an exploratory study investigating the mitigation of individual investors’ belief revisions and...

TRANSCRIPT

An Exploratory Study Investigating the

Mitigation of Individual Investors’ Belief Revisions

and Order Effects

Robert Pinsker Ph.D., CPA

September 9, 2005

Special Thanks to…

Doug Ziegenfuss

Ronny Daigle (LSU)

David Hayes (LSU)

MotivationSequential belief revisions in the financial reporting context have resulted in less-than-optimal decisions made by investors (i.e., order effects; Tuttle et al. 1997) and unintended stock price volatility for the investee firm (Pinsker 2004) Hogarth and Einhorn’s (HE; 1992) belief-adjustment (BA) model has been used as the theoretical framework to extensively study belief revision and order effects in both the psychology and accounting domains

Motivation (Cont.)Existing BA model research has almost exclusively focused on investigating belief revisions made by accountants (tax and audit) The reason may be due to the ability to instruct (through superiors) and regulate (through accounting regulators) in such a way as to “control” the observed biases (e.g., using a peer review process, working in groups, or requiring documentation)Fails to address the order effects found in the individual investor literature even though these investors use accounting information to make important decisions in a capital market setting.

Purpose

One limitation is that the focus has been on finding order effects, rather than finding ways to mitigate themPurposes: to identify and test realistic methods that would mitigate belief revisions and order effects in a financial reporting context (BA model sensitive to context)

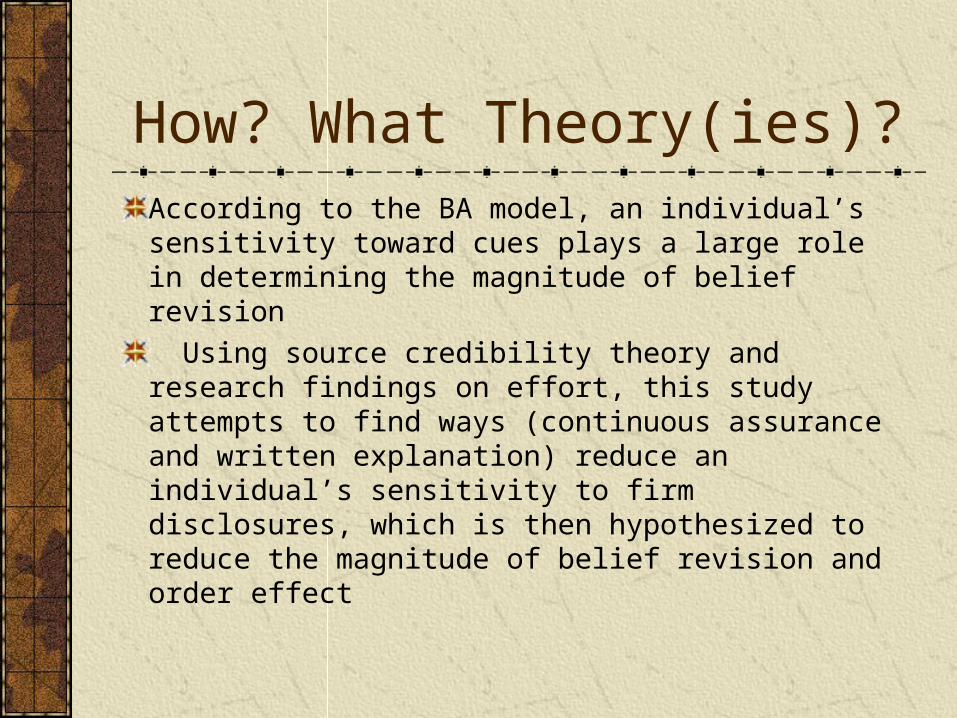

How? What Theory(ies)?

According to the BA model, an individual’s sensitivity toward cues plays a large role in determining the magnitude of belief revision

Using source credibility theory and research findings on effort, this study attempts to find ways (continuous assurance and written explanation) reduce an individual’s sensitivity to firm disclosures, which is then hypothesized to reduce the magnitude of belief revision and order effect

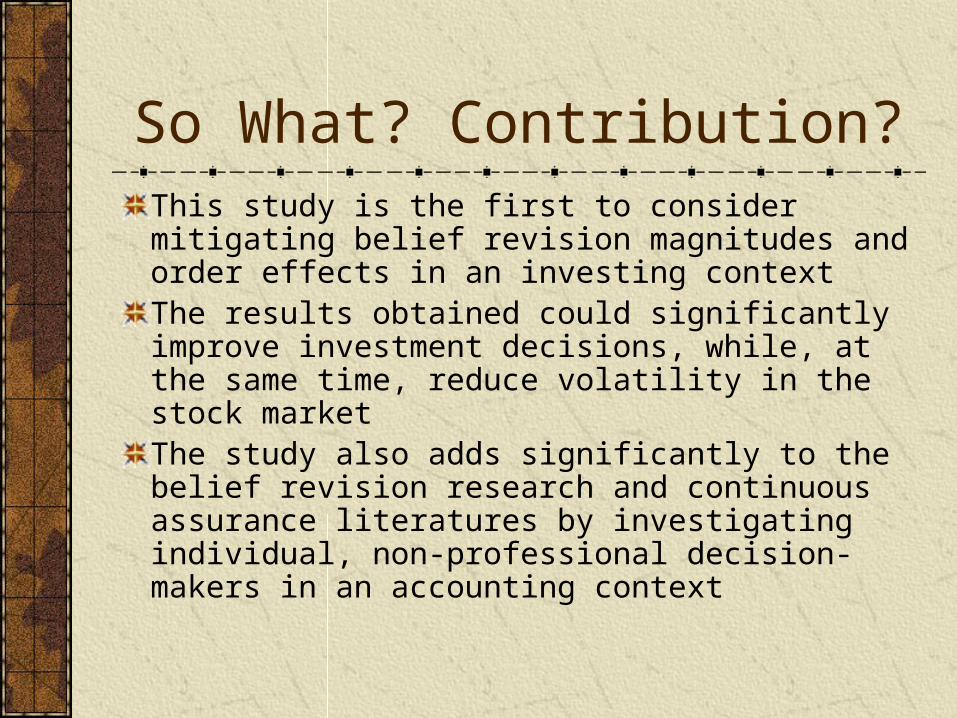

So What? Contribution?This study is the first to consider mitigating belief revision magnitudes and order effects in an investing contextThe results obtained could significantly improve investment decisions, while, at the same time, reduce volatility in the stock marketThe study also adds significantly to the belief revision research and continuous assurance literatures by investigating individual, non-professional decision-makers in an accounting context

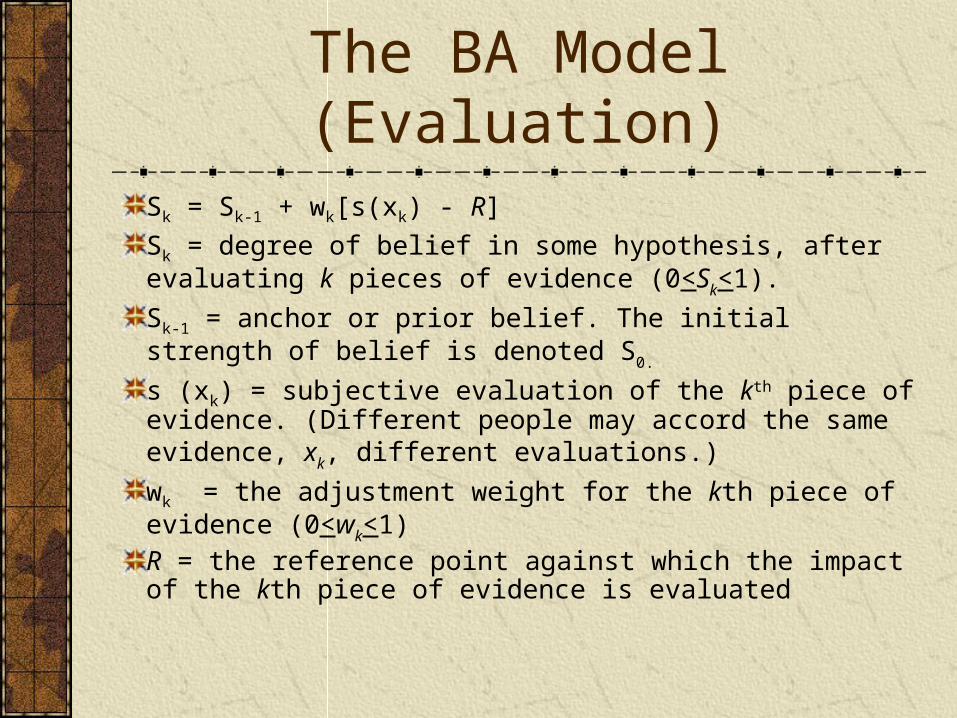

The BA Model (Evaluation)Sk = Sk-1 + wk[s(xk) - R]

Sk = degree of belief in some hypothesis, after evaluating k pieces of evidence (0<Sk<1).

Sk-1 = anchor or prior belief. The initial strength of belief is denoted S0.

s (xk) = subjective evaluation of the kth piece of evidence. (Different people may accord the same evidence, xk, different evaluations.)

wk = the adjustment weight for the kth piece of evidence (0<wk<1)R = the reference point against which the impact of the kth piece of evidence is evaluated

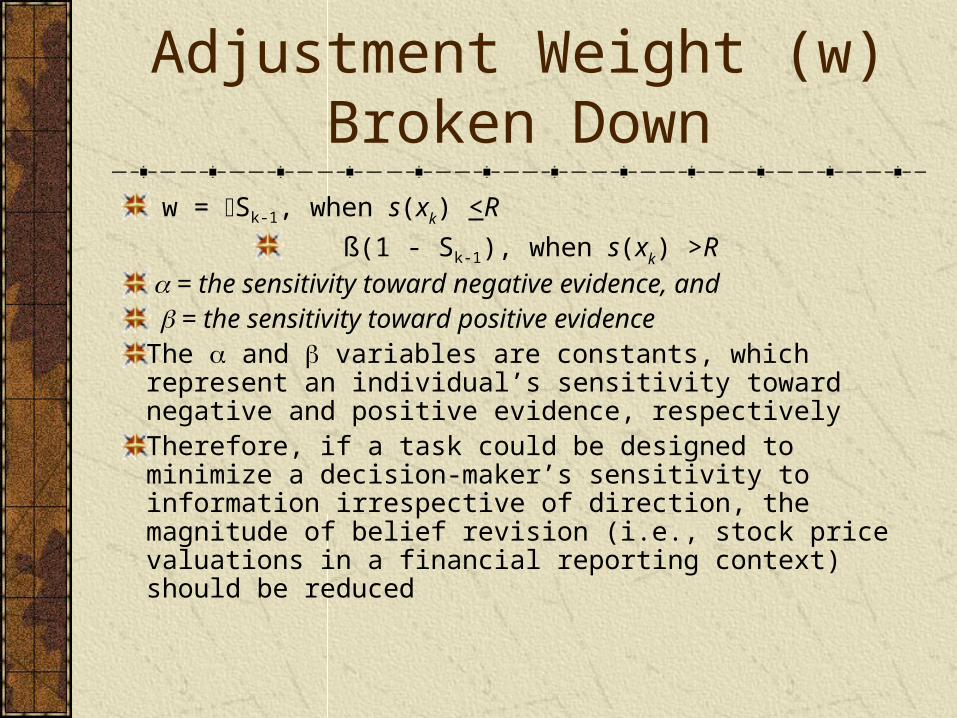

Adjustment Weight (w) Broken Down

w = Sk-1, when s(xk) <R

ß(1 - Sk-1), when s(xk) >R = the sensitivity toward negative evidence, and = the sensitivity toward positive evidenceThe and variables are constants, which represent an individual’s sensitivity toward negative and positive evidence, respectivelyTherefore, if a task could be designed to minimize a decision-maker’s sensitivity to information irrespective of direction, the magnitude of belief revision (i.e., stock price valuations in a financial reporting context) should be reduced

Source Credibility Theory

When investors receive incomplete information, their ability to derive proper firm valuation is hampered since incomplete information increases investor uncertainty (Masters 1989; Miller 2002)

A major reason audits are seen as valuable and credible in the equity marketplace is due to their ability to lower uncertainty in management information, which also reduces the information asymmetry between management and investors

Source Credibility Cont.Business reporting models have changed to a more continuous nature in an attempt to disclose relevant information in a more timely fashion to investors As a result, the annual audit does not represent a source of timely information to the equity marketplaceResearch is currently being conducted in the growing area of continuous assurance (e.g., Kogan et al. 1999; Vasarheyli 2002; Vasarheyli et al. 2004).

Source Credibility FinalA recent study indicated that independent CPA assurance provided on every firm disclosure is relied upon by non-professional investors and also reduces the variation in their stock price valuations when compared to the same disclosures without the assurance (Hunton et al. 2003). If the participants receiving assurance believed the disclosures were more credible due to the existence of CPA assurance, then they were more confident in and less sensitive to the disclosures than the assurance-absent participants

Order EffectsThe linkage between order effects and assurance is unexplored Most research has found recency effectsIf reduced sensitivity, investors should not “need” to resort to recency bias (mitig.)However, psych research indicates individuals more sensitive toward negative cues than positive cues (Kahneman & Tversky 1974), irrespective of order (could be less sensitive, but by differing magnitudes (for + vs. – cues))

Written Explanation“Explanation effect” - the generation of an explanation for the occurrence of an event that increases the judged likelihood of the event (Anderson and Wright 1988)Koonce (1992) reasoned that explanations increase the extent of causal reasoning employed by auditors relative to situations in which written explanations are not requiredAnderson (1983) indicated that if participants imagined themselves performing a target behavior, there was a corresponding change in their behavioral intentions

Explanation Cont.Anderson et al. (1980) found evidence that individuals who develop written explanations are more likely to maintain their existing beliefs even if subsequent information challenges their beliefs than are individuals who have not provided written explanationsGiven the above evidence, it can be reasoned that participants required to provide a written explanation for a task are more attentive to the task (in terms of beliefs) and as a result, expend more effort (e.g., in Koonce 1992)Additionally, since explanation influences processing at the encoding stage (Anderson and Wright 1988), it should have an effect on an individual’s sensitivity, according to the BA model

Explanation Final

In terms of order effects, previous accounting research has taken the perspective that greater participant effort will result in mitigated order effects (Kahle et al. 2005)

How? Experience? Anderson & Wright (1988) found undergrads had recency, but not experienced accountants when using explanation )and counterexplanation). Koonce (1992) found recency mitigated in both (similar to my design)

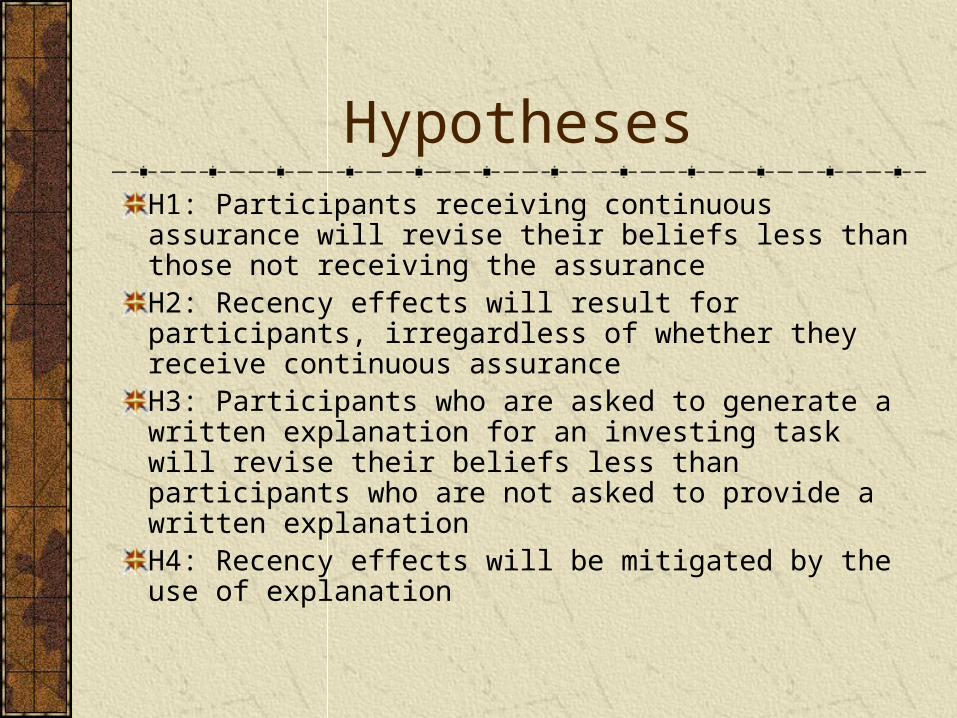

HypothesesH1: Participants receiving continuous assurance will revise their beliefs less than those not receiving the assurance H2: Recency effects will result for participants, irregardless of whether they receive continuous assurance H3: Participants who are asked to generate a written explanation for an investing task will revise their beliefs less than participants who are not asked to provide a written explanation H4: Recency effects will be mitigated by the use of explanation

MethodologyThe experiments consisted of a 3 (mitigation technique: assurance, explanation, and control) by 2 (direction: four positive cues followed by four negative cues or vice versa) between-subjects design Two series of experiments were runThe first experiment used upper-division, undergraduate accounting students and the second experiment involved MBA students completing a financial accounting course

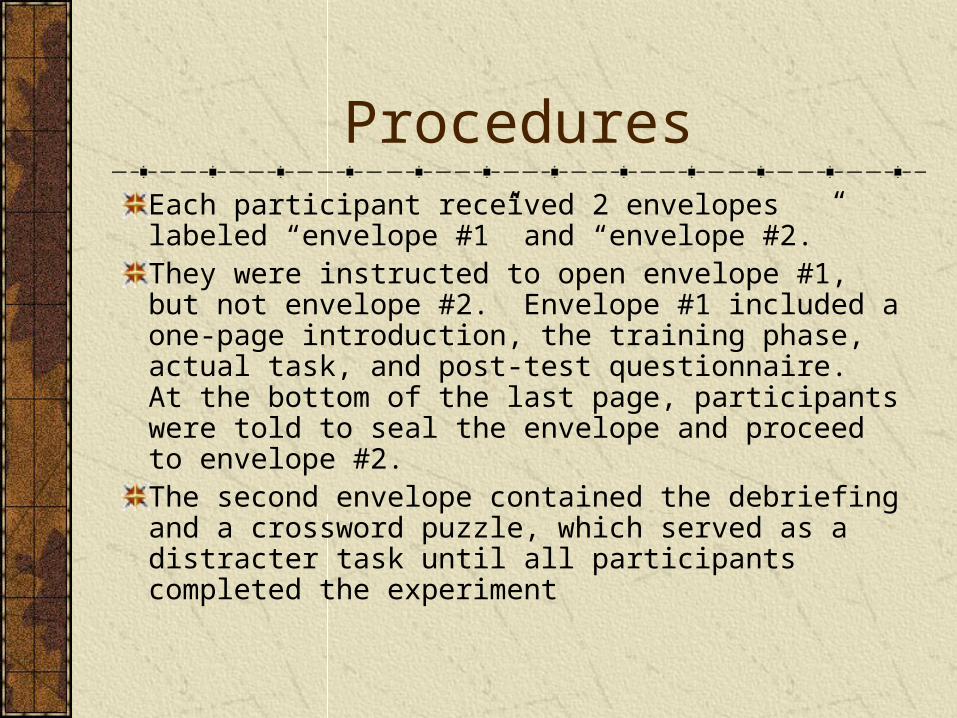

ProceduresEach participant received 2 envelopes labeled “envelope #1” and “envelope #2.” They were instructed to open envelope #1, but not envelope #2. Envelope #1 included a one-page introduction, the training phase, actual task, and post-test questionnaire. At the bottom of the last page, participants were told to seal the envelope and proceed to envelope #2. The second envelope contained the debriefing and a crossword puzzle, which served as a distracter task until all participants completed the experiment

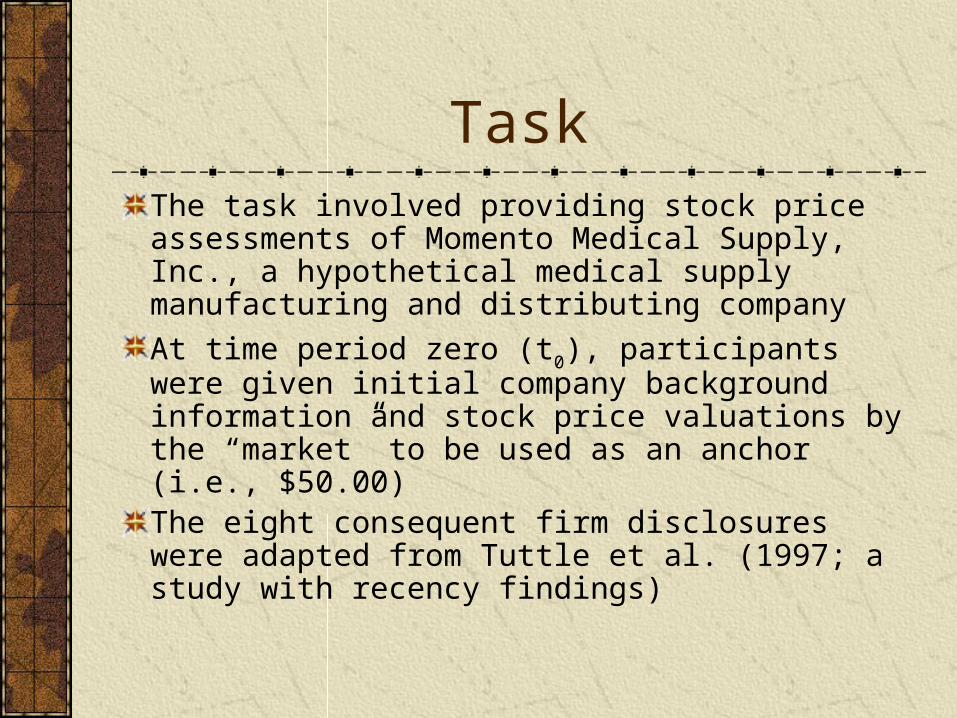

TaskThe task involved providing stock price assessments of Momento Medical Supply, Inc., a hypothetical medical supply manufacturing and distributing company

At time period zero (t0), participants were given initial company background information and stock price valuations by the “market” to be used as an anchor (i.e., $50.00) The eight consequent firm disclosures were adapted from Tuttle et al. (1997; a study with recency findings)

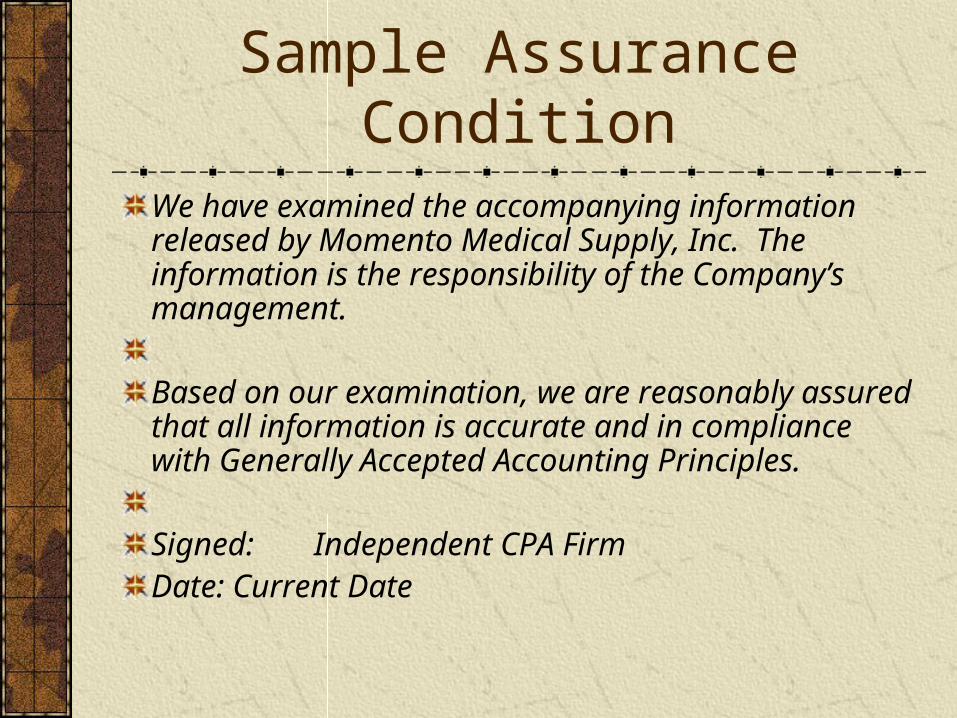

Sample Assurance ConditionWe have examined the accompanying information released by Momento Medical Supply, Inc. The information is the responsibility of the Company’s management. Based on our examination, we are reasonably assured that all information is accurate and in compliance with Generally Accepted Accounting Principles. Signed: Independent CPA FirmDate: Current Date

Sample Explanation Condition

Having read disclosure #1, please write down 1 reason why you would want to buy stock in Momento.

Reason:

Sample Control Condition

The management team here at Momento wants to wish you a very nice day. Please keep our company in mind for all of your medical and pharmaceutical needs.

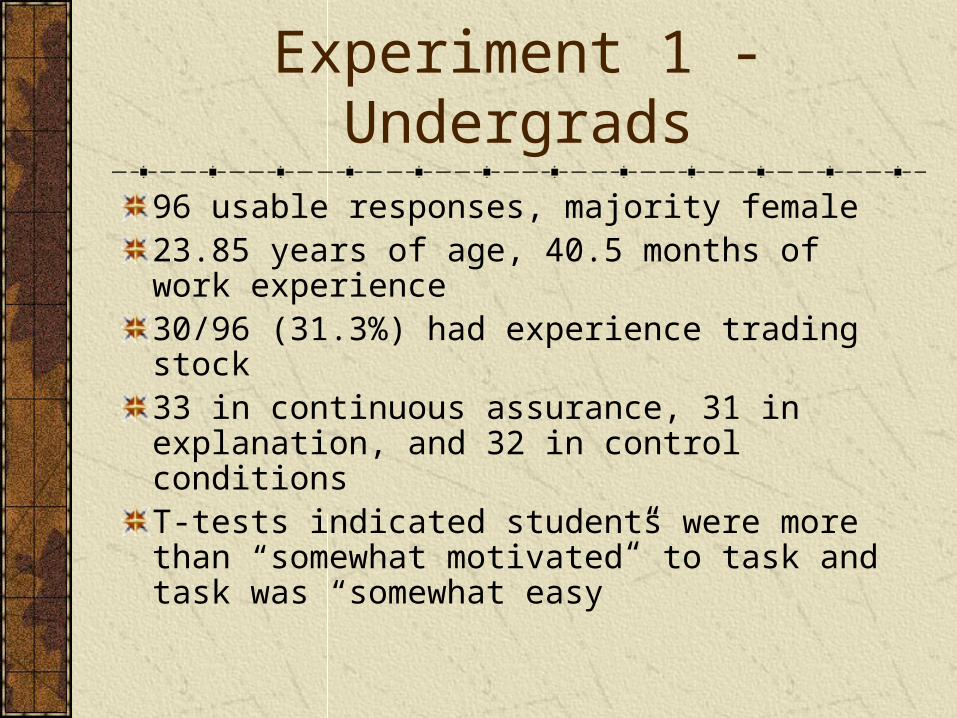

Experiment 1 - Undergrads96 usable responses, majority female23.85 years of age, 40.5 months of work experience30/96 (31.3%) had experience trading stock33 in continuous assurance, 31 in explanation, and 32 in control conditionsT-tests indicated students were more than “somewhat motivated” to task and task was “somewhat easy”

Effort & Manip. ChecksANOVA revealed explanation conditions perceived more effort in task than assurance conditions, but not for control conditionsGood news for assuranceEvidence students did not consciously put forth more effortEvidence indicating correct direction of disclosures and that received correct mitigation technique (if received one at all); MC’s deemed successful

Results – H1Revision 1 = difference between anchor of $50 and 4th valuation (t4)

Revision 2 = difference between t8 and t4

ANCOVA analysis relating to Revision 1 and 2 indicated significant differences for the ‘mitigation technique’ main effect in both sequences ; Bonferroni indicated CA LS means < than control for both sequencesKruskal-Wallis (NP) tests confirmed results; H1 supported

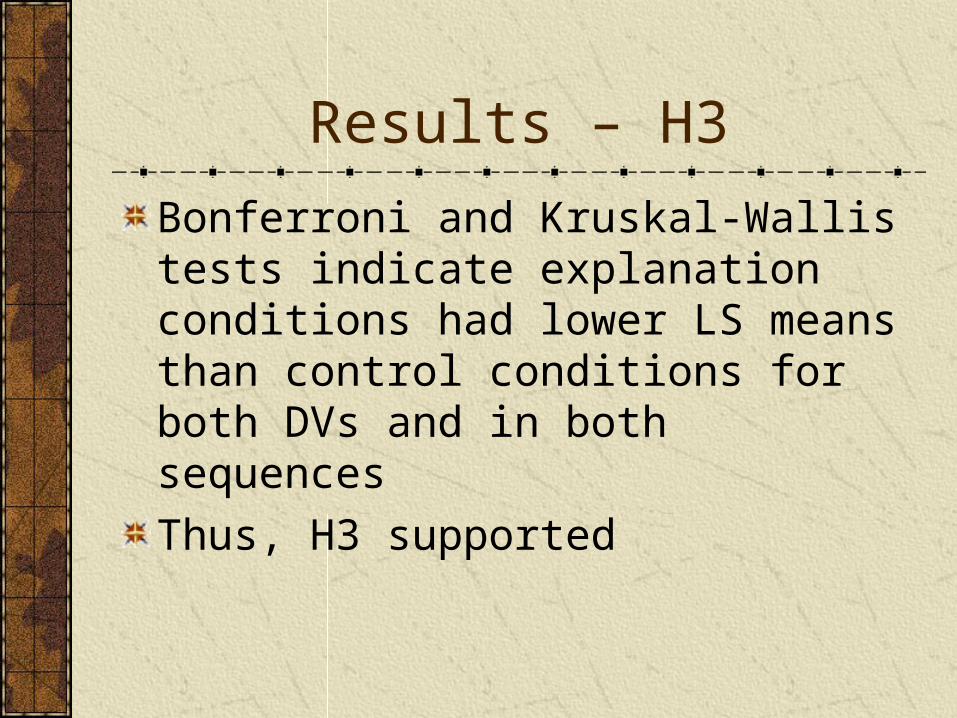

Results – H3

Bonferroni and Kruskal-Wallis tests indicate explanation conditions had lower LS means than control conditions for both DVs and in both sequences

Thus, H3 supported

Results - H2 & H4To test these hypotheses, the least-squared mean at the 8th valuation (t8) is compared for each sequence in all conditions to the original anchor of $50 using hand-calculated t-tests with alpha of 0.01.For all 3 conditions, evidence of recency existed in the +/- sequence, but not in the opposite sequence Recency? Cue weighting were not equally-weighted – negative more than positiveThus, inconclusive results for H2 and H4

Experiment 1 Data

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

$70

$75

1 2 3 4 5 6 7 8

Disclosure Number

Sto

ck P

rice

+/- CA +/- EXPL +/- CTRL -/+ CA -/+ EXPL -/+ CNTRL

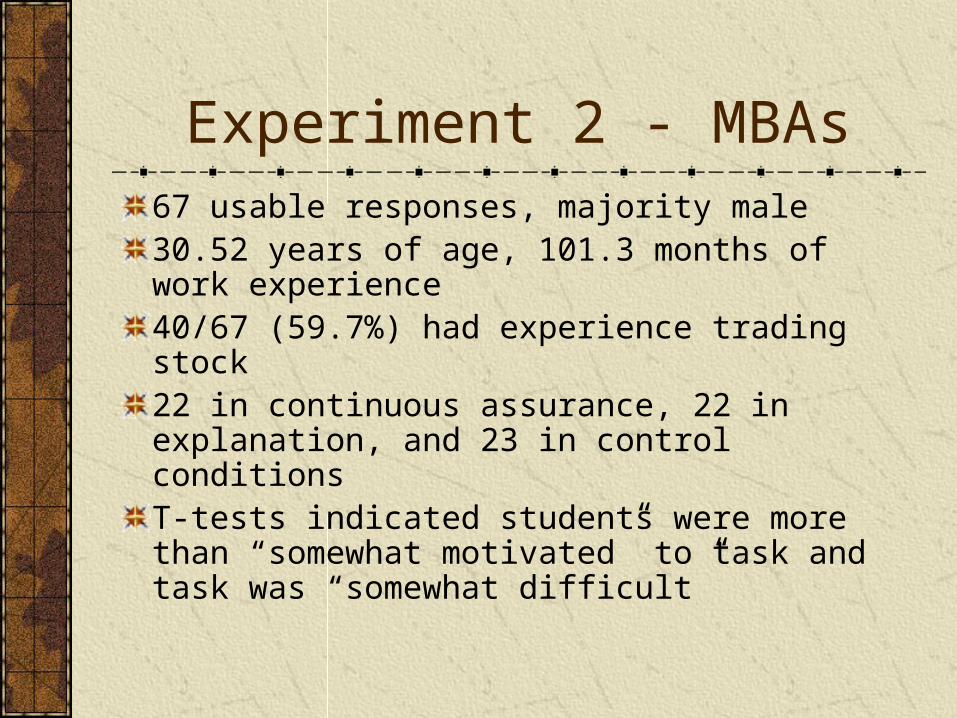

Experiment 2 - MBAs67 usable responses, majority male30.52 years of age, 101.3 months of work experience40/67 (59.7%) had experience trading stock22 in continuous assurance, 22 in explanation, and 23 in control conditionsT-tests indicated students were more than “somewhat motivated” to task and task was “somewhat difficult”

Effort & Manip. Checks

Non-significant ANOVA results for effort between conditionsEvidence students did not consciously put forth more effortEvidence indicating correct direction of disclosures and that received correct mitigation technique (if received one at all); MC’s deemed successful

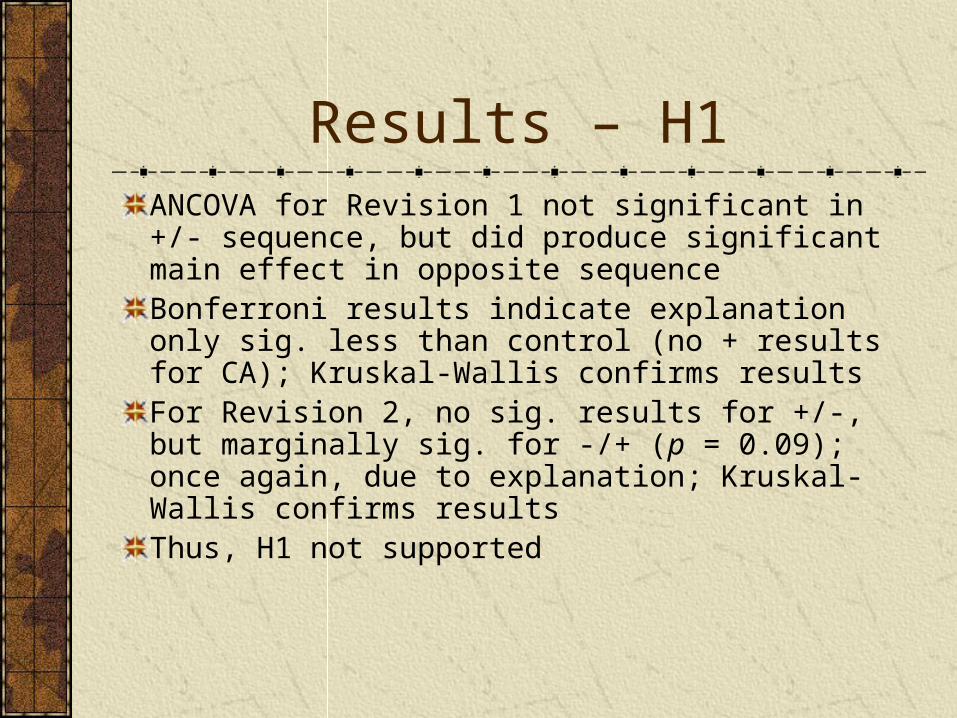

Results – H1ANCOVA for Revision 1 not significant in +/- sequence, but did produce significant main effect in opposite sequenceBonferroni results indicate explanation only sig. less than control (no + results for CA); Kruskal-Wallis confirms resultsFor Revision 2, no sig. results for +/-, but marginally sig. for -/+ (p = 0.09); once again, due to explanation; Kruskal-Wallis confirms resultsThus, H1 not supported

Results – H3For Revision 1, Bonferroni indicates explanation less LS means than control for -/+ sequence only; Kruskal-Wallis results confirm thisFor Revision 2, both Bonferroni and Kruskal-Wallis show good results for -/+ sequence, but disagree in +/- sequenceBonferroni not significant, but Kruskal-Wallis sig (p = 0.05); given normality assumption violations, go with Kruskal-Wallis resultsThus, H3 is partially supported

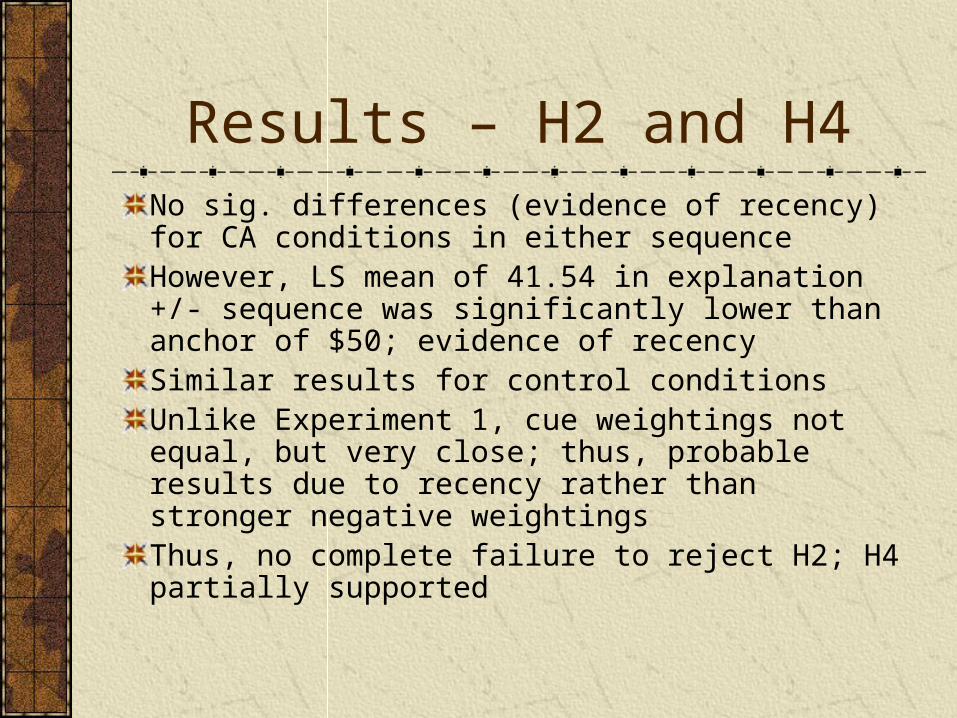

Results – H2 and H4No sig. differences (evidence of recency) for CA conditions in either sequenceHowever, LS mean of 41.54 in explanation +/- sequence was significantly lower than anchor of $50; evidence of recencySimilar results for control conditionsUnlike Experiment 1, cue weightings not equal, but very close; thus, probable results due to recency rather than stronger negative weightingsThus, no complete failure to reject H2; H4 partially supported

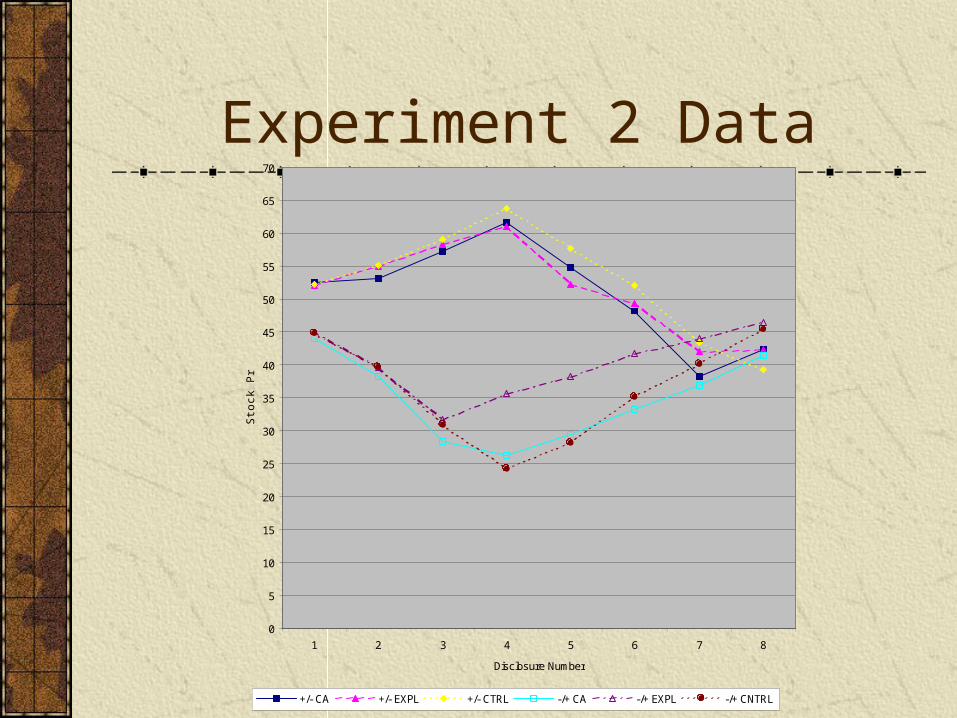

Experiment 2 Data

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

1 2 3 4 5 6 7 8

Disclosure Number

Sto

ck P

rice

+/- CA +/- EXPL +/- CTRL -/+ CA -/+ EXPL -/+ CNTRL

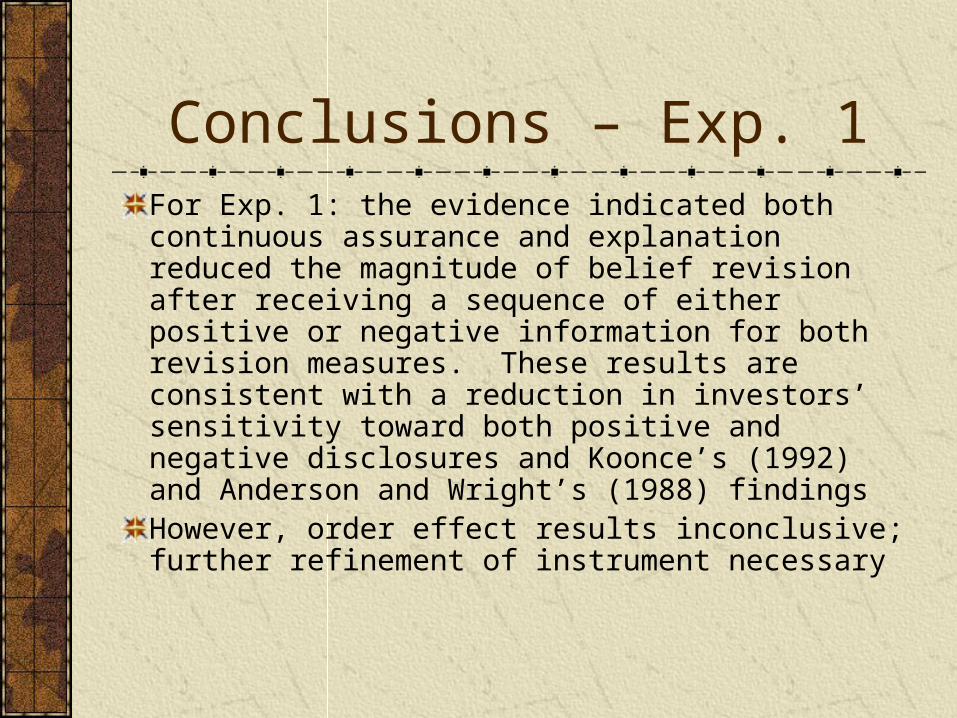

Conclusions – Exp. 1For Exp. 1: the evidence indicated both continuous assurance and explanation reduced the magnitude of belief revision after receiving a sequence of either positive or negative information for both revision measures. These results are consistent with a reduction in investors’ sensitivity toward both positive and negative disclosures and Koonce’s (1992) and Anderson and Wright’s (1988) findingsHowever, order effect results inconclusive; further refinement of instrument necessary

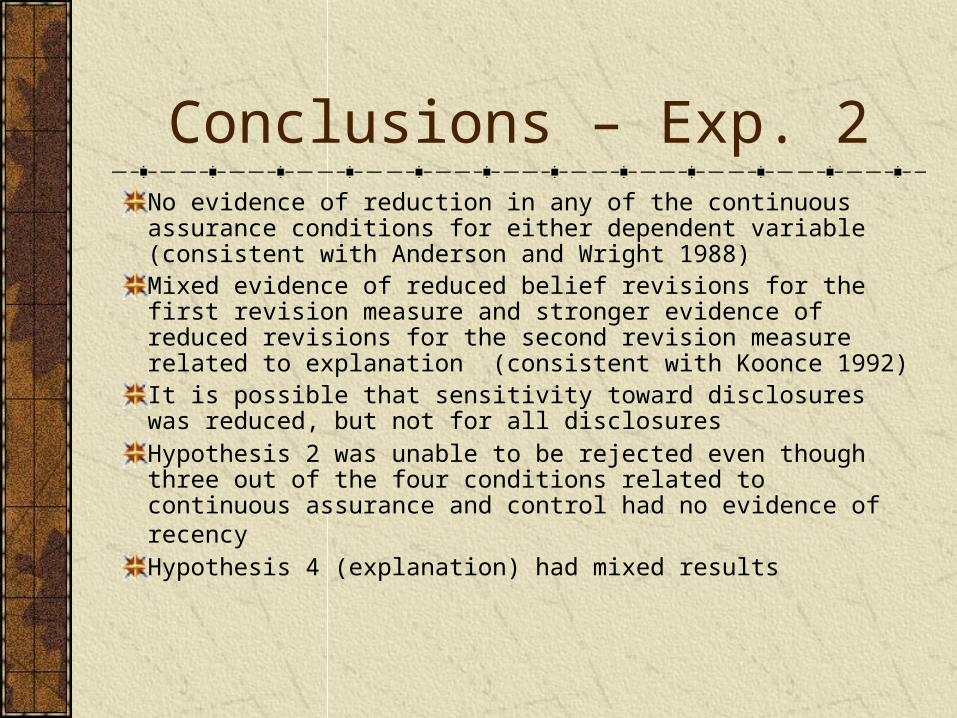

Conclusions – Exp. 2No evidence of reduction in any of the continuous assurance conditions for either dependent variable (consistent with Anderson and Wright 1988)Mixed evidence of reduced belief revisions for the first revision measure and stronger evidence of reduced revisions for the second revision measure related to explanation (consistent with Koonce 1992) It is possible that sensitivity toward disclosures was reduced, but not for all disclosuresHypothesis 2 was unable to be rejected even though three out of the four conditions related to continuous assurance and control had no evidence of recency Hypothesis 4 (explanation) had mixed results

ImplicationsIf novice/inexperienced investors’ interactions with the marketplace play a role in increased volatility (due to their lack of investing knowledge and experience), then using assurance or explanation as mitigation techniques makes senseIndependent accountants would add value through their provision of continuous assurance, while investor trading tools (e.g., E-Trade) could require typed explanations prior to any trades being madeWith regard to the more experienced investors, continuous assurance did not have a strong mitigation effect on their belief revision magnitudes; however, it did mitigate recency effects for both sequences of disclosures

Implications/Future ResearchEven though explanation does not appear to be as strong a mitigation technique for the more experienced traders, it did have some positive resultsFuture research should investigate other groups, such as mutual fund investors and professional analysts, in order to further understand their belief revision processes It should also investigate other mitigation techniques, such as accountability and group decision-making