gazette on 29 November 2012, cancelled the Commercial Companies Law No 15 of 1960. According to article 2 of the Decree, the Company has a period of 6 months from 29 November 2012 to regularize its affairs in accordance with the Companies Law.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

39

First Investment Company K.S.C. (Closed) and its Subsidiaries FIC Annual Report 2012

2.2 BASIS OF CONSOLIDATION

The consolidated financial statements comprise the financial statements of the Parent Company and its subsidiaries as at 31 December 2012.

Subsidiaries are fully consolidated from the date of acquisition, being the date on which the Group obtains control, and continue to be consolidated until the date when such control ceases. Control is achieved where the Group has the power to govern the financial and operating policy of an entity so as to obtain benefits from its activities. This occurs when the Group has more than 50% voting power through ownership or agreements, except where minority rights are such that a minority shareholder is able to prevent the Group from exercising control. In addition control may exist without having more than 50% voting power through ownership or agreements, or in the circumstances of enhanced minority rights, as a consequence of de facto control. De facto control is control without the legal right to exercise unilateral control, and involves decision making ability that is not shared with others and the ability to give directions with respect to the operating and financial policies of the entity concerned.

The financial statements of the subsidiaries are prepared for the same reporting period as the Parent Company, using consistent accounting policies. All intra-group balances, transactions, unrealised gains and losses resulting from intra-group transactions and dividends are eliminated in full.

Total comprehensive income/loss within a subsidiary is attributed to the non-controlling interest even if that results in a deficit balance.

A change in the ownership interest of a subsidiary, without a loss of control, is accounted for as an equity transaction. If the Group loses control over a subsidiary, it:

• Derecognises the assets (including goodwill) and liabilities of the subsidiary• Derecognises the carrying amount of any non-controlling interest• Derecognises the cumulative translation differences recorded in other comprehensive income• Recognises the fair value of the consideration received• Recognises the fair value of any investment retained• Recognises any surplus or deficit in statement of income • Reclassifies the Parent Company’s share of components previously recognised in other comprehensive

income to statement of income or retained earnings, as appropriate.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

40

First Investment Company K.S.C. (Closed) and its Subsidiaries

2.2 BASIS OF CONSOLIDATION (Continued)

Details of subsidiaries are set out below:

NameCountry of

Incorporation% equity interest Principal activity

2012 2011

Al Marwa Holding Company K.S.C. (Closed) Kuwait 99.22% 99.22% Holding company

FIC Projects Development Company Cayman Islands 100% 100% Real estate investmentDeema Real Estate Investment Company L.L.C. Saudi Arabia 95% 95% Real estate investment

First Energy Resource Company K.S.C.(Closed) Kuwait 33.21% 33.21% Investment in energy sector

First Investment Fund E.C. (1) Bahrain 100% 100% Special purpose company for fiduciary assets

FIC Sukuk Company Limited Cayman Islands 100% 100% Holding assets on trust of

sukuk holders

Masadar Energy Company for General Trading W.L.L Kuwait 98% 98% General trading

Shomoul Real Estate Company L.L.C. Saudi Arabia 50% 50% Real estate investment

Yasmeen Al Kuwait Real Estate Company W.L.L. Kuwait 97% 97% Real estate trading

Q80 Valve Industries Factory Kuwait 66.6% 66.6% ManufacturingAsian Petroleum Facilities Maintenance Company W.L.L.

Kuwait 66.6% 66.6% Investment in energysector

1) The Parent Company holds voting capital in First Investment Fund E.C. to manage the funds and fiduciary assets and does not have a beneficial interest in the underlying assets in its capacity as a holding company.

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a) Business Combinations and GoodwillBusiness combinations are accounted for using the acquisition method. The cost of an acquisition is measured as the aggregate of the consideration transferred, measured at acquisition date fair value and the amount of any non- controlling interest in the acquiree. For each business combination, the acquirer measures the non-controlling interest in the acquiree either at fair value or at the proportionate share of the acquiree’s identifiable net assets. Acquisition costs incurred are expensed and included in other expenses.

When the Group acquires a business, it assesses the financial assets and liabilities assumed for appropriate classification and designation in accordance with the contractual terms, economic circumstances and pertinent conditions as at the acquisition date.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

41

First Investment Company K.S.C. (Closed) and its Subsidiaries FIC Annual Report 2012

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)a) Business Combinations and Goodwill (continued)

If the business combination is achieved in stages, the acquisition date fair value of the acquirer’s previously held equity interest in the acquiree is remeasured to fair value at the acquisition date through the consolidated statement of income.

Any contingent consideration to be transferred by the acquirer will be recognised at fair value at the acquisition date. Contingent consideration classified as an asset or liability that is a financial instrument and within the scope of IAS 39 Financial Instruments: Recognition and Measurement, is measured at fair value with changes in fair value recognised either in either profit or loss or as a change to other comprehensive income. If the contingent consideration is not within the scope of IAS 39, it is measured in accordance with the appropriate IFRS. Contingent consideration that is classified as equity is not remeasured and subsequent settlement is accounted for within equity.

Goodwill is initially measured at cost being the excess of the cost of an acquisition over the Group’s share of the acquiree’s fair value of the net identifiable assets as at the date of the acquisition. Any excess, at the date of acquisition, of the Group’s share in the acquiree’s fair value of the net identifiable assets over the cost of the acquisition is recognised in the consolidated statement of income.

After initial recognition, goodwill is measured at cost less any accumulated impairment losses. For the purpose of impairment testing, goodwill acquired in a business combination is, from the acquisition date, allocated to each of the Group’s cash-generating units (CGU) that are expected to benefit from the combination, irrespective of whether other assets or liabilities of the acquiree are assigned to those units.

Where goodwill forms part of a CGU and part of the operation within that unit is disposed of, the goodwill associated with the operation disposed of is included in the carrying amount of the operation when determining the gain or loss on disposal of the operation. Goodwill disposed of in this circumstance is measured based on the relative values of the operation disposed of and the portion of the CGU retained.

b) Revenue recognitionRevenue is recognized to the extent that it is probable that the economic benefits will flow to the Group and the revenue can be reliably measured, regardless of when the payment is being made. Revenue is measured at fair value of the consideration received or receivable, taking into account contractually defined terms of payment. The Group assesses its revenue arrangements against specific criteria in order to determine if it is acting as principal or agent. The Group has concluded that it is acting as a principal in all of its revenue arrangements.

The following specific recognition criteria must also be met before revenue is recognized:

• Sale of properties is recognised when the risk and rewards of ownership have passed to the buyer usually evidenced by transfer of title of the properties.

• Murabaha and ijara income are recognised on a time proportion basis so as to yield a constant periodic rate of return based on the net balance outstanding.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

42

First Investment Company K.S.C. (Closed) and its Subsidiaries

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)b) Revenue recognition (continued)

• Rental income arising from operating leases of investment properties is accounted for on an accrual basis on contract terms.

• Management fees relating to portfolios and fund management, custody and on-going advisory services are recognised as earned.

• Dividend income is recognised when the Group’s right to receive the payment is established.

c) Share based payment transactions The Group operates an equity-settled, share-based Employee Stock Option Plan (ESOP). The cost of equity-settled transactions with employees is measured under the intrinsic value method. Under this method, the cost is determined by comparing the market value of the Parent Company’s shares at each reporting date and the date of final settlement to the exercise price with any change in intrinsic value recognised in the consolidated statement of income.

The cost of equity-settled transactions is recognised, together with a corresponding increase in equity, over the period in which the performance conditions are fulfilled, ending on the date on which the relevant employees exercise their rights. The cumulative expense recognised for equity-settled transactions at each reporting date until the exercise date, reflects the extent to which the exercise period has expired and the number of awards that, in the opinion of the Board of Directors at that date, based on the best available estimate of the number of equity instruments that will ultimately vest.

d) Financial instruments - initial recognition and subsequent measurement

i) Financial assets

Initial recognition and measurement

Financial assets within the scope of IAS 39 are classified as “financial assets at fair value through statement of income”, “loans and receivables” (murabaha and ijara receivables) and “financial assets available-for-sale”. The Group determines the classification of its financial assets at initial recognition.

All financial assets are recognised initially at fair value plus transaction costs, except in the case of financial assets recorded at fair value through statement of income.

Purchases or sales of financial assets that require delivery of assets within a time frame established by regulation or convention in the market place (regular way trades) are recognised on the trade date, i.e., the date that the Group commits to purchase or sell the asset.

Subsequent measurement

The subsequent measurement of financial assets depends on their classification as follows:

Financial assets at fair value through statement of income

These are financial assets that are either financial assets held for trading or those designated as at fair value through statement of income upon initial recognition. A financial asset is classified in this category only if they are acquired principally for the purpose of generating profit from short-term fluctuation in price or if so designated by the management only if criteria under IAS 39 are satisfied.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

43

First Investment Company K.S.C. (Closed) and its Subsidiaries FIC Annual Report 2012

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)d) Financial instruments - initial recognition and subsequent measurement (continued)i) Financial assets (continued)

Financial assets at fair value through statement of income (continued)

Financial assets at fair value through statement of income are carried in the statement of financial position at fair value. Resultant unrealised gains and losses arising from changes in fair value are included in the consolidated statement of income.

The Group evaluates its financial assets held for trading to determine whether the intention to sell them in the near term is still appropriate. When in rare circumstances the Group is unable to trade these financial assets due to inactive markets and management’s intention to sell them in the foreseeable future significantly changes, the Group may elect to reclassify these financial assets. The reclassification to loans and receivables, available-for-sale or held to maturity depends on the nature of the asset. This evaluation does not affect any financial assets designated at fair value through statement of income using the fair value option at designation, these instruments cannot be reclassified after initial recognition.

Financial assets available-for-sale

Financial assets available-for-sale are those financial assets that are not classified as financial assets at fair value through statement of income or held for trading.

After initial recognition, financial assets available-for-sale are subsequently measured at fair value with unrealised gains and losses recognised in the consolidated statement of other comprehensive income until the investment is derecognised, at which time the cumulative gain or loss is recognised in consolidated statement of income, or determined to be impaired, is reclassified to the consolidated statement of income and removed from the available-for-sale reserve. Investments whose fair value cannot be reliably measured are carried at cost less impairment losses, if any.

The Group evaluates whether the ability and intention to sell its financial assets available-for-sale in the near term is still appropriate. When, in rare circumstances, the Group is unable to trade these financial assets due to inactive markets and management’s intention to do so significantly changes in the foreseeable future, the Group may elect to reclassify these financial assets. Reclassification to loans and receivables is permitted when the financial assets meet the definition of loans and receivables and the Group has the intent and ability to hold these assets for the foreseeable future or until maturity. Reclassification to the held-to-maturity category is permitted only when the entity has the ability and intention to hold the financial asset accordingly.

For a financial asset reclassified from the available-for-sale category, the fair value carrying amount at the date of reclassification becomes its new amortised cost and any previous gain or loss on the asset that has been recognised in equity is amortised to consolidated statement of income over the remaining life of the investment using the effective interest rate (EIR) method. Any difference between the new amortised cost and the maturity amount is also amortised over the remaining life of the asset using the EIR. If the asset is subsequently determined to be impaired, then the amount recorded in equity is reclassified to the consolidated statement of income.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

44

First Investment Company K.S.C. (Closed) and its Subsidiaries

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)d) Financial instruments - initial recognition and subsequent measurement (continued)

i) Financial assets (continued)

Reclassification from financial assets available-for-sale to investment in associates is made upon acquisition of significant influence over the investment. Such transfer is made at original cost and any gain or loss previously classified in cumulative changes in fair value reserve is reversed to bring the carrying value to its original cost.

Loans and receivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. After initial measurement, such financial assets are subsequently measured at amortised cost using the EIR method, less impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees or costs that are an integral part of the EIR.

Loans and receivables comprises of following:

Murabaha and ijara receivables Murabaha is an Islamic transaction involving the purchase and immediate sale of an asset at cost plus an agreed profit. The amount due is settled on a deferred payment basis.

Ijara is an Islamic transaction involving purchase and immediate lease of an asset where the lessor conveys to the lessee the right to use the asset for an agreed period of time in return for a payment or a series of payments. At the end of the lease term, the lessee has the option to purchase the asset.

Murabaha and ijara receivables arising from the Group’s financing of transactions on an Islamic basis are stated at amortised cost. Third party expenses such as legal fees, incurred in granting a murabaha or ijara are treated as part of the cost of the transaction.

All murabaha and ijara receivables are recognized when the legal right to control the use of the underlying asset is transferred to the customer.

Derecognition of financial assetsA financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is derecognised when:

• the rights to receive cash flows from the asset have expired • the Group has transferred its rights to receive cash flows from the asset or has assumed an obligation

to pay the received cash flows in full without material delay to a third party under a ‘pass through’ arrangement; and either (a) the Group has transferred substantially all the risks and rewards of the asset, or (b) the Group has neither transferred nor retained substantially all the risks and rewards of the asset, but

has transferred control of the asset.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

45

First Investment Company K.S.C. (Closed) and its Subsidiaries FIC Annual Report 2012

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)d) Financial instruments - initial recognition and subsequent measurement (continued)

i) Financial assets (continued)Derecognition of financial assets (continued)

When the Group has transferred its rights to receive cash flows from an asset or has entered into a pass-through arrangement, and has neither transferred nor retained substantially all of the risks and rewards of the asset, nor transferred control of the asset, the asset is recognised to the extent of the Group’s continuing involvement in the assets. In that case, the Group also recognises an associated liability. The transferred asset and the associated liability are measured on a basis that reflects the rights and obligations that the Group has retained.

Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the Group could be required to repay.

ii) Impairment of financial assetsAn assessment is made at each reporting date to determine whether there is any objective evidence that a financial asset or a group of financial assets may be impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that have occurred after the initial recognition of the asset and that loss event has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated. If such evidence exists, an impairment loss is recognised in the consolidated statement of income.

Evidence of impairment may include indications that the debtors or a group of debtors is experiencing significant financial difficulty, default or delinquency in profit or principal payments, the probability that they will enter bankruptcy or other financial reorganisation and when observable data indicate that there is a measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults. If such evidence exists, an impairment loss is recognised in the consolidated statement of income.

Loans and receivablesLoans and receivables are subject to credit risk provision for loan impairment if there is objective evidence that the Group will not be able to collect all amounts due. The amount of the provision is difference between the carrying amount and the recoverable amount, being the present value of expected future cash flows, including amount recoverable from guarantee and collateral, discounted based on the contractual interest rate. The amount of loss arising from impairment is taken to the consolidated statement of income.

In addition, in accordance with CBK instructions, a minimum general provision of 1% for cash facilities and 0.5% for non cash facilities is made on all applicable credit facilities (net of certain categories of collateral), that are not provided for specifically.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

46

First Investment Company K.S.C. (Closed) and its Subsidiaries

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

d) Financial instruments - initial recognition and subsequent measurement (continued)ii) Impairment of financial assets (continued)

Financial assets available-for-saleFor financial assets available-for-sale, the Group assesses at each reporting date whether there is objective evidence that a financial asset or a group of financial assets available-for-sale is impaired.

In the case of equity investments classified as financial assets available-for-sale, objective evidence would include a significant or prolonged decline in the fair value of the equity investment below its cost. ‘Significant’ is evaluated against the original cost of the investment and ‘prolonged’ against the period in which the fair value has been below its original cost. Where there is evidence of impairment, the cumulative loss measured as the difference between the acquisition cost and the current fair value, less any impairment loss on those financial assets available-for-sale previously recognised in the consolidated statement of income, is removed from other comprehensive income and recognised in the consolidated statement of income. Impairment losses on equity investments are not reversed through the consolidated statement of income; increases in their fair value after impairment is recognised directly in other comprehensive income.

iii) Financial liabilities

Initial recognition and measurementFinancial liabilities within the scope of IAS 39 are classified as financial liabilities at fair value through statement of income and loans and borrowings (‘murabaha payables’ and ‘other liabilities’), as appropriate. The Group determines the classification of its financial liabilities at initial recognition.

All financial liabilities are recognised initially at fair value plus, in the case of loans and borrowings, directly attributable transaction costs.

Financial liabilities designated upon initial recognition at fair value through profit or loss are designated at the initial date of recognition, and only if the criteria in IAS 39 are satisfied. The Group has not designated any financial liability as at fair value through profit or loss.

Subsequent measurementThe measurement of financial liabilities depends on their classification as follows:

Murabaha payableMurabaha payable represents the amount payable on a deferred settlement basis for assets purchased under murabaha arrangements. Murabaha payable is stated at the gross amount of the payable, net of deferred profit payable. Profit payable is expensed on a time apportionment basis taking account of the profit rate attributable and the balance outstanding.

Other liabilitiesLiabilities are recognised for amounts to be paid in the future for goods or services received, whether billed by the supplier or not.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

47

First Investment Company K.S.C. (Closed) and its Subsidiaries FIC Annual Report 2012

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

d) Financial instruments - initial recognition and subsequent measurement (continued)iii) Financial liabilities (continued)

Derecognition of financial liabilitiesA financial liability is derecognised when the obligation specified in the contract is discharged, cancelled or expired. When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognised in consolidated statement of income.

iv) Offsetting of financial instrumentsFinancial assets and financial liabilities are offset and the net amount reported in the consolidated statement of financial position if, and only if, there is a currently enforceable legal right to offset the recognised amounts and there is an intention to settle on a net basis, or to realise the assets and settle the liabilities simultaneously.

v) Fair value of financial instrumentsThe fair value of financial instruments that are traded in active markets at each reporting date is determined by reference to quoted market prices or dealer price quotations (bid price for long positions and ask price for short positions), without any deduction for transaction costs.

For financial instruments not traded in an active market, the fair value is determined using appropriate valuation techniques. Such techniques may include using recent arm’s length market transactions; reference to the current fair value of another instrument that is substantially the same; a discounted cash flow analysis or other valuation models.

An analysis of fair values of financial instruments and further details as to how they are measured are provided in Note 24.

e) Investment in associatesAn associate is an entity in which the Group has significant influence and which is neither a subsidiary nor a joint venture. The Group’s investments in its associates are accounted for using the equity method.

Under the equity method, investment in associates is initially recognised at cost and adjusted thereafter for the post-acquisition change in the Group’s share of net assets of the associate. The Group recognises in the consolidated statement of income its share of the total recognised profit or loss of the associate from the date that influence or ownership effectively commenced until the date that it effectively ceases. Distributions received from an associate reduce the carrying amount of the investment. Adjustments to the carrying amount may also be necessary for changes in the Group’s share in the associate arising from changes in the associate’s equity that have not been recognised in the associate’s statement of income. The Group’s share of those changes is recognised in statement of comprehensive income.

Goodwill relating to the associate is included in the carrying amount of the investment and is neither amortised nor individually tested for impairment.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

48

First Investment Company K.S.C. (Closed) and its Subsidiaries

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)e) Investment in associates (continued)

The reporting dates of the associates and the Group are identical and in case of different reporting date of associate from that of the Group, adjustments are made for the effects of significant transactions or events that occur between that date and the date of the Group’s consolidated financial statements. The associate’s accounting policies conform to those used by the Group for the like transactions and events in similar circumstances.

The consolidated statement of income reflects the Group’s share of results of operations of the associates. When there has been a change recognised directly in the equity of the associate, the Group recognises its share of any changes and discloses this, when applicable, in the consolidated statement of changes in equity. Unrealised gains and losses resulting from transactions between the Group and its associate are eliminated to the extent of the Group’s interest in the associate.

After application of the equity method, the Group determines whether it is necessary to recognize an additional impairment loss on the Group’s investment in its associate. The Group determines at each reporting date whether there is any objective evidence that the investment in the associate is impaired. If this is the case, the Group calculates the amount of impairment as the difference between the recoverable amount of the associate and its carrying value and recognizes the amount as ‘impairment loss’ in the consolidated statement of income.

Upon loss of significant influence over the associate, the Group measures and recognises any retaining investment at its fair value. Any difference between the carrying amount of the associate upon loss of significant influence and the fair value of the remaining investment and proceeds from disposal is recognised in the consolidated statement of income.

f) Investment propertiesInvestment properties are initially measured at cost, including transaction costs. Subsequent to initial recognition, investment properties are stated at fair value, which reflects market conditions at the reporting date. Gains or losses arising from changes in the fair values of investment properties are included in the consolidated statement of income in the period in which they arise.

Investment properties are derecognized either when they have been disposed of or when permanently withdrawn from use and no future economic benefit is expected from its disposal. Any gains or losses on the retirement or disposal of investment property are recognized in the consolidated statement of income in the period of derecognition.

Transfers are made to investment properties only when there is a change in use, evidenced by the end of owner occupation, commencement of an operating lease to another party or completion of construction or development. Transfers are made from investment properties only when there is a change in use, evidenced by commencement of owner occupation or commencement of development with a view to sale. For a transfer from investment property to owner occupied property, the deemed cost for subsequent accounting is the fair value at the date of change in use.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

49

First Investment Company K.S.C. (Closed) and its Subsidiaries FIC Annual Report 2012

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

g) Properties under development Properties under development are developed for future sale in the ordinary course of business, rather than to be held for rental or capital appreciation and are stated at lower of cost and net realizable value. Cost includes freehold rights for land, amounts paid to contractors for construction, borrowing costs, planning and design costs, cost of site preparation, professional fees for legal services, property transfer taxes, construction overheads and other related costs. Net realizable value is based on estimated selling price in the ordinary course of the business, based on market prices at the statement of financial position date, less costs to completion and the estimated cost of sale.

h) Impairment of non-financial assetsThe Group assesses at each reporting date whether there is an indication that an asset may be impaired. If any indication exists, or when annual impairment testing for an asset is required, the Group estimates the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or CGU’s fair value less costs to sell and its value in use and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets. When the carrying amount of an asset or CGU exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount. In assessing value in use, the estimated future cash flows are discounted to their present value using a discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. In determining fair value less costs to sell, an appropriate valuation model is used. These calculations are corroborated by available fair value indicators.

An assessment is made at each reporting date whether there is any indication that previously recognised impairment losses may no longer exist or may have decreased. If such indication exists, the Group estimates the asset’s or CGUs recoverable amount. A previously recognised impairment loss is reversed only if there has been a change in the assumptions used to determine the asset’s recoverable amount since the last impairment loss was recognised. The reversal is limited so that the carrying amount of the asset does not exceed its recoverable amount, nor exceed the carrying amount that would have been determined, net of depreciation, had no impairment loss been recognised for the asset in prior years. Such reversal is recognized in the consolidated statement of income unless the asset is carried at a revalued amount, in which case, the reversal is treated as a revaluation increase.

i) Employees’ end of service benefitsProvision is made for amounts payable to employees under the Kuwaiti labour Law, employee contracts and applicable labour laws in the countries where the subsidiaries operate. This liability, which is unfunded, represents the amount payable to each employee as a result of termination of the reporting date.

j) Treasury sharesTreasury shares consist of the Parent Company’s own issued shares that have been reacquired by the Parent Company and not yet reissued or cancelled. The treasury shares are accounted for using the cost method. Under this method, the weighted average cost of the shares reacquired is charged to a contra account in the equity. When the treasury shares are reissued, gains are credited to a separate account in equity, “treasury shares reserve”, which is not distributable. Any realised losses are charged to the same account to the extent of the credit balance on that account. Any excess losses are charged to retained earnings then to the Group’s voluntary reserve and statutory reserve. Gains realised subsequently on the

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSAt 31 December 2012

50

First Investment Company K.S.C. (Closed) and its Subsidiaries

2.3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)j) Treasury shares (continued)

sale of treasury shares are first used to offset any previously recorded losses in the order of reserves, retained earnings and the treasury shares reserve account. No cash dividends are paid on these shares.

The issue of bonus shares increases the number of treasury shares proportionately and reduces the average cost per share without affecting the total cost of treasury shares. Part of the reserves created or appropriated and retained earnings equivalent to the cost of treasury shares is not available for distribution throughout the holding period.

k) Foreign currency translation

The Group’s consolidated financial statements are presented in Kuwaiti Dinars, which is also the Parent Company’s functional and presentation currency. Each entity in the Group determines its own functional currency and items included in the financial statements of each entity are measured using that functional currency.