alternative lending in japan - store & retrieve data anywhere · lucky bank, aqush, crowdcredit...

TRANSCRIPT

Alternative Lending in Japan

Koichiro (Kay) Okamoto Chief Executive Officer Yayoi Co., Ltd.

April 12th, 2016

© 2016 Yayoi Co., Ltd. All rights reserved.

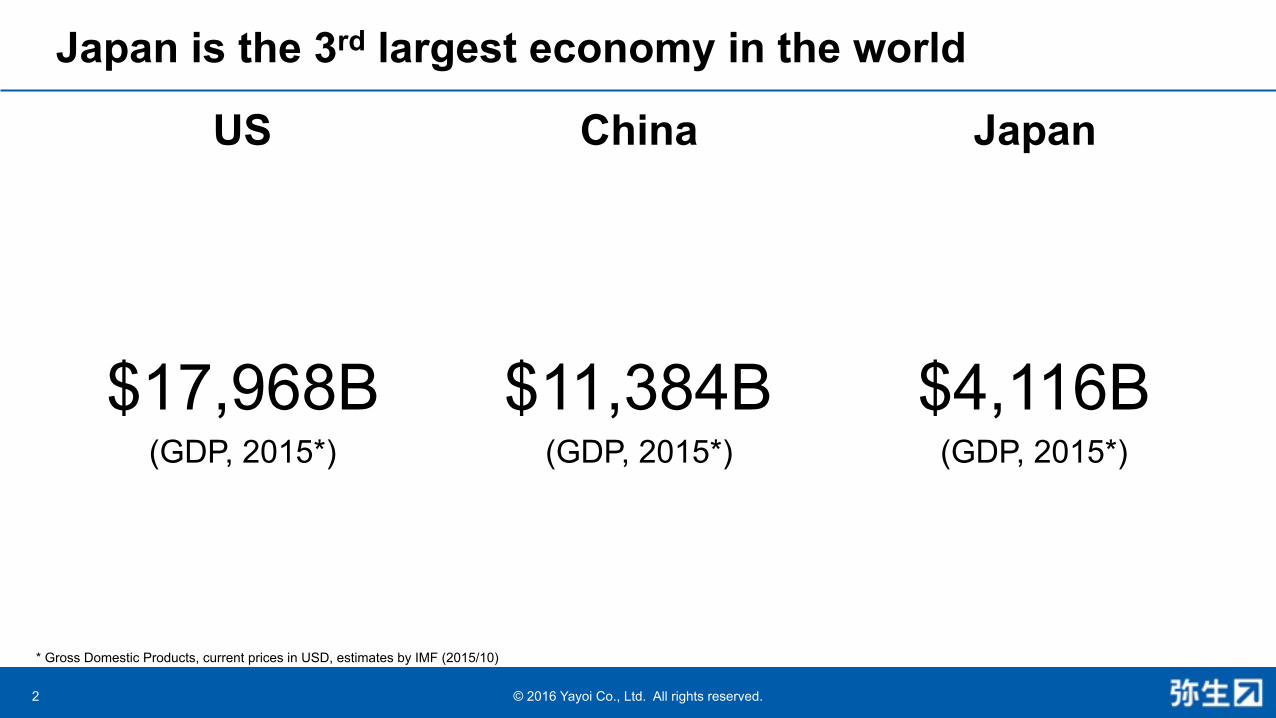

Japan is the 3rd largest economy in the world

$17,968B (GDP, 2015*)

$4,116B (GDP, 2015*)

US Japan

2

$11,384B (GDP, 2015*)

China

* Gross Domestic Products, current prices in USD, estimates by IMF (2015/10)

© 2016 Yayoi Co., Ltd. All rights reserved.

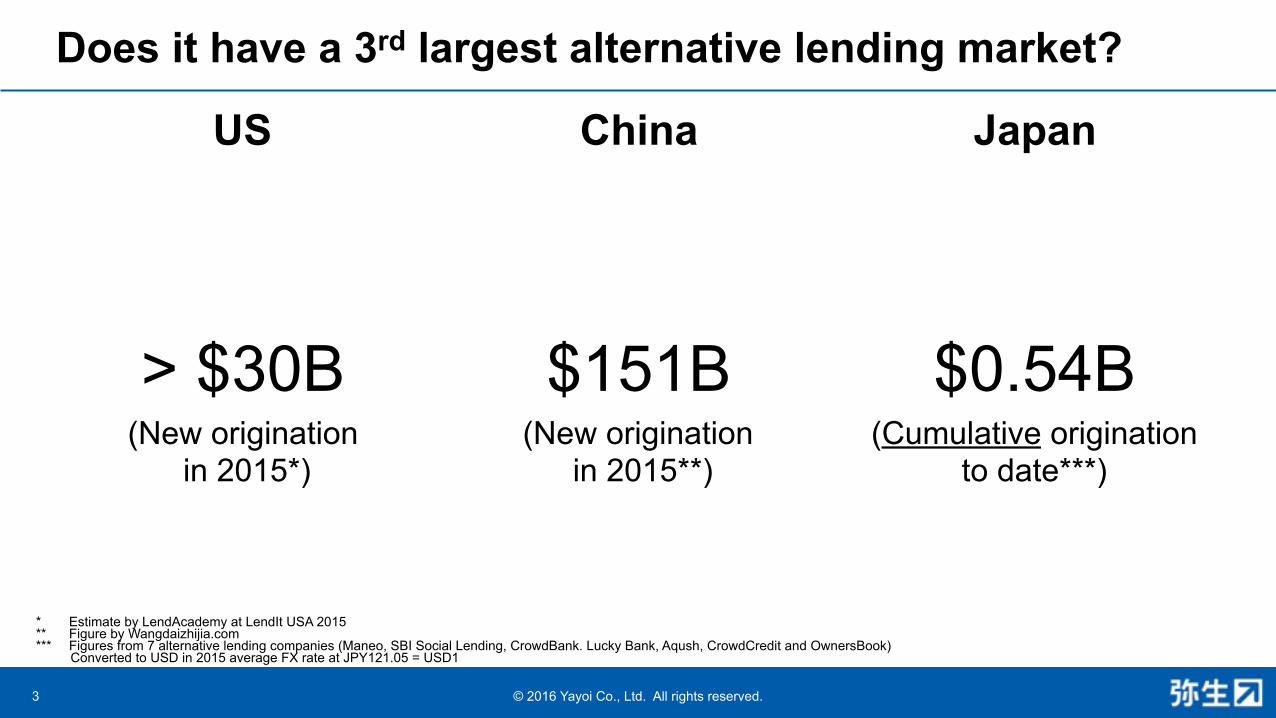

Does it have a 3rd largest alternative lending market?

> $30B (New origination

in 2015*)

$0.54B (Cumulative origination

to date***)

US Japan

3

$151B (New origination

in 2015**)

China

* Estimate by LendAcademy at LendIt USA 2015 ** Figure by Wangdaizhijia.com *** Figures from 7 alternative lending companies (Maneo, SBI Social Lending, CrowdBank. Lucky Bank, Aqush, CrowdCredit and OwnersBook)

Converted to USD in 2015 average FX rate at JPY121.05 = USD1

© 2016 Yayoi Co., Ltd. All rights reserved.

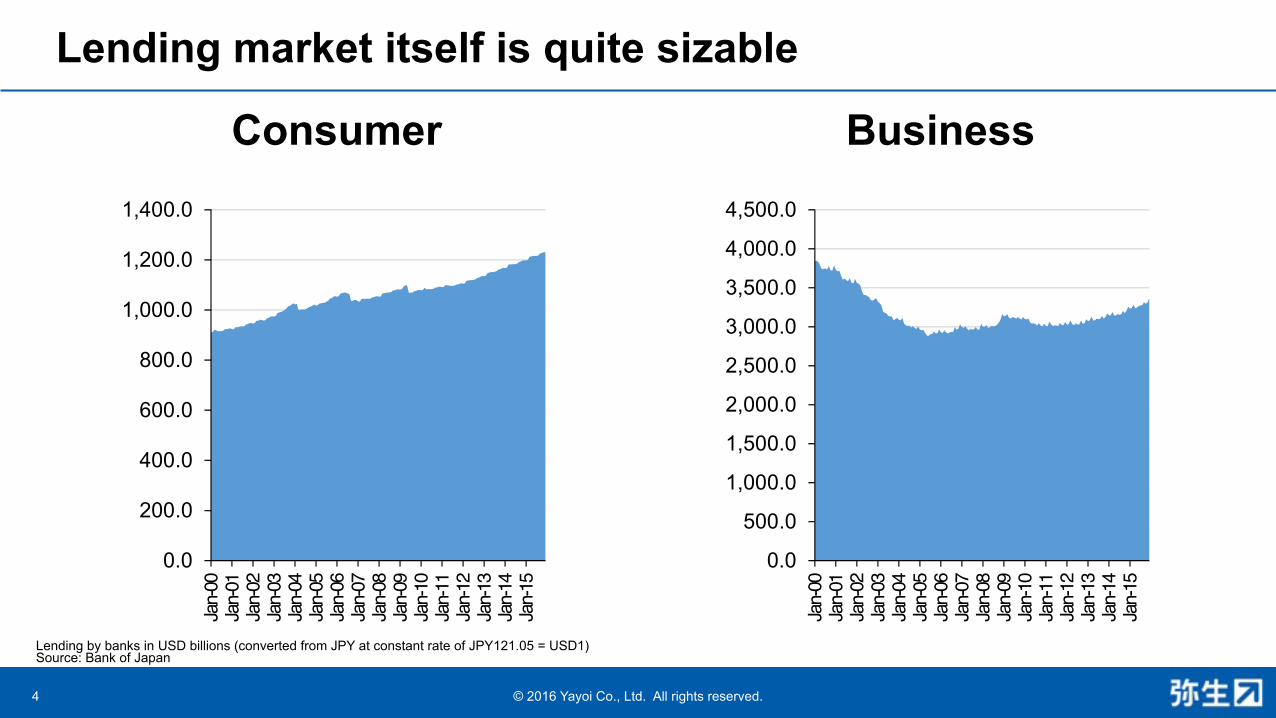

Lending market itself is quite sizable

Consumer Business

4

Lending by banks in USD billions (converted from JPY at constant rate of JPY121.05 = USD1) Source: Bank of Japan

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

4,000.0

4,500.0

Jan-00

Jan-01

Jan-02

Jan-03

Jan-04

Jan-05

Jan-06

Jan-07

Jan-08

Jan-09

Jan-10

Jan-11

Jan-12

Jan-13

Jan-14

Jan-15

© 2016 Yayoi Co., Ltd. All rights reserved.

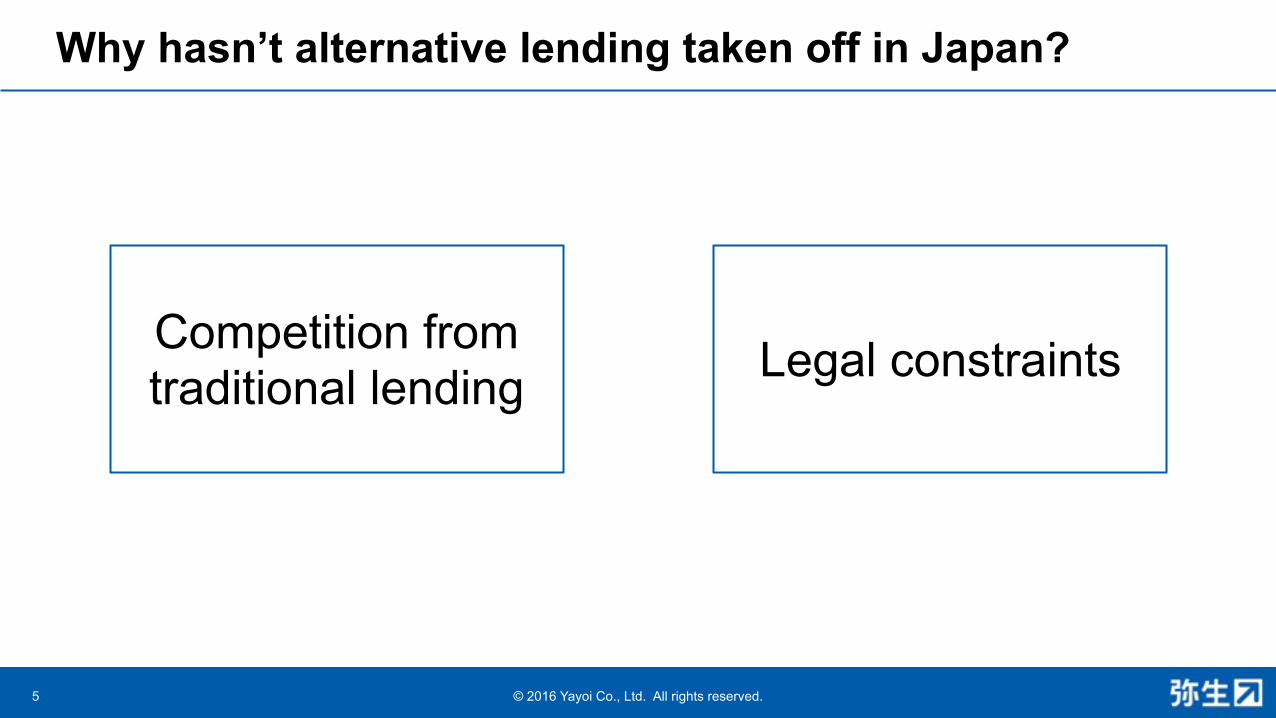

Why hasn’t alternative lending taken off in Japan?

5

Competition from traditional lending Legal constraints

© 2016 Yayoi Co., Ltd. All rights reserved.

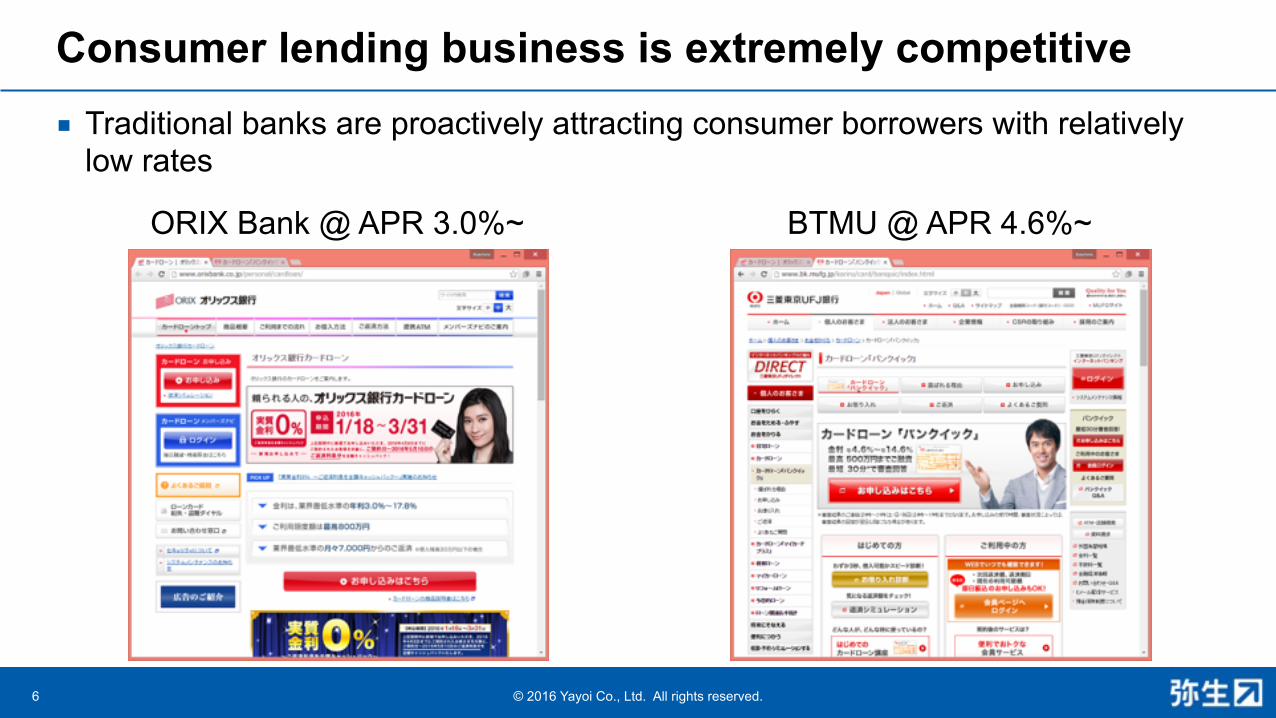

Consumer lending business is extremely competitive■ Traditional banks are proactively attracting consumer borrowers with relatively

low rates

6

ORIX Bank @ APR 3.0%~ BTMU @ APR 4.6%~

© 2016 Yayoi Co., Ltd. All rights reserved.

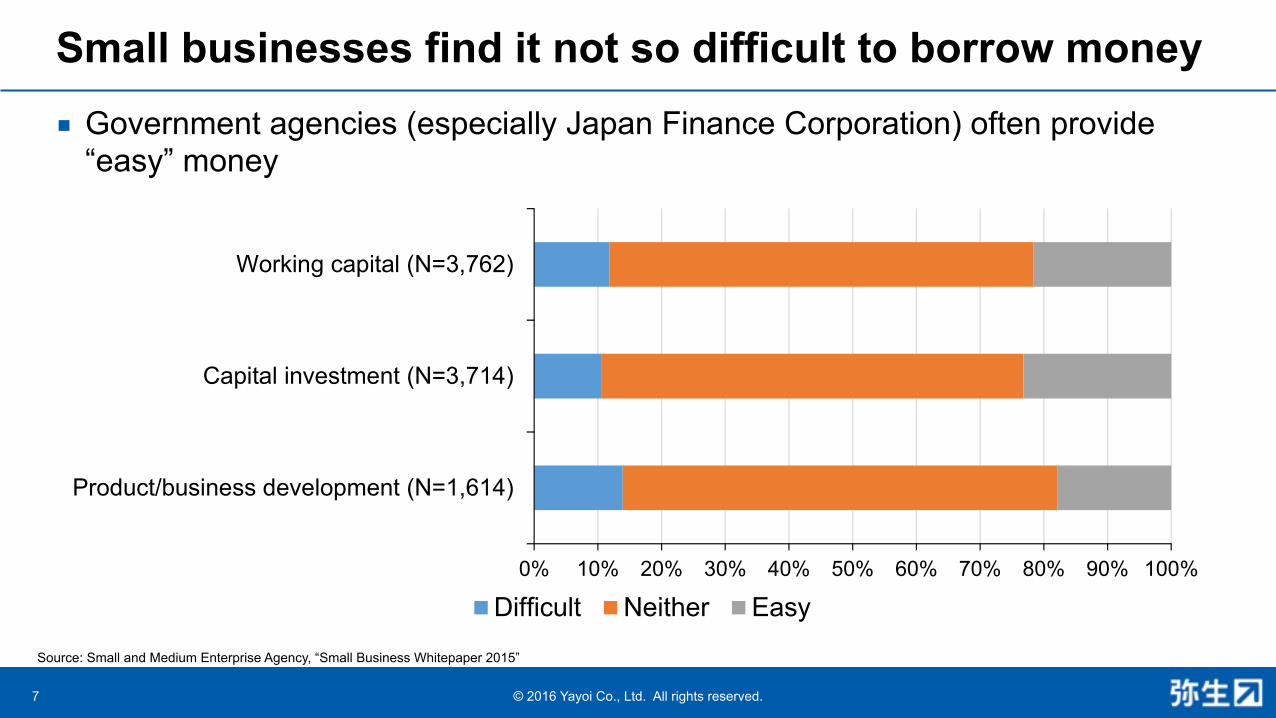

Small businesses find it not so difficult to borrow money■ Government agencies (especially Japan Finance Corporation) often provide

“easy” money

7

Source: Small and Medium Enterprise Agency, “Small Business Whitepaper 2015”

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Product/business development (N=1,614)

Capital investment (N=3,714)

Working capital (N=3,762)

Difficult Neither Easy

© 2016 Yayoi Co., Ltd. All rights reserved.

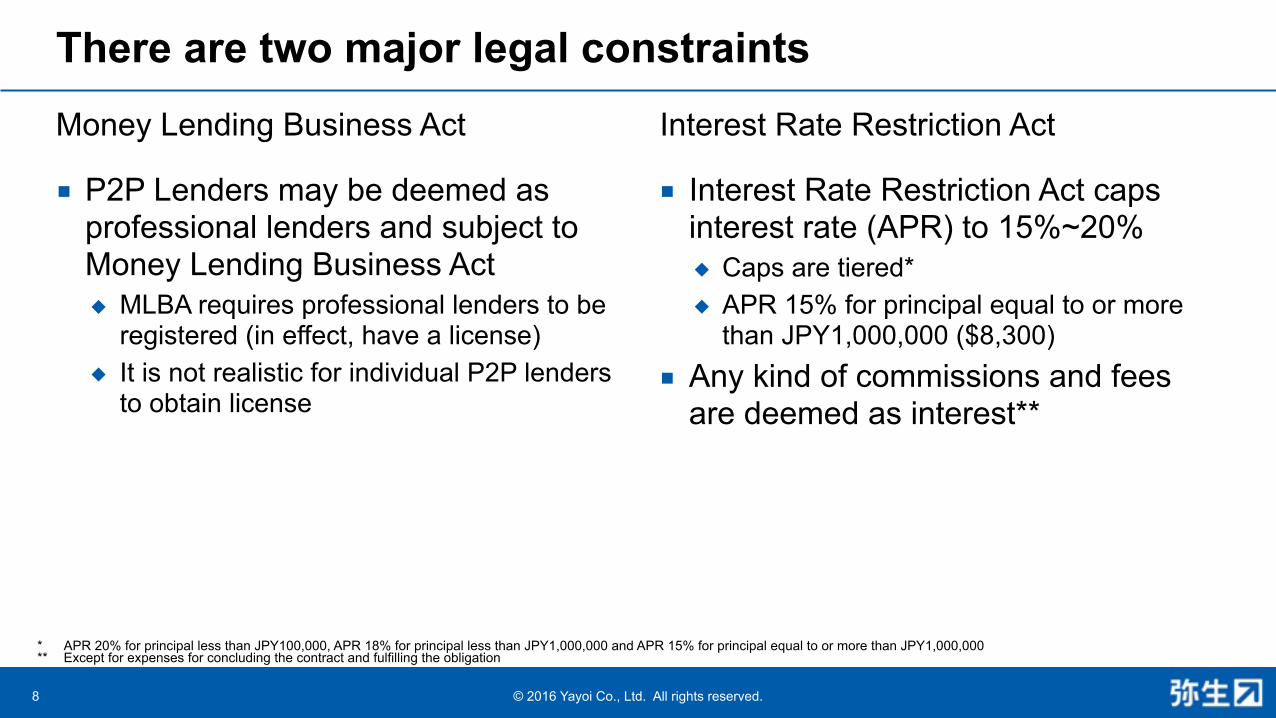

There are two major legal constraints

■ P2P Lenders may be deemed as professional lenders and subject to Money Lending Business Act ◆ MLBA requires professional lenders to be

registered (in effect, have a license) ◆ It is not realistic for individual P2P lenders

to obtain license

■ Interest Rate Restriction Act caps interest rate (APR) to 15%~20% ◆ Caps are tiered* ◆ APR 15% for principal equal to or more

than JPY1,000,000 ($8,300) ■ Any kind of commissions and fees

are deemed as interest**

Money Lending Business Act Interest Rate Restriction Act

8

* APR 20% for principal less than JPY100,000, APR 18% for principal less than JPY1,000,000 and APR 15% for principal equal to or more than JPY1,000,000 ** Except for expenses for concluding the contract and fulfilling the obligation

© 2016 Yayoi Co., Ltd. All rights reserved.

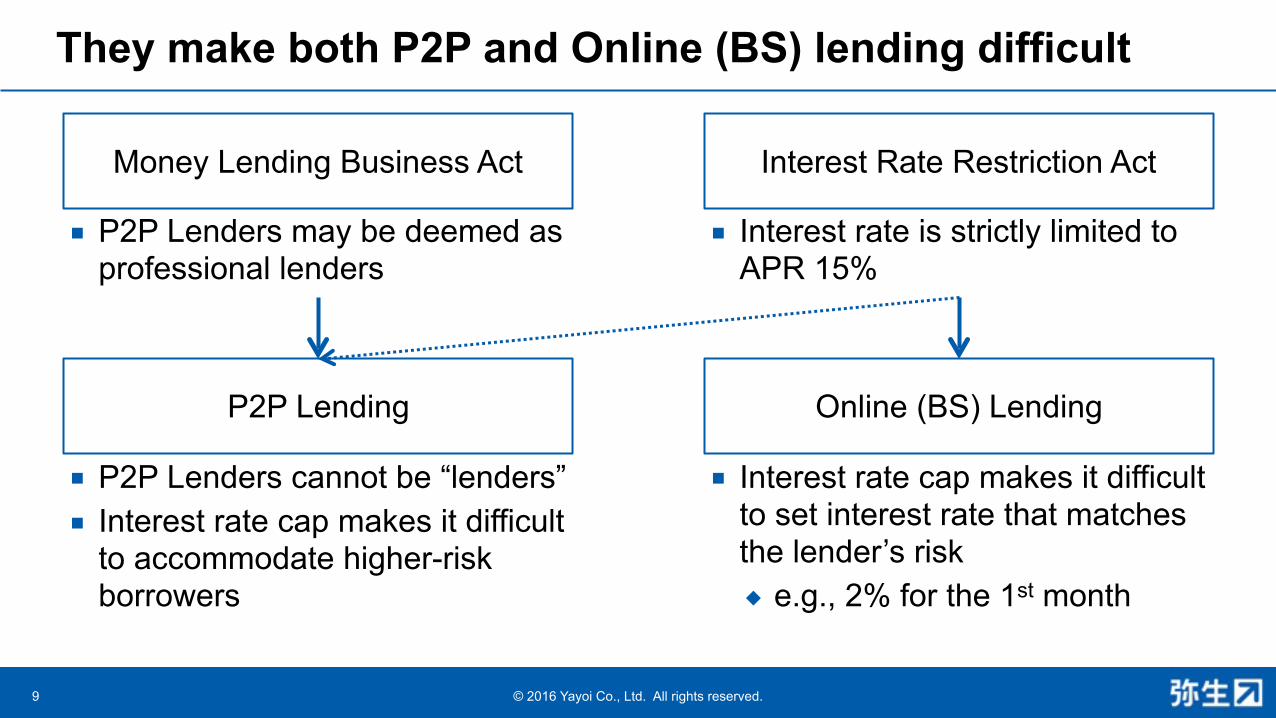

They make both P2P and Online (BS) lending difficult

9

Money Lending Business Act

■ P2P Lenders may be deemed as professional lenders

Interest Rate Restriction Act

■ Interest rate is strictly limited to APR 15%

P2P Lending Online (BS) Lending

■ P2P Lenders cannot be “lenders” ■ Interest rate cap makes it difficult

to accommodate higher-risk borrowers

■ Interest rate cap makes it difficult to set interest rate that matches the lender’s risk ◆ e.g., 2% for the 1st month

© 2016 Yayoi Co., Ltd. All rights reserved.

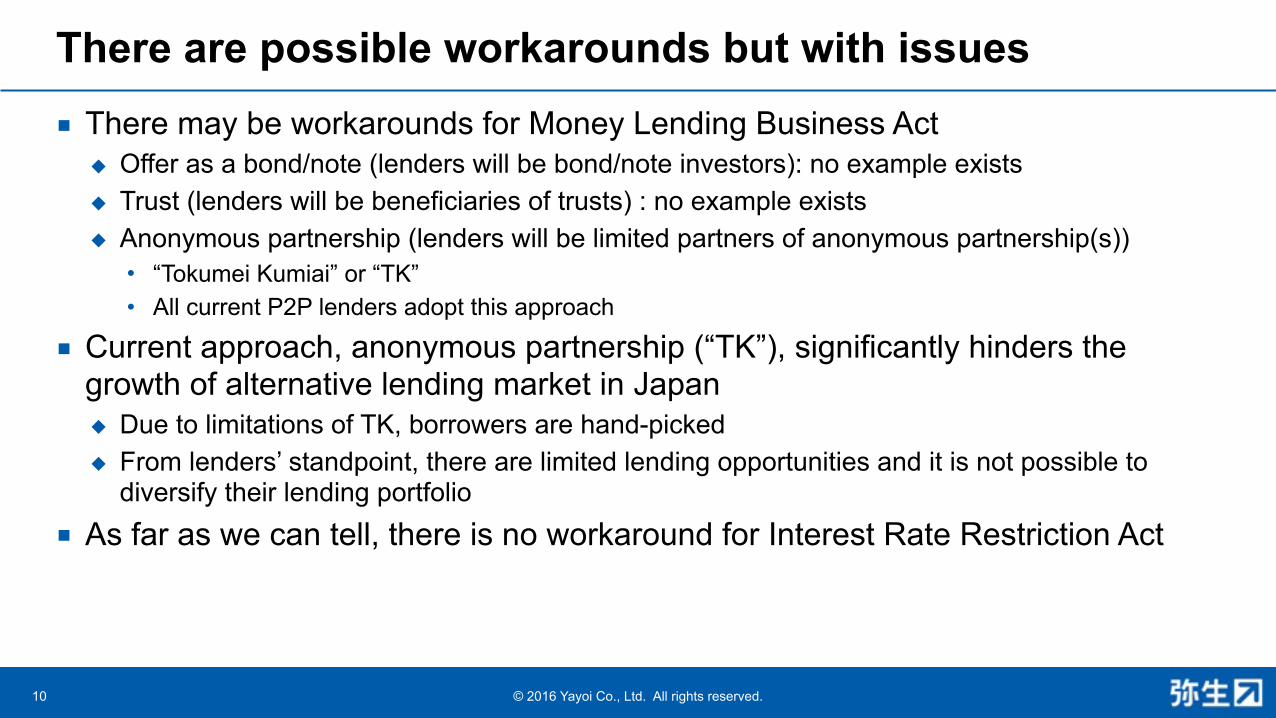

There are possible workarounds but with issues■ There may be workarounds for Money Lending Business Act ◆ Offer as a bond/note (lenders will be bond/note investors): no example exists ◆ Trust (lenders will be beneficiaries of trusts) : no example exists ◆ Anonymous partnership (lenders will be limited partners of anonymous partnership(s))

• “Tokumei Kumiai” or “TK” • All current P2P lenders adopt this approach

■ Current approach, anonymous partnership (“TK”), significantly hinders the growth of alternative lending market in Japan ◆ Due to limitations of TK, borrowers are hand-picked ◆ From lenders’ standpoint, there are limited lending opportunities and it is not possible to

diversify their lending portfolio ■ As far as we can tell, there is no workaround for Interest Rate Restriction Act

10

Alternative lending in Japan: New Hope

© 2016 Yayoi Co., Ltd. All rights reserved.

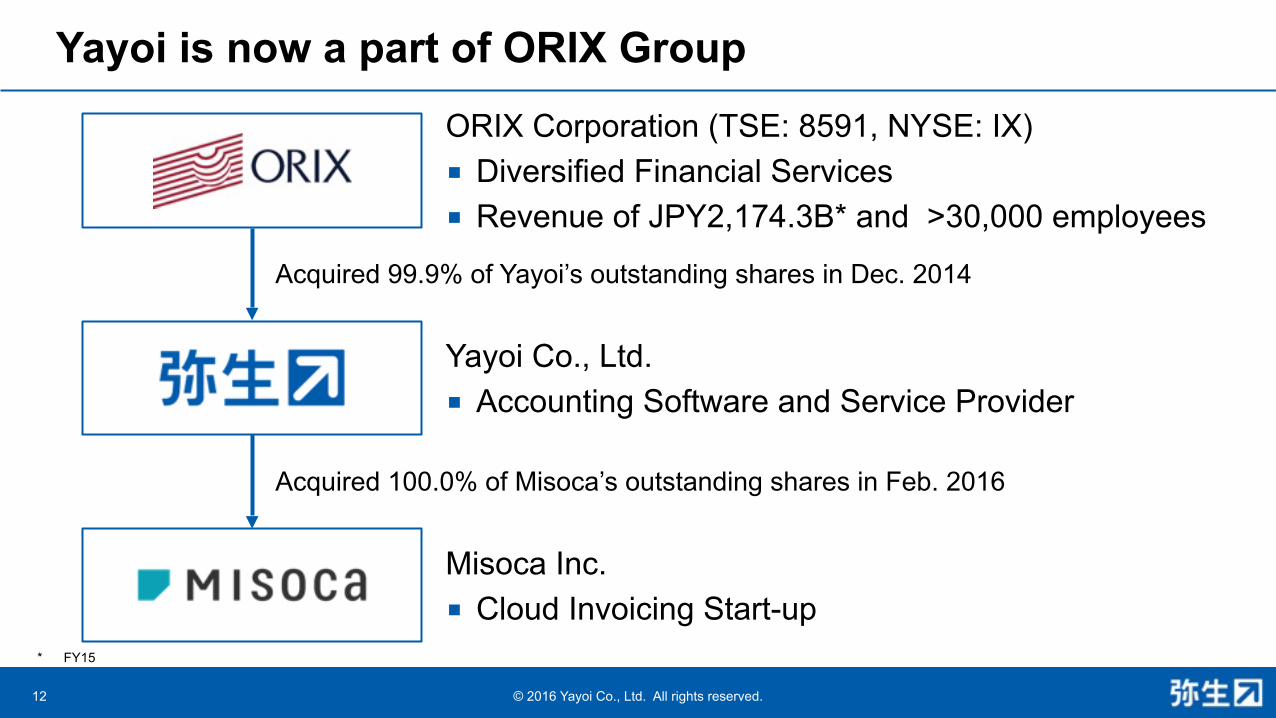

Yayoi is now a part of ORIX Group

12

ORIX Corporation (TSE: 8591, NYSE: IX) ■ Diversified Financial Services ■ Revenue of JPY2,174.3B* and >30,000 employees

Yayoi Co., Ltd. ■ Accounting Software and Service Provider

Misoca Inc. ■ Cloud Invoicing Start-up

Acquired 99.9% of Yayoi’s outstanding shares in Dec. 2014

Acquired 100.0% of Misoca’s outstanding shares in Feb. 2016

* FY15

© 2016 Yayoi Co., Ltd. All rights reserved.

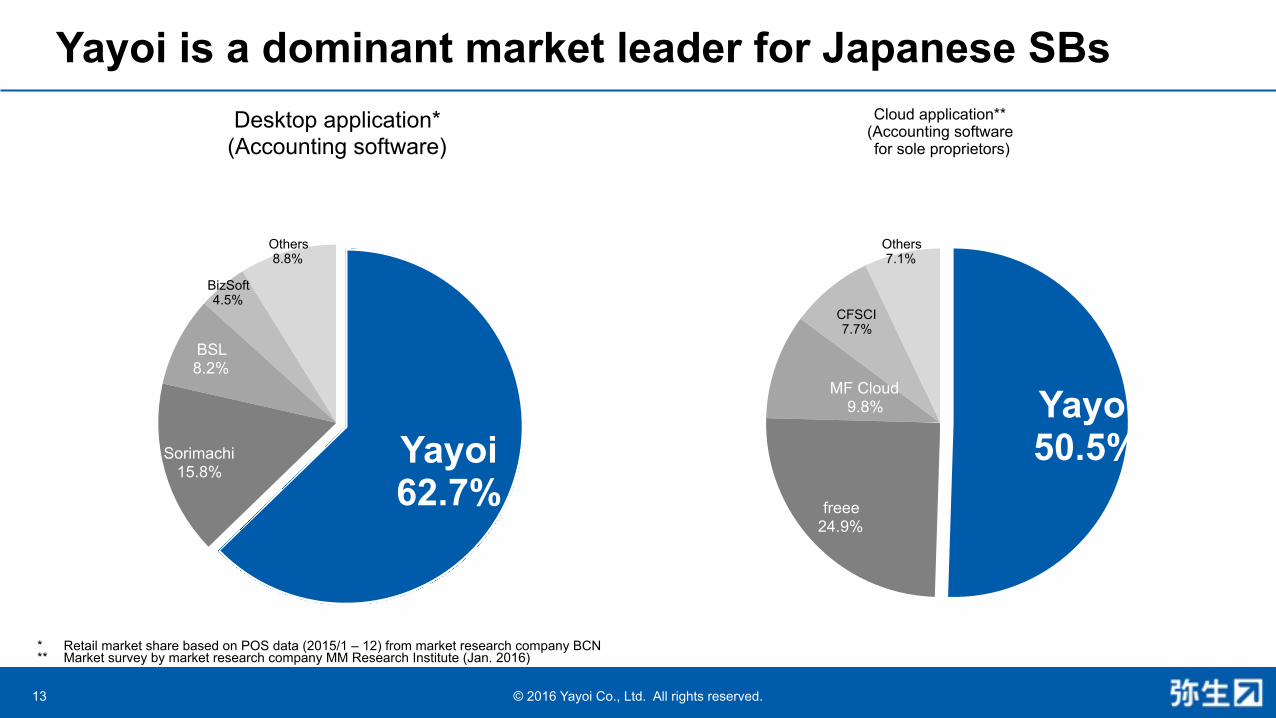

Yayoi is a dominant market leader for Japanese SBs

Others 8.8%

BizSoft 4.5%

BSL 8.2%

Sorimachi 15.8%

Yayoi 62.7%

Others 7.1%

CFSCI 7.7%

MF Cloud 9.8%

freee 24.9%

Yayoi 50.5%

Desktop application*(Accounting software)

Cloud application**(Accounting software for sole proprietors)

13

* Retail market share based on POS data (2015/1 – 12) from market research company BCN ** Market survey by market research company MM Research Institute (Jan. 2016)

© 2016 Yayoi Co., Ltd. All rights reserved.

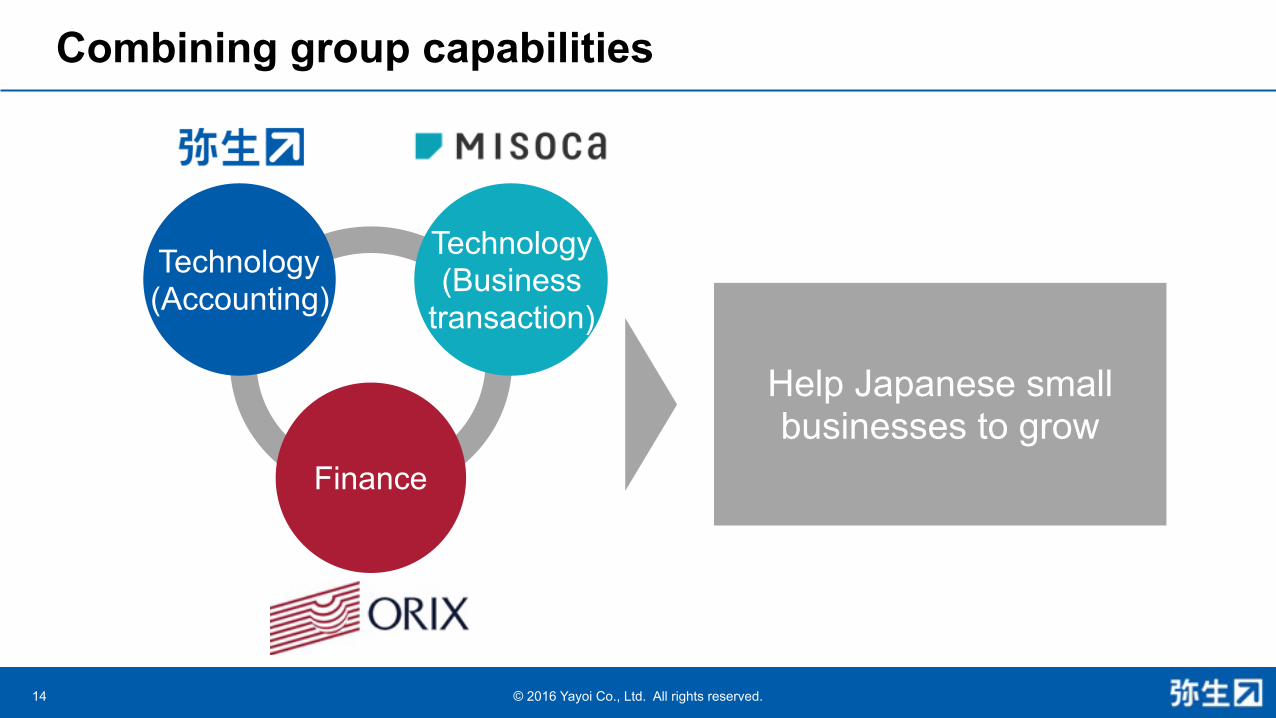

Help Japanese small businesses to grow

Combining group capabilities

14

Technology (Accounting)

Technology (Business

transaction)

Finance

© 2016 Yayoi Co., Ltd. All rights reserved.

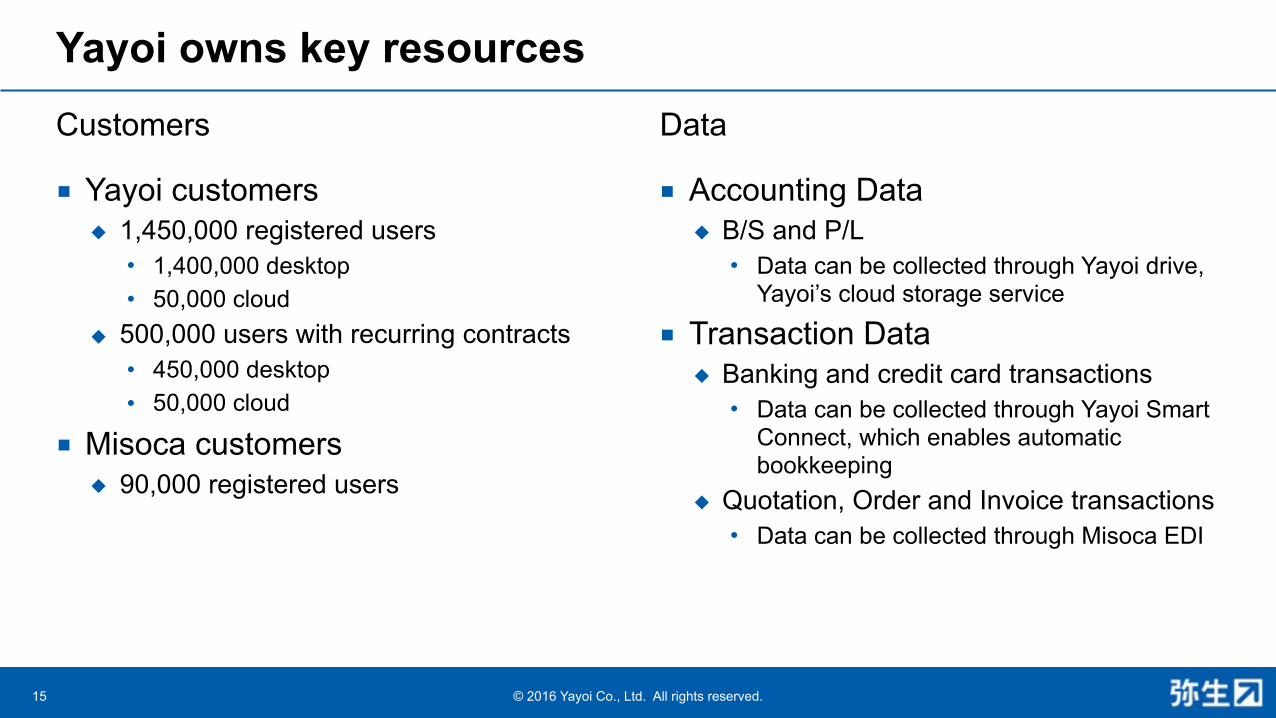

Yayoi owns key resources

■ Yayoi customers ◆ 1,450,000 registered users

• 1,400,000 desktop • 50,000 cloud

◆ 500,000 users with recurring contracts • 450,000 desktop • 50,000 cloud

■ Misoca customers ◆ 90,000 registered users

■ Accounting Data ◆ B/S and P/L

• Data can be collected through Yayoi drive, Yayoi’s cloud storage service

■ Transaction Data ◆ Banking and credit card transactions

• Data can be collected through Yayoi Smart Connect, which enables automatic bookkeeping

◆ Quotation, Order and Invoice transactions • Data can be collected through Misoca EDI

Customers Data

15

© 2016 Yayoi Co., Ltd. All rights reserved.

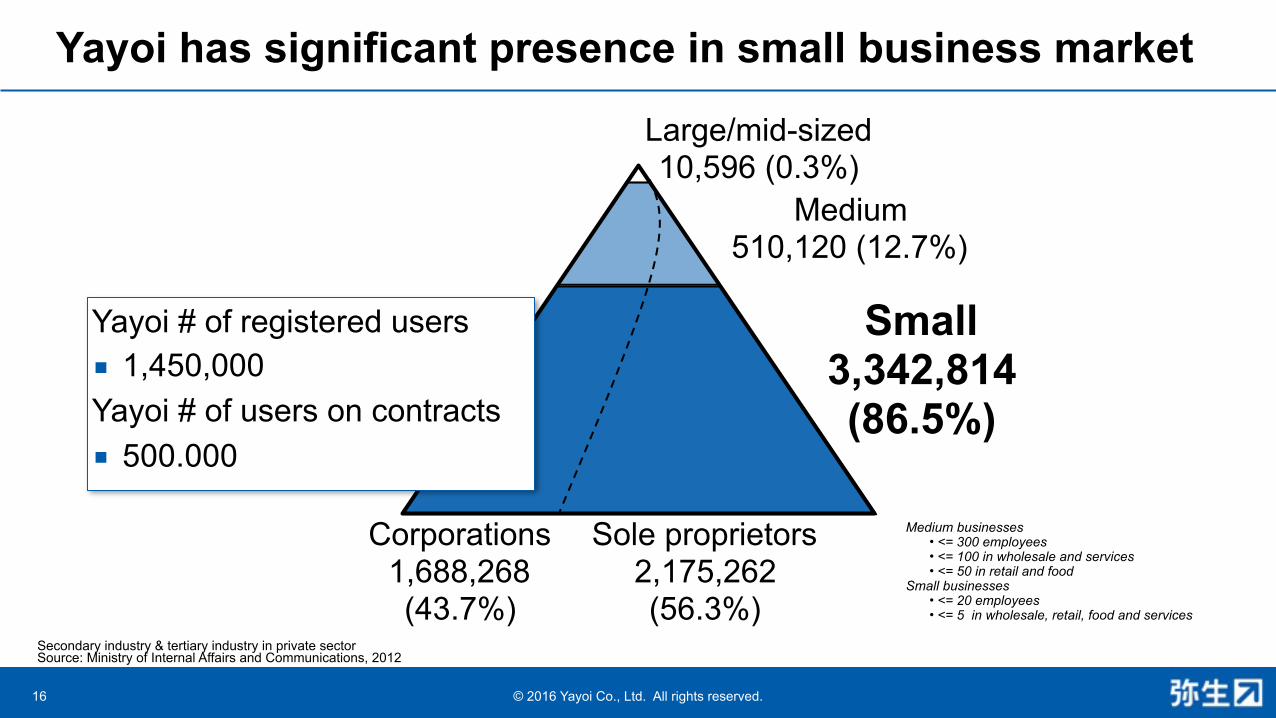

Yayoi has significant presence in small business market

Small 3,342,814 (86.5%)

Medium 510,120 (12.7%)

Large/mid-sized 10,596 (0.3%)

Corporations 1,688,268 (43.7%)

Sole proprietors 2,175,262 (56.3%)

16

Medium businesses • <= 300 employees • <= 100 in wholesale and services • <= 50 in retail and food

Small businesses • <= 20 employees • <= 5 in wholesale, retail, food and services

Secondary industry & tertiary industry in private sector Source: Ministry of Internal Affairs and Communications, 2012

Yayoi # of registered users ■ 1,450,000 Yayoi # of users on contracts ■ 500.000

© 2016 Yayoi Co., Ltd. All rights reserved.

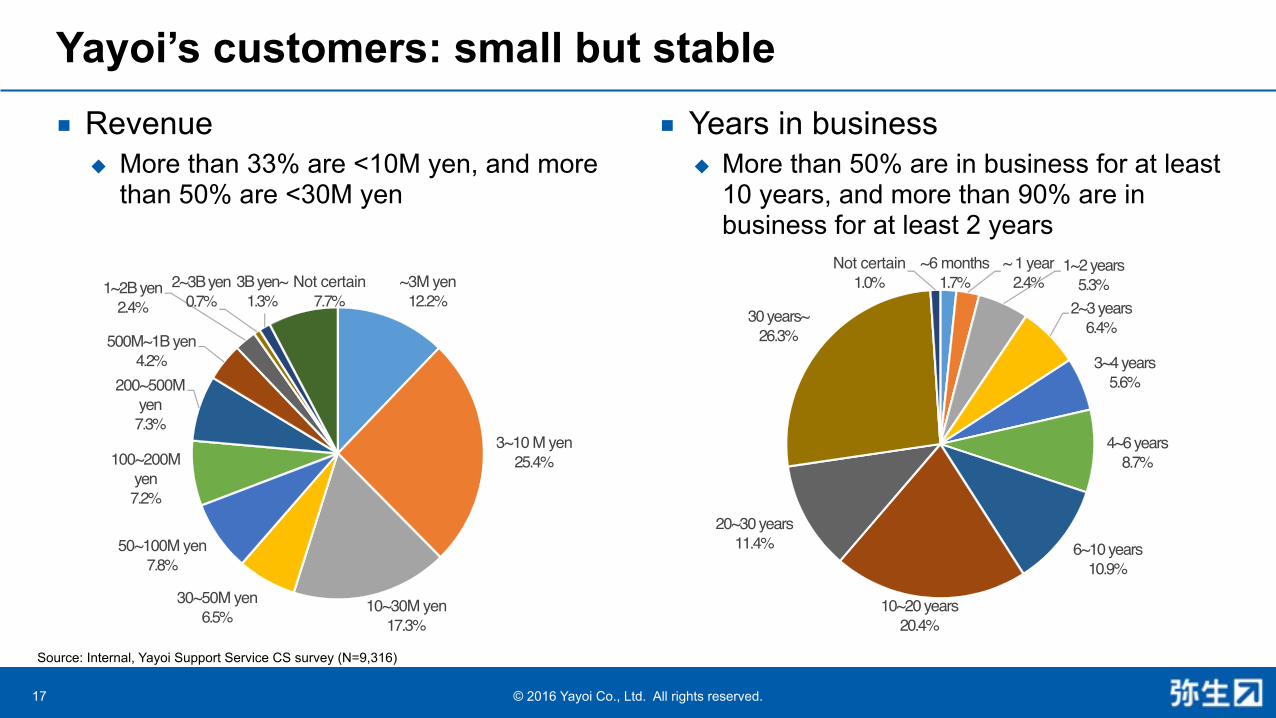

Yayoi’s customers: small but stable■ Revenue ◆ More than 33% are <10M yen, and more

than 50% are <30M yen

■ Years in business ◆ More than 50% are in business for at least

10 years, and more than 90% are in business for at least 2 years

17

Source: Internal, Yayoi Support Service CS survey (N=9,316)

~3M yen12.2%

3~10 M yen25.4%

10~30M yen17.3%

30~50M yen6.5%

50~100M yen7.8%

100~200M yen7.2%

200~500M yen7.3%

500M~1B yen4.2%

1~2B yen2.4%

2~3B yen0.7%

3B yen~1.3%

Not certain7.7%

~6 months1.7%

~ 1 year2.4%

1~2 years5.3%

2~3 years6.4%

3~4 years5.6%

4~6 years8.7%

6~10 years10.9%

10~20 years20.4%

20~30 years11.4%

30 years~26.3%

Not certain1.0%

© 2016 Yayoi Co., Ltd. All rights reserved.

There are demands■ Not all small businesses have solid

relationships with banks■ Not all small businesses rely on bank

loans* ◆ Half of who do have some grumbles

18

46%

10%

27%

22%

27%

68%

0%

20%

40%

60%

80%

100%

Corporation Sole proprietorSolid relationship with Banks Some Relationship with Banks

Limited relationship with Banks* Figures for short-term loans Source: Internal, Web survey to Yayoi registered customers (N=7,609)

49%

16%

36%

54%

15%30%

0%

20%

40%

60%

80%

100%

Corporation Sole proprietorBorrowed from banks Not borrowed from banks No need for loans

© 2016 Yayoi Co., Ltd. All rights reserved.

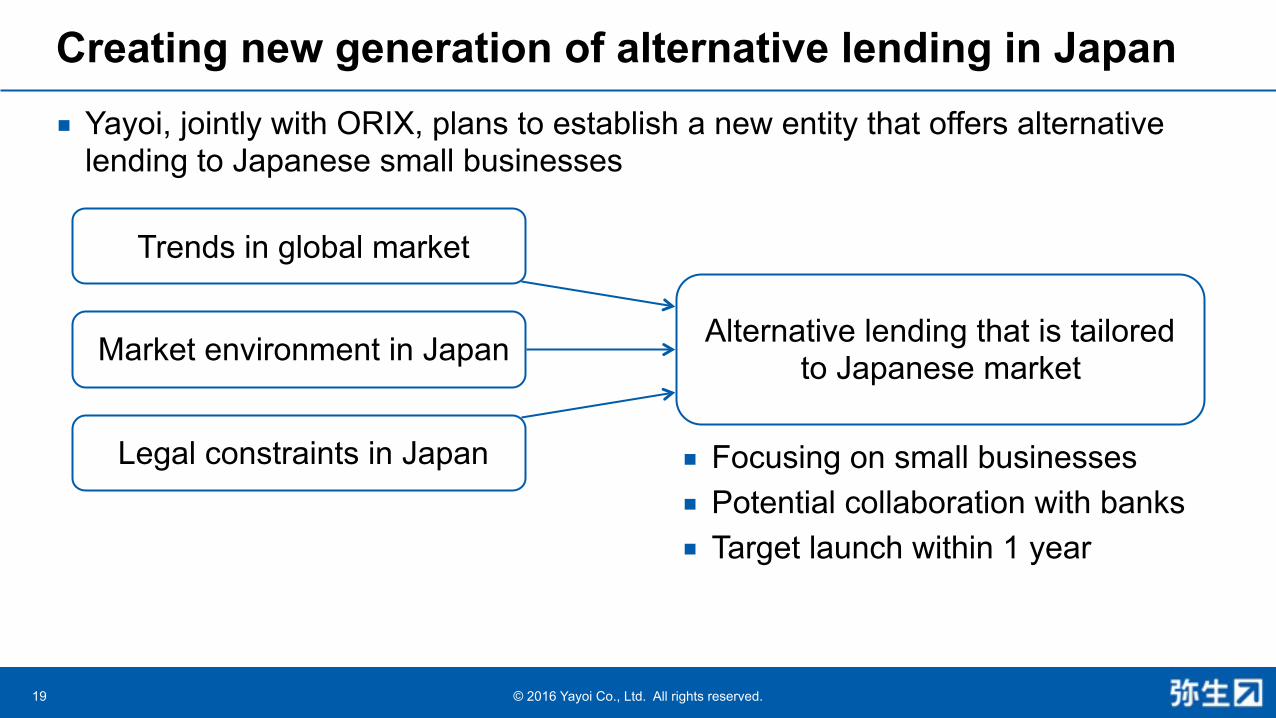

Creating new generation of alternative lending in Japan■ Yayoi, jointly with ORIX, plans to establish a new entity that offers alternative

lending to Japanese small businesses

19

Trends in global market

Alternative lending that is tailored to Japanese market Market environment in Japan

Legal constraints in Japan ■ Focusing on small businesses ■ Potential collaboration with banks ■ Target launch within 1 year

© 2016 Yayoi Co., Ltd. All rights reserved.

Thank you!

To be your “Business Concierge”

20