an empirical study of the causes and consequences of mergers

TRANSCRIPT

AN EMPIRICAL STUDY OF THECAUSES AND CONSEQUENCES OF MERGERS

IN THE CANADIAN CABLE TELEVISION INDUSTRY

by

DAVID PATRICK RONALD BYRNE

A thesis submitted to the Department of Economics

in conformity with the requirements for

the degree of Doctor of Philosophy

Queen’s University

Kingston, Ontario, Canada

December, 2010

Copyright c© David Patrick Ronald Byrne, 2010

Abstract

This dissertation consists of three essays that study mergers and consolidation in the Cana-

dian cable television industry. The first essay provides a historical overview of regulatory

and technical change in the industry, and presents the dataset that I constructed for this

study. The basic pattern of interest in the data is regional consolidation, where dominant

cable companies grow over time by acquiring the cablesystems of small cable operators. I

perform a reduced-form empirical analysis that formally studies the determinants of merg-

ers, and the effect that acquisitions have on cable bundles offered to consumers.

The remaining essays develop and estimate structural econometric models to further

study the determinants and welfare consequences of mergers in the industry. The sec-

ond essay estimates an empirical analogue of the Farrell and Scotchmer (1988) coalition-

formation game. I use the estimated model to measure the equilibrium impact that economies

of scale and agglomeration has on firms’ acquisition incentives. I also study the impact

entry and merger subsidies have on consolidation and long-run market structure. The fi-

nal chapter estimates a variant of the Rochet and Stole (2002) model of multi-product

monopoly with endogenous quality and prices. Using the estimated model I compute the

impact mergers have on welfare. I find that both consumer and producer surplus rise with

acquisitions. I also show that accounting for changes both in prices and products (i.e., cable

bundle quality) is important for measuring the welfare impact of mergers.

i

Dedication

To Marisia, for always understanding, encouraging, and loving me in all that I do.

ii

Acknowledgments

I am very grateful for my supervisors, Chris Ferrall and Susumu Imai for giving me their

time, patience, advice, guidance, and encouragement over the course of my Ph.D. I have

also benefitted from the continual support of Allan Gregory and Roger Ware during my

six years at Queen’s. I am thankful for funding from SSHRC’s Doctoral Canada Graduate

Scholarship, and from the Province of Ontario’s Ontario Graduate Scholarship.

For their many helpful comments and suggestions, I thank the seminar participants

at Mount Allison University, the University of Toronto, Queen’s University, Simon Fraser

University, the University of Alberta, HEC Montreal, Carnegie Mellon (Tepper), University

of Melbourne, Analysis Group (Chicago), the 2009 CEA Annual Meetings, and the 2009

CIREQ Ph.D Students Conference. I have also had very helpful discussions with Victor

Aguirregabiria, Branko Boskovic, Sacha Kapoor, Arvind Magesan, Shannon Seitz, Ryan

Webb, and Jan Zabojnik.

Finally, I thank for my wife, parents, and brothers for their continued love, encourage-

ment and patience.

iii

Table of Contents

Abstract i

Dedication ii

Acknowledgments iii

Table of Contents iv

List of Tables vii

List of Figures ix

Chapter 1: General Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Chapter 2: Cable Television in Canada: Historical and Empirical Perspectives 5

2.1 Historical Overview . . . . . . . . . . . . . . . . . . . . . . . . 6

2.2 The Dataset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

2.3 Descriptive Statistics . . . . . . . . . . . . . . . . . . . . . . . . 14

2.3.1 Market Structure . . . . . . . . . . . . . . . . . . . . . . 14

2.3.2 Cable Prices and Packages . . . . . . . . . . . . . . . . . 17

2.4 Determinants of Acquisitions . . . . . . . . . . . . . . . . . . . 25

2.5 The Effect of Acquisitions on Cable Bundles . . . . . . . . . . . 28

iv

2.5.1 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

2.5.2 Endogeneity of acquisitions . . . . . . . . . . . . . . . . 33

2.6 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Chapter 3: Quantifying Merger Incentives in the Cable Television Industry . . 38

3.1 Related Literature . . . . . . . . . . . . . . . . . . . . . . . . . . 42

3.2 Empirical Motivation . . . . . . . . . . . . . . . . . . . . . . . . 43

3.3 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

3.3.1 Environment . . . . . . . . . . . . . . . . . . . . . . . . 46

3.3.2 Sub-Period 2: LSA Profits . . . . . . . . . . . . . . . . . 48

3.3.3 Sub-Period 1: Acquisition Game . . . . . . . . . . . . . . 51

3.3.4 Equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . 56

3.4 Empirical Implementation . . . . . . . . . . . . . . . . . . . . . 57

3.4.1 Likelihood . . . . . . . . . . . . . . . . . . . . . . . . . 58

3.4.2 Reducing Dimensionality . . . . . . . . . . . . . . . . . 60

3.5 Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

3.5.1 Parameter Estimates . . . . . . . . . . . . . . . . . . . . 61

3.5.2 Economies of Scale, Density, Deregulation and Acquisi-

tion Activity . . . . . . . . . . . . . . . . . . . . . . . . 65

3.5.3 Merger and Entry Policy Experiments . . . . . . . . . . . 69

3.6 Concluding Remarks . . . . . . . . . . . . . . . . . . . . . . . . 72

Chapter 4: The Welfare Effects of Acquisitions in the Cable Television Industry 73

4.1 Related Literature . . . . . . . . . . . . . . . . . . . . . . . . . . 77

4.2 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

v

4.2.1 Overview . . . . . . . . . . . . . . . . . . . . . . . . . . 79

4.2.2 Demand . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

4.2.3 Supply . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

4.3 Empirical Specification . . . . . . . . . . . . . . . . . . . . . . . 84

4.3.1 Estimation . . . . . . . . . . . . . . . . . . . . . . . . . 85

4.3.2 Computational Details . . . . . . . . . . . . . . . . . . . 88

4.3.3 Identification . . . . . . . . . . . . . . . . . . . . . . . . 89

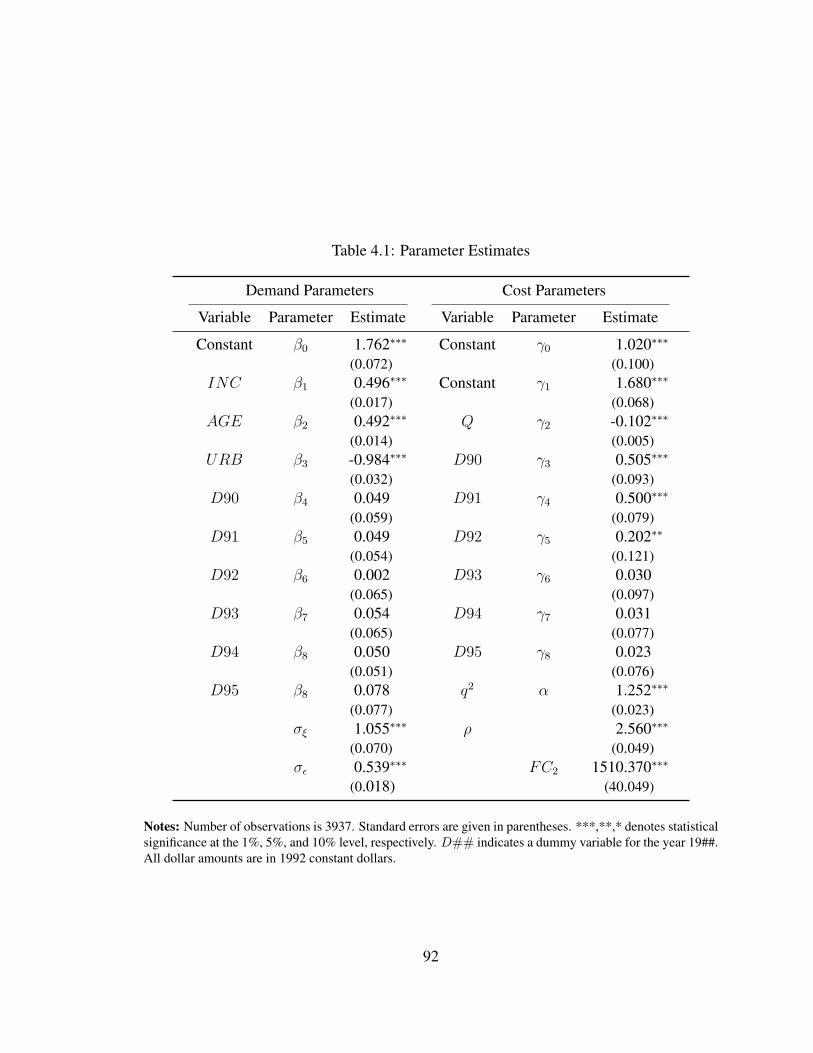

4.4 Estimation Results . . . . . . . . . . . . . . . . . . . . . . . . . 91

4.5 Welfare Effects of Acquisitions . . . . . . . . . . . . . . . . . . 96

4.6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101

Chapter 5: Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

Appendix A: Tables and Figures . . . . . . . . . . . . . . . . . . . . . . . . . . 113

vi

List of Tables

2.1 Trends in Market Structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

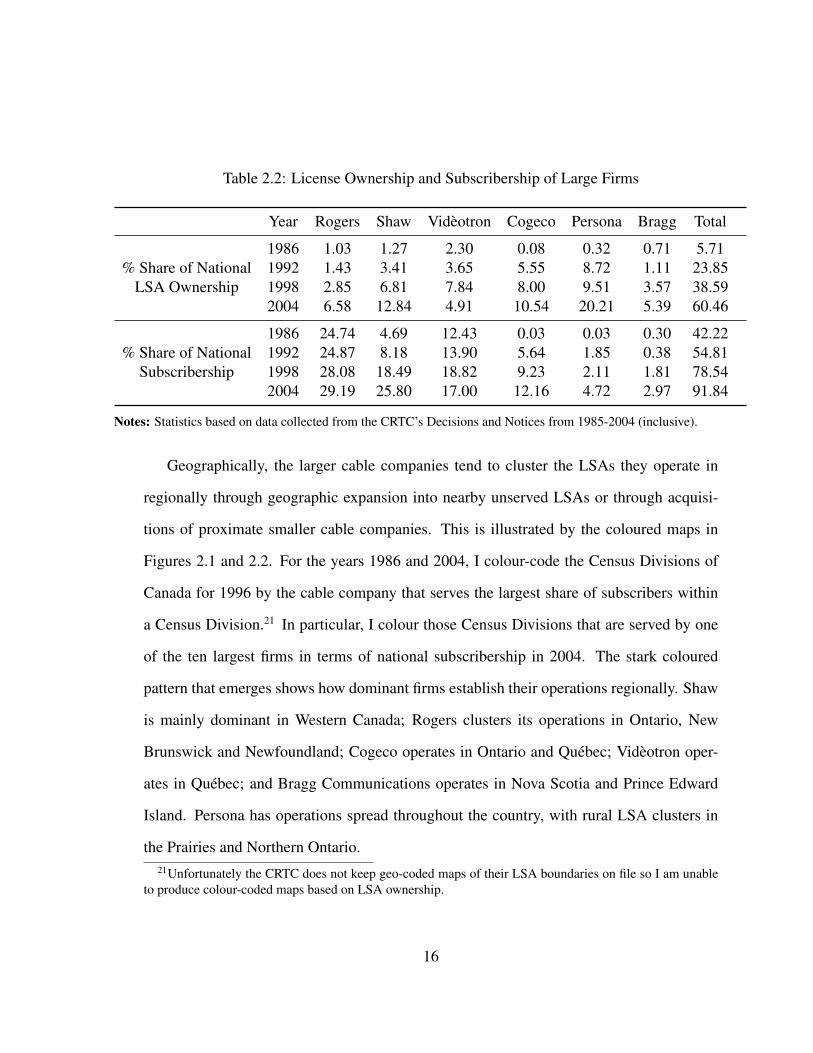

2.2 License Ownership and Subscribership of Large Firms . . . . . . . . . . . . . . 16

2.3 Master Files and Census Data Summary Statistics: 1990-1996 . . . . . . . . . . 21

2.4 Trends in Cable Prices and Channel Offerings . . . . . . . . . . . . . . . . . . 23

2.5 Prices and Packages of Large and Small Firms . . . . . . . . . . . . . . . . . . 24

2.6 Determinants of Mergers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

2.7 Relationship Between Acquisitions and Prices, Channel Counts, Market Shares

and Channel Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

2.8 Tests of Whether Acquired LSAs are Representative . . . . . . . . . . . . . . . 33

2.9 Estimation Results by Large and Not Large Buying Firms in Two-Bundle Markets 35

3.1 Variable Profit Function Parameter Estimates . . . . . . . . . . . . . . . . . . . 62

3.2 Fixed, Acquisition and Entry Cost Parameter Estimates . . . . . . . . . . . . . 65

3.3 Counterfactual Experiments Predictions . . . . . . . . . . . . . . . . . . . . . . 67

3.4 Merger Fees and Entry Subsidies Policy Experiments . . . . . . . . . . . . . . 70

4.1 Parameter Estimates . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 92

4.2 Model Fit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

4.3 Welfare Effect of Mergers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 97

4.4 Decomposition of Merger Welfare Effects . . . . . . . . . . . . . . . . . . . . 101

vii

A.1 Region Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

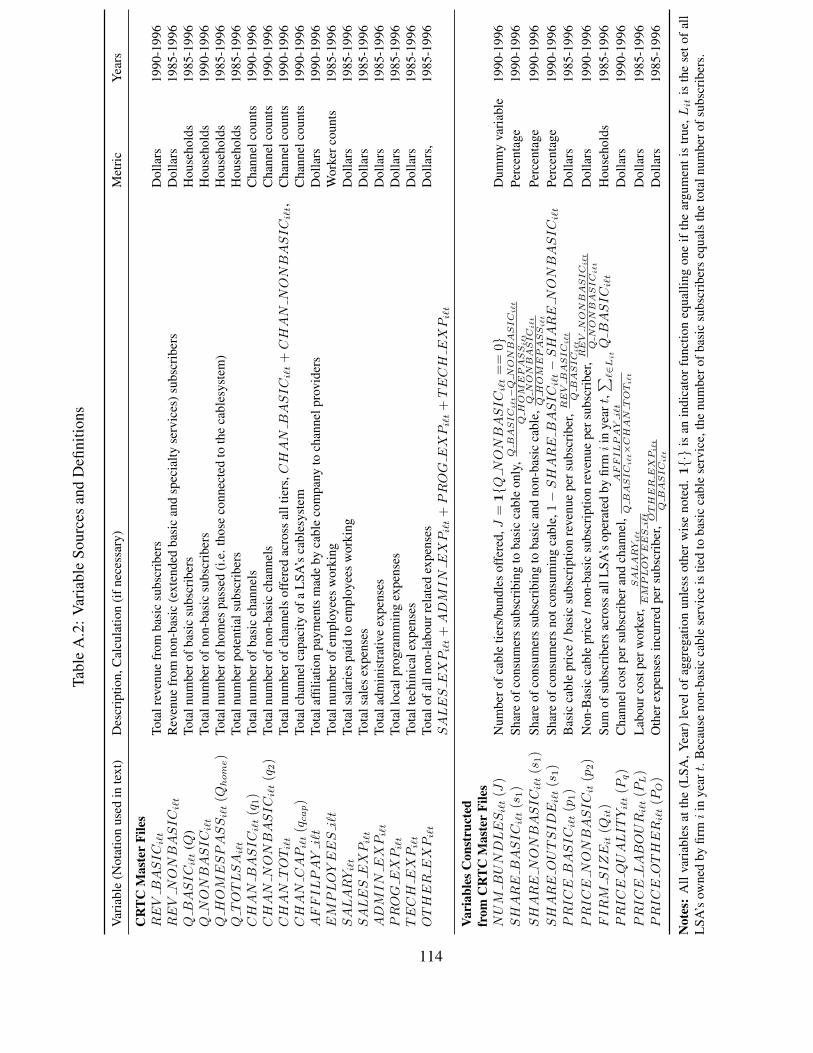

A.2 Variable Sources and Definitions . . . . . . . . . . . . . . . . . . . . . . . . . 114

A.3 License Ownership and Subscribership of Large Firms - All Years . . . . . . . . 116

A.4 Welfare Effect of Mergers (Unacquired LSA’s) . . . . . . . . . . . . . . . . . . 117

viii

List of Figures

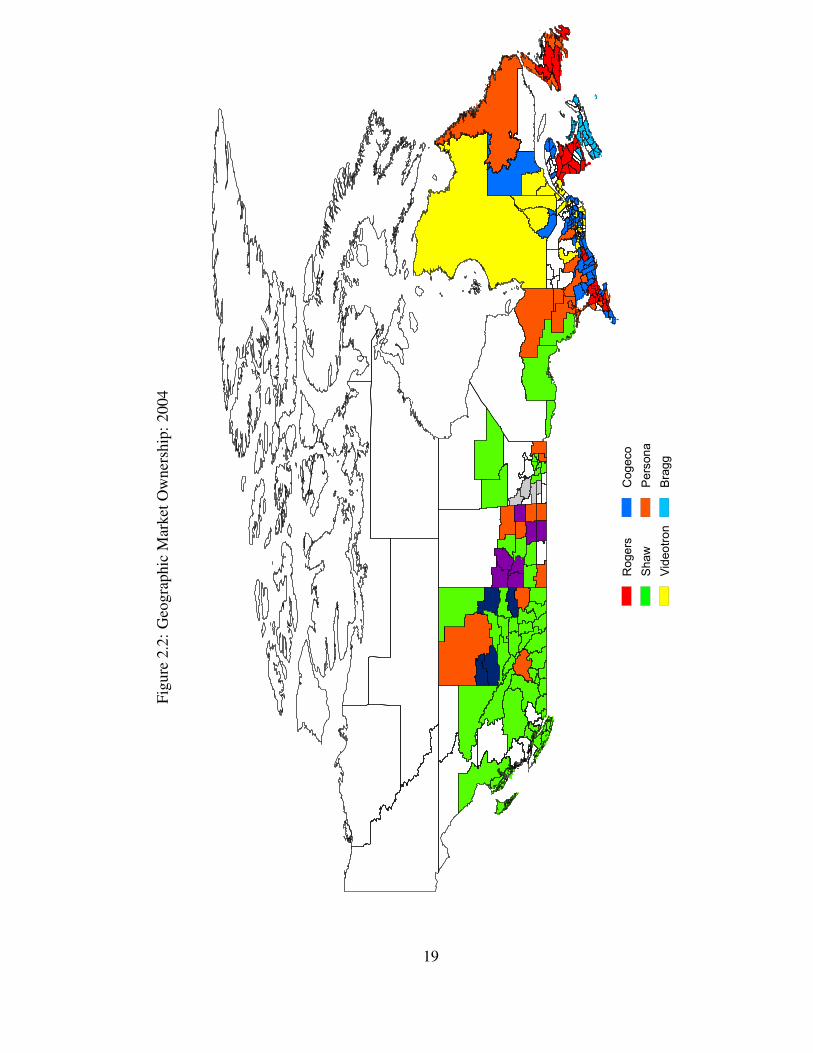

2.1 Geographic Market Ownership: 1986 . . . . . . . . . . . . . . . . . . . . . . . 18

2.2 Geographic Market Ownership: 2004 . . . . . . . . . . . . . . . . . . . . . . . 19

3.1 LSA Buyout Counts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

3.2 Firm Buyout Counts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

3.3 Number of Non-Basic Channels . . . . . . . . . . . . . . . . . . . . . . . . . . 45

3.4 Revenue per Subscriber . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

3.5 Affiliation Cost per Subscriber . . . . . . . . . . . . . . . . . . . . . . . . . . 45

3.6 Profits per Subscriber . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

3.7 Model Predictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

3.8 No Density Economies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

3.9 No Policy Change . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

4.1 Quality vs. Channels (Basic) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.2 Quality vs. Channels (Non-Basic) . . . . . . . . . . . . . . . . . . . . . . . . . . 96

4.3 CS Gains vs. Urban Density . . . . . . . . . . . . . . . . . . . . . . . . . . . . 99

4.4 Merger-Induced Changes in Marginal Costs . . . . . . . . . . . . . . . . . . . 100

A.1 Sample Reporting Form for Broadcast Undertakings . . . . . . . . . . . . . . . 118

A.2 CRTC Decision 89-46 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 121

ix

A.3 CRTC Decision 95-476 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 122

x

Chapter 1

General Introduction

This dissertation consists of three essays that empirically study the determinants and wel-

fare effects of mergers in the Canadian cable television industry.1

The first essay provides context with a historical and empirical overview of the industry.

It opens with an in-depth discussion of technological and regulatory change from the first

Canadian cablesystems in the 1950’s to present-day debates related to competition and the

technological convergence of cable and telephone companies.2 The essay then presents the

dataset that I constructed to carry out the study. These data consist of a rich panel containing

information on cable company entry and exit, acquisitions, subsidiaries, cable company

prices, market shares, channels, costs, and demographics at the local cablesystem level

1I use the words acquisition, merger and buyout interchangeably throughout this dissertation. The focusis on acquisitions however, where there is a selling firm that ceases to exist following a merger. That is, I donot study “mergers of equals.”

2Cablesystems roughly correspond to the cities, towns and villages of Canada. Law (1999) succinctlydefines a “cablesystem” as follows:

“A cablesystem is the cable network around one local head end. The head end is the locationof the equipment that receives the signals that are sent down the cable to the subscriber. Headend apparatus can include devices such as satellite dishes, large antennas for the reception ofover-the-air broadcasts, fibre optic links, video relay equipment, and microwave towers.”

1

from 1986 to 2004. Using these data, I present various summary statistics and empirical

patterns of interest that together tell a story of regional consolidation in the industry, where

dominant cable companies grow over time by acquiring the cablesystems of small cable

operators. By 2004, distinct regional clusters of cablesystems exist in Western Canada,

Ontario, Quebec and in Atlantic Canada.

These basic findings are complemented by two reduced-form analyses that respectively

focus on the determinants of mergers and the effect acquisitions have on prices and channels

offered on cable tiers. First, I estimate a Poirier (1980) bivariate probit model that predicts

the probability that two firms merge. I find that larger differences in firm size (measured by

number of subscribers nationally), and geographic proximity of the cablesystems owned,

have a positive non-negligible impact on the probably that a merger occurs. Second, I

conduct a regression analysis that looks at the relationship between cable prices, the number

of channels offered and whether a cablesystem has been recently acquired. I find that

acquisitions have little impact on cable prices and channels in rural markets where only

basic cable is offered. In larger, more urban cablesystems with both basic and non-basic

cable, the results suggest that basic prices and non-basic channels distinctly rise following

an acquisition.

The second essay further analyses the determinants of acquisitions in the industry. I

develop a model of license ownership that predicts the evolution of profit-maximizing en-

try and acquisition decisions by firms over time, starting from an initial allocation of cable

television licenses. The entry and acquisition process is modelled as a one-sided coalition-

formation game as in Farrell and Scotchmer (1988), where acquisition payoffs depend on

economies of scale and agglomeration/economies of density. I apply the model to the Cana-

dian cable television industry and estimate its parameters using license-level information

2

on acquisition and entry decisions, subscribership, and subscription profits. The model is

estimated in two steps. I first estimate firms license-level profit functions, and then esti-

mate the parameters of the fixed, merger and entry cost functions by Simulated Maximum

Likelihood. Through counterfactual simulations, I use the estimated model to quantify the

extent to which economies of scale and density drive acquisition behaviour, and to evaluate

how merger activity reacts to a partial deregulation that occurs in 1994. I also evaluate poli-

cies that stimulate entry or reduce acquisitions in the early years of the sample. The main

finding is that these policies can lead to more productive dominant firms in the long-run as

the industry consolidates.

The third essay quantifies the effect acquisitions have on welfare. I develop and es-

timate a model of multi-product monopoly in the spirit of Rochet and Stole (2002) that

endogenizes price, quality and the number of cable bundles offered to consumers. I apply

the model to the Canadian cable television industry, and estimate its parameters using panel

data on basic and non-basic cable prices and market shares from 1990-1996. To estimate

the model, I use a Simulated Method of Moments estimator that compares the model’s

predictions for cable prices, market shares and number of products offered to those in the

data. The estimates suggest there are scale effects that reduce cable companies’ marginal

cost of cable bundles, which corroborates previous findings from the U.S. cable television

industry. In light of this finding, I use the estimated model to calculate the welfare effects

of mergers, finding that mergers increase consumer and producer surplus. Prices and cable

quality are predicted to rise with acquisitions, but the increase in the latter is sufficient to

yield gains to consumers. The welfare gains are most pronounced in licenses that large

acquiring cable companies target; namely urban markets where basic and non-basic bun-

dles are offered. I show that accounting for firms’ endogenous quality choice is central to

3

this finding, and that following the common practice of focusing on only price effects of

mergers can lead to incorrect conclusions regarding their impact on welfare.

4

Chapter 2

Cable Television in Canada: Historical

and Empirical Perspectives

This chapter provides a historical and empirical overview of the Canadian cable television

industry. First, I set the context for this thesis by discussing the intertwined history of reg-

ulation and technological change from the 1950’s to present. This discussion updates and

extends previous historical overviews of the industry by Good (1974), McFadyen, Hoskins,

and Gillen (1980), and Law (1997) by making use of the Canadian Radio-television and

Telecommunication Commission’s online database of historical reports and regulatory de-

cisions for the industry.1 I then present the empirical foundation for this dissertation − a

panel dataset at the cablesystem level on market structure and cable offerings that spans

the 1986 to 2004 period. Descriptive statistics on market structure and cable bundles are

presented and I perform a reduced-form empirical analysis of the determinants of mergers

and their impact on cable prices and channel offerings.

1The url for these searchable files is http://www.crtc.gc.ca/eng/dno.htm.

5

2.1 Historical Overview

1950-1980: First Cablesystems and Regulations

The modern era of cable television in Canada dates back to 1952, the year in which the

Canadian Broadcasting Corporation (CBC) is launched, and the first urban cablesystem is

built in London, Ontario.2 Through the 1950’s and 1960’s, cablesystems emerge primarily

in urban parts of Canada until 1968, when the Federal government introduces an array of

new regulations for the industry with the Broadcasting Act.3 The Act confirms the CBC as

the national broadcaster, defines foreign ownership restrictions (i.e. what fraction of broad-

casters are allowed to be owned by non-Canadians), creates Canadian content provisions,

and creates a new national regulatory agency called Canadian Radio-television Commis-

sion (CRTC, or “the Commission”).4 Moreover, the Act creates a new mandatory licensing

scheme for broadcasting that requires cable companies to obtain licenses from the CRTC to

exclusively offer cable television as regulated monopolists within geographic “Local Ser-

vice Areas” (LSAs) or “broadcasting/distributing undertakings” (BDU’s).5 In 1968, there

are approximately 377 previously established cablesystems in Canada that are immediately

adopted by the CRTC as new LSAs with the passing of the Act. The initial regulatory

framework requires the CRTC to regulate licenses’ channel carriage, basic cable prices and

installation fees on a LSA-by-LSA basis.

2The CRTC provides an outline of the history of telecommuncations in Canada on its websitethat I follow and supplement with other sources in discussing the history of the industry. Seehttp://www.crtc.gc.ca/eng/backgrnd/brochures/b19903.htm. The Canadian Communications Foundation alsohas rich documentation of the history of the Canadian cable industry online at http://www.broadcasting-history.ca/index3.php. This subsection draws heavily on the information from these two sites.

3The Broadcasting Act can be found on the web at http://laws.justice.gc.ca/en/B-9.01/index.html.4As of 2010, content rules require at least 60% of all programming between 6:00am and midnight be

“Canadian content”, and at least 50% of programming between 6:00pm and midnight be “Canadian content”,where “Canadian content” is defined by the CRTC. Current foreign ownership restrictions state that at most46.7% of a Canadian broadcasting company may be foreign owned.

5Throughout, I use “licenses,” “Local Service Areas (LSAs).”

6

Under the Act, the CRTC’s original regulatory jurisdiction is strictly over radio and

television companies. This jurisdiction is expanded in 1976 to include all telecommunica-

tions companies (including telephone companies) with the Canadian Radio-television and

Telecommunications Commissions Act.6 This act aptly renames the CRTC to its modern-

day name, the Canadian Radio-television and Telecommunications Commission.

1980’s: Non-Basic Cable and Revamped Regulations

The CRTC overhauls a number of its regulatory practices for broadcasting in the early

1980’s. The revisions are mainly a response to the booming growth of cable television in

Canada, and newly emerging “pay” and “specialty” or “discretionary” television services.

In 1982, the CRTC licenses its first six pay television services in Canada, including chan-

nels such as The Movie Network and First Choice. Another collection of specialty channels

is licensed in 1984, including five Canadian specialty channels (Much Music, TSN, Chi-

navision, Catha, and Telelatino) and seventeen American channels (such as CNN, CMT,

TLC, and The Weather Network). With the additional “higher quality” channels, cable

companies begin tiering their cable packages by offering “basic,” “extended-basic,” and

“pay services.” The latter two services are collectively referred to as “non-basic services.”

The CRTC’s license-by-license, micro-managed regulatory approach to carriage and

pricing becomes increasingly complex and convoluted with the emergence of non-basic

cable services. As a result, the Commission revamps its regulatory framework over the

1984 to 1986 period resulting in the 1986 Cable Television Regulations.7 The Regulations

significantly reduces the regulatory burden of CRTC with respect to basic cable prices by

creating three primary rules that govern basic cable price increases. These rules are defined6The Canadian Radio-television and Telecommunications Commissions Act is documented online at

http://laws.justice.gc.ca/en/C-22/.7The details of the regulations are found at http://www.crtc.gc.ca/eng/archive/1986/PB86-27.htm.

7

in Section 18 of the Regulations as follows: 18(1) partial indexing to 80% of the C.P.I,

18(2) pass-through of unforeseen or uncontrollable costs of a cable licensee, and 18(4)-

18(6) Capital Investment Credit Plan which allows licensees to increase rates to recover

50% of eligible capital expenditures over a five-year window.

Beyond simplifying its approach to basic price regulation, there are two additional

changes implemented by the Regulations worth noting. In Section 8, regulatory classes for

the LSAs are defined based on subscribership: Class 1 (more than 6000 subscribers), Class

2 (between 2000 and 6000 subscribers), and Part 3 (less than 2000 subscribers). These

classes differ by their extent of basic price regulation. Class 1 licenses have more stringent

rules for allowable basic price increases than Class 2 licenses; Part 3 licenses are not price

regulated at all. Section 5 of the Regulations formalizes the “Transfer of Ownership and

Control” procedures that govern acquisitions. These rules require that cable licensees no-

tify the CRTC of transactions where more than 20% of voting shares for a cablesystem are

transferred.

1990-2010: The Digital Age, Technological Convergence, and Deregulation

The 1990’s bring major technological innovations as the industry moves into the Digital

Age. In 1990, Rogers becomes the first cable company in Canada to use fibre-optic cable,

a technology that significantly increases cable companies’ ability to offer many channels

across their LSAs.8 The Commission licenses the first Direct-to-Home (DTH) satellite ca-

ble services in 1995, with Bell ExpressVu being the first DTH provider to subsequently

enter the market in 1998. In response to the emergence of DTH cable service, as well as

growing demand for non-basic channels by the Canadian public, the CRTC holds a call for

8Fibre-optic cables also facilitate cable companies’ entry in the the market for telephone services a decadelater.

8

applications for new specialty and pay television channels in 1994.9 Fifty applications are

submitted, that results in the licensing of eight new specialty channels and two pay chan-

nels. For example, these new channels include Bravo!, Showcase, The Country Network,

and The Discovery Channel.

Through the late 1990’s and early 2000’s the industry enters the Information Age,

and the industry-labelled “Technological Convergence” accelerates as telecommunications

companies such as cable, phone and satellite providers continue to converge in terms of the

products they offer. Digital cable arrives in 1997, as Shaw Cable is the first company to

offer digitally-enhanced services to its subscribers in Western Canada. Canada’s major tele-

phone provider, Bell, is licensed by the CRTC in 1995 to offer cable television and begins

offering its service to local cable markets in 1997. The entry of Bell into the market for ca-

ble television represents the first competitive threat to established cable companies within

their LSAs. Conversely, cable companies enter the market for telephone services during

this period as Bragg Communications becomes the first major Canadian cable company to

offer local telephone service over its fibre optic network in 1999. In the following year

Bragg becomes one of the first telecommunications companies in North America to bundle

digital cable, internet and phone services.10 Heading into this era, the CRTC releases an

important Public Notice on “New Media” on May 17, 1999, which clarifies its stance as

a national regulator on services delivered over the Internet (or “new media”), and how it

relates to the Broadcasting Act.11 The main conclusion of the CRTC is media activities on

the Internet are not to be regulated under the Broadcasting Act.

9See CRTC Public Notice 1994-59 at http://crtc.gc.ca/eng/archive/1994/PB94-59.htm.10See http://www.eastlink.ca/about/milestones/index.asp.11See Broadcasting Public Notice 1999-84 and Telecom Public Notice 99-14 at

http://www.crtc.gc.ca/eng/archive/1999/PB99-84.htm.

9

The exclusive licensing scheme set out in the 1968 Broadcasting Act begins being dis-

mantled in 2001 with the release of Public Notice 2001-59 by the Commission. The Com-

mission introduces two initiatives; one to completely deregulate smaller/rural LSAs, and

the second to replace the territorial licensing of broadcast undertakings with a regional

licensing scheme. This regulatory overhaul is mainly a response to the emergence of dom-

inant regionally-based cable companies in Canada, and increased competition in the indus-

try from telephone and DTH satellite companies. The regional licensing scheme requires

firms to hold one license for all of their LSAs within each LSA class for a given region.12

Instead of having up to hundreds of individual licenses for all the territories served by dom-

inant firms such as Rogers, Shaw, and Cogeco, they now have at most three licenses within

a given region in Canada, which significantly reduces their regulatory burden. These regu-

latory changes are carried out in CRTC Decisions 2002-45 and 2004-382, when the CRTC

revokes the local licenses and associated regulation for all Part 3 and Class 2 LSAs in 2002

and 2004 respectively.

Looking to the future, the CRTC’s most recent comprehensive stance on the trajectory

of broadcasting and telecommunications in Canada is contained in the December 2006 re-

port entitled “The Future Environment Facing the Canadian Broadcasting System.”13 As

outlined in the report, the rapid growth of over-the-air Digital Signals, High Definition

Television, Internet Protocol Television, and the offering of handheld devices by cable and

telephone companies has created a myriad of regulatory challenges for the CRTC. In the

face of such rapid technical and regulatory change in broadcasting and telecommunica-

tions, the Federal Government issues a Telecommunications Policy Review for Canada in

12The CRTC divided Canada into five regions: Region 1: British Columbia, the Yukon, Nunavut, theNorthwest Territories; Region 2: Alberta, Saskatchewan, and Manitoba; Region 3: Ontario; Region 4:Quebec; Region 5: New Brunswick, Nova Scotia, Prince Edward Island, and Newfoundland.

13This detailed report is found online at http://www.crtc.gc.ca/eng/publications/reports/broadcast/rep061214.htm.

10

2007.14 The Government of Canada’s overall message to the CRTC is to “accelerate the

pace of deregulation of competitive telecommunications markets” and “to rely on market

forces as much as possible to achieve the policy objectives of the Telecommunications Act.”

In short, the Federal government wants to ensure that (de)regulatory reform keeps pace with

technical change, while maintaining affordability and sufficient Canadian content for con-

sumers of various forms of media. The proposal for a more market-oriented approach to

governing broadcasting and telecommunications in Canada stands in stark contrast to the

history of heavy regulation. Recently, this new regulatory approach has come to the fore-

front with additional proposals to reduce the stringency of foreign ownership restrictions

of broadcasting and telecommunications companies in Canada.15

2.2 The Dataset

Turning to empirics, I now describe the dataset that is the focal point of the dissertation.

For completeness, I provide details on all variables used throughout this thesis in Table A.2

of the Appendix.

The primary data source is the CRTC Master Files for the 1986-1996 period.16 They

contain detailed information on firms’ revenues, costs, number of households, and sub-

scribership, broken down by basic and non-basic services, and are at the LSA, year level

14The Policy Review can be found at http://www.telecomreview.ca/eic/site/tprp-gecrt.nsf/eng/rx00069.html.

15See for example “Tories to launch plans for telecom shakeup” (2010, June 4), The Globe and Mail.Interestingly, the demarcation of “telecommunications” and “broadcasting” in Canada that has been main-tained since the Telecommunications Act of 1993 has been brought into question since these proposed reducedforeign ownership restrictions only apply to telecom (i.e. phone and internet) companies, and not cable com-panies. See “Can’t separate telecom, broadcasting: CRTC head” (2010, June 8), The Globe and Mail.

16Stephen Law graciously provided these data. They have been previously used in Law (1999) and subse-quent papers. To the best of my knowledge, these data are not publicly available from 1997 onwards, withthe exception of the data collected by the private marketing firm Media Stats (http://www.mediastats.com/).

11

of aggregation. The data also have unique identifiers and location names for all LSAs and

cable companies which is useful for matching the other data sources listed below to the

Master Files dataset. The information contained in the Master Files is collected and ver-

ified by Statistics Canada on behalf of the CRTC through cable companies’ submission

of “Annual Return of Broadcasting Distribution Licensee” forms. An example of one of

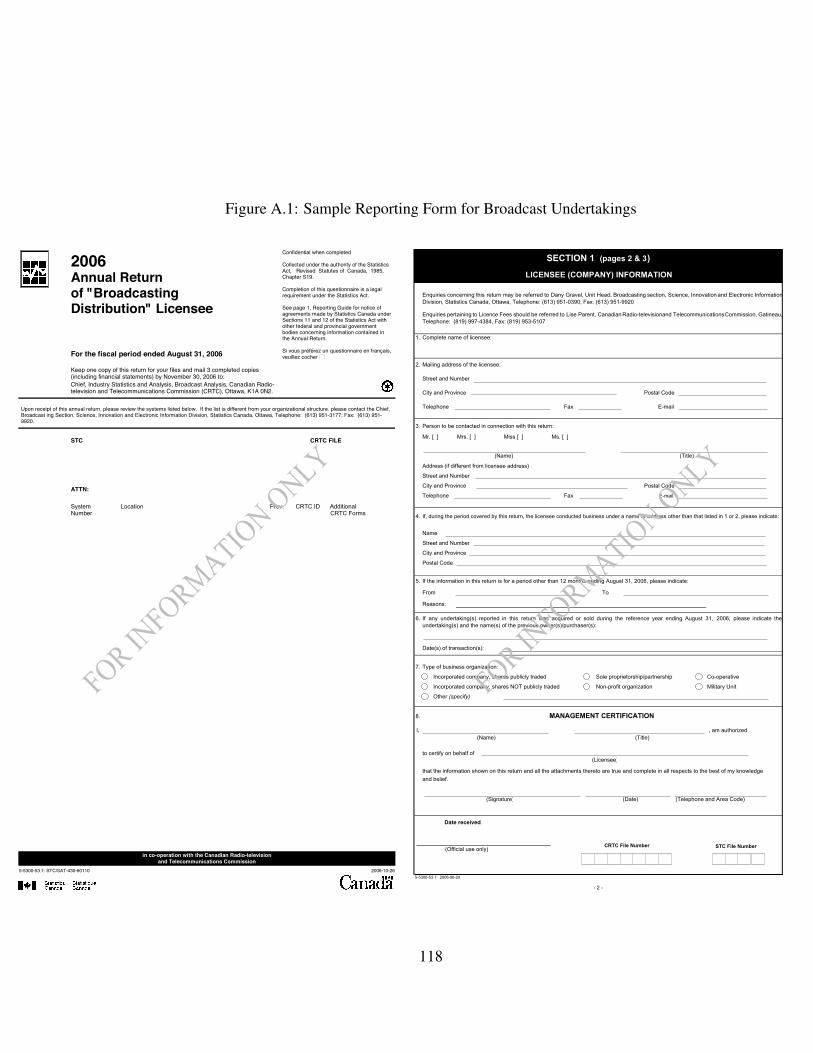

these forms for 2006 is provided in Figure A.1 in Appendix A. Having access to these

forms is helpful in understanding exactly how the variables contained in the Master Files

are constructed.

The second data source is the CRTC’s Decision and Notices (DNO) archives.17 For

each LSA, the CRTC maintains searchable archives online for all LSA-ownership related

decisions from 1984 onwards. Example decision files include new license applications, li-

cense renewals and revocations, as well as license buyouts among cable companies. Using

these decision files, I track the current cable operator (if there is one) for all 1262 LSAs

defined in the Master Files over the 1985-2004 period. For each acquisition, I record the

acquisition date, the identity of the buying and selling firms, the LSAs involved, and the

transaction price (where available). I also identify new entrant cable companies in the sam-

ple. Although the Master Files contain information on how licenses are allocated across

firms in a given year, it is important for my empirical analysis that the exact timing of

acquisition and entry decisions, as well as the firms and locations involved, be accurately

recorded. Further, the information contained in the Decision and Notice files allows me

to identify the subsidiaries of large cable companies that differ by name from their parent

company. The Master Files often fail to distinguish subsidiaries from their parent compa-

nies, which would otherwise undermine calculation of the number of subscribers a firm has

nationally. Figures A.2 and A.3 in the Appendix provide examples of acquisition files that17All of the CRTC’s Decisions and Notices are documented online at http://www.crtc.gc.ca/eng/dno.htm.

12

I use to construct these data.

I also collect information from the 1986, 1991, 1996, and 2001 Canadian Censuses

on the total number of households, average household income, average household size,

average age, unemployment rate, educational attainment (fraction of population with post-

secondary education), and urban density (population per square kilometre). These data

are obtained using the program PCensus (http://www.tetrad.com/software/pcensus/). The

LSA name identifiers are matched to their corresponding Census Subdivision to obtain the

above Census aggregates at the LSA level. I use the 1996 Geosuite package from Statistics

Canada to track location-specific household counts and urban density as it provides a more

accurate measure of the local population and urban density than what a location’s Census

Subsidivision yields.18 Moreover, Geosuite provides data for 1991 household counts and

urban density, correcting for differences in Census boundaries between Census years. For

non-Census years, I follow Holmes (2010) and impute a census variable xt according to

the following weighted average: xt =(

T2−tT2−T1

)xT1 +

(t−T1

T2−T1

)xT2 for t ∈ (T1, T2), where

T2 > T1 are Census years 1 and 2. Geographic information on LSA latitudes and longitudes

are obtained using location name searches from Google Maps (http://maps.google.com/).19

For my empirical analyses, I require a measure of a firm’s national subscribership in

a given year (i.e. the total number of subscribers across all LSAs that a cable company

currently operates in). The total number of subscribers is relatively well-reported, as I

have information on these figures for all 1262 LSAs in the Master Files. Using these

data, and Census information on the total number of households in a given location, I

interpolate missing years’ subscribership data. This provides an estimate of market size18Documentation on the 1996 Geosuite package is listed at http://geodepot.statcan.ca/Diss/Data/GeoSuite/GeoSuite e.cfm19I obtain the centre of a location by doing a name search for a LSA, and then use the script

javascript:void(prompt(’’,gApplication.getMap().getCenter())). Ideally, I woulduse geo-coded maps containing LSA boundaries to track the ‘location’ of LSAs in the sample, however inmy discussions with the CRTC, it has become evident that no such maps exist.

13

for all locations over the entire 1986-2004 period, which allows me to estimate a firm’s

national subscribership for every year.

2.3 Descriptive Statistics

2.3.1 Market Structure

Table 2.1 summarizes annual entry and acquisition activity at the firm and LSA level from

1986 to 2004. At the firm level, there is a very active entry during the late 1980’s after

which firm entry slows and continues throughout the sample until 2001. The net effect of

firm entry and acquisition causes the number of firms to rise then fall over time from 408

cable companies in 1986 to 280 firms in 2004. LSA entry and acquisitions show a similar

pattern. Cable companies actively expand into new geographic licenses in the early part of

the sample and LSA acquisitions remain active throughout.

The persistent acquisitions reported in Table 2.1 point to the fact that the industry is con-

solidating over time. Table 2.2 further illustrates this fact by reporting the shares of LSA

and subscribers served nationally from 1986 to 2004 by the 6 largest cable companies in of

terms national subscribership in 2004.20 Collectively, the largest firms increase their pres-

ence nationally over time from owning 6% of the LSAs in 1986 to over 60% of the LSAs in

2004, as illustrated in the top panel of Table 2.2. In terms of national subscribership, the six

largest firms increase their national presence from serving 42% of all subscribers in 1986 to

92% in 2004. Specifically, Persona and Cogeco respectively experience the most growth in

LSA ownership and subscribership. Amongst the larger cable companies, the firms differ

20For brevity, I only report numbers for 1986, 1992, 1998 and 2004 in Table 2.2. In the Appendix I producefigures for all years between 1986 and 2004 in Table A.3.

14

Table 2.1: Trends in Market Structure

Firm-Level Tabulations LSA-Level TabulationsYear Firms Entries Acquisitions LSAs Entries Acquisitions

1986 408 40 6 1262 119 71987 448 54 15 1262 108 151988 483 53 30 1262 122 771989 464 20 43 1262 25 611990 432 17 55 1262 16 1581991 416 18 41 1262 20 581992 421 21 28 1262 22 611993 423 22 25 1262 19 311994 419 15 25 1262 9 371995 402 11 45 1262 9 1751996 384 9 30 1262 4 431997 375 5 26 1262 0 871998 359 4 28 1262 0 771999 342 3 31 1262 0 1262000 326 4 23 1262 0 1292001 293 5 49 1262 0 2062002 286 1 12 1262 0 352003 283 0 1 1262 0 12004 280 0 4 1262 0 44

Total - 302 517 - 473 1428

Notes: Statistics based on data collected from the CRTC’s Decisions and Notices from 1985-2004 (inclusive).

substantially in their shares of LSAs and national subscribership. Although Persona oper-

ates in a relative large share of LSAs (20.21% in 2004), it has a relatively small share of

national subscribership (4.72% in 2004), reflecting the fact that Persona specializes in op-

erating rural licenses. Conversely, Rogers cable owns a relatively small share of the LSAs

nationally (7% in 2004), but has a large share of national subscribership (29% in 2004) as

it mainly draws its subscribership from a collection of densely populated LSAs in Southern

Ontario by 2004.

15

Table 2.2: License Ownership and Subscribership of Large Firms

Year Rogers Shaw Videotron Cogeco Persona Bragg Total

1986 1.03 1.27 2.30 0.08 0.32 0.71 5.71% Share of National 1992 1.43 3.41 3.65 5.55 8.72 1.11 23.85

LSA Ownership 1998 2.85 6.81 7.84 8.00 9.51 3.57 38.592004 6.58 12.84 4.91 10.54 20.21 5.39 60.46

1986 24.74 4.69 12.43 0.03 0.03 0.30 42.22% Share of National 1992 24.87 8.18 13.90 5.64 1.85 0.38 54.81

Subscribership 1998 28.08 18.49 18.82 9.23 2.11 1.81 78.542004 29.19 25.80 17.00 12.16 4.72 2.97 91.84

Notes: Statistics based on data collected from the CRTC’s Decisions and Notices from 1985-2004 (inclusive).

Geographically, the larger cable companies tend to cluster the LSAs they operate in

regionally through geographic expansion into nearby unserved LSAs or through acquisi-

tions of proximate smaller cable companies. This is illustrated by the coloured maps in

Figures 2.1 and 2.2. For the years 1986 and 2004, I colour-code the Census Divisions of

Canada for 1996 by the cable company that serves the largest share of subscribers within

a Census Division.21 In particular, I colour those Census Divisions that are served by one

of the ten largest firms in terms of national subscribership in 2004. The stark coloured

pattern that emerges shows how dominant firms establish their operations regionally. Shaw

is mainly dominant in Western Canada; Rogers clusters its operations in Ontario, New

Brunswick and Newfoundland; Cogeco operates in Ontario and Quebec; Videotron oper-

ates in Quebec; and Bragg Communications operates in Nova Scotia and Prince Edward

Island. Persona has operations spread throughout the country, with rural LSA clusters in

the Prairies and Northern Ontario.21Unfortunately the CRTC does not keep geo-coded maps of their LSA boundaries on file so I am unable

to produce colour-coded maps based on LSA ownership.

16

The main feature of the industry that induces firms to cluster their operations is po-

tential agglomeration/density economies in operating geographically proximate licenses.

For example, signals can be transmitted from a local head-end across many LSAs meaning

fixed operating costs from operating a head-end can potentially be spread across many lo-

cal markets. Figure A.3 provides an example of an acquisition that occurs for this reason.

The extent to which signals can be transmitted across locations is restricted by the fact

that signal quality deteriorates as the distance between the subscribers and the origin of a

channel’s signal grows. Economies of density can also be generated by cable companies’

ability to spread fixed administrative and technical/support services across local LSAs.

2.3.2 Cable Prices and Packages

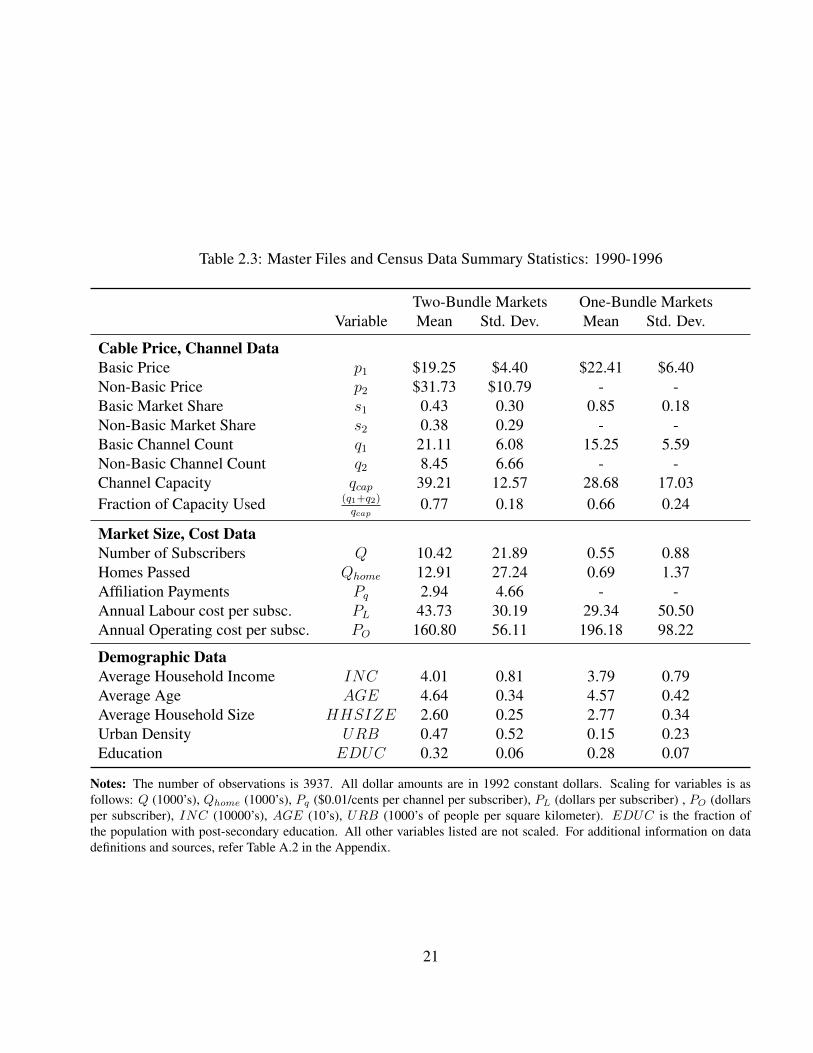

Table 2.3 contains summary statistics for LSAs where only basic cable is offered (here-

after, one-bundle markets), and for those where both basic and non-basic cable are offered

(hereafter, two-bundle markets). Throughout, I use pj, qj, sj to represent prices, “quality”

(measured by channel counts), and market shares for cable bundle j.22 Basic packages are

indexed by j = 1 and non-basic packages by j = 2. The first panel shows that the aver-

age one-bundle market has 85% of its total population subscribing to basic cable, paying

$22.41 for the bundle and getting 15 channels.23 For an average two-bundle market, 43%

of consumers subscribe to only basic cable while 38% subscribe to both basic and non-

basic services. Basic bundles in two-bundle markets cost $19.25 and provide 21 channels

on average, while adding the non-basic bundle costs provides 8 additional channels for an

22This notation for cable prices, quality and shares is used in Chapter 4 below, so I employ it here forconsistency. Of course, raw channel counts can inaccurately measure cable quality if consumers’ derivedifferent levels of utility from different channels. Unfortunately, data on channel identity is not currentlyavailable for my sample.

23All dollar amounts are in 1992 constant dollars throughout.

17

Figu

re2.

1:G

eogr

aphi

cM

arke

tOw

ners

hip:

1986

Rogers

Shaw

Videotron

Cogeco

Persona

Bragg

18

Figu

re2.

2:G

eogr

aphi

cM

arke

tOw

ners

hip:

2004

Rogers

Shaw

Videotron

Cogeco

Persona

Bragg

19

extra $12.48.24 The top panel also shows that firms are generally not channel-capacity con-

strained within their LSAs as cable operators in one- and two-bundle markets respectively

use 66% and 77% of their total available channel capacity on average.

The second and third panels of Table 2.3 summarize market size, cost and demographic

data. One-bundle markets have 5,500 subscribers on average, while the average numbers

of homes passed (i.e. the total number of households currently hooked up to a local ca-

blesystem, not of all of which necessarily subscribe to cable) is 6,900. This compares to

averages of 10,420 and 12,910 subscribers and homes passed in two-bundle markets. This

difference in average market size for one- and two-bundle markets suggests that there are

additional fixed costs cable companies must pay to offer non-basic cable services.

The cost data show that on average a cable operator pays $2.94 cents per channel per

subscriber in affiliation payments to upstream non-basic channel providers. The final two

variables in the panel report sample averages for LSA-level per-subscriber labour and op-

erating expenses (i.e. sales, administration, technical, and local programming expenses).

For one-bundle markets average labour and operating expenditures are $29.34 and $196.18

per subscriber respectively, and for two-bundle markets they are $43.73 and $160.80. The

higher average labour cost for two-bundle markets suggests that there are additional labour

costs in offering non-basic cable. The lower per-subscriber operating costs suggest that

sunk expenditures for basic services can be also be applied to non-basic services. The cen-

sus data summary statistics in the third panel of Table 2.3 show that with the exception

of urban density, demographics are relatively similar across one- and two-bundle markets.

These statistics indicate that two-bundles are offered in relatively more urbanized markets.

24Note that there is a tying requirement whereby a consumer must subscribe to basic cable in order tosubscribe to non-basic cable services. The average price for non-basic cable consists of the $19.25 for basicservices, plus the additional $12.48 for non-basic cable, therefore yielding a total average price of $31.73 forthose consumers who subscribe to both basic and non-basic services.

20

Table 2.3: Master Files and Census Data Summary Statistics: 1990-1996

Two-Bundle Markets One-Bundle MarketsVariable Mean Std. Dev. Mean Std. Dev.

Cable Price, Channel DataBasic Price p1 $19.25 $4.40 $22.41 $6.40Non-Basic Price p2 $31.73 $10.79 - -Basic Market Share s1 0.43 0.30 0.85 0.18Non-Basic Market Share s2 0.38 0.29 - -Basic Channel Count q1 21.11 6.08 15.25 5.59Non-Basic Channel Count q2 8.45 6.66 - -Channel Capacity qcap 39.21 12.57 28.68 17.03Fraction of Capacity Used (q1+q2)

qcap0.77 0.18 0.66 0.24

Market Size, Cost DataNumber of Subscribers Q 10.42 21.89 0.55 0.88Homes Passed Qhome 12.91 27.24 0.69 1.37Affiliation Payments Pq 2.94 4.66 - -Annual Labour cost per subsc. PL 43.73 30.19 29.34 50.50Annual Operating cost per subsc. PO 160.80 56.11 196.18 98.22

Demographic DataAverage Household Income INC 4.01 0.81 3.79 0.79Average Age AGE 4.64 0.34 4.57 0.42Average Household Size HHSIZE 2.60 0.25 2.77 0.34Urban Density URB 0.47 0.52 0.15 0.23Education EDUC 0.32 0.06 0.28 0.07

Notes: The number of observations is 3937. All dollar amounts are in 1992 constant dollars. Scaling for variables is asfollows: Q (1000’s), Qhome (1000’s), Pq ($0.01/cents per channel per subscriber), PL (dollars per subscriber) , PO (dollarsper subscriber), INC (10000’s), AGE (10’s), URB (1000’s of people per square kilometer). EDUC is the fraction ofthe population with post-secondary education. All other variables listed are not scaled. For additional information on datadefinitions and sources, refer Table A.2 in the Appendix.

21

Table 2.4 reports annual trends in cable package prices and channel counts from 1990 to

1996 for one- and two-bundle markets. For two-bundle markets, basic prices trend upward

over the sample, while non-basic prices follow a “U-shape,” initially falling in 1993-1994

and then rising through 1995-1996.25 The average channel counts in columns four and five

show that the number of channels offered in basic and non-basic services is rising over

time. These changes in bundle prices and channel counts partly reflect the increase in the

number of licensed non-basic services by the CRTC in the 1990’s, as discussed in section

2.1 above. There is considerably more growth in the number of non-basic channels offered,

which more than doubles from 1990 to 1996. The market share averages in columns six

and seven provide evidence of consumer switching in response to the enriched non-basic

services over time. Between 1990 and 1996, the share of consumer subscribing to basic-

only services falls by 25%, while non-basic subscription rates rise by 64%. One-bundle

markets see an increase in their average price from $20.81 in 1990 to $24.20 in 1996,

and basic packages experience more than a 50% increase in average channel offerings

from approximately 12 to 19 channels. Within one-bundle markets, the share of consumers

purchasing basic service out of all homes passed is stable, hovering between 84% and 86%.

Another pattern of interest is how LSA-level cable prices, channels and demographics

vary with the size of cable companies. There is an exhaustive empirical literature on the

cable television industry for the U.S. that finds larger horizontal firm size reduces cable

companies’ channel costs which in turn affects the prices and composition of their cable

bundles.26 Scale effects in marginal costs arise through negotiations over per-subscriber

channel prices between upstream channel providers and downstream cable companies.

Larger firms are in better negotiating positions as they can offer larger audiences to channel25Recall these amounts are in real terms (1992=100).26See for example Chipty (1995), Ford and Jackson (1997), Chipty and Snyder (1999), and Crawford and

Yurukoglu (2010).

22

Table 2.4: Trends in Cable Prices and Channel Offerings

Year p1 p2 q1 q2 s1 s2

Two-Bundle Markets1990 17.91 32.13 20.08 5.89 0.52 0.281991 18.25 32.23 20.40 6.18 0.54 0.281992 18.97 31.09 20.45 7.28 0.46 0.351993 19.48 29.92 20.27 8.39 0.38 0.441994 19.82 30.26 21.03 8.91 0.36 0.451995 19.97 32.84 22.15 10.98 0.37 0.431996 20.13 33.20 23.57 11.32 0.39 0.46

One-Bundle Markets1990 20.81 - 12.08 - 0.84 -1991 22.15 - 13.75 - 0.84 -1992 22.52 - 14.97 - 0.84 -1993 23.23 - 15.25 - 0.84 -1994 22.87 - 15.69 - 0.84 -1995 22.62 - 17.83 - 0.86 -1996 24.20 - 18.65 - 0.85 -

Notes: Yearly means presented in each column. All dollar amounts are in 1992 constant dollars.

providers, who in turn are concerned with viewership for the advertisements they air be-

tween their shows. Recent findings by Crawford and Yurukoglu (2010) suggest that large

U.S. cable companies such as Comcast obtain up to 13% lower channel costs than smaller

cable operators.

Table 2.5 illustrates the impact of firms’ size on cable bundles by presenting sample

means for LSA-level cable prices, channels, market shares and demographics conditional

on whether a market is served by one of the ten largest firms (or “large firms”) by national

23

Table 2.5: Prices and Packages of Large and Small Firms

Two-Bundle Markets One-Bundle MarketsVariable Big 10 Not Big 10 Big 10 Not Big 10

p1 18.53 19.62 20.10 22.54p2 30.41 32.41 - -s1 0.34 0.48 0.86 0.85s2 0.45 0.34 - -q1 22.89 20.20 20.22 15.07q2 12.11 6.57 - -

Q 19.67 5.68 0.72 0.55INC 4.18 3.91 3.66 3.81AGE 4.60 4.65 4.60 4.56

HHSIZE 2.57 2.61 2.69 2.77URB 0.68 0.37 0.30 0.15

EDUC 0.33 0.31 0.34 0.28

Notes: Means for each variable are presented in each column. All dollar amounts are in 1992 constant dollars.All other variables are scaled as noted in the footnote of Table 2.3.

subscribership in 1996.27 The patterns for cable bundles are clear for both one- and two-

bundle markets; larger cable companies offer more channels in their packages for lower

prices on average. The differences are most stark for channel counts; large firms offer

nearly double the number of non-basic channels on average in two-bundle markets, and

36% more basic channels in one-bundle markets. Relatedly, large firms on average tend

to have a larger share of subscribers out of all homes passed in one-bundle markets, and

a larger relative share of consumers buying non-basic packages in two-bundle markets. In

fact, the majority of consumers in two-bundle markets served by large cable companies

subscribe to non-basic cable on average, while the opposite is true for two-bundle markets

27I denote firms outside of the largest ten as “small firms.” The findings from this table are consistent forvarious definitions of “large” firms (top five, ten, twenty, thirty, etc.). The ten firms comprising the largefirms are Rogers, Shaw, Videotron, Cogeco, C.F. Cable, Telecable Des Milles-Iles, Cablecasting, VideonCablesystems, and Cablenet .

24

served by smaller firms. The bottom panel of Table 2.5 shows that on average, large cable

companies tend to serve markets with a larger subscriber base and higher urban density.

The differences in other demographics across markets served by large and non-large firms

are negligible. Taken together, the results from this table are suggestive of scale effects

on cable prices and bundle composition. Chapter 4 further investigates the extent to which

channel cost reducing scale effects are responsible for these differences.

2.4 Determinants of Acquisitions

The summary statistics describe a consolidation process where large cable companies ac-

quire small cable companies over time. Further, acquiring companies target small firms

whose LSAs are geographically proximate to their own cable systems, which leads to the

observed clustering of cable ownership in 2004. These two facts suggest that economies of

scale and density affect firms’ merger decisions. To formally investigate the determinants

of mergers, I estimate the following bivariate probit model that predicts the probability that

firm i and j enter into a merger in year t:

a∗ijt = Xijtβ1 + εijt; aijt = 1a∗ijt > 0 (2.1)

a∗jit = Xijtβ2 + εjit; ajit = 1a∗jit > 0 (2.2)

The term 1· is an indicator function, a∗ijt is firm i’s latent utility from entering a merger

with firm j in year t, and aijt is firm i’s binary decision to agree to enter an i − j merger

in year t (and vice-versa with a∗jit and ajit for firm j). The error terms are assumed to

be drawn from a mean-zero bivariate normal distribution, with normalized variances equal

to one and correlation coefficient ρ. In the data, the aijt decisions are partially observed

25

since I only observe acquisitions where both aijt and ajit equal one. To accommodate this

partial observability, I estimate equations 2.1 and 2.2 using the Poirier (1980) bivariate

probit model. 28

I include three variables of interest in Xij related to potential merging firms’ relative

size and geographic proximity of their LSAs. The size variables are ∆Qijt = Qit − Qjt

and (∆Qijt)2), where Qit is the number of subscribers firm i has nationally in year t. Dif-

ferences in firm size between two merging firms serve as a proxy for gains from a merger

due to economies of scale. Including the square of firm size differences in Xij allows me

to see if these returns are increasing or decreasing in the size differential between merging

parties. My economies of density variable is constructed as: densij =∑

`∈Lit

∑`′∈Ljt

1d``′

where Lit and Ljt are the sets of LSAs owned by firm i and j in year t respectively, and

d``′ is the Great Circle Distance between LSA ` and `′, as measured using their coordi-

nates from name searches with Google Maps. I focus on local density effects by setting

d``′ = ∞ for d``′ > 100 km. This measure of geographic complementarity between firms

i and j is similar to that used by Jia (2008). I also include dummy variables for years and

“regions” in Canada to account for year- and region-specific factors that drive acquisition

behaviour. These regions are broadly defined (ten total) and are constructed using the Cen-

sus Economic Regions from Statistics Canada for 2001. They are listed in Table A.1 of the

Appendix.

I estimate the model under two restrictions to simplify the estimation procedure and

interpretation of the results. First, following Brasington (1999), I estimate the model un-

der the restriction that both sides of a merger use the same decision making model, i.e.

β1 = β2. Second, I assume firms only consider merger partners whose LSAs are located

28Brasington (1999) uses this empirical model to study spatial patterns in the consolidation of schooldistricts in the major metropolitan areas of Ohio.

26

Table 2.6: Determinants of Mergers

Parameter MarginalVariable Estimate Effect

∆ Qijt 0.104∗∗∗ 0.083∗∗∗

(0.013) (0.011)(∆ Qijt)

2 -0.037∗∗∗ -0.029∗∗∗

(0.006) (0.005)densijt 0.101∗∗∗ 0.081∗∗∗

(0.021) (0.016)Constant 0.001 -

(0.001) -ρ 0.897 -

(1.414) -Year Fixed Effects Y YRegion Fixed Effects Y Y

P (aijt = 1, ajit = 1|Xijt) 0.021LL -1460.600N 15667# Acquisitions 340

Notes: ***, **, * indicate statistical significance at the 1%, 5%, and 10% levels respectively. Standard errorsare reported in parentheses. The total number of subscribers Qij is in terms of millions.

in the region they operate in. This assumption allows me to greatly reduce the size of the

set of potential mergers when computing the likelihood for the model. For firms that are

located in multiple regions of Canada, I assume there is a regional manager that makes

within-region acquisition decisions for a firms regional subsidiary. These regional man-

agers make merger decisions in isolation, ignoring the simultaneous merger decisions of

the firm’s other regional managers across Canada. This assumption is very much in-line

with how acquisition decisions for large firms are made in practice. In fact, the raw data

assigns different firm identifiers to the regional subsidiaries of the large cable companies

like Rogers, Shaw, Cogeco, Persona.

27

The estimation results and corresponding marginal effects (computed at sample means)

are presented in Table 2.6. I find that economies of scale and density have positive impact

on the probability that two cable companies merge, with statistically significant estimates

and marginal effects at the one-percent level (evaluated at sample means). The estimates

for differences in firm size and its square show that the larger the difference in firm size

between two firms, the more likely they are to merge. However this size effect is diminish-

ing as the difference in firm size grows. The marginal effect from the linear term on ∆ Qij

implies an increase in the probability of acquisition by 8.3%, which is four times the mean

predicted acquisition probability of 2%. Similarly, the marginal effect of densij increases

the probability of acquisition by 8.1%

2.5 The Effect of Acquisitions on Cable Bundles

It is also of interest to see what effect acquisitions have on cable price, channels offered,

market shares and channel costs (non-basic affiliation payments per subscriber per month

denoted by affilpay2). I investigate these effects empirically using the following regression

that predicts y`kt for license ` served by cable company k at time t:

yk`t = β0 + β1A`t + β2Qkt +Xk`tβ3 +Dtβ4 + FE` + εk`t (2.3)

I separately estimate (2.3) for two and one-bundle markets for each of y`kt ∈ p1, p2, q1, q2, s1,

s2, affilpay2.29 The covariates of interest are a dummy variable A`t which equals one if

29Throughout this section, I focus on a subsample of LSAs that do not experience a change in the numberof products offered (i.e., locations that do not switch from one to two-bundle markets or vice versa) over the1990-1996 period. In total, 18 out of 784 LSAs experience such a change in the number of products offered.None of these changes correspond to an acquisition. The estimation samples for one and two-bundle marketsafter removing these locations contain 891 and 2790 observations, respectively.

28

LSA ` is acquired in year t and all years thereafter, and the horizontal size of firm k in

LSA ` in year t, Qkt (i.e., firm k’s national subscribership). The vector Xk`t consists

of location and firm control variables including average household income, average age,

average household size, the proportion of the population with post-secondary education,

urban density, the number of homes passed, and a dummy variable equalling one if firm

k is a multi-system operator. To account for year and location unobserved heterogeneity,

I include time and LSA fixed effects (respectively, Dt and FE`). The final term εk`t is

an idiosyncratic error term. Under this LSA fixed-effects specification, the identification

of β1 relies on within license variation over time in basic and non-basic prices, channel

counts, market shares and affiliation payments before and after an acquisition. Within li-

cense variation in the various dependent variables and firm size, which is mainly generated

by acquisitions, is what identifies β2.

2.5.1 Results

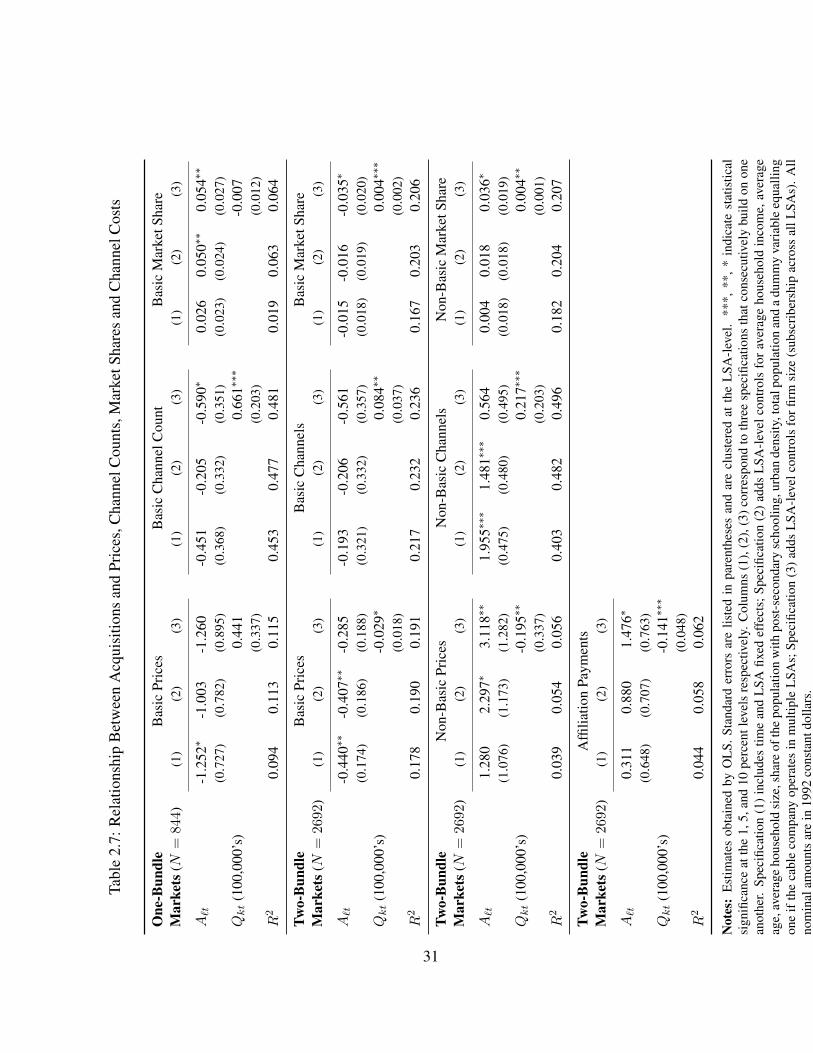

Table 2.7 presents the OLS estimates for β1 and β2 for each dependent variable using three

different specifications. Specification (1) includes the merger dummy and a full set of year

and LSA fixed effects. Specification (2) adds the vector of LSA and firm specific controls

(Xk`t) and specification (3) adds cable operator firm size (Qkt). Comparing the estimates

for β1 across specifications (1) and (2) shows that controlling for local factors beyond

the location-specific fixed effects does not have large impact on the results. The sign of

all the estimates remain the same, and the magnitudes and statistical significances of the

estimates are comparable. Overall, the estimates from the top panel in Table 2.7 indicate

that following acquisitions, one-bundle markets experience small declines in basic prices

29

and channel counts, and a slight 5.0% increase in basic market shares. The results for two-

bundle markets in the second and third panels suggest that basic prices and channels counts

slightly fall following acquisitions, while non-basic prices and channel counts experience

relatively large, statistically significant increases of $2.30 and 1.48, respectively. Affiliation

payments are also predicted to rise by $0.88 per-subscriber following mergers, though the

change is not statistically significant.

By comparing the results for specifications (2) and (3), I can assess the extent to which

merger effects correspond to merger-induced changes in horizontal firm size of a LSA’s

local monopolist. The estimates of β1 and β2 in the top panel of Table 2.7 show that

basic prices and channel counts are still predicted to fall with acquisitions in one-bundle

markets, however the firm size effects suggest that larger firms tend to offer more basic

channels at higher prices (though only the estimates for the basic channel count equation

are statistically significant).

For example, if the median-sized company operating in a one-bundle market in 1993

(Tofino Television) is acquired by its nearby regionally dominant firm (Shaw Cable) the

coefficient estimates predict that basic prices and channel counts would respectively fall

and rise by $1.68 and 3.82 channels, respectively. The predicted change in market shares

remain similar for one-bundle markets under column (3) (subscription rates rise by 5.3%)

with firm size having a negligible effect.

30

Tabl

e2.

7:R

elat

ions

hip

Bet

wee

nA

cqui

sitio

nsan

dPr

ices

,Cha

nnel

Cou

nts,

Mar

ketS

hare

san

dC

hann

elC

osts

One

-Bun

dle

Bas

icPr

ices

Bas

icC

hann

elC

ount

Bas

icM

arke

tSha

reM

arke

ts(N

=84

4)(1

)(2

)(3

)(1

)(2

)(3

)(1

)(2

)(3

)

A`t

-1.2

52∗

-1.0

03-1

.260

-0.4

51-0

.205

-0.5

90∗

0.02

60.

050∗∗

0.05

4∗∗

(0.7

27)

(0.7

82)

(0.8

95)

(0.3

68)

(0.3

32)

(0.3

51)

(0.0

23)

(0.0

24)

(0.0

27)

Qkt

(100

,000

’s)

0.44

10.

661∗∗∗

-0.0

07(0

.337

)(0

.203

)(0

.012

)R

20.

094

0.11

30.

115

0.45

30.

477

0.48

10.

019

0.06

30.

064

Two-

Bun

dle

Bas

icPr

ices

Bas

icC

hann

els

Bas

icM

arke

tSha

reM

arke

ts(N

=26

92)

(1)

(2)

(3)

(1)

(2)

(3)

(1)

(2)

(3)

A`t

-0.4

40∗∗

-0.4

07∗∗

-0.2

85-0

.193

-0.2

06-0

.561

-0.0

15-0

.016

-0.0

35∗

(0.1

74)

(0.1

86)

(0.1

88)

(0.3

21)

(0.3

32)

(0.3

57)

(0.0

18)

(0.0

19)

(0.0

20)

Qkt

(100

,000

’s)

-0.0

29∗

0.08

4∗∗

0.00

4∗∗∗

(0.0

18)

(0.0

37)

(0.0

02)

R2

0.17

80.

190

0.19

10.

217

0.23

20.

236

0.16

70.

203

0.20

6

Two-

Bun

dle

Non

-Bas

icPr

ices

Non

-Bas

icC

hann

els

Non

-Bas

icM

arke

tSha

reM

arke

ts(N

=26

92)

(1)

(2)

(3)

(1)

(2)

(3)

(1)

(2)

(3)

A`t

1.28

02.

297∗

3.11

8∗∗

1.95

5∗∗∗

1.48

1∗∗∗

0.56

40.

004

0.01

80.

036∗

(1.0

76)

(1.1

73)

(1.2

82)

(0.4

75)

(0.4

80)

(0.4

95)

(0.0

18)

(0.0

18)

(0.0

19)

Qkt

(100

,000

’s)

-0.1

95∗∗

0.21

7∗∗∗

0.00

4∗∗

(0.3

37)

(0.2

03)

(0.0

01)

R2

0.03

90.

054

0.05

60.

403

0.48

20.

496

0.18

20.

204

0.20

7

Two-

Bun

dle

Affi

liatio

nPa

ymen

tsM

arke

ts(N

=26

92)

(1)

(2)

(3)

A`t

0.31

10.

880

1.47

6∗

(0.6

48)

(0.7

07)

(0.7

63)

Qkt

(100

,000

’s)

-0.1

41∗∗∗

(0.0

48)

R2

0.04

40.

058

0.06

2

Not

es:

Est

imat

esob

tain

edby

OL

S.St

anda

rder

rors

are

liste

din

pare

nthe

ses

and

are

clus

tere

dat

the

LSA

-lev

el.

***,

**,

*in

dica

test

atis

tical

sign

ifica

nce

atth

e1,

5,an

d10

perc

entl

evel

sre

spec

tivel

y.C

olum

ns(1

),(2

),(3

)cor

resp

ond

toth

ree

spec

ifica

tions

that

cons

ecut

ivel

ybu

ildon

one

anot

her.

Spec

ifica

tion

(1)

incl

udes

time

and

LSA

fixed

effe

cts;

Spec

ifica

tion

(2)

adds

LSA

-lev

elco

ntro

lsfo

rav

erag

eho

useh

old

inco

me,

aver

age

age,

aver

age

hous

ehol

dsi

ze,s

hare

ofth

epo

pula

tion

with

post

-sec

onda

rysc

hool

ing,

urba

nde

nsity

,tot

alpo

pula

tion

and

adu

mm

yva

riab

leeq

ualli

ngon

eif

the

cabl

eco

mpa

nyop

erat

esin

mul

tiple

LSA

s;Sp

ecifi

catio

n(3

)ad

dsL

SA-l

evel

cont

rols

for

firm

size

(sub

scri

bers

hip

acro

ssal

lLSA

s).

All

nom

inal

amou

nts

are

in19

92co

nsta

ntdo

llars

.

31

The column (3) estimates in the bottom three panels of Table 2.7 contain various in-

dividually statistically significant estimates (at conventional levels) for β1 and β2 for two-

bundle markets. Interpreting the β1 estimates, basic prices and channel counts fall with

acquisitions, while non-basic prices and channel counts rise. The firm size coefficients am-

plify the magnitude of these effects for basic and non-basic prices and non-basic channel

counts, while they offset the acquisition effect for basic channel counts. The magnitude of

these effects are again best illustrated by way of example. Consider a hypothetical acquisi-

tion of the median sized firm operating in a two-bundle market in 1993 (AGI Cablevision)

by its nearby dominant firm (Shaw Cable). The estimates predict that such an acquisition

leads to negligible changes in basic prices and services in two-bundle markets with a $0.47

predicted fall in basic cable prices and a less than 0.003 predicted fall in basic channels of-

fered. The predictions for non-basic services starkly contrast these findings as the estimates

imply large differences in prices ($1.82 higher) and channels offered (2.03 more channels)

following the acquisition. The results from the basic and non-basic market share equations

suggest that a modest share of consumers switch from basic to non-basic cable following

an acquisition.

The final set of specification (3) estimates in the bottom panel of Table 2.7 show there

are statistically significant relationships between non-basic per-subscriber affiliation pay-

ments, and acquisitions and firm size. The parameter estimates highlight two opposing

forces that potentially drive non-basic channel costs. Controlling for firm size, affiliation

payments are predicted rise by $1.48 per subscriber following acquisitions, on average. To

the extent that higher quality channels are more costly to cable providers (Crawford and

Yurukoglu (2010)), this estimate provides some additional evidence that acquisitions lead

to higher quality cable. Conversely, larger firms are predicted to realize lower affiliation

32

Table 2.8: Tests of Whether Acquired LSAs are Representative

Basic Non-Basic Basic Non-Basic Basic Non-Basic FirmPrice Price Channels Channels Share Share Size

One-BundleMarkets (N = 680)Coefficient on -0.697 - -0.252 - -0.102∗∗∗ - -0.001LSA ever acquired (1.109) - (0.802) - (1.039) - (0.069)

Two-BundleMarkets (N = 1910)Coefficient on -0.263 -0.283 0.476 -0.424 -0.001 -0.028 -0.901∗∗

LSA ever acquired (0.448) (0.853) (0.500) (0.453) (0.027) (0.025) (0.374)

Notes: Estimates obtained by OLS. Standard errors are listed in parentheses and are clustered at the LSA-level. ***,**, * indicate statistical significance at the 1, 5, and 10 percent levels respectively. The specification is analogous toSpecification (2) from Table 2.7, expect the LSA fixed effects are replace with province dummies. All nominal amountsare in 1992 constant dollars.

payments, which suggests there may be scale effects. The estimates imply that affiliation

payments are predicted to rise by $0.54 per subscriber following the hypothetical AGI Ca-

blevision/Shaw merger, even though there is a large predicted rise in non-basic prices and

channel counts, as discussed above.

2.5.2 Endogeneity of acquisitions

If firms’ acquisition decisions are driven by target firms’ basic or non-basic cable prices,

channel counts and so on, the OLS estimates of β1 and β2 in Table 2.7 will suffer from

selection bias. For example, if large cable companies acquire small ones because small

firms offer poor non-basic cable services (i.e. low non-basic channel counts), then the OLS

estimates for β1 and β2 would be biased upward due to selection effects.

As a first check on potential endogeneity issues, I compare the pre-merger charac-

teristics of acquired LSAs to non-acquired LSAs prior to acquisitions to see if there are

33

systematic differences in the types of LSAs that are acquired.30 Using the sample of all

non-acquired LSAs and pre-merger observations for all acquired LSAs, I regress a given

LSA-level characteristic on a dummy variable that equals one if a LSA is subsequently ac-

quired. If the coefficient estimate on the acquisition dummy is statistically significant, then

the dependent variable for acquired LSAs systematically differs from non-acquired LSAs.

I present the results from these regressions for one and two-bundle markets in Table 2.8,

where the dependent variables are basic and non-basic prices, channel counts and market

shares, as well as horizontal firm size (national subscribership) of a LSA’s current cable

company.31 For one-bundle markets, the only statistically significant estimate is for basic

shares (at the 1% level), suggesting that acquiring firms potentially target one-bundle mar-

kets with low-demand. For two-bundle markets, only the regression where firm size is the

dependent variable delivers a statistically significant result (at the 5% level). The coeffi-

cient estimate suggests that two-bundle markets served by smaller firms are more likely to

be acquired, which reflects the aforementioned fact that the dominant firms are involved in

the majority of acquisitions. There do not appear to be systematic differences in acquired

LSAs based on the characteristics of the current cable bundles since as other estimates are

statistically insignificant.

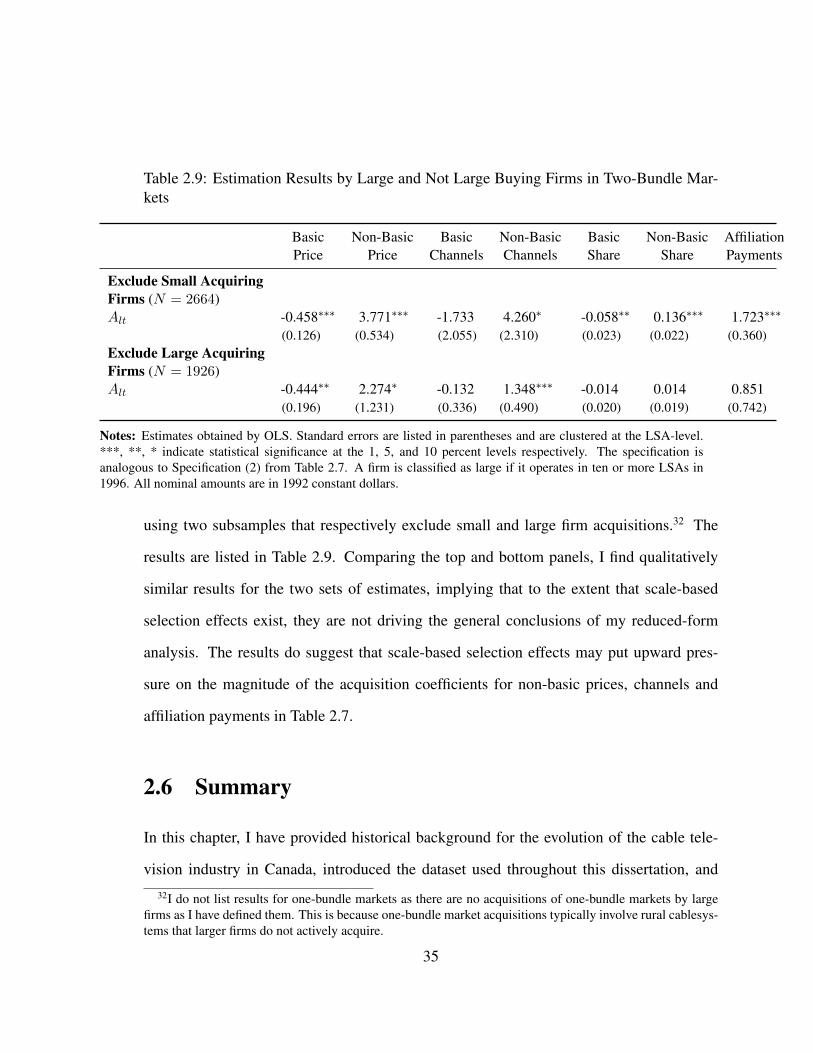

As another check on endogeneity, I re-estimate equation (2.3) using sub-samples of

the data that vary the extent to which selection effects matter. For example, acquisitions

involving the dominant firms may be more influenced by selection effects as scale efficien-

cies may allow larger companies to offer more lucrative bundles that potentially earn higher

profits. I continue to classify a firm as “large” if it is one of the ten largest cable companies

in 1996 by national subscribership. I re-estimate equation (2.3) for two-bundle markets30The two merger endogeneity checks in this subsection follow Sweeting (2010)’s approach.31I include time dummies and the firm and demographic controls from above in the regressions, and replace

the LSA fixed effects with province fixed effects.

34

Table 2.9: Estimation Results by Large and Not Large Buying Firms in Two-Bundle Mar-kets

Basic Non-Basic Basic Non-Basic Basic Non-Basic AffiliationPrice Price Channels Channels Share Share Payments

Exclude Small AcquiringFirms (N = 2664)Alt -0.458∗∗∗ 3.771∗∗∗ -1.733 4.260∗ -0.058∗∗ 0.136∗∗∗ 1.723∗∗∗

(0.126) (0.534) (2.055) (2.310) (0.023) (0.022) (0.360)Exclude Large AcquiringFirms (N = 1926)Alt -0.444∗∗ 2.274∗ -0.132 1.348∗∗∗ -0.014 0.014 0.851

(0.196) (1.231) (0.336) (0.490) (0.020) (0.019) (0.742)

Notes: Estimates obtained by OLS. Standard errors are listed in parentheses and are clustered at the LSA-level.***, **, * indicate statistical significance at the 1, 5, and 10 percent levels respectively. The specification isanalogous to Specification (2) from Table 2.7. A firm is classified as large if it operates in ten or more LSAs in1996. All nominal amounts are in 1992 constant dollars.

using two subsamples that respectively exclude small and large firm acquisitions.32 The

results are listed in Table 2.9. Comparing the top and bottom panels, I find qualitatively

similar results for the two sets of estimates, implying that to the extent that scale-based

selection effects exist, they are not driving the general conclusions of my reduced-form