angle jun ppt

TRANSCRIPT

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 1/14

Sanjoy Bhagat

Rolling Mill- II, May

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 2/14

0

500

1000

1500

2000

2500

3000

3500

4000

4500

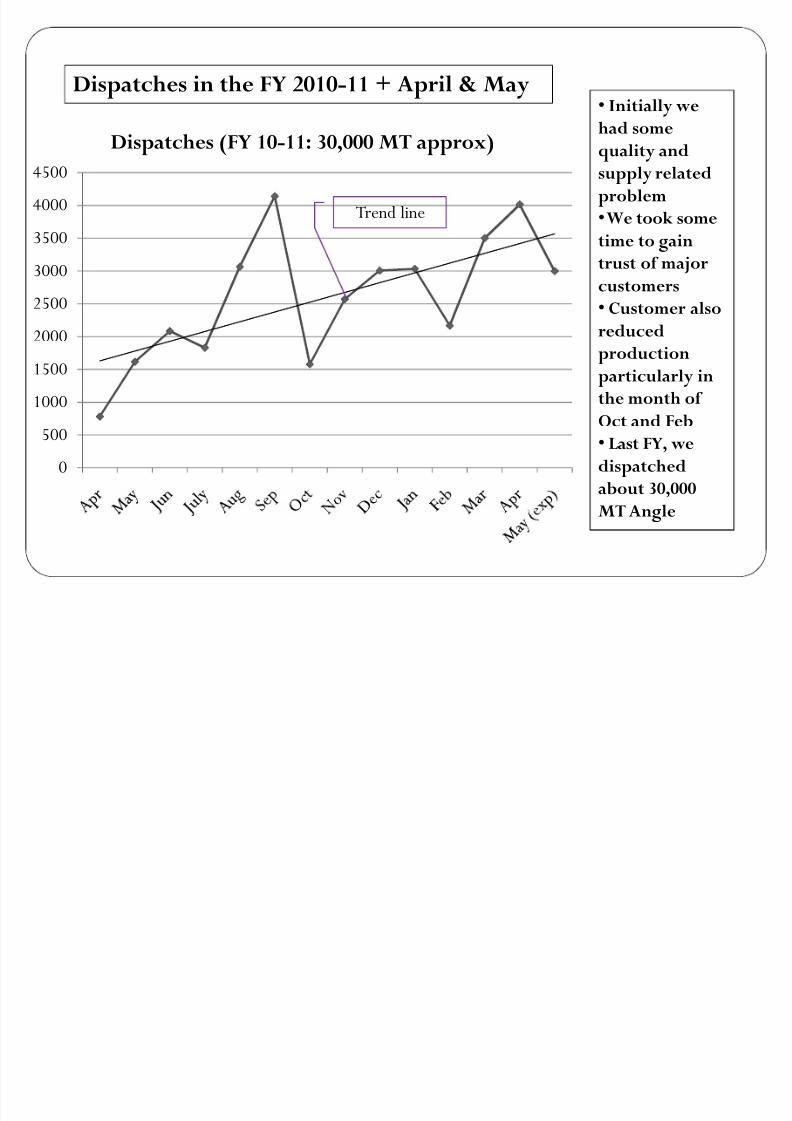

Dispatches (FY 10-11: 30,000 MT approx)

Dispatches in the FY 2010-11 + April & May Initially we

had somequality and

supply related

problem

We took some

time to gain

trust of major

customers

Customer also

reduced

production

particularly in

the month of

Oct and Feb

Last FY, we

dispatched

about 30,000

MT Angle

Trend line

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 3/14

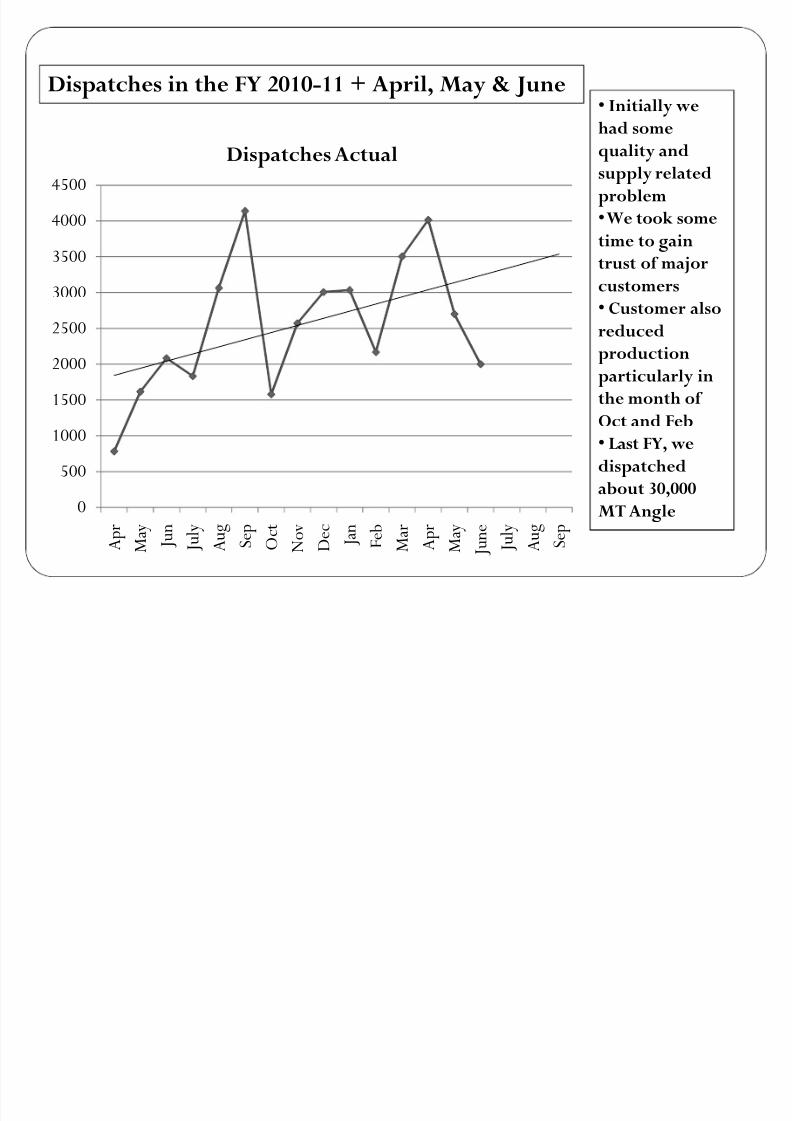

Dispatches in the FY 2010-11 + April, May & June Initially we

had somequality and

supply related

problem

We took some

time to gain

trust of major

customers

Customer also

reduced

production

particularly in

the month of

Oct and Feb

Last FY, we

dispatched

about 30,000

MT Angle0

500

1000

1500

2000

2500

3000

3500

4000

4500

A p r

M

a y

J u n

J u l y

A u g

S e p

O c t

N

o v

D e c

J a n

F e b

M a r

A p r

M

a y

J u n e

J u l y

A u g

S e p

Dispatches Actual

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 4/14

0

500

1000

1500

2000

2500

3000

3500

4000

4500

A p r

M

a y

J u n

J u l y

A u g

S e p

O c t

N

o v

D e c

J a n

F e b

M a r

A p r

M

a y

J

u n e

J u l y

A u g

S e p

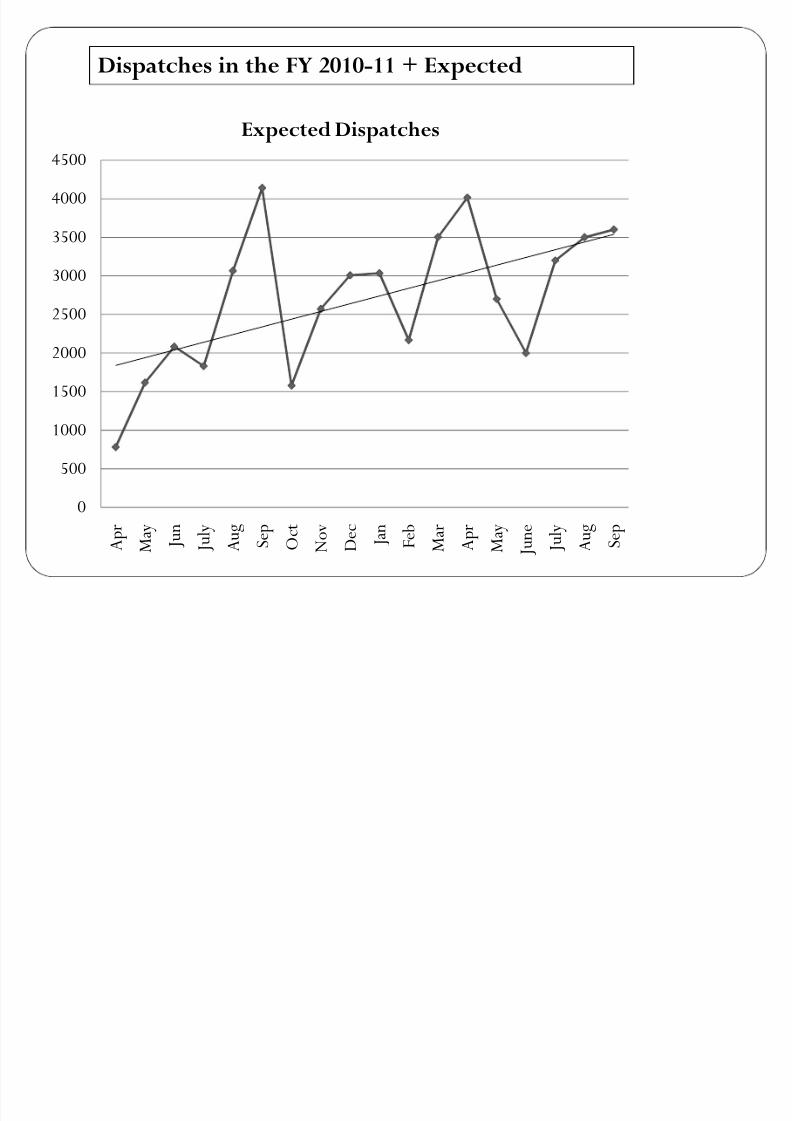

Expected Dispatches

Dispatches in the FY 2010-11 + Expected

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 5/14

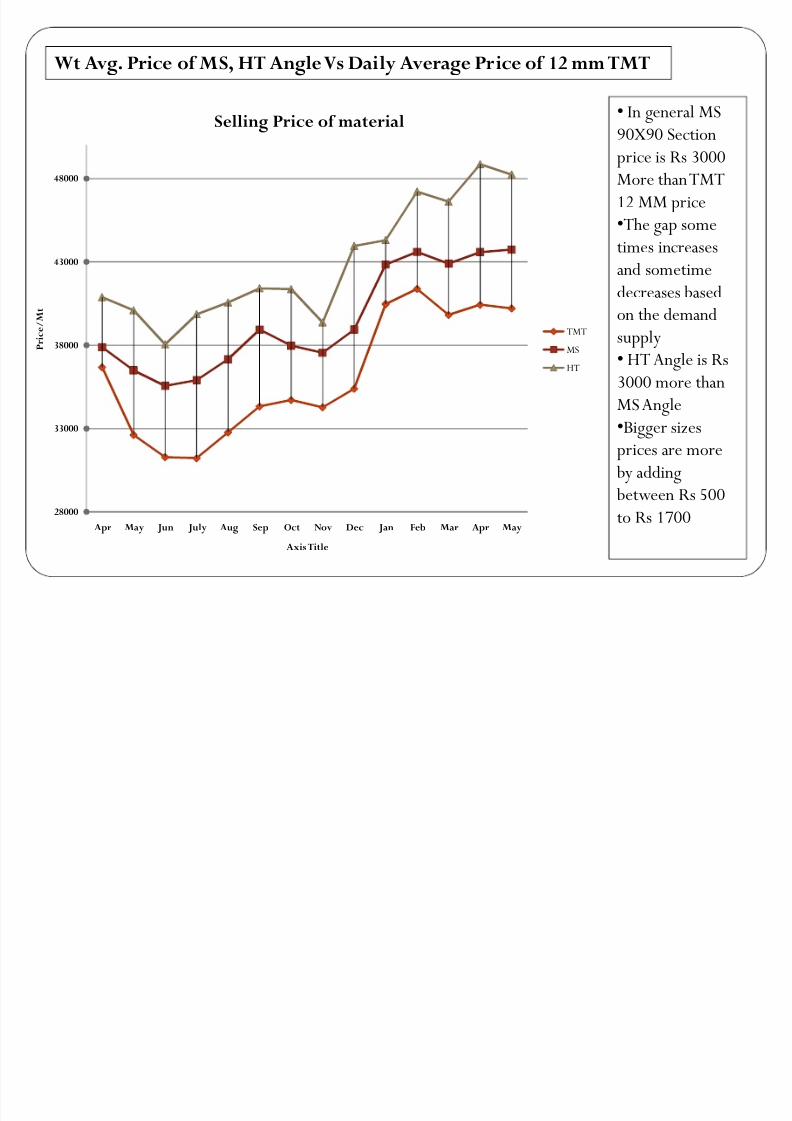

Wt Avg. Price of MS, HT Angle Vs Daily Average Price of 12 mm TMT

In general MS

90X90 Sectionprice is Rs 3000

More thanTMT

12 MM price

The gap some

times increases

and sometime decreases based

on the demand

supply

HT Angle is Rs

3000 more than

MSAngleBigger sizes

prices are more

by adding

between Rs 500

to Rs 1700 28000

33000

38000

43000

48000

Apr May Jun July Aug Sep Oct Nov Dec Jan Feb Mar Apr May

P r i c e / M t

Axis Title

Selling Price of material

TMT

MS

HT

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 6/14

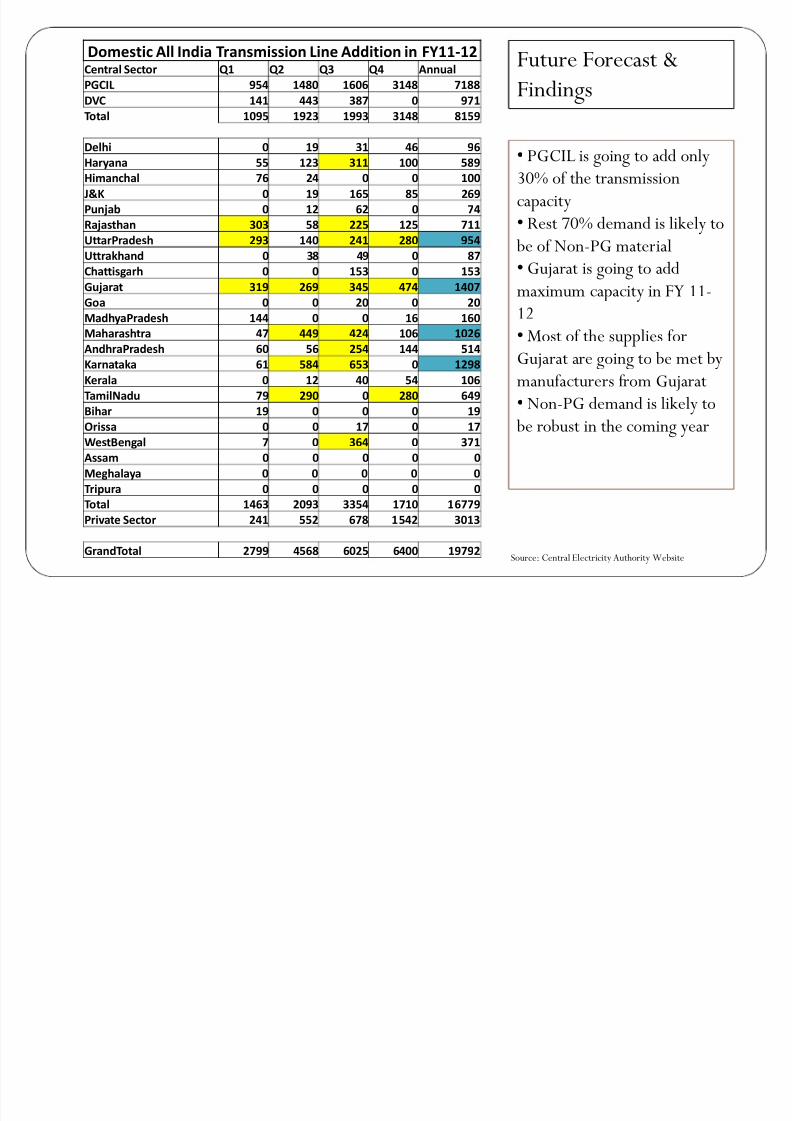

Domestic All India Transmission Line Addition in FY11-12Central Sector Q1 Q2 Q3 Q4 Annual

PGCIL 954 1480 1606 3148 7188

DVC 141 443 387 0 971

Total 1095 1923 1993 3148 8159

Delhi 0 19 31 46 96

Haryana 55 123 311 100 589

Himanchal 76 24 0 0 100

J&K 0 19 165 85 269

Punjab 0 12 62 0 74

Rajasthan 303 58 225 125 711

UttarPradesh 293 140 241 280 954

Uttrakhand 0 38 49 0 87

Chattisgarh 0 0 153 0 153Gujarat 319 269 345 474 1407

Goa 0 0 20 0 20

MadhyaPradesh 144 0 0 16 160

Maharashtra 47 449 424 106 1026

AndhraPradesh 60 56 254 144 514

Karnataka 61 584 653 0 1298

Kerala 0 12 40 54 106

TamilNadu 79 290 0 280 649

Bihar 19 0 0 0 19Orissa 0 0 17 0 17

WestBengal 7 0 364 0 371

Assam 0 0 0 0 0

Meghalaya 0 0 0 0 0

Tripura 0 0 0 0 0

Total 1463 2093 3354 1710 16779

Private Sector 241 552 678 1542 3013

GrandTotal 2799 4568 6025 6400 19792

PGCIL is going to add only

30% of the transmission

capacity

Rest 70% demand is likely to

be of Non-PG material

Gujarat is going to addmaximum capacity in FY 11-

12

Most of the supplies for

Gujarat are going to be met by

manufacturers f rom Gujarat

Non-PG demand is likely to

be ro bust in the coming year

Future Forecast &

Findings

Source: Central ElectricityAuthority Website

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 7/14

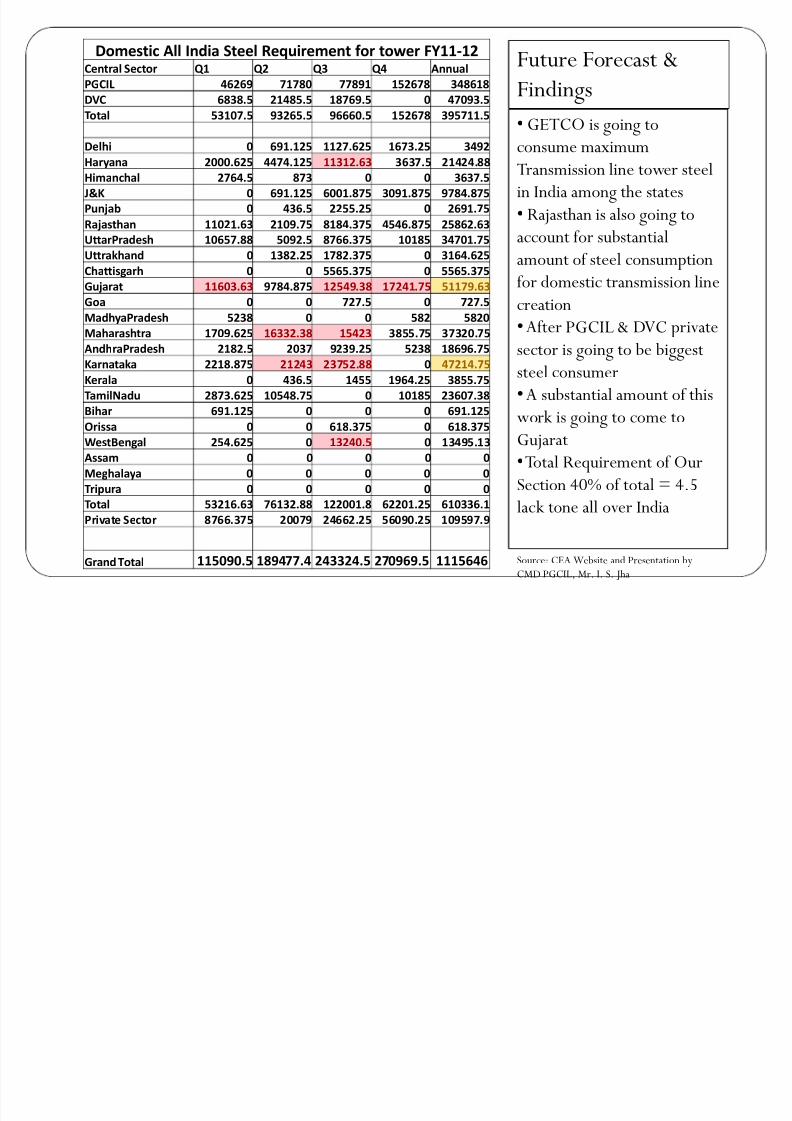

Domestic All India Steel Requirement for tower FY11-12Central Sector Q1 Q2 Q3 Q4 Annual

PGCIL 46269 71780 77891 152678 348618

DVC 6838.5 21485.5 18769.5 0 47093.5

Total 53107.5 93265.5 96660.5 152678 395711.5

Delhi 0 691.125 1127.625 1673.25 3492

Haryana 2000.625 4474.125 11312.63 3637.5 21424.88

Himanchal 2764.5 873 0 0 3637.5

J&K 0 691.125 6001.875 3091.875 9784.875

Punjab 0 436.5 2255.25 0 2691.75

Rajasthan 11021.63 2109.75 8184.375 4546.875 25862.63

UttarPradesh 10657.88 5092.5 8766.375 10185 34701.75

Uttrakhand 0 1382.25 1782.375 0 3164.625

Chattisgarh 0 0 5565.375 0 5565.375Gujarat 11603.63 9784.875 12549.38 17241.75 51179.63

Goa 0 0 727.5 0 727.5

MadhyaPradesh 5238 0 0 582 5820

Maharashtra 1709.625 16332.38 15423 3855.75 37320.75

AndhraPradesh 2182.5 2037 9239.25 5238 18696.75

Karnataka 2218.875 21243 23752.88 0 47214.75

Kerala 0 436.5 1455 1964.25 3855.75

TamilNadu 2873.625 10548.75 0 10185 23607.38

Bihar 691.125 0 0 0 691.125Orissa 0 0 618.375 0 618.375

WestBengal 254.625 0 13240.5 0 13495.13

Assam 0 0 0 0 0

Meghalaya 0 0 0 0 0

Tripura 0 0 0 0 0

Total 53216.63 76132.88 122001.8 62201.25 610336.1

Private Sector 8766.375 20079 24662.25 56090.25 109597.9

Grand Total 115090.5 189477.4 243324.5 270969.5 1115646

Future Forecast &

Findings

GETCO is going to

consume maximum

Transmission line tower steel

in India among the states

Rajasthan is also going to

account for su bstantial

amount of steel consumption

for domestic transmission line creation

After PGCIL & DVC private

sector is going to be biggest

steel consumer

A su bstantial amount of this

work is going to come toGujarat

Total Requirement of Our

Section 40% of total = 4.5

lack tone all over India

Source: CEA Website and Presentation by

CMD PGCIL, Mr. I. S. Jha

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 8/14

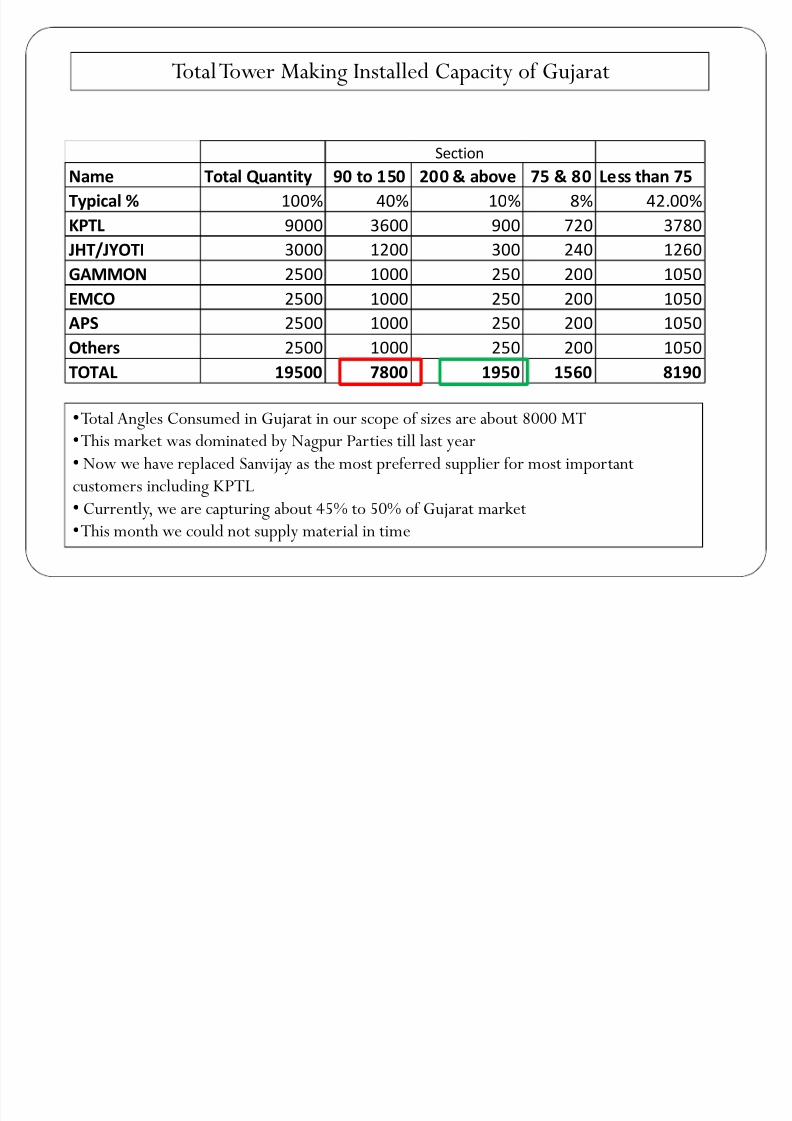

Name Total Quantity 90 to 150 200 & above 75 & 80 Less than 75

Typical % 100% 40% 10% 8% 42.00%

KPTL 9000 3600 900 720 3780

JHT/JYOTI 3000 1200 300 240 1260

GAMMON 2500 1000 250 200 1050

EMCO 2500 1000 250 200 1050

APS 2500 1000 250 200 1050

Others 2500 1000 250 200 1050

TOTAL 19500 7800 1950 1560 8190

Section

TotalTower Making Installed Capacity of Gujarat

TotalAngles Consumed in Gujarat in our scope of sizes are a bout 8000 MTThis market was dominated by Nagpur Parties till last year

Now we have replaced Sanvijay as the most pref erred supplier for most important

customers including KPTL

Currently, we are capturing a bout 45% to 50% of Gujarat market

This month we could not supply material in time

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 9/14

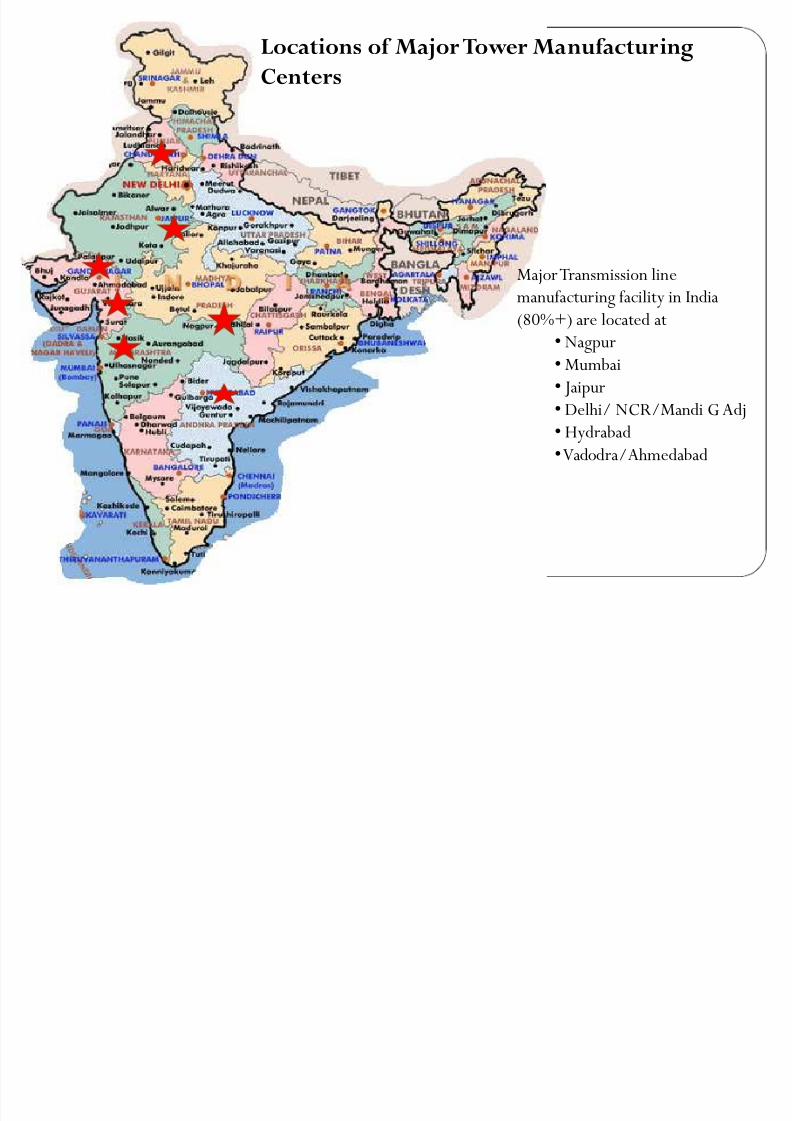

Locations of Major Tower Manufacturing

Centers

Major Transmission line manufacturing facility in India

(80%+) are located at

Nagpur

Mum bai

Jaipur

Delhi/ NCR/Mandi G Adj Hydra bad

Vadodra/Ahmeda bad

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 10/14

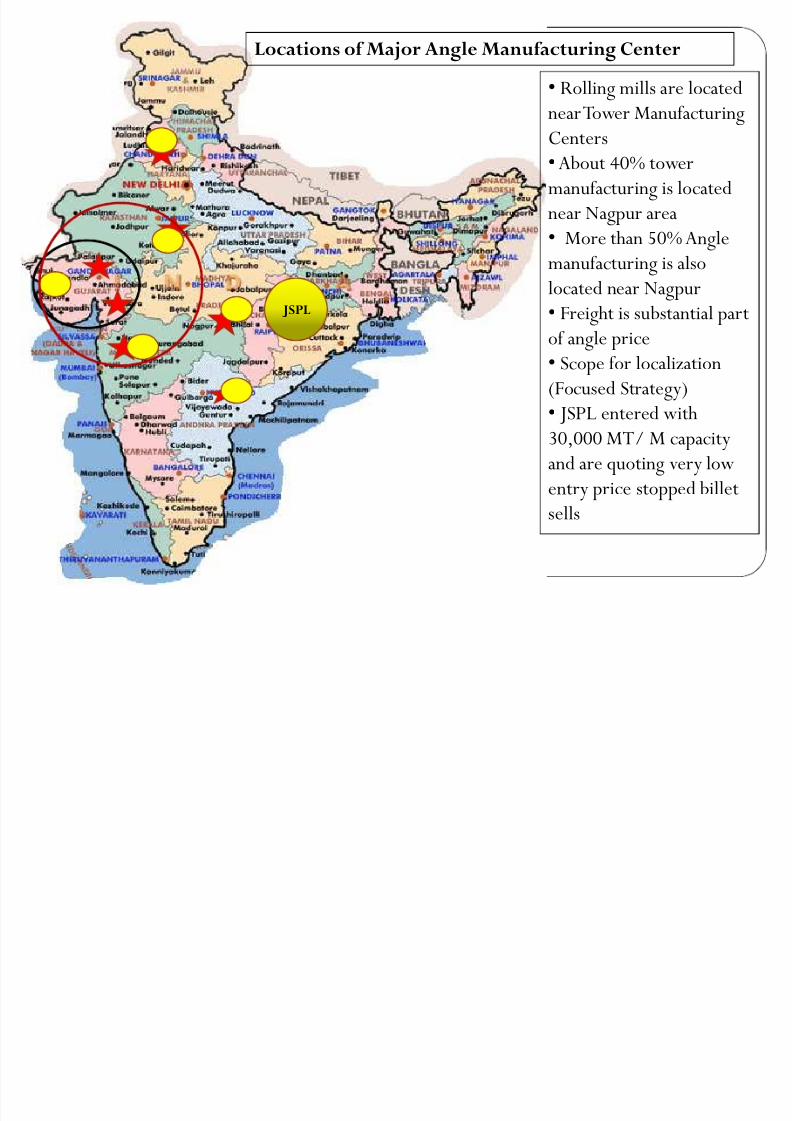

JSPL

Locations of Major Angle Manufacturing Center

Rolling mills are located

near Tower Manufacturing

CentersA bout 40% tower

manufacturing is located

near Nagpur area

More than 50% Angle

manufacturing is also

located near Nagpur

Freight is su bstantial part

of angle price

Scope for localization

(Focused Strategy)

JSPL entered with30,000 MT/ M capacity

and are quoting very low

entry price stopped billet

sells

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 11/14

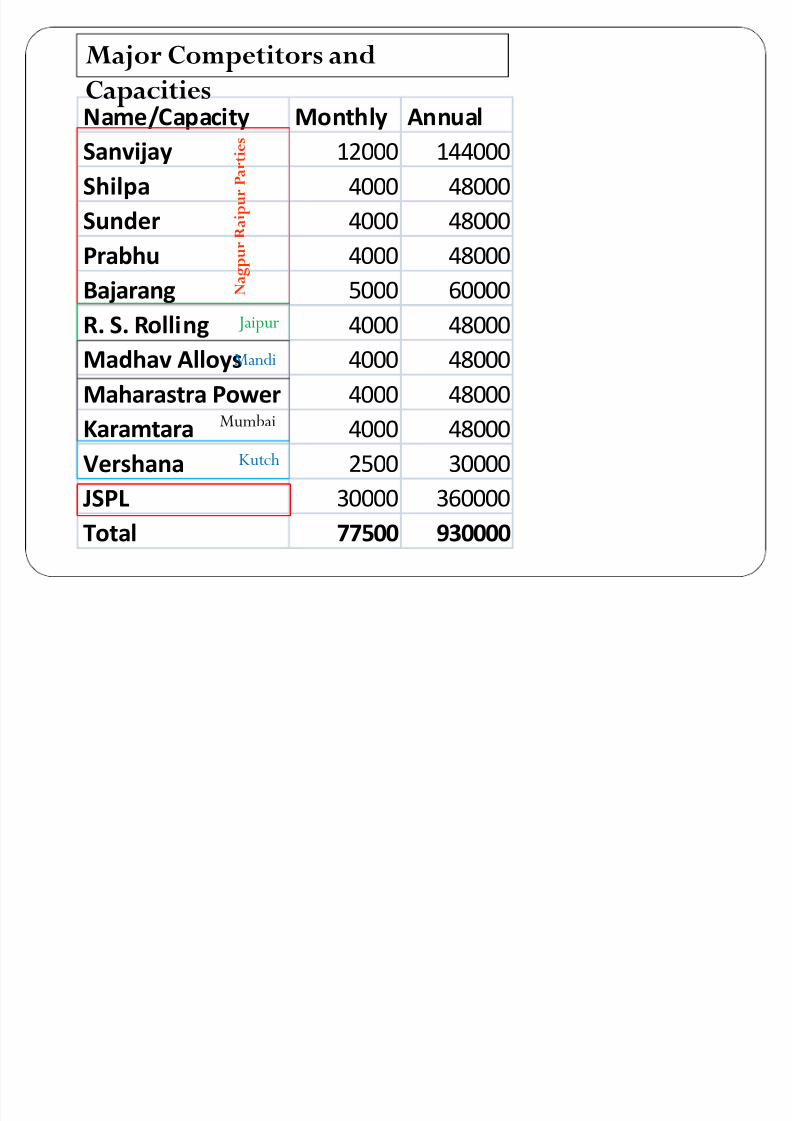

Name/Capacity Monthly Annual

Sanvijay 12000 144000

Shilpa 4000 48000

Sunder 4000 48000

Prabhu 4000 48000

Bajarang 5000 60000

R. S. Rolling 4000 48000

Madhav Alloys 4000 48000

Maharastra Power 4000 48000

Karamtara 4000 48000

Vershana 2500 30000

JSPL 30000 360000

Total 77500 930000

Major Competitors and

Capacities

N a g p u r R a i p u r P a r t i e s

Jaipur

Mandi

Mum bai

Kutch

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 12/14

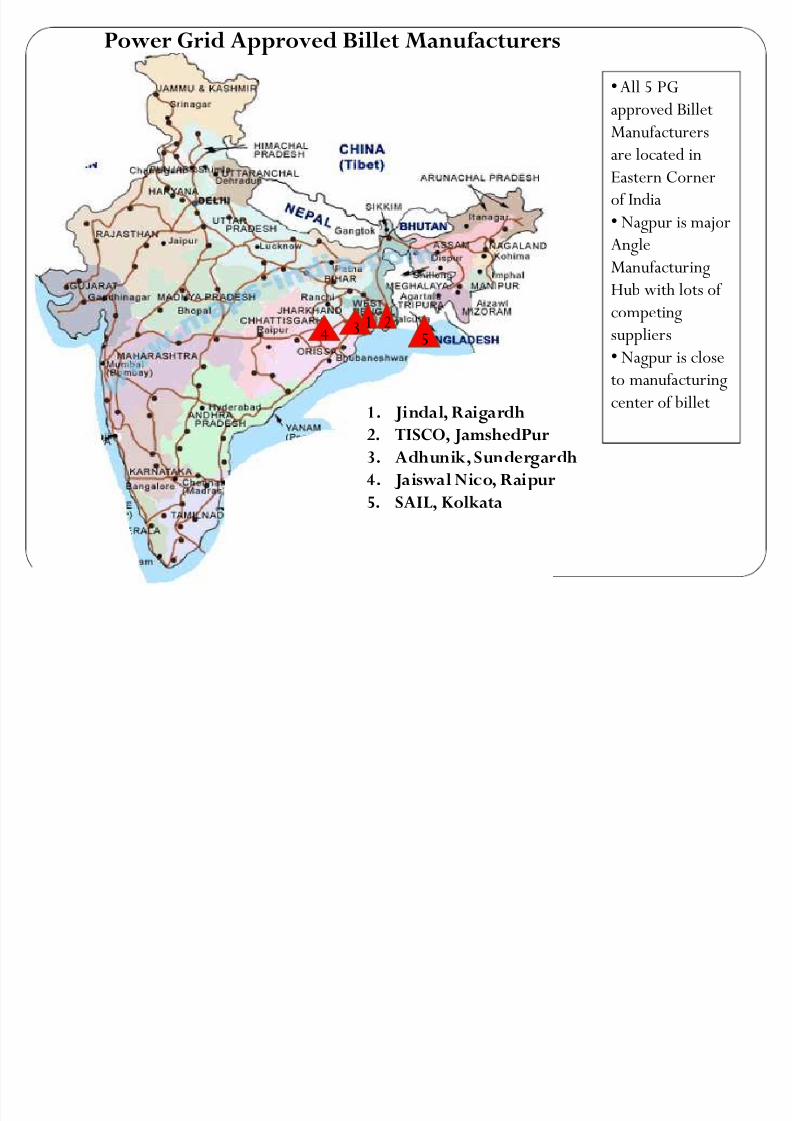

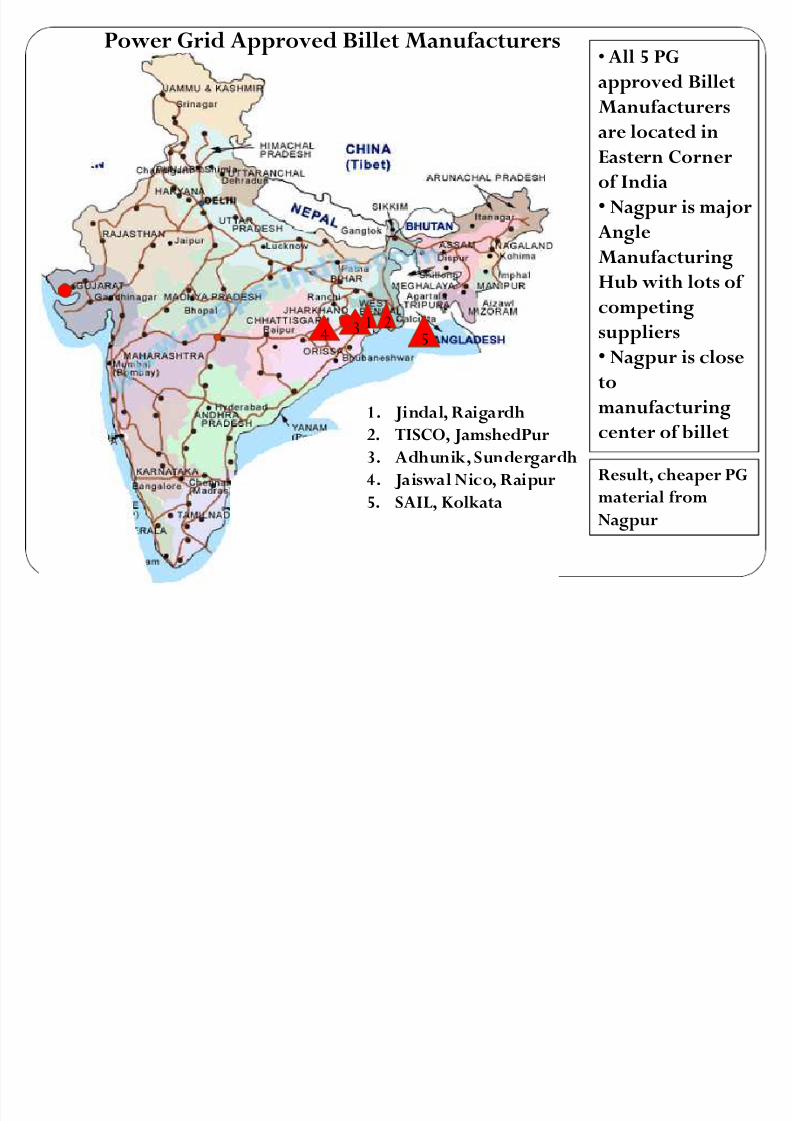

54 3 21

Power Grid Approved Billet Manufacturers

1. Jindal, Raigardh2. TISCO, JamshedPur

3. Adhunik, Sundergardh

4. Jaiswal Nico, Raipur

5. SAIL, Kolkata

All 5 PG

approved Billet

Manufacturersare located in

Eastern Corner

of India

Nagpur is major

Angle

Manufa

cturingHu b with lots of

competing

suppliers

Nagpur is close

to manufacturing

center of billet

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 13/14

54 3 21

Power Grid Approved Billet Manufacturers

1. Jindal, Raigardh2. TISCO, JamshedPur

3. Adhunik, Sundergardh

4. Jaiswal Nico, Raipur

5. SAIL, Kolkata

All 5 PG

approved Billet

Manufacturers

are located inEastern Corner

of India

Nagpur is major

Angle

Manufacturing

Hub with lots of competing

suppliers

Nagpur is close

to

manufacturingcenter of billet

Result, cheaper PG

material from

Nagpur

8/3/2019 Angle Jun Ppt

http://slidepdf.com/reader/full/angle-jun-ppt 14/14

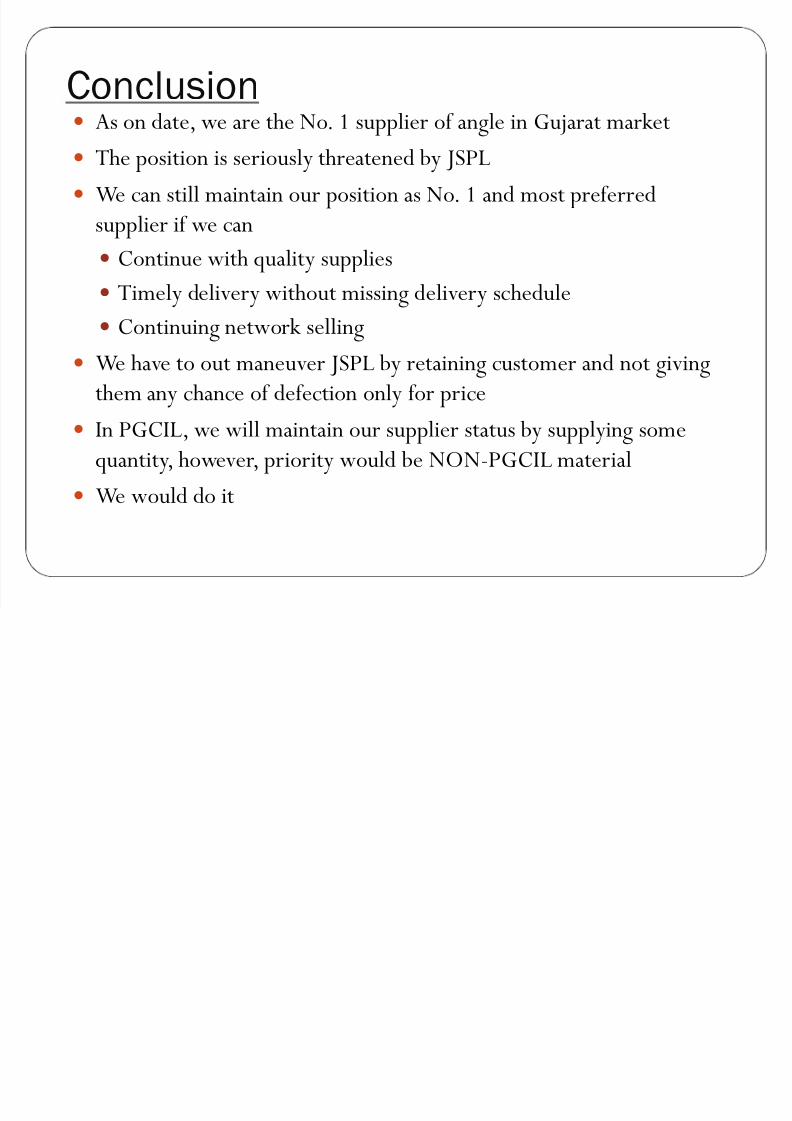

Conclusiony As on date, we are the No. 1 supplier of angle in Gujarat market

y The position is seriously threatened by JSPL

y We can still maintain our position as No. 1 and most pref erred

supplier if we can

y Continue with quality supplies

y Timely delivery without missing delivery schedule

y Continuing network selling

y We have to out maneuver JSPL by retaining customer and not giving

them any chance of def ection only for price

y In PGCIL, we will maintain our supplier status by supplying some

quantity, however, priority would be NON-PGCIL material

y We would do it