annual general meeting 21 may 2014 - oracle power plc · pakistan energy yearbook – projected...

TRANSCRIPT

Annual General Meeting

21 May 2014

The information contained in this confidential document (“Presentation”) has been prepared by Oracle Coalfields plc (the “Company”). It has not been fully verified and is subject to material updating, revision and further amendment.

This Presentation has not been approved by an authorised person in accordance with Section 21 of the Financial Services and Markets Act 2000 (“FSMA”) and therefore it is being delivered for information purposes only to a very limited

number of persons and companies who are persons who have professional experience in matters relating to investments and who fall within the category of person set out in Article 19 of the Financial Services and Markets Act 2000

(Financial Promotion) Order 2005 (the “Order”) or are high net worth companies within the meaning set out in Article 49 of the Order or are otherwise permitted to receive it. Any other person who receives this Presentation should not

rely or act upon it. By accepting this Presentation and not immediately returning it, the recipient represents and warrants that they are a person who falls within the above description of persons entitled to receive the Presentation. This

Presentation is not to be disclosed to any other person or used for any other purpose.

Please note that the information in this Presentation has yet to be announced or otherwise made public and as such constitutes relevant information for the purposes of section 118 of FSMA and non-public price sensitive information for

the purposes of the Criminal Justice Act 1993. You should not therefore deal in any way in the securities of the Company until after the formal release of an announcement by the Company as to do so may result in civil and/or criminal

liability.

While the information contained herein has been prepared in good faith, neither the Company nor any of its shareholders, directors, officers, agents, employees or advisers give, have given or have authority to give, any representations

or warranties (express or implied) as to, or in relation to, the accuracy, reliability or completeness of the information in this Presentation, or any revision thereof, or of any other written or oral information made or to be made available to

any interested party or its advisers (all such information being referred to as “Information”) and liability therefore is expressly disclaimed. Accordingly, neither the Company nor any of its shareholders, directors, officers, agents,

employees or advisers take any responsibility for, or will accept any liability whether direct or indirect, express or implied, contractual, tortious, statutory or otherwise, in respect of, the accuracy or completeness of the Information or for

any of the opinions contained herein or for any errors, omissions or misstatements or for any loss, howsoever arising, from the use of this Presentation.

This Presentation may contain forward-looking statements that involve substantial risks and uncertainties, and actual results and developments may differ materially from those expressed or implied by these statements. These forward-

looking statements are statements regarding the Company's intentions, beliefs or current expectations concerning, among other things, the Company's results of operations, financial condition, prospects, growth, strategies and the

industry in which the Company operates. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. These forward-

looking statements speak only as of the date of this Presentation and the Company does not undertake any obligation to publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date

of this Presentation.

Neither the issue of this Presentation nor any part of its contents is to be taken as any form of commitment on the part of the Company to proceed with any transaction and the right is reserved to terminate any discussions or

negotiations with any prospective investors. In no circumstances will the Company be responsible for any costs, losses or expenses incurred in connection with any appraisal or investigation of the Company. In furnishing this

Presentation, the Company does not undertake or agree to any obligation to provide the recipient with access to any additional information or to update this Presentation or to correct any inaccuracies in, or omissions from, this

Presentation which may become apparent.

This Presentation should not be considered as the giving of investment advice by the Company or any of its shareholders, directors, officers, agents, employees or advisers. In particular, this Presentation does not constitute an offer or

invitation to subscribe for or purchase any securities and neither this Presentation nor anything contained herein shall form the basis of any contract or commitment whatsoever. Any decision to subscribe for the Company’s securities

must be made only on the basis of the information contained in the admission document in its final form relating to the Company, which may be different to the information contained in this Presentation. Each party to whom this

Presentation is made available must make its own independent assessment of the Company after making such investigations and taking such advice as may be deemed necessary. In particular, any estimates or projections or opinions

contained herein necessarily involve significant elements of subjective judgment, analysis and assumptions and each recipient should satisfy itself in relation to such matters.

You should be aware of the risks associated with this type of investment and that in emerging markets such as Pakistan, the risks are far greater than in more developed markets (including significant legal, economic and political risks)

and that the Company could potentially lose the benefit of its assets in Pakistan. You acknowledge the high number of expenses and difficulties frequently encountered by companies in the early stages of development, particularly

companies operating in emerging markets and you should be aware that this may lead to the loss of your entire investment.

Neither this Presentation nor any copy of it may be (a) taken or transmitted into Australia, Canada, Japan, the Republic of Ireland, the Republic of South Africa or the United States of America (each a “Restricted Territory”), their

territories or possessions; (b) distributed to any U.S. person (as defined in Regulation S under the United States Securities Act of 1933 (as amended)) or (c) distributed to any individual outside a Restricted Territory who is a resident

thereof in any such case for the purpose of offer for sale or solicitation or invitation to buy or subscribe any securities or in the context where its distribution may be construed as such offer, solicitation or invitation, in any such case

except in compliance with any applicable exemption. The distribution of this document in or to persons subject to other jurisdictions may be restricted by law and persons into whose possession this document comes should inform

themselves about, and observe, any such restrictions. Any failure to comply with these restrictions may constitute a violation of the laws of the relevant jurisdiction.

2

DISCLAIMER

SUMMARY

Oracle advancing its US$1.5bn integrated thermal coal and power plant project in Pakistan, the Thar Coalfield, Province of Sindh, Pakistan;

Oracle is in the process of securing funding from large Chinese groups and power off-take with K-Electric (formerly Karachi Electric Supply Company);

Block VI project is based on 5m tpa coal supplying 600 MW mine-mouth power plant;

Allowable Mine and Power Plant Project IRR of 20.5% in US dollar terms for life of project for projects that reach financial close before the end of 2014 and IRR of 20% in US dollar terms thereafter;

Strong federal and provincial government support.

3

RISING ENERGY & COAL DEMAND

4

• Pakistan has a population of 180m people, sixth largest in the world;

• GDP growth has averaged 4.8%;

• Pakistan relies on imports for more than 20% of its energy needs;

• Critical power shortage in Pakistan; regular power cuts and blackouts;

• Demand for electricity in Pakistan projected to outstrip supply over next 20 years;

• Domestic coal expected to become important as an energy resource;

• Coal burnt for power generation is expected to rise to 25% by 2025;

• Demand for domestic coal supported by steady rise in international energy prices;

• Over reliance on imports of energy; accounts for over 40% of energy use.

Coal accounts for less than 1% of Pakistan’s power sector ... The government projects a rise to 25% of the energy mix by 2025 as part of its energy plan

PAKISTAN’S POWER DEMAND SUPPLY

FORECAST & KEY INTITIATIVES

5

Daimer – Basha Dam (4500 MW)

Average 2% Growth rate assumed

Thar Coal (1200 MW)

Peak Demand

Supply

Average 3% Growth rate based on GDP & Population

Growth

Only plants that have achieved or are likely to achieve financial close included in the supply forecast

Source : Thar Coal Energy Board, Government of Sindh

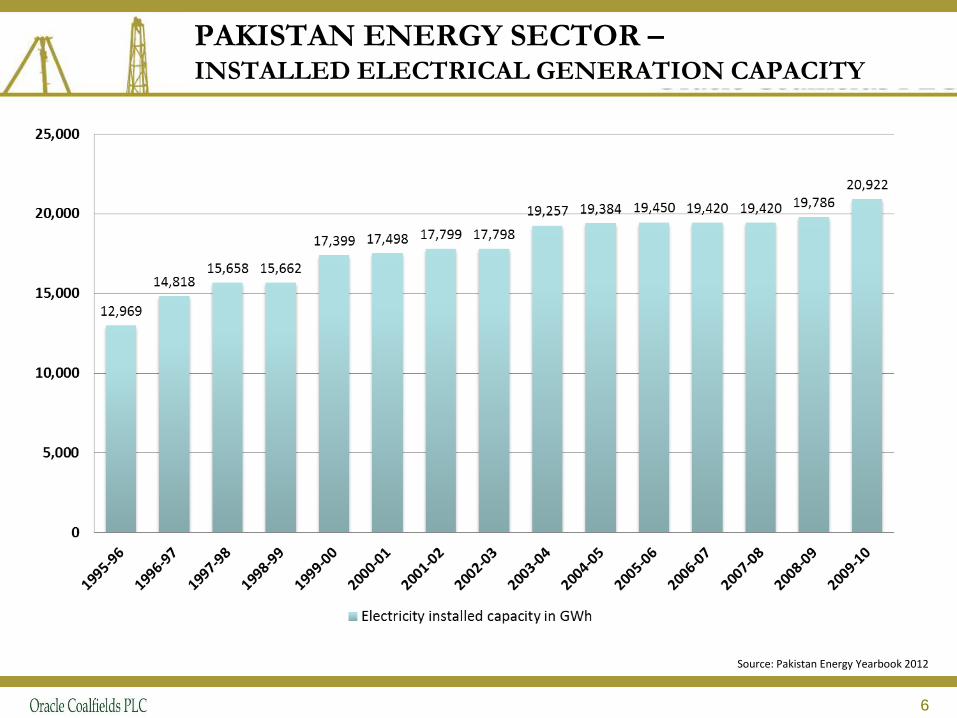

PAKISTAN ENERGY SECTOR – INSTALLED ELECTRICAL GENERATION CAPACITY

6

Source: Pakistan Energy Yearbook 2012

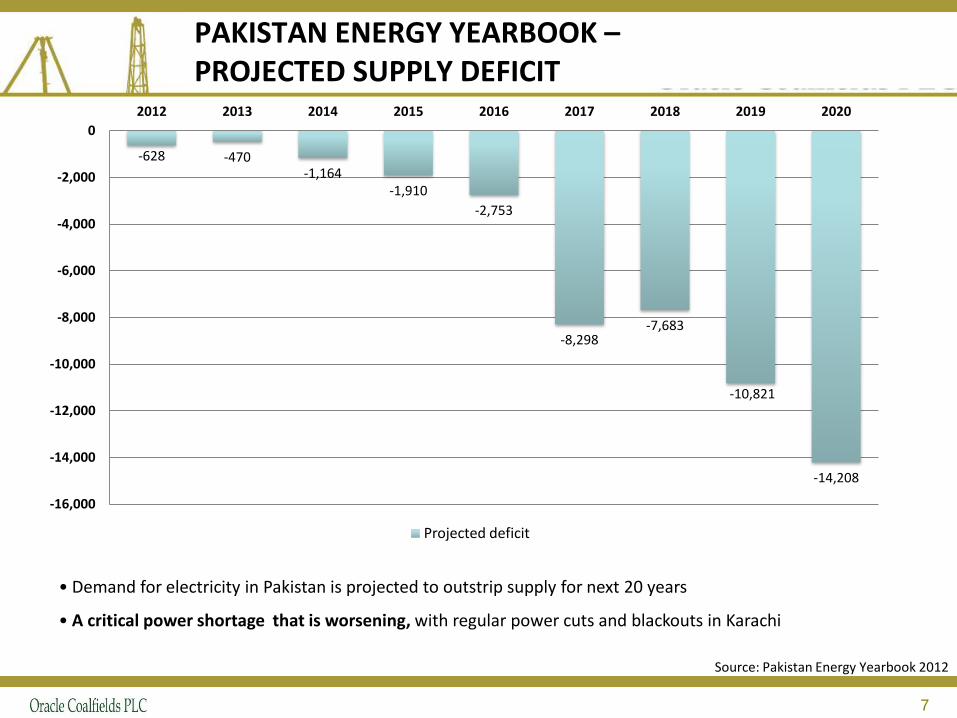

PAKISTAN ENERGY YEARBOOK – PROJECTED SUPPLY DEFICIT

7

• Demand for electricity in Pakistan is projected to outstrip supply for next 20 years

• A critical power shortage that is worsening, with regular power cuts and blackouts in Karachi

-628 -470 -1,164

-1,910

-2,753

-8,298 -7,683

-10,821

-14,208

-16,000

-14,000

-12,000

-10,000

-8,000

-6,000

-4,000

-2,000

0

2012 2013 2014 2015 2016 2017 2018 2019 2020

Projected deficit

Source: Pakistan Energy Yearbook 2012

THAR COALFIELD PROJECT

Located in Sindh Province, South Eastern Pakistan 380km east of Karachi sea port;

175 billion tonnes potential in the Thar coalfield of lignite coal, or 50 billion tonnes of oil equivalent (i.e. greater than the oil reserves of Saudi Arabia and Iran);

Supported by the Thar Coal & Energy Board which enables fast- tracking for Thar projects;

Located in a Special Economic Zone; provides tax incentives;

Cost-Plus Pricing Mechanism; immune to international seaborne coal prices;

Government is supportive and is promoting the use of domestic coal as alternative to imported oil & gas;

Sindh government – keen to progress development; Energy Department;

Sindh government undertaking a series of infrastructure development initiatives including the building of new roads to the coalfield and an airport to service the coalfield.

Sindh Province

Karachi Oracle Project

Area

8

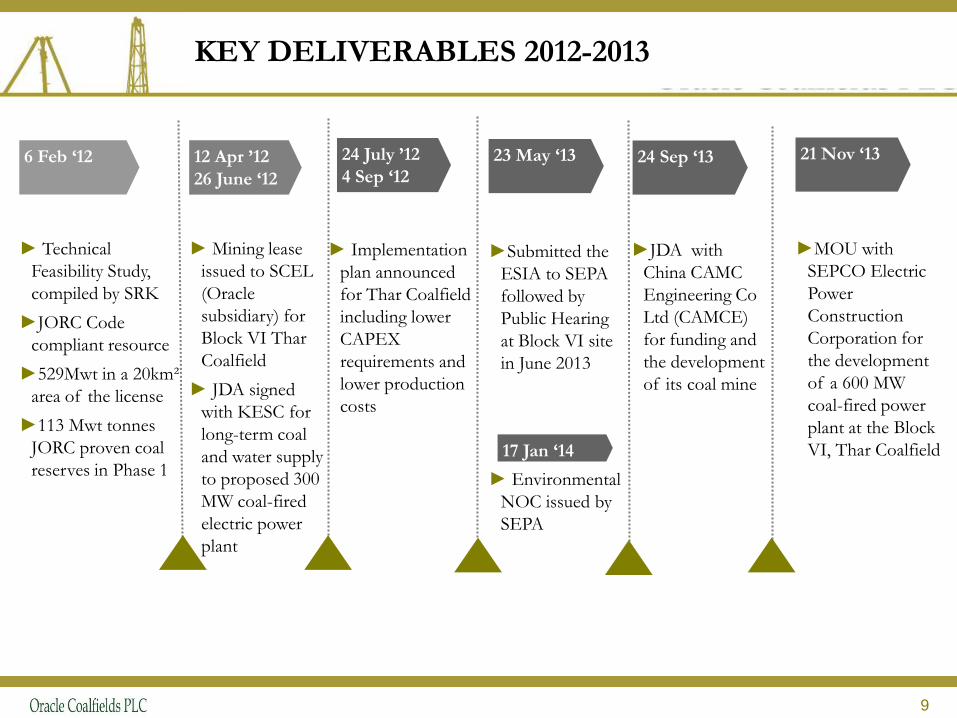

KEY DELIVERABLES 2012-2013

6 Feb ‘12

► Technical

Feasibility Study,

compiled by SRK

►JORC Code

compliant resource

►529Mwt in a 20km²

area of the license

►113 Mwt tonnes

JORC proven coal

reserves in Phase 1

12 Apr ’12

26 June ‘12

► Mining lease

issued to SCEL

(Oracle

subsidiary) for

Block VI Thar

Coalfield

► JDA signed

with KESC for

long-term coal

and water supply

to proposed 300

MW coal-fired

electric power

plant

24 July ’12

4 Sep ‘12

► Implementation

plan announced

for Thar Coalfield

including lower

CAPEX

requirements and

lower production

costs

24 Sep ‘13

►JDA with

China CAMC

Engineering Co

Ltd (CAMCE)

for funding and

the development

of its coal mine

21 Nov ‘13

►MOU with

SEPCO Electric

Power

Construction

Corporation for

the development

of a 600 MW

coal-fired power

plant at the Block

VI, Thar Coalfield

23 May ‘13

►Submitted the

ESIA to SEPA

followed by

Public Hearing

at Block VI site

in June 2013

► Environmental

NOC issued by

SEPA

9

17 Jan ‘14

GROWTH STRATEGY 2014-2015 & KEY ISSUES

1H 2014

►Power Plant EPC

►Mine contractor

►Mine EPC

►Resettlement Plan

2H 2014

1H 2015

2H 2015

►Access road

►Offices &

accommodation

►Power plant

construction begins

►Dewatering begins

► Coal price

►Electricity tariff

►Transmission line

Planning

►Final Investment

Decision

►Overburden

removal

►Mine

construction

10

STRATEGIC RELATIONSHIPS

SEPCO Electric Power Construction Corporation to develop 600 MW power plant

China CAMC Engineering for the development of the coal mine

K-Electric (formally Karachi Electric Supply Company) enter long term PPA and potential equity investor in the power plant

11

MOU WITH CHINESE POWER GROUP ‘SEPCO’

SEPCO Electric Power Construction Corporation

One of China's leading power construction groups;

A company of Power Construction Corporation of China, a major state-owned power business;

Completed construction of 560 power generation units with a total installed capacity of over 93,000MW, transmission lines with a total length of over 18,000km.

Intention of MoU

The development of a 600 MW coal-fired power plant at the Block VI, Thar Coalfield, Province of Sindh, Pakistan;

Planning for an integrated power station to cover its design, construction and operation as well as the financing and investment required;

SEPCO will focus on the development and construction of the power plant;

Undertaking Power Plant feasibility study and EIA;

Provide equity and debt for power plant.

12

JDA WITH CHINESE ENERGY GROUP ‘CAMCE’

China CAMC Engineering Co Ltd (CAMCE)

A subsidiary of China National Machinery Industry Corporation (SINOMACH), which is a major state-owned industrial giant - a Global 500 enterprise;

Extensive experience in international project construction and management.

Intention of JDA

The funding for mine construction;

Mine development and production (*Note: In view of the partnership with SEPCO, CAMCE

shall develop the open-pit mine to support 600MW mine mouth power plant with estimated annual coal production of 5 million tonnes per annum);

13

JDA SIGNING CEREMONY WITH CAMCE

14

Source: Oracle Coalfields September 2013, Beijing

JDA WITH K-ELECTRIC

Intention of JDA

Enter long-term Power Purchase Agreement;

Initially develop 300MW mine-mouth power plant at Block VI site

(*Note: In view of the partnership with SEPCO, the development of power plant will be considered jointly with SEPCO taking the lead).

15

JDA SIGNING CEREMONY WITH KESC

16

Source: Oracle Coalfields July 2012, Karachi

17

AIM: ORCP

Mine Power Plant

*Sindh Electric Power Ltd

Ownership breakdown

Ownership breakdown

*To be registered with SECP

INTENDED COMPANY STRUCTURE

Sindh Carbon Energy Ltd

17

BUSINESS MODEL

18

Government of Sindh

K-ELECTRIC

Transmission Line

Coal Sales Agreement

Power Purchase Agreement, Implementation Agreement

Sindh Carbon Energy Limited

Mining Lease

NEPRA

Cement Other IPPs

(coal conversion)

NTDC

Sindh Electric Power Ltd

Coal Sales Agreements

Electricity tariff

DE-RISKING

19

Technical & Operational risks reduced through the engagement of highly reputable advisors including SRK, Dargo Associates, Mott MacDonald and Wardell Armstrong.

Political and regulatory risks. Development of Thar coal recognised to be of critical importance to the country. If there are adverse regulatory changes, they should be compensated through the fixed IRR.

Security. The company has security precautions in place and will implement additional measures as the project develops.

Environmental and reputational risks. ESIA report prepared by Wardell Armstrong fully to internationally accepted standards. Social Responsibility Programme established, that includes the resettlement of local inhabitants.

Financing risks reduced through engaging with well-financed parties, CAMCE and SEPCO, to provide both debt and equity.

Exchange rate risk. The allowed IRR of 20.5% is US Dollar denominated.

SUMMARY POINTS

20

Compelling valuation, attractive returns;

Oracle’s risk profile has reduced considerably;

New emphasis on the development of domestic energy; resources;

Power generation from Oracle’s Thar coal to be highly competitive;

Attractive development opportunity offering high returns;

Indigenous solution to energy shortage.

APPENDICES

21

22

CORPORATE OVERVIEW

Market cap (£m) 6.00* No. of shares (m) 327* *as of May 2014

Top 10 shareholders Shahrukh Khan 9.9% Andrew Neubauer 6.9% Starvest PLC 6.7% Sunvest Corporation 6.1% Merrion 4.2% Philip Richards 3.9% WH Ireland 3.9% Danske Bank 3.7% GH Pratt 3.2% B Rowan 3.1% Source: Argus Vickers as of February 2014

Nominated Adviser: Grant Thornton UK LLP

Broker: Peterhouse Capital

Solicitors : Trowers & Hamlins LLP UK

Hafeez Pirzada Law Associates / Haidermota & Co.

Corporate Advisers (Pakistan): A.F. Ferguson & Co

Auditors: Price Bailey LLP UK

Financial PR: Fortbridge Consulting /Blythe Weigh

22

DIRECTORS

Adrian Loader

Chairman

► Extensive international experience from Royal Dutch Shell

►Held regional responsibility for Shell's operations in Pakistan

►Board Director of Holcim and Sherritt International

►Has previously been appointed to the following public

company boards - Alliance-Unichem, Shell Canada Ltd,

Alliance-Boots and Candax Energy Inc

Roderick Stead

Non-Executive Director

► Considerable experience in a wide variety of management

roles in the oil, gas, coal, mining and forestry industries in

different environments

►Board experience in over 25 companies

►Worked in several international locations for the Royal Dutch Shell Group of Companies

23

Anthony Scutt

Senior Independent Non-Executive Director

► Qualified Chartered Secretary and a Certified Internal Auditor with the US Institute of Internal Auditors

►Over 30 years of financial management expertise with Shell International Petroleum

►A Non-Executive director of Starvest plc and Beowulf Mining plc

Shahrukh Khan

Chief Executive Officer

► Over nine years’ experience in project finance, with a particular focus upon the natural resource and

infrastructure related sector

►Specialist expertise in large and complex projects

SENIOR MANAGEMENT

Brian Rostron Mining & Contracts Manager ► More than 30 years experience within the civil engineering and mining sectors

►Worked with international mining consultancies on coal mining projects in Montenegro, Russia and Poland.

►He is a member of the Institution of Materials Minerals and Mining,

Simon Smith

Finance Manager

►Background in finance from a twenty-five year career in Shell, in a variety of posts.

►He was Finance Director in Sierra Leone and in Egypt where he also deputised for the Chief Executive. He also worked in Shell’s M&A unit, particularly on the sale of Billiton, Shell’s Metals division, the sale of Shell’s agrochemical interests and the early expansion into eastern Europe.

24

Tony Everitt Company Secretary ► Awarded a BSc in Mathematics with Computer Science from Sussex University. Qualified as a Chartered Accountant in 1991.The next 10 years were spent gaining a wide range of accounting, taxation and auditing experience in an accountancy practice before being admitted as a partner in 2001.

►He left the partnership in 2005 to form his own accountancy practice where he continues to operate as a sole practitioner.

25

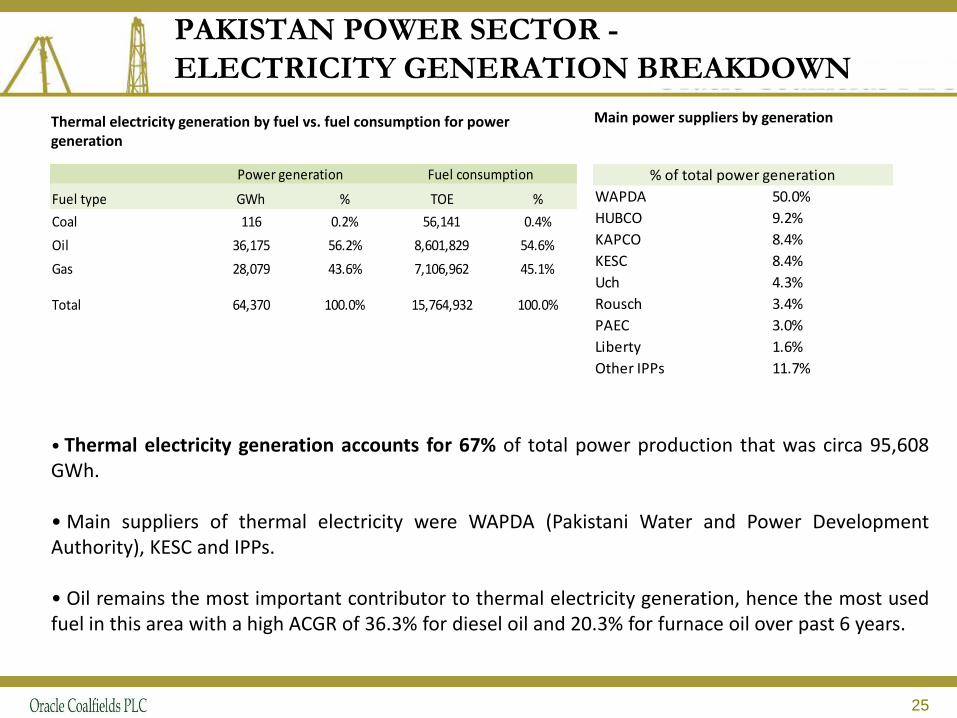

PAKISTAN POWER SECTOR -

ELECTRICITY GENERATION BREAKDOWN

Thermal electricity generation by fuel vs. fuel consumption for power generation

• Thermal electricity generation accounts for 67% of total power production that was circa 95,608 GWh. • Main suppliers of thermal electricity were WAPDA (Pakistani Water and Power Development Authority), KESC and IPPs. • Oil remains the most important contributor to thermal electricity generation, hence the most used fuel in this area with a high ACGR of 36.3% for diesel oil and 20.3% for furnace oil over past 6 years.

Main power suppliers by generation

Fuel type GWh % TOE %

Coal 116 0.2% 56,141 0.4%

Oil 36,175 56.2% 8,601,829 54.6%

Gas 28,079 43.6% 7,106,962 45.1%

Total 64,370 100.0% 15,764,932 100.0%

Power generation Fuel consumption

WAPDA 50.0%

HUBCO 9.2%

KAPCO 8.4%

KESC 8.4%

Uch 4.3%

Rousch 3.4%

PAEC 3.0%

Liberty 1.6%

Other IPPs 11.7%

Total 100.0%

% of total power generation

PAKISTAN ENERGY SECTOR –

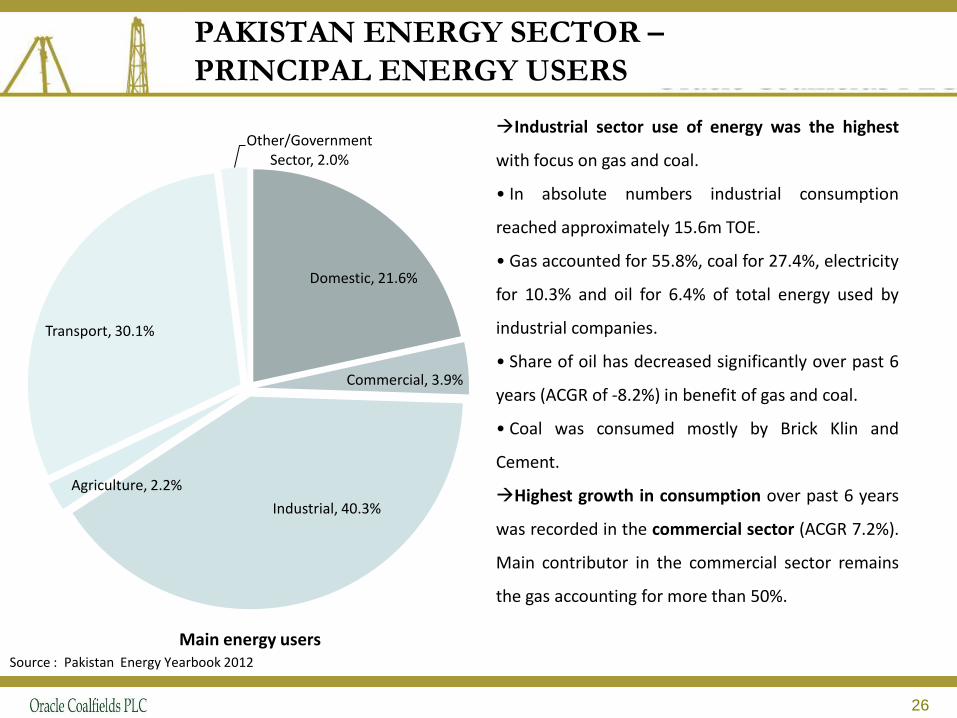

PRINCIPAL ENERGY USERS

26

Domestic, 21.6%

Commercial, 3.9%

Industrial, 40.3%

Agriculture, 2.2%

Transport, 30.1%

Other/Government Sector, 2.0%

Source : Pakistan Energy Yearbook 2012

Main energy users

Industrial sector use of energy was the highest

with focus on gas and coal.

• In absolute numbers industrial consumption

reached approximately 15.6m TOE.

• Gas accounted for 55.8%, coal for 27.4%, electricity

for 10.3% and oil for 6.4% of total energy used by

industrial companies.

• Share of oil has decreased significantly over past 6

years (ACGR of -8.2%) in benefit of gas and coal.

• Coal was consumed mostly by Brick Klin and

Cement.

Highest growth in consumption over past 6 years

was recorded in the commercial sector (ACGR 7.2%).

Main contributor in the commercial sector remains

the gas accounting for more than 50%.

PAKISTAN ENERGY SECTOR –

ELECTRICITY GENERATION BY FUEL TYPE

27

Coal, 0.10%

Oil, 37.80%

Gas, 29.40%

Hydel, 29.40%

Nuclear and Imported, 3.30%

Electricity generation by source

Coal use in power generation Coal-sources generation capacity is projected to increase substantially as part of the government’s energy plan. In 2011-12 coal accounted for less than 1% of Pakistan’s power sector which is expected to rise to 25% by 2025.

Source : Pakistan Energy Yearbook 2012

BLOCK VI COAL RESOURCE - 1

28

Oracle Coalfields main resource, Thar Block VI, is located in Sindh Province, south eastern Pakistan some 380km east of Karachi’s sea port. It forms part of a 175bn lignite coalfield that extends for some 9,100 km²;

Extensive work has been undertaken on the assessment of the commercial viability of the resource by government initiatives and independent international consultants;

Following a drilling programme, SRK Consultants assessed a JORC mineral resource of 529m wet tonnes (mwt) over an area of 20 km² with proven reserves of 113mwt in Phase 1. Oracle’s total resource amounts to 1.4bn tonnes;

Commercially viable lignite coal, with low ash and sulphur content;

Lignite coal suitable for power generation and for industry use, in particular, the cement industry. These sectors are anticipated to be the main off-takers;

Moisture content averages 46%; there is potential to de-water and to supply other industries.

BLOCK VI COAL RESOURCE - 2

29

• Coal in Phase 1 ranges between 16.9m to 39.76m lignite to sub-bituminous in rank;

• The average gross calorific value is 3,182 k cal/wet kg;

• The average ash content is 5.89% and the average sulphur content is 0.91%, as received.

Oracle Coalfields - JORC mineral resource, Phase 1 & 2

Resource Tonnage Moisture RD Gross CV Ash Sulphur

Mwt % wg/cu m kcal/wkg % %

Measured 151 48.0 1.15 3,025 5.10 0.60

Indicated 308 45.3 1.15 3,257 5.60 0.91

Sub total 459 46.2 1.15 3,181 5.44 0.81

Inferred 70 45.4 1.15 3,193 8.90 1.58

Total 529 46.1 1.15 3,182 5.89 0.91Source : SRK, Technical Feasibility Study

BLOCK VI PHASE 1 AND PHASE 2 MINING AREA

30

INTERNATIONALY RENOWNED CONSULTANTS/EXPERTS

31

ENERGY CRISIS & COST TO THE ECONOMY

32

Total cost of load shedding to the economy

Cost as percentage of GDP

Loss of employment in the economy

Loss of exports

USD 2.5 billion

2 % decrease

400,000 jobs

USD 1 Billion

Increasing dependence on expensive imported energy puts a severe constraint on ability to pay Import bill expected to increase to above USD 8 billion by 2020 Source: State of the Economy – Emerging from Crisis 2008, Beacon House National University publication Pakistan Economic Survey 2009

Electricity shortage of more than 4500 MW and frequent power cuts translate to:

Impact/Year

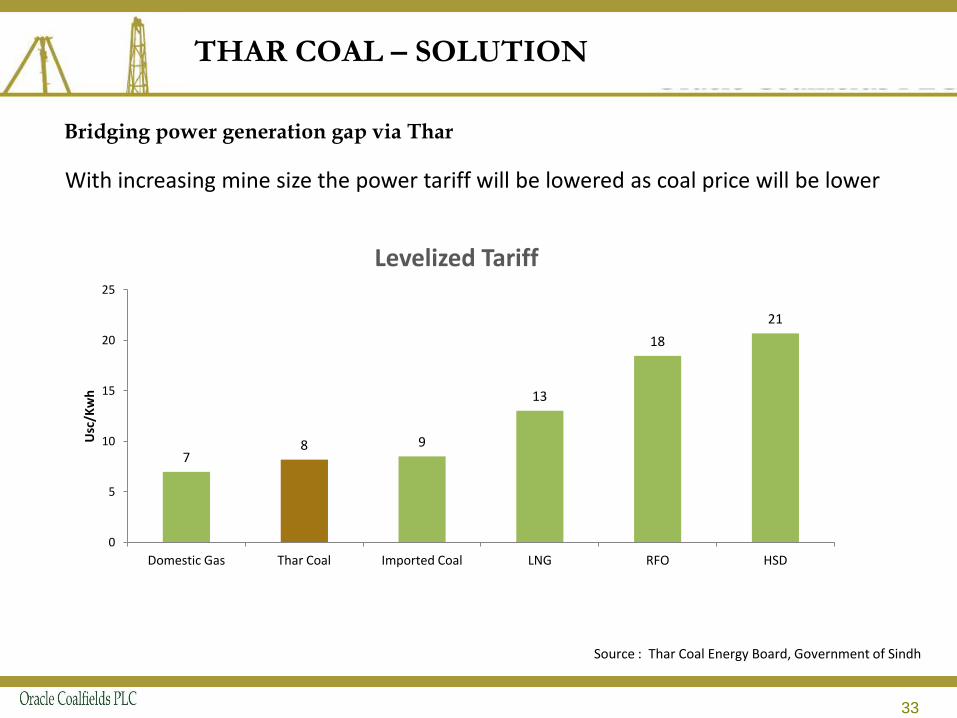

THAR COAL – SOLUTION

33

Source : Thar Coal Energy Board, Government of Sindh

Bridging power generation gap via Thar

With increasing mine size the power tariff will be lowered as coal price will be lower

7 8 9

13

18

21

0

5

10

15

20

25

Domestic Gas Thar Coal Imported Coal LNG RFO HSD

Usc

/Kw

h

Levelized Tariff

GLOBAL LIGNITE COAL COMPARISON

34

Country % age of Electricity

Generated from Coal

Lignite Reserves Billion tonnes

Energy Use (Kg of Oil equivalent per capita)

2009-2013

Access to electricity (% of population)

Ease of Doing

Business Index 1-highest

South Africa 94 30.15* 2795 75.8 41

Poland 93 1.37 2505 NA 45

China 81 18.6 2029 99.7 96

Australia 69 37.2 5892 NA 11

India 68 4.5 614 75 134

Czech Republic 62 0.98 4073 NA 75

USA 49 30.16 6793 NA 4

Germany 49 40.6 3754 NA 21

World Average 41 195.38 1892

Pakistan 0.1 186.2** 482 67.3 110

* Sub bituminous & Anthracite reserves only ** Thar Coal Resources are 175 billion tonnes Proven Reserve in 9 explored Blocks alone is 20 billion tonnes

Source : Thar Coal Energy Board, Government of Sindh

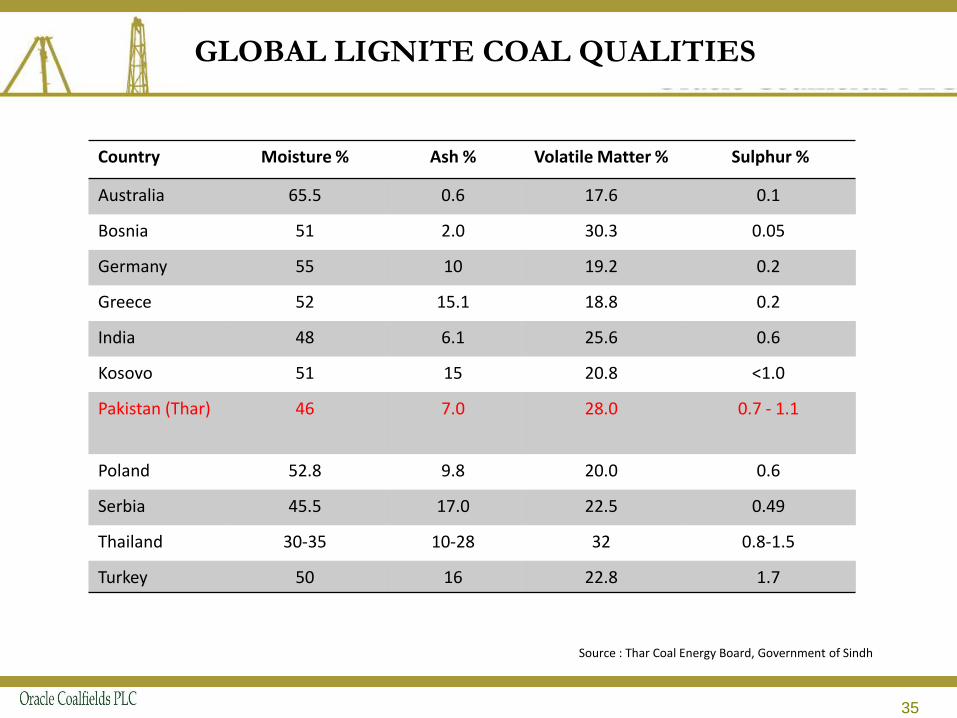

GLOBAL LIGNITE COAL QUALITIES

35

Country Moisture % Ash % Volatile Matter % Sulphur %

Australia 65.5 0.6 17.6 0.1

Bosnia 51 2.0 30.3 0.05

Germany 55 10 19.2 0.2

Greece 52 15.1 18.8 0.2

India 48 6.1 25.6 0.6

Kosovo 51 15 20.8 <1.0

Pakistan (Thar) 46 7.0 28.0 0.7 - 1.1

Poland 52.8 9.8 20.0 0.6

Serbia 45.5 17.0 22.5 0.49

Thailand 30-35 10-28 32 0.8-1.5

Turkey 50 16 22.8 1.7

Source : Thar Coal Energy Board, Government of Sindh

COMPARISON OF THAR LIGNITE

WITH OTHER COUNTRIES

36

Deposit Stripping Ratio

(m³ : t) Heating Value (MJ/kg)

Thar 6.6 : 1 11.6 (5000 Btu/lb)

Kosovo 1 : 1 7.8 (3350 Btu/lb)

Rhenish Area, Germany 4.9 : 1 8.9 (3830 Btu/lb)

Hambach, Germany 6.3 : 1 10.5 (4510 Btu/lb)

Hungary 9 : 1 7.1 (3050 Btu/lb)

Greece 10:1 5.02 (2159 Btu/lb)

Source : Thar Coal Energy Board, Government of Sindh