an irreversible trend towards financial innovation

TRANSCRIPT

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Opportunities UT & Jupiter Financial Innovation SICAV

September 2020

AN IRREVERSIBLE TREND TOWARDS FINANCIAL INNOVATION

Guy de Blonay

Fund Manager

Global Financials & Financial Innovation

Antoine Hucher

Analyst

Global Financials & Financial Innovation

Jenna Zegleman

Product Specialist

Global Financials & Financial Innovation

1

For professional and institutional investors only. Not for retail investors.

Investment approach

● Experienced manager with a demonstrated track record of generating returns in a variety of market conditions

● Seeks to identify sub-sector fundamental themes through investments in companies with prices that do not reflect longer-term trends

● Opportunistic, effective and dynamic capital allocation across geographies, sub-sectors, growth, yield and special situations categories

Global Financials & Financial Innovation strategy

The strategy

The views expressed are those of the presenter at the time of preparation and may change in the future.

High conviction global investment for capital growth over the long term.

Liquidity is a key criteria

for investment.

2512

_2359

2

For professional and institutional investors only. Not for retail investors.

Risk metrics

Volatility**

Performance since inception in GBP

Performance and risk metricsJupiter Financial Opportunities – UT

Sharpe ratio**

1,943.4

8.3 12.9 18.3

-5.2

27.99.6

193.8

0.4

34.9

13.9

-9.9

19.3

-18.6-50

0

50

100

150

200

Sin

ce

ince

ptio

n*

201

5

201

6

201

7

201

8

201

9

YTD

(%)Jupiter Financial Opportunities I Acc MSCI ACWI/Financials

1900

1950

Past performance is no guide to the future.Fund performance data is calculated on a NAV to NAV or bid to NAV basis dependent on the period of reporting, all performance is net of fees with income reinvested.

Source: Morningstar, in GBP, to 31.08.20. Comparator benchmark: MSCI ACWI/Financials. *Based on daily returns since fund launch on 02.06.97.

**The volatility and Sharpe ratios are based on annualised figures for monthly returns. Risk free rate of 3 months Libor GBP.

-0.13

0.22

0.62

0.81

Since inception

3 years

3 years

Sharpe ratio**

16.90

24.74

17.14

20.15

Since inception

2512

_2359

3

For professional and institutional investors only. Not for retail investors.

Underlying principles and areas of focus

The strategy’s ESG approach

Typical areas of focus

1. Corporate

governance

● Management succession & remuneration

● Composition and expertise of the board

● Transparency of investor communication

2. Business ethics

● Regulatory risks

● Issues around anti-trust and tax avoidance

● Appetite for risks, check & control procedures

3. Data privacy &

security

● Policies in place to handle customer data and manage

risks related to cyber-attacks

● Track record on data breaches

4. Human Capital● Policies in place to attract, retain and reward talent

● Track record on employee retention and job preservation

5. Climate

● Energy efficiency of operations and commitment to

cutting carbon emissions

● Exposure to carbon-intensive sectors

Alignment of all stakeholders’ interests

Sustainability

Employees

Shareholders Customers

Business

model

Financial

modelTrade

practices

2512

_2359

4

For professional and institutional investors only. Not for retail investors.

Disruptive technology & innovation

The opportunity

Steve Jobs

Innovation is the ability to see change as an opportunity –

not a threat.

Doug Merritt, CEO of Splunk Inc.

Covid-19 has transformed the world into one that requires

rapidly accelerated digital transformation to keep

organisations moving – we are seeing some resilient

customers complete three-to-five year projects in just months.

2512

_2359

5

For professional and institutional investors only. Not for retail investors.

The digitalisation of financial services

The opportunity

The views expressed are those of the presenter at the time of preparation and may change in the future.

Ralph Hamers, CEO ING, upcoming CEO UBS

We want to be a tech company with a banking license.

● In the context of an unstoppable trend towards digitalisation, financial institutions need to leverage modern technologies to compete

successfully.

● The strategy aims to identify leading users and enablers of innovation in several areas:

Digital Banking

● Internet Finance

● Mobile banking

● Customer Experience

Digital Payments

● Electronic payments

● Digital wallets

● E-commerce

Data & security

● Analytics & Big Data

● Artificial Intelligence

● Cyber-security

Banking Software

● Cloud computing

● Remote working

● Collaboration tools

2512

_2359

6

For professional and institutional investors only. Not for retail investors.

● Data Analytics

● Financial Information Services

● Transaction Management Systems

● Electronic payments and e-commerce

● Banking Software

● Remote working / collaboration tool

● Cyber-security

● Data centers & cloud computing

● IT Services

● Investment Banks

● Thrifts and Mortgage Banks

● Broker Dealers

● Asset Managers

● Life & Non-life Insurance

● Speciality Finance (Credit Cards, Leasing, Financial Guarantors)

● Exchanges

● Property, REITs

● Private Equity

Enablers of financial innovationTraditional financials

The global financials and financial technology universeImportant and diverse sub-sectors

The Financial Technology universe is large and diverse with a low correlation between the different sub-sectors

2512

_2359

7

For professional and institutional investors only. Not for retail investors.

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Dec 17 Aug 18 May 19 Dec 19 Aug 20

MSCI Europe/Financials

-25.2%

S&P 500 Sec/Financials

-5.0%

-40%

-20%

0%

20%

40%

60%

80%

100%

Dec 17 Aug 18 May 19 Dec 19 Aug 20

MSCI World/Financials

-12.0%

MSCI World/Information Tech

93.6%

Low correlation between sub-sectors

Geographical divergence Sector divergence Historical sub-sector divergence*

Geographical, sector and sub-sector divergence offers opportunities

Historical example for illustrative purposes only. Company examples are for illustrative purposes only and are not a recommen dation to buy or sell.

Source: Jupiter/Morningstar, USD, 01.01.18 to 31.08.20.

*Source: Bloomberg, in USD, 31.12.06 to 31.12.07.

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

Dec-06 Apr-07 Aug-07 Dec-07

Deutsche Börse AG 120.0%

Citigroup Inc -44.7%

S&P 500 Index 5.6%

2512

_2359

8

For professional and institutional investors only. Not for retail investors.

Portfolio construction

Yield

Typical selection criteria:

● Dividend yield >5%

● Payout ratio >50%

● Core Tier One Basel III >12%

● Price to Earnings <14x

● Price to Tangible book value <2x

● Return on Equity >13%

Growth

Two areas of focus:

● Emerging Markets

● Structural Growth

Special Situations

Typical area of focus:

● New management

● New strategy, targets

● Sale non-core asset

● Cost cutting

● Return on Equity

● Payout ratio

The reference

Holding examples are for illustrative purposes only and are not a recommendation to buy or sell. Not Fund restrictions, repre sents fund manager style.

Focus: Profitability vs. Revenue growth

Flexibility of geographical and sub-sector divergence is key to the strategy

2512

_2359

9

For professional and institutional investors only. Not for retail investors.

Traditional financials names must adopt new technologies

Source: www.celent.com as at March 2018.

Satya Nadella, CEO of Microsoft on the impact of Covid-19

We have seen two years' worth of digital transformation in two months.

● Spending on technology by banks in the Americas, Europe and

Asia-Pacific is forecast to increase 4.2 per cent this year to just

over $261bn

● This is broken down as follows:

● 45 per cent in North America and

● 32 per cent in Europe

● The figure is forecast to reach $296.5bn by 2021

An unstoppable trend towards digitalisation forces financial

institutions to leverage modern technologies to compete

successfully. The current coronavirus crisis is strengthening the

technology trends that are assaulting the incumbent in the

industry. Any business that is too distracted by short-term

resilience testing will lose ground further over the medium term.

$261.1

$272.6

$284.5

2018

2019

2020

2021

CAGR 4.2%

North America Ο $114.9 bn

Europe Ο $87.7 bn

Asia-Pacific Ο $75.1 bn

Latin America Ο $21.8 bn

$296.5

Sum of IT spending

2512

_2359

10

For professional and institutional investors only. Not for retail investors.

A structural trend, evidenced

1. Poll carried out by Gallup News: http://news.gallup.com/poll/193706/americans-foresee-death-cash-lifetime.aspx

2. HSBC “Disruptive Technologies” paper, January 2018.

3. https://customers.microsoft.com/en-gb/story/hiscox

4. Sergio Ermotti at the BAML 23 rd Annual Financials CEO Conference, 27.09.18.

5. HSBC “Disruptive Technologies” paper, January 2018.

62% of people in the US think that they may see the death

of cash within their lifetime1

Using the Microsoft Intelligent Cloud has helped

Hiscox cut their analysis of flood risk data from 8

months to 12 hours3

Chinese mobile payments totalled $9trn

in 2017, 80x greater than in the US2

Only 15% of Swedish population used cash

for their most recent transaction5

“It’s like if you don’t eat for 3 days then you

lose weight. If you don’t drink then you die.” Sergio Ermotti, CEO of UBS AG on fintech spending.4

“We have seen two years' worth of digital

transformation in two months”Satya Nadella, CEO of Microsoft on the impact of Covid-19

“Your business must be contactless. Your customers can

pay online, over the phone or in a contactless way” Jacinda Ardern, PM of New Zealand advising businesses on way to engage customers following

the Covid-19 outbreak

“Coronavirus is speeding up the death of cash”Gary Cohn, Financial Times

2512

_2359

11

For professional and institutional investors only. Not for retail investors.

60%

28%

9%

0%

20%

40%

60%

80%

2006 2018 2028e

26%

45%52%

63%69%

0%

20%

40%

60%

80%

Italy Western Europe France Nordics UK

Cash usage is falling steadily in the UK

Cash as a % of UK transactions

● In 2006, 60% of all payments in the UK were made using cash,

this fell to 28% in 2018

● By 2028, it is predicted cash will be used for just 9% of

transactions, according to figures from UK Finance

● Contactless payments are contributing to the transition and

are expected to represent 37% of transactions in the UK in

2028 (19% in 2018)

● Cash withdrawals in the UK have halved since the outbreak of

Covid-19 (LINK)

● In other European countries like Germany and Italy, the

transition to cashless payments is still in its infancy

A structural trend, evidenced: The death of cash in the UKGlobal usage of digital payment methods is rising as cash usage falls

Source: UK Finance (“UK Payment Markets 2019”), Euromonitor International Consumer Finance 2019 Edition.

Cash penetration remains lows across Continental Europe

2018 card payment penetration (by value)

2512

_2359

12

For professional and institutional investors only. Not for retail investors.

● E-commerce is growing mid-to-high teens when retail sales

are up low-to-mid single digits

● There is still a long runway to go as e-commerce represents

less than 20% of retails sales in most major economies except

China

● Covid-19 is likely to result into permanent shifts in merchant

and consumer behaviours with many companies setting up an

online store for the first time

A structural trend, evidenced: E-commerceThe rise of e-commerce result into higher online payments volumes

Source: Euromonitor International Consumer Finance 2019 Edition.

21%

17%

15%

9%8%

7% 7%

0%

5%

10%

15%

20%

25%

China UK US France Japan Germany Brazil

The penetration of e-commerce remains low in most countries

E-commerce as a % of retail sales (2018)

2512

_2359

13

For professional and institutional investors only. Not for retail investors.

The cloud transition is accelerating● A Gartner study showed savings of up to 55% over three years

for a company migrating workloads from an on premise data

center to AWS

● A cloud-based IT architecture also allows for faster software

upgrades and is thus an enabler of innovation

● At end 2019, only 22% of IT workloads were located in the

public cloud but this figure is expected to increase to 50% by

2022

● Comments from Microsoft Azure and AWS suggest Covid-19 is

accelerating the transition

A structural trend, evidenced: Cloud computingCloud Computing is a key enabler of digitalisation; the transition away from the old

“on premise” architectures is accelerating

Source: AlphaWise, Morgan Stanley, Gartner.

62%55%

33%

22%29%

50%

16% 16% 17%

0%

20%

40%

60%

80%

100%

End of 2019 Today End of 2022On premise Today Other

Location of IT workloads

2512

_2359

14

For professional and institutional investors only. Not for retail investors.

26%27%

25%

17%

4%

2%

0%

5%

10%

15%

20%

25%

30%

0% will

remain

remote

5% will

remain

remote

10% will

remain

remote

20% will

remain

remote

50% will

remain

remote

>50% will

remain

remote

● Millennials expect to be able to work from home; studies from

Harvard and Stanford suggest remote working lead to lower

employee attrition and higher productivity

● Remote working can also be a driver of cost savings for

companies through real estate optimisation

● Yet, in 2018 only 5% of US workers worked from home on a

full-time basis (10% at least one day a week and 40%+

occasionally)

● A survey from Gartner show 74% of companies are likely to

increase their number of remote workers post Covid-19

A structural trend, evidenced: Working-from-homeThe number of remote workers is likely to increase permanently as a result of Covid-19

Source: Gartner.

74% of companies plan to shift to more remote work post Covid

What % of your workforce will remain permanently remote post-Covid

who were not remote before Covid?

2512

_2359

15

For professional and institutional investors only. Not for retail investors.

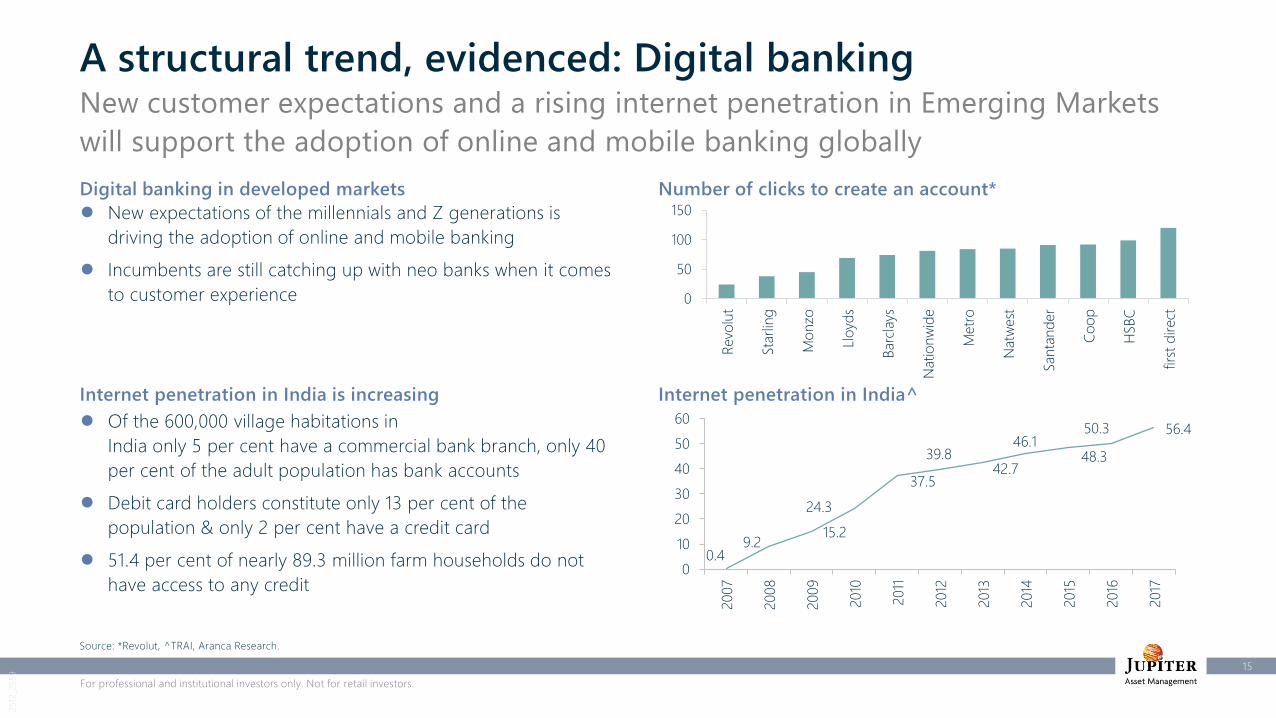

A structural trend, evidenced: Digital banking

● New expectations of the millennials and Z generations is

driving the adoption of online and mobile banking

● Incumbents are still catching up with neo banks when it comes

to customer experience

● Of the 600,000 village habitations in

India only 5 per cent have a commercial bank branch, only 40

per cent of the adult population has bank accounts

● Debit card holders constitute only 13 per cent of the

population & only 2 per cent have a credit card

● 51.4 per cent of nearly 89.3 million farm households do not

have access to any credit

New customer expectations and a rising internet penetration in Emerging Markets

will support the adoption of online and mobile banking globally

Source: *Revolut, ^TRAI, Aranca Research.

0.49.2

15.2

24.3

37.5

39.842.7

46.148.3

50.3 56.4

0

10

20

30

40

50

60

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

0

50

100

150

Revo

lut

Sta

rlin

g

Mo

nzo

Llo

yds

Barc

lays

Natio

nw

ide

Metr

o

Natw

est

Santa

nd

er

Co

op

HSBC

firs

t d

irect

Digital banking in developed markets

Internet penetration in India is increasing Internet penetration in India^

Number of clicks to create an account*

2512

_2359

16

For professional and institutional investors only. Not for retail investors.

Our current positioning

Top 10 holdings Sector breakdown Regional allocation

(%)

Paypal 5.4

MercadoLibre 4.8

S&P Global 4.3

Splunk 4.0

Fidelity National Information 4.0

LSE 4.0

Banque Cantonale Vaudoise 4.0

Adyen 3.8

Deutsche Boerse 3.6

Global Payments 3.3

Total 41.3

(%)

Financial Services 34.3

Support Services 24.2

Software & Computer Services 17.9

Banks 6.0

Real Estate Investment Trusts 4.8

General Retailers 4.8

Real Estate Investment & Services 2.1

Finance and Credit Services 2.0

Nonlife Insurance 1.6

Cash 2.4

Total 100.0

(%)

North America 56.9

Europe ex. UK 20.9

UK 10.5

Caribbean & Latin America 7.3

Asia Pacific ex. Japan 2.0

Cash 2.4

Total 100.0

Jupiter Financial Opportunities Fund – UT

Holding examples are for illustrative purposes only and are not a recommendation to buy or sell.

Source: Jupiter, 31.07.20.

2512

_2359

17

For professional and institutional investors only. Not for retail investors.

● Long term capital growth

● Combination of top-down/bottom-up stock analysis

● Sub-sector fundamental themes

● Opportunistic and effective with capital allocation

● Disciplined process built around Growth, Yield and Special Situations

● Concentrated portfolio

● Portfolio constructed independent of benchmark

● Majority of research conducted internally

● Looks to generate returns in any market conditions

Global Financials & Financial Innovation strategy

Summary

The views expressed are those of the presenter at the time of preparation and may change in the future. Generating return in any market condition is a fund manager aim.

2512

_2359

18

For professional and institutional investors only. Not for retail investors.

APPENDIX

2512

_2359

19

For professional and institutional investors only. Not for retail investors.

Fund manager profile

Jenna Zegleman

Product Specialist

9 years’ experience

Lead Manager

Guy de Blonay

Fund Management

Director, Global

Equities Team

25 years’ experience

2010–Present Lead Manager, Global Financials & Innovation

UK domiciled Financial Opps Unit Trust: €609m

UK Domiciled International Financials Unit Trust: €53m

Jupiter Financial Innovation SICAV: €65m

Total Strategy AUM: €728m

Formerly at Henderson Global Investors Ltd

New Star Asset Management Ltd

Jupiter Asset Management Ltd

Apr 09 – Oct 09

Sep 01 – Apr 09

Sep 95 – Apr 01

Education Law (University of Geneva) Philosophy (Institute Florimont)

Current role

(from 03.18)

Product Specialist - Asian Income, Global Emerging Markets and

Financial Strategies

Formerly at Rathbone Bros PLC, Collectives Research Analyst

Journalist / Editor at FE Trustnet

News Reporter, Investment Adviser, Financial Times

Feb 15 – Feb 18

Sep 12 – Feb 15

Aug 11 – Sep 12

Education MA International Journalism, City University, London

BA Media Communication, Asbury University, USA

Current role

(from 11.18)

Analyst – Global Financials and Financial Innovation strategies

Formerly at Exane BNP Paribas Research Analyst,

Sell Side Equity Research Analyst

Jan 13 – Oct 19

Education MSc Management, Essec Business School, Paris and Singapore

BSc Mathematics and Economics, Madeleine Danielou Institute, Paris

Antoine Hucher

Analyst

6 years’ experience

Supported by the Global Equities team

Jason Pidcock (27 )

Stuart Cox (26)

Abbie Llewellyn Waters (14)

Gregory Herbert (17)

Dan Carter (17)

Mitesh Patel (13)

Mark Evans (18)

And by wider Jupiter teams

CIO OfficeStephen Pearson (34)

Katharine Dryer (23)

Risk analysisVeronica Lazenby (25)

Mark Dempsey (24)

European EquitiesMark Heslop (21)

Mark Nichols (19)

Multi assetTalib Sheikh (22)

Mark Richards (20)

Emerging marketsRoss Teverson (21)

Avinash Vazirani (26)

Global Fixed IncomeAriel Bezalel (23)

Alejandro Arévalo (22)

Absolute returnJames Clunie (31)

Environment &

SustainabilityCharles Thomas (23)

Jon Wallace (11)

Governance

and Sustainability

Ashish Ray (16) Head of Governance and Sustainability

Andrew Mortimer (14) Governance and Sustainability Analyst

Laura Conigliaro (2) Governance and Sustainability Analyst

2512

_2359

20

For professional and institutional investors only. Not for retail investors.

APPENDIXJupiter Financial Opportunities Fund - UT

2512

_2359

21

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Opportunities Fund – UT

Cumulative performance

Past performance is no guide to the future.Source: Morningstar in GBP as at 31.08.20. Fund performance data is calculated on a NAV to NAV or bid to NAV basis dependent on the period of reporting, all performance is net of fees with income reinvested. *Since inception:

02.06.97. Comparator benchmark: MSCI ACWI/Financials. The Fund has permission to enter into derivative transactions but only for the purposes of efficient management of the portfolio and not for investment purposes.

Outperformance 28.2% 42.7% 43.2% 1749.7%

9.633.9

83.3

1,943.4

-18.6 -8.8

40.1

193.8

-50%

0%

50%

100%

150%

200%

250%

300%

YTD 3 years 5 years Since

inception*

Jupiter Financial Opportunities Fund I Acc MSCI ACWI/Financials

1900

1950

2512

_2359

22

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Opportunities Fund – UT

Guy de Blonay; calendar year track record

Past performance is no guide to the future.The Henderson New Star Global Financials was a UCITS structure and was managed by Guy de Blonay from 28.12.01 to 20.10.09 pri or to joining Jupiter. The performance figures are shown as a representation of Guy’s experience only

and are not indicative of any potential future performance. The strategy used may not be representative of the strategy used for any future funds. Guy became lead manager of Jupiter Financial Opportunities on 01.01.11. Source:

Morningstar, bid to bid, income reinvested 31.12.01 to 31.08.20 in GBP. Fund performance data is calculated on a NAV to NAV o r bid to NAV basis dependent on the period of reporting, all performance is net of fees with income

reinvested. Comparator benchmark: MSCI ACWI/Financials.

-5

35

25

49

24

9

-41

45

-2

-24

19

26

48

1318

-5

28

10

-24

26

11

26

10

-6

-36

27

10

-18

2420

10

0

35

14

-10

19

-19

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 YTD

Henderson New Star Global Financials I Acc Jupiter Financial Opportunities I Acc MSCI ACWI/Financials

2512

_2359

23

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Opportunities Fund – UT

Performance

Past performance is no guide to the future.Fund performance data is calculated on a NAV to NAV or bid to NAV basis dependent on the period of reporting, all performance is net of fees with income reinvested.

Source: FE Fundinfo in GBP, to 31.08.20. Target benchmark: MSCI ACWI/Financials. Guy de Blonay became co-manager of the Fund from 01.06.10 and the lead manager from 01.01.11.

(%) YTD 1 year 3 years 5 years

Jupiter Financial Opportunities I ACC 9.6 5.0 33.9 83.3

MSCI ACWI/Financials -18.6 -14.4 -8.8 40.1

Relative 28.2 19.4 42.7 43.2

(%) 2019 2018 2017 2016 2015

Jupiter Financial Opportunities I ACC 27.9 -5.2 18.3 12.9 8.3

MSCI ACWI/Financials 19.3 -9.9 14.0 34.9 0.4

2512

_2359

24

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Opportunities Fund – UT

12-month rolling performance

Past performance is no guide to the future.Fund performance data is calculated on a NAV to NAV or bid to NAV basis dependent on the period of reporting, all performance is net of fees with income reinvested.

Source: FE Fundinfo in GBP, to 31.08.20. Since inception: 02.06.97. Fund manager inception: 01.06.10. Target benchmark: MSCI ACWI/Financials

(%)01 Sep '15 to

31 Aug '16

01 Sep '16 to

31 Aug '17

01 Sep '17 to

31 Aug '18

01 Sep '18 to

31 Aug '19

01 Sep '19 to

31 Aug '20

Jupiter Financial Opportunities I ACC 10.9 23.4 15.2 10.7 5.0

MSCI ACWI/Financials 19.1 29.0 4.7 1.8 -14.4

2512

_2359

25

For professional and institutional investors only. Not for retail investors.

● The fund invests in a specific market sector, so may be subject to greater volatility risk over short periods of time.

● The fund may use derivatives which may result in large fluctuations in the value of the fund.

● Counterparty risk may cause losses to the fund.

● This fund invests mainly in shares and it is likely to experience fluctuations in price which are larger than funds that inve st only in bonds

and/or cash.

● The Key Investor Information Document, Supplementary Information Document and Scheme Particulars are available from Jupiter on

request.

● This fund can invest more than 35% of its value in securities issued or guaranteed by an EEA state.

Jupiter Financial Opportunities Fund

2512

_2359

26

For professional and institutional investors only. Not for retail investors.

APPENDIXJupiter Financial Innovation - SICAV

2512

_2359

27

For professional and institutional investors only. Not for retail investors.

Our current positioning

Top 10 holdings Sector breakdown Regional allocation

(%)

Paypal 5.3

MercadoLibre 4.8

S&P Global 4.2

Fidelity National Information 4.0

Okta 4.0

Sea 4.0

Adyen 3.8

Alibaba 3.6

Costar 3.4

Global Payments 3.3

Total 40.4

(%)

Software & Computer Services 44.0

Financial Services 30.3

Support Services 20.6

General Retailers 9.9

Banks 4.6

Nonlife Insurance 3.7

Real Estate Investment Trusts 3.3

Technology Hardware & Equipment 1.8

Real Estate Investment & Services 1.5

Cash -19.7

Total 100.0

(%)

North America 76.9

Europe ex UK 16.5

UK 10.1

Asia Pacific ex Japan 9.3

Caribbean & Latin America 6.8

Cash -19.7

Total 100.0

Jupiter Financial Innovation - SICAV

Holding examples are for illustrative purposes only and are not a recommendation to buy or sell.

Source: Jupiter, 31.07.20.

2512

_2359

28

For professional and institutional investors only. Not for retail investors.

Risk metrics

Volatility**

Performance since inception in EUR

Performance and risk metricsJupiter Financial Innovation - SICAV

Past performance is no indication of current or future performance, doesn’t take into account commissions and costs incurred on the issue/redemption of shares.Source: Morningstar, NAV to NAV, gross income reinvested, net of fees, in EUR, to 31.08.20. *Based on daily returns since fun d launch on 02.11.06.

**The volatility and Sharpe ratios are based on annualised figures for monthly returns. Risk free rate of Euribor 3 Months.

Since inception

3 years

3 years

19.03

26.09

20.55

21.74

Sharpe ratio**

0.02

0.13

0.58

0.37

Performance ranking

Since inception 1 year 3 years

Jupiter Financial

Innovation L EUR Acc2 / 10 3 / 17 2 / 15

105.4

12.60.1

14.9

-11.6

32.0

11.113.95.7

16.49.6

-10.9

26.4

-22.7-40

-20

0

20

40

60

80

100

120

Sin

ce

ince

ptio

n*

201

5

201

6

201

7

201

8

201

9

YTD

(%)Jupiter Financial Innovation L EUR Acc MSCI ACWI/Financials

2512

_2359

Since inception

29

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Innovation - SICAV

Cumulative performance

Past performance is no indication of current or future performance. Performance data does not take into account commissions a nd costs incurred on the issue and redemption

of shares. Source: FE fundinfo in EUR, NAV to NAV, gross income reinvested, net of fees, to 31.08.20. Guy became lead manager of Jupiter Financial Innovatio n on 01.01.15. The fund changed its name, objective and

investment policy as at 03.12.18. *Since inception: 02.11.06.

11.1 10.9

32.4

51.8

105.4

-22.7-13.4

-5.8

14.3 13.9

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

YTD 1 year 3 years 5 years Since inception*

Jupiter Financial Innovation L EUR Acc MSCI ACWI/Financials

Outperformance 33.8% 24.3% 38.2% 37.5% 91.5%

2512

_2359

30

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Innovation - SICAV

Guy de Blonay; calendar year track record

Past performance is no indication of current or future performance, doesn’t take into account commissions and costs incurred on the issue/redemption of shares.The Henderson New Star Global Financials was a UCITS structure and was managed by Guy de Blonay from 28.12.01 to 20.10.09 prior to joining Jupiter, all Figures in GBP. The performance figures

are shown as a representation of Guy’s experience only and are not indicative of any potential future performance. The strate gy used may not be representative of the strategy used for any future funds. Guy became

lead manager of Jupiter Financial Innovation on 01.01.15. Source: Morningstar, NAV to NAV, gross income reinvested, net of fe es, to 31.08.20 in EUR. Fund performance data is calculated on a NAV to NAV or bid to NAV

basis dependent on the period of reporting, all performance is net of fees with net income reinvested. The fund changed its n ame, objective and investment policy as at 03.12.18.

-11

2024

51

26

0

-55

40

13

0

15

-12

32

11

-28

1610

30

12

-14

-51

33

6

16

10

-11

26

-23

-80%

-60%

-40%

-20%

0%

20%

40%

60%

2002 2003 2004 2005 2006 2007 2008 2009 2015 2016 2017 2018 2019 YTD

Henderson New Star Global Financials I Acc Jupiter Financial Innovation L EUR Acc MSCI ACWI/Financials GTR

2512

_2359

31

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Innovation - SICAV

Performance

Past performance is no indication of current or future performance, doesn’t take into account commissions and costs incurred on the issue/redemption of shares.Source: FE fundinfo, NAV to NAV, gross income reinvested, net of fees, to 31.08.20. Guy became lead manager of Jupiter Financial Innovation on 01.01.15. The fund changed its name, objective and investment policy

as at 03.12.18.

(%) YTD 1 year 3 years 5 years

Jupiter Financial Innovation L A Inc GBP 17.0 9.5 28.7 86.9

MSCI ACWI/Financials in GBP -18.6 -14.4 -8.8 40.1

Relative 35.5 23.9 37.5 46.8

(%) 2019 2018 2017 2016 2015

Jupiter Financial Innovation L A Inc GBP 25.1 -10.6 18.8 16.9 6.2

MSCI ACWI/Financials in GBP 19.3 -9.9 14.0 34.9 0.4

2512

_2359

32

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Innovation - SICAV

Performance

Past performance is no indication of current or future performance, doesn’t take into account commissions and costs incurred on the issue/redemption of shares.Source: FE fundinfo, NAV to NAV, gross income reinvested, net of fees, to 31.08.20. Guy became lead manager of Jupiter Financial Innovation on 0 1.01.15. The fund changed its name, objective and investment policy

as at 03.12.18.

(%) YTD 1 year 3 years 5 years

Jupiter Financial Innovation L Acc EUR 11.1 10.9 32.4 51.8

MSCI ACWI/Financials in EUR -22.7 -13.4 -5.8 14.3

Relative 33.8 24.3 38.2 37.5

(%) 2019 2018 2017 2016 2015

Jupiter Financial Innovation L Acc EUR 32.0 -11.6 14.9 0.1 12.6

MSCI ACWI/Financials in EUR 26.4 -10.9 9.6 16.4 5.7

2512

_2359

33

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Innovation - SICAV

Performance

Past performance is no indication of current or future performance, doesn’t take into account commissions and costs incurred on the issue/redemption of shares.Source: FE fundinfo, NAV to NAV, gross income reinvested, net of fees, to 31.08.20. Guy became lead manager of Jupiter Financial Innovation on 01.01.15. The fund changed its name, objective and investment policy

as at 03.12.18.

(%) YTD 1 year 3 years 5 years

Jupiter Financial Innovation L Acc USD 16.7 8.9 28.2 85.5

MSCI ACWI/Financials in USD -18.6 -14.4 -8.8 40.1

Relative 35.3 23.4 36.9 45.4

(%) 2019 2018 2017 2016 2015

Jupiter Financial Innovation L Acc USD 29.4 -15.5 30.5 -3.0 0.8

MSCI ACWI/Financials in USD 24.1 -15.2 24.8 13.1 -5.1

2512

_2359

34

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Innovation - SICAV

Performance

Past performance is no indication of current or future performance, doesn’t take into account commissions and costs incurred on the issue/redemption of shares.Source: FE fundinfo, NAV to NAV, gross income reinvested, net of fees, to 31.07.20. Guy became lead manager of Jupiter Financial Innovation on 01.01.15. The fund changed its name, objective and investment policy

as at 03.12.18.

(%) YTD 1 year 3 years 5 years

Jupiter Financial Innovation L HSC Acc USD 10.8 2.6 35.9 N/A

MSCI ACWI/Financials in EUR -22.7 -13.4 -5.8 N/A

Relative 33.5 15.9 41.6 N/A

(%) 2019 2018 2017 2016 2015

Jupiter Financial Innovation L HSC Acc USD 35.6 -9.4 16.6 0.4 N/A

MSCI ACWI/Financials in EUR 26.4 -10.9 9.6 16.4 N/A

2512

_2359

35

For professional and institutional investors only. Not for retail investors.

Jupiter Financial Innovation - SICAV

12-month rolling performance

(%)

01 Sep '15 to

31 Aug '16

01 Sep '16 to

31 Aug '17

01 Sep '17 to

31 Aug '18

01 Sep '18 to

31 Aug '19

01 Sep '19 to

31 Aug '20

Jupiter Financial Innovation L EUR Acc -2.1 17.1 14.8 4.0 10.9

MSCI ACWI/Financials 2.0 18.9 7.9 0.8 -13.4

Past performance is no indication of current or future performance, doesn’t take into account commissions and costs incurred on the issue/redemption of shares.

Source: Morningstar, NAV to NAV, gross income reinvested, net of fees, in EUR, to 31.08.2020.

2512

_2359

36

For professional and institutional investors only. Not for retail investors.

Available share classes

Reinvestment and payment of dividends takes place on the 10th business day after quoted ex date.

** The Ongoing Charges Figure is based on fees and expenses for the year ended 30.09.19. It includes the Annual Management Ch arge and aggregate operating fees chargeable to the fund. Where the fund invests in

other funds, it includes the impact of the charges made in those funds. Jupiter does not engage in stock lending. For details of all share classes and fees and charges, please refer to the Prospectus and Annual Report

for each financial year . Note: HSC = Hedged.

Share class Currency Distribution policy ex date* ISIN Bloomberg AMC OCF**

L EUR Acc EUR Accumulation N/A LU0262307480 JGGFLEU LX 1.50% 1.72%

L GBP A Inc GBPAnnual distribution

(reinvested)30.09 LU0262308454 JGGFLGB LX 1.50% 1.72%

D GBP Acc GBP Accumulation N/A LU0946220695 JGGFDGA LX 0.75% 0.95%

D EUR Acc EUR Accumulation N/A LU0946220265 JGGFDAE LX 0.75% 0.95%

L USD Acc USD Accumulation N/A LU0262307720 JGGFLUS LX 1.50% 1.72%

L USD Acc HSC USD Accumulation N/A LU1314348803 JGFLUAH LX 1.50% 1.72%

D USD Acc USD Accumulation N/A LU0946220349 JGGFDAU LX 0.75% 0.95%

2512

_2359

37

For professional and institutional investors only. Not for retail investors.

● The fund uses derivatives, which may increase volatility; the Fund’s performance is unlikely to track the performance of broader

markets.

● Losses on short positions may be unlimited.

● Counterparty risk may cause losses to the fund.

● The fund can use gearing to increase exposure to financials markets, which may cause large fluctuations in the value of the portfolio.

● The fund invests in a specific market sector, so may be subject to greater volatility risk over short periods of time.

● This fund invests mainly in shares and it is likely to experience fluctuations in price which are larger than funds that inve st only in bonds

and/or cash.

● The Key Investor Information Document and Prospectus are available from Jupiter on request.

● This fund can invest more than 35% of its value in securities issued or guaranteed by an EEA state.

● Synthetic Risk Reward Indicator (SRRI) as per the most up to date Key Investor Information Document (07.02.20).

For share class L Eur Acc:

Jupiter Financial Innovation

Synthetic Risk Reward Indicator (SRRI) is based on past data, may change over time and may not be a reliable indication of th e future risk profile of the Fund. The lowest category does not mean 'no risk'.

Please see the Key Investor Information Document for further information.

1 2 3 4 5 6 7

Typically lower rewards,

lower risk

Typically higher rewards,

higher risk

2512

_2359

38

For professional and institutional investors only. Not for retail investors.

This presentation is intended for investment professionals and not for

the benefit of retail investors. Market and exchange rate movements

can cause the value of an investment to fall as well as rise, and you may

get back less than originally invested. Initial charges are likely to have a

greater proportionate effect on returns if investments are liquidated in

the shorter term. Any data or views given should not be construed as

investment advice.

Past performance is no indication of current or future performance.

Performance data does not take into account commissions and

costs incurred on the issue and redemption of shares. Company

examples are for illustrative purposes only and are not a

recommendation to buy or sell. Quoted yields are not guaranteed

and may change in the future. Awards and ratings should not be

taken as a recommendation.

Every effort is made to ensure the accuracy of the information but

no assurance or warranties are given. It is not an invitation to

subscribe for shares in the Jupiter Global Fund (the Company) or

any other fund managed by Jupiter Asset Management Limited.

The Company is a UCITS fund incorporated as a Société Anonyme

in Luxembourg and organised as a Société d’investissement à

Capital Variable (SICAV). This information is only directed at

persons residing in jurisdictions where the Company and its shares

are authorised for distribution or where no such authorisation is

required.

The sub fund(s) may be subject to various other risk factors, please

refer to the Prospectus for further information.

Prospective purchasers of shares of the sub fund(s) of the Company

should inform themselves as to the legal requirements, exchange

control regulations and applicable taxes in the countries of their

respective citizenship, residence or domicile. Subscriptions can only

be made on the basis of the current Prospectus and the Key

Investor Information Document (KIID), accompanied by the most

recent audited annual report and semi-annual report. These

documents are available for download from www.jupiteram.com.

The KIID and, where required, the Prospectus, along with other

advertising materials which have been approved for public

distribution in accordance with the local regulations are available in

English, Dutch, French, Finnish, German, Italian, Portuguese,

Spanish and Swedish. Before subscribing, please read the

Prospectus. Hard copies may be obtained free of charge upon

request from any of :

The Company Custodian and Administrator : JP Morgan Bank

Luxembourg S.A, 6 Route de Trèves, Senningerberg, L-2633,

Luxembourg; and from certain of the Company’s distributors;

Austria: Jupiter Asset Management International S.A., Austria

branch, Goldenes Quartier, Tuchlauben 7a, 1010 Vienna, Austria;

Belgium: BNP Paribas Securities Services, Boulevard Louis Schmidt 2,

1040 Brussels; France: CACEIS Bank France, 1/3 Place Valhubert,

75013 Paris, France; Germany: Jupiter Asset Management

International S.A., Frankfurt branch, whose registered office is at:

Roßmarkt 10, 60311 Frankfurt, Germany; Italy: BNP Paribas Securities

Services, Milan branch, Piazza Lina Bo Bardi, 3 20124 Milano, Italy.

Allfunds Bank, S.A.U., Milan Branch, Via Bocchetto 6, 20123 Milano,

Italy. Société Générale Securities Services, Via Benigno Crespi 19,

20159 Milano, Italy. The Fund has been registered with the

Commissione Nazionale per le Società e la Borsa (CONSOB) for the

offer in Italy to retail investors; Luxembourg: the Company's

registered office; 6 Route de Trèves, Senningerberg, L-2633,

Luxembourg; Spain: Allfunds Bank, C/ La Estafeta 6, Edificio 3, 28109

Alcobendas, Madrid, Spain. For the purposes of distribution in

Spain, the Company is registered with the Spanish Securities

Markets Commission – Comisión Nacional del Mercado de Valores

(“CNMV”) under registration number 1253, where complete

information, including a copy of the marketing memorandum, is

available from the Company authorised is distributors.

Subscriptions should be made through a locally authorised

distributor. The net asset value available on www.jupiteram.com.

Sweden: Jupiter Asset Management International S.A., Nordic

branch, 4th Floor, Strandvagen 7A, 114 56 Stockholm, Sweden;

Switzerland: Copies of the Memorandum and Articles of

Association, the Prospectus, KIIDs and the annual and semi-annual

reports of the Company may be obtained free of charge from the

Company’s representative and paying agent in Switzerland, BNP

Paribas Securities Services, Paris, Succursale de Zurich, whose

registered office is at Selnaustrasse 16, 8002 Zurich, Switzerland;

United Kingdom: Jupiter Asset Management Limited (the

Investment Manager), registered address: The Zig Zag Building, 70

Victoria Street, London, SW1E 6SQ, United Kingdom, authorised

and regulated by the Financial Conduct Authority.

Issued by The Jupiter Global Fund and/or Jupiter Asset

Management International S.A. (JAMI, the Management Company),

registered address: 5, Rue Heienhaff, Senningerberg L-1736,

Luxembourg which is authorised and regulated by the Commission

de Surveillance du Secteur Financier.

No part of this presentation may be reproduced in any manner

without the prior permission of the Company or JAMI.

Disclosure

2512

_2359

39

For professional and institutional investors only. Not for retail investors.

Industry Classification Benchmark (‘ICB’) is a product of FTSE International Limited (‘FTSE’) and all intellectual property r ights in and to ICB

vest in FTSE. Jupiter Asset Management Limited has been licensed by FTSE to use ICB. ‘FTSE®’ is a trade mark owned by the Lon don

Stock Exchange Plc and is used by FTSE under licence. FTSE and its licensors do not accept liability to any person for any lo ss or damage

arising out of any error or omission in ICB.

This document contains information based on the FTSE 100 Index. ‘FTSE®’ is a trade mark owned by the London Stock Exchange Pl c and

is used by FTSE International Limited (‘FTSE’) under licence. The FTSE 100 Index is calculated by FTSE. FTSE does not sponsor, endorse or

promote the product referred to in this document and is not in any way connected to it and does not accept any liability in r elation to its

issue, operation and trading. All copyright and database rights in the index values and constituent list vest in FTSE.

This document contains information based on the MSCI World and MSCI AC World Financials Indices. Neither MSCI nor any other p arty

involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or represent ations with

respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all w arranties of

originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Wi thout limiting

any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, c omputing or

creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits)

even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted w ithout MSCI’s

express written consent.

Indices disclosure

2512

_2359