an examination of the uncertainty of global lng supply and

TRANSCRIPT

1

An Examination of the Uncertainty

of Global LNG Supply

and Demand

23October 2015

CRICOS Provider Code Curtin 00301J; UWA 00126G

The Australian Centre for Natural Gas Management

ALP Group Participants

2

Wang Jiayue (Eric) China International Petroleum and Chemical United Co., Ltd.

Zhang Yan (Wendy) CNOOC Gas and Power Group

Wu Kun (Cathy) Guangdong Dapeng LNG Co., Ltd.

Wang Huiyi (Jessie) Shenzhen Energy Group Co., Ltd.

Li Chuanlong (Alex) Guangdong Yuehua Power Co., Ltd

Wang Xiang (Sean) Guangzhou Gas Group Co., Ltd

Overview

3

Introduction

Supply

Demand

Conclusion

Conclusion

Uncertainties

4

Market research / analysis reports

I. Introduction

Main data of NG in 2014 by region unit : billion cubic meter

Region Proved

reserves R/P ratio Production LNG

imports Pipeline imports

Total North America 12,146.9 12.8 948.4 11.6 116.9

Total S. & Cent. America 7,663.5 43.8 175.0 21.4 17.8

Total Europe & Eurasia 58,034.2 57.9 1,002.4 52.1 435.7

Total Middle East 79,813.9 >100 601.0 5.4 27.2

Total Africa 14,151.8 69.8 202.6 8.5

Total Asia Pacific 15l263.5 28.7 531.2 242.7 57.8

Total World 187,073.8 54.1 3,460.6 333.3 663.9

5

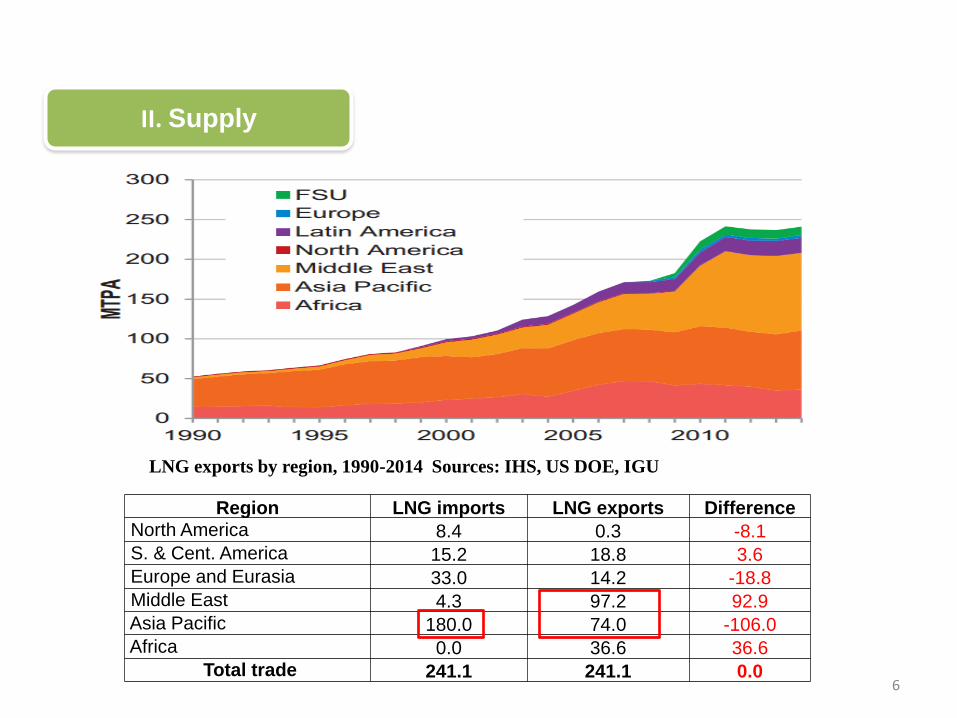

II. Supply

Source: BP statistical review of world energy 2015

6

II. Supply

Region LNG imports LNG exports Difference North America 8.4 0.3 -8.1

S. & Cent. America 15.2 18.8 3.6 Europe and Eurasia 33.0 14.2 -18.8

Middle East 4.3 97.2 92.9

Asia Pacific 180.0 74.0 -106.0

Africa 0.0 36.6 36.6

Total trade 241.1 241.1 0.0

LNG exports by region, 1990-2014 Sources: IHS, US DOE, IGU

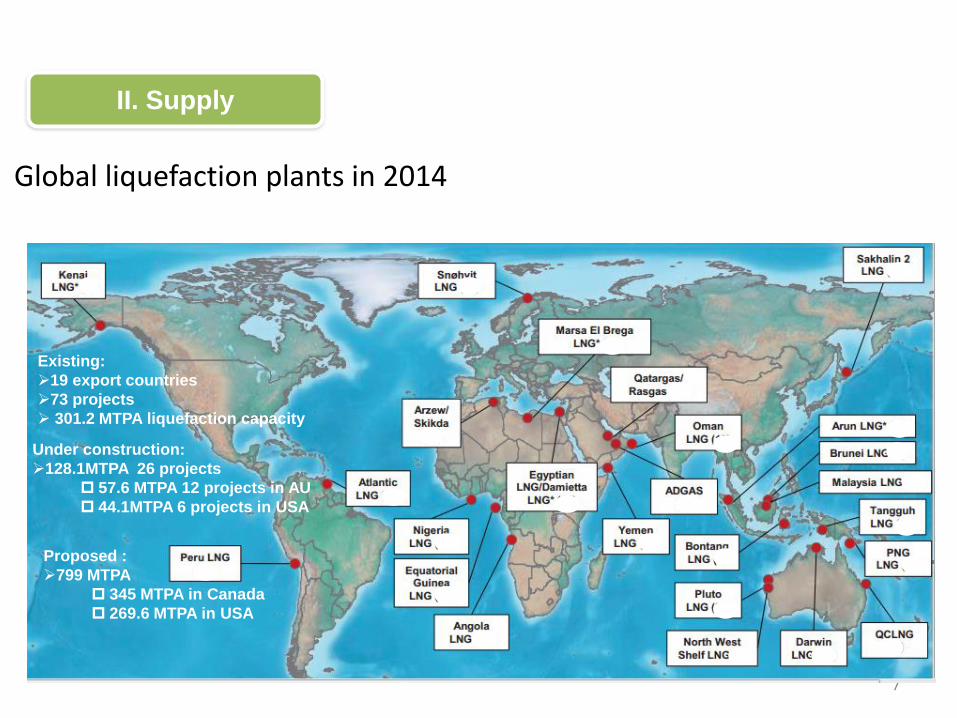

Global liquefaction plants in 2014

7

II. Supply

Existing:

19 export countries

73 projects

301.2 MTPA liquefaction capacity

Under construction:

128.1MTPA 26 projects

57.6 MTPA 12 projects in AU

44.1MTPA 6 projects in USA

Proposed :

799 MTPA

345 MTPA in Canada

269.6 MTPA in USA

8

II. Supply

Global Liquefaction Capacity

Build-Out,1990-2020 Liquefaction capacity by region in 2008,

2014 and 2020

Note: liquefaction capacity only refers to existing and under construction projects.

Sources: IHS, Company Announcements

Region 2008 2014 2020

(anticipated)

% growth

2008-2014

(actual)

%growth

2014-2020

(anticipated)

North

America 1.5 1.5 44.1 0 2840

S. & Cent.

America 15.5 20 20.5 29 3

Europe and

Eurasia 3.4 13.8 30.3 306 120

Middle East 46.8 100.8 100.8 115 0

Asia Pacific 81.2 95.3 158.1 17 66

Africa 58.7 69.9 69.9 19 0

Total 207 301.3 423.7 45 41

9

Summary

• Qatar is the largest LNG exporter currently.

• Australia will overtake Qatar as the largest liquefaction capacity holder since Seven projects are expected to be ready before 2018.

• US is anticipated to be the third largest liquefaction capacity holder because it has four LNG projects under construction.

• Russia is diversifying its gas export to Asia as well as Europe.

• The immediate future of LNG plants does not look promising due to the low utilization rate of liquefaction plants and the low LNG price.

II. Supply

III. Demand

Primary energy world consumption Million tonnes oil equivalent

• Natural gas :1/4 of global energy demand

• LNG:10% of natural gas

• Three main LNG demand regions: Asia Pacific, Europe and South &

Central America

III. Demand

Major gas trade movements 2014

Trade flows worldwide (billion cubic metres)

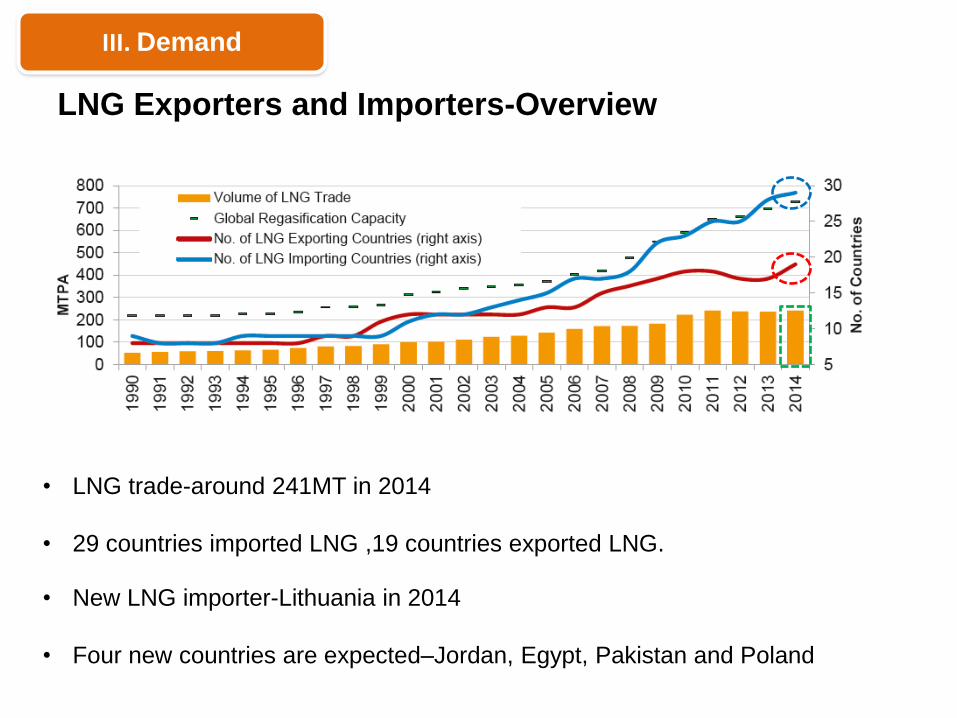

LNG Exporters and Importers-Overview

• LNG trade-around 241MT in 2014

• 29 countries imported LNG ,19 countries exported LNG.

• New LNG importer-Lithuania in 2014

• Four new countries are expected–Jordan, Egypt, Pakistan and Poland

III. Demand

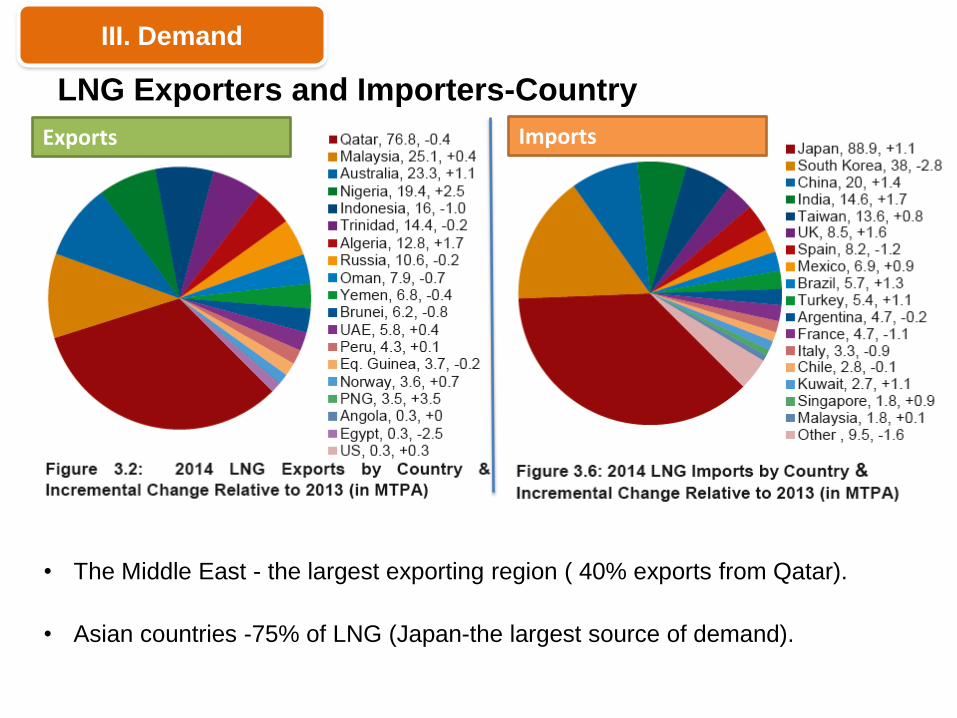

LNG Exporters and Importers-Country

• The Middle East - the largest exporting region ( 40% exports from Qatar).

III. Demand

Exports Imports

• Asian countries -75% of LNG (Japan-the largest source of demand).

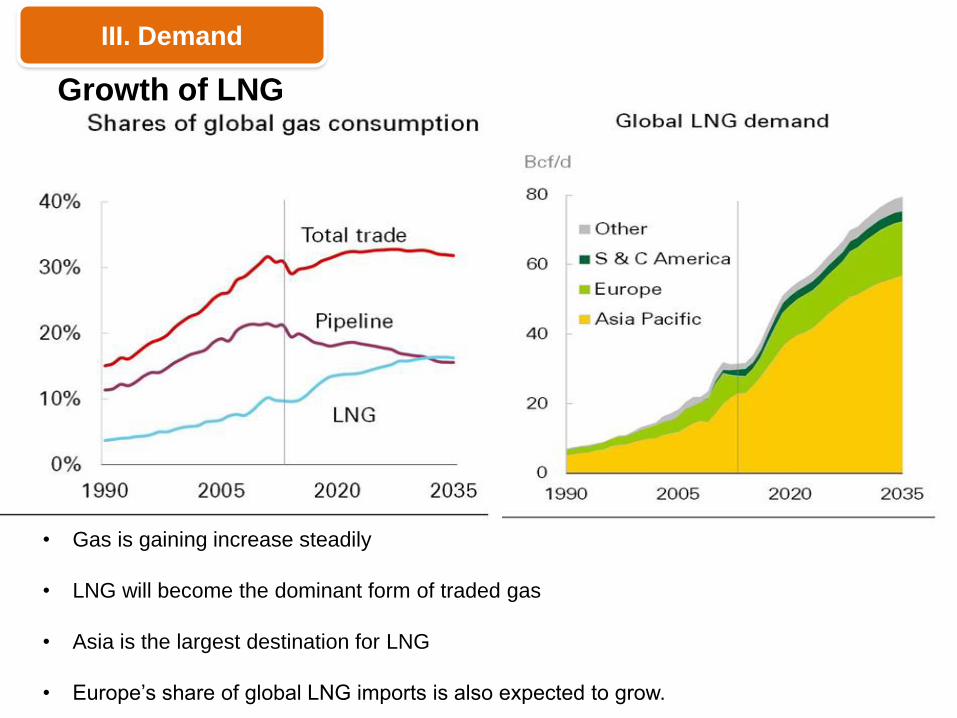

Growth of LNG

• Gas is gaining increase steadily

• LNG will become the dominant form of traded gas

• Asia is the largest destination for LNG

• Europe’s share of global LNG imports is also expected to grow.

III. Demand

New Projects are at risk of delivering inadequate returns

IV. Uncertainty

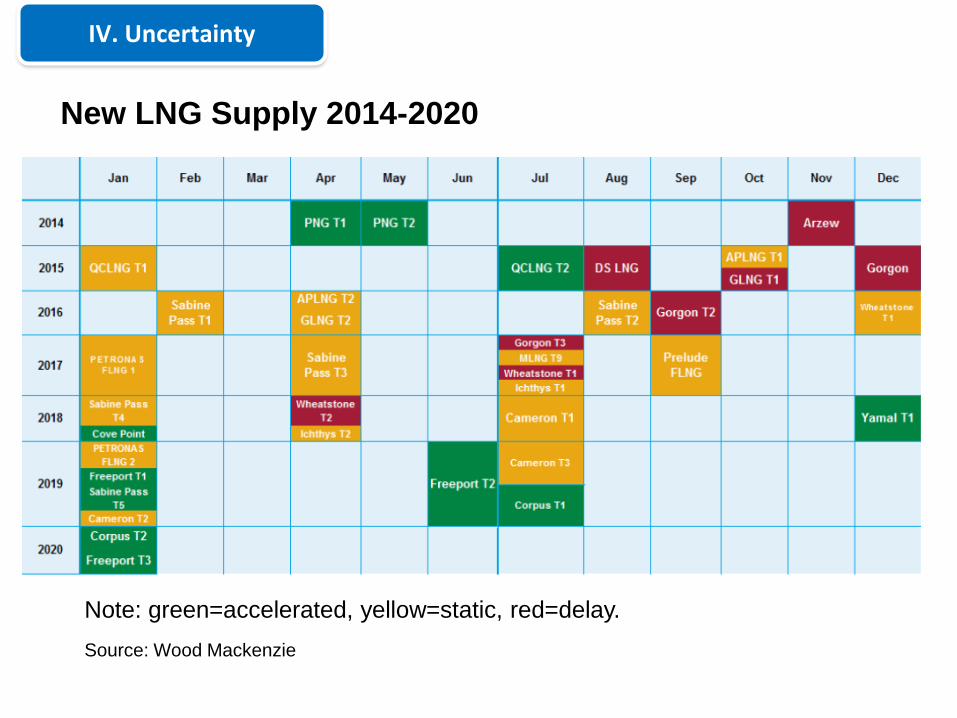

New LNG Supply 2014-2020

Note: green=accelerated, yellow=static, red=delay.

Source: Wood Mackenzie

IV. Uncertainty

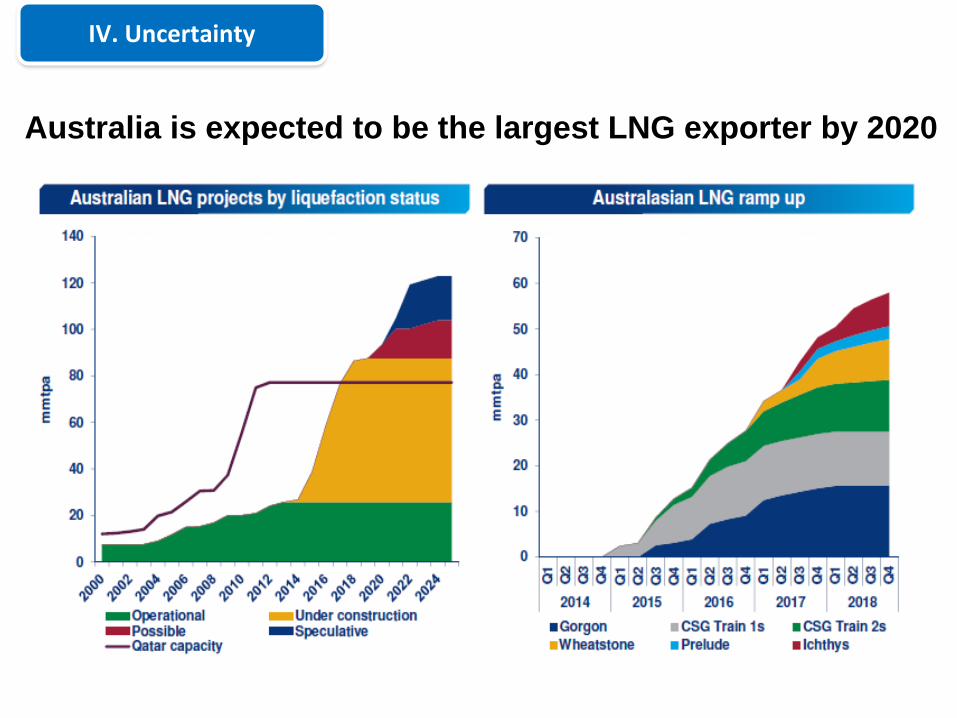

Australia is expected to be the largest LNG exporter by 2020

IV. Uncertainty

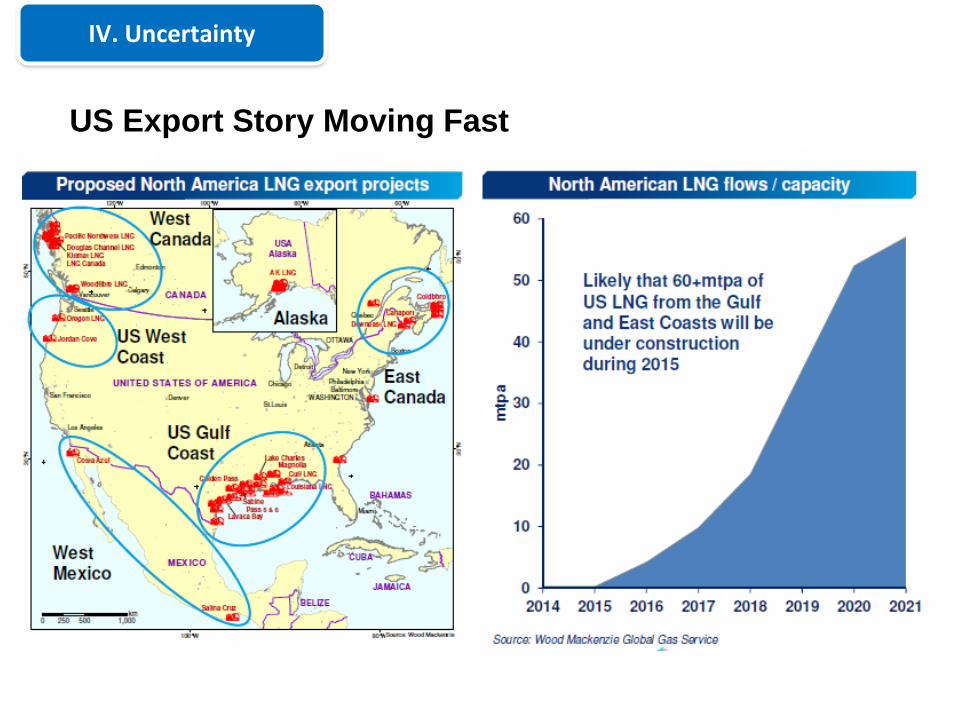

US Export Story Moving Fast

IV. Uncertainty

Challenges for Greenfield LNG

IV. Uncertainty

LNG Demand Growth Uncertainties

IV. Uncertainty

• LNG industry, Supply growth, next five years

• Worldwide, 122 mtpa

• LNG export from the US Gulf of Mexico

• Five new trains, 21 mtpa

• Six new markets; Egypt, Jordan, Pakistan, Philippines,

Poland, Uruguay.

21

VI. Conclusion

• Uncertainties on the demand side, Japanese , Chinese

economy, etc.

• Volatile, uncertain.

22

VI. Conclusion