alumetal group h1 2016 financial results · 18th july 2016 beginning of purchase and preparation of...

TRANSCRIPT

19th August 2016

Alumetal Group

H1 2016 financial results

H1 2016 and LTM at glance

Volume sales – 83k tons in H1 2016 and 161k tons in LTM

EBITDA – PLN 67 mn in H1 2016 and PLN 126 mn in LTM

Net profit – PLN 55 mn in H1 2016 and PLN 102 mn in LTM

Operational cash flow – PLN 72 mn in H1 2016 and PLN 147 mn in LTM

Payment of dividend – PLN 39 mn on 7th June 2016

Net debt – PLN 79 mn (0,6xEBITDA)

Motor vehicle registrations in the EU in thou. units

In H1 2016 motor vehicles registrations in the UE increased by 8,8% yoy, of which passagnercars (PC) sales increased by 9,4% and commercial vehicles (CV) sales went up by 13,5%

In LTM sale volume of motor vehicles in UE increased by 10,2% yoy to the level of 16,6 mnunits (9,8% increase in PC and 12,8% increase in CV)

9%

5%

6% 4%

9%

8%

10% 11%

9%

-

500 000

1 000 000

1 500 000

2 000 000

2 500 000

3 000 000

3 500 000

4 000 000

4 500 000

5 000 000

1q'13 1q'14 2q'13 2q'14 3q'13 3q'14 4q'13 4q'14 1q'14 1q '15 2q'14 2q'15 3q'14 3q'15 4q '14 4q '15 1q '15 1q '16 2q '15 2q '16

CV PC

11%

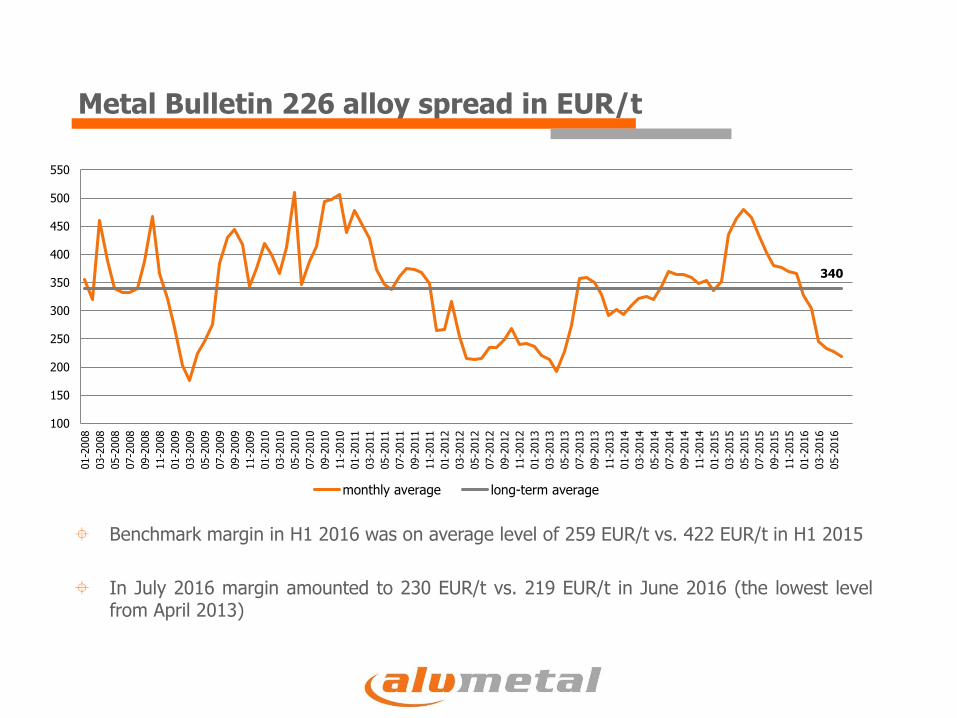

Metal Bulletin 226 alloy spread in EUR/t

Benchmark margin in H1 2016 was on average level of 259 EUR/t vs. 422 EUR/t in H1 2015

In July 2016 margin amounted to 230 EUR/t vs. 219 EUR/t in June 2016 (the lowest levelfrom April 2013)

340

100

150

200

250

300

350

400

450

500

550

01-2

008

03-2

008

05-2

008

07-2

008

09-2

008

11-2

008

01-2

009

03-2

009

05-2

009

07-2

009

09-2

009

11-2

009

01-2

010

03-2

010

05-2

010

07-2

010

09-2

010

11-2

010

01-2

011

03-2

011

05-2

011

07-2

011

09-2

011

11-2

011

01-2

012

03-2

012

05-2

012

07-2

012

09-2

012

11-2

012

01-2

013

03-2

013

05-2

013

07-2

013

09-2

013

11-2

013

01-2

014

03-2

014

05-2

014

07-2

014

09-2

014

11-2

014

01-2

015

03-2

015

05-2

015

07-2

015

09-2

015

11-2

015

01-2

016

03-2

016

05-2

016

monthly average long-term average

Volume sales in thou. tons

In H1 2016 sales volume decreased by 5% yoy to 83 thou. tons

In LTM sales volume amounted to 161 thou. tons which is 2% decrease in comparison to2015

41,3 40,2

86,7

82,6

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

100,0

2Q'15 2Q'16 1H'15 1H'16

88,1

99,4

126,9

156,1164,8

160,8

-

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

180,0

2011 2012 2013 2014 2015 LTM

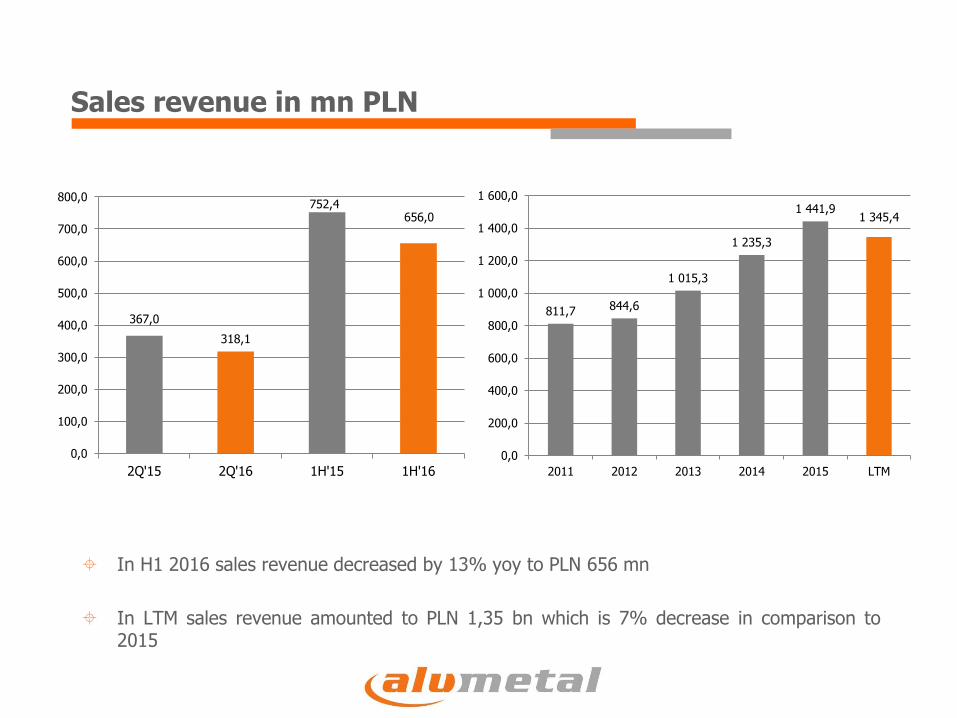

Sales revenue in mn PLN

In H1 2016 sales revenue decreased by 13% yoy to PLN 656 mn

In LTM sales revenue amounted to PLN 1,35 bn which is 7% decrease in comparison to2015

367,0

318,1

752,4656,0

0,0

100,0

200,0

300,0

400,0

500,0

600,0

700,0

800,0

2Q'15 2Q'16 1H'15 1H'16

811,7 844,6

1 015,3

1 235,3

1 441,91 345,4

0,0

200,0

400,0

600,0

800,0

1 000,0

1 200,0

1 400,0

1 600,0

2011 2012 2013 2014 2015 LTM

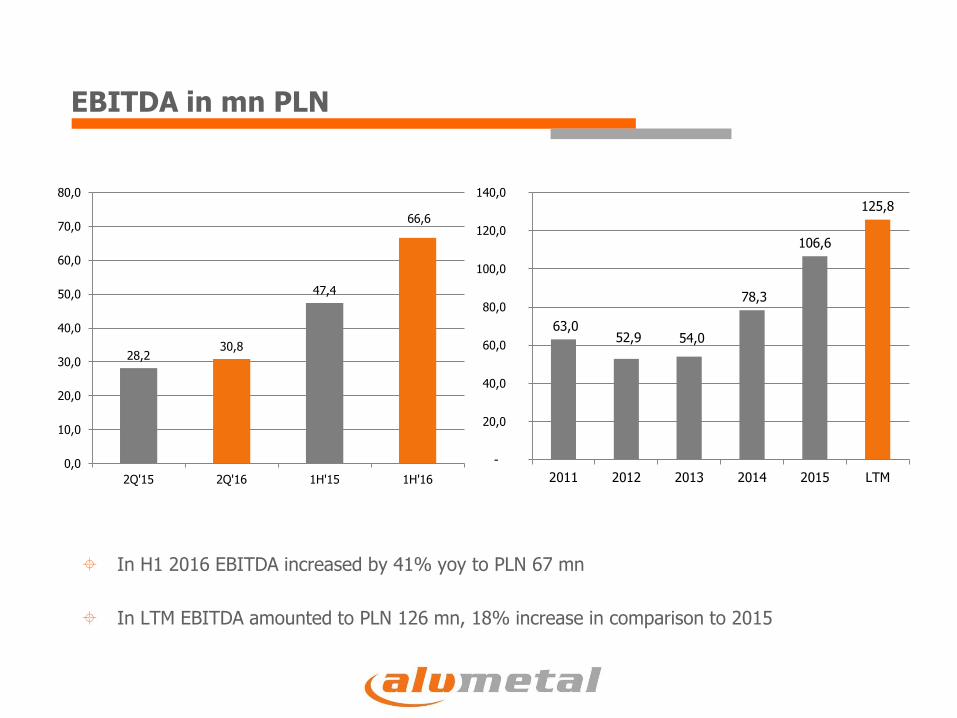

EBITDA in mn PLN

In H1 2016 EBITDA increased by 41% yoy to PLN 67 mn

In LTM EBITDA amounted to PLN 126 mn, 18% increase in comparison to 2015

28,230,8

47,4

66,6

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

2Q'15 2Q'16 1H'15 1H'16

63,0 52,9 54,0

78,3

106,6

125,8

-

20,0

40,0

60,0

80,0

100,0

120,0

140,0

2011 2012 2013 2014 2015 LTM

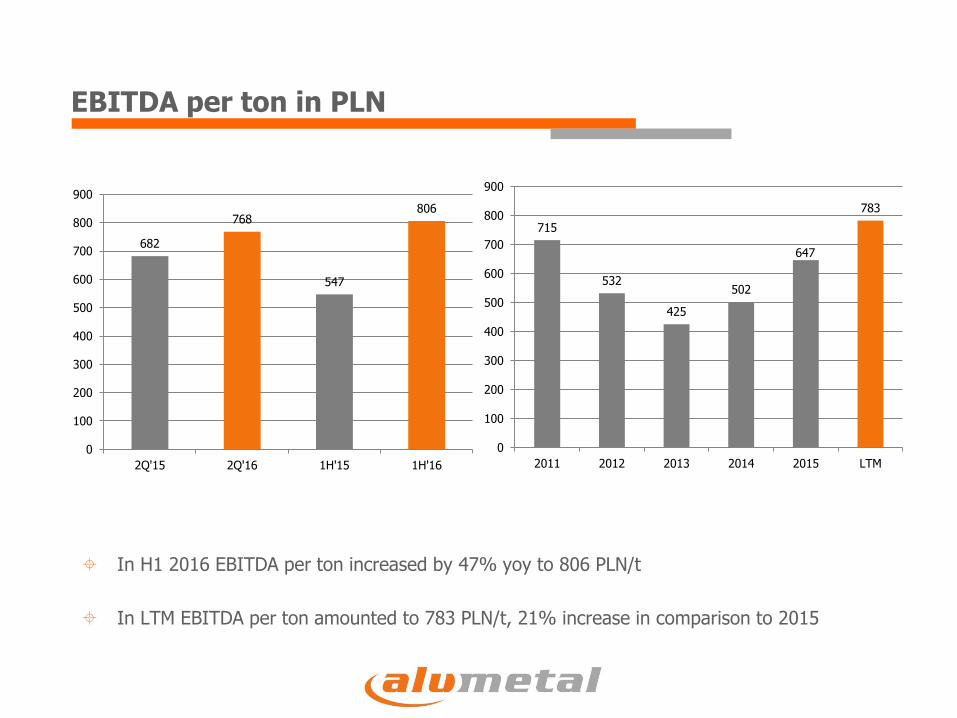

EBITDA per ton in PLN

In H1 2016 EBITDA per ton increased by 47% yoy to 806 PLN/t

In LTM EBITDA per ton amounted to 783 PLN/t, 21% increase in comparison to 2015

682

768

547

806

0

100

200

300

400

500

600

700

800

900

2Q'15 2Q'16 1H'15 1H'16

715

532

425

502

647

783

0

100

200

300

400

500

600

700

800

900

2011 2012 2013 2014 2015 LTM

Net profit in mn PLN

In H1 2016 net profit increased by 76% yoy to PLN 55 mn

In LTM net profit amounted to PLN 102 mn, 31% increase in comparison to 2015

21,6

26,631,4

55,3

0,0

10,0

20,0

30,0

40,0

50,0

60,0

2Q'15 2Q'16 1H'15 1H'16

43,9

34,5 35,8

58,9

77,7

101,5

-

20,0

40,0

60,0

80,0

100,0

120,0

2011 2012 2013 2014 2015 LTM

The impact of one-off events on financial results (thou. PLN)

1Q’15 2Q’15 3Q’15 4Q’15 2015 1Q’16 2Q’16 LTM

Valuation of management option scheme and annual bonus for achieving higher than budgeted results

-1 205 - 265 - 381 - 1 614 -3 465 -394 -130 -2 519

Impairment write-down of equipment - 867 -867 -867

Net impairment write-down of receivables from entities undergoing corporate recovery proceedings

-7 329 -7 329 366 -6 963

Impact on EBITDA -1 205 -265 -381 -9 810 -11 660 -394 236 -10 349

Income tax 774 774 -70 704

Impact on net profit -1 205 -265 -381 -9 037 -10 887 -394 167 -9 644

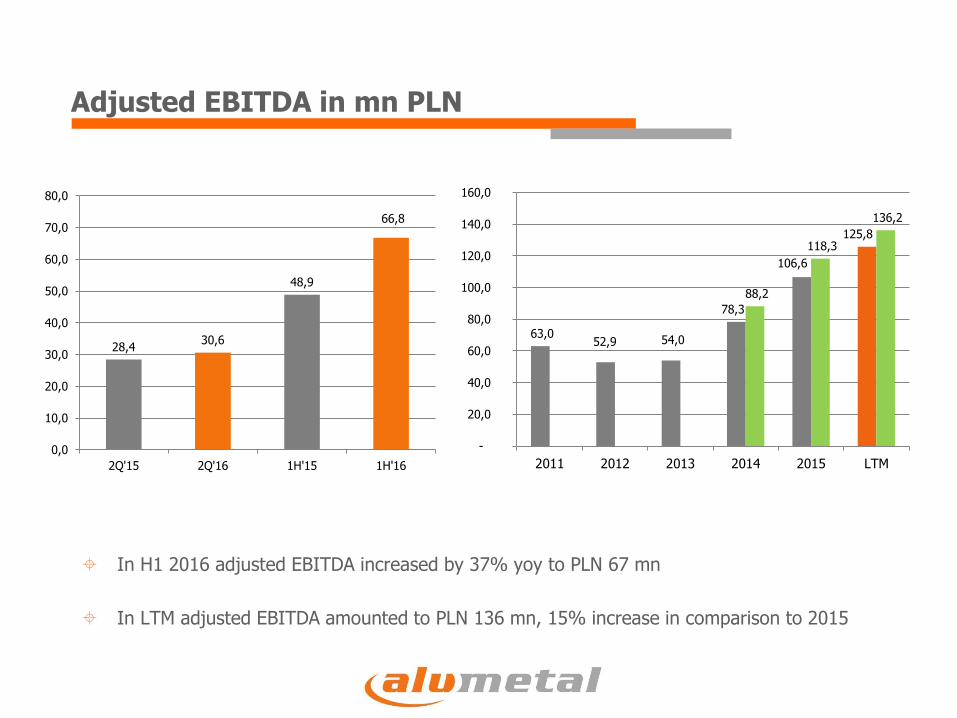

In H1 2016 adjusted EBITDA increased by 37% yoy to PLN 67 mn

In LTM adjusted EBITDA amounted to PLN 136 mn, 15% increase in comparison to 2015

Adjusted EBITDA in mn PLN

28,430,6

48,9

66,8

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

2Q'15 2Q'16 1H'15 1H'16

63,0 52,9 54,0

78,3

106,6

125,8

88,2

118,3

136,2

-

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

2011 2012 2013 2014 2015 LTM

In H1 2016 adjusted EBITDA per ton increased by 43% yoy to 808 PLN/t

In LTM adjusted EBITDA per ton amounted to 847 PLN/t, 18% increase in comparison to 2015

Adjusted EBITDA per ton in PLN

689

762

564

808

0

100

200

300

400

500

600

700

800

900

2Q'15 2Q'16 1H'15 1H'16

715

532

425

502

647

783

565

718

847

0

100

200

300

400

500

600

700

800

900

1 000

2011 2012 2013 2014 2015 LTM

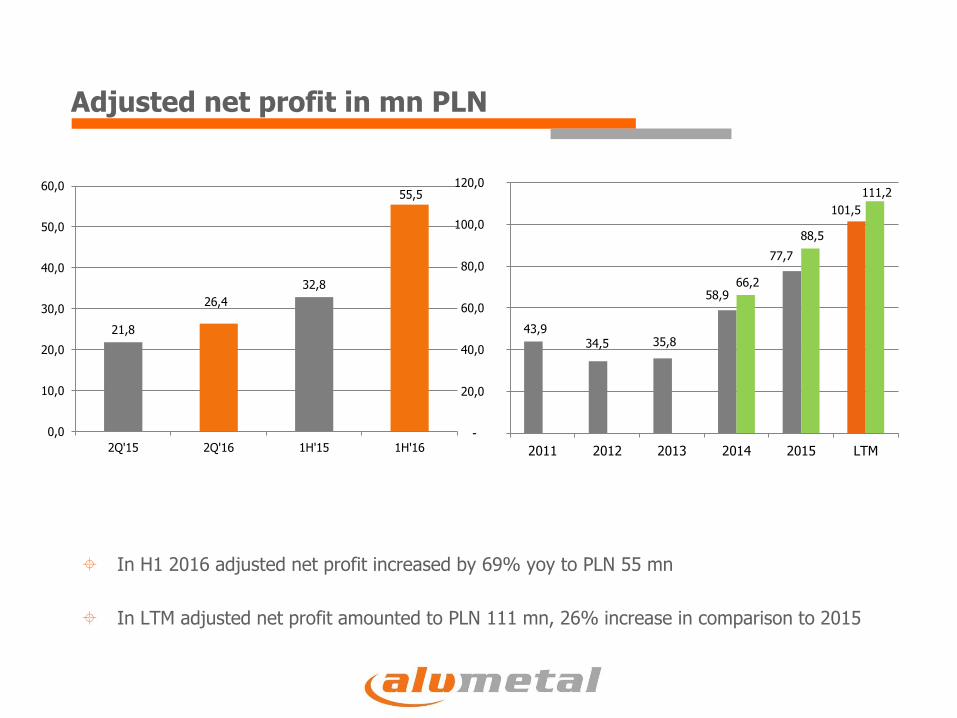

Adjusted net profit in mn PLN

In H1 2016 adjusted net profit increased by 69% yoy to PLN 55 mn

In LTM adjusted net profit amounted to PLN 111 mn, 26% increase in comparison to 2015

21,8

26,4

32,8

55,5

0,0

10,0

20,0

30,0

40,0

50,0

60,0

2Q'15 2Q'16 1H'15 1H'16

43,9 34,5 35,8

58,9

77,7

101,5

66,2

88,5

111,2

-

20,0

40,0

60,0

80,0

100,0

120,0

2011 2012 2013 2014 2015 LTM

Capex in mn PLN

In H1 2016 capex amounted to PLN 67 mn

PLN 3,8 mn maintenance capex

PLN 2,5 mn metal management

PLN 61,1 mn product mix/ production capacity increase (project in Hungary)

In LTM capex amounted to PLN 104 mn which is 121% higher than in 2015

* including cash credited to the account of the collateral manager (construction trustee service)

6,0

41,7

10,2

67,4*

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

2Q'15 2Q'16 1H'15 1H'16

64,2

38,6 33,5

10,8

47,3*

104,4

-

20,0

40,0

60,0

80,0

100,0

120,0

2011 2012 2013 2014 2015 LTM

*

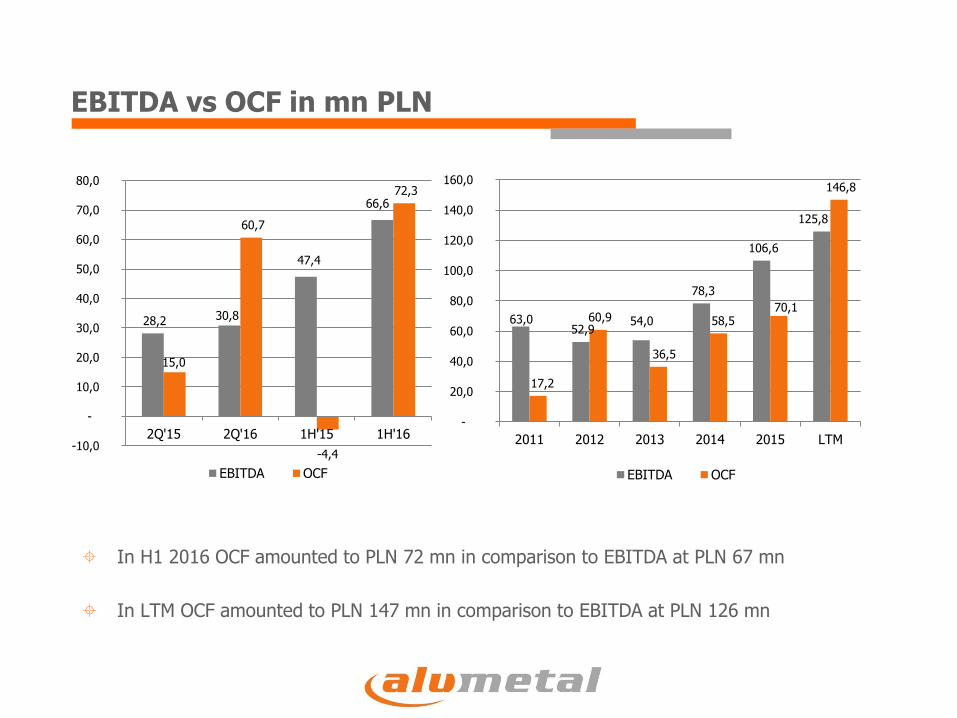

EBITDA vs OCF in mn PLN

In H1 2016 OCF amounted to PLN 72 mn in comparison to EBITDA at PLN 67 mn

In LTM OCF amounted to PLN 147 mn in comparison to EBITDA at PLN 126 mn

28,2 30,8

47,4

66,6

15,0

60,7

-4,4

72,3

-10,0

-

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

2Q'15 2Q'16 1H'15 1H'16

EBITDA OCF

63,0 52,9

54,0

78,3

106,6

125,8

17,2

60,9

36,5

58,5 70,1

146,8

-

20,0

40,0

60,0

80,0

100,0

120,0

140,0

160,0

2011 2012 2013 2014 2015 LTM

EBITDA OCF

Net debt and effective CIT rate

Net debt Effective CIT rate

At the end of H1 2016 net debt amounted to PLN 79 mn and Net debt/EBITDA ratioincreased from 0,4 at the end of 2015 to 0,6 at the end of June 2016

Effective CIT rate in H1 2016 amounted to 3,3%

112,1

72,1 70,2

45,4 46,7

79,1

1,8

1,41,3

0,6

0,4

0,6

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2,0

0,0

20,0

40,0

60,0

80,0

100,0

120,0

2011 2012 2013 2014 2015 1H2016

12,3%

7,8%

1,7%

1,1%

3,2% 3,3%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

14,0%

2011 2012 2013 2014 2015 1H'16

Current status of Hungarian project

18th April 2016 first application for reimbursement of part of the capex was filed to HIPA,accepted on 4th August, payment expected in September

8th July 2016 second application for reimbursement of part of the capex was filed to HIPA

18th July 2016 beginning of purchase and preparation of scrap

5th August 2016 plant usage permit obtained

Completion of costruction works, the current progress of assembly works at 85%

Launching first production line after obtaining neccessary permits

The process of recruitment and training of employees is in progress

The project is on time, capex 2-4% above the budget

Development of infrastructure, purchase and installation of equipment technology – at leastdoubling the production capacity (currently 7 thous. tons)

Launching new production technology of master alloys

The extension of the product portfolio

Strengthen the Alumetal Group's position on the European market, expansion into newmarkets

Capex at max PLN 58,5 mn, financing from own resources, CIT allowance

Capex payment in 2016-2018 (mostly in 2017)

Commencement of production in 2Q 2018

Expansion of Master Alloys

Summary

In H1 2016 very good financial results, despite lower sales volume and highpressure on margins on some alloys kinds – financial results in line with theManagement Board expectations

Continuous favorable market environment in regards to demand for secondaryaluminium alloys – high growth of motor vehicle sale in UE

Management believes in achievement of the financial targets required to excercisethe third tranche of the managerial option scheme (increase of EBITDA and netprofit per share in 2016 by at least 10%) – H1 2016 financial result is a very goodbase to realize goals

Realization of dividend policy (50% of net profit) – dividend payment on 7th June2016

The Hungarian project is on time with small capex overrun