analyst presentation 2015/16

TRANSCRIPT

Analyst and Investor Presentation

11 November 2015

2015/16 Interim results - 30 September 2015

“Our turnaround is on course”

Legal disclaimer

This presentation has been prepared by Flybe Group plc (the “Company”). This presentation does not constitute or form part of any offer to sell or issue, or

invitation to purchase or subscribe for, or any solicitation of any offer to purchase or subscribe for, any securities of the Company or in any other entity, nor

shall this document or any part of it, or the fact of its presentation, form the basis of, or be relied on in connection with, any contract or investment decision, nor

does it constitute a recommendation regarding the securities of the Company or any other company.

The information contained in this presentation has not been independently verified. This presentation does not purport to be all-inclusive or to contain all the

information that a prospective investor in securities of the Company may desire or require in deciding whether or not to offer to purchase such securities.

No representation or warranty, express or implied, is made or given by or on behalf of the Company or any of its affiliates (within the meaning of Rule 405

under the US Securities Act 1933) (“Affiliates”), members, directors, officers or employees or any other person as to the accuracy, completeness or fairness of

the information or opinions contained in this presentation or any other material discussed verbally. None of the Company or any of its Affiliates, members,

directors, officers or employees nor any other person accepts any liability whatsoever for any loss howsoever arising from any use of this presentation or its

contents or otherwise arising in connection therewith.

The information in this presentation includes forward-looking statements which are based on the Company's or, as appropriate, the Company's directors'

current expectations and projections about future events. These forward-looking statements may be identified by the use of forward-looking terminology,

including the terms "believes", "estimates", "plans", "projects", "anticipates", "expects", "intends", "may", "will" or "should" or, in each case, their negative or

other variations or comparable terminology, or by discussion of strategy, plans, objectives, goals, future events or intentions. These forward-looking

statements, as well as those included in any other material discussed at any analyst presentation, are subject to risks, uncertainties and assumptions about the

Company and its subsidiaries and investments, including, among other things, the development of its business, trends in its operating industry, and future

capital expenditures. In light of these risks, uncertainties and assumptions, the events or circumstances referred to in the forward-looking statements may differ

materially from those indicated in these statements.

Forward-looking statements may and often do materially differ from actual results. None of the future projections, expectations, estimates or prospects in this

presentation should be taken as forecasts or promises nor should they be taken as implying any indication, assurance or guarantee that the assumptions on

which such future projections, expectations, estimates or prospects have been prepared are correct or exhaustive or, in the case of the assumptions, fully

stated in the presentation. Forward-looking statements speak only as of the date of this presentation. Subject to obligations under the listing rules and

disclosure rules made by the Financial Services Authority under Part VI of the Financial Services and Markets Act 2000 (as amended), neither the Company

nor any of its affiliates, or individuals acting on its behalf, undertakes to publicly update or revise any such forward-looking statement, whether as a result of

new information, future events or otherwise. As a result of these risks, uncertainties and assumptions, you should not place undue reliance on these forward-

looking statements as a prediction of actual results or otherwise.

The information and opinions contained in this presentation and any other are material discussed verbally are provided as at the date of this presentation and

are subject to verification, completion and change without notice.

In giving this presentation, neither the Company nor its advisers and/or agents undertakes any obligation to provide the recipient with access to any additional

information or to update this presentation or any additional information or to correct any inaccuracies in any such information which may become apparent.

© Flybe 2015 2 © Flybe 2015 2

Agenda

Welcome – Saad Hammad

Business update – Saad Hammad

Financial review – Philip de Klerk

Summary & Q&A

© Flybe 2015 3

Business update – Saad Hammad

© Flybe 2015 3

Key H1 highlights

• Strong core business performance

– Third consecutive quarter with double digit capacity, passenger volume and

revenue growth

– Continued unit cost reduction

– Return to profit

– Improved cash generation

• Project Blackbird complete

– Solutions for all surplus 14 E195 jets now delivered

– c£40m mitigation vs. £80m of outstanding lease obligations

© Flybe 2015 4 © Flybe 2015 4

FINANCIAL REVIEW

• Revenue and profit improvement in core business

• Sustained improvement in cost per seat excluding fuel

• Cash generation improved in H1 with overall net cash inflow from

operating activities of £21.3m (H1 2014/15: inflow of £6.5m)

• At 30 September 2015, the Group’s balance sheet remained strong with

net assets of £172.8m, including total cash of £197.2m and net funds of

£86.3m, up £9.6m vs. year end

© Flybe 2015 6

Key H1 2015/16 Group Financials - Summary

Net funds = Total cash less total borrowings

© Flybe 2015 7 Company Confidential & Proprietary

• Revenue growth driven by

13.1% increase in UK capacity

• Within H1 2015/16 Group

Revenue - FAS 3rd party revenue £8.7m

- Other revenue £5.9m

- Contract flying (White Label)

£5.0m

Group revenue increased by 10.3% in line with plan

Flybe Group Revenue Components H1 2014/15 vs. H1 2015/16

Encouraging H1 profit development

© Flybe 2015 8

£m H1 2014/15 H1 2015/16 YOY change

Flybe UK (0.7) 23.5 24.2

FAS 1.5 (0.3) (1.8)

Group costs (1.8) (2.1) (0.3)

Adjusted profit/(loss) before tax (1.0) 21.1 22.1

Revaluation gains/(losses) on USD loans (2.3) 1.8 4.1

Reported profit/(loss) of continuing operations before tax (3.3) 22.9 26.2

Tax (charge) /credit (0.1) 3.9 4.0

Profit/(loss) of continuing operations after tax (3.4) 26.8 30.2

Discontinued Operations (12.0) 0.0 12.0

Reported profit/(loss) after tax (15.4) 26.8 42.2

Adjusted EBITDAR 47.0 70.5 23.5

Earnings/(loss) per share (basic), pence (7.1) 12.3 19.4

RPS dilution managed while driving double digit seat capacity growth

© Flybe 2015 9

Flybe UK H1 2014/15 vs. H1 2015/16

Operational Headlines & Unit Revenue by Component

Operational Headlines

Unit Revenue by Component

H1 2014/15 H1 2015/16 YOY Change %

Seats, m 5.2 5.9 13.1 %

Passengers, m 4.1 4.5 10.2 %

Load factor, % 78.2 % 76.3 % (2.0) ppts

Average passenger sector length, km 495 479 (3.2)%

£ per seat H1 2014/15 H1 2015/16 YOY Change

Passenger revenue 54.75 54.56 (0.3)%

Other revenue, incl. contract flying 2.61 1.85 (29.1)%

Total Flybe UK revenue 57.36 56.42 (1.6)%

Hedging continues to be in line with policy

10

Fuel

Market price down by 42% in US dollars

But largely hedged, so effective price down 13% at USD 835

USD

Market rate adverse by 7%

Post hedge rate improved by 3% at USD 1.62

Resulting in GBP cost of fuel falling by 16%

Outlook

Fuel: 86% hedged in H2 at USD 855, 70% H1 next year at USD 668

USD : 76% hedged in H2 at USD 1.57, 65% H1 next year at USD 1.54

© Flybe 2015 10

We improved profit per seat

11

1.6% decrease in

Total Revenue Per Seat

8.9% decrease in

Cost Per Seat

(7% decrease at constant currency)

• Total Flybe UK revenue per seat includes ticket revenue, ancillary revenue, refunds and hardblock codeshare revenue

• Cost per seat is Flybe UK adjusted cost

• Profit per seat is Total Flybe UK revenue less Flybe UK adjusted cost

© Flybe 2015

£4.18 improvement in

Profit Per Seat

7.0% reduction in Cost Per Seat at constant currency

© Flybe 2015 12

Costs exclude USD loan revaluation.

Surplus aircraft cost is included within aircraft ownership and maintenance cost.

Flybe UK H1 2014/15 vs. H1 2015/16 Unit Cost Bridge

Cost per seat reduced by 5.8% excl.

£4m historical EU261 provision in

prior year

Strong operating cash flow of £21.3m

© Flybe 2015 13

Includes: • £7.7m aircraft parts and

modifications • £3.7m land & buildings, plant &

equipment, assets under construction

Group Cash Flow Bridge 2014/15 to H1 2015/16

195.9 197.2

21.3 (12.3) (7.7)

0

50

100

150

200

250

Total cash at March 2015 Operating cash flow Investing activities Financing activities Total cash at September2015

£m

• Revenue and profit improvement in core business

• Sustained improvement in cost per seat excluding fuel

• Cash generation improved in H1 with overall net cash inflow from

operating activities of £21.3m (H1 2014/15: inflow of £6.5m)

• At 30 September 2015, the Group’s balance sheet remained strong with

net assets of £172.8m, including total cash of £197.2m and net funds of

£86.3m, up £9.6m vs. year end

© Flybe 2015 14

Key H1 2015/16 Group Financials - Summary

Net funds = total cash less total borrowings

BUSINESS UPDATE

• Continued progress in building a strong core business

- Revenue growth and cost improvement plus operational and white

label progress

- Positive Like-for-Like route performance has supported investment

in new routes

• Solutions for last major legacy issue, E195s (Project Blackbird)

delivered

• Q3 performance to date is in line with management expectations

• Now focussed on profitable capacity growth

© Flybe 2015 16

Summary

We have delivered consistent top-line growth for three consecutive quarters

Flybe UK seat and passenger revenue growth, 2012 – 2015 by quarter

17 © Flybe 2015

Immediate

Actions

E195

Mitigations

Start of Republic

Q400 deliveries

Improved a/c

utilisation

18 © Flybe 2015

13.1% increase in Seat Capacity

10.2% increase in

Passenger Volumes

13.1% seat capacity growth has been accompanied by 10.2% passenger volume growth and sustained sector leadership

0.4ppts increase in UK Regional

Domestic Sector Share

Source: Flybe, CAA Monthly Stats Oct 13 – Sep 15

+ =

Despite capacity growth, we have improved yields with limited load factor and RPS dilution

19

Decreased but still high load factor

Increased yields….

© Flybe 2015

A small reduction in revenue per seat

+1.6%

-2 ppts

(0.3)%

• 7.0% CPS reduction including fuel (at constant

currency)

• Also, 5.8% CPS reduction excluding fuel:

- lower surplus aircraft cost with the mitigations

from flying 3 E195 aircraft in H1

- non-recurrence of one-time charge for historic

EU261 liabilities

- lower aircraft and ownership costs & lower

marketing spend

Reduction in Cost Per Seat (CPS) Operational Delivery in H1 maintained

Gains in Aircraft Utilisation Sustained

Brussels Airlines contract extended by 2 years as of

October 2015 with 2 Q400 aircraft

SAS operations with two ATRs started in Stockholm on

time and on budget

White Label progress

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%

15 Mins Arr OTP Flown as % of Scheduled

H1 FY15

H1 FY16

% of

Flights

+26 bps +8 bps

84.4% 84.2%

99.2% 99.1%

Daily

Block

Hours

per a/c

(12 mos

moving

average)

Cost improvement plus operational and white label progress

© Flybe 2015 20

Strong performance on unchanged LFL routes has supported investment in new routes

H1 2015/16 % of Total Seat Capacity Route Category with RPS Change vs. Prior Year

4.6%

(31)% vs.

network average

(7.8)%

34%

% RPS

change vly

21 © Flybe 2015

69%

19%

8%

4%

Unchanged Routes

New Routes

Routes with >20% cap.increase

Routes with >20% cap. decrease

% of H1 2015/16 Total Seat Capacity

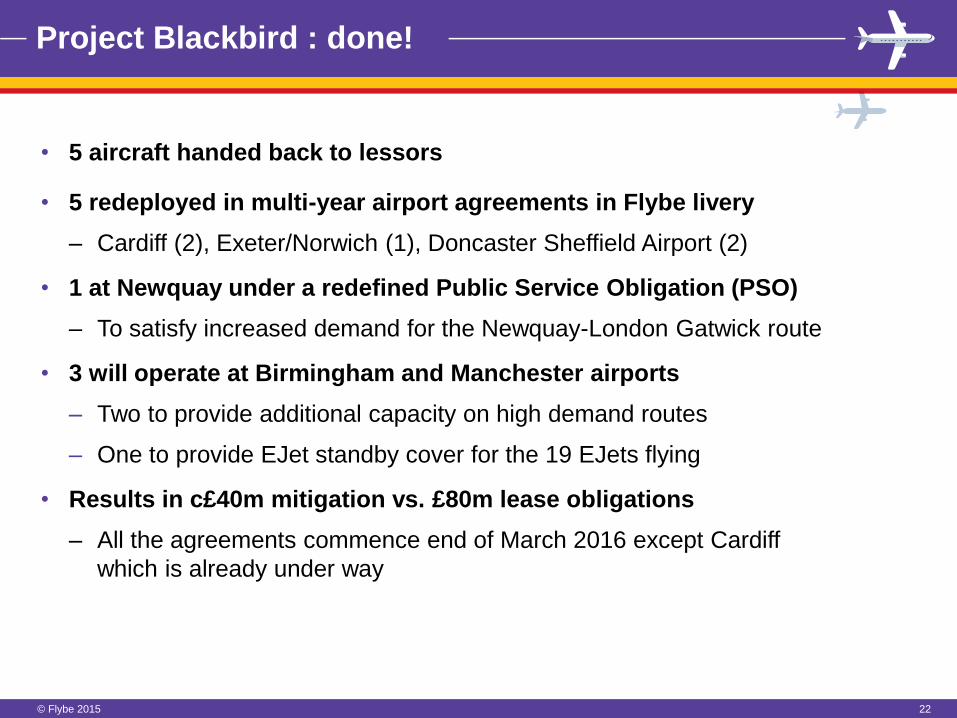

Project Blackbird : done!

© Flybe 2015 22

• 5 aircraft handed back to lessors

• 5 redeployed in multi-year airport agreements in Flybe livery

– Cardiff (2), Exeter/Norwich (1), Doncaster Sheffield Airport (2)

• 1 at Newquay under a redefined Public Service Obligation (PSO)

– To satisfy increased demand for the Newquay-London Gatwick route

• 3 will operate at Birmingham and Manchester airports

– Two to provide additional capacity on high demand routes

– One to provide EJet standby cover for the 19 EJets flying

• Results in c£40m mitigation vs. £80m lease obligations

– All the agreements commence end of March 2016 except Cardiff

which is already under way

Project Blackbird Portfolio: Complete

© Flybe 2015 23

G-FBEA: Returned G-FBEB: Returned G-FBEC: Returned G-FBED: Returned

G-FBEE: Returned

G-FBEN: Flying at EXE/NWI G-FBEM: Flying at NQY

G-FBEF: Flying at Cardiff G-FBEI: Flying at Cardiff

G-FBEG: Spare at BHX G-FBEH: Flying at BHX G-FBEJ: Flying at MAN

G-FBEK: Flying at DSA G-FBEL: Flying at DSA

Q3 performance to date is in line with management expectations

Q3 headlines as at 9th November (% change vs. prior year):

• Seat capacity up by c13%

• c51% of seats sold vs. c56% in the prior year

• Yield up c4%

• Passenger revenue per seat down by c6%

We enter the winter season with solid momentum

• We enter winter appropriately positioned

• Industry-wide seat capacity growth and benefit from lower fuel cost

• Flybe will retain focus on cost control and disciplined approach to capacity

investment - investing in winter primarily in additional frequencies on 18

established routes (only 4 new routes)

• Targeting to enhance regional connectivity for business customers with

higher frequency schedule

© Flybe 2015 24

We have now completed Chapter 3 of our transformation

March

2014

Jul-Sept

2014 2015-2017

Immediate Actions

• Cash

• Cost

• Configuration

• Commercialisation

• Confidence

• Cost base resizing

• Exit Finland JV

• Resolve fleet issues:

- Q400 mods, E175 order

- E195s (Project Blackbird)

Nov

2013

Nov

2014

• Core UK revenue growth

• New routes & bases

• Codeshares

• Partnerships

Mar

2015

Chapter 1

Restructuring

Chapter 2

Rebirth

Chapter 3

Growth platforms

&

Legacy solutions

New growth platforms Legacy issue solutions

© Flybe 2015 25

Company Confidential & Proprietary

• £22.5m restricted cash released

• £150m net capital raise

• Brand relaunch

• Purple-isation

© Flybe 2015 25

Our attention now is firmly shifting to Chapter 4

Flybe’s Journey

Chapter 1: Restructuring

Chapter 2: Rebirth (strengthen balance sheet, relaunch brand)

Chapter 3: Establish growth platforms, while resolving legacy issues

Chapter 4: Profitable growth

Time saving connectivity for regional customers

26

Focus on our compelling USP:

© Flybe 2015

We are building off solid foundations

27 © Flybe 2015 Company Confidential & Proprietary

• Number of aircraft: 70 (49 Q400, 11 E175, 9 E195, 1 ATR72-600)

• Number of routes: 149 Winter 2015, 62 departure points (34 UK, 28 EU)

• Number of bases: 10

• Codeshare partners: 8 (+17 interline agreements)

• Pax total: c8m

• Pax split: c50% business, c25% VFR, c25% leisure

• Bookings split: 80% website, 20% indirect channels

• Number of FTEs: 1,979

• Culture: Purple

Flybe as at end H1 2015/16

SUMMARY

Summary

• Strong core business performance

– Third consecutive quarter with double digit capacity, passenger volume and

revenue growth

– Continued unit cost reduction

– Return to profit

– Improved cash generative

• Project Blackbird complete

– Solutions for all surplus 14 E195 jets now delivered

– c£40m of mitigation vs. £80 outstanding lease obligations

• Outlook for winter is cautiously optimistic

– We enter winter appropriately positioned

– Industry-wide seat capacity growth and benefit from lower fuel cost

– Flybe disciplined with focused investment on enhancing regional connectivity

for business customers with higher frequency schedule

© Flybe 2015 29 © Flybe 2015 29 Company Confidential & Proprietary

Q&A

APPENDIX

Financial calendar

• FY16 Q3 RNS – 28 January 2016

• FY16 results – 9 June 2016

• AGM – 27 July 2016

© Flybe 2015 32 32

Group balance sheet

© Flybe 2015 33 33

£m Sep-15 Mar-15 YOY change

Aircraft 163.7 166.4 (2.7)

Other property, plant and equipment 23.7 22.7 1.0

Net funds 86.3 76.7 9.6

Derivative financial instruments (16.4) (7.2) (9.2)

Other working capital (95.0) (115.6) 20.6

Deferred tax 13.1 8.5 4.6

Other non-current assets and liabilities (2.5) (11.5) 9.0

Net assets and shareholders' funds 172.8 140.0 32.8

Group – Fleet under management

34 © Flybe 2015 34

Sep-15 Mar-15 Movements

Embraer 118-seat E195 regional jet 9 10 (1)

Embraer 88-seat E175 regional jet 11 11 -

Bombardier 78-seat Q400 turboprop 49 45 4

ATR72-600 turboprop 1 - 1

Group fleet under management 70 66 4

Held on operating lease 56 52 4

Owned and debt financed 14 14 -

Group fleet under management 70 66 4

Total seats in fleet 5,894 5,658

Average seats per aircraft 84.2 85.7

Average age of fleet (years) 7.3 7.0

Flybe Group - impact of fuel and hedging positions

© Flybe 2015 35

As we hedge most of our fuel and USD exposure, we do not fully benefit

from falling oil prices until the end of 2015/16

H1 2014/15 H1 2015/16 Change

Jet fuel, $ / metric tonne

Market rate $(954) $(551) $(402)

Effective price $(959) $(835) $(124)

Current hedge portfolio:

- H2 2015/16 – 86% hedged at $855 per tonne

- H1 2016/17 – 70% hedged at $668 per tonne

GBP:USD rate

Market rate $1.62 $1.51 $0.11

Effective price $1.57 $1.62 $(0.06)

Current hedge portfolio:

- H2 2015/16 – 76% hedged at $1.57

- H1 2016/17 – 65% hedged at $1.54

Actual cost of fuel, £ / metric tonne (612) (514) (98)