an interest rate model for counterparty credit risk - tu delft

TRANSCRIPT

Delft University of TechnologyFaculty of Electrical Engineering, Mathematics and Computer Science

Delft Institute of Applied Mathematics

An interest rate model for counterparty credit risk

A thesis submitted to theDelft Institute of Applied Mathematicsin partial fulfillment of the requirements

for the degree

MASTER OF SCIENCEin

APPLIED MATHEMATICS

by

M.C.A. de Ruijter

Delft, the NetherlandsMay 2010

Copyright c© 2010 by M.C.A. de Ruijter. All rights reserved.

MSc THESIS APPLIED MATHEMATICS

“An interest rate model for counterparty

credit risk”

M.C.A. de Ruijter

Delft University of Technology

Daily supervisors Responsible professor

Drs. J. Hommels (Rabobank) Prof. dr. F.M. Dekking

Dr. J.A.M. van der Weide (TU Delft)

Other thesis committee members

Prof. dr. C.W. Oosterlee

June 2010 Delft, the Netherlands

ii

Abstract

Counterparty credit risk is one of the many types of risk a financial institution such as a bankhas to deal with. It is defined as the risk that the counterparty to a derivative transactioncould default before the final settlement of the transaction´s cash flows. Quantifying counter-party credit risk is complicated since the loss due to the default of a counterparty is uncertainfor a derivative contract. The future value of a derivative contract depends on one or severalmarket factors. To calculate the counterparty credit risk we estimate the exposure distribu-tion for each of the derivative contracts with a certain counterparty. This can amongst othersbe done by Monte Carlo simulation. It involves using Monte Carlo simulation to generate alarge number of possible future scenarios for several market factors. These scenarios will thenbe used to value every derivative contract, through time. This results in a exposure distribution.

Before we can generate these scenarios we have to develop a model for each of the marketfactors. In this thesis we will focus on the development of a model for the interest rates. We willresearch several options for the estimaton of the parameters such as maximum likelihood butalso methods based on the market expectations theory and the characteristics of the historicaldata. The model used here is a geometric Brownian motion with mean reversion process forthe forward rates. Using the historical data we will assess the fit of this model to the historicaldata. We will research options to change the parameter estimates in such a way that we willnot underestimate the counterparty credit risk. We will also research the assumptions madein the model. The performance of the model chosen will also be assessed by the calculation ofthe characteristics of the exposure distribution for two interest rate derivatives, the interest rateswap and the forward rate agreement.

iii

iv

Preface

This is it, the report of my Master’s thesis at Rabobank International. Several months precededthis report, for which the foundation was laid in July 2009. During my studies, I got more andmore interested in the applications of mathematics in finance. After attending various courseson finance, Hans van der Weide pointed me on the opportunity to do an internship for my thesisat Rabobank International. From my curiosity in finance, it seemed to me as a great chance tosee how to apply mathematical principles in a business setting. More specifically, I have put mymathematical knowledge to use in the area of counterparty credit risk. A very interesting topic,where I learned a lot about in a very short period. Besides content-wise, the project exhibitedthe interesting company Rabobank International, great colleagues, and a challenging workingenvironment.

Therefore, I would like to first of all thank my supervisor at Rabobank International, JasperHommels. From the start of my internship, his support has enabled me to complete this thesiswork. In our meetings, he provided great input and together we cracked various challenges.Furthermore, I want to thank everybody I met during my internship at Rabobank for theirinterest in my work, especially everybody at the Quantative Risk Analytics deparment.

Without support from Delft University of Technology, I would not have been able to performthis project. First of all, thanks to Hans van der Weide for pointing out the opportunity of grad-uating at Rabobank International. It triggered me to make the first step towards performingthis thesis work. Michel Dekking and Kees Oosterlee, I want to thank you together with Hansfor reviewing this thesis report and my thesis defence.

Furthermore, I want to thank my family and friends, especially my boyfriend. Besides listeningto every issue I had when writing this thesis and all the enthusiastic stories about what I wasworking on, he was also a great help with some of the figures.

A final thanks goes to you, my reader. Thanks for your interest in this report and my thesiswork. This work considerably contributed to my knowledge on finance and counterparty creditrisk. Curious about what I learned? Please continue and have fun reading!

Marieke de RuijterAmsterdam, The Netherlands

June, 2010

v

vi

Contents

List of Figures ix

List of Tables xi

List of Abbreviations xiii

1 Counterparty credit risk 1

1.1 Potential future exposure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.2 Exposure at default . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.3 Outline . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

2 Interest rate products 9

2.1 Forward rate agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.2 Interest rate swaps . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.3 The historical exposure for the FRA and the IRS . . . . . . . . . . . . . . . . . . 13

3 Data analysis 17

3.1 Interest rate data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

3.2 Forward rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3.3 Yield curve . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4 Interest rate models 21

4.1 Requirements for the interest rate model . . . . . . . . . . . . . . . . . . . . . . . 21

4.2 Potential models for the interest rate . . . . . . . . . . . . . . . . . . . . . . . . . 22

4.3 Modeling forward rates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

4.4 Geometric Brownian motion with mean reversion . . . . . . . . . . . . . . . . . . 25

4.5 Correlation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

4.5.1 Proof of equation (4.28) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

4.6 Disadvantage of the model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

5 Calibration 33

5.1 Estimation of the correlation ρ . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

5.2 The method of least squares/maximum likelihood estimation . . . . . . . . . . . 34

5.2.1 Independent estimation of σ . . . . . . . . . . . . . . . . . . . . . . . . . . 39

5.3 Market expectations theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

5.3.1 Disadvantages of this approach . . . . . . . . . . . . . . . . . . . . . . . . 42

5.3.2 Advantages of this approach . . . . . . . . . . . . . . . . . . . . . . . . . . 44

5.4 Using long term quantiles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

5.5 Comparison of methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

vii

viii CONTENTS

6 Residuals 57

6.1 Standard normal distributed residuals . . . . . . . . . . . . . . . . . . . . . . . . 576.1.1 Kurtosis scaling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 596.1.2 Quantile scaling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 606.1.3 Comparison of scaling methods . . . . . . . . . . . . . . . . . . . . . . . . 61

6.2 Independent and identically distributed residuals . . . . . . . . . . . . . . . . . . 64

7 Conclusions 71

Bibliography 74

A Calculations method of least squares 77

B Calculations maximum likelihood method 79

C Value of the floating leg part in an IRS 81

List of Figures

1.1 Illustration of how to compute the PFE. . . . . . . . . . . . . . . . . . . . . . . . 4

1.2 Illustration of the computation of the effective EPE. . . . . . . . . . . . . . . . . 6

2.1 Notional outstanding per type of OTC derivative. . . . . . . . . . . . . . . . . . . 9

2.2 Notional outstanding per interest rate product. . . . . . . . . . . . . . . . . . . . 10

2.3 The exposure for a FRA starting at 26-04-2005. . . . . . . . . . . . . . . . . . . . 14

2.4 The exposure for a IRS starting at 20-12-2002. . . . . . . . . . . . . . . . . . . . 14

3.1 The 6 months and 20 years tenor points for the EUR interest rate data. . . . . . 18

3.2 The 6 months and 20 years tenor points for the USD interest rate data. . . . . . 18

3.3 The stepwise behavior of the 1 month EUR interest rate. . . . . . . . . . . . . . 19

3.4 The 6 months to 1 year forward rate, calculated from the interest rate data. . . . 19

3.5 Fitted yield curve at 3-12-2008 (black solid) and 2-12-2009 (green dashed). . . . . 20

4.1 A simulated path for the geometric Brownian motion with mean reversion model. 28

4.2 The correction factor c depending on the size of the time step ∆t. . . . . . . . . 30

4.3 The influence of the start value on the mean reversion. . . . . . . . . . . . . . . . 31

5.1 Density of bootstrapped estimators for k including the input value (red line). . . 36

5.2 Density of bootstrapped estimators for θ including the input value (red line). . . 36

5.3 Density of bootstrapped estimators for σ including the input value (red line). . . 37

5.4 Estimator for k through time using partitions of 1000 observations. . . . . . . . . 38

5.5 Estimator for θ through time using partitions of 1000 observations. . . . . . . . . 38

5.6 Estimator for σ through time using partitions of 1000 observations. . . . . . . . . 38

5.7 Implied expectations and the approximation by equation (5.15). . . . . . . . . . . 41

5.8 Estimates for k for the last 1000 days in the dataset. . . . . . . . . . . . . . . . . 43

5.9 Estimates for θ for the last 1000 days in the dataset. . . . . . . . . . . . . . . . . 43

5.10 The humped yield curve at 18-12-2008. . . . . . . . . . . . . . . . . . . . . . . . . 44

5.11 Approximation of the implied expectation of a humped yield curve. . . . . . . . . 44

5.12 The 2.5% and 97.5% quantiles of the simulated 5-10y forward rate. . . . . . . . . 45

5.13 The 2.5% and 97.5% quantiles of the simulated exposure for an FRA. . . . . . . 46

5.14 The 95% confidence interval for the 6 months to 1 year EUR forward rate. . . . . 49

5.15 The 95% confidence interval for the 0 to 1 month EUR forward rate. . . . . . . . 49

5.16 The 95% confidence interval for the 1 year EUR interest rate. . . . . . . . . . . . 50

5.17 The 95% confidence interval for the 20 years EUR interest rate. . . . . . . . . . . 50

5.18 The simulated PFE for an IRS where we pay floating and receive fixed. . . . . . 52

5.19 The simulated PFE for an IRS where we pay fixed and receive floating. . . . . . 52

5.20 The simulated PFE for an FRA where we pay floating and receive fixed. . . . . . 53

5.21 The simulated PFE for an FRA where we pay fixed and receive floating. . . . . . 54

ix

x LIST OF FIGURES

6.1 The density of the residuals for the USD 1y-2y forward rate. . . . . . . . . . . . 586.2 The density of the residuals R for the USD 1y-2y forward. . . . . . . . . . . . . . 596.3 The distribution of σεε for the different scaling methods. . . . . . . . . . . . . . . 626.4 The quantiles for an interest rate swap using different scaling methods. . . . . . . 636.5 The quantiles for the 6m-1y EUR forward rate using different scaling methods. . 636.6 Clustering in the EUR 10y-20y forward rate residuals. . . . . . . . . . . . . . . . 656.7 Autocorrelation function for the EUR 10y-20y forward rate residuals. . . . . . . . 656.8 Simulated quantiles for the 5 to 10 year forward rates. . . . . . . . . . . . . . . . 676.9 Simulated quantiles for the 5 to 10 year forward rates. . . . . . . . . . . . . . . . 686.10 Simulated quantiles for a 5 year interest rate swap. . . . . . . . . . . . . . . . . . 68

List of Tables

5.1 Estimates for k, θ and σ using the method of least squares/maximum likelihood 355.2 Estimates for σ. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 395.3 Estimates for k, θ and σ using market expectations theory. . . . . . . . . . . . . 415.4 Available long term interest rate data per tenor point. . . . . . . . . . . . . . . . 475.5 Quantiles and parameter estimates for the long term quantile method. . . . . . . 48

6.1 Kurtosis of the historical residuals and the resulting scaling for σ. . . . . . . . . . 606.2 Quantiles of the historical residuals and the resulting scaling for σ. . . . . . . . . 616.3 Parameter estimates for GARCH parameters. . . . . . . . . . . . . . . . . . . . . 666.4 Estimates for σt0 and the long term mean for σ. . . . . . . . . . . . . . . . . . . . 67

xi

xii LIST OF TABLES

List of Abbreviations

CCR counterparty credit risk

CRD Capital Requirements Directive

CSA credit support annex

DNB De Nederlandse Bank

EAD exposure at default

EE expected exposure

EPE expected positive exposure

FRA forward rate agreement

IRS interest rate swap

OTC over-the-counter

PFE potential future exposure

SFT security financing transaction

xiii

xiv LIST OF TABLES

Chapter 1

Counterparty credit risk

Financial institutions are subject to several types of risk such as credit risk and market risk.To safeguard themselves against these risks and to meet regulations these institutions have toquantify the risks they bear. One of these risks is counterparty credit risk, the risk that thecounterparty to a derivative transaction could default before the final settlement of the transac-tion’s cash flows1. Only over-the-counter (OTC) derivatives and security financing transactions(SFT) are subject to counterparty credit risk, since exchange-traded derivatives payments areguaranteed by the exchange. Counterparty credit risk is similar to other types of credit risk,for example the credit risk involved with a loan, since the cause of the loss is the default ofthe counterparty. Two distinctive features of counterparty credit risk are the uncertainty ofthe magnitude of the possible loss and the fact that both parties in a contract may face anexposure, which is the positive value of the contract assuming zero recovery in case of default.For a derivative contract the value depends on the future development of one or several marketfactors, such as interest rates. We can illustrate the bilateral nature of the risk by consideringan interest rate product with a certain counterparty, where for us the value of the contract willrise as interest rates rise. Then if interest rates rise the counterparty owes us money. However,if interest rates decrease the value of the contract will be negative for us, which means that weowe the counterparty money. So depending on the development of future interest rates bothparties can have an exposure.

Two examples of over-the-counter derivatives are interest rate swaps (IRS) and forward rateagreements (FRA). In an interest rate swap two parties agree to swap floating interest rate pay-ments for fixed interest rate payments based on a specified notional. In a forward rate agreementtwo parties agree to swap a floating interest rate payment for a fixed interest rate payment on aspecified notional for a single specified future period. Despite of the fact that in these contractsthe notional and fixed payments are agreed on, the future floating interest rate depends on thedevelopment of the interest rates and cannot be determined in advance. The value of an interestrate swap or a forward rate agreement will thus be uncertain for any time point in the future.The forward rate agreement and the interest rate swap will be discussed in detail in chapter2. Both the interest rate swap and the forward rate agreement fall in the category of interestrate derivatives. Besides interest rate derivatives also credit, equity, currency and commodityderivatives fall under over-the-counter derivatives and are subject to counterparty credit risk. Iffor example a financial institution has such a OTC-derivative contract with a certain counter-party and this counterparty defaults during the maturity of the contract there are two possiblescenarios. If the value of the contract is negative, meaning that the financial institution owesthis counterparty money, there will be no loss to the financial institution. This institution will

1Quoted from article 5:1 in DNB [7], documentation of the Dutch Central Bank.

1

2 CHAPTER 1. COUNTERPARTY CREDIT RISK

close out their position by paying the market value of the contract to the defaulting counterpartyand enter a similar contract with another counterparty where they will receive the market valueof the contract. If the value of the contract is positive, the financial institution will also closeout their position, making a claim equal to the positive value of the contract. Depending onthe recovery rate they may recover a part of the value of the contract. However, to enter asimilar contract with another counterparty the institution will have to pay the market value ofthe contract. The loss will thus be equal to the value of the contract less any recovery value.This means that only when the value of the contract is positive the financial institution willsuffer a credit loss in case of default of the counterparty.

Security lending transactions, repos and sell/buy back transactions are examples of securityfinancing transactions. These kind of transactions are also subject to counterparty credit risk.The common factor in these transactions is the temporary transfer of a security. In a securitylending transaction a security is temporarily lent by one party (the lender) to another party(the borrower) mostly on a collateralized basis. The borrower is obliged to return the secu-rities and will have to pay a certain fee for the lending. This lending is done to cover shortpositions for example. With a repo or sale and repurchase agreement one party (the seller)sells securities to another party (the buyer) where the parties agree that these securities will berepurchased at a specified date for a specified price. A sell/buy back transaction is similar to arepo but technically consists of two transactions; the selling of the securities and a simultaneousforward repurchase. The purpose of a repo or a sell/buy back transaction is either the transferof ownership of the security or to obtain a loan, generally at a lower rate then an unsecuredloan. The rate for this loan is lower since, in case of default of the seller the buyer still ownsthe securities. Just as with OTC derivatives the magnitude of the possible loss in case of de-fault is uncertain since this will depend on the value of the securities involved in the transaction2.

Also Rabobank will have to quantify their counterparty credit risk. To be compliant with themost risk sensitive measures for counterparty credit risk the Horizon project has been set up inRabobank. The goal of the project is two-fold. Firstly, Rabobank wants to be able to assess thepossible future exposure for every counterparty as accurately as possible to be confident that thefuture exposure for a counterparty does not exceed the limits set for this exposure. Secondly,Rabobank wants to be compliant with the most sophisticated regulations for capital reserves. Inthe Netherlands banks are regulated by the Dutch central bank (DNB). The Dutch regulationsfor counterparty credit risk are described in the Supervisory Regulation on Solvency Require-ments for Credit Risk see DNB [7]. These regulations are based on the Capital RequirementsDirective (CRD) which is meant to implement a supervisory framework for financial institutionsin the European Union.

The Horizon project consists of several steps. First, huge amounts of historical data for severalrisk drivers have to be collected and processed. Then models will have to be developed for therisk drivers. The Rabobank will then use Monte Carlo simulation to generate future scenariosfor these risk drivers. Using these scenarios the derivative contracts will be valuated, which iswhy the next step is to develop pricing functions for each of the derivative contracts. Withthese pricing functions we will obtain the value of several derivative contracts in all generatedscenarios. The last step in the project is then to process this data into a report based on whichseveral decisions about the counterparty credit risk can be made. During my internship atRabobank I cooperated on the development of models for the risk drivers, specifically on themodel for interest rates. The main purpose of this thesis is to develop an interest rate model

2More information about this kind of transactions can be found in Fabozzi and Mann [9].

1.1. POTENTIAL FUTURE EXPOSURE 3

for counterparty credit risk. This involves answering the following questions:

• How will the interest rate model be used to quantify counterparty credit risk?

• What interest rate products will be priced using this interest rate model?

• What kind of historical interest data do we have? How can we use this data?

• Which models are available for interest rates? What specific requirements do we have foran interest rate model for counterparty credit risk? Why do we choose a certain model?

• What are the characteristics of the chosen interest rate model? How do we simulate interestrates using this model?

• How can we incorporate correlation between interest rates at different maturities, interestrates of different currencies and other risk drivers?

• How do we calibrate the parameters in the chosen model?

• Which assumptions are made in the model? Are these assumptions reasonable using thehistorical data?

• What are the restrictions of the model used?

In this thesis we will try to answer all of these questions. In the rest of this chapter we willdescribe how the interest rate will be used to quantify counterparty credit risk and what measuresare available for this purpose. In section 1.1 the potential future exposure is defined. Thismeasure is used internally to be able to compare the possible future exposure to the limits setfor this exposure. We will describe the process used to quantify counterparty credit risk ingreat detail in this section. Section 1.2 will be used to explain how financial institutions shouldcompute their regulatory capital for counterparty credit risk. This involves a different measure,the exposure at default.

1.1 Potential future exposure

To quantify counterparty credit risk, the exposure per counterparty is calculated. The exposureper counterparty is defined as the maximum of zero and the market value of the portfolio ofderivative positions with this counterparty. This is the amount that would be lost due to defaultof the counterpary in case of zero recovery. Since the value of OTC-derivatives changes overtime due to market factors such as interest rates, only the current exposure can be calculatedwith certainty. The future exposure is uncertain. However large exposures would lead to largelosses in case of default of the counterpary, so a bank will set limits to the amount of exposureover time for every counterparty. One can assess the possible exposure for a certain time t in thefuture by calculating the exposure in several possible future scenarios for time t, where each ofthese scenarios corresponds to a possible set of market conditions. The exposure, computed foreach of these scenarios, will lead to a distribution of the potential exposure for the future time t.Using this distribution the potential future exposure (PFE) at time t is defined as a high, in thiscase 97.5% quantile of the exposure distribution. The PFE at time t is then the exposure thatwill only be exceeded with 2.5% probability. This quantity can be compared to the limits setfor the amount of exposure for a counterparty. Figure 1.1 illustrates the computation of the PFE.

In the Horizon project the Rabobank will implement Monte Carlo simulation to quantify expo-sure. Monte Carlo simulation is time consuming, depending on the number of counterparties,

4 CHAPTER 1. COUNTERPARTY CREDIT RISK

Now Future dateHistory

PFE

Figure 1.1: Illustration of how to compute the PFE.

the number of transactions per counterparty and the number of scenarios generated, but is ableto capture the correlation between transactions and will as a consequence give a more accuratedistribution of the exposure compared to other methods. As described in Gregory [11] there areseveral methods to quantify exposure. The most simple method is an add-on method. Here theexposure is determined as the current exposure plus a component representing the uncertaintyin the exposure for the future. This add-on would ideally be different for every contract, ac-counting for the specifics of the transaction. However, for simplicity some of these specifics willbe ignored which can make the method inaccurate. A more complicated method is defining a(semi-)analytical expression for the exposure. By making assumptions about the market factors,one could approximate the potential future exposure analytically. Although an analytical ex-pression is easy to work with, the assumptions made will have to be over-simplifying to allow theexposure to be approximated analytically. Furthermore, using this method calculations throughtime are independent.

As mentioned above the calculation of the potential future exposure requires us to assess thedistribution of the exposure. Using Monte Carlo simulation we construct this distribution bygenerating a lot of scenarios corresponding to different market circumstances and calculate theexposure for every derivative at several future time points. To value, for example, a forward rateagreement we will have to model interest rates since the value of the forward rate agreementat a future date t depends on the interest rate at this time t. To calculate the potential futureexposure for several other transactions also foreign-exchange rates and credit spreads will bemodeled and simulated. To illustrate the calculation of the potential future exposure assumethat we have one contract with a certain counterparty. The value of this contract at a certaintime point t is given by V (t). The exposure E for this contract at some future time point t1 isthen given by

E(t1) = max(0, V (t1))

However the value of the contract at time t1 is unknown since the value changes due to changes

1.2. EXPOSURE AT DEFAULT 5

in the market. We assume that the value of this product depends on the interest rate. If weare able to model the interest rate we can, by simulating several scenarios of possible future in-terest rates calculate a range of possible future values for the contract V1(t1), . . . , Vn(t1). Usingthis values we can calculate the exposure in every scenario leading to a set of possible futureexposures E1(t1), . . . , En(t1). The potential future exposure is then given by the 97.5% quantileof the empirical distribution of possible exposures. When we assume that there is more thanone contract with a certain counterparty the potential future exposure for this counterparty isgiven by the sum of potential exposures per contract. The parties in a derivative contract canreduce their counterparty credit risk by means of a ISDA3 master agreement. In this agreementthe parties can decide on a netting agreement. In case of a netting agreement the value of allcontracts with this counterparty in a netting set are netted. In this case the exposure of a setof contracts is only the net positive value. An option in the ISDA master agreement is thecredit support annex (CSA). In case of a CSA one or both of the counterparties to a contractare required to pay collateral when the exposure exceeds some pre-specified threshold. Thiscollateral will reduce the exposure below the threshold. More on this approach can be found inZhu and Pykhtin [16].

1.2 Exposure at default

The regulation of banks on an international level started in 1974 following the collapse of theHerstatt Bank in Germany and the Franklin National Bank in the US due to amongst otherthings, bad international supervision. To improve international supervision the Basel Commit-tee on Banking Supervision was created. Their work led to the introduction of the Basel CapitalAccord in 1988, a framework for credit risk measurement. The current regulations are based ona revision of this capital accord, referred to as Basel II. The Basel II supervisory framework isimplemented in Europe through the CRD. The purpose of these regulations is to ensure thatevery bank holds capital reserves appropriate to the risk the bank is exposed to. This shouldstabilize the banking system and guarantee that banks have a sound risk management. The cap-ital reserves based on these regulations are usually referred to as regulatory capital. Recently,the Basel Committee on Banking Supervision has published a number of proposals to reformthe international supervisory framework as a result of the latest/current financial crisis. Oneof these proposals, which can be found in Basel [3] is to strengthen CCR capital requirements,since the financial crisis has shown that the current regulatory capital treatment for CCR is in-sufficient. This proposal may eventually lead to changes or additions to the Basel II framework.Since these changes have not been implemented so far we will in this thesis focus on the currentregulations.

The current regulations for credit risk include four methods for computing counterparty creditrisk, see DNB [7]. These methods are:

• Original exposure method

• Mark-to-market method (current exposure method)

• Standardized method

• Internal model method (IMM)

3ISDA stands for International Swaps and Derivatives Association. This organization has created the masteragreement, which is a standardized contract for derivative transactions.

6 CHAPTER 1. COUNTERPARTY CREDIT RISK

Each of the subsequent methods is more risk sensitive than the previous but also more complex.The basic idea of these methods is to compute the loan equivalent exposure at default (EAD).A financial institution is supposed to choose a method that is appropriate for the nature andsize of their exposures. The original exposure method, which is the least risk sensitive method,may only be applied by institutions that fall under the ”des minimis” regulation. The internalmodel method, which is the most sophisticated method is subject to prior approval of the DutchCentral bank. With the Horizon project the Rabobank aims at implementing this method. Inthe internal model method the exposure at default will be computed using a model that specifiesa forecasting distribution for market variables such as interest rates. The exposure is then com-puted for a contract at a future date using the changes in the market variables. The frameworkdescribed for computing the potential future exposure in the previous section is similar to theframework needed to compute the EAD using the internal model method.

Effective EE

Exposure

Time

Effective EPE

EPE

EE

Figure 1.2: Illustration of the computation of the effective EPE.

Using the internal model method one will have to determine the loan equivalent exposure atdefault for every counterparty. The exposure at default is used to calculate the required capitalreserves. The actual exposure at default is a random exposure. We do not know the exposureat default unless we know when the counterparty will default. To simplify calculations we willuse the loan equivalent exposure at default which involves calculating a fixed exposure, allowingderivative positions to be treated similar to the more simple loans. The most natural choice forthis fixed exposure is the expected positive exposure (EPE). This is a loan equivalent measuresince the expected loss for the counterparty will in this case be equal for both random and fixedexposures. The exposure at default is then given by

EAD = α · Effective EPE

To obtain the EAD, we multiply the effective EPE by a constant factor α, which will amongstothers account for the correlation between exposures and defaults. For the internal modelmethod the value of α is set at a level of 1.4. However, a financial institution can obtain approvalto compute their own estimate for α subject to a floor of 1.2. If we use the models for marketvariables to simulate future scenarios and value the contracts with a certain counterparty in eachof these scenarios we have an exposure distribution. Using this distribution we can estimate theexpected exposure (EE) at any future time t as the average over the exposure in every scenario

1.3. OUTLINE 7

for time t. As a function of time the expected exposure will initially increase but from the pointwhere the maturity is reached the exposure will be equal to zero. It is however likely that thebank will enter new transactions in the future. This will result in roll-over risk, the additionalexposure generated by future financial transactions. To account for the roll-over risk we will usethe effective EE which will be a monotonically increasing function of t since it is defined by

Effective EE(t) = max(EE(t− 1), EE(t))

The average of the effective EE over time is then denoted as the effective expected positiveexposure, needed to compute the exposure at default. Figure 1.2 illustrates how the effectiveEPE is computed.

1.3 Outline

In the introduction we have explained the main purpose of this thesis: the development of aninterest rate model. We aim to answer the questions in this chapter. In this chapter we havealready explained how counterparty credit risk is quantified and why we need an interest ratemodel. We have also described the use of the model: simulating future scenarios for the interestrates. These scenarios will then be used to value derivatives. In chapter 2 we will describe twoof the most important OTC derivatives, the interest rate swap and the forward rate agreement.We will explain how these products are valued. Though the thesis we will use these products toassess the performance of the model.

The next step in the development of an interest rate model is analyzing the available data. Wewant to use this data to calibrate the parameters in the model but also to assess the fit of themodel. In the Horizon project the interest rate model will be used for interest rates for differentcurrencies. In this thesis we will only consider EUR and USD interest rates. We will limit theanalysis of the historical data to the historical interest rates for these two currencies.

Then we will choose one of the many available interest rate models in chapter 4. This chapterwill start by stating the specific requirements for the interest rate model for counterparty creditrisk. Then we will describe and compare several well known models. We will explain the choicefor the final model used and we will describe exactly how this model is defined and how we cansimulate interest rates using this model. We will also consider how correlation between interestrates at different maturities can be incorporated into the model.

After the model is selected, we have to estimate the parameters. In chapter 5 we will firstdescribe how the correlation is estimated. Then we will estimate the other parameters basedon the historical data using several methods. Each of these methods has both advantages anddisadvantages. We will use the interest rate swap and the forward rate agreement to assess theperformance of these methods for parameter estimation. We will choose one of these methods.This method will be used in the rest of the thesis.

The historical data has been used for the estimation of the parameters but can also be used toassess certain assumptions made in the interest rate model. In chapter 6 we will show whetherthe model is suitable for the historical data. We will test the assumption that the residualsin the model are standard normal distributed and that these residuals are independent. Wepropose some practical alternatives and assess the results of these alternatives by consideringthe impact on the potential future exposure for the interest rate swap.

8 CHAPTER 1. COUNTERPARTY CREDIT RISK

Finally, we will conclude this thesis in chapter 7 by summarizing the results of the assessmentof the model and making some general comments on the use of the model.

Chapter 2

Interest rate products

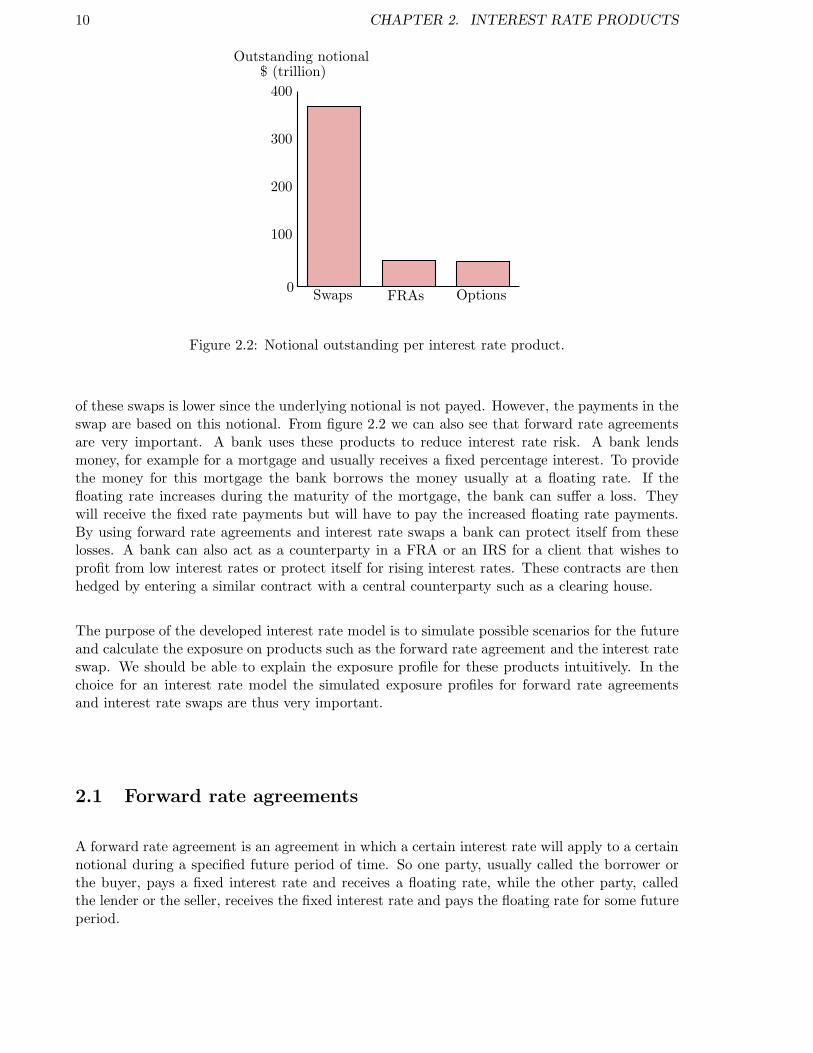

In chapter 1 we have described how counterparty credit risk can be quantified. The scenariosgenerated using the interest rate models will be used to calculate the potential future exposureor the exposure at default for several derivative products depending on interest rates, interestrate derivatives. To be able to assess the model adequately we have to consider the exposure forsome important interest rate products. For this reason we will describe two basic but importantinterest rate products in this chapter. Interest rate products account for the biggest part of thetotal outstanding notional of OTC derivatives as can be seen in figure 2.1. The first productconsidered is the forward rate agreement (FRA). With this agreement an interest rate specifiedin the contract will apply to a specified notional value for a specified future period of time. Thesecond product we consider is the interest rate swap (IRS). In an interest rate swap two partiesagree to swap at specified future dates floating rate payments for fixed rate payments based onan agreed notional. In figure 2.2 we can see that the major part of the outstanding notional ininterest rates products is due to interest rate swaps1. Note however that the total market value

Interest rate

Foreign exchange

CDS

$ (trillion)

0

100

200

300

400

Outstanding notional

500

Commodity

OtherEquity linked

Figure 2.1: Notional outstanding per type of OTC derivative.

1The data for these figures is from BIS [2]

9

10 CHAPTER 2. INTEREST RATE PRODUCTS

Swaps FRAs Options

$ (trillion)

0

100

200

300

400

Outstanding notional

Figure 2.2: Notional outstanding per interest rate product.

of these swaps is lower since the underlying notional is not payed. However, the payments in theswap are based on this notional. From figure 2.2 we can also see that forward rate agreementsare very important. A bank uses these products to reduce interest rate risk. A bank lendsmoney, for example for a mortgage and usually receives a fixed percentage interest. To providethe money for this mortgage the bank borrows the money usually at a floating rate. If thefloating rate increases during the maturity of the mortgage, the bank can suffer a loss. Theywill receive the fixed rate payments but will have to pay the increased floating rate payments.By using forward rate agreements and interest rate swaps a bank can protect itself from theselosses. A bank can also act as a counterparty in a FRA or an IRS for a client that wishes toprofit from low interest rates or protect itself for rising interest rates. These contracts are thenhedged by entering a similar contract with a central counterparty such as a clearing house.

The purpose of the developed interest rate model is to simulate possible scenarios for the futureand calculate the exposure on products such as the forward rate agreement and the interest rateswap. We should be able to explain the exposure profile for these products intuitively. In thechoice for an interest rate model the simulated exposure profiles for forward rate agreementsand interest rate swaps are thus very important.

2.1 Forward rate agreements

A forward rate agreement is an agreement in which a certain interest rate will apply to a certainnotional during a specified future period of time. So one party, usually called the borrower orthe buyer, pays a fixed interest rate and receives a floating rate, while the other party, calledthe lender or the seller, receives the fixed interest rate and pays the floating rate for some futureperiod.

2.2. INTEREST RATE SWAPS 11

We will use the following notation in the definition of the FRA:

N = notional underlying the contractrfix = fixed interest rate agreed on in the contractT0 = starting date of the contractT1 = effective date, which is the first day of the agreed FRA− periodT2 = termination date, which is the last day of the agreed FRA− period

At the termination date of the contract one would receive (or pay) the difference between thefloating rate and the fixed rate for the period T2 − T1 for the notional N . Here we assume thatthe period between the effective date T1 and the termination date T2 is less than a year. Thisperiod is usually 3 or 6 months. The cashflow at time T2 would then be given by

C = N(

er(T1;T1,T2)(T2−T1) − 1− rfix · (T2 − T1))

(2.1)

However we assume2 here that the forward rate agreement is settled at the effective date T1. Atthis point the actual interest rate used for the FRA-period is known. Because of this settlement,the actual cashflow as a result of the contract will be at T1. To obtain this cashflow we discount(2.1) from time T2 to T1. If we pay fixed and receive the floating rate payment the cashflow isequal to

V (T1) = Ce−r(T1;T1,T2)(T2−T1) (2.2)

Furthermore, we assume that the fixed rate in the contract is chosen in such a way that thevalue of the contract is zero at T0: V (T0) = 0. Since the FRA is settled at T1 the value will onlydiffer from zero in the interval [T0, T1]. To determine the value of the FRA at a time point t inthis interval we need an estimate for the interest rate at time T1 with maturity T2 − T1. We usethe forward rate for the period [T1, T2] at t. Furthermore, we have to discount with the interestrate at t with maturity T2 denoted by r(t; t, T2) . The value of a FRA in the interval [T0, T1] isthen given by

V (t) =

0 t = T0

Ce−r(t;T1,T2)(T2−t) t ∈ (T0, T1)

Ce−r(T1;T1,T2)(T2−T1) t = T1

0 t > T1

(2.3)

As mentioned in the introduction the exposure of a single contract is given by maximum ofthe value of the contract and zero. If we want to calculate the potential future exposure fora forward rate agreement, we simulate a huge number of interest rate scenarios and value theforward rate agreement in each of these scenarios through time. The potential future exposureat time t is then given by the 97.5% quantile of the range of values of the forward rate agreementin every interest rate scenario at time t. Because of the settlement at time T1 the exposure canonly be positive in the interval [0, T1].

2.2 Interest rate swaps

An interest rate swap is an interest rate derivative where one party swaps their interest ratepayments with the interest rate payments of the other party. In most cases floating interestrate payments are swapped for fixed interest rate payments or vice versa. In this product thereis a maturity M, a number of fixed rate payments n1 and a number of floating rate paymentsn2. Furthermore the parties have agreed on a fixed interest rate and the notional N where the

2This assumption is common, see page 85 in Hull [12]: Usually FRAs are settled at time T1 rather than T2.

12 CHAPTER 2. INTEREST RATE PRODUCTS

payments are based on. In different currencies the number of payments may differ, for examplefor EUR interest rate swaps it is convention that the fixed rate payments occur every year andthe floating payments every six months. For USD interest rate swaps it is convention that fixedpayments occur every 6 months and floating payments every three months.

There are several ways to value an interest rate swap. One might have seen the analogy betweenan interest rate swap with only one payment and the forward rate agreement described above.An interest rate swap can be seen as a portfolio of forward rate agreements payed in arrears.Another way to valuate an interest rate swap is by regarding the swap as a long position in onebond combined with a short position in another bond. We describe this method to value theinterest rate swap. We assume that the notional is exchanged at the maturity of the contract,which justifies this approach. However, since both parties pay the notional at the maturity ofthe contract, this leads to a payment with a net value of zero. We can define these two bondshere using the following notation:

Bfix = value of a fixed rate bond underlying the swapBfl = value of a floating rate bond underlying the swapN = notional principal underlying the swapti = time until ith payment is exchangedr(t; t, ti) = interest rate corresponding to maturity tirfix = fixed interest rate agreed on in the contractk = fixed payment made on the payment datesk∗ = floating payment made on the payment dates

Note that k is a payment fixed during the contract while k∗ is different for every payment,depending on the floating rate for the payment at hand. The value of the interest rate swapwhen fixed payments are received and floating payments are paid at time t, is given by

V (t) = Bfix(t)−Bfl(t) (2.4)

For an interest rate swap where one pays the fixed leg and receives the floating leg the valueof the interest rate swap is exactly the opposite: V (t) = Bfl(t) − Bfix(t). The value of thefixed-rate bond underlying the swap is given by the sum of the discounted fixed-payments andthe discounted notional:

Bfix(t) =

n1∑

i=1

1{t>ti}ke−r(t;t,ti)ti +Ne−r(t;t,tn)tn (2.5)

where n1 is the total number of fixed-payments. Using the fixed rate one can calculate the fixedpayments k. If there are m1 fixed rate payment per year, k is given by

k = N · rfix ·1

m1(2.6)

The value of the floating-rate bond is equal to a newly issued floating-rate bond after eachpayment. This is explained by an example in appendix C. Right after a payment the floating-ratepayment is known so the value of this floating-rate bond is equal to the discounted floating-ratepayment. The value of the floating-rate bond at a given day t is

Bfl(t) = (N + k∗)e−r(t;t,ti)ti (2.7)

Here i is the first payment after time t such that ti is the time until the next payment andr(t; t, t1) the interest rate corresponding to this maturity. We assume that the floating rate is

2.3. THE HISTORICAL EXPOSURE FOR THE FRA AND THE IRS 13

continuously compounding so, given m2 floating payments per year k∗ is given by

k∗ = N

(

exp

(

rfl ·1

m2

)

− 1

)

(2.8)

Here rfl is the floating rate set at the moment that the previous floating payment is due. Thismeans that at every moment the next floating payment is known. We assume that the fixedrate agreed on in the interest rate swap contract is chosen in such a way that the initial valueof the contract is 0.

By describing the interest rate swap we can already get an idea of the exposure of an interestrate swap. At t = 0 the exposure is zero. From this point the exposure will increase until thefirst payment. With every payment the exposure will decrease since part of the value of thecontract is already payed. At the maturity of the contract the value will have decreased to zeroagain.

2.3 The historical exposure for the FRA and the IRS

Using the historical data we can show the exposure of a forward rate agreement and an interestrate swap through time. This will give an idea of what the exposure can look like. For theforward rate agreement we start the contract at 26-04-2005 and take t = 0 at this date. Thestarting date of the FRA-period will be exactly one year later so T1 = 1. The termination dateof the contract will be 3 months after T1 so we have T2 = 1.25. We assume for simplicity thatN = 1. The fixed rate is chosen in such a way that the value of the contract is zero at the startdate of the contract t = 0. This means that the fixed rate in the contract is given by

rfix =er(0;T1,T2)(T2−T1) − 1

T2 − T1(2.9)

We assume that in this contract the fixed rate is payed and the floating rate is received. Infigure 2.3 we can see the value of this FRA given by the red dashed line. Where the valueof the FRA is positive this is equal to the exposure at that time. The exposure is given bythe blue line. We can see that the exposure is zero at t = 0 and then decreases initially. Fromt = 50 the value of the contract increases. At T1 the exposure drops to zero since the FRA is set-tled at this time. In the interval [T1, T2] the exposure is zero since the contract is already settled.

For the interest rate swap we will start the contract at 20-12-2002. The maturity of this contractwill be 5 years with annual payments for both the fixed and the floating leg. We assume that inthis contract we will pay floating and receive fixed. As in the FRA contract we choose the fixedrate in such a way that the value of the contract is zero at the start date of the contract. Thismeans that we have Bfix = Bfl which results in:

rfix =1− e−r(0;0,tn)tn

1m2

∑n1

i=1 e−r(0;0,ti)ti

(2.10)

From the red dashed line representing the value of the IRS in figure 2.4 we see that the value ofthe IRS is initially increasing. After about 240 days the value of the swaps decreases. The valueis negative from about 500 days after the start of the contract. At the termination date of thecontract the last payment is due which reduces the value of the interest rate swap to zero. The

14 CHAPTER 2. INTEREST RATE PRODUCTS

0 50 100 150 200 250 300−1.5

−1

−0.5

0

0.5

1

1.5

2

2.5

3

3.5x 10

−3

Time (days)

Figure 2.3: The exposure for a FRA starting at 26-04-2005.

0 200 400 600 800 1000 1200−0.03

−0.02

−0.01

0

0.01

0.02

0.03

0.04

0.05

0.06

Time (days)

3rdpayment

2ndpayment

1stpayment 4th

payment

5thpayment

Figure 2.4: The exposure for a IRS starting at 20-12-2002.

2.3. THE HISTORICAL EXPOSURE FOR THE FRA AND THE IRS 15

black vertical lines in this figure indicate the times at which payments are due. Note that asthe contract is maturing the value curve is less spiky. This is caused by the fact that after eachpayment there is one insecure factor removed from the price. The value between the last twopayments is almost constant. This is because right after the fourth payment is due the floatingrate for the last payment is known, reducing the insecurity in the pricing. In future chapterswe will use the exposure profiles of forward rate agreements and interest rate swaps to assess,for example, the estimates for the parameters in the process. The exposure for this interest rateswap is given by the blue line.

16 CHAPTER 2. INTEREST RATE PRODUCTS

Chapter 3

Data analysis

In the calibration and testing of the model historical interest rate data will be used. It isimportant to analyze this data first to get an idea of the data that is available and how it canbe used in the derivation of the model. The interest rate model should also be suitable for thehistorical data. Since in this thesis we will only look at the model for Euro and United Statesdollar interest rates, we require historical interest rates for both of these currencies. The dataarchive used by Rabobank contains daily interest rate data for these currencies from 22-01-2001until 01-12-2009, which is about 9 years of data. Interest rates are not the same for everymaturity. Generally the interest rate for a maturity of 30 years will be higher than the interestrate for a maturity of 1 month. To capture this relation between maturity and interest ratethrough time, the dataset contains information for 9 maturities. These maturities are calledtenor points and will be denoted by τ . The available tenor points for the interest rates are 1month, 3 months, 6 months, 1 year, 2 years, 5 years, 10 years, 20 years and 30 years. For thetenor points corresponding to a maturity less than or equal to 1 year the rates are given bythe interbank rate for this maturity. For tenor points corresponding to maturities longer than1 year the data corresponds to the swap rate for this maturity. The dataset consists of 2313data points for each of the nine maturities. In this thesis we assume that a year is 250 businessdays, excluding weekends and holidays. Since there was a change in the type of interest ratedata recorded after day 2038 in the dataset, resulting in a large jump from day 2038 to 2039 wehave shifted the data to remove these large jumps.

3.1 Interest rate data

In this section we will analyze the dataset in order to detect outliers or specific periods in theinterest rate data. These interest rates are continuous compounding rates. For all tenor pointsthe interest rates vary between 0.1% and 7.6%. For most of the history given, the interestrates corresponding to longer maturities such as 20 or 30 year are higher than the interest ratescorresponding to shorter maturities like 1 or 3 months. There is however a period in whichall interest rates are rather high with only small differences between the interest rates for dif-ferent tenor points. This period is followed by relatively low interest rates especially for theshort maturities. For the EUR interest rates this period corresponds to late 2007 to early 2009.For the USD interest rate this period is slightly earlier, starting in 2006 continuing through2007. These periods are due to the recent financial crisis, which started in 2006 in the UnitedStates and around 2007 in Europe. Figure 3.1 shows the 6 months and 20 years tenor pointsfor the EUR interest rates. In figure 3.2 one can see these tenorpoints for the USD interest rates.

Another notable aspect of the dataset is the stepwise change in several of the short maturity

17

18 CHAPTER 3. DATA ANALYSIS

0 500 1000 1500 20000

0.01

0.02

0.03

0.04

0.05

0.06

0.07

Time (days)

6m IR

20y IR

Figure 3.1: The 6 months and 20 years tenor points for the EUR interest rate data.

0 500 1000 1500 20000

0.01

0.02

0.03

0.04

0.05

0.06

0.07

Time (days)

6m IR

20y IR

Figure 3.2: The 6 months and 20 years tenor points for the USD interest rate data.

interest rates. This stepwise behavior is most obvious in the 1 month EUR interest rate, whichcan be seen in figure 3.3. The stepwise behavior of this interest rate is caused by the sensitivityof these short maturity interest rates to the policy of the central banks.

3.2 Forward rates

Forward rates are rates of interest implied by the current interest rates for a period of timein the future. For the pricing of interest rate products not only interest rates are used butalso forward rates. For example, in a forward rate agreement where we pay fixed and receivefloating rate for a period of 3 months starting 9 months from now the forward rate from 9 to12 months is chosen for the fixed rate to guarantee that the value of the contract is zero at thecontract date. Since the forward rate at time t is actually the interest rate for a future period oftime [T1, T2] we will denote the T1, T2-forward rate by r(t;T1, T2). This implies that the inter-

3.2. FORWARD RATES 19

0 500 1000 1500 20000

0.01

0.02

0.03

0.04

0.05

0.06

0.07

Time (days)

Figure 3.3: The stepwise behavior of the 1 month EUR interest rate.

0 500 1000 1500 20000

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.04

0.045

Time (days)

Figure 3.4: The 6 months to 1 year forward rate, calculated from the interest rate data.

est rate at time t for a maturity T will be denoted by r(t; t, T ). All times will be denoted in years.

If we consider the current interest rates for a maturity T1 and T2 where T2 > T1, the T1, T2-forward rate will be defined in such a way that there is no arbitrage possible. If 1 euro would beinvested at this moment for T2 years one would receive exp(r(0; 0, T2) · T2) after T2 years. Thisamount should be equal to the amount received when we first invest 1 euro for T1 years andthen reinvest for the period [T1, T2] for the current forward rate in this period: exp(r(0; 0, T1) ·T1) exp(r(0;T1, T2) · (T2 − T1)). If we solve this we find that the forward rate at time 0 for theperiod [T1, T2] is given by1

r(0;T1, T2) =r(0; 0, T2) · T2 − r(0; 0, T1) · T1

T2 − T1(3.1)

Using the relation given above we can compute the forward rates from the interest rate data.Figure 3.4 shows the 6 months to 1 year EUR forward rate through time. At every time point t

1This definition of the forward rate is also used in Hull [12].

20 CHAPTER 3. DATA ANALYSIS

0 5 10 15 20 25 300

0.01

0.02

0.03

0.04

0.05

0.06

Maturity (years)

Figure 3.5: Fitted yield curve at 3-12-2008 (black solid) and 2-12-2009 (green dashed).

this is the forward rate for the period 6 months to 1 year from t, implied in the interest rates attime t. We see in this figure that the behavior of the forward rate through time is very similarto the behavior of the interest rates.

3.3 Yield curve

The yield curve is the curve that represents the relation between the interest rate and the cor-responding maturity. Since the dataset used here consists of interest rates for several maturitieswe can construct the yield curve. The yield curve is most often2 upward sloping but in cases ofuncertainty or decline in the economy and in cases of deflation the shape of the yield curve canbe flat or negatively sloped. The upward sloping yield curve can be explained by the liquidity

preference theory. This is a theory from economics in which one assumes that the long-terminterest rates include a premium for the added risk of having the money fixed for a longer periodof time. This results in higher interest rates for long-term maturities.

Another theory motivating the shape of the yield curve is the market expectations hypothesis.With this hypothesis one assumes that the shape of the yield curve represents the expectationof the market participants for the future interest rates. Here an upward sloping yield curveis explained by the expectation that interest rates will rise in the future. If we for exampleassume that T1 and T2 are two maturities with T1 < T2 then the current forward rate from T1 toT2 implied in the yield curve is equal to the expected interest rate for the maturity T2−T1 at T1.

In figure 3.5 one can see the yield curve for two dates in the dataset for EUR interest rates.The black dots indicate the interest rates observed at 3-12-2008. The black line is a line fittedthrough these observations using cubic splines. This line is humped and does not have thetypical upward sloping shape. This could be explained by the uncertainty in the economy atthis time. The green dots indicate the interest rates observed at the last observation in the dataset, 2-12-2009. The green line is fitted through these dots using cubic splines. Here we see thetypical shape of the yield curve, although the 30 years tenor point is slightly lower than the 20years tenor point.

2See section 4.10 Theories of the term structure of interest rates in Hull [12].

Chapter 4

Interest rate models

As described earlier we need a model for the interest rates to be able to simulate interest ratescenarios for the future and determine the exposure profiles for products depending on theinterest rates. Using this profiles we will be able to calculate the potential future exposure for acounterparty. In the previous chapters we have described several of these interest rate productsand analyzed the historical data that will be used in the parameter estimation. In this chapterwe will describe the selection of the interest rate model and motivate the choice for the modelthat we will focus on in this thesis. The Horizon project and also the research on suitableinterest rate models started before my internship at Rabobank. A description of the research isincluded to give the reader a complete overview of the process and motivation for this model.We will conclude this chapter with a detailed description of the chosen interest rate model.

4.1 Requirements for the interest rate model

Modeling interest rates is very complex. To know exactly what the interest rates will be in thefuture one should know all factors that influence the interest rate and be able to estimate thesefactors. Since this is seen as an impossible job several stochastic models have been developedfor the interest rates. A large number of these models are described in Brigo and Mercurio[4]. Each of these models has both advantages and disadvantages. To choose between differentmodels we will have to keep the purpose of the model in mind. In this section we will list severalrequirements for the interest rate model.

• The model is required to simulate sensible interest rates. We require that both the interestrates and the forward rates are positive. Furthermore, the model must be suitable for thesimulation of interest rates for different currencies. To limit the extent of this thesis wewill only consider the two most important currencies for Rabobank, the Euro (EUR) andthe United States dollar (USD). Forward rates should be positive since these rates are usedin a interest rates swap or forward rate agreement as estimate for future interest rates.

• The model is required to be implementable without complex numerical approximation.Most of the models in Brigo and Mercurio [4] are described by a stochastic differentialequation. If this stochastic differential equation cannot be solved analytically we will haveto use numerical approximation techniques. However, with this numerical approximationwe will make a small error every step. For this reason it is preferable that the stochasticdifferential equation defining the model is analytically solvable. This allows us to simulatescenarios fast and efficient. The resulting (long term) behavior of the interest rates willbe transparent.

21

22 CHAPTER 4. INTEREST RATE MODELS

• The parameters in the model are required to be calibrated with the historical data available.These parameters should be reasonable and stable with respect to small changes in thedata.

• The model should allow for the definition of a clear correlation structure between interestrates at different maturities, interest rates in different currencies and other risk drivers.

• The model must generate reasonable exposure profiles for the derivatives (for example theinterest rate swap and the forward rate agreement).

• The model should be able to simulate interest rates using time steps of varying sizes.This is because the exposure exists for the maturity of a contract, which can be up to 30years. We would therefore want to compute the potential future exposure daily for thenext month but also in 10 years. It would however be very time consuming to simulateten years ahead using daily steps.

• The model should be used and accepted in the industry.

4.2 Potential models for the interest rate

In chapter 1 we have described the purpose of the interest rate model. We will use simulatedinterest rates to calculate prices for amongst others the interest rate swap through time. Tocalculate these prices while the contract is maturing, we will need simulated interest rates atevery maturity. For example, to value an interest rate swap we need to discount all fixed ratepayments using interest rates corresponding to the time to the payments. The simulation ofinterest rates at different maturities can be done in various ways. Firstly, we could simulatethe interest rates at several industry standard maturities. These standard maturities are, forexample the maturities in the historical dataset. A second option is to simulate the yield curveor properties of this yield curve through time. Although modeling the entire yield curve throughtime would give us the opportunity to calculate the interest rate at every maturity, we only havehistorical interest rate data available at 9 industry standard tenor points. The interest rateswill be modeled at these tenor points. Furthermore, it is chosen that one model will be used forall tenor points and all currencies. Per tenor point the parameters in the model will be calibrated.

The simplest models tested are Brownian motion models. Here we use the term Brownianmotion models for a group of models based on Brownian motion. The models in this group aredefined by the following general stochastic differential equation:

dr(t) = (b+ ar(t))dt+ σdW (t) + ξdJ(λ) (4.1)

Here b, a and σ > 0 are constants, W (t) is the Wiener process, ξ is a jump either random orconstant and J(λ) is a Poisson process with parameter λ. The Wiener process, the Poissonprocess and the jump ξ are assumed to be independent. The models in this group are:

• Simple Brownian motion (a = 0, b = 0, ξ = 0)

• Brownian motion with drift (a = 0, b 6= 0, ξ = 0)

• Brownian motion with mean reversion (a 6= 0, b 6= 0, ξ = 0) also known as the Vasicekmodel

• Brownian motion with mean reversion and jumps (a 6= 0, b 6= 0, ξ 6= 0), see Das [6]

4.2. POTENTIAL MODELS FOR THE INTEREST RATE 23

The main disadvantage of these models is the possibility to generate negative interest rates.Furthermore, the estimation of the parameters in the Brownian motion with mean reversionand jumps is very complicated. For these reasons all of these models are considered unsuitable.

The next group of models researched are geometric Brownian motion (GBM) models. Thesemodels are in a way the exponential versions of the Brownian motion models above. Themodels have the advantage that the simulated interest rates are always positive. The geometricBrownian motion models are:

• Simple geometric Brownian motion defined by dr(t) = σr(t)dW (t)

• Geometric Brownian motion with drift defined by dr(t) = µr(t)dt+ σr(t)dW (t)

• Geometric Brownian motion with mean reversion given by d ln(r(t)) = k (θ − ln(r(t))) dt+σdW (t)1

• Geometric Brownian motion with mean reversion and jumps given by d ln(r(t)) =k (θ − ln(r(t))) dt+ σdW (t) + ξdJ(λ)

In the stochastic differential equations above σ > 0, µ, k > 0, θ and λ are assumed to beconstant. W (t) is the Wiener process, ξ is a random or constant jump and J(λ) is a Poissonprocess. Again the Wiener process, the Poisson process and the jump ξ are assumed to be inde-pendent. Again the option with jumps was considered too complex because there is no analyticalsolution to the differential equation and the estimation of the parameters is very complicated.Furthermore using this option, determining a correlation structure is too complicated or notfeasible since we have to deal with two random processes. The other models in this group arerejected since it is possible to generate interest rates that will lead to negative forward rates.When pricing an interest rate swap or a forward rate agreement we will use these forward rates.Negative forward rates are considered unrealistic. Furthermore, the simple GBM model and theGBM model with drift are unbounded if t increases. This will lead to a very wide distributionin 10 to 30 years. Interest rates simulated using these models can be as high as 50% which isvery unrealistic with respect to the historically observed rates.

Another researched model is the Cox-Ingersoll-Ross or CIR model. The interest rates in thismodel are given by

dr(t) = a(b− r(t))dt+ σ√

r(t)dW (t) (4.2)

Here a,b and σ are considered constant and W (t) is the Wiener process. This model is how-ever not analytically solvable and therefore rejected. The Variance-Gamma process was alsoconsidered. Here interest rates satisfy the following equation:

r(t) = B(G(t);µ, σ) (4.3)

where G(t) is a Gamma process. Here B(t;µ, σ) is the Brownian motion process with drift givenby the stochastic differential equation:

dB(t) = µdt+ σdW (t) (4.4)

where µ and σ are constant and W (t) is again the Wiener process. In this model interest ratesare modeled as Brownian motion where the time follows a Gamma process. More on this modelcan be found in Madan et al. [13]. Estimating parameters for this model is very complicated.

1This model is known as the Black-Karasinski model as described on page 73 of Brigo and Mercurio [4].

24 CHAPTER 4. INTEREST RATE MODELS

Furthermore, determining a correlation structure was considered difficult or infeasible.

The last model researched is the principal components model. For a description of the modelwe follow Reimers and Zerbs [14]. The idea behind this model is that we see the interest ratesas linear combination of several principal components. Principal component analysis involvescomputing the eigenvalue decomposition of the covariance matrix of the historical data. Ap-plying principal components analysis to the historical dataset of log interest rates will give usthese independent principal components x1, . . . , x9. The first of these components will accountfor as much of the variability in the data as possible. Each of the other components will accountas much as possible for the remaining variability in the data. In the example in the article ofReimers and Zerbs three principal components account for almost all variability in the data. Inthis model the interest rates are constructed as follows:

ln (r(t)) = ln (r∞) +k∑

i=1

bixi(t) (4.5)

Here r∞ is the long term mean for the interest rates, bi are coefficients corresponding to theith principal component and xi is the ith principal component. Simulation of interest ratesaccording to this model involves simulating the principal components. These are modeled as amean reverting process with long term mean zero:

dxi(t) = −axi(t)dt+ σdW (t) (4.6)

Here a and σ > 0 are considered constant. The difference between this model and the modelsabove is that interest rates for different tenor points are here considered as a linear combinationof the same components. In the other models the interest rate at every tenor point is consideredseparately. Furthermore, if a major part of the variance can be explained by only three princi-pal components, the simulation would be more efficient. One would only have to simulate thesethree components. Also in this model it can not be guaranteed that the forward rates computedfrom the simulated interest rates are positive. Furthermore, the components in this model donot really have an intuitive meaning.

From this research we can conclude that modeling the interest rates was not satisfactory. Severalmodels were omitted because of difficulties in simulation or parameter estimation. Other modelswere unrealistic since there was a significant possibility that the generated interest rates arenegative. The geometric Brownian motion with mean reversion and the principal componentsmodel are considered the best options if we do not take into account the problem of simulatingnegative forward rates.

4.3 Modeling forward rates

Most of the research was focussed on the modeling of interest rates. However, for all the modelsconsidered, there is a possibility for negative forward rates. By the definition of the forwardrates in equation (3.1) we can derive when the forward rate will be positive:

r(0; 0, T2) >T1

T2r(0; 0, T1) (4.7)

However, none of the models described above will always satisfy this constraint. Motivated bythis drawback and inspired by amongst others the model for the interest rate curve known asthe Heath-Jarrow-Morton framework it was decided to model the forward rates instead of the

4.4. GEOMETRIC BROWNIAN MOTION WITH MEAN REVERSION 25

interest rates. In chapter 3 we have seen how the historical forward rates evolved through time.This data shows similar figures compared to plotting historical interest rate data. Althoughpositive interest rates cannot guarantee positive forward rates, we will have positive interestrates if the forward rates are positive. Because of the relation between interest rate and forwardrates we will be able to construct interest rates from the simulated forward rates.

In chapter 3 on data analysis we have already explained how one can derive forward rates fromthe interest rates in the historical dataset. We can describe this more generally; given theinterest rates r(0; 0, τi) and r(0; 0, τi+1) with maturities τi and τi+1 respectively, the forwardrate r(0; τi, τi+1) is given by

r(0; τi, τi+1) =τi+1 · r(0; 0, τi+1)− τi · r(0; 0, τi)

τi+1 − τi(4.8)

where τi is in the set of tenor points. From this definition for the forward rates we can, giventhe forward rate and the interest rate at the preceding tenor point, derive the interest rate:

r(0; 0, τi+1) =τiτi+1

r(0; 0, τi) +τi+1 − τiτi+1

r(0; τi, τi+1) (4.9)

Remember that we also define the forward rate from time zero to the first tenor point. This isactually equivalent to modeling the interest rate at the first tenor point. Since we simulate allforward rates of which the first is actually the interest rate we can recursively reconstruct allinterest rates. This leads to the following expression for the interest rate for the nth tenor pointin terms of forward rates:

r(0; 0, τn) =τ1τn

r(0; 0, τ1) +n−1∑

i=1

τi+1 − τiτn

r(0; τi, τi+1) (4.10)

Since we have shown that it is possible to calculate forward rates from interest rate and toreconstruct interest rates from forward rates, we will from now on focus on modeling the forwardrates. We will develop a model that simulates the forward rates between two successive interestrates. From the research described above we can conclude that using the requirements in section4.1 two models were found suitable; the geometric Brownian motion with mean reversion modeland the principal components approach. If we use these models for the forward rates we cansimulate positive forward rates and thus positive interest rates. The stochastic differentialequation defining geometric Brownian motion with mean reversion is analytically solvable, whichmakes it easy to implement and allows us to vary the size of the time step during the simulations.In the principal components approach we can also analytically solve the equation defining thecomponents. However, geometric Brownian motion with mean reversion is a more commonlyused2 and a more transparent model. For these reasons it was decided that the forward rateswill be modeled by geometric Brownian motion with mean reversion.

4.4 Geometric Brownian motion with mean reversion

In this section we will describe the geometric Brownian motion by a stochastic differentialequation and we will derive several properties of the process. To be able to simulate forwardrates using geometric Brownian motion with mean reversion we propose a discretization of the

2Quoted from page 74 in Brigo and Mercurio [4]: (..) the rather good fitting quality of the model to marketdata (..) has made the model quite popular among practitioners and financial engineers.

26 CHAPTER 4. INTEREST RATE MODELS

stochastic differential equation. In the next chapter we will describe several methods for param-eter estimation, both based on historical data as on expectations for the future.

As explained in the section 4.3 we decided to model the forwards instead of the interest rates.From this point on we will only work with the forward rates. Using the relation between theforward rates and interest rates in section 4.3 it is always possible to calculate interest ratesfrom these forward rates. We define geometric Brownian motion with mean reversion for theforward rates by the following stochastic differential equation:

d ln(r(t; t+ τi, t+ τi+1)) = k(θ − ln(r(t; t+ τi, t+ τi+1)))dt+ σdW (t) (4.11)

r(0; τi, τi+1) = r0 (4.12)

with k > 0, θ and σ > 0 constant. From this point on we assume that time t is always measuredin years. If we would replace ln(r(t; t+ τi, t+ τi+1)), the logarithm of the forward rates, by X(t)we would get the following stochastic differential equation for the logarithm of the forward rates:

dX(t) = k(θ −X(t))dt + σdW (t) (4.13)

This can easily be recognized as an Ornstein-Uhlenbeck process or simply Brownian motionwith mean reversion. We can see that simulating forward rates following a geometric Brownianmotion with mean reversion process is actually similar to simulating the log forward rates fol-lowing Brownian motion with mean reversion. Since Brownian motion with mean reversion isless complicated we will work here with the logarithms of the forward rates.

The Brownian motion with mean reversion process is given by the differential equation (4.13)subject to some initial condition X(0). Here θ is usually noted as the mean reversion level. Thisis the level to which the process converges through time. The parameter k is usually referred toas the mean reversion speed. This parameter indicates how fast the process is being pulled tothe long term mean. The process will be mean reverting if k > 0. This differential equation hasan explicit solution given by:

X(t) = X(0)e−kt + θ(1− e−kt) + σ

∫ t

0e−k(t−s)dW (s) (4.14)

From this solution and the fact that W (t) − W (s) ∼ N(0,√

(t − s)) it follows that X(t) is aGaussian process with mean

E [X(t)] = X(0)e−kt + θ(1− e−kt) (4.15)

and covariance

Cov (X(s),X(t)) = σ2 e−k(s+t)

2k

(

e2kmin(s,t) − 1)

(4.16)