alternative investments and transparency— two … · steve deutsch, cfa, caia december 10, 2009...

TRANSCRIPT

Steve Deutsch, CFA, CAIADecember 10, 2009

Alternative Investments and Transparency—Two Pension Fund Challenges

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

3 Morningstar/Barron’s 2009

Alternative Investment Survey

3 Transparency

Research Technology Design

Pensionand LifeStocks

Exchange-TradedFunds

SeparateAccounts/

CITs

MutualFunds

VariableAnnuities

Closed-EndFunds

CapitalMarkets

HedgeFunds 529 Plans PEF

SoftwarePrint Internet and Services

Individuals Advisors Institutions

Core Databases

Core Skills

Media

Audiences

Geography

One central database—to all Morningstar products 3

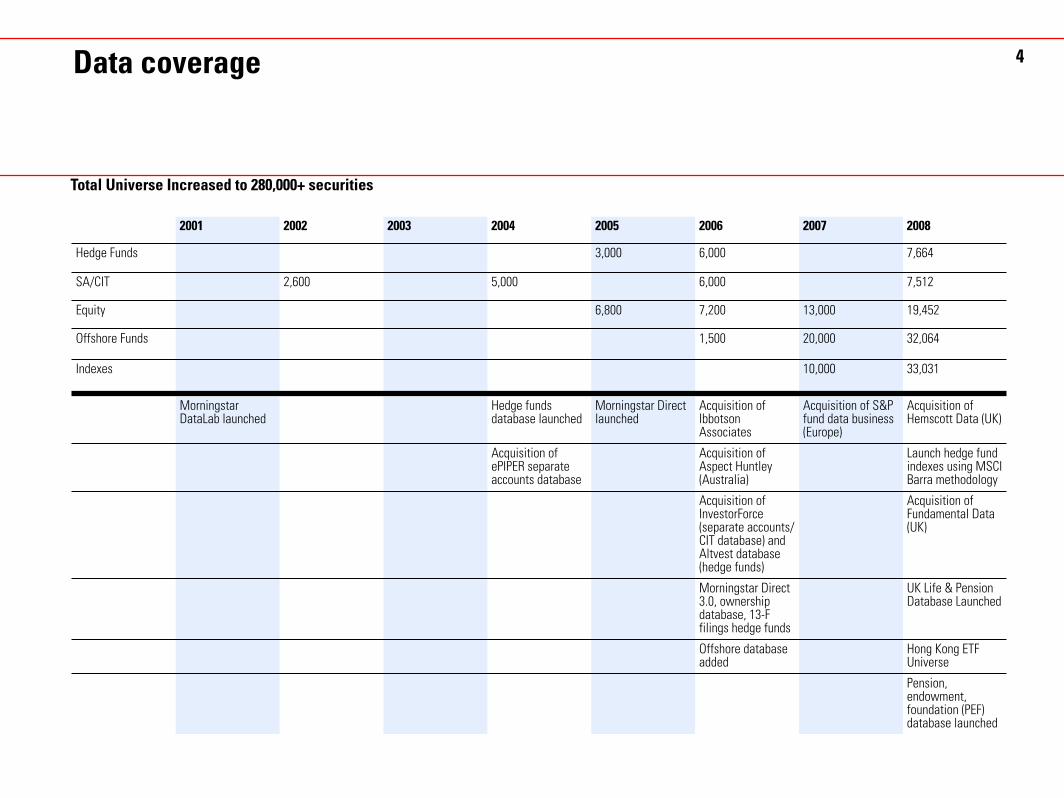

Data coverage

2001 2002 2003 2004 2005 2006 2007 2008

Hedge Funds 3,000 6,000 7,664

SA/CIT 2,600 5,000 6,000 7,512

Equity 6,800 7,200 13,000 19,452

Offshore Funds 1,500 20,000 32,064

Indexes 10,000 33,031

Morningstar DataLab launched

Hedge funds database launched

Morningstar Direct launched

Acquisition of Ibbotson Associates

Acquisition of S&P fund data business (Europe)

Acquisition of Hemscott Data (UK)

Acquisition of ePIPER separate accounts database

Acquisition of Aspect Huntley (Australia)

Launch hedge fund indexes using MSCI Barra methodology

Acquisition of InvestorForce (separate accounts/CIT database) and Altvest database (hedge funds)

Acquisition of Fundamental Data (UK)

Morningstar Direct 3.0, ownership database, 13-F filings hedge funds

UK Life & Pension Database Launched

Offshore database added

Hong Kong ETF Universe

Pension, endowment, foundation (PEF) database launched

Total Universe Increased to 280,000+ securities

4

3 Morningstar/Barron’s 2009

Alternative Investment Survey

3 Transparency

Predominant Survey Participant

6

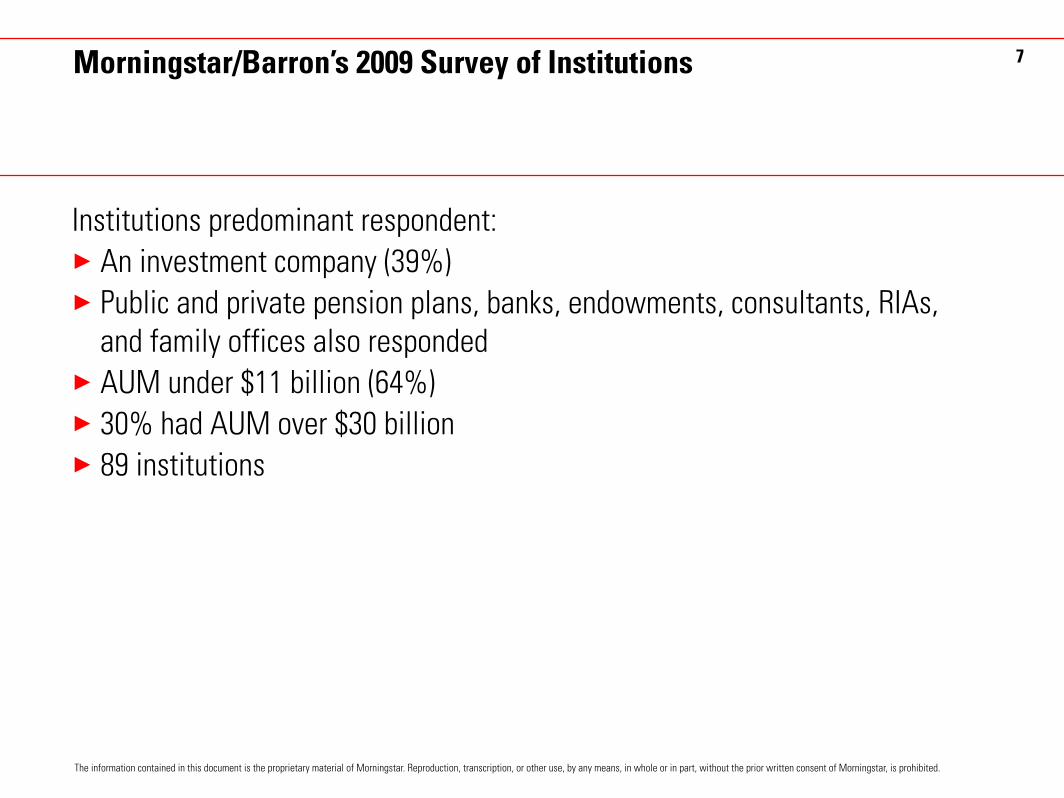

Morningstar/Barron’s 2009 Survey of Institutions

Institutions predominant respondent:

3 An investment company (39%)

3 Public and private pension plans, banks, endowments, consultants, RIAs,

and family offices also responded

3 AUM under $11 billion (64%)

3 30% had AUM over $30 billion

3 89 institutions

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

7

Defining the Alternative Universe—2009

8

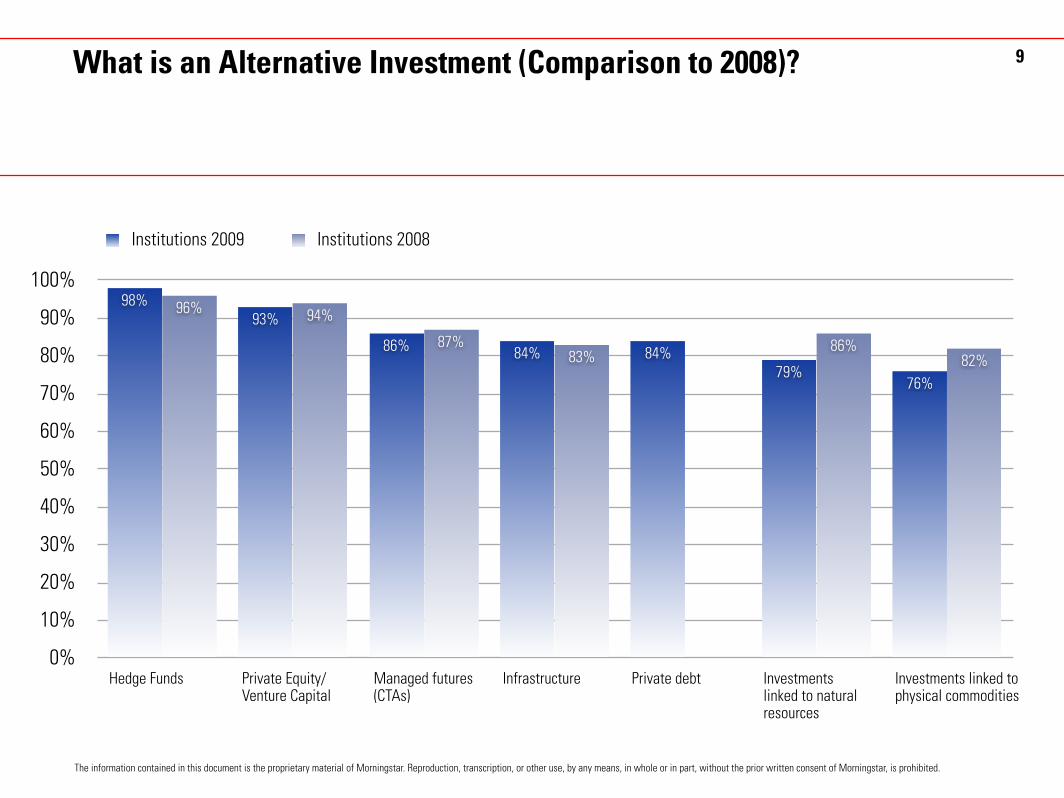

What is an Alternative Investment (Comparison to 2008)?

Hedge Funds

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

82%86%

83%87%

94%96%

76%79%

84%84%86%

93%

98%

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Institutions 2009 Institutions 2008

Private Equity/Venture Capital

Managed futures (CTAs)

Infrastructure Private debt Investments linked to natural resources

Investments linked to physical commodities

9

Retrospective and Prospective Alternative Growth

10

Estimated Average Annual Growth in Alternative AUM (2004–2009)

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

40%

2%

16%14%

20%

39%

8%

Institutions

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

0% 1–10% 11–20% 21–30% Greater than30%

Usage declined(<0%)

11

Anticipated Importance of Alternatives to Traditional Investments (Comparison to 2008)

0%

5%

10%

15%

20%

25%

30%

35%

13%

17%

33%

24%

13%12%

17%

35%

23%

13%

Institutions 2009 Institutions 2008

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Much less important Somewhat less important

As important Somewhat more important

Much more important

12

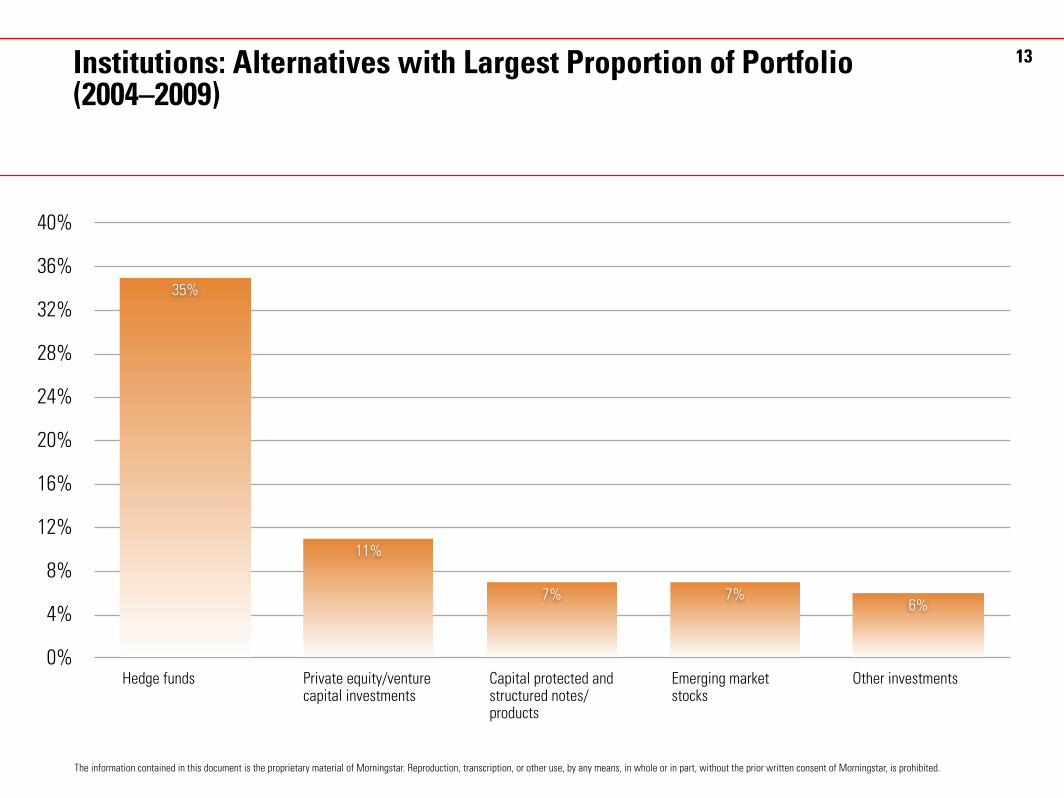

Institutions: Alternatives with Largest Proportion of Portfolio (2004–2009)

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

40%

6%7%7%

11%

35%

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Hedge funds Private equity/venture capital investments

Capital protected and structured notes/products

Emerging market stocks

Other investments

13

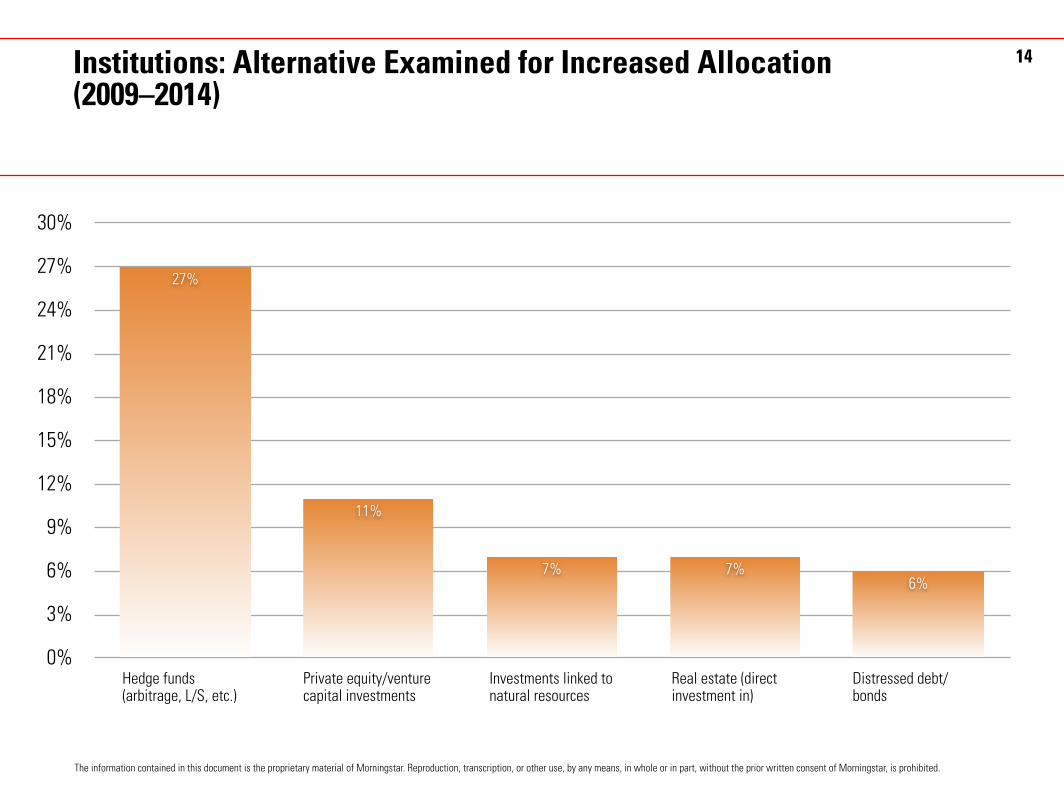

Institutions: Alternative Examined for Increased Allocation (2009–2014)

0%

3%

6%

9%

12%

15%

18%

21%

24%

27%

30%

6%7%7%

11%

27%

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Hedge funds (arbitrage, L/S, etc.)

Private equity/venture capital investments

Investments linked to natural resources

Real estate (direct investment in)

Distressed debt/bonds

14

What’s Driving or Holding Back Alternative Growth?

15

What Top Three Investment Objectives Are Driving Alternative Investment Growth?

0%

8%

16%

24%

32%

40%

48%

56%

64%

72%

80%

17%17%

37%

51%

80%

Institutions 2009

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Addressing portfolio diversification with a low correlating asset

Absolute returns Different investment techniques (like arbitrage or shorting)

Filling portfolio allocations (core-satellite model)

Poor stock market returns

16

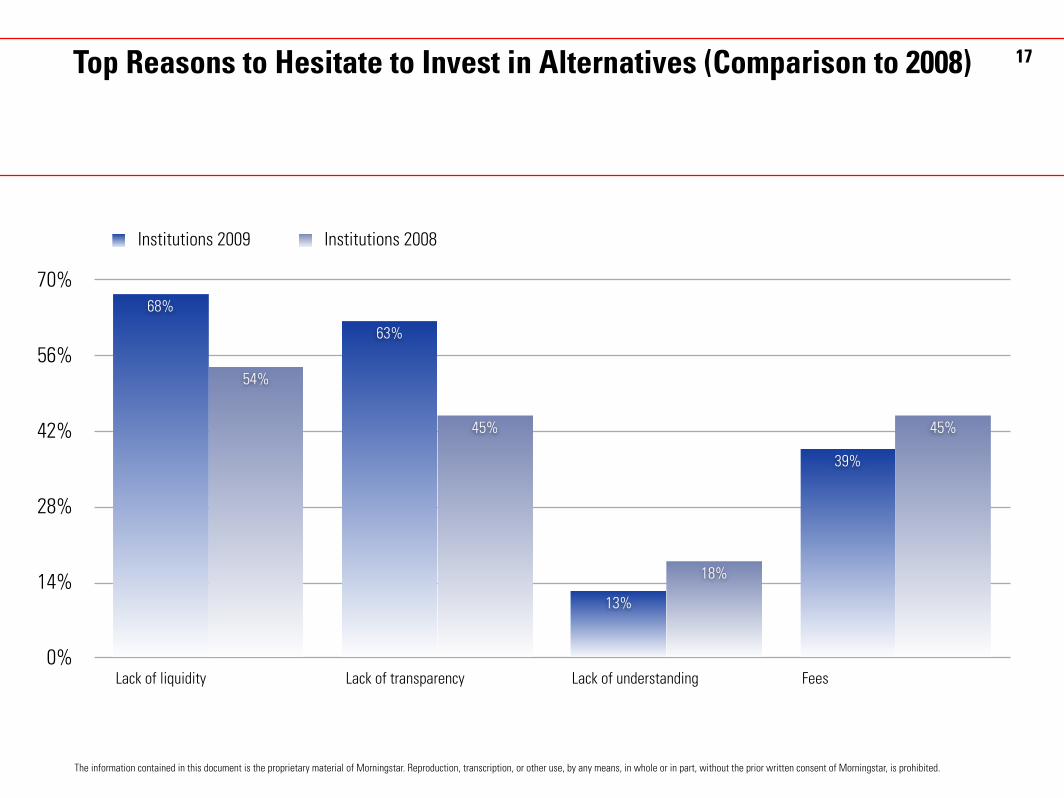

Top Reasons to Hesitate to Invest in Alternatives (Comparison to 2008)

0%

14%

28%

42%

56%

70%

45%

18%

45%

54%

39%

13%

63%

68%

Institutions 2009 Institutions 2008

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Lack of liquidity Lack of transparency Lack of understanding Fees

17

Effect of the 2008–09 Recession

18

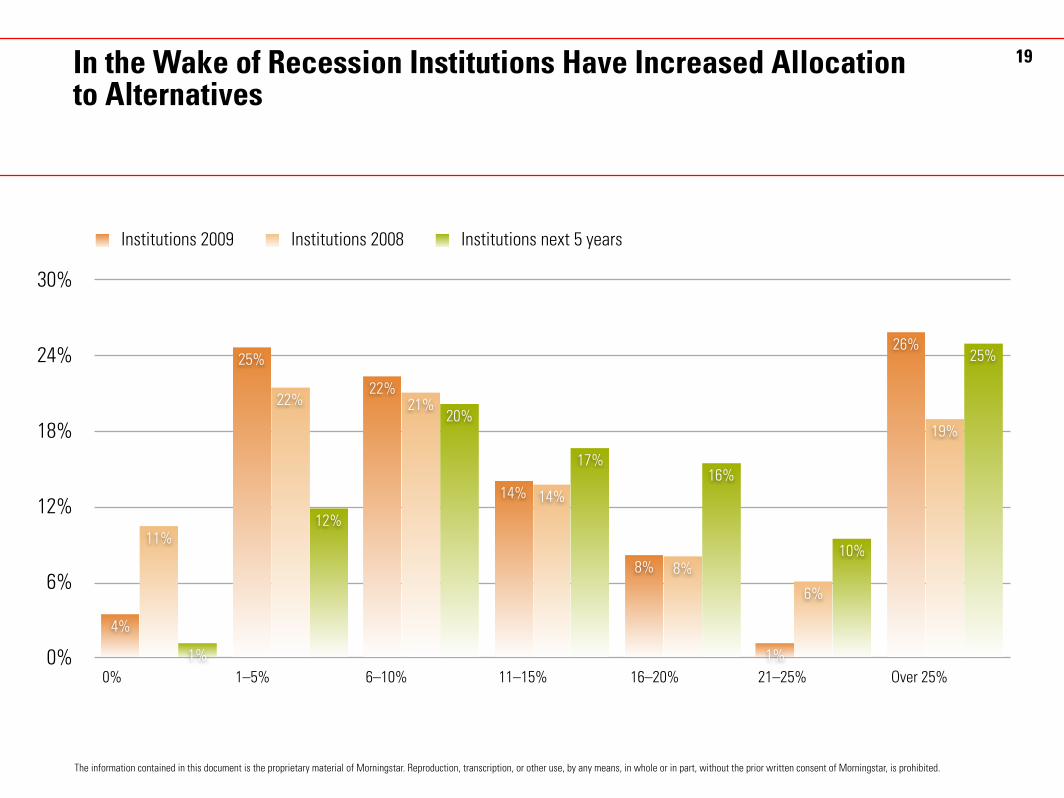

In the Wake of Recession Institutions Have Increased Allocation to Alternatives

0%

6%

12%

18%

24%

30%

25%

10%

16%17%

20%

12%

1%

19%

6%

8%

14%

21%22%

11%

26%

1%

8%

14%

22%

25%

4%

Institutions 2009 Institutions 2008 Institutions next 5 years

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

0% 1–5% 6–10% 11–15% 16–20% 21–25% Over 25%

19

In Light of the Performance of Alternative Investments Since Late 2008, Has Your Institutional Investment Committee Rethought

Investing In Alternatives? If Yes, How?

Institutional responses to this question were generally mixed, with a significant portion indicating that they have not made any changes

“It remains that the asset classes are as interesting as ever but better tackled in a different way: more focused and transparent products.”

“More diligent review process”

Reconsidering alternative investments with respect to:

3 Liquidity requirements

3 Regulatory oversight

3 Transparency

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

20

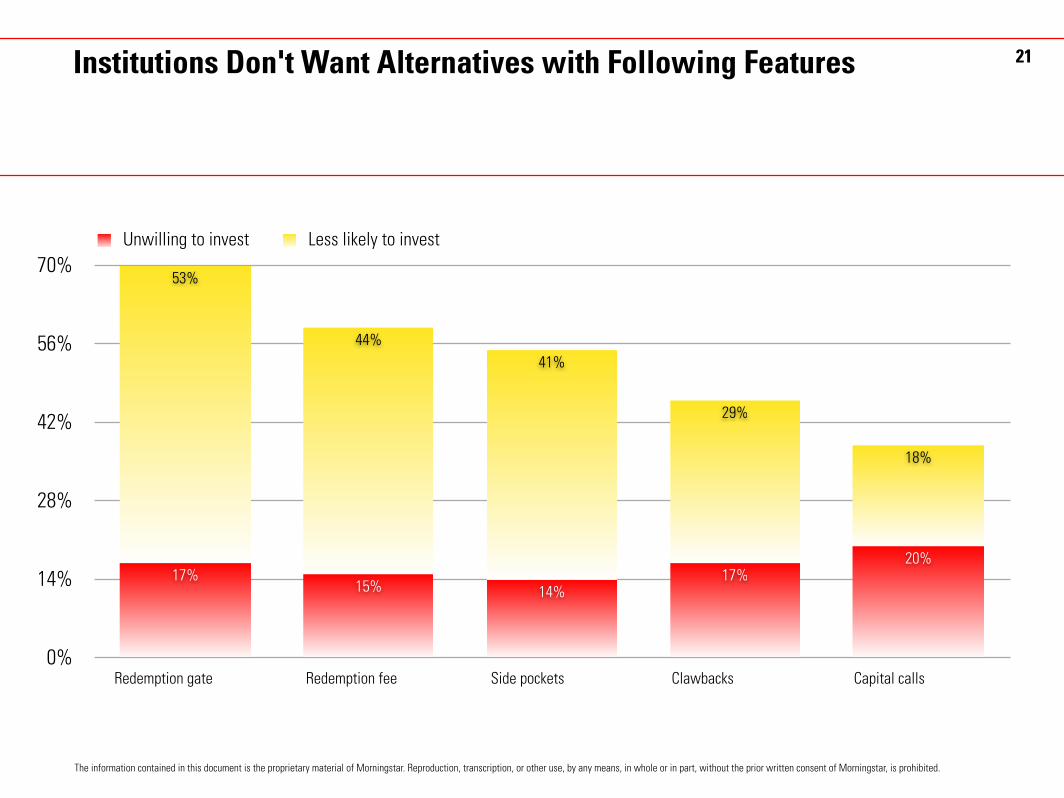

Institutions Don't Want Alternatives with Following Features

0%

14%

28%

42%

56%

70%

18%

29%

41%

44%

53%

20%17%

14%15%17%

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Redemption gate Redemption fee Side pockets Clawbacks

Unwilling to invest Less likely to invest

Capital calls

21

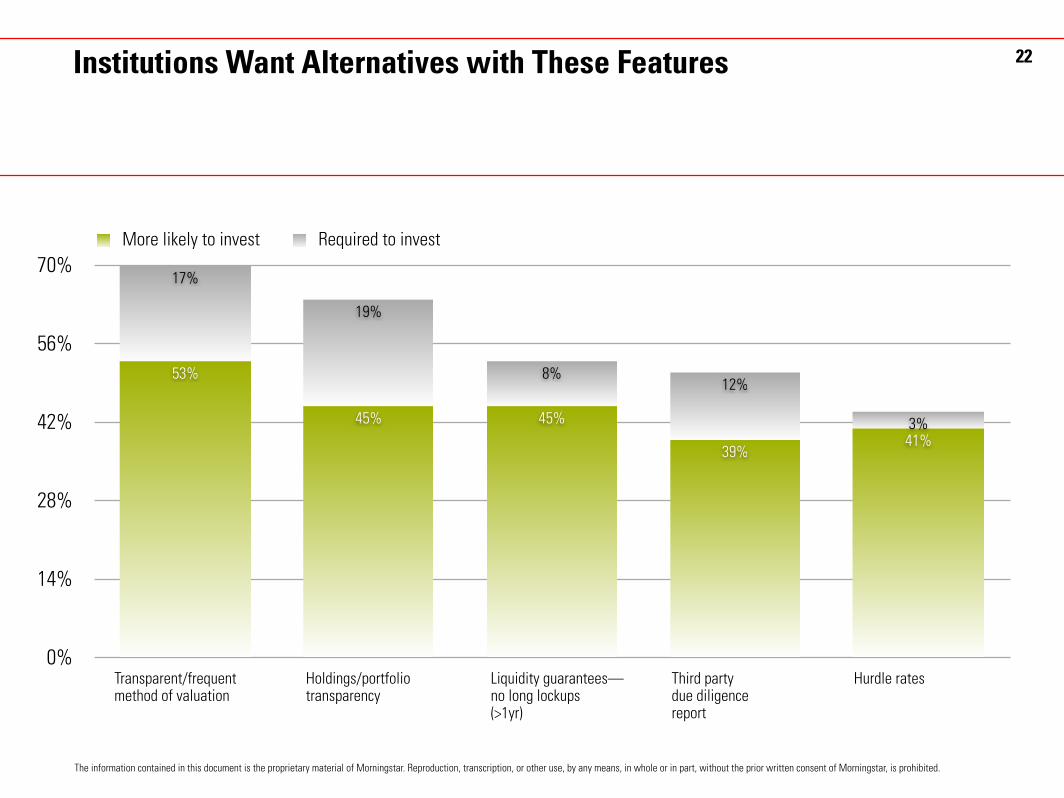

Institutions Want Alternatives with These Features

0%

14%

28%

42%

56%

70%

3%

12%8%

19%

17%

41%39%

45%45%

53%

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Transparent/frequent method of valuation

Holdings/portfoliotransparency

Liquidity guarantees—no long lockups(>1yr)

Third party due diligencereport

More likely to invest Required to invest

Hurdle rates

22

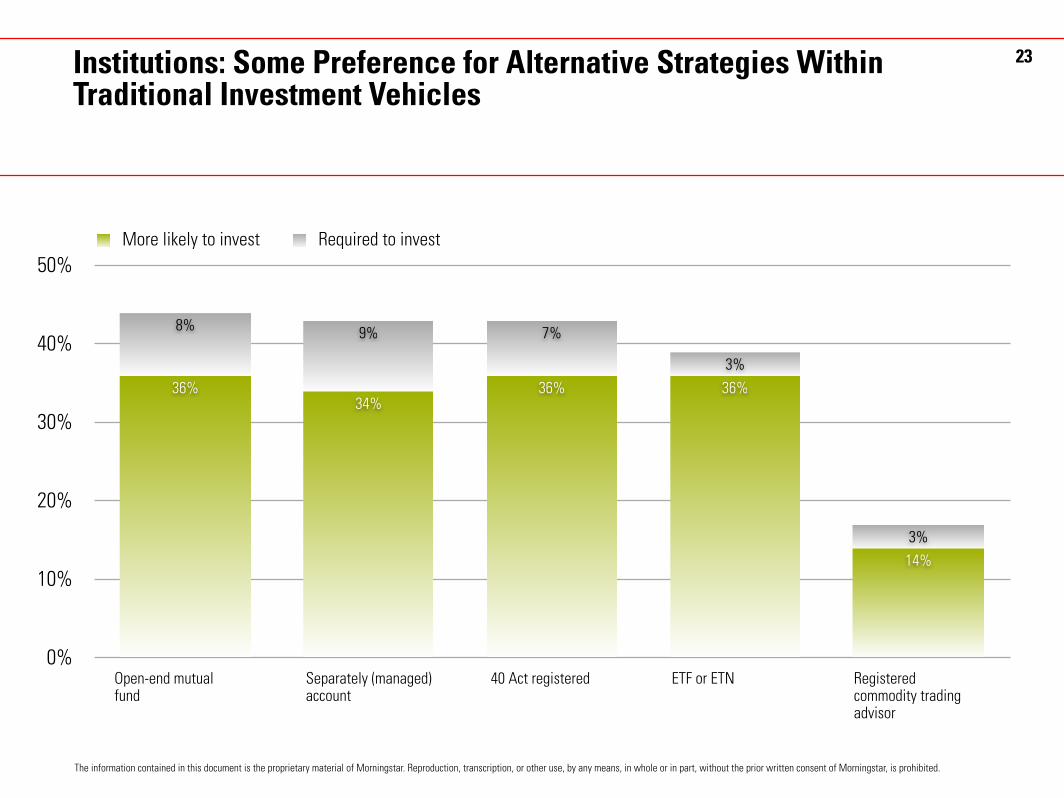

Institutions: Some Preference for Alternative Strategies Within Traditional Investment Vehicles

0%

10%

20%

30%

40%

50%

3%

3%

7%9%8%

14%

36%36%34%

36%

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Open-end mutual fund

Separately (managed) account

40 Act registered ETF or ETN

More likely to invest Required to invest

Registered commodity trading advisor

23

Overall Conclusions: Morningstar/Barron’s 2009 Alternative Investment Survey

3 Transition, adoption of alternatives still underway—shift, increased

importance relative to traditional investments

3 Recession has just increased diligence, research

3 For institutions investing in alternatives, the predominant

objective—more than ever—remains the “best of both worlds”— portfolio diversification and absolute returns, but with the positive traits

of traditional investment vehicles—liquidity, transparency

3 Alternatives becoming available in numerous investment vehicles despite

strong association to hedge funds

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

24

3 Morningstar/Barron’s 2009

Alternative Investment Survey

3 Transparency

Transparency—The Concept

3“The United States, once a bastion of trust for its transparency…is beginning

to be viewed with some skepticism around the world…”

3“…no sensible market participant I know questions any longer the need for

greater transparency…”

3“…transparency is a key to the long-term stability of global financial markets…”

David Smick in “The World is Curved: Hidden Dangers to the Global Economy.”

26

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Transparency—The Reality

3 After economic and financial correction: “transparency”—obtaining

agreement on specific and meaningful measures is the challenge.

3 In comparison to individual investors, are institutional investors

second-class citizens?

27

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

“This is The Institutional Market?”

3 Availability of information—economic disincentive for intermediaries

(consultants/advisors)

3 Lack of transparency ≠ outperformance.

3 Lack of transparency = inefficient institutional market

3 Who watches the watchmen—delegation

3 Voluntary codes of conduct—with low hurdles toward compliance

3 Too many conferences where presenters are paying

28

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Solutions. Not Just Problems.

3 It’s 2010.

3 Share the information. In public databases and don’t pay to be included

in the database.

3 Use the information and re-examine all relationships and

assumptions regularly

3 Codes with teeth and precision

3 Form your own conferences, designations for trustees and drop out

of free conferences

29

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

The Case for a PEF database

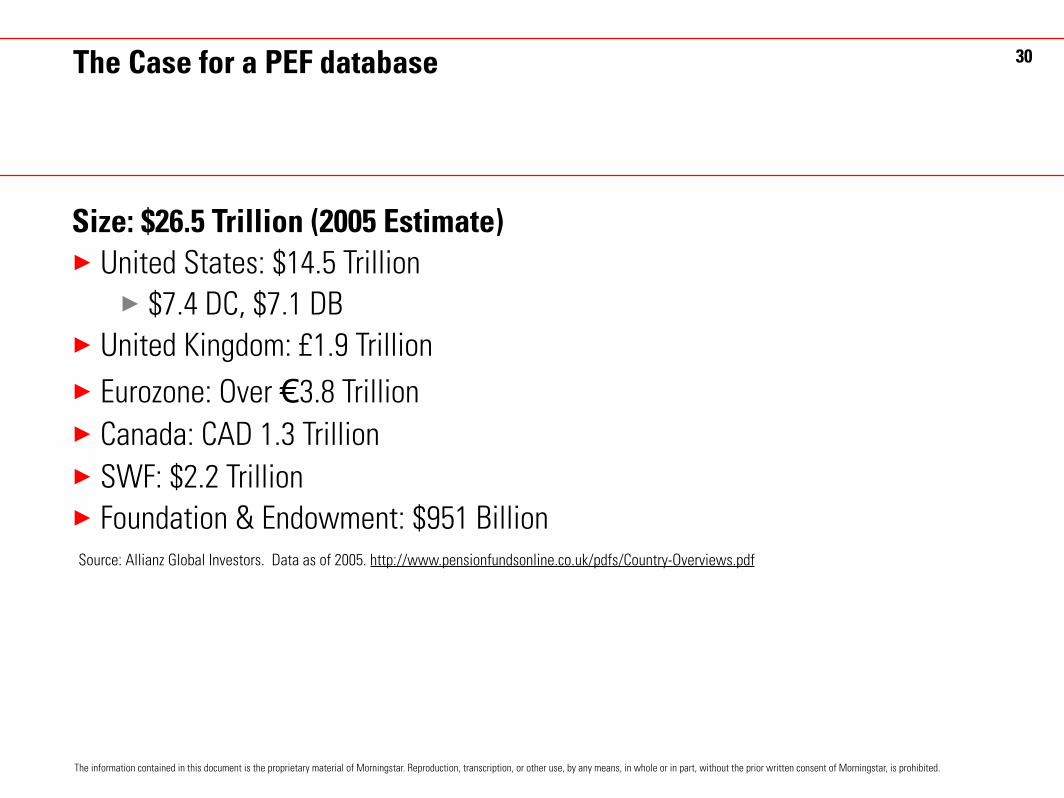

Size: $26.5 Trillion (2005 Estimate)

3 United States: $14.5 Trillion

3 $7.4 DC, $7.1 DB

3 United Kingdom: £1.9 Trillion

3 Eurozone: Over €3.8 Trillion

3 Canada: CAD 1.3 Trillion

3 SWF: $2.2 Trillion

3 Foundation & Endowment: $951 BillionSource: Allianz Global Investors. Data as of 2005. http://www.pensionfundsonline.co.uk/pdfs/Country-Overviews.pdf

30

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

The Case for a PEF database

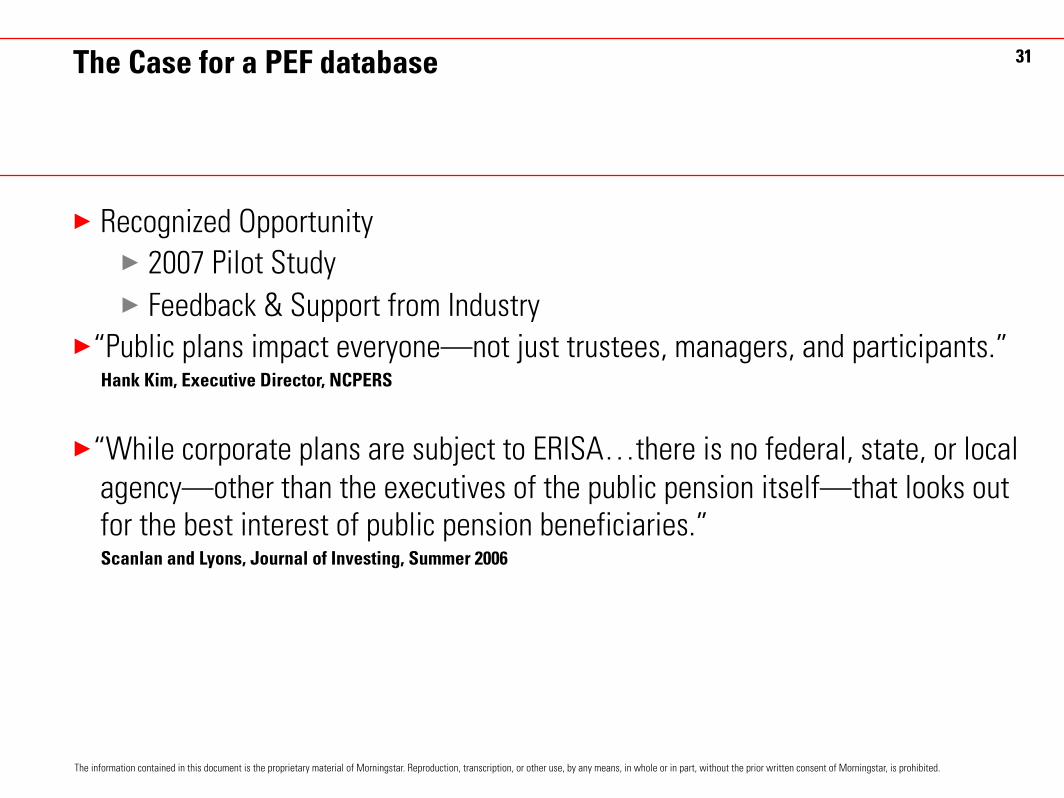

3 Recognized Opportunity

3 2007 Pilot Study

3 Feedback & Support from Industry

3“Public plans impact everyone—not just trustees, managers, and participants.” Hank Kim, Executive Director, NCPERS

3“While corporate plans are subject to ERISA…there is no federal, state, or local

agency—other than the executives of the public pension itself—that looks out for the best interest of public pension beneficiaries.” Scanlan and Lyons, Journal of Investing, Summer 2006

31

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

The relative performance record and asset allocation of public defined benefit plans—released December 2007

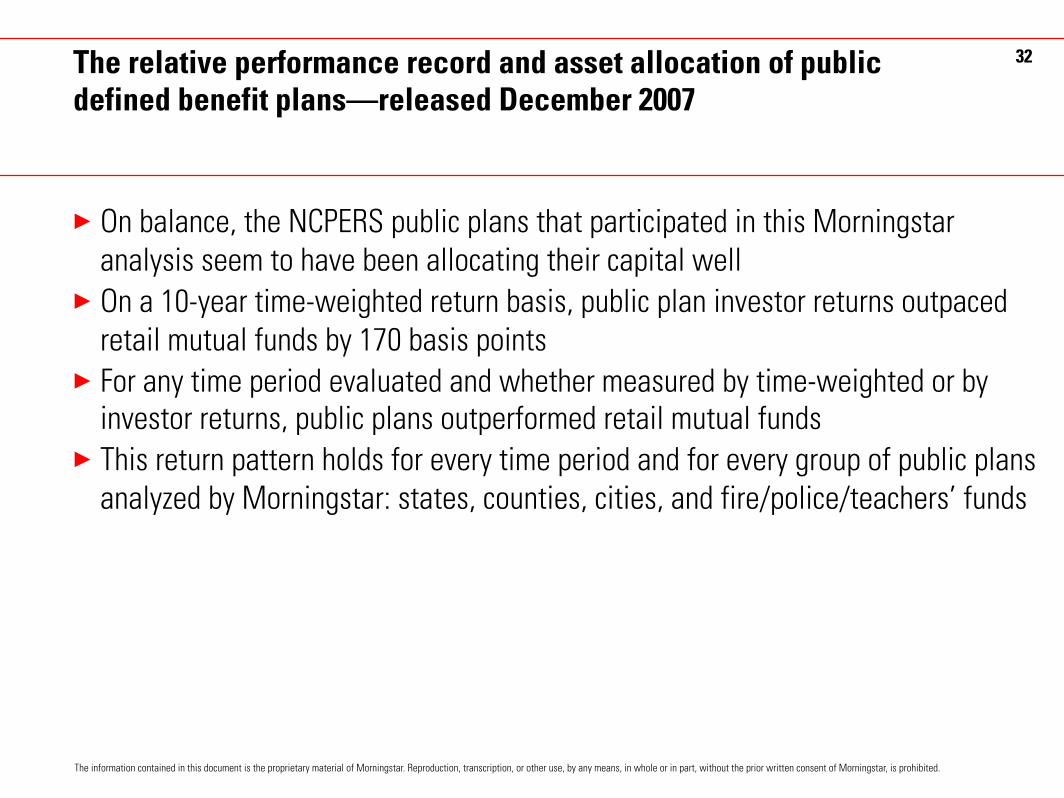

3 On balance, the NCPERS public plans that participated in this Morningstar

analysis seem to have been allocating their capital well

3 On a 10-year time-weighted return basis, public plan investor returns outpaced

retail mutual funds by 170 basis points

3 For any time period evaluated and whether measured by time-weighted or by investor returns, public plans outperformed retail mutual funds

3 This return pattern holds for every time period and for every group of public plans

analyzed by Morningstar: states, counties, cities, and fire/police/teachers’ funds

32

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

The relative performance record and asset allocation of public defined benefit plans—released December 2007

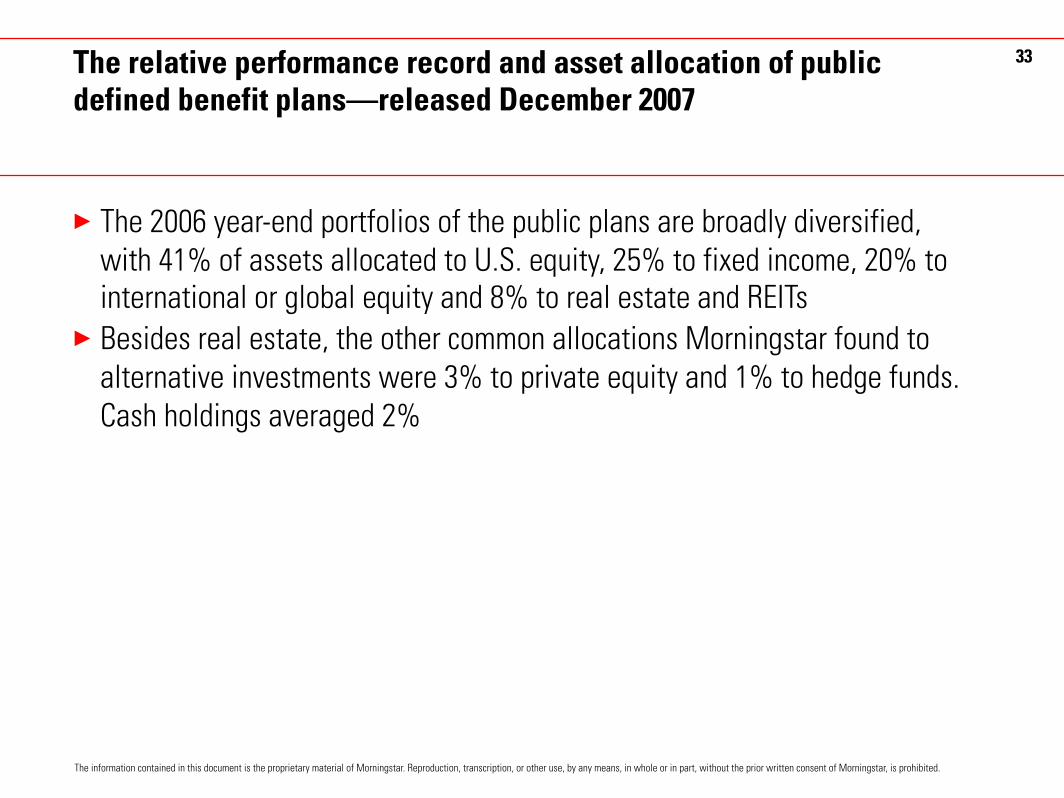

3 The 2006 year-end portfolios of the public plans are broadly diversified,

with 41% of assets allocated to U.S. equity, 25% to fixed income, 20% to international or global equity and 8% to real estate and REITs

3 Besides real estate, the other common allocations Morningstar found to

alternative investments were 3% to private equity and 1% to hedge funds.

Cash holdings averaged 2%

33

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

The Case for a PEF database

3 “Investors First”

3 Lack of Oversight

3 Fiduciary responsibility of trustees & consultants v/s dearth of

benchmarking opportunities

3 Confusing disclosures: assumptions vary wildly and impact

reporting significantly

3 Information disconnect between beneficiaries, fiduciaries,

and asset managers

3 Abundance of Information—disaggregated

3 Demographic wave—help prepare

34

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

The Case for a PEF database

3 Deliver an even more compelling database to institutional users

3 Direct & Document Interface: bring pension plan information into 2010—

electronic, comprehensive, searchable, screenable

3 Rate Consultants’ Plans

3 Profiles

3 Insight for trustees at meetings

3 Plan pages for participants

35

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Steering committee

3 Senior staff from both Morningstar and Ibbotson Associates

3 Dr. P. Brett Hammond, managing director and chief investment strategist for

TIAA-CREF Asset Management

3 T. Britton Harris, CIO, Teacher Retirement System of Texas

3 Hank Kim, executive director and counsel for the National Conference on Public

Employee Retirement Systems

3 Dr. Olivia S. Mitchell, professor at the Wharton School of the University of

Pennsylvania and executive director of The Pension Research Council

3 Anna M. Rappaport, past president of The Society of Actuaries and founder of

Anna Rappaport Consulting

36

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

Key takeaways of pension, endowment, foundation database

3 Greater transparency and easy information access into these bedrock

vehicles for preparing for retirement, funding education institutes, or charities is long overdue

3 Donors are more involved and want to monitor their “investments” and future

retirees need to understand how they and their plan choices are doing on a truly

relative and regular basis

3 Morningstar wants to contribute to better plans, more efficiencies on a

national scope

37

The information contained in this document is the proprietary material of Morningstar. Reproduction, transcription, or other use, by any means, in whole or in part, without the prior written consent of Morningstar, is prohibited.

For information on the Pension/Endowment/Foundation databaseSteve Deutsch