alterra capital partners,...

TRANSCRIPT

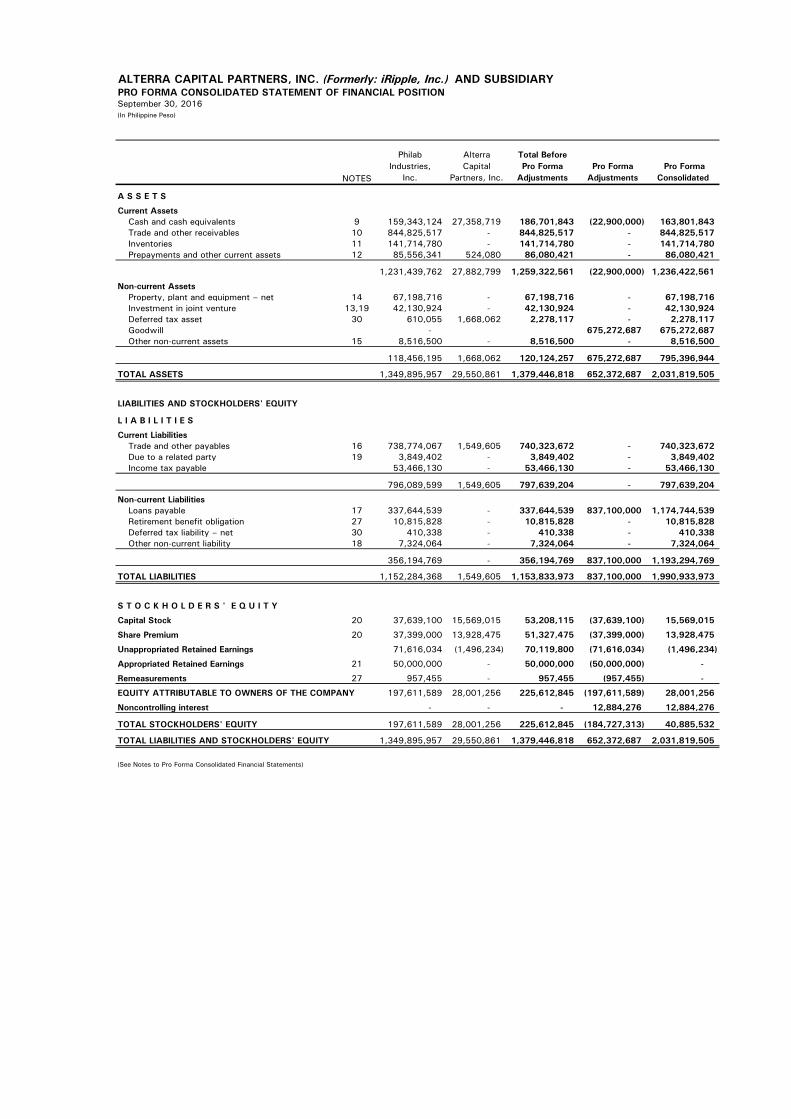

ALTERRA CAPITAL PARTNERS, INC. (Formerly: iRipple, Inc.) AND SUBSIDIARYPRO FORMA CONSOLIDATED STATEMENT OF FINANCIAL POSITIONSeptember 30, 2016(In Philippine Peso)

NOTES

Philab Industries,

Inc.

Alterra Capital

Partners, Inc.

Total Before Pro Forma

AdjustmentsPro Forma

Adjustments Pro Forma

Consolidated

A S S E T S

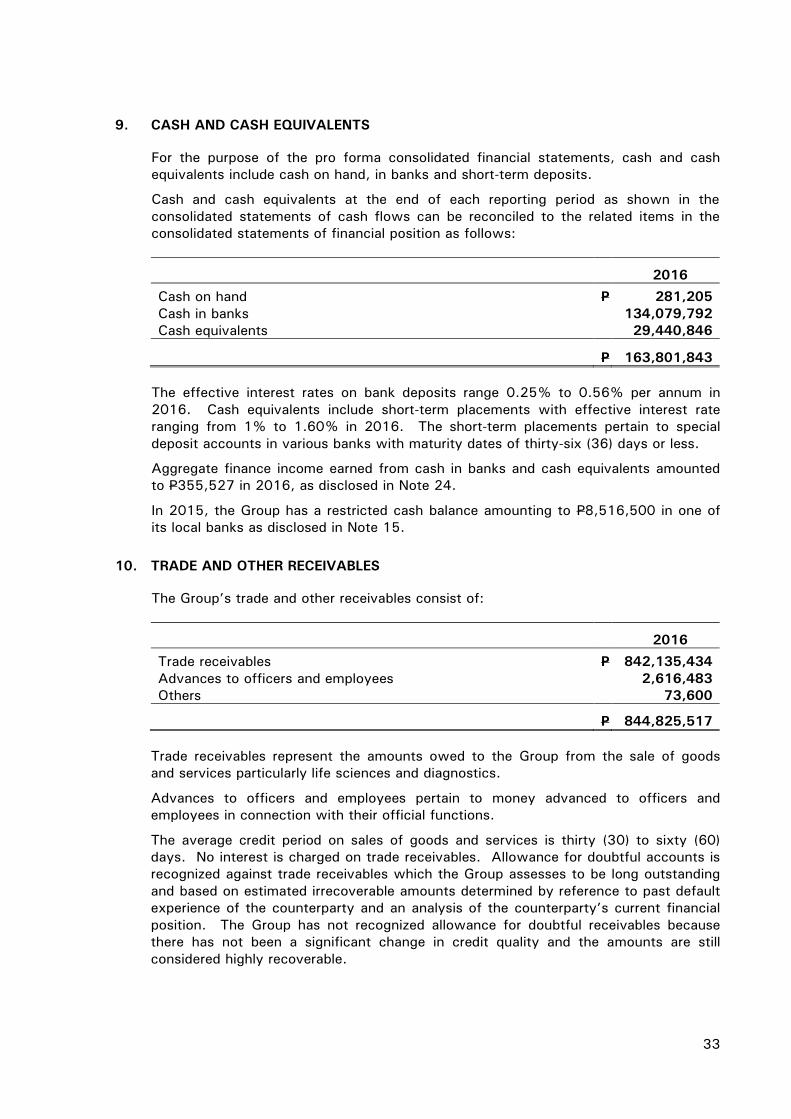

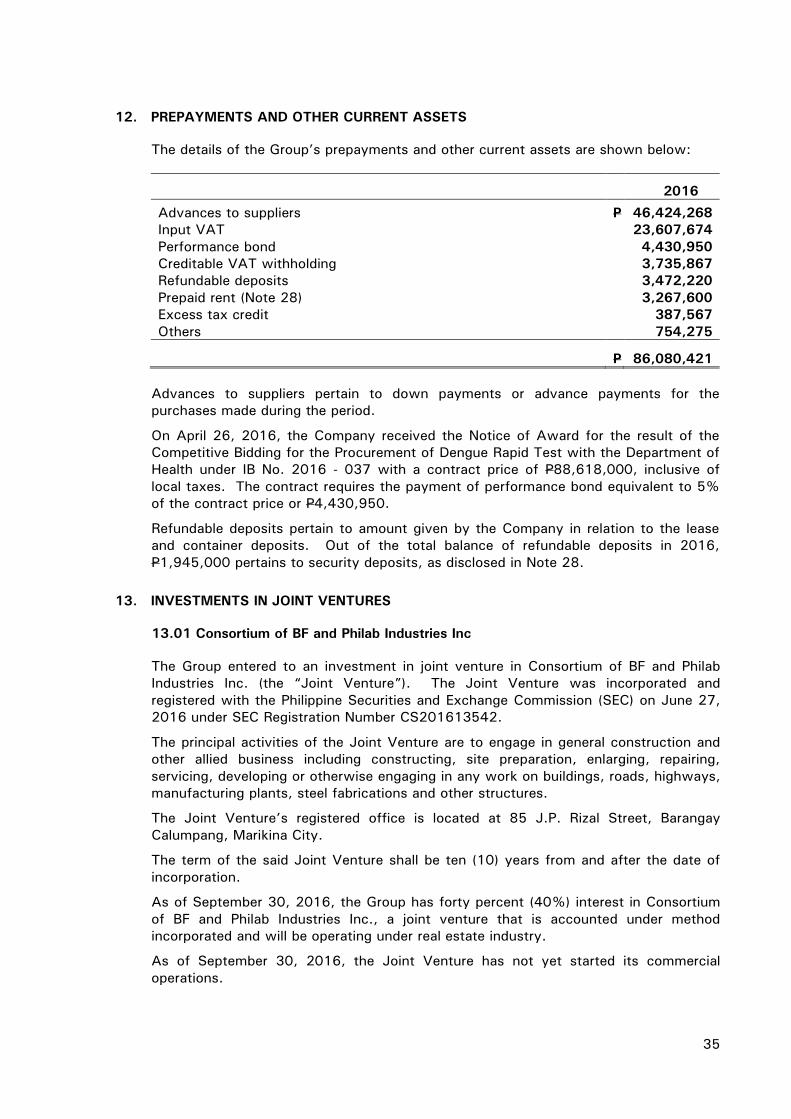

Current AssetsCash and cash equivalents 9 159,343,124 27,358,719 186,701,843 (22,900,000) 163,801,843 Trade and other receivables 10 844,825,517 - 844,825,517 - 844,825,517 Inventories 11 141,714,780 - 141,714,780 - 141,714,780 Prepayments and other current assets 12 85,556,341 524,080 86,080,421 - 86,080,421

1,231,439,762 27,882,799 1,259,322,561 (22,900,000) 1,236,422,561

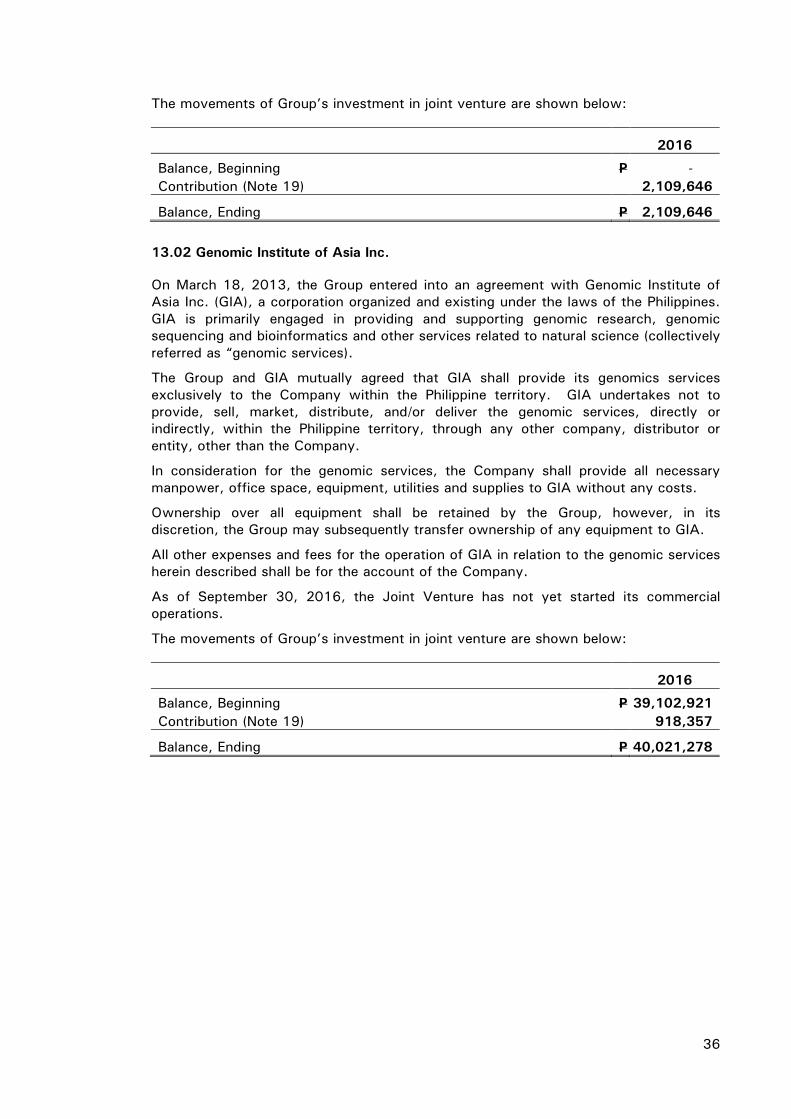

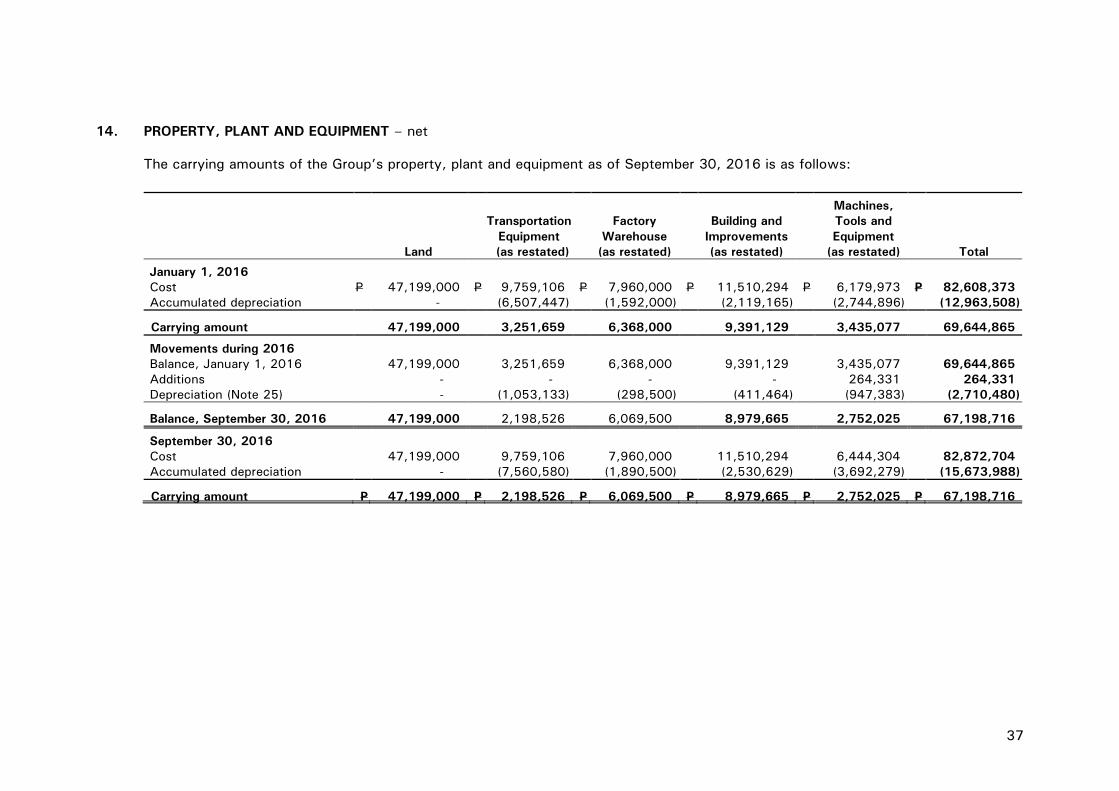

Non-current AssetsProperty, plant and equipment – net 14 67,198,716 - 67,198,716 - 67,198,716 Investment in joint venture 13,19 42,130,924 - 42,130,924 - 42,130,924 Deferred tax asset 30 610,055 1,668,062 2,278,117 - 2,278,117 Goodwill - 675,272,687 675,272,687 Other non-current assets 15 8,516,500 - 8,516,500 - 8,516,500

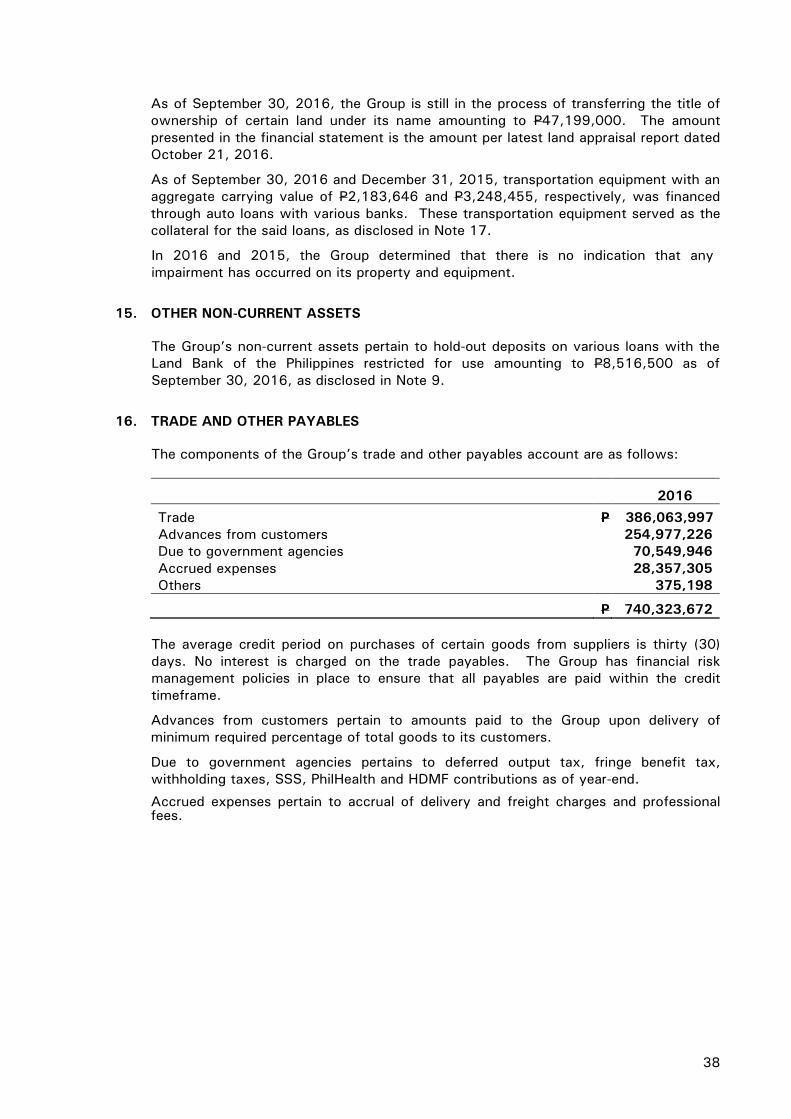

118,456,195 1,668,062 120,124,257 675,272,687 795,396,944

TOTAL ASSETS 1,349,895,957 29,550,861 1,379,446,818 652,372,687 2,031,819,505

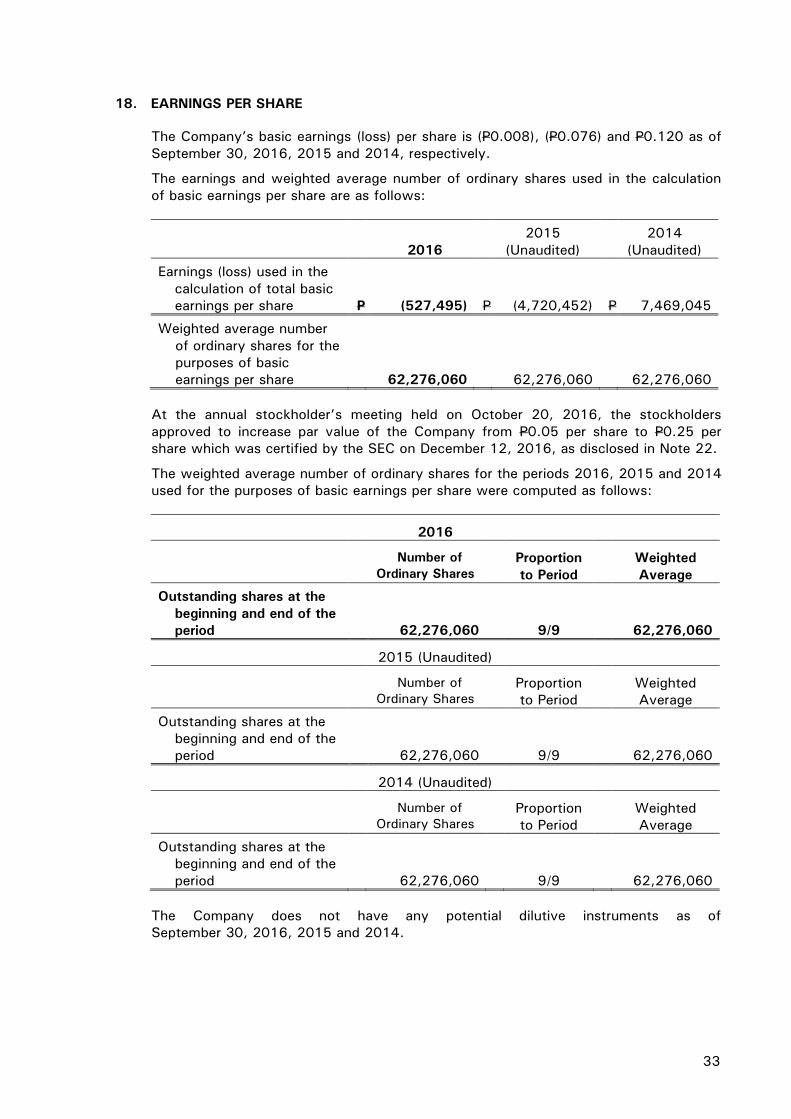

Current LiabilitiesTrade and other payables 16 738,774,067 1,549,605 740,323,672 - 740,323,672 Due to a related party 19 3,849,402 - 3,849,402 - 3,849,402 Income tax payable 53,466,130 - 53,466,130 - 53,466,130

796,089,599 1,549,605 797,639,204 - 797,639,204

Non-current LiabilitiesLoans payable 17 337,644,539 - 337,644,539 837,100,000 1,174,744,539 Retirement benefit obligation 27 10,815,828 - 10,815,828 - 10,815,828 Deferred tax liability – net 30 410,338 - 410,338 - 410,338 Other non-current liability 18 7,324,064 - 7,324,064 - 7,324,064

356,194,769 - 356,194,769 837,100,000 1,193,294,769

TOTAL LIABILITIES 1,152,284,368 1,549,605 1,153,833,973 837,100,000 1,990,933,973

Capital Stock 20 37,639,100 15,569,015 53,208,115 (37,639,100) 15,569,015

Share Premium 20 37,399,000 13,928,475 51,327,475 (37,399,000) 13,928,475

Unappropriated Retained Earnings 71,616,034 (1,496,234) 70,119,800 (71,616,034) (1,496,234)

Appropriated Retained Earnings 21 50,000,000 - 50,000,000 (50,000,000) -

Remeasurements 27 957,455 - 957,455 (957,455) -

EQUITY ATTRIBUTABLE TO OWNERS OF THE COMPANY 197,611,589 28,001,256 225,612,845 (197,611,589) 28,001,256

Noncontrolling interest - - - 12,884,276 12,884,276

TOTAL STOCKHOLDERS' EQUITY 197,611,589 28,001,256 225,612,845 (184,727,313) 40,885,532

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY 1,349,895,957 29,550,861 1,379,446,818 652,372,687 2,031,819,505

(See Notes to Pro Forma Consolidated Financial Statements)

LIABILITIES AND STOCKHOLDERS' EQUITY

L I A B I L I T I E S

S T O C K H O L D E R S ' E Q U I T Y

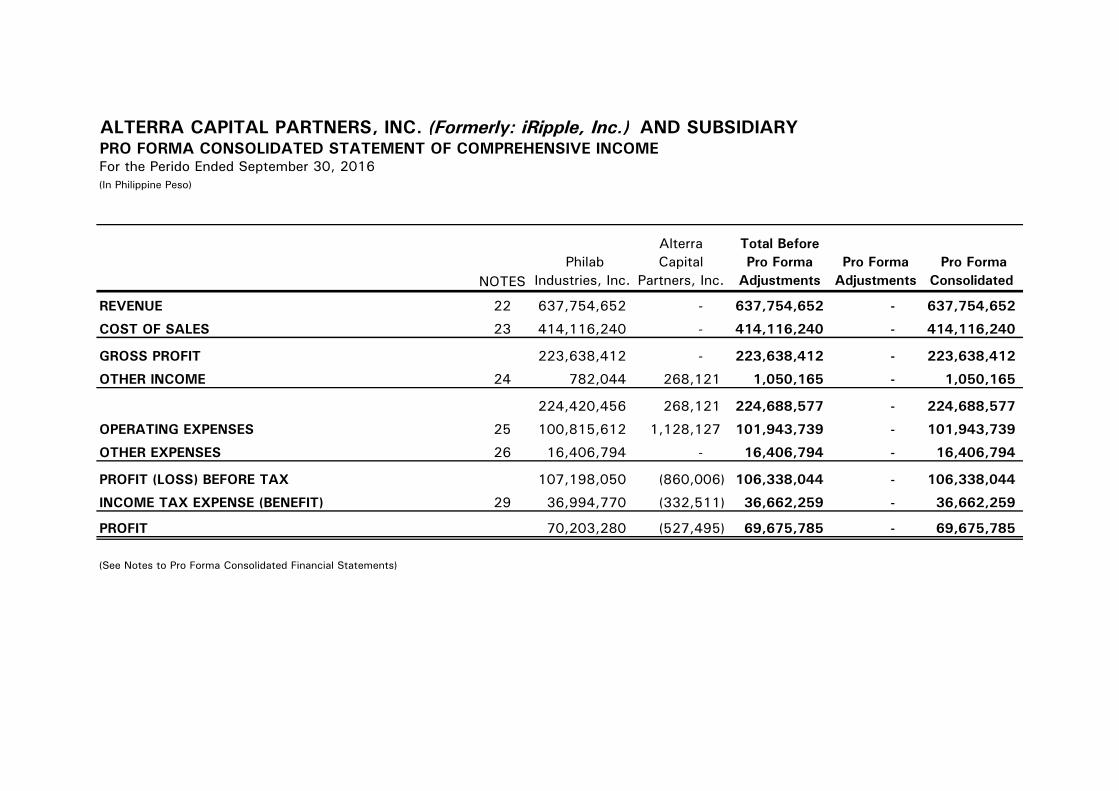

ALTERRA CAPITAL PARTNERS, INC. (Formerly: iRipple, Inc.) AND SUBSIDIARYPRO FORMA CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOMEFor the Perido Ended September 30, 2016(In Philippine Peso)

NOTES Philab

Industries, Inc.

Alterra Capital

Partners, Inc.

Total Before Pro Forma

AdjustmentsPro Forma

Adjustments Pro Forma

Consolidated

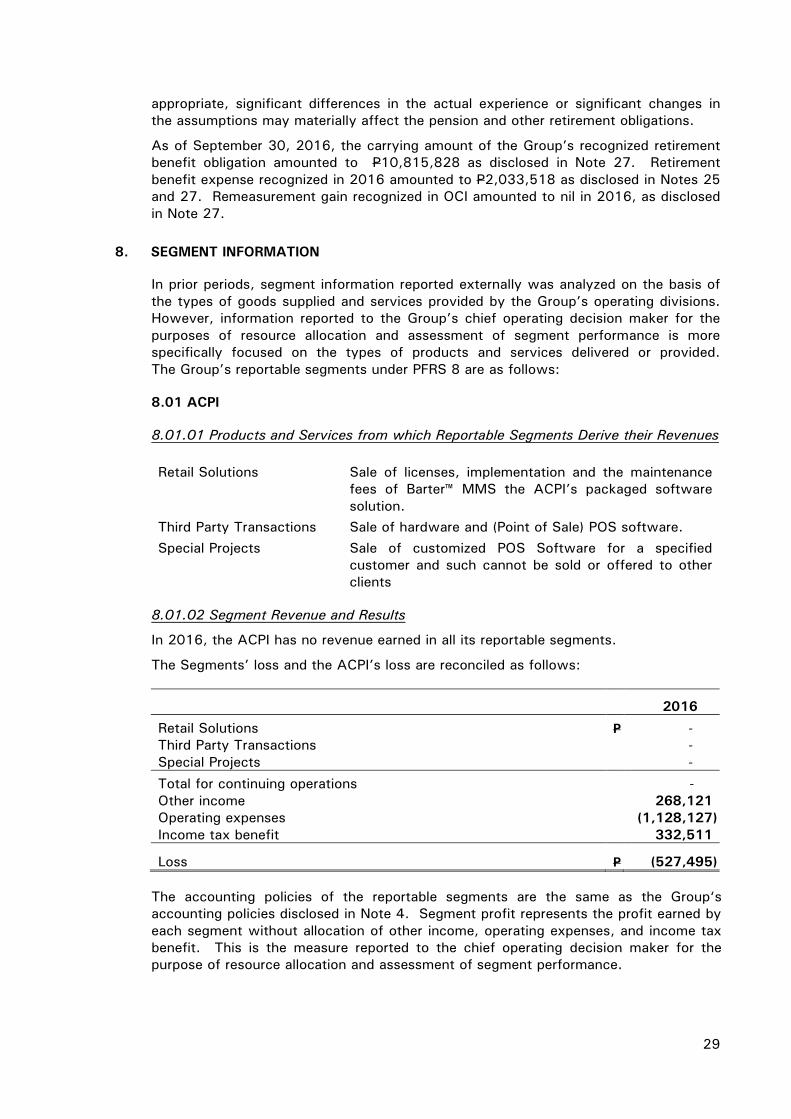

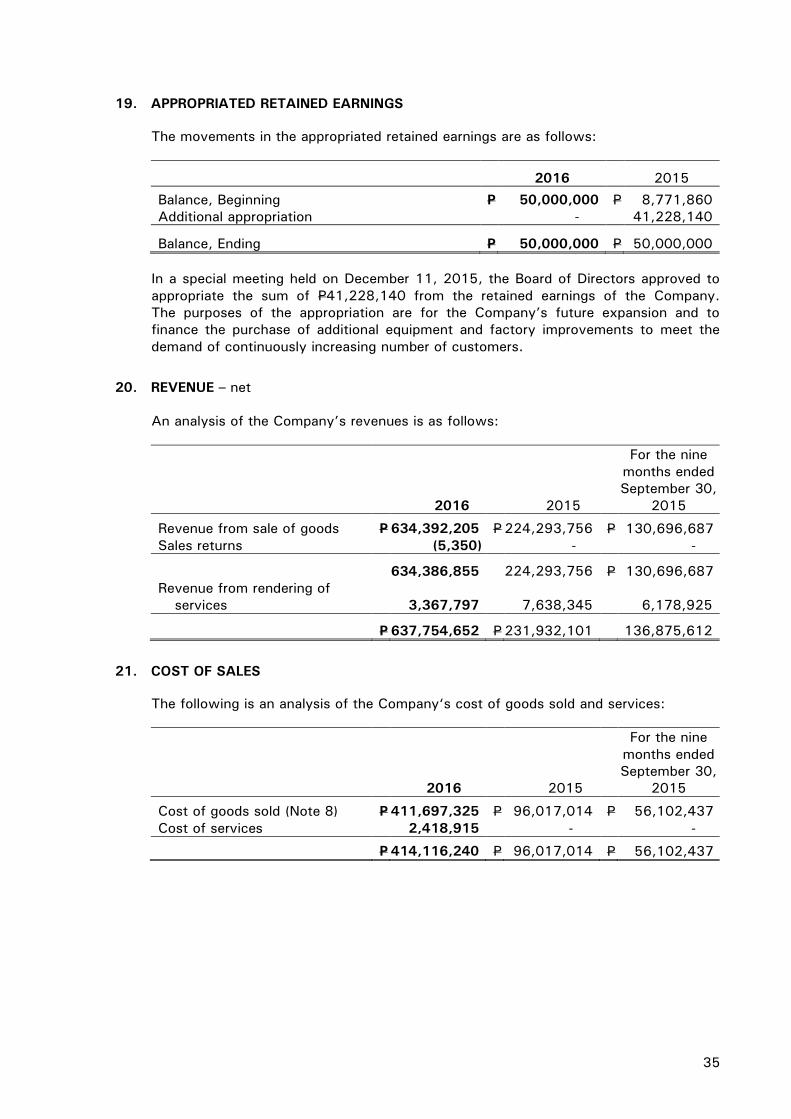

REVENUE 22 637,754,652 - 637,754,652 - 637,754,652

COST OF SALES 23 414,116,240 - 414,116,240 - 414,116,240

GROSS PROFIT 223,638,412 - 223,638,412 - 223,638,412

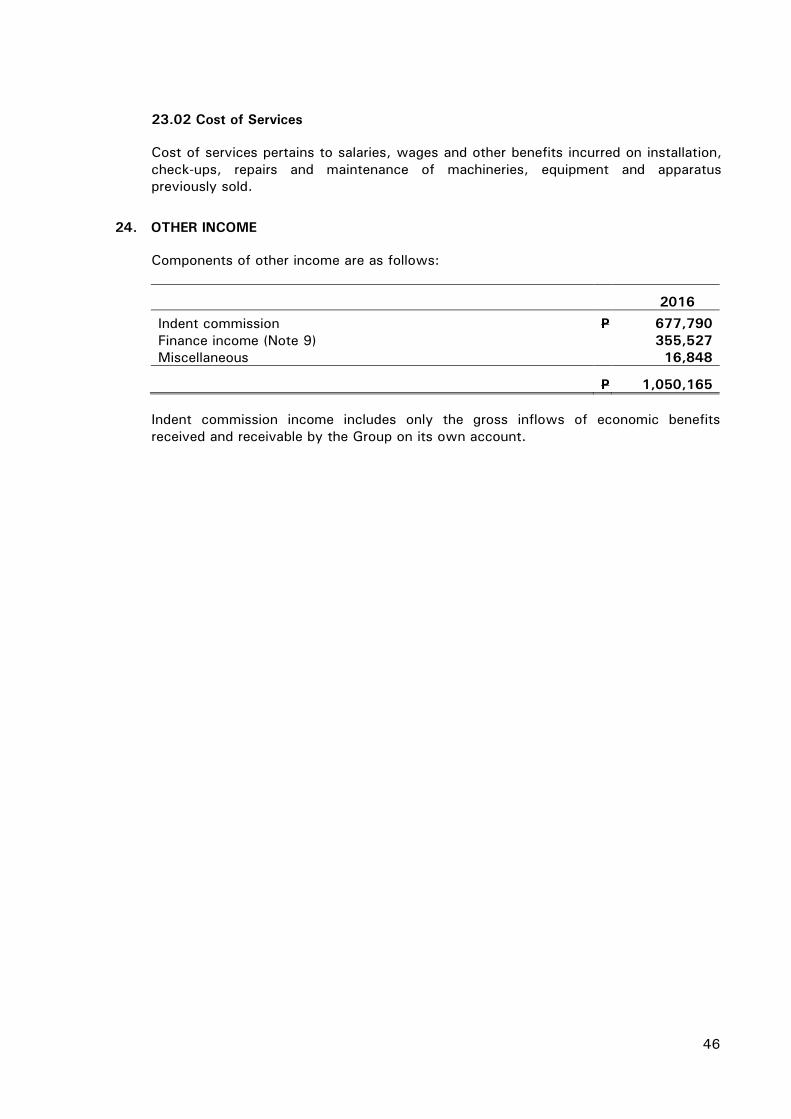

OTHER INCOME 24 782,044 268,121 1,050,165 - 1,050,165

224,420,456 268,121 224,688,577 - 224,688,577

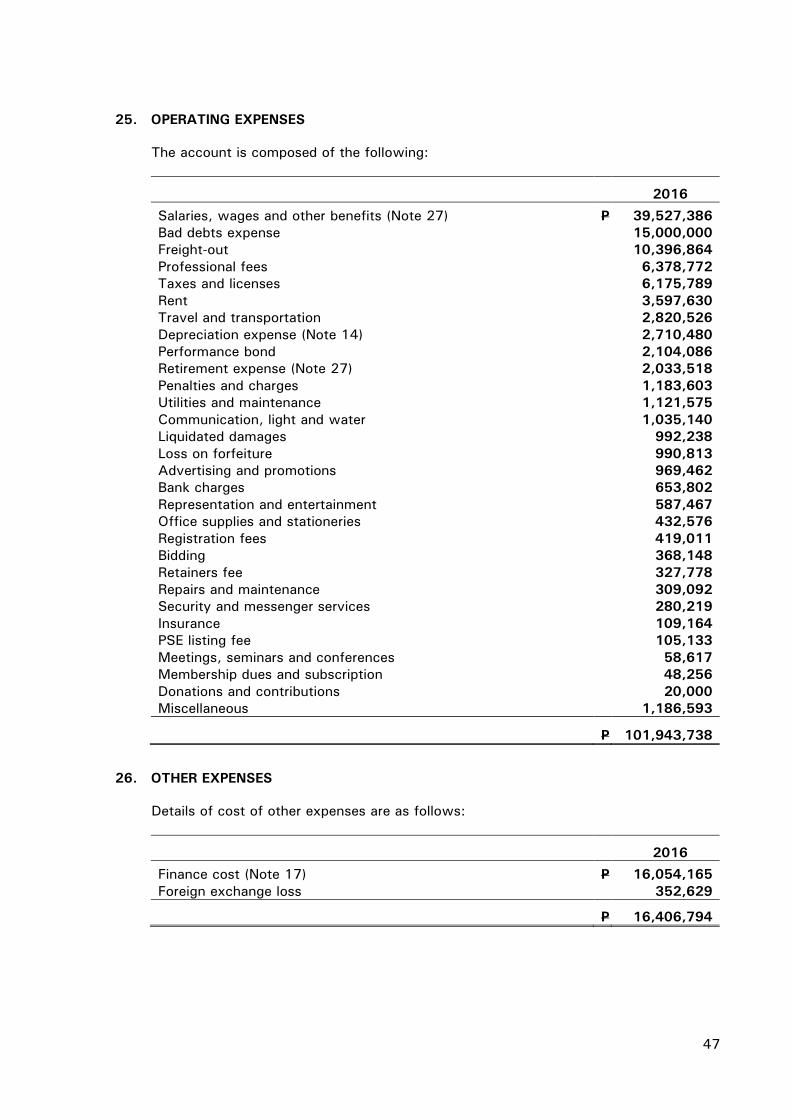

OPERATING EXPENSES 25 100,815,612 1,128,127 101,943,739 - 101,943,739

OTHER EXPENSES 26 16,406,794 - 16,406,794 - 16,406,794

PROFIT (LOSS) BEFORE TAX 107,198,050 (860,006) 106,338,044 - 106,338,044

INCOME TAX EXPENSE (BENEFIT) 29 36,994,770 (332,511) 36,662,259 - 36,662,259

PROFIT 70,203,280 (527,495) 69,675,785 - 69,675,785

(See Notes to Pro Forma Consolidated Financial Statements)

1

ALTERRA CAPITAL PARTNERS, INC. (Formerly: iRipple, Inc.) AND SUBSIDIARY

NOTES TO PRO FORMA CONSOLIDATED FINANCIAL STATEMENTS September 30, 2016

1. CORPORATE INFORMATION

Alterra Capital Partners, Inc. (the “ACPI“ or “Company”) is a service and trading corporation incorporated and registered with the Philippine Securities and Exchange Commission (SEC) on November 21, 2000. The Company’s primary purpose is to engage in the business of a holding company by buying and holding shares of other companies, whether common, preferred, treasury, founders or other kinds of shares, either by subscribing to the unissued shares of the capital stock in public or private offering or by purchasing the shares of other stockholders by way of assignment in private sale; to invest in the stock or equity of other companies; to acquire rights in the stock of other companies by way of sake, pledge, chattel mortgage or assignment; to sell, dispose, assign, pledge or convey any or all or its shareholdings in other companies in favor of qualified persons by way of private sale, assignment or other form of private conveyance, all in accordance with the Corporation Code, the Securities Regulation Code and other applicable laws and regulations; to vote its shareholdings in other companies and exercise all the rights of a shareholder under the Corporation Code and applicable laws provided that it will not act as stockbroker or dealer of securities.

The Company started its commercial operations in January 2002. The Company is substantially owned by Filipino individuals and the control rests with the members of the Board.

The Company’s registered office address is located at 8th floor, 1128 38th Avenue, Fort Bonifacio Global City, Taguig City, Metro Manila.

1.01 Status of Operations

On August 25, 2009, the Company completed its Initial Public Offering (IPO) of 4,579,122 new ordinary shares (approximately 29.41% of the total outstanding ordinary shares) at an offer price of P4.37 per share for a total gross proceeds of P19,987,444.

At the special meeting of the Board of Directors (BOD) on May 28, 2015, the following amendments on the Articles of Incorporation (AOI) were unanimously approved:

a. The name of the Corporation shall be Alterra Capital Partners, Inc.

b. The primary purpose of the Corporation is to engage in the business of a holding company by buying and holding shares of other companies, whether common, preferred, treasury, founders or other kinds of shares, either by subscribing to the unissued shares of the capital stock in public or private offering or by purchasing the shares of other stockholders by way of assignment in private sale; to invest in the stock or equity of other companies; to acquire rights in the stock of other companies by way of sake, pledge, chattel mortgage or assignment; to sell, dispose, assign, pledge or convey any or all or its shareholdings in other companies in favor of qualified persons by way of private sale, assignment or other form of private conveyance, all in accordance with the Corporation Code, the Securities Regulation Code and other applicable laws and regulations; to vote its shareholdings in other companies and exercise all the rights of a shareholder

2

under the Corporation Code and applicable laws provided that it will not act as stockbroker or dealer of securities.

c. The principal office of the Corporation is to be established at 2286 Pasong Tamo Extension, Makati City.

At the special meeting of the BOD held on June 22, 2015, the BOD authorized to reduce the par value of its shares from one peso per share (P1/sh) to five centavos per share (P0.05/sh), resulting in the increase in the number of its shares from 20,000,000 shares to 400,000,000 shares.

The Company entered into various sale and assignment of assets and assumption of liabilities with Movmento, Inc., a corporation organized and existing under the laws of the Philippines. The following are the transactions that transpired during the year:

1. On March 5, 2015, the Company entered into a “Deed of sale of assets with assumption of liabilities”. The Company, the “Seller” is the owner of various assets and likewise the obligor for various accounts payable, accrued expenses and other liabilities incurred in relation to the use of the said assets. Movmento, Ins., the “Buyer” has offered to acquire the assets and assume its related liabilities. The Company accepted the said offer for the consideration and under the terms and conditions set forth.

Therefore, for and in consideration of the foregoing premises and the covenants contained, the parties agreed as follows:

a. For and in consideration of the total sum of P21,052,143, purchase price, broken down into cash in the amount of P30,181,618 and the acceptance and assumption by the buyer of the assumed liabilities in the total amount of P9,129,475, receipt of which is acknowledged by the seller and the assumption of which liabilities is confirmed by the buyer, the seller absolutely and unconditionally assigns, cedes, conveys and transfers to the buyer, and the buyer purchases, acquires and accepts from the seller, any and all of the seller’s rights, title, interest and obligations of the seller in and to the assets and assumed liabilities.

The carrying amounts of the assets sold are as follows:

Trade and other receivables: Trade P 15,407,554 Less: Allowance for doubtful accounts (705,347) Due from a related party 5,098,769 Accrued revenue 3,072,095 Advances to officers and employees 1,497,181 Reimbursable from clients 947,598 Accrued interest 41,564 Others 802,072 P 26,161,486

Finance lease receivables 2,143,195 2,143,195 Inventories: Merchandise inventory 1,165,531 Leased asset inventory 252,643 1,418,174

Other current assets: Prepaid rent 1,552,817 Security deposits 239,328 SSS claims 10,350 1,802,495

Deferred tax assets 987,330 987,330

P 32,512,680 P 32,512,680

3

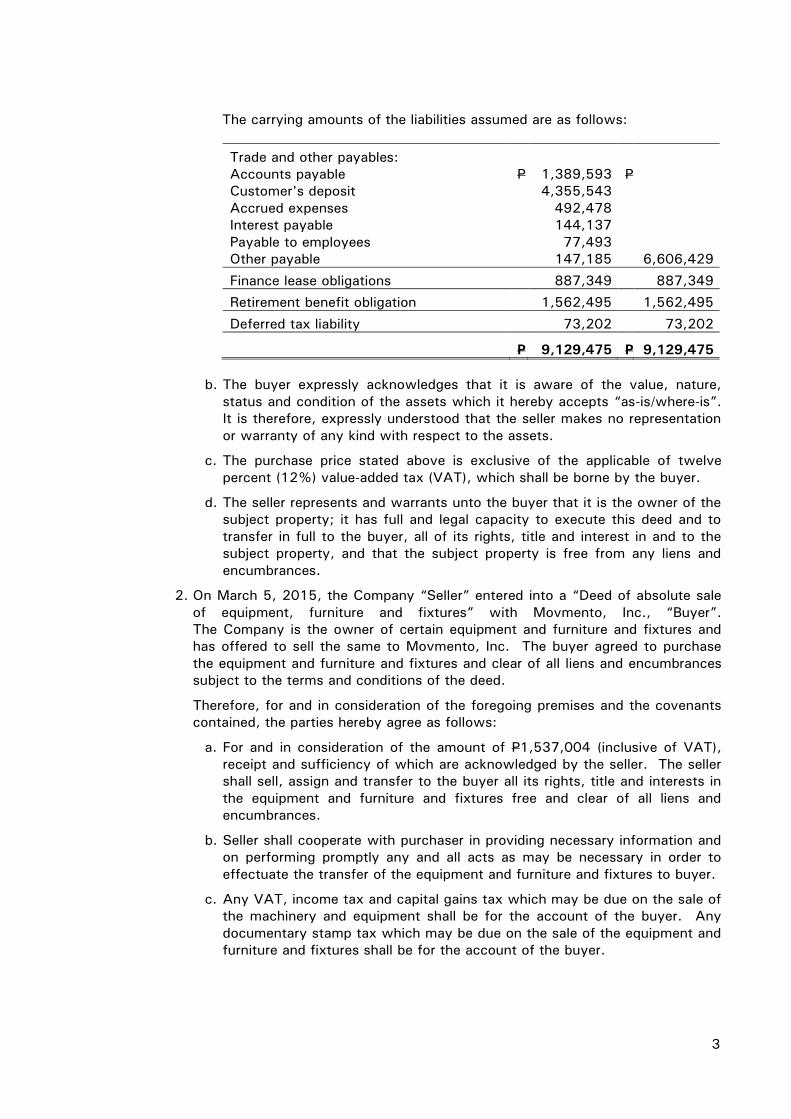

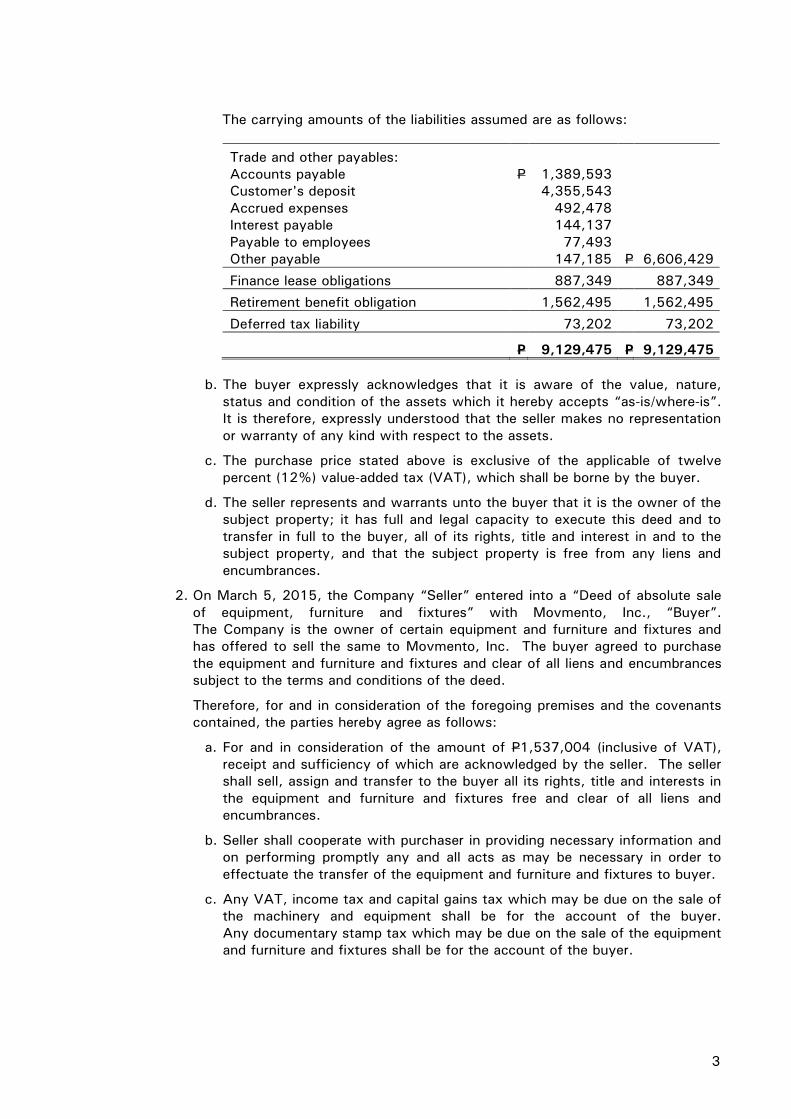

The carrying amounts of the liabilities assumed are as follows:

Trade and other payables: Accounts payable P 1,389,593 P Customer's deposit 4,355,543 Accrued expenses 492,478 Interest payable 144,137 Payable to employees 77,493 Other payable 147,185 6,606,429

Finance lease obligations 887,349 887,349 Retirement benefit obligation 1,562,495 1,562,495

Deferred tax liability 73,202 73,202

P 9,129,475 P 9,129,475

b. The buyer expressly acknowledges that it is aware of the value, nature, status and condition of the assets which it hereby accepts “as-is/where-is”. It is therefore, expressly understood that the seller makes no representation or warranty of any kind with respect to the assets.

c. The purchase price stated above is exclusive of the applicable of twelve percent (12%) value-added tax (VAT), which shall be borne by the buyer.

d. The seller represents and warrants unto the buyer that it is the owner of the subject property; it has full and legal capacity to execute this deed and to transfer in full to the buyer, all of its rights, title and interest in and to the subject property, and that the subject property is free from any liens and encumbrances.

2. On March 5, 2015, the Company “Seller” entered into a “Deed of absolute sale of equipment, furniture and fixtures” with Movmento, Inc., “Buyer”. The Company is the owner of certain equipment and furniture and fixtures and has offered to sell the same to Movmento, Inc. The buyer agreed to purchase the equipment and furniture and fixtures and clear of all liens and encumbrances subject to the terms and conditions of the deed.

Therefore, for and in consideration of the foregoing premises and the covenants contained, the parties hereby agree as follows:

a. For and in consideration of the amount of P1,537,004 (inclusive of VAT), receipt and sufficiency of which are acknowledged by the seller. The seller shall sell, assign and transfer to the buyer all its rights, title and interests in the equipment and furniture and fixtures free and clear of all liens and encumbrances.

b. Seller shall cooperate with purchaser in providing necessary information and on performing promptly any and all acts as may be necessary in order to effectuate the transfer of the equipment and furniture and fixtures to buyer.

c. Any VAT, income tax and capital gains tax which may be due on the sale of the machinery and equipment shall be for the account of the buyer. Any documentary stamp tax which may be due on the sale of the equipment and furniture and fixtures shall be for the account of the buyer.

4

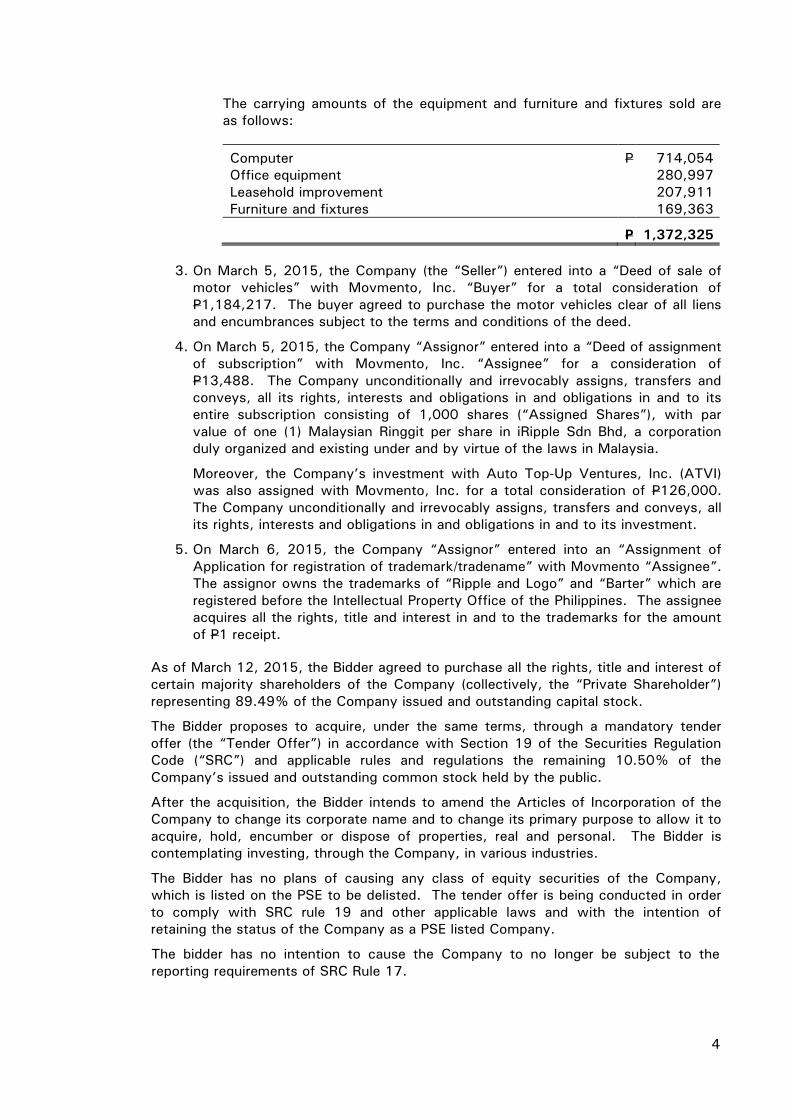

The carrying amounts of the equipment and furniture and fixtures sold are as follows:

Computer P 714,054 Office equipment 280,997 Leasehold improvement 207,911 Furniture and fixtures 169,363

P 1,372,325

3. On March 5, 2015, the Company (the “Seller”) entered into a “Deed of sale of motor vehicles” with Movmento, Inc. “Buyer” for a total consideration of P1,184,217. The buyer agreed to purchase the motor vehicles clear of all liens and encumbrances subject to the terms and conditions of the deed.

4. On March 5, 2015, the Company “Assignor” entered into a “Deed of assignment of subscription” with Movmento, Inc. “Assignee” for a consideration of P13,488. The Company unconditionally and irrevocably assigns, transfers and conveys, all its rights, interests and obligations in and obligations in and to its entire subscription consisting of 1,000 shares (“Assigned Shares”), with par value of one (1) Malaysian Ringgit per share in iRipple Sdn Bhd, a corporation duly organized and existing under and by virtue of the laws in Malaysia.

Moreover, the Company’s investment with Auto Top-Up Ventures, Inc. (ATVI) was also assigned with Movmento, Inc. for a total consideration of P126,000. The Company unconditionally and irrevocably assigns, transfers and conveys, all its rights, interests and obligations in and obligations in and to its investment.

5. On March 6, 2015, the Company “Assignor” entered into an “Assignment of Application for registration of trademark/tradename” with Movmento “Assignee”. The assignor owns the trademarks of “Ripple and Logo” and “Barter” which are registered before the Intellectual Property Office of the Philippines. The assignee acquires all the rights, title and interest in and to the trademarks for the amount of P1 receipt.

As of March 12, 2015, the Bidder agreed to purchase all the rights, title and interest of certain majority shareholders of the Company (collectively, the “Private Shareholder”) representing 89.49% of the Company issued and outstanding capital stock.

The Bidder proposes to acquire, under the same terms, through a mandatory tender offer (the “Tender Offer”) in accordance with Section 19 of the Securities Regulation Code (“SRC”) and applicable rules and regulations the remaining 10.50% of the Company’s issued and outstanding common stock held by the public.

After the acquisition, the Bidder intends to amend the Articles of Incorporation of the Company to change its corporate name and to change its primary purpose to allow it to acquire, hold, encumber or dispose of properties, real and personal. The Bidder is contemplating investing, through the Company, in various industries.

The Bidder has no plans of causing any class of equity securities of the Company, which is listed on the PSE to be delisted. The tender offer is being conducted in order to comply with SRC rule 19 and other applicable laws and with the intention of retaining the status of the Company as a PSE listed Company.

The bidder has no intention to cause the Company to no longer be subject to the reporting requirements of SRC Rule 17.

5

Under a Sale and Purchase Agreement dated August 12, 2016 executed by and among Conrado Rafael C. Alcantara, Alfonso S. Anggala and Start Alliance Securities Corp. (the “selling shareholders”), on one hand, and Genomics, Inc. and Hector Thomas A. Navasero (the “buyers”), on the other, the selling shareholders agreed to sell, assign, transfer and convey to the buyers, and the buyers agreed to purchase, acquire and accept from the selling shareholders, all of the rights, title and interest of the selling shareholders in and to Two Hundred Eight Million Six Hundred Twenty-Four Thousand and Eight Hundred and One (208,624,801) common shares representing approximately 67% of the outstanding capital stock of the Company. This agreement to sell and purchase the Company’s shares was made subject to the completion of certain conditions precedent, including the completion of a mandatory tender offer for all of the remaining shares of the Company, the price at which the selling shareholders agreed to sell, and the buyers agreed to purchase, the Company shares is the aggregate amount of Three Hundred Sixty-Two Million Three Hundred Twenty-Four Thousand Nine Hundred Sixty One and 21/100 Pesos (P362,324,961.21) or One and 74/100 (P1.74) per share.

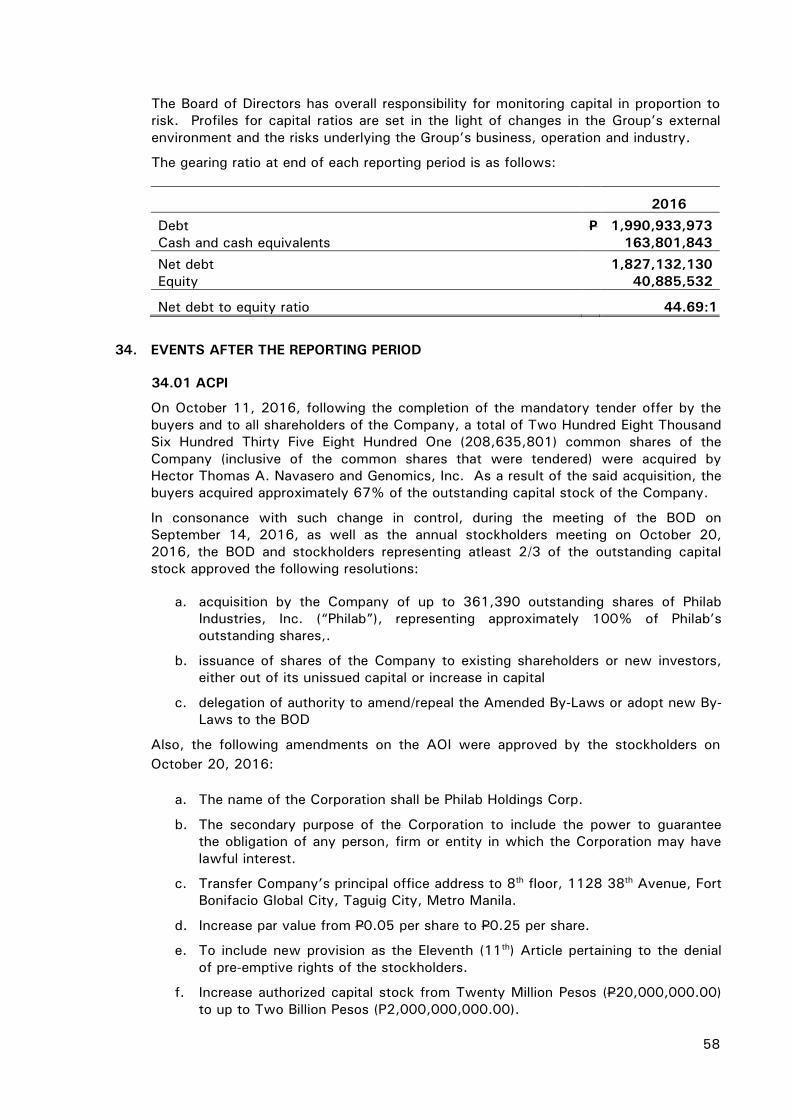

On October 11, 2016, following the completion of the mandatory tender offer by the buyers and to all shareholders of the Company, a total of Two Hundred Eight Thousand Six Hundred Thirty Five Eight Hundred One (208,635,801) common shares of the Company (inclusive of the common shares that were tendered) were acquired by Hector Thomas A. Navasero and Genomics, Inc. As a result of the said acquisition, the buyers acquired approximately 67% of the outstanding capital stock of the Company, as disclosed in Note 34.

In consonance with such change in control, during the meeting of the BOD on September 14, 2016, as well as the annual stockholders meeting on October 20, 2016, the BOD and stockholders representing atleast 2/3 of the outstanding capital stock approved the following resolutions, as disclosed in Note 34:

a. acquisition by the Company of up to 361,390 outstanding shares of Philab Industries, Inc. (“PII”), representing approximately 100% of Philab’s outstanding shares,

b. issuance of shares of the Company to existing shareholders or new investors, either out of its unissued capital or increase in capital, and

c. delegation of authority to amend/repeal the Amended By-Laws or adopt new By-Laws to the BOD

Also, the following amendments on the AOI were approved by the stockholders on October 20, 2016, as disclosed in Note 34:

a. The name of the Corporation shall be Philab Holdings Corp.

b. The secondary purpose of the Corporation to include the power to guarantee the obligation of any person, firm or entity in which the Corporation may have lawful interest.

c. Transfer Company’s principal office address to 8th floor, 1128 38th Avenue, Fort Bonifacio Global City, Taguig City, Metro Manila.

d. Increase par value from P0.05 per share to P0.25 per share.

e. To include new provision as the Eleventh (11th) Article pertaining to the denial of pre-emptive rights of the stockholders.

f. Increase authorized capital stock from Twenty Million Pesos (P20,000,000.00) to up to Two Billion Pesos (P2,000,000,000.00).

6

Items b, c, d and e from the above were certified by the SEC on December 12, 2016, as disclosed in Note 34.

The above resolutions and amendments on the AOI, taken together, if and when fully implemented, will result in the backdoor listing of Philab Industries.

On December 19, 2016, the Company acquired Three Hundred Fifty One Thousand Seven Hundred Forty (351,740) shares, representing 93.43% of the total outstanding capital stock of Philab at the price of P2,445 per share or the aggregate price of Eight Hundred Sixty Million Pesos (P860,000,000.00), as disclosed in Note 34.

As further disclosed in Note 34, on December 19, 2016, the Company entered into subscription agreements with certain subscribers who subscribed to its increase in capital stock. Such subscribers include some of the selling shareholders of Philab, as well as non-related or affiliated subscribers to ensure continued compliance with the minimum public ownership requirement. The increase in capital stock of the Company is still currently in process with the SEC.

2. PRO FORMA CONSOLIDATED FINANCIAL STATEMENTS ASSUMPTIONS

2.01 Objective of the Pro Forma Consolidated Financial Statements

The objectives of this pro forma financial information is to show what the significant effects of the historical financial information might have been had the pooled economic business components been combined on September 30, 2016. However, the pro forma financial information is not necessarily indicative of the results of operations or related effects in the financial position that would have been attained had the above mentioned transaction actually occurred earlier.

The pro forma consolidated financial information reflects the pro forma adjustments to present the significant effects of the following historical transactions based on the assumption that the foregoing occurred prior to September 30, 2016.

2.01.01 Omnibus Loan and Security Agreement with Altus Capital Corporation

In the special meeting of the BOD of the Company held on December 15, 2016, the BOD approved and authorized the Company (as borrower) to enter into an omnibus loan and security agreement with Altus Capital Corporation for the amount of P400,000,000.00 to be repaid within 30 months with interest at a rate of 15% per annum. The purpose of the loan is, among others, for working capital requirements.

The pro forma consolidated financial information presents the related effects of the above loan on September 30, 2016.

2.01.02 Loan Agreement with Various Non-Bank Entities

On January 2017, the Company entered into a loan agreement with various non-bank entities, for an aggregate amount of P437,100,000.00 maturing on August 15, 2017 with interest at a rate of 5% per annum plus 10% term premium. The purpose of the loan is, among others, for working capital requirements.

The pro forma consolidated financial information presents the related effects of the above loan on September 30, 2016.

7

2.01.03 ACPI’s Acquisition of PII’s certain outstanding shares

On December 19, 2016, the Company acquired Three Hundred Fifty One Thousand Seven Hundred Forty (351,740) shares, representing 93.48% of the total outstanding capital stock of Philab at the price of P2,445 per share or the aggregate price of Eight Hundred Sixty Million Pesos (P860,000,000.00), as disclosed in Note 32.

The pro forma consolidated financial information presents the related effects of the above acquisition on September 30, 2016.

The pro forma consolidated financial information also gives effect to the elimination of intercompany transactions and balances of the entity acquired included in the pro forma consolidation as of September 30, 2016.

2.02 Management Assumptions in Developing Pro Forma Adjustments

The Management assumes that the following transactions which have occurred or were planned to occur and recognized subsequent to September 30, 2016, have instead occurred on September 30, 2016 as these transactions have considerable impact on the assumed assets of the Company and its subsidiary.

x the Company have already received proceeds from the availed loans on September 30, 2016; and

x The Company acquired ownership interest in PII on September 30, 2016.

2.03 Pro Forma Adjustments

Proforma adjustments were made to the September 30, 2016 historical consolidated financial information of the Company and its acquired subsidiary, which include the following:

x recognition of the proceeds received from the availed loans;

x recognition of identified assets and liabilities of PII and the related operations as well as the accumulated retained earnings as of September 30, 2016. The difference between the balances of the asset acquired and liabilities assumed was recognized in retained earnings;

x elimination of intercompany and inter-business transactions and account balances

3. ADOPTION OF NEW AND REVISED ACCOUNTING STANDARDS

The Philippine Financial Reporting Standards Council (FRSC) approved the issuance of new and revised Philippine Financial Reporting Standards (PFRS). The term “PFRS” in general includes all applicable PFRS, Philippine Accounting Standards (PAS), and Interpretations issued by the Philippine Interpretations Committee (PIC), Standing Interpretations Committee (SIC) and International Financial Reporting Interpretations Committee (IFRIC) which have been approved by the FRSC and adopted by SEC.

These new and revised PFRS prescribe new accounting recognition, measurement and disclosure requirements applicable to the Company. When applicable, the adoption of the new standards was made in accordance with their transitional provisions, otherwise the adoption is accounted for as change in accounting policy under PAS 8, Accounting Policies, Changes in Accounting Estimates and Errors.

8

3.01 New and Revised PFRSs Applied with No Material Effect on the Financial Statements

The following new and revised PFRSs have also been adopted in these financial statements. The application of these new and revised PFRSs has not had any material impact on the amounts reported for the current and prior years but may affect the accounting for future transactions or arrangements.

x Amendments to PFRS 10, PFRS 12 and PAS, 28 Investment Entities: Applying the Consolidation Exception

The amendments confirm that the exemption from preparing consolidated financial statements for an intermediate parent entity is available to a parent entity that is a subsidiary of an investment entity, even if the investment entity measures all of its subsidiaries at fair value.

In addition, it clarifies that a subsidiary that provides services related to the parent's investment activities should not be consolidated if the subsidiary itself is an investment entity.

Moreover, it clarifies that when applying the equity method to an associate or a joint venture, a non-investment entity investor in an investment entity may retain the fair value measurement applied by the associate or joint venture to its interests in subsidiaries.

And, an investment entity measuring all of its subsidiaries at fair value shall provide the disclosures relating to investment entities as required by PFRS 12.

The amendments are effective for annual periods beginning on or after 1 January 2016 and must be applied retrospectively. Earlier application is permitted.

x PFRS 11, Joint Arrangements – Accounting for Acquisitions of Interests in Joint Operations

Amendments in PFRS 11 require an acquirer of an interest in a joint operation in which the activity constitutes a business to apply the accounting principles and disclosure requirements in PFRS 3 and other PFRS for business combinations. This is applicable in initial acquisition and acquisition of initial interest in a joint operation. This is applicable prospectively to annual periods beginning January 1, 2016.

x PFRS 14, Regulatory Deferral Accounts

PFRS 14 issued on January 30, 2014, provides temporary guidance for first-time adopters of PFRS on accounting for regulatory deferral account balances. Regulatory deferral account balances are describe as amounts of expense or income that would not be recognized as assets or liabilities in accordance with other Standards, but that qualify to be deferred because the amount is included, or is expected to be included, by the rate regulator in establishing the price(s) that an entity can charge to customers for rate-regulated goods or services.

PFRS 14 permits an entity that adopts PFRS to continue to use, in its first and subsequent PFRS financial statements, its previous generally accepted accounting principles (GAAP) accounting policies for the recognition, measurement, impairment and derecognition of regulatory deferral account balances without specifically considering the requirements of paragraph 11 of PAS 8. PFRS 14 requires entities to present regulatory deferral account balances as separate line items in the statement of financial position and to present movements in those account

9

balances as separate line items in the statement of profit or loss and other comprehensive income. PFRS 14 also requires specific disclosures to identify the nature of, and risks associated with, the rate regulation that has resulted in the recognition of regulatory deferral account balances in accordance with this Standard.

PFRS 14 is effective for a period beginning on or after January 1, 2016. Earlier application is permitted.

x Amendments to PAS 1, Disclosure Initiative

The amendments clarify that information should not be obscured by aggregating or by providing immaterial information. Materiality considerations shall apply to all parts of the financial statements even if when a standard requires a specific disclosure.

In addition, the amendments introduce a clarification that the list of line items to be presented in the statement of financial position and statement of comprehensive income can be disaggregated and aggregated as relevant. Also, it clarifies that an entity's share of other comprehensive (OCI) of equity-accounted associates and joint ventures should be presented in aggregate as single line items based on whether or not it will subsequently be reclassified to profit or loss.

Further, the amendments add additional examples of possible ways of ordering the notes to clarify that understandability and comparability should be considered when determining the order of the notes. The IASB also removed guidance and examples with regard to the identification of significant accounting policies that were perceived as being potentially unhelpful.

x PAS 16, Property, Plant and Equipment and PAS 38, Intangible Assets – Clarification of Acceptable Methods of Depreciation and Amortization

The amendments clarify that revenue-based depreciation is not appropriate for property, plant and equipment. Revenue-based amortization is allowed only when the intangible assets are expressed as a measure of revenue or when it can be demonstrated that revenue and the consumption of economic benefits of the intangible asset are highly correlated. This is effective prospectively from January 1, 2016. Earlier application is permitted.

x PAS 27, Separate Financial Statements – Equity Method in Separate Financial Statements

The amendments in PAS 27 permit an entity to account its investments in subsidiaries, joint ventures and associates using the equity method as described in PAS 28 in its separate financial statements. The amendments shall be applied for annual periods beginning January 1, 2016 retrospectively. Earlier application is permitted.

x Improvements to PFRS (2014) – Effective for annual periods beginning on or after January 1, 2016. Earlier application is permitted.

PFRS 5, Non-current Assets Held for Sale and Discontinued Operations – The amendments require that an asset reclassified directly from being held sale to being held for distribution, or directly from being held for distribution to being held for sale, the requirements for classification, presentation and measurement shall continue to be applied in accordance with this standard

10

PFRS 7, Financial Instruments: Disclosure – The amendments clarify that the right to service a financial asset transferred may be retained for a fee that is included in the servicing contract. The right to earn a fee for servicing the financial asset is generally continuing involvement for the purpose of applying the disclosure requirements. The service contract must be assessed to determine whether there is a continuing involvement in the financial asset transferred.

Further, the additional disclosure required by amendments to PFRS 7, Disclosure –Offsetting Financial Assets and Financial Liabilities is not specifically required for all interim periods. For condensed financial interim financial statements, the disclosure requirements are required to be given if the financial statements are prepared in accordance with PAS 34, Interim Financial Reporting when the inclusion would be required by the standard.

PAS 19, Employee Benefits – It clarifies that the high quality corporate bonds used to estimate the discount rate for post-employment benefit obligations should be denominated in the same currency as the liability and that the depth of the market for high quality corporate bonds should be assessed at the currency level.

PAS 34, Interim Financial Reporting – It clarifies that information shall be disclosed either in the notes to the interim financial statements or elsewhere in the interim financial report, by incorporating cross-reference from the interim financial statements to the other part of the interim financial report which is available to users on the same terms as the interim financial statements and at the same time.

x PIC Q&A No. 2015-01 Conforming Changes in PIC Q&As – Cycle 2015

This Q&A No. 2015-01 sets out the amendments to certain PIC Q&As. These changes are made as a consequence of the issuance of new Philippine Financial Reporting Standards (PFRS) and amendments to certain existing PFRS that are effective as of January 1, 2013.

3.02 New and Revised PFRSs in Issue but Not Yet Effective

The Company will adopt the following standards and interpretations enumerated below when they become effective. Except as otherwise indicated, the Company does not expect the adoption of these new and amended PFRS, to have significant impact on the financial statements.

3.02.01 Standard Adopted by FRSC and Approved by the Board of Accountancy (BOA)

x PFRS 9, Financial Instruments – Hedge Accounting and Amendments to PFRS 9, PFRS 7 and PAS 39 (2013)

PFRS 9 (2013) includes the new hedge accounting requirements that align hedge accounting more closely with risk management, establish a more principle-based approach to hedge accounting and address inconsistencies and weaknesses in the hedge accounting model in PAS 39. One of the significant changes is that inclusion of non-financial items into the type of transactions eligible for hedge accounting, provided that the risk component is separately identifiable and reliably measurable. Entities were given an accounting policy choice between applying the hedge accounting requirements of PFRS 9 and continuing to apply the hedge accounting requirements in PAS 39. Also, the disclosure on hedge accounting and risk management disclosures were improved.

11

PFRS 9 (2013) does not have a mandatory effective date, early application is permitted.

x PFRS 9, Financial Instruments (2014)

PFRS 9, amended on July 24, 2014, made limited amendments to the requirements for classification and measurement of financial assets and requirements for impairment.

The amendments introduce a ‘fair value through other comprehensive income’ measurement category for particular simple debt instruments. Also it introduced impairment requirements relating to the accounting for an entity’s expected credit losses on its financial assets and commitments to extend credit. These requirements eliminate the threshold that was in PAS 39 for the recognition of credit losses. Under the impairment approach in PFRS 9 it is no longer necessary for a credit event to have occurred before credit losses are recognized. Instead, an entity always accounts for expected credit losses, and changes in those expected credit losses. The amount of expected credit losses is updated at each reporting date to reflect changes in credit risk since initial recognition and, consequently, more timely information is provided about expected credit losses.

PFRS 9 supersedes PFRS 9 (2009), PFRS 9 (2010) and PFRS 9 (2013) and is effective retrospectively for annual periods beginning on or after January 1, 2018, with earlier application permitted.

x PFRS 10, Consolidated Financial Statements and PAS 28, Investments in Associates and Joint Ventures – Sale or Contribution of Assets between an Investor and its Associate or Joint Venture

The amendments clarify the treatment of the sale or contribution of assets between an investor and its associate and joint venture. This requires an investor in its financial statements to recognize in full the gains and losses arising from the sale or contribution of assets that constitute a business while recognize partial gains and losses if the assets do not constitute a business (i.e. up to the extent only of unrelated investor share).

On January 13, 2016, the FRSC decided to postpone the original effective date of January 1, 2016 of the said amendments until the IASB has completed its broader review of the research project on equity accounting that may result in the simplification of accounting for such transactions and of other aspects of accounting for associates and joint ventures.

x PFRS 16, Leases

Introduces a single lessee accounting model and requires a lessee to recognize assets and liabilities for all leases with a term of more than 12 months, unless the underlying asset is of low value. A lessee is required to recognize a right-of-use asset representing its right to use the underlying leased asset and a lease liability representing its obligation to make lease payments.

On the other hand, it substantially carries forward the lessor accounting requirements in PAS 17. Accordingly, a lessor continues to classify its leases as operating leases or finance leases, and to account for those two types of leases differently.

Effective for annual periods beginning on or after January 1, 2019, however, earlier application is not permitted until the FRSC has adopted the new revenue recognition standard.

12

x IFRIC 15, Agreements for the Construction of Real Estate

The Interpretation addresses how entities should determine whether an agreement for the construction of real estate is within the scope of PAS 11, Construction Contracts, or PAS 18, Revenue, and when revenue from the construction of real estate should be recognized. The requirements have not affected the accounting for the Company’s construction activities.

Effectivity of this interpretation has been deferred until the final Revenue standard is issued by International Accounting Standards Board (IASB), and an evaluation of the requirements of the final Revenue standard against the practices of the Philippine real estate industry is completed.

x Amendments to PAS 7, Disclosure Initiative

The amendments require an entity to provide disclosures that enable users of financial statements to evaluate changes in liabilities arising from financing activities, including both changes arising from cash flows and non-cash charges.

Effective for annual periods beginning on or after January 1, 2017 and shall be applied prospectively, with earlier application permitted.

x Amendments to PAS 12, Recognition of Deferred Tax Assets for Unrealized Losses

The amendments clarify that unrealized losses on debt instruments measured at fair value in the financial statements but at cost for tax purposes can give rise to deductible temporary differences.

In addition, these clarify that the carrying amount of an asset does not limit the estimation of probable future taxable profits and that when comparing deductible temporary differences with future taxable profits, the future taxable profits excludes tax deductions resulting from the reversal of those deductible temporary differences.

Effective for annual periods beginning on or after January 1, 2017 and shall be applied retrospectively, with earlier application permitted.

3.02.02 Standard Adopted by FRSC but pending for Approval of the BOA

x Amendments to PFRS 2, Classification and Measurement of Share-based Payment Transactions

The amendments clarify the accounting for the effects of vesting conditions on the measurement of a cash-settled share-based payment transaction; the classification of a share-based payment transaction with net settlement features for withholding tax obligations; and modification to the terms and conditions of share-based payment transactions that will result to change in classification from cash-settled to equity-settled.

The amendments are effective for annual periods beginning on or after January 1, 2018. Retrospective application is permitted if elected for all of the aforementioned amendments and other criteria are met.

13

x PIC Q&A No. 2016-02 PAS 32 and PAS 38 – Accounting Treatment of Club Shares Held by an Entity

A proprietary club share entitles the shareholder to a residual interest in the net assets upon liquidation which justifies that such instrument is an equity instrument and thereby qualifies as a financial asset to be accounted for under PAS 39, Financial Instruments: Recognition and Measurement.

A non-proprietary club share, though an equity instrument in its legal form, is not an equity instrument in the context of PAS 32. Furthermore, it does not entitle the holder to a contractual right to receive cash or another financial asset from the issuing corporation. The holder of the share, in substance, only paid for the privilege to enjoy the club facilities and services but not for ownership of the club. In such case, the holder must account for the share as an intangible asset under PAS 38.

4. BASIS FOR THE PREPARATION AND PRESENTATION OF FINANCIAL STATEMENTS

4.01 Statement of Compliance

The consolidated pro forma financial statements of the Company and its subsidiary (the “Group”) have been prepared in conformity with Philippine Financial Reporting Standards (PFRS) and are under the historical cost convention, except for certain financial instruments that are carried either at fair value or at amortized cost, and inventories carried at net realizable value.

4.02 Functional and Presentation Currency

Items included in the financial statements of the Group are measured using Philippine Peso (P), the currency of the primary economic environment in which the Group operates (the “functional currency”).

The Group chose to present its financial statements using its functional currency.

5. BASIS OF CONSOLIDATION AND COMPOSITION OF THE GROUP

5.01 Basis of Consolidation

The pro forma consolidated financial statements incorporate the financial statements of the Company and the acquired subsidiary. Control is achieved when the Company has power over the investee, is expose, or has rights, to variable returns from its involvement with the investee, and has the ability to use its power to affect its returns.

The Company reassess whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of these three elements of control. When the Company has less than a majority of the voting rights of an investee, it has power over the investee when the voting rights are sufficient to give it the practical ability to direct the relevant activities of the investee unilaterally.

The Company considers all relevant facts and circumstances in assessing whether or not the Company’s voting rights in an investee are sufficient to give power, including:

x the size of the Company’s holding of voting rights relative to the size and dispersion of holdings of other vote holders;

x potential voting rights held by the Company, other vote holders or other parties;

14

x rights arising from other contractual arrangements; and

x any additional facts and circumstances that indicate that the Company has, or does not have, the current ability to direct the relevant activities at the time the decisions need to be made, including voting patterns from previous shareholders’ meetings.

5.02 Composition of the Group

Details of the Company’s subsidiary as of September 30, 2016 are as follows:

The significant financial information on the financial statements of the subsidiary of the Company as of and for the period ended September 30, 2016 are shown below. The Summarized financial information below represents amounts before intra group eliminations.

5.02.01 Philab Industries, Inc. (PII)

PII was incorporated and registered with the Philippine Securities and Exchange Commission (SEC) on February 19, 1980 under SEC Registration Number 91302.

The principal activities of the Company are to manufacture, sell, export, import and otherwise deal in all kinds and classes of scientific, medical, educational, electronics, laboratory, research, testing and measuring machineries, equipment, apparatus, furniture and fixtures, including their accessories, attachments and spare parts, as well as in any and all articles, goods, wares and merchandise or kindred nature.

The PII’s registered office address is located at 7487 Bagtikan Street, San Antonio Village, Makati City.

The significant information on the reviewed financial statements of PII as of and for the period ended September 30, 2016 are as follows:

2016

Financial Position: Current Assets P 1,231,439,762 Non-current Assets 118,456,195 Total assets 1,349,895,957

Current Liabilities 796,089,599 Non-current Assets 356,194,769

Total liabilities 1,152,284,368 Equity 197,611,589

Results of operations:: Revenue 637,754,652 Cost and expenses 467,517,804 Profit 70,203,280

6. SIGNIFICANT ACCOUNTING POLICIES

Principal accounting and financial reporting policies applied by the Group in the preparation of its financial statements are enumerated below and are consistently applied to all the years presented, unless otherwise stated.

15

6.01 Financial Assets

Financial assets are initially measured at fair value, plus transaction costs, except for those financial assets classified as at fair value through profit or loss, which are initially measured at fair value.

Financial assets that are subsequently measured at cost or at amortized cost, and where the purchase or sale are under a contract whose terms require delivery of such within the timeframe established by the market concerned are initially recognized on the trade date.

Financial assets are classified into the following specified categories: financial assets at fair value through profit or loss’ (FVTPL), ‘held-to-maturity’ investments, ‘available-for-sale’ (AFS) financial assets and ‘loans and receivables’. The classification depends on the nature and purpose of the financial assets and is determined at the time of initial recognition.

The Group’s financial assets include cash and cash equivalents, trade and other receivables, performance bond and refundable deposits presented under prepayments and other current assets and hold-out deposit presented other non-current assets.

6.01.01 Effective Interest Method

The effective interest method is a method of calculating the amortized cost of a debt instrument and of allocating finance income over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash receipts including all fees on points paid or received that form an integral part of the effective interest rate, transaction costs and other premiums or discounts, through the expected life of the debt instrument, or, where appropriate, a shorter period to the net carrying amount on initial recognition.

Income is recognized on an effective interest basis for debt instruments other than those financial assets classified as at FVTPL.

6.01.02 Amortized Cost

Amortized cost is computed using the effective interest method less any allowance for impairment and principal repayment or reduction. The calculation takes into account any premium or discount on acquisition and includes transaction costs and fees that are an integral part of effective interest rate.

6.01.03 Cash and cash equivalents

Cash includes cash on hand measured at face value and cash deposits held at call with bank that are subject to insignificant risk of change in value. This shall be measured at undiscounted amount of the cash or other consideration expected to be paid or received.

Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash with maturities of three (3) months or less from the date of acquisition and that are subject to an insignificant risk of change in value.

6.01.04 Trade and Other Receivables

Trade and other receivables that have fixed or determinable payments that are not quoted in an active market are classified as ‘loans and receivables’. Loans and other receivables are measured at amortized cost using the effective interest method, less any impairment. Finance income is recognized by applying the effective interest rate, except for short-term receivables when the recognition of interest would be immaterial.

16

6.01.05 Impairment of Financial Assets

Financial assets, other than those at FVTPL, are assessed for indicators of impairment at the end of each reporting period. Financial assets are impaired where there is objective evidence that, as a result of one or more events that occurred after the initial recognition of the financial asset, the estimated future cash flows of the investment have been affected.

Objective evidence of impairment could include:

x significant financial difficulty of the issuer or counterparty; or

x default or delinquency in interest or principal payments; or

x it becoming probable that the borrower will enter bankruptcy or financial re-organization; or

x the lender, for economic or legal reasons relating to the borrower’s financial difficulty, grants the borrower a concession that the lender would not otherwise consider; or

x the disappearance of an active market for that financial asset because of financial difficulties; or

x observable data indicating that there is a measurable decrease in the estimated future cash flows from a group of financial assets since the initial recognition of those assets, although the decrease cannot yet be identified with the individual financial assets in the group, including (i) adverse changes in the payment status of borrowers in the group (e.g. an increased number of delayed payments or an increased number of credit card borrowers who have reached their credit limit and are paying the minimum monthly amount); or (ii) national or local economic conditions that correlate with defaults on the assets in the group (e.g. an increase in the unemployment rate in the geographical area of the borrowers, a decrease in property prices for mortgages in the relevant area, a decrease in oil prices for loan assets to oil producers, or adverse changes in industry conditions that affect the borrowers in the group).

Other factors may also be evidence of impairment, including significant changes with an adverse effect that have taken place in the technological, market, economic or legal environment in which the issuer operates.

For certain categories of financial asset, such as trade receivables, assets that are assessed not to be impaired individually are, in addition, assessed for impairment on a collective basis. Objective evidence of impairment for a portfolio of receivables could include the Group’s past experience of collecting payments, an increase in the number of delayed payments in the portfolio past the average credit period of thirty (30) to sixty (60) days, as well as observable changes in national or local economic conditions that correlate with default on receivables.

For financial assets carried at amortized cost, the amount of the impairment is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the financial asset’s original effective interest rate.

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets with the exception of trade receivables, where the carrying amount is reduced through the use of an allowance account. When a trade receivable is considered uncollectible, it is written off against the allowance account. Subsequent recoveries of amounts previously written off are credited against the allowance account. Changes in the carrying amount of the allowance account are recognized in profit or loss.

17

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, the previously recognized impairment loss is reversed through profit or loss to the extent that the carrying amount of the investment at the date the impairment is reversed does not exceed what the amortized cost would have been had the impairment not been recognized.

6.01.06 Derecognition of Financial Assets

The Group derecognizes a financial asset only when the contractual rights to the cash flows from the asset expire, or when it transfers the financial asset and substantially all the risks and rewards of ownership of the asset to another entity. If the Group neither transfers nor retains substantially all the risks and rewards of ownership and continues to control the transferred asset, the Group recognizes its retained interest in the asset and an associated liability for amounts it may have to pay. If the Group retains substantially all the risks and rewards of ownership of a transferred financial asset, the Group continues to recognize the financial asset and also recognizes a collateralized borrowing for the proceeds received.

6.02 Prepayments and Other Current Assets

Prepayments and other current assets represent expenses not yet incurred but already paid in cash. These are initially recorded as assets and measured at the amount of cash paid. Subsequently, these are charged to profit or loss as they are consumed in operations or expire with the passage of time.

Prepayments and other current assets are classified in the statement of financial position as current assets when the expenses related to these are expected to be incurred within one year or the Group’s normal operating cycle whichever is longer. Otherwise, these are classified as non-current assets. This account consists of advances to suppliers, input VAT, performance bond, creditable VAT withholding, refundable deposits, prepaid rent, deferred input tax, excess tax credit and others alike.

6.03 Interests in Joint Arrangement

A joint arrangement is a contractual arrangement whereby the Group and other parties have agreed sharing of control of an arrangement, which exist only when decisions about relevant activities require the unanimous consent of the parties sharing. The sharing of control is also known as joint control. A joint arrangement can either be a joint venture or a joint operation.

6.03.01 Joint Venture

A joint venture is a joint arrangement whereby the Group and other parties that have joint control of the arrangement have rights to the net assets of the arrangement. The Group reports its interests in a joint venture using equity method, except when the investment is classified as held for sale, in which case it is accounted for in accordance with PFRS 5, Non-current Assets Held for Sale and Discontinued Operations.

Under the equity method, an investment in joint venture is initially recognized in the statement of financial position at cost and adjusted thereafter to recognize the Group’s share of the profit or loss and other comprehensive income of the associate. When the Group’s share of losses of a joint venture exceeds the Group’s interest in that joint venture (which includes any long-term interests that, in substance, form part of the Group’s net investment in the joint venture), the Group discontinues recognizing its share of further losses. Additional losses are recognized only to the extent that the

18

Group has incurred legal or constructive obligations or made payments on behalf of the joint venture.

Any excess of the cost of acquisition over the Group’s share of the net fair value of the identifiable assets, liabilities and contingent liabilities of the joint venture recognized at the date of acquisition is recognized as goodwill. The goodwill is included within the carrying amount of the investment and is assessed for impairment as part of that investment. Any excess of the Group’s share of the net fair value of the identifiable assets, liabilities and contingent liabilities over the cost of acquisition, after reassessment, is recognized immediately in profit or loss.

Where the Group transacts with its jointly controlled entities, unrealized profits and losses are eliminated to the extent of the Group’s interest in the joint venture.

When the equity method is discontinued Group recognizes its retained interest at fair value. The difference between the carrying amount of the investment at the time the equity method was discontinued and the fair value of retained interest plus any proceeds from disposing of a part of interest is recognized in profit or loss. Amounts that were previously recognized in other comprehensive income in relation to the investment are accounted on the basis as would have been required if the investee had directly disposed of the related assets or liabilities.

The requirements of PAS 39 are applied to determine whether it is necessary to recognize any impairment loss with respect to the Group’s investment in joint venture. When necessary, the entire carrying amount of the investment (including goodwill) is tested for impairment in accordance with PAS 36, Impairment of Assets as a single asset by comparing its recoverable amount (higher of value in use and fair value less costs to sell) with its carrying amount. Any impairment loss recognized forms part of the carrying amount of the investment. Any reversal of that impairment loss is recognized in accordance with PAS 36 to the extent that the recoverable amount of the investment subsequently increases.

6.04 Inventories

Inventories are stated at the lower of cost or net realizable value. Costs, including an appropriate portion of fixed and variable overhead expenses, are determined using the first-in, first-out (FIFO) method. Net realizable value represents the estimated selling price for inventories less all estimated costs of completion and costs necessary to make the sale.

When the net realizable value of the inventories is lower than the cost, the Group provides for an allowance for the decline in the value of the inventory and recognizes the write-down as an expense in the statement of comprehensive income. The amount of any reversal of any write-down of inventories, arising from an increase in net realizable value, is recognized as a reduction in the amount of inventories recognized as an expense in the period in which the reversal occurs.

When inventories are sold, the carrying amount of those inventories is recognized as an expense in the period in which the related revenue is recognized.

19

6.05 Property, Plant and Equipment

Property, plant and equipment are initially measured at cost. The cost of an asset consists of its purchase price and costs directly attributable to bringing the asset to its working condition for its intended use. Subsequent to initial recognition property, plant and equipment are carried at cost less accumulated depreciation and accumulated impairment losses.

Subsequent expenditures relating to an item of property, plant and equipment that have already been recognized are added to the carrying amount of the asset when it is probable that future economic benefits, in excess of the originally assessed standard of performance of the existing asset, will flow to the Group. All other subsequent expenditures are recognized as expenses in the period in which those are incurred.

Major spare parts and stand-by equipment qualify as property, plant and equipment; when the Group expects to use them during more than one period. Similarly, if the spare parts and servicing equipment can be used only in connection with an item of property, plant and equipment, they are accounted for as property, plant and equipment.

Depreciation is computed on the straight-line method based on the estimated useful lives of the assets as follows:

Factory warehouse 20 years Building and improvements 15 years Transportation equipment 5 years Machines, tools and equipment 5 years

Stand-by equipment is depreciated from the date it is made available for use over the shorter of the life of the stand-by equipment or the life of the asset the stand-by equipment is part of while major spare parts are depreciated over the period starting when it is brought into service, continuing over the lesser of its useful life and the remaining expected useful life of the asset to which it relates.

The assets’ residual values, useful lives and depreciation methods are reviewed, and adjusted prospectively if appropriate, if there is an indication of a significant change since the last reporting date.

An item of property, plant and equipment is derecognized on disposal, or when no future economic benefits are expected from use or disposal. Gains or losses arising from derecognition of a property, plant and equipment are measured as the difference between the net disposal proceeds and the carrying amount of the asset and are recognized in profit or loss.

6.06 Impairment of Assets

At each reporting date, the Group assesses whether there is any indication that any assets other than inventories and financial assets that are within the scope of PAS 39, Financial Instruments: Recognition and Measurement may have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss, if any. Where it is not possible to estimate the recoverable amount of an individual asset, the Group estimates the recoverable amount of the cash-generating unit to which the asset belongs. When a reasonable and consistent basis of allocation can be identified, assets are also allocated to individual cash-generating units, or otherwise they are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation basis can be identified.

20

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset or cash-generating unit is estimated to be less than its carrying amount, the carrying amount of the asset or cash-generating unit is reduced to its recoverable amount. An impairment loss is recognized as an expense.

When an impairment loss subsequently reverses, the carrying amount of the asset or cash-generating unit is increased to the revised estimate of its recoverable amount, but the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognized for the asset or cash-generating unit in prior years. A reversal of an impairment loss is recognized as an income.

6.07 Borrowing Costs

All other borrowing costs are recognized in profit or loss in the period in which they are incurred.

6.08 Financial Liabilities and Equity Instruments

6.08.01 Classification as Debt or Equity

Debt and equity instruments are classified as either financial liabilities or as equity in accordance with the substance of the contractual arrangements.

6.08.02 Financial Liabilities

Financial liabilities are classified as either financial liabilities ‘at FVTPL’ or ‘other financial liabilities’.

The Group’s financial liabilities include trade and other payables (except for due to government agencies), due to a related party, loans payable, other non-current liability.

6.08.03 Other Financial Liabilities

Other financial liabilities are initially measured at fair value inclusive of directly attributable transaction costs.

Other financial liabilities are subsequently measured at amortized cost using the effective interest method, with finance cost recognized on an effective yield basis.

The effective interest method is a method of calculating the amortized cost of a financial liability and of allocating finance cost over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments through the expected life of the financial liability, or, where appropriate, a shorter period to the net carrying amount on initial recognition.

21

6.08.04 Derecognition of Financial Liabilities

The Group derecognizes financial liabilities when, and only when, the Group’s obligations are discharged, cancelled or expired. When an existing liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability. The difference between the carrying amount of the financial liability derecognized and the consideration paid and payable is recognized in profit or loss.

6.08.05 Equity Instruments

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. Equity instruments issued by the Group are recognized at the proceeds received, net of direct issue costs.

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or options are shown in equity as a deduction from the proceeds, net of tax.

6.09 Employee Benefits

6.09.01 Short-term Benefits

The Group recognizes a liability net of amounts already paid and an expense for services rendered by employees during the accounting period. Short-term benefits given by the Group to its employees include salaries and wages, SSS, PhilHealth, and Pag-ibig contributions and other employee benefits.

6.09.02 Post-employment Benefits

The Group has an unfunded and non-contributory defined benefit retirement plan. This benefit defines an amount of pension benefit that an employee will receive on retirement, usually dependent on one or more factors such as age, years of service and compensation.

The cost of providing benefits is determined using the Projected Unit Credit Method which reflects services rendered by employees to the date of valuation and incorporates assumptions concerning employees’ projected salaries. Post-employment expenses include current service cost, past service cost, and net interest on defined benefit asset/liability. Remeasurements which include cumulative actuarial gains and losses, return on plan assets, and changes in the effects of asset ceiling are recognized directly in other comprehensive income and is also presented under equity in the separate statement of financial position.

Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions are charged or credited to equity in OCI in the period in which they arise.

Past-service costs are recognized immediately in profit or loss.

The liability recognized in the statement of financial position in respect of defined benefit pension plans is the present value of the defined benefit obligation at the end of the reporting period. The defined benefit obligation is calculated annually by an independent actuary using the projected unit credit method. The present value of the defined benefit obligation is determined by discounting the estimated future cash outflows using interest rates of government securities, equity securities and other securities that are denominated in the currency in which the benefits will be paid, and that have terms to maturity approximating to the terms of the related pension obligation.

22

6.10 Provisions and Contingencies

Provisions are recognized when the Group has a present obligation, whether legal or constructive, as a result of a past event, it is probable that the Group will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation.

The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation at the end of the reporting period, taking into account the risks and uncertainties surrounding the obligation. Where a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows.

When some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, a receivable is recognized as an asset if it is virtually certain that reimbursement will be received and the amount of the receivable can be measured reliably.

Provisions are reviewed at each reporting date and adjusted to reflect the current best estimate.

6.11 Revenue Recognition

Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Group and the revenue can be measured reliably. Revenue is measured at the fair value of the consideration received or receivable and represents amounts receivable for goods and services provided in the normal course of business. Revenue is reduced for estimated customer returns, rebates and other similar allowances.

The gross inflows of economic benefits include amounts collected on behalf of the principal and which do not result in increases in equity for the Group. The amounts collected on behalf of the principal are not revenue. Instead, revenue is the amount of commission.

6.11.01 Sale of Goods

Revenue from the sale of goods is recognized when all the following conditions are satisfied:

x the Group has transferred to the buyer the significant risks and rewards of ownership of the goods;

x the Group retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold;

x the amount of revenue can be measured reliably;

x it is probable that the economic benefits associated with the transaction will flow to the Group; and

x the costs incurred or to be incurred in respect of the transaction can be measured reliably.

ACPI derives its revenue from sale of goods encompasses sale of hardware and point-of-sale (POS) software.

PII derives its revenue from sale of goods pertains to sale of manufactured and purchased classes of scientific, medical, educational, electronics, laboratory, research, testing and measuring machineries, equipment, apparatus, furniture and fixtures, including their accessories, attachments and spare parts, as well as in any and all articles, goods, wares and merchandise.

23

6.11.02 Rendering of Services

Revenue from a contract to provide services is recognized by reference to the stage of completion of the contract. Revenue from rendering of services is recognized when all the following conditions are satisfied:

x the amount of revenue can be measured reliably;

x it is probable that the economic benefits associated with the transaction will flow to the Group;

x the stage of completion of the transaction can be measured reliably; and

x the costs incurred for the transaction and the costs to complete the transaction can be measured reliably.

ACPI derives its revenue from service pertains to installation, check-ups and repairs and maintenance of machineries, equipment and apparatus sold.

PII derives its revenue from rendering of services encompasses sale of licenses, implementation and the maintenance fees of Barter™ MMS, and sale of customized POS software for a specified customer.

6.11.03 Finance Income

Finance income is recognized when it is probable that the economic benefits will flow to the Group and the amount of revenue can be measured reliably. Finance income is accrued on a time proportion basis, by reference to the principal outstanding and at the effective interest rate applicable, which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial asset to that asset’s net carrying amount on initial recognition.

6.12 Expense Recognition

Expense encompasses losses as well as those expenses that arise in the course of the ordinary activities of the Group.

The Group recognizes expenses in the statement of comprehensive income when a decrease in future economic benefits related to a decrease in an asset or an increase of a liability has arisen that can be measured reliably.

6.13 Leases

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. All other leases are classified as operating leases.

6.13.01 The Group as a Lessee

Assets held under finance leases are initially recognized as assets of the Group at their fair value at the inception of the lease or, if lower, at the present value of the minimum lease payments. The corresponding liability to the lessor is included in the statements of financial position as a finance lease obligation.

Lease payments are apportioned between finance expenses and reduction of the lease obligation so as to achieve a constant rate of interest on the remaining balance of the liability. Finance expenses are recognized immediately in profit or loss.

24

Operating lease payments are recognized as an expense on a straight-line basis over the lease term, except where another systematic basis is more representative of the time pattern in which economic benefits from the leased asset are consumed. Contingent rentals arising under operating leases are recognized as an expense in the period in which they are incurred.

In the event that lease incentives are received to enter into operating leases, such incentives are recognized as a liability. The aggregate benefit of incentives is recognized as a reduction of rental expense on a straight-line basis, except where another systematic basis is more representative of the time pattern in which economic benefits from the leased asset are consumed.

6.14 Foreign Currency Transactions and Translation

In preparing the financial statements of the Group, transactions in currencies other than the Group’s functional currency, i.e. foreign currencies, are recognized at the rates of exchange prevailing at the dates of the transactions. At the end of each reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at that date.

Exchange differences are recognized in profit or loss in the period in which they arise.

6.15 Related Parties and Related Party Transactions

A related party is a person or entity that is related to the Group that is preparing its financial statements. A person or a close member of that person’s family is related to Group if that person has control or joint control over the Group, has significant influence over the Group, or is a member of the key management personnel of the Group or of a parent of the Group.

An entity is related to the Group if any of the following conditions applies:

x The entity and the Group are members of the same group (which means that each parent, subsidiary and fellow subsidiary is related to the others).

x One entity is an associate or joint venture of the other entity (or an associate or joint venture of a member of a group of which the other entity is a member).

x Both entities are joint ventures of the same third party.

x One entity is a joint venture of a third entity and the other entity is an associate of the third entity.

x The entity is a post-employment benefit plan for the benefit of employees of either the Group or an entity related to the Group. If the Group is itself such a plan, the sponsoring employers are also related to the Group.

x The entity is controlled or jointly controlled by a person identified above.

x A person identified above has significant influence over the entity or is a member of the key management personnel of the entity (or of a parent of the entity).

x Management entity providing key management personnel services to a reporting entity.

Close members of the family of a person are those family members, who may be expected to influence, or be influenced by, that person in their dealings with the Group and include that person’s children and spouse or domestic partner; children of that person’s spouse or domestic partner; and dependents of that person or that person’s spouse or domestic partner.

25

A related party transaction is a transfer of resources, services or obligations between related parties, regardless of whether a price is charged.

6.16 Taxation

Income tax expense represents the sum of current and deferred tax.

6.16.01 Current Tax

The tax currently payable is based on taxable profit for the year. Taxable profit differs from profit as reported in the statement of comprehensive income because of items of income or expense that are taxable or deductible in other years and items that are never taxable or deductible. The Group’s liability for current tax is calculated using tax rates that have been enacted or substantively enacted by the end of the reporting period.

6.16.02 Deferred Tax

Deferred tax is recognized on temporary differences between the carrying amounts of assets and liabilities in the financial statements and the corresponding tax bases used in the computation of taxable profit. Deferred tax liabilities are generally recognized for all taxable temporary differences. Deferred tax assets are generally recognized for all deductible temporary differences, carry forward of unused tax credits from excess Minimum Corporate Income Tax (MCIT) over Regular Corporate Income Tax (RCIT) and unused Net Operating Loss Carryover (NOLCO), to the extent that it is probable that taxable profits will be available against which those deductible temporary differences and carry forward of unused MCIT and unused NOLCO can be utilized. Deferred income tax, however, is not recognized when it arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction that affects neither the accounting profit nor taxable profit or loss.