american realty advisors house view: h1 2021

TRANSCRIPT

American Realty Advisors

House View:H1 2021Investment Outlook

American Realty Advisors 2

U.S. Real Estate Investment Outlook H1 2021

Macroeconomic Context

• As expected, the recovery received

a double shot in the arm with the

increased availability of vaccines

and a further round of stimulus

under the Biden administration.

• We expect U.S. GDP to expand by

~6.5% for the year.

• Divergences in the labor recovery

(age, income, education level)

remain a risk; how cities seek to

solve increasing inequalities could

drive policy for decades to come.

Real Estate Markets

• Industrial fundamentals have

continued their fiery streak

unabated, as occupiers continue to

shore up their inventories.

• Except for hotels, distressed real

estate deals in other sectors have

not materialized as some capital

raisers had hoped.

• With a lower return environment

expected across asset classes,

many investors have increased

their target allocations to real

estate.

Images: (Above) Bolstered household finances from the

latest stimulus round are driving a renewed resurgence in

demand for goods. (Below) Companies are beginning to

cautiously call employees back to the office.

Invigorated by policy support and vaccine distribution, the U.S. economy is poised for growth

ARA House View H1 2021

American Realty Advisors 3

While health concerns remain the predominant constraint, many facets of the U.S. recovery are nearing pre-pandemic levels

0

20

40

60

80

100

120

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21

Re

co

ve

ry T

rack

er

Current State of Play

ARA House View H1 2021

Oxford Economics’ National Recovery Tracker examines six dimensions relative to their pre-pandemic state. Each index is calculated as the equal-weighted average of multiple high-frequency indicators.

Source: American Realty Advisors based on data from Oxford Economics as of May 2021

U.S. Recovery Tracker, January 2020 – April 2021 (January 2020 = 100)

Financial

Demand

EmploymentProduction

Overall

Mobility

Health

American Realty Advisors 4

Disparity in recovery for low-wage earners suggests there remains a ways to go to achieving full employment

Employment Backdrop Strengthening, But Not For Everyone

Change in employment rates among workers by wage bracket, January 2020 – March 2021

Note: Percentages reflect employment percentage relative to January 2020 baseline. Data is not seasonally adjusted.

Source: American Realty Advisors based on data from the Opportunity Insights Economic Tracker, Earnin, Intuit, Kronos and Paychex as of April 2021

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

$60k+ $27k-$60K <$27K

• The national unemployment rate

has improved meaningfully from the

14.8% peak recorded in April 2020,

and currently stands at 6.1%.

• Yet gains have been uneven across

the income spectrum.

• Relative to January 2020,

employment among those making

$60K+ was back to pre-pandemic

levels as of March, while those

making less than $27K remained

30% below pre-pandemic levels.

• While many of these roles are

concentrated in services that are

heavily reliant on in-person contact

and thus should return as openings

progress, it will take time to absorb

the slack.

ARA House View H1 2021

American Realty Advisors 5

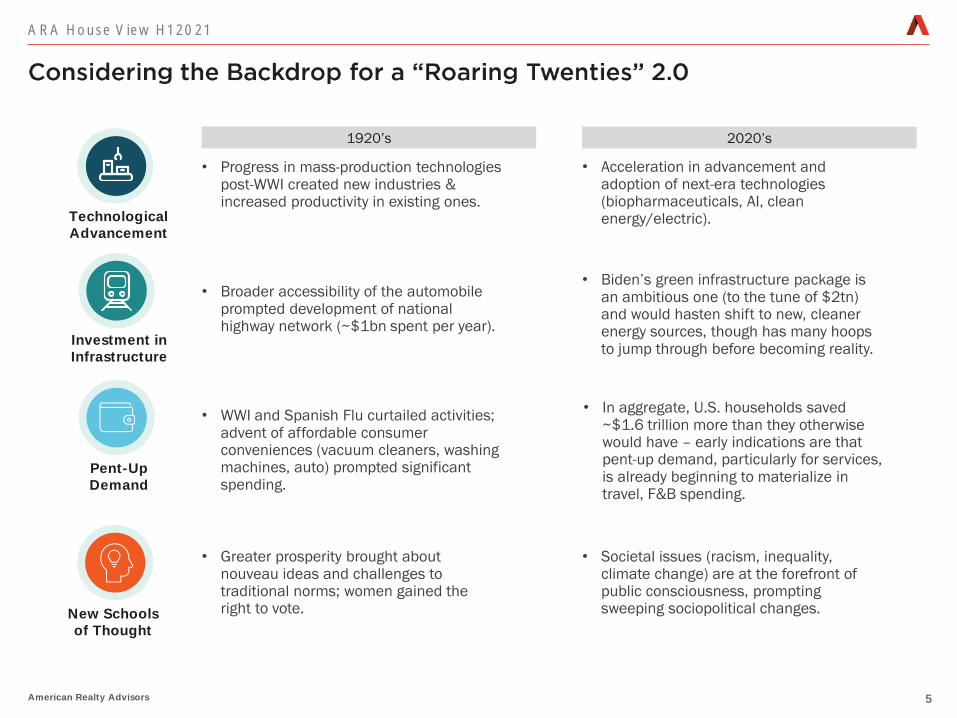

• Progress in mass-production technologies post-WWI created new industries & increased productivity in existing ones.

1920’s 2020’s

Technological Advancement

Investment in Infrastructure

Pent-Up Demand

New Schools of Thought

• Acceleration in advancement and adoption of next-era technologies (biopharmaceuticals, AI, clean energy/electric).

• Broader accessibility of the automobile prompted development of national highway network (~$1bn spent per year).

• Biden’s green infrastructure package is an ambitious one (to the tune of $2tn) and would hasten shift to new, cleaner energy sources, though has many hoops to jump through before becoming reality.

• WWI and Spanish Flu curtailed activities; advent of affordable consumer conveniences (vacuum cleaners, washing machines, auto) prompted significant spending.

• In aggregate, U.S. households saved ~$1.6 trillion more than they otherwise would have – early indications are that pent-up demand, particularly for services, is already beginning to materialize in travel, F&B spending.

• Greater prosperity brought about nouveau ideas and challenges to traditional norms; women gained the right to vote.

• Societal issues (racism, inequality, climate change) are at the forefront of public consciousness, prompting sweeping sociopolitical changes.

ARA House View H1 2021

Capital Markets

American Realty Advisors 7

The recent retreat in long-term Treasury yields suggests bond market investors believe the forthcoming acceleration in inflation will be relatively short-lived

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2.0%

U.S. 10-Year bond yield, January 2020 – May 2021

Source: American Realty Advisors based on data from Macrobond and Oxford Economics as of May 2021

• The unprecedented levels of

stimulus, supply shortages and

surging demand have prompted

some to speculate the U.S. may be

entering a new inflationary period.

• Yet despite what is sure to be higher

inflation in 2021, Treasury yields

have begun to modestly unwind

from their March highs.

• It seems the persistent reinforcing

of the Fed’s new inflation policy

framework is forcing market

participants to back off expectations

of additional rate hikes between

now – 2023.

• We believe inflation to be a

temporary factor over the next 1-2

years but does not present material

downside risk to CRE.

Capital Markets - ARA House View H1 2021

Reading the Tea Leaves on Inflation

American Realty Advisors 8

.Source: American Realty Advisors based on data from CoStar as of May 2021

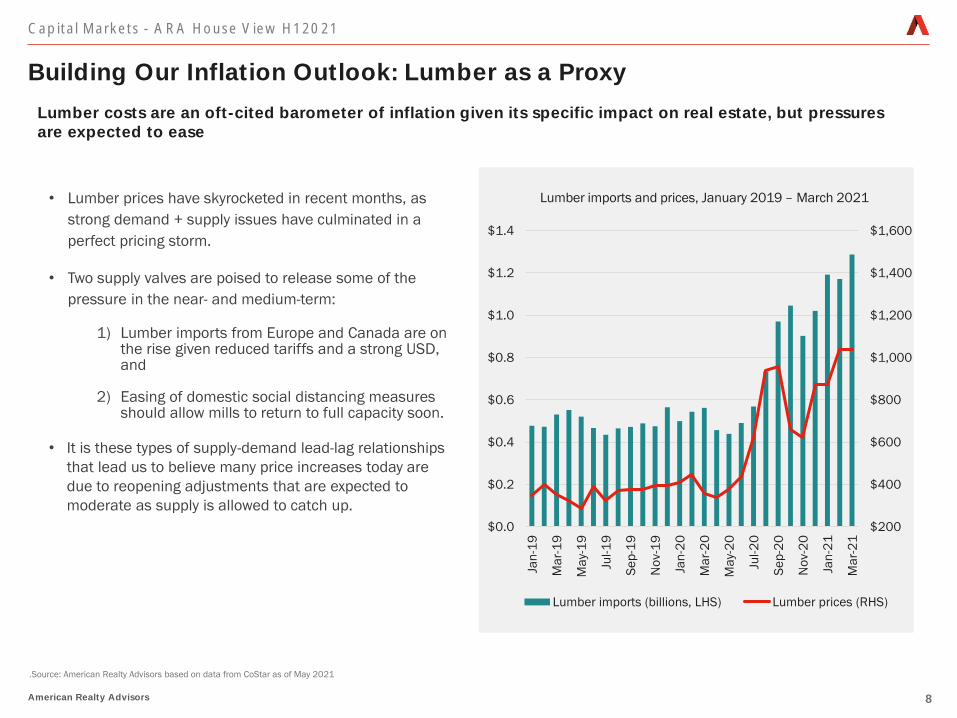

• Lumber prices have skyrocketed in recent months, as

strong demand + supply issues have culminated in a

perfect pricing storm.

• Two supply valves are poised to release some of the

pressure in the near- and medium-term:

1) Lumber imports from Europe and Canada are on the rise given reduced tariffs and a strong USD, and

2) Easing of domestic social distancing measures should allow mills to return to full capacity soon.

• It is these types of supply-demand lead-lag relationships

that lead us to believe many price increases today are

due to reopening adjustments that are expected to

moderate as supply is allowed to catch up.

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

Jan

-19

Ma

r-1

9

Ma

y-1

9

Jul-1

9

Se

p-1

9

No

v-1

9

Jan

-20

Ma

r-2

0

Ma

y-2

0

Jul-2

0

Se

p-2

0

No

v-2

0

Jan

-21

Ma

r-2

1

Lumber imports (billions, LHS) Lumber prices (RHS)

Lumber imports and prices, January 2019 – March 2021

Capital Markets - ARA House View H1 2021

Building Our Inflation Outlook: Lumber as a Proxy

Lumber costs are an oft-cited barometer of inflation given its specific impact on real estate, but pressures are expected to ease

American Realty Advisors 9

Note: Quarterly 10-Year Treasury data reflects the rate at the end of the quarter.

Source: American Realty Advisors based on data from Macrobond and NCREIF as of May 2021

Rolling quarterly U.S. cap rates by property type and 10-Year U.S. Treasury yields, Q1 2000 – Q1 2021 (Q1 2000 = 100)

• Historically there has been the belief that

when interest rates rise, real estate cap rates

increase to account for the added cost to

borrow capital; however, that has not always

been the case.

• In fact, the U.S. 10-Year has had several

bouts of short-term increases that have not

produced a corresponding increase in cap

rates.

• This is because cap rates are influenced not

just by borrowing costs, but by other factors

(capital dry powder, rising demand, reduced

supply) that occur in a rising rate

environment and keep values intact.

0

20

40

60

80

100

120

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Q1

20

17

Q1

20

18

Q1

20

19

Q1

20

20

Q1

20

21

Industrial Apartment Office Retail US10Y

Capital Markets - ARA House View H1 2021

What Impact Could Transitory Inflation Have on Cap Rates?

Real estate cap rates have demonstrated an ability to absorb modest increases in the 10Y in the past

American Realty Advisors 10

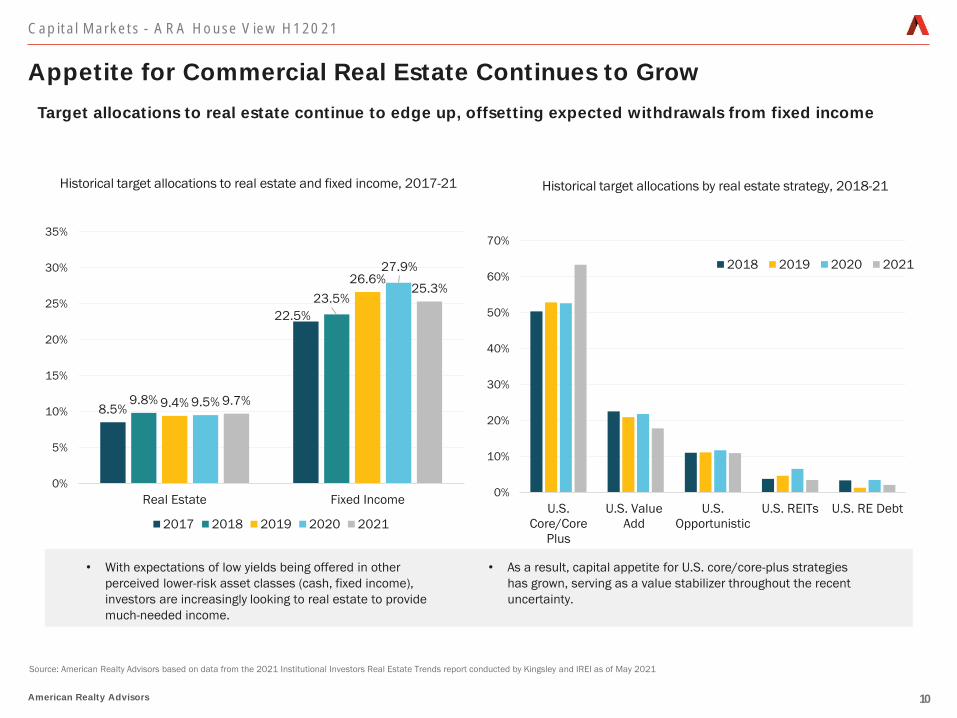

Historical target allocations to real estate and fixed income, 2017-21

Source: American Realty Advisors based on data from the 2021 Institutional Investors Real Estate Trends report conducted by Kingsley and IREI as of May 2021

• With expectations of low yields being offered in other

perceived lower-risk asset classes (cash, fixed income),

investors are increasingly looking to real estate to provide

much-needed income.

8.5%

22.5%

9.8%

23.5%

9.4%

26.6%

9.5%

27.9%

9.7%

25.3%

0%

5%

10%

15%

20%

25%

30%

35%

Real Estate Fixed Income

2017 2018 2019 2020 2021

• As a result, capital appetite for U.S. core/core-plus strategies

has grown, serving as a value stabilizer throughout the recent

uncertainty.

0%

10%

20%

30%

40%

50%

60%

70%

U.S.

Core/Core

Plus

U.S. Value

Add

U.S.

Opportunistic

U.S. REITs U.S. RE Debt

2018 2019 2020 2021

Historical target allocations by real estate strategy, 2018-21

Capital Markets - ARA House View H1 2021

Appetite for Commercial Real Estate Continues to Grow

Target allocations to real estate continue to edge up, offsetting expected withdrawals from fixed income

American Realty Advisors 11

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

14

Q1

14

Q3

15

Q1

15

Q3

16

Q1

16

Q3

17

Q1

17

Q3

18

Q1

18

Q3

19

Q1

19

Q3

20

Q1

20

Q3

21

Q1

Apartment Industrial Office Retail

Note: Data reflects transactions of US $2.5 million and greater and includes individual, portfolio and entity-level transactions.

Source: American Realty Advisors based on data from Real Capital Analytics and Preqin as of May 2021

• After the pause in transaction volumes in Q2/Q3 2020,

volume surged in the fourth quarter as investors sought

opportunities to deploy capital.

• This has had the effect of re-accelerating the pace of

year-over-year price growth across sectors, buoying

values (a phenomenon we anticipated in our H2 2020

House View).

• Given it seems that the lion’s share of fundamental

weakness is behind us and there remains significant dry

powder earmarked for U.S. real estate ($250 billion), we

expect values to continue to rise.

Year-over-year change in RCA CPPI by sector, 1Q 2014 – 1Q 2021

Capital Markets - ARA House View H1 2021

Real Estate Price Growth Continues

Property prices continue to expand, with growth firmly re-accelerating in hardest-hit sectors

American Realty Advisors 12

-15

-10

-5

0

5

10

15

Office Retail Industrial Apartment NPI - All Office Retail Industrial Apartment NPI - All

(%)

ARA Consensus Actual

2020 total return forecasts are based on the November 2020 submission by ARA and the PREA Consensus Survey results. 2021 projections reflect the ARA submission as well as the overall consensus as of the February 2021

survey.

Source: American Realty Advisors based on data from the PREA Consensus Survey, November 2020 and February 2021

Total return forecasts, actual compared to ARA, PREA consensus 2020 and predictions for 2021

2020 2021

Capital Markets - ARA House View H1 2021

Leading With Conviction: The Outlook for Property Type Total Returns

ARA Research forecasts of total returns have been more accurate than the consensus, and suggest there is increasing reason for optimism

Property Markets

American Realty Advisors 14

-15

-10

-5

0

5

10

15

20

25

Industrial Apartment Office Retail

2/3rds of Markets Fall in This Range Index Max Min

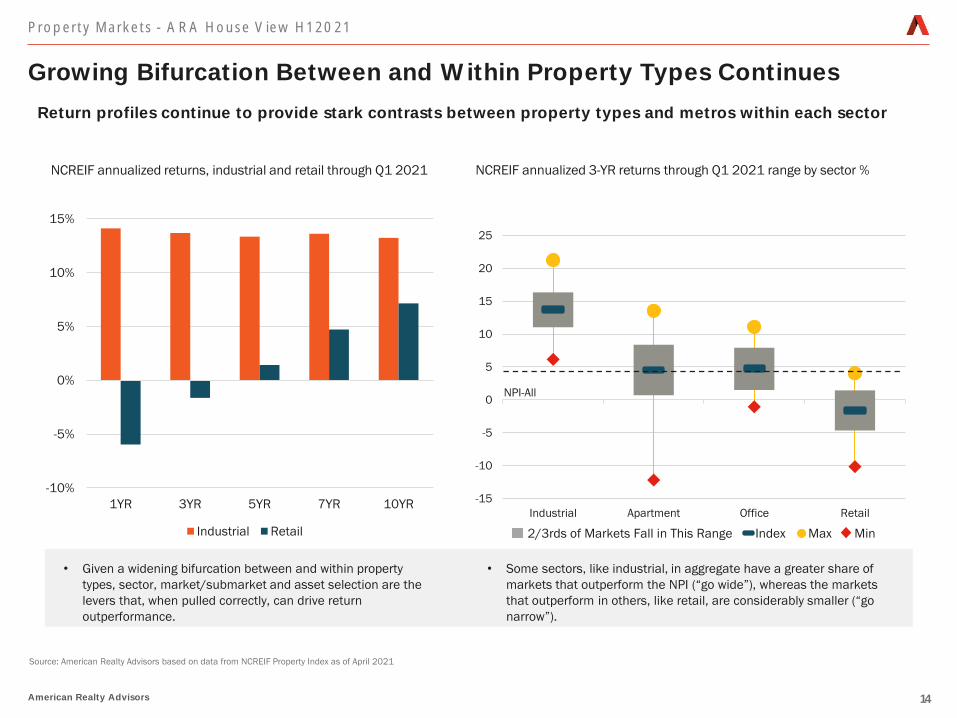

Growing Bifurcation Between and Within Property Types Continues

Source: American Realty Advisors based on data from NCREIF Property Index as of April 2021

-10%

-5%

0%

5%

10%

15%

1YR 3YR 5YR 7YR 10YR

Industrial Retail

NCREIF annualized returns, industrial and retail through Q1 2021 NCREIF annualized 3-YR returns through Q1 2021 range by sector %

• Given a widening bifurcation between and within property

types, sector, market/submarket and asset selection are the

levers that, when pulled correctly, can drive return

outperformance.

• Some sectors, like industrial, in aggregate have a greater share of

markets that outperform the NPI (“go wide”), whereas the markets

that outperform in others, like retail, are considerably smaller (“go

narrow”).

NPI-All

Property Markets - ARA House View H1 2021

Return profiles continue to provide stark contrasts between property types and metros within each sector

American Realty Advisors 15

Pandemic-Spurred Shifts in Supply Chains Boosting Industrial

• The pandemic spurred major

changes in the way consumers

and goods suppliers interact, but

also highlighted the fragility of

“just-in-time” supply chain models.

• As a result, companies are being

forced to re-evaluate their models

with the long term in mind.

• Companies are preparing for

increased demand for online

purchasing, greater supply chain

redundancies and increased near-

shoring, all of which should serve

to boost demand for warehouse

space.

Shifts resulting from the pandemic by % of organizations experiencing the change

and what share believe the changes will/will not stick

Source: American Realty Advisors based on data from McKinsey & Company survey report How COVID-19 has pushed companies over the technology

tipping point – and transformed business forever dated October 2020

% of organizations experiencing change

% who believe change will stick

% who believe change will not stick

Increasing customer

demand for online

purchasing/servicing

Qualification of add’l

suppliers to build

redundancy in supply

chain

Increase in

nearshoring and/or

insourcing practices

62% 21% 15%

53%48%

41%

27% 31% 35%

Property Markets - ARA House View H1 2021

Major shifts during the pandemic are increasingly likely to stick through the recovery, creating further tailwinds for the industrial sector

American Realty Advisors 16

Property Markets - ARA House View H1 2021

Balancing Price and Growth

Estimated current market cap rate compared to ARA research 5-year rent growth forecast

Note: Estimated market cap rates are based on CBRE-EA estimates as of Q4 2020, adjusted downward by 50 bps to account for actual transaction cap rates.

Source: American Realty Advisors based on data from CBRE-EA and CoStar as of May 2021

ATL

AUS

BALT

BOS

CHT

CHI COLUM

DFWDEN

OAK

FLL

HOU

INDY

IE

KC

LA

MEM

MIA

MSP

NASH

NY

NNJOC

ORL

PHL

PHX

PORTRAL

SLC

SAN ANT

SD

SEA

SJ

STL

TAM

DC

WPB

1%

2%

3%

4%

5%

6%

7%

3.0% 3.5% 4.0% 4.5% 5.0% 5.5%

AR

A R

ese

arc

h 5

-Ye

ar

Re

nt

Gro

wth

CA

GR

Fo

reca

st

(20

21

-25

)

Estimated current market cap rate

• Industrial cap rates continue to compress

given the seemingly insatiable investor and

occupier demand.

• While the outlook for the sector remains

robust, investors should hedge going-in

pricing relative to prospects for future rental

rate growth.

• At a 3.37% rent growth CAGR, a going-in cap

rate of 4.6% in Indianapolis is relatively less

appealing than a 4.5% cap rate in Atlanta

with a 4.8% rent growth CAGR – so market

selection, even in a hot sector, is still key.

Highly infill

markets with

high rent

growth

potential

Most attractive combination of

pricing and rent growth potential

Primarily a

yield play

With industrial a key sector focus for many, pricing relative to growth continues to be a critical lens

American Realty Advisors 17

Atlanta

Austin

Charleston

Charlotte

Columbus

Dallas

Denver

Miami

Tampa

West Palm Beach

Orlando

Houston Jacksonville

Las Vegas

Nashville

Phoenix

Portland

RaleighReno

Inland Empire

Sacramento

Salt Lake City

San Antonio Seattle

1%

2%

3%

4%

5%

6%

7%

8%

9%

15% 20% 25% 30% 35% 40% 45%

5-Yr Cumulative Supply as % of Inventory

Multifamily Market Selection: Measuring Migration (and Supply)

Source: American Realty Advisors based on data from CoStar and ARA proprietary forecasts as of May 2021

• There continues to be significant capital pursuing multifamily

deals in Sun Belt/ “Smile” markets as investors follow renters

south and west; yet not all these metros are created equal.

• We prefer a strategy that is focused primarily on those markets

that have a supportive combination of both high in-migration and

relatively less supply growth (like Austin, Phoenix and Raleigh), with

a narrower focus in markets where market-level supply is expected

to be higher.

21-25 Avg. Rent Growth

<2%

2-3%

3%+

Property Markets - ARA House View H1 2021

The magnitude of in-

Cu

mu

lati

ve N

et

Mig

rati

on

20

21

-25

as %

of

Cu

rre

nt

Po

pu

lati

on

American Realty Advisors 18

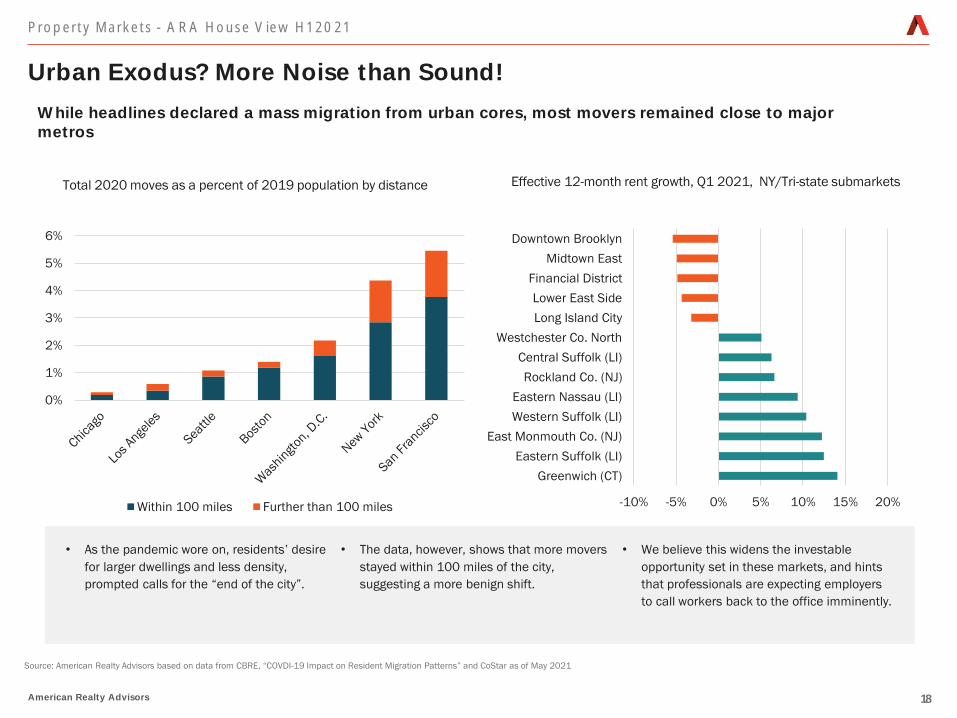

Urban Exodus? More Noise than Sound!

Source: American Realty Advisors based on data from CBRE, “COVDI-19 Impact on Resident Migration Patterns” and CoStar as of May 2021

Total 2020 moves as a percent of 2019 population by distance

0%

1%

2%

3%

4%

5%

6%

Within 100 miles Further than 100 miles

• As the pandemic wore on, residents’ desire

for larger dwellings and less density,

prompted calls for the “end of the city”.

• The data, however, shows that more movers

stayed within 100 miles of the city,

suggesting a more benign shift.

• We believe this widens the investable

opportunity set in these markets, and hints

that professionals are expecting employers

to call workers back to the office imminently.

-10% -5% 0% 5% 10% 15% 20%

Greenwich (CT)

Eastern Suffolk (LI)

East Monmouth Co. (NJ)

Western Suffolk (LI)

Eastern Nassau (LI)

Rockland Co. (NJ)

Central Suffolk (LI)

Westchester Co. North

Long Island City

Lower East Side

Financial District

Midtown East

Downtown Brooklyn

Effective 12-month rent growth, Q1 2021, NY/Tri-state submarkets

Property Markets - ARA House View H1 2021

While headlines declared a mass migration from urban cores, most movers remained close to major metros

American Realty Advisors 19

Office Opportunities Beyond the Tech Heavyweights

• Many office strategies over the last

cycle have been centered on

Innovation Hubs, with investors

focused on capturing the growth

from tech demand.

• Yet markets primarily driven by firms

seeking lower cost structures have

also offered a compelling total

return profile.

• Markets in this category (such as

Atlanta and Charlotte) consistently

lead the pack, frequently beating

out NPI-Office and NPI-All returns.

• While helpful in crafting thematic

strategies, these groupings can

mask meaningful variation in

performance even within the same

set – so market (and asset)

selection is key.

-1%

1%

3%

5%

7%

9%

1YR 3YR 5YR 7YR

Innovation Hubs Traditional Tenancies Competitive Costs

Value-weighted aggregate total returns of office markets by primary driver through Q1 2021

Innovation hubs are markets where tech/biotech/creative are larger share of office-using employment growth than the national average. Traditional tenancy

markets are those where FIRE employment growth represents a larger share of office-using employment growth than the national average. Competitive costs

are markets with growth in a variety of office-using employment sectors with strong in-migration.

Source: American Realty Advisors based on data from NCREIF as of May 2021

NPI-Office NPI-All

Property Markets - ARA House View H1 2021

Lower-cost office markets may also offer a compelling return profile

American Realty Advisors 20

Offices: The Best and the Rest

.Source: American Realty Advisors based on data from CoStar as of May 2021

• The pandemic has reinforced bifurcations in

performance between and within sectors, with the best

doing better and the rest falling further behind.

• Knowing which assets have the staying power to

continue to be “the best” then is critical to creating

outperformance.

• Office assets that are currently highly-leased historically

retain their elevated occupancy levels; however, this

same persistency in performance is also true at the

bottom, as buildings with occupancy below 75% today

have seen a sharp erosion since 2014 that looks to be

accelerating.

• Investors should aim to purchase only best-in-class

office assets, which provide steadier demand

performance, or acquire office product that lends itself

to top-tier repositioning plays.

52%

57%

62%

67%

72%

77%

82%

87%

92%

97%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

95%-100% 90%-95% 85%-90%

80%-85% 75%-80% 75% & Below

Office occupancy by current occupancy profile, 2000-2020

Property Markets - ARA House View H1 2021

There seems to exist a persistency in office occupancy for best-in-slippery slope

American Realty Advisors 21

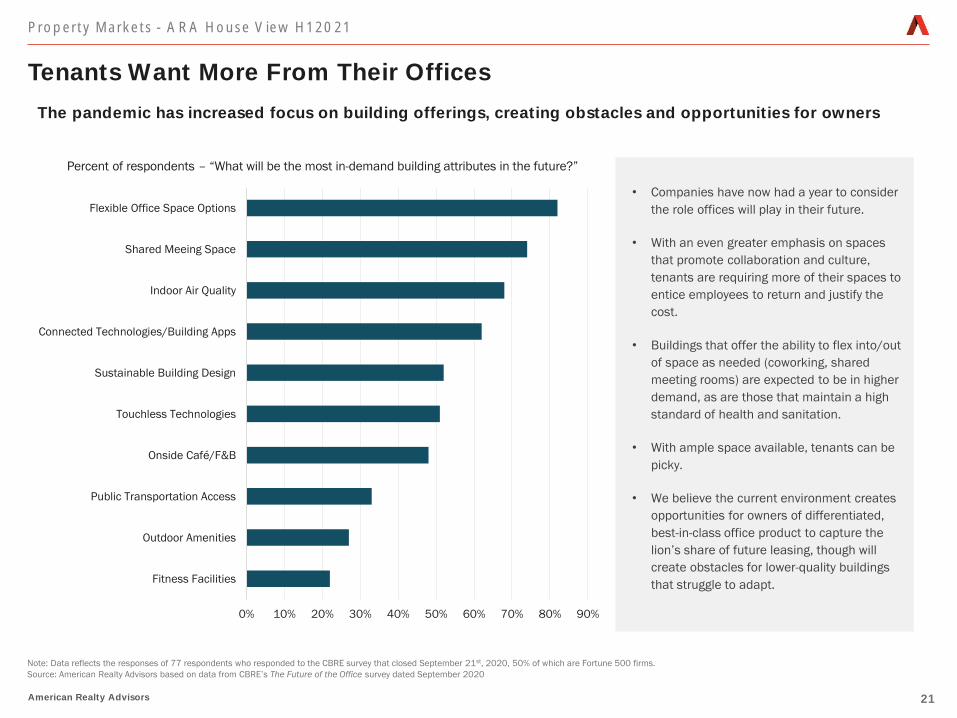

Percent of respondents – “What will be the most in-demand building attributes in the future?”

• Companies have now had a year to consider

the role offices will play in their future.

• With an even greater emphasis on spaces

that promote collaboration and culture,

tenants are requiring more of their spaces to

entice employees to return and justify the

cost.

• Buildings that offer the ability to flex into/out

of space as needed (coworking, shared

meeting rooms) are expected to be in higher

demand, as are those that maintain a high

standard of health and sanitation.

• With ample space available, tenants can be

picky.

• We believe the current environment creates

opportunities for owners of differentiated,

best-in-class office product to capture the

lion’s share of future leasing, though will

create obstacles for lower-quality buildings

that struggle to adapt.

Tenants Want More From Their Offices

Note: Data reflects the responses of 77 respondents who responded to the CBRE survey that closed September 21st, 2020, 50% of which are Fortune 500 firms.

Source: American Realty Advisors based on data from CBRE’s The Future of the Office survey dated September 2020

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Flexible Office Space Options

Shared Meeing Space

Indoor Air Quality

Connected Technologies/Building Apps

Sustainable Building Design

Touchless Technologies

Onside Café/F&B

Public Transportation Access

Outdoor Amenities

Fitness Facilities

Property Markets - ARA House View H1 2021

The pandemic has increased focus on building offerings, creating obstacles and opportunities for owners

American Realty Advisors 22

Selecting a Specialty Sector: Why We Favor Single-Family Rentals

.

Source: American Realty Advisors based on data from Real Capital Analytics, NCREIF, John Burns Real Estate Consulting and CoStar as of May 2021

Property Markets - ARA House View H1 2021

Confluence of strong foundational demand + cyclical cost elements + potential for cap rate compression-driven appreciation makes SFR an increasingly attractive complement to our existing residential strategies

Millennials getting

married, having

children (4.7MM)

Downsizing Baby

Boomers (4MM)

COVID fuels

demand for

outdoor space

Limited for-sale

availability driving

rapid home price

appreciation

Student loan burdens, disadvantaged

earnings potential post-GFC and pandemic

prevent would-be buyers from being able to

sufficiently save for a down payment

Construction, land prices

rising (rents trend higher

to account for costs)

Significant capital appetite for the

space, yet institutional penetration

in segment still early innings (~2%)

creates ability to ride capital

compression wave.

Investment Case for Single-Family Rentals

American Realty Advisors 23

Industrial

• Increase in domestic

stockpiling will further

increase demand in the

“too-hot-to-stop” sector.

• Demand for industrial

assets in infill locations will

continue to expand as

growing e-commerce market

heightens need for last-mile

logistics centers.

Multi-Family

• As cities retained the lion’s

share of their residents,

landlords are expected to be

able to recoup pandemic-

induced concessions.

• Sun Belt strategies should

target cities with high in-

migration and low incoming

supply, which are likely to

offer the strongest return

opportunities.

Office

• Migration trends show most

workers expect to return to

the office, indicating WFH

may be less disruptive in the

long term.

• Best-in-class assets will

remain in high demand as

quality considerations

evolve to encompass

sanitation and space

flexibility.

Retail

• Retailers will receive a boost

as vaccination efforts and

better weather allow officials to

ease business restrictions.

• With the personal savings rate

still significantly exceeding pre-

pandemic levels, consumers

are well equipped to act on

pent-up demand this summer,

particularly for services.

Outlook for Property Sectors

• Though SFR received a boost from the pandemic, demand is expected

to persist long term as the segment fulfills the needs and wants of

both downsizing Baby Boomers and upgrading Millennials.

• Investors will look toward build-for-rent neighborhoods as opposed to

scattered purchasing strategies, as management of contiguous

communities more closely mirrors that of traditional multi-family.

With post-pandemic optimism on the rise, opportunities are beginning to emerge in all real estate sectors.

Single-Family Rental

Property Markets - ARA House View H1 2021

American Realty Advisors 24

Implications for Core and Value-Add Strategies

Core • Increase leasing rates in industrial and

residential to drive income growth while

continuing to “blend and extend” office

and retail tenants.

• Control operating/capital costs and

focus on re-engaging building services

and tenant amenities for occupancy

ramp up in 2H 2021.

• Timely executive renovation and

development business plans for

residential and industrial assets to meet

robust tenant demand.

• Continue to focus on leasing strategies for

office/retail to increase occupancy,

extend WALT and drive cash flow.

• Remain flexible and responsive to

disposition opportunities where high

buyer demand results in pricing premium.

• Wide market focus on outperforming

sectors, highly selective in others where

strike zone for outperformance is

narrower.

• Pivot office offerings to capture stronger

life science demand.

• Add purpose-built single-family rental

communities in high-growth markets as

diversifier in residential allocation.

• Build, lease and sell stabilized single-

family rental projects into deep capital

pool.

• Move contrarian to office uncertainty for

assets that have the potential to be

best-in-class.

• Industrial demand expected to increase

by 850 million sf by 2023, continue to

pursue development/lease-up plays.

Asset Management Portfolio Construction

Value-Add

Portfolio Implications - ARA House View H1 2021

quality photo

American Realty Advisors 25American Realty Advisors

The pandemic era

has intensified

existing trends,

reinforcing

bifurcations between

relative winners and

losers.

Summary and Strategy Implications

• The U.S. economy’s recovery in the first half of 2021 was stronger

than we originally anticipated, enhanced by an accelerated vaccine

distribution and further governmental stimulus.

• We expect full-year 2021 to be one of the strongest for GDP growth

in recent memory, with a period of above-trend growth for 1-2 more

years.

• While this should serve to boost real estate fundamentals overall,

we believe the pace of structural change has been accelerated,

widening the performance gap between and within sectors.

• Pricing and fundamentals may send opposing signals of where the

opportunities lie; which to pursue depends on strategy (core vs.

value-add) and hold period.

• Though the current backdrop is not without risks, we are focused on

orienting our assets to best capitalize on accelerating

fundamentals' momentum and identifying mispriced opportunities

that offer enhanced return potential.

American Realty Advisors 26

Disclaimer: The information in this presentation is as of June 3, 2021 unless specified otherwise and is for your informational and educational purposes only, is not intended to be relied on to make

any investment decisions, and is neither an offer to sell nor a solicitation of an offer to buy any securities or financial instruments in any jurisdiction. This presentation expresses the views of American

Realty Advisors, LLC ("ARA") as of the date indicated and such views are subject to change without notice. The information in this presentation has been obtained or derived from sources believed by

ARA to be reliable but ARA does not represent that this information is accurate or complete and has not independently verified the accuracy or completeness of such information or assumptions on

which such information is based. Models used in any analysis may be proprietary, making the results difficult for any third party to reproduce. Past performance of any kind referenced in the information

above in connection with any particular strategy should not be taken as an indicator of future results of such strategies. It is important to understand that investments of the type referenced in the

information above pose the potential for loss of capital over any time period. This presentation is proprietary to ARA and may not be copied, reproduced, republished, or posted in whole or in part, in any

form and may not be circulated or redelivered to any person without the prior written consent of ARA. Photos used in this presentation were selected based on visual appearance, are used for illustrative

purposes only, are not necessarily reflective of all the investments made by ARA or which ARA may make in the future.

Forward-Looking Statement: This presentation contains forward-looking statements within the meaning of federal securities laws. Forward-looking statements are statements that do not

represent historical facts and are based on our beliefs, assumptions made by us, and information currently available to us. Forward-looking statements in this newsletter are based on our current

expectations as of the date of this presentation, which could change or not materialize as expected. Actual results may differ materially due to a variety of uncertainties and risk factors. Except as

required by law, ARA assumes no obligation to update any such forward-looking statements.

Disclosures

ARA House View H1 2021

Jay ButterfieldExecutive Managing Director,

Head of Business Development

213.233.5743

Sabrina UngerManaging Director,

Research & Strategy

213.233.5846

Britteni LupeAnalyst,

Research & Strategy

213.233.5780

Printed in-house

Headquarters Office 515 S. Flower St.

49th Floor

Los Angeles, CA 90071

T 213.233.5700F 213.947.1480

LOS ANGELES | CHICAGO | NEW YORK | ORLANDO | PHILADELPHIA | SAN FRANCISCO

For More Information, Please Contact: