analisis triulanan peremangan moneter … santoso, shinta r.i. soekro, darmansyah, hilde d. sihaloho...

TRANSCRIPT

1ANALISIS TRIWULANAN: Perkembangan Moneter, Perbankan dan Sistem Pembayaran, Triwulan II - 2007

BULLETIN OF MONETARY ECONOMICS AND BANKING

Center for Central Banking Research and EducationBank Indonesia

PatronDewan Gubernur Bank Indonesia

Board of Editor

Prof. Dr. Anwar NasutionProf. Dr. Miranda S. Goeltom

Prof. Dr. InsukindroProf. Dr. Iwan Jaya Azis

Prof. Iftekhar HasanProf. Dr. Masaaki Komatsu

Dr. M. SyamsuddinDr. Perry Warjiyo

Dr. Iskandar Simorangkir Dr. Solikin M. JuhroDr. Haris Munandar

Dr. Andi M. Alfian ParewangiDr. M. Edhie Purnawan

Dr. Burhanuddin AbdullahDr. Andi M. Alfian Parewangi

Editorial Chairman

Dr. Perry Warjiyo

Managing EditorDr. Darsono

Dr. Siti AstiyahDr. Andi M. Alfian Parewangi

SecretariatIr. Triatmo Doriyanto, M.S

Nurhemi, S.E., M.ATri Subandoro, S.E

This bulletin is published by Bank Indonesia, Center for Central Banking Research and Education. Contents and results research in the writings in this bulletin entirely the responsibility of the authors and not an official view of Bank Indonesia.

We invite all parties to write in this bulletin paper delivered in the form files to Center for Central Banking Research and Education, Bank Indonesia, Tower Sjafruddin Prawiranegara Floor 21; Jl. M.H. Thamrin No. 2, Central Jakarta, email: [email protected]

The Bulletin is published quarterly in April, July, October and January, for who wish to obtain this publication can contact the Dissemination Unit - Dissemination Division Statistics and Management Intern, Department of Statistics, Bank Indonesia, Tower Sjafruddin Prawiranegara floor 2; Jl. M.H. Thamrin No. 2, Central Jakarta, tel. (021) 2981-8206. For request subscribe: tel. (021) 2981-6571, fax. (021) 3501912.

Quarterly Outlook on Monetary, Banking, and Payment System In Indonesia:

Quarter III, 2014

TM. Arief Machmud, Syachman Perdymer, Muslimin Anwar, Nurkholisoh Ibnu Aman,

Tri Kurnia Ayu K, Anggita Cinditya Mutiara K, Illinia Ayudhia Riyadi

The Determining Factors Of Currency Redenomination Success:

Experimental And Historical Aproach

Andika Pambudi, Bambang Juanda, D.S. Priyarsono

Foreign Exchange Expectations in Indonesia: Regime Switching Chartists &

Fundamentalists Approach

Ferry Syarifuddin, Noer Azam Achsani, Dedi Budiman Hakim, Toni Bakhtiar

Asset Securitization and the Real Sector Performance:

An Alternative Source of Financing for SME’s

Wijoyo Santoso, Shinta R.I. Soekro, Darmansyah, Hilde D. Sihaloho

Determinant Of Non Performing Loan: The Case Of Islamic Bank In Indonesia

Irman Firmansyah

BULLETIN of moNETary EcoNomIcsaNd BaNkINg

Volume 17, Number 2, October 2014

153

221

133

183

251

This page intentionally left blank

133Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

1 Authors are researcher on Monetary and Economic Policy Department (DKEM). TM_Arief Machmud ([email protected]); Syachman Perdymer ([email protected]); Muslimin AAnwar ([email protected]); Nurkholisoh Ibnu Aman ([email protected]); Tri Kurnia Ayu K ([email protected]); Anggita Cinditya Mutiara K ([email protected]); Illinia Ayudhia Riyadi ([email protected]).

Indonesia’s economy in the third quarter of 2014 indicate that macroeconomic stability and the

financial system maintained and supported by a process of economic adjustment towards more balanced.

This condition is reflected in a declining current account deficit, subdued inflation and well managed

domestic demand, despite growth in the domestic economy which is expected to slow down. Meanwhile,

the stability of the financial system remains solid, sustained by the resilience of the banking system and

the relatively subdued performance of the financial markets. The national payment system continues to

run smoothly in supporting the economy.

Keywords: macroeconomy, monetary, economic outlook.

JEL Classification: C53, E66, F01, F41

Abstract

QUARTERLY OUTLOOK ON MONETARY, BANKING, AND PAYMENT

SYSTEM IN INDONESIA:QUARTER III, 2014

TM. Arief Machmud, Syachman Perdymer, Muslimin Anwar, Nurkholisoh Ibnu Aman, Tri Kurnia Ayu K,

Anggita Cinditya Mutiara K, Illinia Ayudhia Riyadi1

134 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

I. GLOBAL DEVELOPMENT

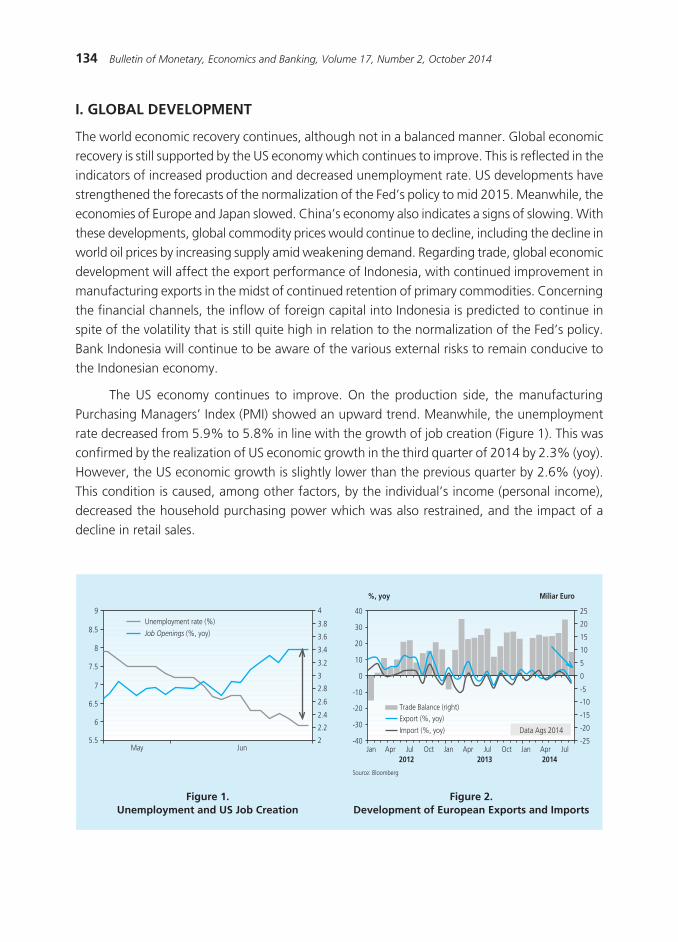

The world economic recovery continues, although not in a balanced manner. Global economic recovery is still supported by the US economy which continues to improve. This is reflected in the indicators of increased production and decreased unemployment rate. US developments have strengthened the forecasts of the normalization of the Fed’s policy to mid 2015. Meanwhile, the economies of Europe and Japan slowed. China’s economy also indicates a signs of slowing. With these developments, global commodity prices would continue to decline, including the decline in world oil prices by increasing supply amid weakening demand. Regarding trade, global economic development will affect the export performance of Indonesia, with continued improvement in manufacturing exports in the midst of continued retention of primary commodities. Concerning the financial channels, the inflow of foreign capital into Indonesia is predicted to continue in spite of the volatility that is still quite high in relation to the normalization of the Fed’s policy. Bank Indonesia will continue to be aware of the various external risks to remain conducive to the Indonesian economy.

The US economy continues to improve. On the production side, the manufacturing Purchasing Managers’ Index (PMI) showed an upward trend. Meanwhile, the unemployment rate decreased from 5.9% to 5.8% in line with the growth of job creation (Figure 1). This was confirmed by the realization of US economic growth in the third quarter of 2014 by 2.3% (yoy). However, the US economic growth is slightly lower than the previous quarter by 2.6% (yoy). This condition is caused, among other factors, by the individual’s income (personal income), decreased the household purchasing power which was also restrained, and the impact of a decline in retail sales.

Figure 1.Unemployment and US Job Creation

Figure 2. Development of European Exports and Imports

������������������������������������������

���

��

�

���

�

���

���

��

��

���

�

���

��

��

���

���� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ���

���� ���� ����

���

���

���

���

�

��

��

��

��

������ �����������

���

���

���

���

��

�

�

��

��

��

��

��������������

�����������

�������������������������� ����������� ����

135Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

The European economy is slowing as external pressure, weakened production, and potential deflation continues. External pressure is evident by declining export growth as the Chinese economy is slowing (Figure 2). In addition, deflationary pressures and the continuing geopolitical problems of Russia still suppresses the production. This is indicated by developments in the manufacturing PMI which is in a downward trend.

The Japanese economy also experienced a slowdown driven by a weakening of production. This is indicated by the continued contraction of the production index, while at the end of the third quarter, the Japanese PMI was lower than the previous quarter. This condition is driven by the depreciation of the yen which has led to a weakening of output due to high import prices amidst limited export growth. On the other hand, demand has not improved, as indicated by department store sales that are still negative. Meanwhile, a Reuter’s survey revealed that there is deteriorating sentiment against large companies, both in manufacturing and non-manufacturing sectors. The negative sentiments are in line with the increase in the consumption tax, the increase in input prices due to the depreciation of the exchange rate, and a weakening global economy, especially China and Europe.

China’s economy is still indicating slow growth. On the demand side, the slowdown came mainly from a decline in consumption and investment growth (Figure 3). Meanwhile, in terms of production, the decline in growth mainly came from the real estate sector (tertiary industry). With these developments, the Central Bank of China (CBC) responded through a relaxation of the application rules for home loans by lowering the percentage of second home mortgages with a down payment of 30% to 60%of the house value, which came into effect the beginning of October 2014.

The Indian economy expanded and grew more than previous forecasts. The increase was driven by production activities, as indicated by the Indian PMI at a level of expansion, while the growth index showed stable production. In addition, the infrastructure index was also in an upward trend. On the domestic front, the economy indicated increasing domestic car sales and imports continue to grow. Improvements of the Indian economy are in line with the positive sentiment after the election of a new government which for example encourages the implementation of structural reforms, among others measures, in the fields of energy, infrastructure development and increase direct investment.

International trade activity decreased with the development of the global economic slowdown by major countries of the world. This is indicated by the volume of world trade which is lower than previous forecasts as well as global commodity prices that are still declining. The low growth in the world trade volume is driven by geopolitical issues and the impact of the extreme cold weather in the US in the first half that continued into the third quarter. Also, global commodity prices are still declining. The coal price decline is driven by an abundant supply and weak demand, especially from China. The weakening of the Chinese economy also decreased the price of nickel, tin, aluminum and rubber. Meanwhile, oil prices continue to decline, in line

136 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

with the increased supply amid weak global demand. The weakening of oil prices is due to several factors, particularly fundamental factors of competition between oil producing countries and geopolitics. The fundamental factors are related to the increasing positions of the world’s oil over supply. Meanwhile, there is competition between oil producing countries encouraged by the attitude of Saudi Arabia which has no intention to reduce production amid slowing demand in order to maintain market share. Factors associated with the easing of geopolitical tensions in the Middle East and North Africa have led to a return to operation for several oil refineries in Iraq and Libya.

The global financial markets experienced a correction due to strong forecasts of implementation for the Fed’s normalization policy mid-2015. The pressure on the global financial markets was also derived from a release of the IMF related to the decline in the global economic growth which encouraged negative sentiment. Meanwhile, a majority of the global currencies weakened against the US dollar, especially Asian emerging market (EM) currencies, including the Indonesian Rupiah, which was in line with rising investor concern over global geopolitical turmoil. With these developments, the Asian stock markets continued to move up although the volume of non-resident net inflows into Asian stock markets continued to decline (Figure 4).

Figure 3.China’s Economic Growth

Figure 4.Global Stock Market Performance

��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ������ ��� ��� ��� ��� ��� ��� ��� ��� ������� ���� ���� ���� ���� ����

��

�

�

��

��

����������

����� ��������������

����� ������������

��� ��� ��� ��� ��� ��� ��� ��� ��� ������� ���� ���� ���� ����

�����

��

��

���

���

���

���

���

���

���

�������

�����

���

���

���

���

��

��

����� ������ ��

� ���

����������

II. THE DYNAMICS OF Indonesia’S MACROECONOMY

2.1. Economic Growth

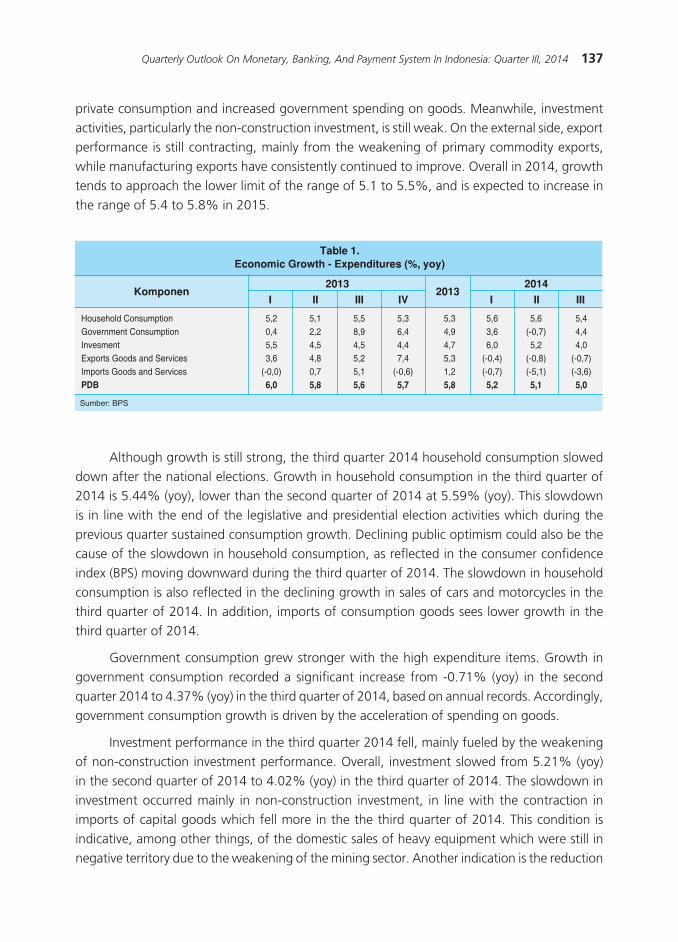

Along with the weak global demand, domestic economic growth tends to be moderated. Economic growth in the third quarter of 2014 is 5.01% (yoy), lower than the economic growth in the second quarter 2014 at 5.12% (yoy) (Table 1). Increased consumption is sustained by strong

137Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

private consumption and increased government spending on goods. Meanwhile, investment activities, particularly the non-construction investment, is still weak. On the external side, export performance is still contracting, mainly from the weakening of primary commodity exports, while manufacturing exports have consistently continued to improve. Overall in 2014, growth tends to approach the lower limit of the range of 5.1 to 5.5%, and is expected to increase in the range of 5.4 to 5.8% in 2015.

Although growth is still strong, the third quarter 2014 household consumption slowed down after the national elections. Growth in household consumption in the third quarter of 2014 is 5.44% (yoy), lower than the second quarter of 2014 at 5.59% (yoy). This slowdown is in line with the end of the legislative and presidential election activities which during the previous quarter sustained consumption growth. Declining public optimism could also be the cause of the slowdown in household consumption, as reflected in the consumer confidence index (BPS) moving downward during the third quarter of 2014. The slowdown in household consumption is also reflected in the declining growth in sales of cars and motorcycles in the third quarter of 2014. In addition, imports of consumption goods sees lower growth in the third quarter of 2014.

Government consumption grew stronger with the high expenditure items. Growth in government consumption recorded a significant increase from -0.71% (yoy) in the second quarter 2014 to 4.37% (yoy) in the third quarter of 2014, based on annual records. Accordingly, government consumption growth is driven by the acceleration of spending on goods.

Investment performance in the third quarter 2014 fell, mainly fueled by the weakening of non-construction investment performance. Overall, investment slowed from 5.21% (yoy) in the second quarter of 2014 to 4.02% (yoy) in the third quarter of 2014. The slowdown in investment occurred mainly in non-construction investment, in line with the contraction in imports of capital goods which fell more in the the third quarter of 2014. This condition is indicative, among other things, of the domestic sales of heavy equipment which were still in negative territory due to the weakening of the mining sector. Another indication is the reduction

Table 1.Economic Growth - Expenditures (%, yoy)

Komponen2013

I II III IV I II III

20142013

Household Consumption 5,2 5,1 5,5 5,3 5,3 5,6 5,6 5,4Government Consumption 0,4 2,2 8,9 6,4 4,9 3,6 (-0,7) 4,4Invesment 5,5 4,5 4,5 4,4 4,7 6,0 5,2 4,0Exports Goods and Services 3,6 4,8 5,2 7,4 5,3 (-0,4) (-0,8) (-0,7)Imports Goods and Services (-0,0) 0,7 5,1 (-0,6) 1,2 (-0,7) (-5,1) (-3,6)PDB 6,0 5,8 5,6 5,7 5,8 5,2 5,1 5,0

Sumber: BPS

138 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

in the production capacity utilization rates in the industry that shows a lack of incentives for businesses to invest. As the non-construction investment slowed down, similarly construction investment also slowed. In accordance with the historical trend, this condition is caused by the behavior of “wait-and-see” by investors during the election. Indications of a slowdown in construction investment is also reflected in slowing sales of cement and building materials imports in the third quarter 2014.

On the external side, export performance is still contracting. Exports in the third quarter of 2014 record a growth of -0.70% (yoy), slightly better than growth in the previous quarter at -0.76% (yoy). Export performance is still contracted, particularly in the export of primary commodities, due to weak global demand (Figure 5). Though still contracting, exports recorded improvement. This was driven by manufacturing exports which are still positive and the beginning realization of natural resources (mining) exports, in particular mineral concentrate exports (Figure 6).

The response of the limited performance of exports and non-construction investment is a third quarter 2014 import contraction. Imports again experience a smaller contraction from -5.05% (yoy) in the second quarter of 2014 to -3.63% (yoy) in the third quarter of 2014. On closer examination, the contraction occurred in the group of capital goods imports in line with the weakening of non-construction investments. Meanwhile, imports of consumer goods still contracted due to reduced imports of passenger cars, durable goods, and nondurable goods. In contrast, imports of raw materials grew positively, among others, in the form of foodstuffs (raw and processed) for industry, raw materials for industry, and fuel for industrial machinery.

Figure 5.World Trade Volume (Imports)

Figure 6.Real non-oil export growth

����

��������������������������� ���

� � �� ������ ���� ����

������

��

�

�

�

�

�

�

������������ �����

��������� ������� ���������

� � �� �� � � �� �� � � �� �� �� �� ���� ������ ����

�����������

���

���

���

���

�

��

��

��

��

��

���� ����

������

����

�����������

�����

�� �� ��

139Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

By sector, the slowing economic growth in the third quarter of 2014 is derived from lower growth in the manufacturing sector and nontradables sectors. The manufacturing sector growth slowed with weakening domestic demand and limited export performance. The slowdown is mainly in the sub-sectors of food, beverages and tobacco, chemical subsector, and the cement subsector. The building sector also contracted due to the behavior of wait-and-see businessmen to invest during the election. Trade, hotels and restaurants slowed due to the retention of international trade activity and the reduced effects of the election of previous quarter. Although growth is still high, the transport and communications sector grew less than the previous quarter at the close of the election campaign. Meanwhile, the slowdown in the financial sector, leasing, and services occurred with slowing credit growth. On the other hand, agriculture and mining growth increased compared to the previous quarter. An increase in the agricultural sector comes from the increasing growth of the food crops subsector mainly corn and soybeans. The mining sector contracted in the first quarter and the second in 2014 due to delays in mineral exports, however it bounced back with positive growth with the implementation of the Mining Law.

Regional and national economic slowdown came mainly from the weakening of economic growth in Sumatra. In addition to Sumatra, the national economic slowdown is driven by the economic slowdown that occurred in Jakarta and a contraction in NTB. The economic slowdown in Sumatra, is driven by a decline in commodity exports. Jakarta’s economy also slowed due to a slowdown in the construction sector. Meanwhile, NTB contracted significantly due to a decline in mining sector performance. On the other hand, economic growth in the region increased

Picture 1.Map of Regional Economic Growth Third Quarter 2014

gPDRB > 7% 5% < gPDRB < 6% 4% < gPDRB < 5% gPDRB Negative6% < gPDRB < 7% gPDRB < 4%

ACEH2.7

SUMUT5.3

RIAU1.7

KEP. BABEL4.6

DKI JAKARTA6 JATENG

5.4

SULTENG6.6

KALTIM3.2

KALBAR4.5

SULUT7

MALUT5.9

PAPBAR6.4

PAPUA4.1

BALI6.5 NTT

KEP. RIAU6.9

LAMPUNG5.6

BENGKULU5.1

BANTEN5

SULSEL6.2

SULBAR10

JABAR5.6 JATIM

5.9NTB

KALTENG5.5

KALSEL4.8

GORONTALO7.8

MALUKU7.3

SULTRA7.7

SUMSEL4.3

JAMBI6.6

DIY4.0

SUMBAR5.0

SUMATERA

I II III I II IIIIV2013 2014

4.54.95.4

876543

%, yoy

JAKARTA

I II III I II IIIIV2013 2014

4.04.14.0

876543

%, yoy

JAWA (Excl. Jkt)

I II III I II IIIIV2013 2014

5.65.65.7

876543

%, yoy

KTI

I II III I II IIIIV2013 2014

5.14.94.7

876543

%, yoy

NASIONAL

I II III I II IIIIV2013 2014

5.05.15.2

876543

%, yoy

140 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

in line with the East Region of Indonesia’s (KTI) export of mineral commodities. Meanwhile, the economy of the Java (besides Jakarta) remained relatively high and with stable growth in line with the continued improvement in manufacturing exports as a result of the US economic recovery (Picture 1).

In line with the slowdown of economic growth, the unemployment rate in August 2014 increased. In August 2014, the unemployment rate stood at 5.94%, higher than in February 2014 which amounted to 5.70%. This increase was driven by a decrease in the employment rate. This decreased uptake corresponds with the slowdown in the manufacturing sector, transport and communications, finance and services sector, among others. Meanwhile, the absorption of labor in the agricultural sector tends to be stable, even uptake in the building sector and trade actually increased.

2.2. Indonesia’s Balance of Payments

Indonesia’s balance of payments (BOP) showed better performance in line with a process towards a more balanced and sustainable economic adjustment. Overall, the balance of payments in the third quarter of 2014 has a surplus of 6.5 billion US dollars, an increase of 4.3 billion dollars in the previous quarter (Figure 7). An improved balance of payments surplus is mainly driven by a decreased current account deficit compared to the previous quarter. An increase in the balance of payments surplus in turn pushed up the foreign exchange reserve from 107.7 billion US dollars at the end of the second quarter of 2014 to 111.2 billion US dollars by the end of the third quarter of 2014. The amount of the reserve is sufficient to finance payments for imports and government foreign debt for 6.3 months, and is adequate by international standards (Figure 8).

Figure 7.Indonesia’s Balance of Payments

Figure 8.Development of Reserves

�����������

�� �� �� �� �� �� �� �� �� �� �� �� ���� ���� ����������

������

������

�����

����

����

�����

�����

���� ���� ����� ����

���������� �����������������������������������������������

��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ������ ��� ���

�����������

���� ���� ���� ����

��

��

���

���

� �

���

�

�

�

�

������������������������������������ ��������������� ���������

141Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

The decreased current account deficit is underpinned by stabilization policies pursued by Bank Indonesia and the Government. The current account deficit in the third quarter 2014 amounted to 6.8 billion US dollars (3.07% of GDP), lower than the deficit of 8.7 billion dollars (4.06% of GDP) in the second quarter of 2014 and lower than the deficit for the same period in 2013 at 8.6 billion US dollars (3.89% of GDP). Although the oil trade deficit remains large, improvement in the current account is mainly supported by the return of the merchandise trade balance surplus with an increase in the non-oil trade surplus. The increased non-oil surplus compared to the previous quarter was mainly driven by a decline in non-oil imports, particularly imports of raw materials, in line with a moderation in domestic demand. In annual terms, non-oil imports in the third quarter 2014 still contracted 2.7%. Exports of primary products increased, partly due to increased mineral permits and the recovery of raw mineral exports. Non-oil surpluses also contributed to the improvement even though the overall, non-oil exports still recorded a decline. Although the decline is on a quarterly basis, the annual non-oil exports in the third quarter of 2014 returned a positive growth of 3.1% after the last two years of decrease. The non-oil export growth was supported by higher export prices and improved export demand, particularly for vegetable oils and manufactured products. Along with the continuing US recovery, some export products such as textile manufacturing, metal goods, processed foods, and vehicles and parts have increased. On the oil side, the oil and gas trade balance deficit in the third quarter 2014 is influenced by the high imports of oil and gas, and oil exports declined with the decline in world oil prices. In addition, the reduced pressure of the current account deficit is influenced by seasonal patterns and the services account deficit of lower primary income.

Meanwhile, investor confidence is still positive on the prospects of the Indonesian economy as encouraged by strong foreign capital inflows. In the third quarter of 2014, the capital and financial account surplus reached 13.7 billion US dollars, mainly supported by inflows of foreign capital in the form of direct investment and the withdrawal of foreign corporate loans. On the other hand, portfolio investment inflows are lower than the previous quarter. The decline is influenced by sentiment, both from external and domestic sources. In addition, the placement of domestic private savings abroad also increased. Overall, the surplus in the capital and financial accounts recorded third quarter 2014 is still quite large and can fully finance the current account deficit, although it is lower than the second quarter 2014 surplus of 14.3 billion US dollars.

2.3. Rupiah Exchange Rate

The weakened rupiah is mainly influenced by global sentiment. In the third quarter of 2014, the rupiah weakened on average 1.2% (qtq) to the level of Rp11, 770 per US dollar. In point-to-point, the rupiah also weakened by 2.71% to a level of Rp12,185 per US dollar (Figure 9). Pressure on the rupiah is influenced by both external and internal factors. External pressures were triggered by concerns about the normalization of the Fed policy, geopolitical dynamics, and the

142 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

2.4. Inflation

Inflation maintained its downward trend that is supported by the prospect of achieving the 2014 inflation target of 4.5 ± 1%. Inflation in the third quarter of 2014 is 4.53% (yoy), down from 6.70% (yoy) in the previous quarter. Inflation is maintained and supported by the control of the core inflation and foods volatility. Unbridled core inflation was supported by a decline in global commodity prices, moderate demand and subdued inflation expectations. Meanwhile, volatile food inflation is also relatively low, due to a sufficient food supply. By contrast, inflation in administered prices increased, mainly driven by increases in the TTL RT and LPG of 12 kg.

The downward trend in inflation in the third quarter of 2014, is supported by, among others things, a relatively low volatile food inflation rate. The volatile food inflation in the third quarter 2014 is 4.21% (yoy), lower than the second quarter of 2014 which was 6.74% (yoy) (Figure 11). The drop in inflation is mainly driven by high enough food supplies and relatively smooth distribution. The commodity price corrections of onion varieties eased inflation, as a result of a harvest supply glut that took place at a variety of production centers. Meanwhile, the price of rice in this quarter is relatively restrained, in line with the forecasts of a sufficient

global economic slowdown. The external pressures also affected the currencies of countries in the region, including Indonesia (Figure 10). The weakening rupiah was influenced by internal factors to Indonesia, such as the behavior of investors who awaited the formation of the new cabinet and the government work program. Depreciation pressure in the third quarter 2014 is reflected on some external indicators such as the VIX Index and CDS that increased. However, the volatility of the rupiah is still controlled, and lower than the Turkish lira, Brazilian real and South African rand. Looking ahead, Bank Indonesia will continue to maintain the stability of the exchange rate in accordance with fiscal fundamentals.

Figure 9.Rupiah Exchange Rate

Figure 10.Regional Exchange Rates

� � ������ � � ���� �� � ��� �� �� � ��� ���� � � ���� ���� � ������ � � �� ���� ����� �� ��� � ������

�������

��� ��� ��� �� ��� �� � � ���

������

������

������

������

������

������

������ ������

������

������������ ������

������

������

������������

������

�������������������������� ����������� �������������

������ ������ ����� ����� ����� ����� ���� �����

���

���

���

���

� �

���

��

��

���

���

������������������

�������������� ������

����

����

����

����

�����

�����

�����

�����

�����

�����

�����

�����

�����

�����

�����

�����

�����

�����

�����

����

143Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

supply of rice at the end of the harvest season. In addition, a weakened El Nino in the fourth quarter also contributed in controlling volatile food inflation in the third quarter of this year.

Decline in inflation in the third quarter 2014 is also supported by control of the core inflation in line with the decrease of external and domestic pressures. Core inflation in the third quarter 2014 is recorded at 4.04% (yoy), down compared to the previous quarter at 4.81% (yoy). Reduced external pressure is primarily driven by a decrease in global prices, amid pressure of a weakening rupiah at the end of the third quarter of 2014. Domestically, despite an increased seasonal demand due to the Muslim Holiday of Eid and the new school year, the pressure of demand is fundamentally slowed with declining economic activity. In addition, inflation expectations in the third quarter is still restrained.

There are indications of rising inflationary expectations related to oil price hikes. This is reflected in higher inflation expectations by retailers by the end of 2014 in line with the increasing concern of rising fuel prices (Figure 12). In addition, an indication of rising inflation expectations is also reflected in the financial sector.

Meanwhile, inflationary pressures from administered prices increased mainly driven by higher TTL RT. The impact of rising TTL Household group (R-2 and R-1) Phase I (July 1, 2014) and Phase II (1 September 2014) as well as the adjustment of rates for group R-3 (> 6600VA) encouraged high inflation as contributed by the electricity rates reaching 0.25%. In addition, the increase in seasonal demand ahead of the Muslim Holiday Eid pushes up rates of transportation groups such as inter-city transport and air transport.

Spatially, the inflation pressure in the third quarter in the various regions is relatively restrained. It is powered by low volatile food inflation with adequate food supplies amid rising

Figure 11Annual Inflation

Figure 12Retailer Price expectations

����

� � � � ���� � � � ���� � � � ���� � � � ���� � � � ���� � � � ���� � � �

������

���� ���� ���� ���� ���� ���� ����

���

��

�

�

��

��

����

����

����

��������� ��� ����������������������

����������

�����

� �� � ���� �� � ���� �� � ���� �� � ��� � �� � ��� � �� � ���� �� � ��� � �� � ��� � �� � ���� �� � �

���� ���� ���� ���� ���� ���� ���� ���� ��������

���

���

���

���

���

��� ��

��

��

�

�

��� �

�������� ������������������ �������������������������������������� �� �������������������������������������� ��

144 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

demand for the religious festivities. However, some areas such as West Sumatra, Bengkulu, Bangka Belitung, Banten, and West Kalimantan noted high inflation, in the range of 6% (yoy), as a result of a rise in TTL and LPG 12 kg (Figure 13).

III. THE DYNAMICS OF MONETARY, BANKING, AND PAYMENT SYSTEM

3.1. Monetary

The interest rates and money supply development is still in accordance with the direction of the monetary policy adopted by Bank Indonesia. During the third quarter of 2014, interbank rates were relatively stable while bank interest rates still maintained an upward trend. An increase in interest rates occurred amid slowing economic growth in the third quarter of 2014, and its effect on the dynamics of liquidity in the economy is relatively stable even though liquidity in the interbank market tended to increase.

The Interbank Money Market in the third quarter 2014 is marked by a relatively stable the interbank O/N rate, while the average total volume of the Interbank Money Market is in relative decline. This indicates that the liquidity conditions in the overnight Interbank Money Market is relatively stable. The weighted average interbank rate in the third quarter 2014 amounted to 5.86% which is relatively the same compared to the previous quarter. Relatively stable interest rate movements of the Interbank Money Market triggered an overnight spread effect to stabilize the overnight deposit facility at 11bps, while having a similar effect on the BI rate which also stabilized at 164bps, indicating an absence of the liquidity crunch on the interbank money market. While the average total volume of Interbank Money Market showed a relative decrease from Rp12.1 trillion to Rp11.8 trillion, the average volume of the overnight

Picture 2.Distribution maps of Consumer Price Index (CPI) Inflation (%, yoy)

Inf > 6.2% 4.1% < Inf < 5.0% Inf < 4.1%5.0% < Inf < 6.2%

ACEH5.4

SUMUT4.4

RIAU5.5

KEP. BABEL5.4

DKI JAKARTA5.2 JATENG

5

SULTENG7.3

KALTIM4.6

KALBAR5.4

SULUT6.4

MALUT5.9

PAPBAR5.1

PAPUA4.7

BALI5.1 NTT

4.6

KEP. RIAU4.5

LAMPUNG4.5

BENGKULU5.8

BANTEN6.7

SULSEL4.7

SULBAR4.4

JABAR4 JATIM

4.6NTB4.7

KALTENG5.2

KALSEL5.6

GORONTALO3.7

MALUKU6

SULTRA3.3

SUMSEL3.4

JAMBI4.1

DIY4.4

SUMBAR6.3

National: 4.83% (yoy)

145Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

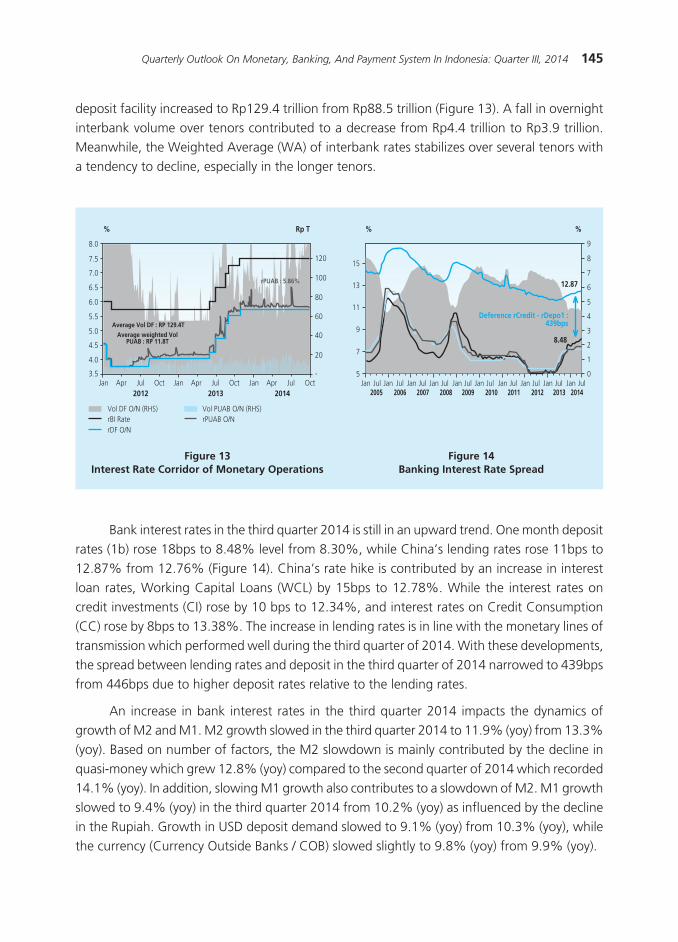

Bank interest rates in the third quarter 2014 is still in an upward trend. One month deposit rates (1b) rose 18bps to 8.48% level from 8.30%, while China’s lending rates rose 11bps to 12.87% from 12.76% (Figure 14). China’s rate hike is contributed by an increase in interest loan rates, Working Capital Loans (WCL) by 15bps to 12.78%. While the interest rates on credit investments (CI) rose by 10 bps to 12.34%, and interest rates on Credit Consumption (CC) rose by 8bps to 13.38%. The increase in lending rates is in line with the monetary lines of transmission which performed well during the third quarter of 2014. With these developments, the spread between lending rates and deposit in the third quarter of 2014 narrowed to 439bps from 446bps due to higher deposit rates relative to the lending rates.

An increase in bank interest rates in the third quarter 2014 impacts the dynamics of growth of M2 and M1. M2 growth slowed in the third quarter 2014 to 11.9% (yoy) from 13.3% (yoy). Based on number of factors, the M2 slowdown is mainly contributed by the decline in quasi-money which grew 12.8% (yoy) compared to the second quarter of 2014 which recorded 14.1% (yoy). In addition, slowing M1 growth also contributes to a slowdown of M2. M1 growth slowed to 9.4% (yoy) in the third quarter 2014 from 10.2% (yoy) as influenced by the decline in the Rupiah. Growth in USD deposit demand slowed to 9.1% (yoy) from 10.3% (yoy), while the currency (Currency Outside Banks / COB) slowed slightly to 9.8% (yoy) from 9.9% (yoy).

����������������������� ��

��� �������� ��� ������ ��� ��� ������ ��� ��� ������

���

���

���

���

���

���

���

���

���

��

�������������������������������� ��

��������� ���

�����

�

��

��

��

�

��

��

������������������������������

��� ������������� ������

��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ����

�

�

��

��

��

�

�

�

�

�

�

�

�

�

�

�

�

�����

����������������������� ������ �

���

���� ���� ���� ���� ���� ���� ���� ���� ��� ���

deposit facility increased to Rp129.4 trillion from Rp88.5 trillion (Figure 13). A fall in overnight interbank volume over tenors contributed to a decrease from Rp4.4 trillion to Rp3.9 trillion. Meanwhile, the Weighted Average (WA) of interbank rates stabilizes over several tenors with a tendency to decline, especially in the longer tenors.

Figure 13Interest Rate Corridor of Monetary Operations

Figure 14Banking Interest Rate Spread

146 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

Based on the above factors, the decline of Net Foreign Assets (NFA) is a major factor for the decline in M2 amidst an increase in Net Domestic Assets (NDA). NFA growth slowed to 14.6% (yoy) from 29.2% (yoy), while the NDA increased from 8.1% (yoy) to 10.5% (yoy). The NFA decrease is influenced by a decrease in foreign exchange reserves of the central bank and increased (net) liabilities of commercial banks to non-residents (NR); whereas the increase in NDA is due to increased bills to the central government.

3.2. Banking Industry

The stability of the financial system remains solid sustained by the resilience of the banking system and the relatively subdued performance of the financial markets. The resilience of the banking industry remains strong although credit risk and market liquidity is fairly maintained, as well as strong capital backing. A relatively stable financial market performance is supported by relatively good capital market performance during the third quarter 2014 and an increase in yield of government securities in all tenors on a quarterly basis.

The pace of credit growth slowed contributed by Working Capital Loans (WCL). As of the third quarter of 2014, credit growth slowed to 13.2% (yoy) from 17.2% (yoy); yet grew 8.2% (ytd). Slowing the rate of credit is still contributed by Credit for Working Capital (CWC) that has a share of 48.0%, (whereas the share of CI and CC is 24.5% and 27.5%, respectively). Based on its use; the CWC type of credit growth and CI fell to 13.3% (yoy) and 16.4% (yoy) from 17.3% (yoy) and 22.5% (yoy), respectively compared to the second quarter of 2014. Similarly, credit growth of CC types also fell to 10.1% (yoy) from 12.7% (yoy) (Figure 15). By sector, the trade sector still has the largest share of total loans which reached 22%, and is followed by the processing industry with a share of 18%. Slowing credit expansion is contributed by

Figure 15.Loan Growth by Expenditure

Figure 16.Growth in Deposits

��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ���

������������������

���� �������� ���� ����

�����

��

�

��

�

�

��

��

���

��

�������������

�������

��

��

�

�

�

�

���� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ��� ���

������

���� ���� ���� ���� ����

�

�

��

��

��

��

�� �� ���������������������������

��������������������������������� ����

��

�

�

��

��

��

147Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

manufacturing and trade. The manufacturing sector growth slowed to 16.1% (yoy) from 24.9% (yoy), while the trade sector credit growth also slowed to 13.9% (yoy) from 18.3% (yoy).

Deposit growth slowed slightly, triggered by a decrease in the Current Account Savings Account (CASA), which consists of current and savings accounts. In the third quarter of 2014, the demand for deposits and savings growth slowed to 7.0% (yoy) and 7.1% (yoy) from 10.2% (yoy) and 9.5% (yoy), respectively. Actual deposit growth increased to 21.4% (yoy) from 18.5% (yoy). Thus, the slowdown in deposit growth is contributed by the decline in the CASA, which fell to 53.1% in the third quarter 2014 from 54.2% in the previous quarter (Figure 17). Although lower than the second quarter of 2014, growth in deposits in September 2014 increased compared to the previous month and stood at 13.32% (yoy). This is in line with the government’s financial operations which were expansionary. Further, the bank liquidity in the third quarter of 2014 is maintained.

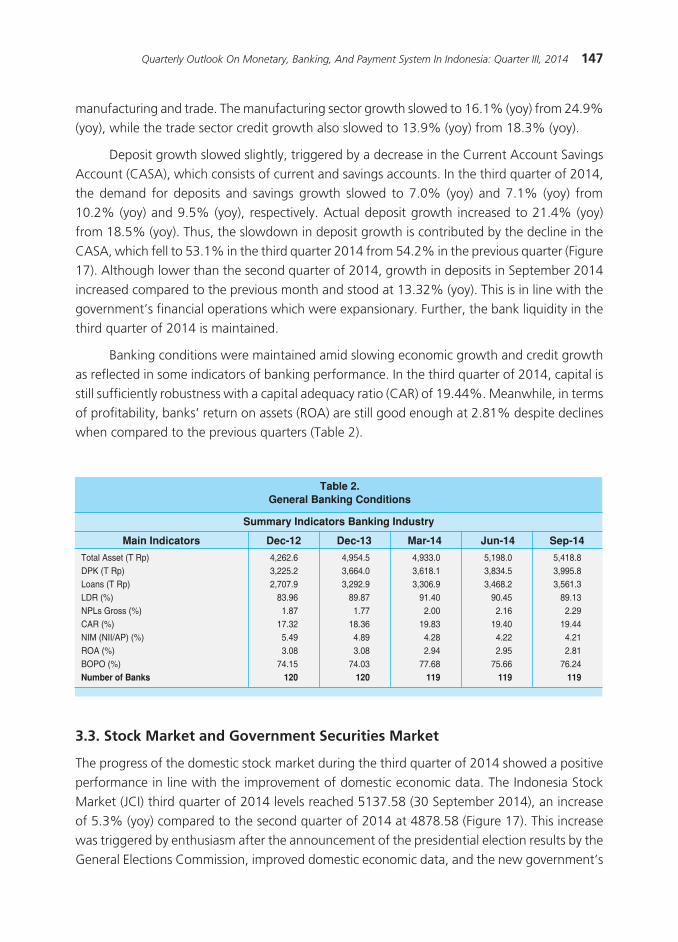

Banking conditions were maintained amid slowing economic growth and credit growth as reflected in some indicators of banking performance. In the third quarter of 2014, capital is still sufficiently robustness with a capital adequacy ratio (CAR) of 19.44%. Meanwhile, in terms of profitability, banks’ return on assets (ROA) are still good enough at 2.81% despite declines when compared to the previous quarters (Table 2).

3.3. Stock Market and Government Securities Market

The progress of the domestic stock market during the third quarter of 2014 showed a positive performance in line with the improvement of domestic economic data. The Indonesia Stock Market (JCI) third quarter of 2014 levels reached 5137.58 (30 September 2014), an increase of 5.3% (yoy) compared to the second quarter of 2014 at 4878.58 (Figure 17). This increase was triggered by enthusiasm after the announcement of the presidential election results by the General Elections Commission, improved domestic economic data, and the new government’s

Table 2.General Banking Conditions

Summary Indicators Banking Industry

Main Indicators Dec-12 Dec-13 Mar-14 Jun-14 Sep-14

Total Asset (T Rp) 4,262.6 4,954.5 4,933.0 5,198.0 5,418.8DPK (T Rp) 3,225.2 3,664.0 3,618.1 3,834.5 3,995.8Loans (T Rp) 2,707.9 3,292.9 3,306.9 3,468.2 3,561.3LDR (%) 83.96 89.87 91.40 90.45 89.13NPLs Gross (%) 1.87 1.77 2.00 2.16 2.29CAR (%) 17.32 18.36 19.83 19.40 19.44NIM (NII/AP) (%) 5.49 4.89 4.28 4.22 4.21ROA (%) 3.08 3.08 2.94 2.95 2.81BOPO (%) 74.15 74.03 77.68 75.66 76.24Number of Banks 120 120 119 119 119

148 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

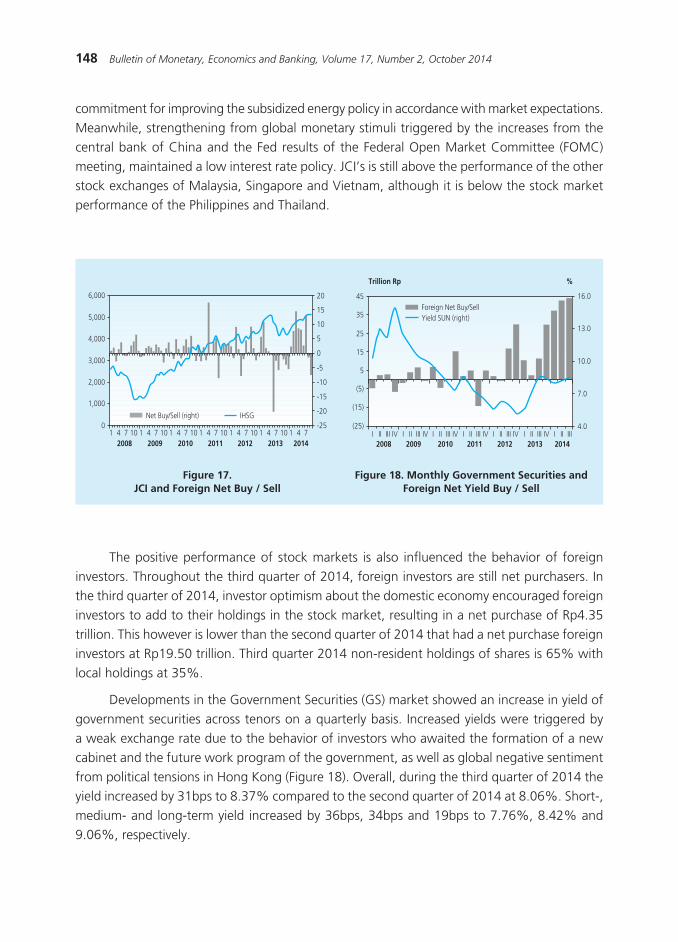

The positive performance of stock markets is also influenced the behavior of foreign investors. Throughout the third quarter of 2014, foreign investors are still net purchasers. In the third quarter of 2014, investor optimism about the domestic economy encouraged foreign investors to add to their holdings in the stock market, resulting in a net purchase of Rp4.35 trillion. This however is lower than the second quarter of 2014 that had a net purchase foreign investors at Rp19.50 trillion. Third quarter 2014 non-resident holdings of shares is 65% with local holdings at 35%.

Developments in the Government Securities (GS) market showed an increase in yield of government securities across tenors on a quarterly basis. Increased yields were triggered by a weak exchange rate due to the behavior of investors who awaited the formation of a new cabinet and the future work program of the government, as well as global negative sentiment from political tensions in Hong Kong (Figure 18). Overall, during the third quarter of 2014 the yield increased by 31bps to 8.37% compared to the second quarter of 2014 at 8.06%. Short-, medium- and long-term yield increased by 36bps, 34bps and 19bps to 7.76%, 8.42% and 9.06%, respectively.

� � � �� � � � �� � � � �� � � � �� � � � �� � � � �� � � ����� ���� ���� ���� ���� ���� ����

���

�

�

��

��

��

��

���

���

���

�

�����

�����

�����

�����

�����

�����

�������� ������������

� �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ��� �� � �� ������� ���� �������� ���� ���� ����

����

����

���

�

��

��

��

��

���

���

����

����

��������� ������������

����������� �

������������ ��

commitment for improving the subsidized energy policy in accordance with market expectations. Meanwhile, strengthening from global monetary stimuli triggered by the increases from the central bank of China and the Fed results of the Federal Open Market Committee (FOMC) meeting, maintained a low interest rate policy. JCI’s is still above the performance of the other stock exchanges of Malaysia, Singapore and Vietnam, although it is below the stock market performance of the Philippines and Thailand.

Figure 17.JCI and Foreign Net Buy / Sell

Figure 18. Monthly Government Securities and Foreign Net Yield Buy / Sell

149Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

Weakening GS prices followed an increase in GS yield utilized by non-residents who continued to add to their holdings in the government securities market. During the third quarter of 2014, the net purchase of foreign investors was Rp43.79 trillion, higher than the second quarter of 2014 at Rp42.68 trillion. During the same period, ownership of government securities by banks, foreign insurance and pension funds also increased, so that the proportion of government securities holdings by BI decreased. Foreign investors were buyers of government securities throughout the tenor, so that the amount of foreign ownership in government securities in the third quarter of 2014 increased to 36.17% compared to 34.51% of the previous quarter.

3.4. Payment System Developments

Payment system developments in the cash group is generally in line with the development of the domestic economy, especially the household consumption sector. The daily average currency in circulation in the third quarter 2014 amounted to Rp491.3 trillion and grew 12.6% (yoy), down from the previous growth quarter of 13.9% (yoy), and likewise down for the same quarter of the previous year at 11.1% (yoy). The currency in circulation is in line with the slowing growth in household consumption and GDP of quarterly reports.

In the middle of the currency in circulation growth trend, Bank Indonesia continued to improve the feasibility of the money supply. During the third quarter of 2014, some 1.3 billion pieces / chips of Money-Not-Fit for-Circulation (MNFC) worth Rp29.7 trillion was destroyed and replaced with money fit for circulation. Total destruction of MNFC was higher than the second quarter of 2014 totaling 1 billion pieces / chips or Rp22.6 trillion worth of currency. The increased MNFC destruction was due to the increased amount of money in conditions not fit for circulation that were deposited by banks to Bank Indonesia.

The fixed payment transactions system ran smoothly during the third quarter of 2014. In the third quarter 2014 the non-cash payment system transactions increased both in terms of value and volume of transactions. The increased value of transactions stood at Rp8, 742.8 trillion (QtQ rise by 26.97%), and an increase in the volume of transactions stood at 36.12 million transactions (QtQ rise by 3.16%) when compared to the previous quarter (Table 3). In the reporting period, the increase in the value of the transactions occurred in all groups, especially monetary transactions. On the other hand, the increase in the volume of transactions caused by increasing public transactions through non-cash instruments was in line with the celebrations of the Muslim Eid Festivities and the Presidential general election of 2014.

150 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

In harmony with the increase in the value and volume of the non-cash payment system transactions in the third quarter of 2014, payment transactions settled through the Bank Indonesia Real Time Gross Settlement (BI-RTGS) also increased both in terms of value and volume. The BI-RTGS is the fund settlement system. The Bank Indonesia-Scripless Securities Settlement System (BI-SSSS), as well as the Funds Transfer and Scheduled Clearing by Bank Indonesia (SKNBI) reached 100% in the third quarter of 2014. The value of transactions of settled payments through the BI-RTGS increased by Rp5, 716.17 trillion (QtQ rose by 23.67%) to reach Rp Rp29, 866.56 trillion compared to the previous quarter was at Rp24, 150.39 trillion. The volume of payment transactions settled through the BI-RTGS increased by 48.60 thousand (QtQ rose by 1.09%) to reach 4.52 million transactions, compared with the previous quarter at 4.47 million transactions.

IV. ECONOMIC OUTLOOK

Bank Indonesia expects the economy will still experience an adjustment while macroeconomic stability is maintained. Economic growth in 2014 is estimated to be at the lower limit of 5.1 to 5.5% projection. It is affected by the growth of the world GDP that is not as strong as earlier forecasted and budget savings for the State Budget Year 2014. The projected growth in the world economy is expected to be weak resulting from export performance that is not as strong as previously expected, while the government’s austerity budget pushes a slowdown in government consumption. By 2015, economic growth is expected to bounce back and be in the range of 5.4 to 5.8%. Improvement is in line with global economic forecasts of conditions that would be better than a year earlier. This would contribute to export growth which is also forecasted to increase.

In line with the moderation of economic growth, inflation in 2014 is estimated to be lower than inflation in 2013 and will be heading towards the 2015 inflation target of 4 + 1%. In quarter IV-2014, inflation is expected to increase again in line with the assumption

Table 3.Non-Cash Payment System Developments

Non-Cash PaymentSystem Transaction

2013

Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014

BI-RTGS 18,778.31 21,410.40 26,369.50 24,403.80 23,817.80 24,150.40 29,866.56 BI-SSSS 4,939.05 5,299.70 8,259.90 8,233.40 7,173.60 6,396.90 9,366.77Clearance 547.87 605.70 680.80 708.00 667.80 710.70 716.36APMK 901.67 989.60 1,039.40 1,073.90 1,082.20 1,158.52 1,208.91Credit Card 51.09 55.23 57.08 59.62 59.78 63.65 64.41ATM Card & ATM/Debit 850.58 934.38 982.36 1,014.28 1,022.42 1,094.87 1,144.50Electronic Money 0.59 0.68 0.90 0.74 0.73 0.83 0.86Total 25,167.48 28,306.07 36,350.55 34,419.79 33,860.26 32,417.39 41,159.47

151Quarterly Outlook On Monetary, Banking, And Payment System In Indonesia: Quarter III, 2014

that the exchange rate would further depreciate and air freight rates would increase. With such developments, inflation in 2014 is estimated upwards. Meanwhile, inflation for 2015 is expected to rise related to the adjustment of some administered prices, such as the upper limit air freight rates and the price of LPG (March and August 2015), as well as the projection of the high pressures on volatile foods and further exchange rate depreciation. However, inflation in 2015 is estimated to be in the target range of 4.0 ± 1%

Bank Indonesia will keep a close watch some of the risks shadowing the economic adjustment process going forward. Globally, among other risks associated with the normalization of the Fed’s policy plans, is the economic vulnerability of emerging markets and economic weakness in a number of countries. On the domestic front, the risk that requires attention is the potential for inflationary pressures due to adjustments in administered prices such as subsidized fuel prices and electricity tariffs. In addition to inflation, domestic risks also arise from the potential reversal of capital flows (capital reversal) with the normalization of the Fed’s policy and high foreign debt position.

152 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

This page intentionally left blank

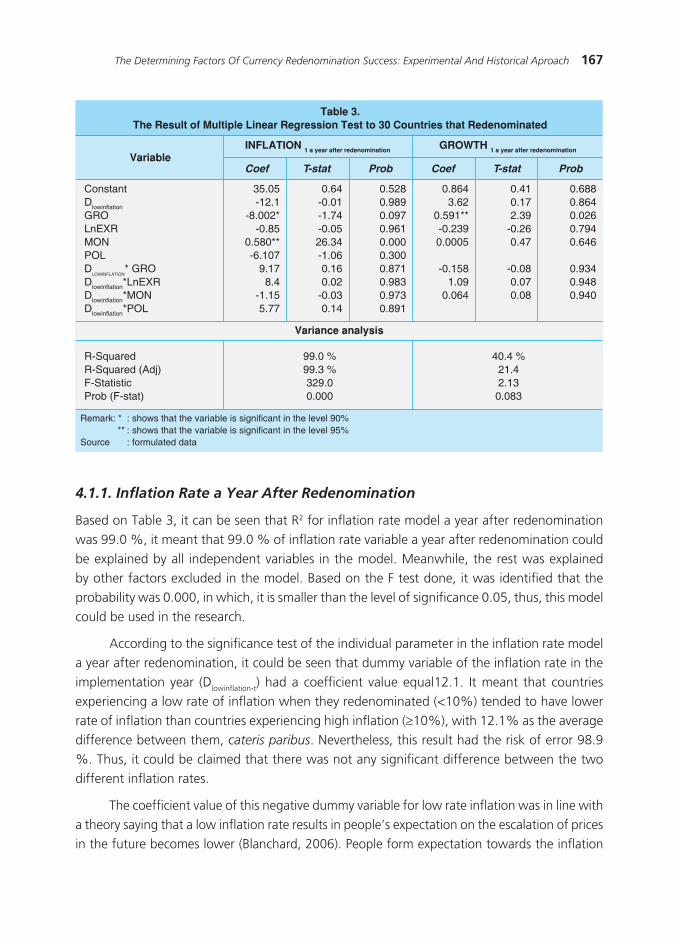

153The Determining Factors Of Currency Redenomination Success: Experimental And Historical Aproach

THE DETERMINING FACTORS OF CURRENCY REDENOMINATION SUCCESS:

EXPERIMENTAL AND HISTORICAL APROACH

Andika Pambudi1

Bambang Juanda2

D.S. Priyarsono2

Redenomination is a simplification of nominal value of currency by reducing digit (zero number)

without reducing the real value of the currency. The main objective of this research was to examine

whether the economic conditions at the time of redenomination may affect the success of currency

redenomination. The methods used were regression analysis on historical data of 30 countries which

are involved in redenominating their currencies, economic experiments with t-test, and survey of people’

perspective.Based on regression analysis, inflation will decrease and economic growth will rise higher

after redenomination, if previously a country have experienced high economic growth as well. Based on

experimental research, when inflation was high, redenomination could increase the selling price. Otherwise,

when inflation was low, redenomination could decrease the selling price. Changes in selling price after

redenomination was not affected significantly by differences in economic growth conditions. In different

economic conditions, redenomination policy did not significantly affect the changes number of transactions

and total value of transactions in the market. From the survey results, public did not believe government

can control inflation after redenomination. Redenomination also will not affect consumption pattern.

Abstract

Keywords: Redenomination, Inflation, Economic Growth, Experiment

JEL Classification: C91, E31, E42, E58,

1 Peneliti di Center for Public Policy Transformation (www.transformasi.org).2 Departemen Ilmu Ekonomi, Fakultas Ekonomi dan Manajemen IPB – Penulis Korespondensi ([email protected]).

154 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

I. INTRODUCTION

Redenomination is a simplification of nominal value of a currency by reducing digits (zero number) without reducing the real value of the currency. Bank Indonesia (BI) has planned the redenomination of Rupiah by reducing three zero digits of the currency value, goods prices as well as wages. Too big nominal value of a currency reflects that in the past, a country had encountered high inflations or it had experienced a pretty bad economic fundamental condition (Kesumajaya, 2011). Moreover, if a country constantly encounters a high inflation every year, the value of the currency towards the goods will be lower (Amir, 2011). 55 countries have redenominated, some of them result in success and some result in failure. One of the indicators of the redenomination application success is the inflation rate after the redenomination being applied. It will be considered a failure if a high inflation or a hyperinflation happens after the implementation.

Nowadays, Indonesia, that plans to perform redenomination, has encountered some turmoil and instabilities in its both currency value and inflation rate. Before its independence, in 1944 the value of Rupiah was almost as valuable as USD; Rp 1,88 per USD. Then on March 7th 1946 the value crash of Rupiah happened for the first time as much as 30 percent, so it was Rp 2,65 per USD. In 1950 the government performed sanering of Rp 5 and above so the value became only half of the previous value. The government then performed the second sanering on 25th August 1959 by cutting the value of Rupiah.

The high rate of inflation results in the weakening of currency value. This can be seen that in 1960s, Indonesia encountered an extremely high hyperinflation that hit its peak in 1966 as much as 1136 percent. Subsequently, in 1971 the value of Rupiah was depreciated and it reached the value of Rp 415 per USD (World Bank, 2012). After 68 years of independence, the value of Rupiah now is about Rp 9.700 per USD. That more depreciated value becomes one of the government’s reasons to have determination to boost Rupiah’s prestige. This moment is considered right because Indonesia’s current inflation rate is relatively stable in the last few years. Even, it can be declared that the inflation is creeping (creeping inflation) in type or occurs in around one digit every year. This constant inflation reflects price stability for some goods that form consumers’ price level.

The government aims at increasing Rupiah’s credibility is a positive effect of redenomination, yet its implementation also has negative effects. One of them is the people’s misperception that they think it is a sanering. Sanering is a policy of omitting zeros in a currency, yet this cutting is not done to the goods price so the people’s purchasing power decreases. This people’s misconception of redenomination may cause a state of panic resulting in economic situation turmoil. In addition, redenomination will increase companies and banking operational expenses because they have to replace their information and technology system. They certainly need some time to implement new accounting technology to adjust to nominal simplification. Bank Indonesia will also spend high expense to issue new redenominated money as well as public

155The Determining Factors Of Currency Redenomination Success: Experimental And Historical Aproach

dissemination. Redenomination will also cause other social effects in terms of public distrust to Rupiah (Kesumajaya, 2011).

According to Wibowo (2013), an effect that will come into view because of this currency nominal change is the emergence of psychological bias so called money illusion. Most people will assume that goods price is cheaper because of the omission of zeros from the previous currency. For instance, there is an escalation of goods price as much as of Rp 7.000, consumers will find this very hard. However, after redenomination the escalation is only Rp 7 and they will find it trouble-free whereas they have exactly the same value. Consumers pay less attention to the re- scaling process of the old Rupiah nominal value to the new one. Money Illusion will affect the consumers more when they review the real value of goods they have bought because of the simultaneous nominal change. Redenomination drives into bigger consumption behavior. New prices are perceived cheaper because of money illusion and consumers’ willingness to pay increases. By seeing this people’s behavior, producers will escalate the price up to consumers’ tolerated limit.

Pros and cons of redenomination policy scheme reflect a public speculation about unpredictability of consequence that might happen if redenomination of Rupiah is implemented at the moment. Research on probable effects needs to be scientifically investigated through experimental method. According to Juanda (2010) the data of experiment results will be more easily interpreted in the effort of concluding causal relationship compared to data of survey result or secondary data. This investigation is aimed at noticing contributing factors to the success of the currency redenomination. The factors are economic condition when redenomination policy is implemented. The condition covers among others inflation rate. The success of redenomination can be seen through the change of inflation rate and the economic growth after redenomination being implemented.

The scope of this study is divided into three sections. First, it gives identification of contributing factors to the success of redenomination policy in a country through a study to secondary data that come from some historical information of countries that have redenominated. Second, it analyzes the impacts of Rupiah redenomination policy on the behaviors of economic subjects (pelaku ekonomi). The behaviors effects of the subjects will be further investigated to see the economic performance (kinerja perekonomian). Third, it records people’s perspective as producers and consumers on the currency redenomination policy. In the effort of investigating the second section of this study, the data used will be gathered through experimental method. The economic performance being investigated, like inflation rate and economic growth will be viewed based on the change of the number of transaction and the average prices after redenomination generated from the responses of experiment simulation. The term redenomination in this paper refers to the policy of three zeros reduction in the value of Rupiah, price unit, wage unit (unit harga, unit upah) and everything valued by the currency.

156 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

II. THEORETCAL REVIEW

2.1. The Linkage of Redenomination and Economic Performance

There are relatively not many studies investigating the role of redenomination in economic performance. Yet, there are some opinions stating that a country’s decision to redenominate is strictly influenced by the prior economic condition. Additionally, the change of economic indicators in a country can also be influenced by the implementation of currency redenomination policy.

Suhendra and Handayani (2012) investigated the connection between redenomination policy and the inflation rate, exchange rate, economic growth and export value (nilai ekspor). The data on the economic indicators of 27 countries redenominated showed that inflation and economic growth were two variables significantly influenced by currency redenomination. Meanwhile, the high inflation rate was the most dominant driving factor for a country to decide to redenominate its money value. This finding is in line with what Mosley (2005) says that the current and the past inflation are the most important predictors whether or not to redenominate.

Iona (2005) investigated long-term advantages of redenomination, reasons of redenomination implementation timing, their influence to the price. The result of the study revealed that the long- term impacts of redenomination were: 1) public trust establishment to domestic currency; 2) the increase of saving in domestic currency; and 3) the money saved out of national monetary system will flow to market. Redenomination will be successfully implemented if it meets the two requirements as follow: 1) low inflation rate with decreasing tendency; and 2) the success of economic reformation and reconstruction program, like the high growth of real GDP (Gross Domestic Product). If those two requirements are met, redenomination will be useful. Iona (2005) also says that indicators that have to be monitored to assess the impacts of redenomination are Consumer Price Index, purchasing power, exchange rate, 1- month deposit average ( rata-rata deposito 1-bulan), Consumer Trust Index, Business Trust Index. (Indeks Kepercayaan Konsumen, dan Indeks Kepercayaan Bisnis).

2.2. The Relation between Redenomination and Economic Subjects’ Behaviors

Some impacts that might occur in the implementation of redenomination are the emergence of psychological bias called money illusion (Wibowo, 2013). This illusion can come into view because of the nominal change of goods price resulted from redenomination. Most people will perceive cheaper goods price due to the value omission of zero from the previous currency. Hobijn et al (2006) point out that money illusion has occurred in some European country changing their currency into Euro. Euro whose fewer nominals (nominal yang lebih sedikit) compared to the prior currency is perceived cheaper by the people. Hobijn et al (2006)

157The Determining Factors Of Currency Redenomination Success: Experimental And Historical Aproach

thinks that the escalation of the price after redenomination can be explained by the general model of menu cost price, by inputting companies’ decision when they adopt new currency.

Furthermore, consumers will re-evaluate their financial strategy management to adapt to new currency especially when the new and the old currency are used in concert, waiting for the old to disappear. Marques and Dehaene (2004) state that there are two major processes that can take place when a country adapt a new currency : rescaling (changing all prices in old currency into the new money values all at once) or re-learning ( remembering new price of the consumers’ good one at a time). The first process is predicted to experience effortless adjustment to the new currency; meanwhile the latter will encounter more complex and longer adjustment.

In the meantime, Money/Euro Illusion shows that the price perception in new denomination is smaller and lower currency than when it is stated in the previous currency if it has higher nominal (Gamble et al. 2002). This demonstrates that individuals adjust themselves to the new currency with its smaller nominal value, at least, they encounter difficulty in understanding the real value of goods and services. Money illusion’s effect can also happen to cheap goods or when the escalation of the price is only few cents. If the availability of cents (coins) is not fulfilled by the government, consumers will tend to allow the escalation of the price without demanding change from the seller. This phenomenon is called trivialization.

Trivialization case can be observed in Ghana whose inflation rate increases as much as 5% per year after redenomination. One of the factors causing the redenomination failure is that 70% of money circulating in Ghana is out of banking system. Ghana’s cash transactions are more dominant than its banking transaction. To make things worse, the government hasn’t been able to change the new currency into the old currency after two years of redenomination. Mehdi and Reza (2012) also state that the reduction of the currency nominal value will invite psychological and social impacts. When a currency has a low nominal value, then the people will think that the currency has a strong value.

Lianto and Suryaputra (2012) did a research to identify the impacts of redenomination implementation in Indonesia based on Indonesian’s perspective. The data gathered through surveying 100 people who have knowledge on redenomination and the data were then analyzed by employing Structural Equation Modelling. It could be seen that the most influential impact of redenomination was that it could increase the credibility of Indonesia in front of other countries. The other finding was that the Indonesian considered redenomination to be beneficial for them. If it was implemented successfully, Rupiah would be stronger and it would boost the people’s trust to their currency.

158 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

2.3. The Experiment in the Study of Economic Policy

Economic experiment can be used to study an economic policy as well as to review an economic theory. One of the illustrations is what Juanda et al (2011) did in studying and comparing systemic impacts resulted from the policy of Century Bank rescue effort and its closure policy issued by the government. The result of the study showed that Century Bank closure resulted in a relatively very low impact. A sufficiently huge systemic impact would emerge if the closure in that critical time was done to an immense bank. In a normal situation (in the absence of turmoil), the closure of a small problematic bank like Century will not cause systemic impacts. Bank pressure and failure potential were extremely low since the economic stability was maintained. Thus, there was no decrease in the trust of the customers to banking.

Another research investigating a policy through experimental method is a study of tax compliance rate in the self- assessment tax collection system implemented in Indonesia (Juanda, 2010). The study looked into the influence of assessment chance impacts, fine, and educational level to the compliance of taxpayers in reporting Letter of Notification (Surat Pemberitahuan (SPT)), by controlling other factors, they were arranged to be the same (ceteris paribus). Factors that influenced taxpayers’ compliance rate were difficult to do through survey design because of environmental influences or objects of the study. Study result confirmed that the higher the tax assessment change and the bigger the fine would positively influence the taxpayers’ compliance in doing tax liabilities. Additionally, Juanda (2010) observed the tax compliance rate of “experiment subject” undergraduate students was higher compared to graduate students whose relatively higher knowledge. Moreover, the higher the taxpayers’ income, the lower their compliance was.

III. METHODOLOGY

3.1. Kinds and Data sources

The data used in this study were both primary and secondary data. Primary data were gathered through experiment. The primary data gathered were the responses of the subjects (simulation subjects) as the economic subjects in the experiment could be observed from the decisions they took. Additionally, the primary data were also collected through a survey to 168 respondents consisted of 86 lecturers of IPB, 27 IPB students, and 55 of the general public to see their perspectives on redenomination policy impacts on the national economy. This survey was intended to gain judgements, opinions and perspectives about the redenomination policy that would be implemented by the government.

159The Determining Factors Of Currency Redenomination Success: Experimental And Historical Aproach

Table 1.Countries that Have Redenominated Their Currency

No

1 Finland 1963 2 2 Iceland 1981 2 3 Israel 1985 3 4 Bolivia 1987 6 5 Uganda 1987 2 6 Nicaragua 1988 3 7 Peru 1991 6 8 Argentina 1992 4 9 The Sudan 1992 1 10 Latvia 1993 2 11 Letonia 1993 200 Rublu = 1 Lats 12 Macedonia 1993 2 13 Mexico 1993 3 14 Moldova 1993 3 15 Uruguay 1993 3 16 Brazil 1994 2,750 Cruzeiros Reais = 1 Real 17 Croatia 1994 3 18 Georgia 1995 6 19 Poland 1995 4 20 Ukraine 1996 5 21 Russia 1998 3 22 Angola 1999 6 23 Bulgaria 1999 3 24 Belarus 2000 3 25 Romania 2005 4 26 Turkey 2005 6 27 Azerbaijan 2006 1 28 Mozambique 2006 3 29 Ghana 2007 4 30 Venezuela 2008 3

Source: Iona (2005)

Countries Redenomination time Omitted Zeroes

In the interim, the secondary data employed in this study were the historical data of 30 countries that had redenominated their currency since 1963 until 2008 and they are presented in Table 1. The historical data consisted of some macro-economy indicators in the year, in which redenomination was implemented in a certain country and a year after that. The variables used were inflation rate, economic growth, exchange rate, the growth of money in circulation and the government form. The secondary data were collected from the publications of World Bank, International Monetary Fund, and Center for Systemic Peace. Information about the resources of the employed variables in the analytical model is presented as follow.

160 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

3.2. Multiple Regression Model

The estimation method that was used to study influential factors to the implementation of redenomination employed multiple regressions. Exogenous variables or independent variables in this study were inflation rate, economic growth, exchange rate, the growth of money in circulation and the government form. Meanwhile, observed variables (endogenous) or dependent variable was the success or failure of the redenomination implementation that was measured through inflation rate and economic growth a year after redenomination was implemented in each country.

In this study, regression process was done by regressing independent variables in form of economic performance of a country that was influential to the success or the failure of redenomination (dependent variables). Dependent variable (Y) or influenced variable was economic performance indicators that reflected the success of redenomination implementation. Thus, this variable used economic performance accomplishment a year after the policy. In the meantime, independent variables (X) or the influential variables was a country economic performance when redenomination was implemented for the first time. This model had never been applied before in its relation to currency redenomination. And, the linier regression model in this study was as follow.

(1)

Inflation rate (%) World Bank, 2012, World Development Indicators 2012. (http://data.worldbank.org/indicator/FP.CPI.TOTL.ZG)

Economic growth (%) World Bank, 2012, World Development Indicators 2012. (http://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG)

Exchange rate to USD ($ US) World Bank, 2012, World Development Indicators 2012. (http://data.worldbank.org/indicator/PA.NUS.FCRF)

The growth of money in World Bank, 2012, World Development Indicators 2012. circulation (%) (http://data.worldbank.org/indicator/FM.LBL.BMNY.ZG)

The government form index The Center for Systemic Peace, 2012, Polity IV Project (http://www.systemicpeace.org/polity/polity4.htm)

Indicator Source

161The Determining Factors Of Currency Redenomination Success: Experimental And Historical Aproach

where:

β0 = Intercept

β1,... β9 = Parameter

Yafter redenoi = Success indicator of currency redenomination for country number-i:

a) Low inflation a year after redenomination (percent)

b) Economic growth a year after redenomination (percent)

Dlowinflation- i = Dummy condition low inflation rate in the year of redenomination implantation for country number-i, with the value of:

1 = low inflation (< 10%) and 0 = high inflation (≥10%)

GROi = Economic growth in the year of redenomination implementation for country number-i (percent)

LnEXRi = Natural Logarithm of currency exchange rate to dollar in the year in which redenomination is implemented for country number -i ($ US/ Domestic Currency)

MONi = The growth of money in circulation in the year of redenomination implementation for country number -i (percent)

POLi = The government form index in the year of redenomination implementation for country number -i (percent), with the value of

min = -10 (very autocratic); max = 10 (very democratic)

Some assumptions underlying the model are: (i) dependent variable is a non- stochastic (fixed) variable, it means that it has been specified or not a random variable; (ii) there is no perfect linier relationship between independent variables or there is no collinear problem; (iii) a residual component εi has expectation value equal zero or E(εi) = 0; (iv) constant variance for all observations or var(εi) = σ2; (v) there is no relation or correlation between residue εi or cov(εi, εj) = 0 for i ≠ j; and, (vi) residual component is normally distributed.

Hypothesis Testing of Regression Parameter

Subsequently, to partially see the influence of the independent variables, t-test was used. This test will be useful if variance analysis test shows, at least, one independent variable influence the dependent one. This t-test employment is advantageous to show which independent variable is the most influential to the dependent variable. The partial hypothesis could be formulated as follow.

162 Bulletin of Monetary, Economics and Banking, Volume 17, Number 2, October 2014

H0 : βi= 0

H1 : βi ≠ 0; (i=1,2,3,4)

While the statistical test could be formulated as follow.

(2)

Null hypothesis is accepted if the absolute value of t is bigger than the t-table or if the p-value is smaller than level level of significance (α) as big as 10 percent, then null hypothesis is rejected or in other words H1 is accepted. It means that independent variable i is influential to dependent variable if other factors are constant (cateris paribus). Value-p is a probability (risk) of error in drawing conclusion of H1.

3.3. Experiment Simulation Design

This experiment was a simulation of economic activity to see the influence or response of currency redenomination towards producers and consumers behavioral change. The response to economic behavior change could be seen from the percentage of selling price change after redenomination as a proxy of inflation rate, the percentage of number of transaction change after redenomination as well as the percentage of transaction value change after redenomination as a proxy of the economic growth rate.

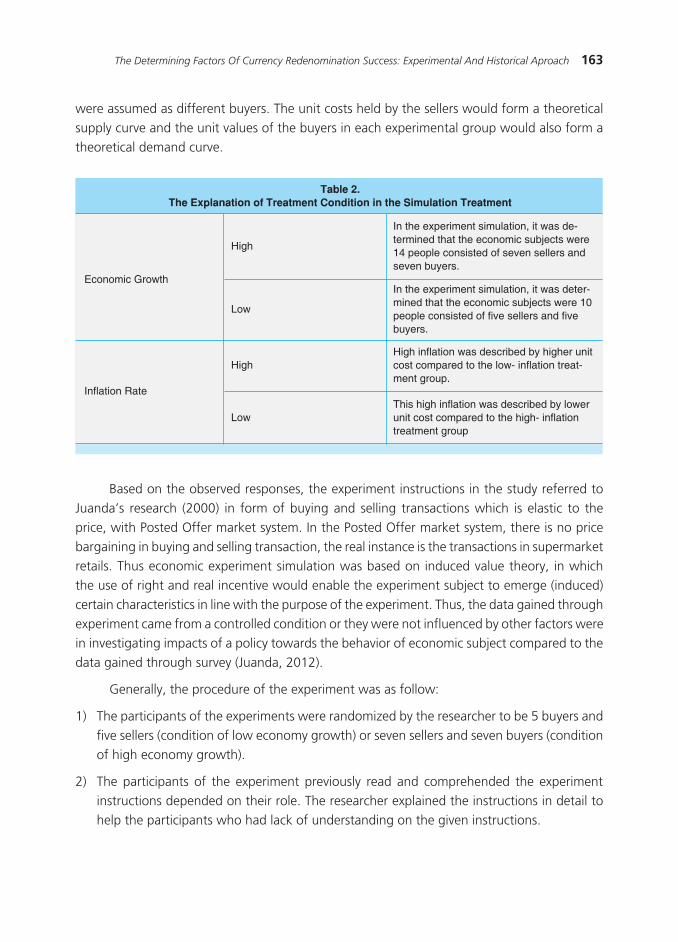

The economic experiment in this study involved 48 undergraduate students of IPB Economy and Management Faculty as experimental subjects. They were divided into four treatment combinations, so each combination consisted of 10 or 14 students. In the group of high growth economy treatment, 5 people acted as sellers and 5 others as buyers. In the other group of high-growth economy treatment, both buyers and sellers were seven people. The choice of respondents acting as buyers or sellers was done through drawing system. Factors that would be observed to see their influences were:

1. Economic growth, consisted of two levels: 1) high- economy growth (seven sellers and seven buyers); and 2) low-growth economy (five sellers and five buyers).

2. Inflation rate consisted of two levels: 1) high inflation (the unit cost of seller is big); and 2) low inflation (the unit cost of seller was small).