aixtron investor presentation · aixtron investor presentation ir presentation – h1/2015 ......

TRANSCRIPT

AIXTRON Investor Presentation IR Presentation – H1/2015 (FSE: AIXA, ISIN DE000A0WMPJ6, NASDAQ: AIXG, ISIN: US0096061041)

© AIXTRON Investor Relations, September 2015

Forward-Looking Statements

This document may contain forward-looking statements regarding the business, results of operations, financial condition and earnings outlook of AIXTRON within the meaning of the safe harbor provisions of the US Private Securities Litigation Reform Act of 1995. These statements may be identified by words such as “may”, “will”, “expect”, “anticipate”, “contemplate”, “intend”, “plan”, “believe”, “continue” and “estimate” and variations of such words or similar expressions. These forward-looking statements are based on our current views and assumptions and are subject to risks and uncertainties. You should not place undue reliance on these forward-looking statements. Actual results and trends may differ materially from those reflected in our forward-looking statements. This could result from a variety of factors, such as actual customer orders received by AIXTRON, the level of demand for deposition technology in the market, the timing of final acceptance of products by customers, the condition of financial markets and access to financing for AIXTRON, general conditions in the market for deposition plants and macroeconomic conditions, cancellations, rescheduling or delays in product shipments, production capacity constraints, extended sales and qualification cycles, difficulties in the production process, the general development in the semi-conductor industry, increased competition, fluctuations in exchange rates, availability of public funding, fluctuations and/or changes in interest rates, delays in developing and marketing new products, a deterioration of the general economic situation and any other factors discussed in any reports or other announcements field by AIXTRON with the U.S. Securities and Exchange Commission. Any forward-looking statements contained in this document are based on current expectations and projections of the Executive Board and on information currently available to it and are made as at the date hereof. AIXTRON undertakes no obligation to revise or update any forward-looking statements as a result of new information, future events or otherwise, unless expressly required to do so by law.

AIXTRON INVESTOR PRESENTATION

2

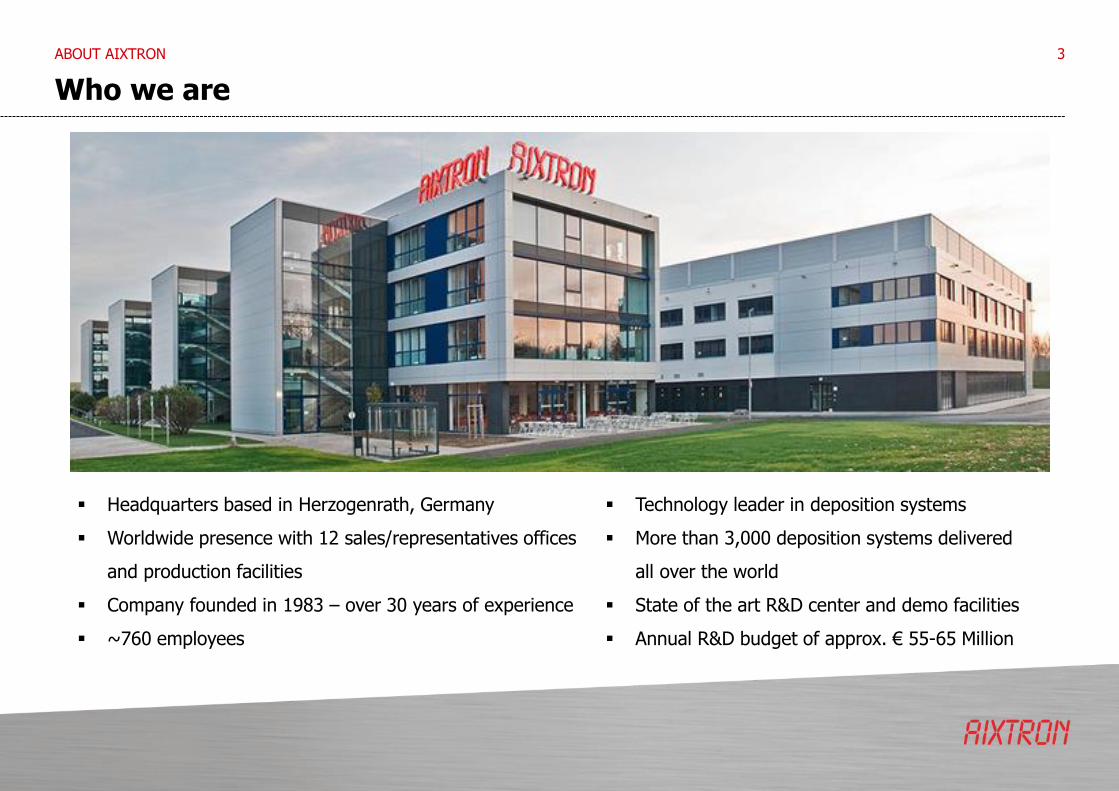

Who we are

Headquarters based in Herzogenrath, Germany

Worldwide presence with 12 sales/representatives offices

and production facilities

Company founded in 1983 – over 30 years of experience

~760 employees

Technology leader in deposition systems

More than 3,000 deposition systems delivered

all over the world

State of the art R&D center and demo facilities

Annual R&D budget of approx. € 55-65 Million

3 ABOUT AIXTRON

Our Technology. Your FUTURE.

AIXTRON TECHNOLOGIES 4

Compound Semiconductors

Silicon Semiconductors

Organic

Carbon

LED Lighting Memory & Logic

OLED Power Management

Equipment Order Intake per Quarter

OPERATIONS 5

Source: Deutsche Bank Equity Research, AIXTRON SE

0

50

100

150

200

250

1Q98

2Q98

3Q98

4Q98

1Q99

2Q99

3Q99

4Q99

1Q00

2Q00

3Q00

4Q00

1Q01

2Q01

3Q01

4Q01

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

2Q11

3Q11

4Q11

1Q12

2Q12

3Q12

4Q12

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

Compound Semiconductor Market China Investments

driven by notebook

backlighting

driven by LED TV

driven by strategic China investments

(EUR million)

driven by mobile phone

penetration

driven by telecom/datacom and mobile phone

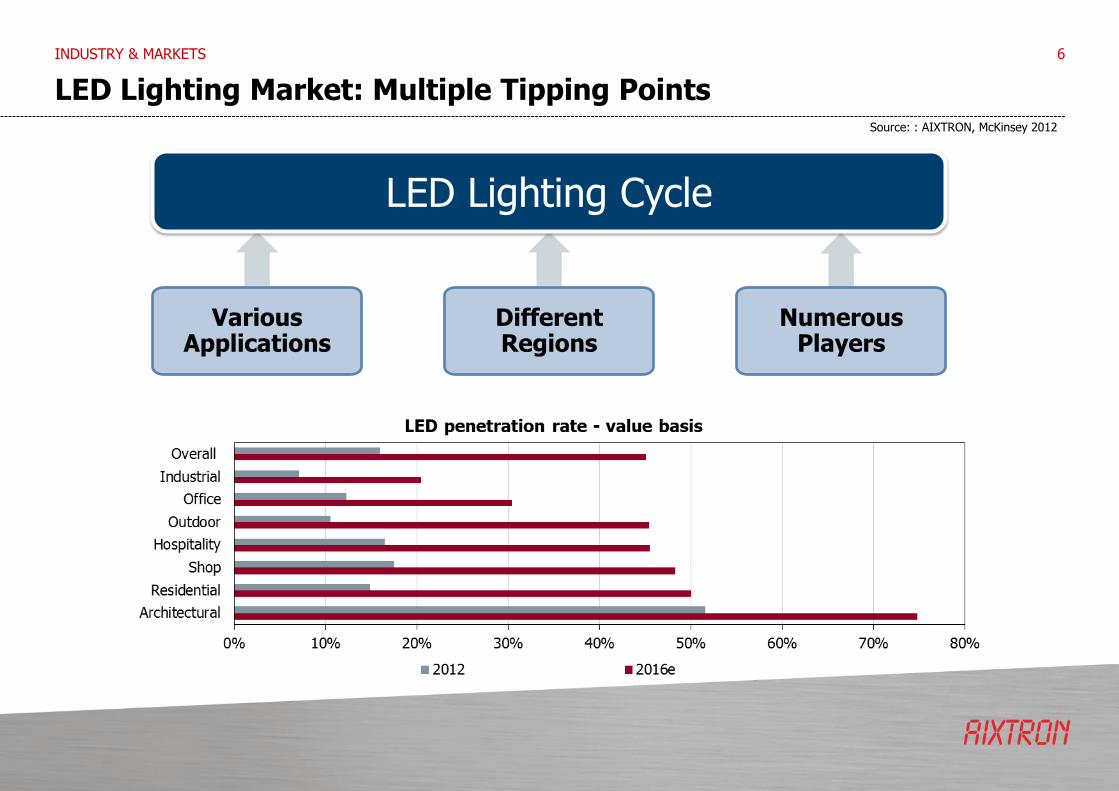

LED Lighting Market: Multiple Tipping Points

INDUSTRY & MARKETS 6

Various Applications

Different Regions

Numerous Players

LED Lighting Cycle

Source: : AIXTRON, McKinsey 2012

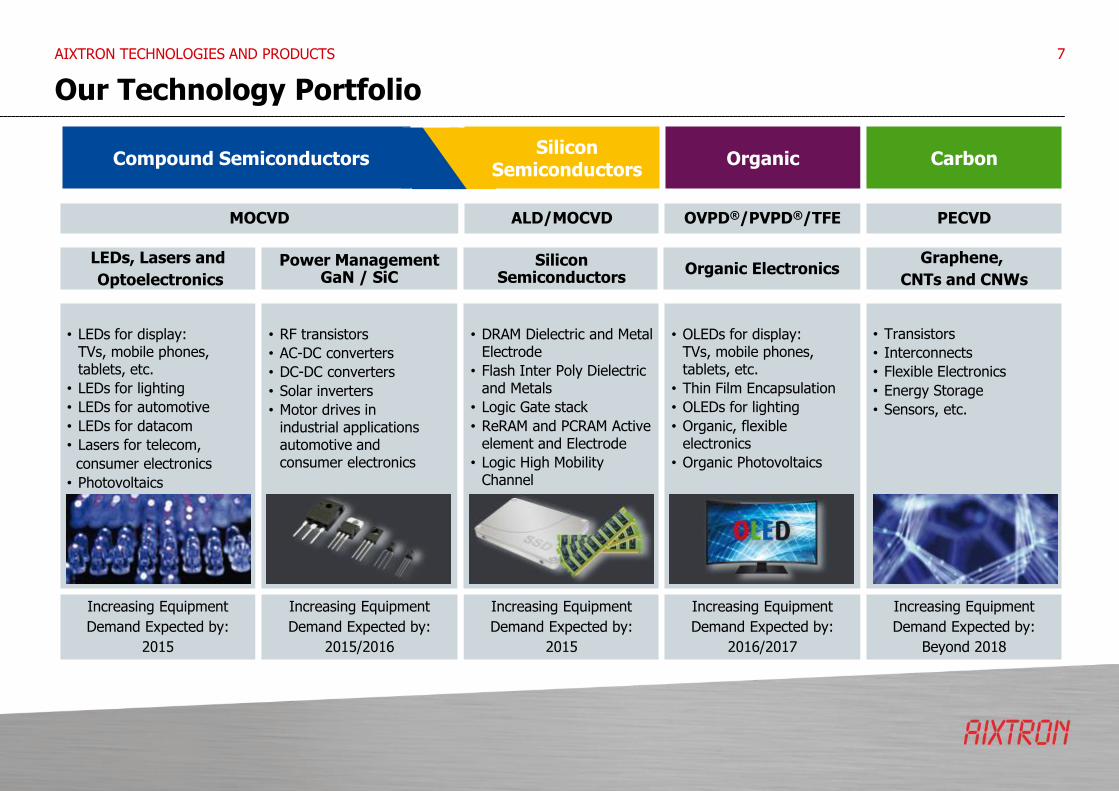

Compound Semiconductors

MOCVD ALD/MOCVD

LEDs, Lasers and

Optoelectronics

• LEDs for display: TVs, mobile phones, tablets, etc.

• LEDs for lighting

• LEDs for automotive

• LEDs for datacom

• Lasers for telecom,

consumer electronics

• Photovoltaics

Increasing Equipment

Demand Expected by:

2015

Our Technology Portfolio

7

Silicon Semiconductors

• RF transistors

• AC-DC converters

• DC-DC converters

• Solar inverters

• Motor drives in industrial applications automotive and consumer electronics

Power Management GaN / SiC

• DRAM Dielectric and Metal Electrode

• Flash Inter Poly Dielectric and Metals

• Logic Gate stack

• ReRAM and PCRAM Active element and Electrode

• Logic High Mobility Channel

Silicon Semiconductors

Increasing Equipment

Demand Expected by:

2015

Increasing Equipment

Demand Expected by:

2015/2016

• OLEDs for display: TVs, mobile phones, tablets, etc.

• Thin Film Encapsulation

• OLEDs for lighting

• Organic, flexible electronics

• Organic Photovoltaics

• Transistors

• Interconnects

• Flexible Electronics

• Energy Storage

• Sensors, etc.

Organic Electronics Graphene,

CNTs and CNWs

Organic Carbon

OVPD®/PVPD®/TFE PECVD

Increasing Equipment

Demand Expected by:

2016/2017

Increasing Equipment

Demand Expected by:

Beyond 2018

AIXTRON TECHNOLOGIES AND PRODUCTS

H1/2015 Financial Highlights

Sales: Volume below expectations due to delays in AIX R6 shipments

Gross Margin: Lower than expected due to impact from AIX R6 qualification process

OPEX on track: EUR 39.1m (target run-rate around EUR 80m on an annual basis)

Solid Cash Position: EUR 255.4m as of June 30, 2015 (EUR 268.1m as of Dec 31, 2014)

Order Backlog: EUR 91.2m as of June 30, 2015 (EUR 69.0m as of Jan 1st, 2015)

FINANCIALS 8

Market Prospects

Short-Term • Further increasing adoption of LEDs for exterior, public infrastructure & commercial lighting

• Increased adoption of LEDs for consumer & residential lighting

• Market positioning of the new AIX R6 MOCVD tool for LED manufacturing

• Increasing adoption of GaN for power electronics

• Increased emergence of silicon carbide (SiC) hybrid automotive & photovoltaic applications

• Next generation NAND, DRAM & PRAM memory applications

Mid- to Long-Term • Development of organic semiconductors applications using efficient deposition and thin-film

encapsulation technologies

• Development of GaN-on-Si based power electronics or LEDs

• Further development of plastic electronics/flexible TFT backplanes

• Increased development for specialized compound solar cells

• Higher demand for High-k as well as interconnect components

• Progress in the convergence of compound material applications, e. g. substituting materials in the silicon semiconductor industry

• Development of applications using carbon nanostructures including graphene

FUTURE MARKETS 9

AIXTRON INVESTOR PRESENTATION 10

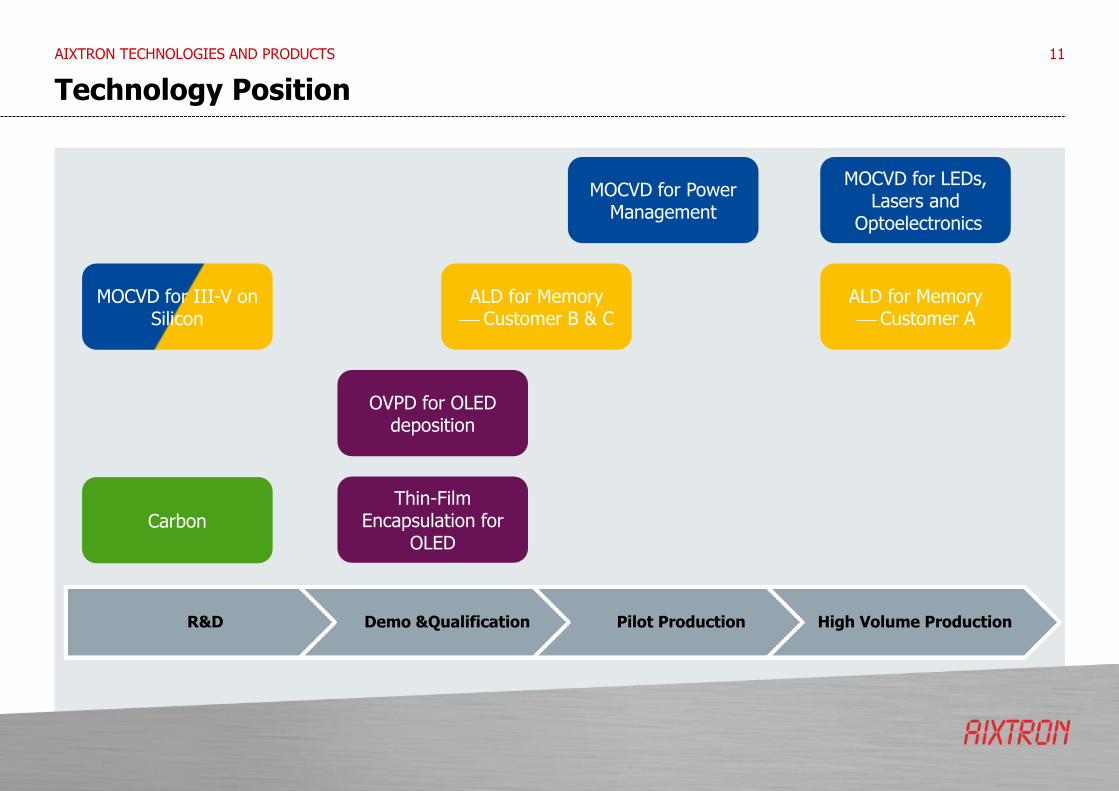

Technology Position

AIXTRON TECHNOLOGIES AND PRODUCTS 11

R&D Demo &Qualification Pilot Production High Volume Production

MOCVD for III-V on Silicon

Carbon

Thin-Film Encapsulation for

OLED

OVPD for OLED deposition

ALD for Memory Customer B & C

ALD for Memory Customer A

MOCVD for LEDs, Lasers and

Optoelectronics

MOCVD for Power Management

0

10,000

20,000

30,000

40,000

50,000

60,000

2014e

2015e

2016e

2017e

2018e

HB L

ED

Mark

et (2

" Equiv

ale

nt W

afe

r in

000)

Mobile & Others Display Lighting

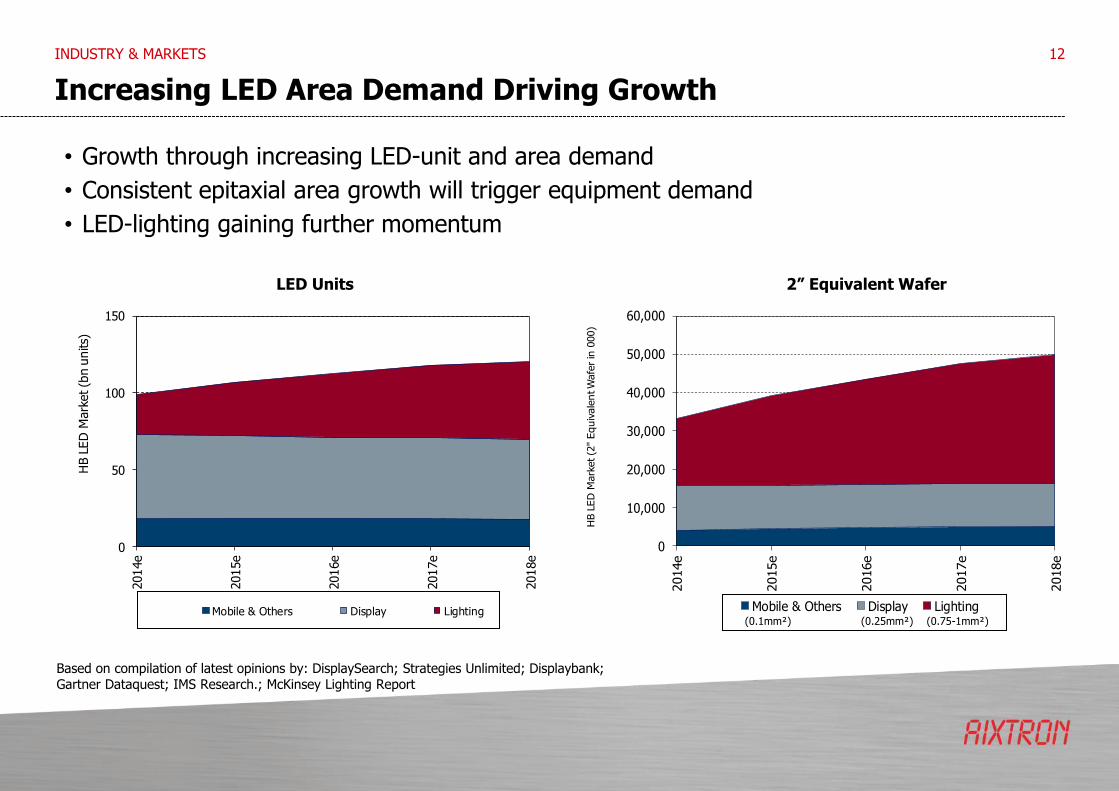

Increasing LED Area Demand Driving Growth

INDUSTRY & MARKETS 12

0

50

100

150

2014e

2015e

2016e

2017e

2018e

HB L

ED

Mark

et (b

n u

nits)

Mobile & Others Display Lighting

• Growth through increasing LED-unit and area demand

• Consistent epitaxial area growth will trigger equipment demand

• LED-lighting gaining further momentum

Based on compilation of latest opinions by: DisplaySearch; Strategies Unlimited; Displaybank; Gartner Dataquest; IMS Research.; McKinsey Lighting Report

(0.1mm²) (0.25mm²) (0.75-1mm²)

LED Units 2” Equivalent Wafer

Production Supply 3rd Party Estimates for HB LEDs

INDUSTRY & MARKETS 13

• Analysts’ Bull-Bear MOCVD system demand estimates

• Larger area and future replacement to drive equipment demand

• SSL is the strongest driver for material area growth

• Incremental LED units and area growth every year

Based on compilation of latest opinions by: Strategies Unlimited; DisplaySearch; Gartner Dataquest; IMS Res; McKinsey Lighting Report; Baader Bank; Bankhaus Lampe; Berenberg; Canaccord Genuity; CLSA; Commerzbank; Deutsche Bank, DZ Bank; Exane BNP; Goldman Sachs; JG Capital; JP Morgan; Liberum; Morgan Stanley; Needham; Susquehanna; UBS

Incremental LED Units Incremental Material Area

0

5

10

2014e 2015e 2016e 2017e 2018e

Incre

menta

l H

B L

ED

s (b

n u

nits)

Incremental HB LEDs - Units

0

200

400

600

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2014e 2015e 2016e 2017e 2018e

Required n

um

ber

of

MO

CVD r

eact

ors

Incr

em

enta

l HB L

EDs

(2"

Equiv

ale

nt

Wafe

r in

000)

Incremental HB LEDs - Area (LHS)

MOCVD Systems - Bear (RHS)

MOCVD Systems - Bull (RHS)

Compound Semiconductors – Power Electronics

AIXTRON TECHNOLOGIES AND PRODUCTS 14

Consumer Electronics & IT Automotive Energy Industrial

Power Management

GaN

• Electronic appliances

• Computing

• Wireless charging

• Power supplies

• PFC

• Infotainment

• GPS

• Connected car

• Autonomous driving

• EMI/EMC

• Adaptive cruise control

GaN / SiC

• General Automotive

Electronics

• HEV/EV

• Charging stations

• Inverter / motor drives

• Converter

• Radar test applications

• Power Grid / Smart Meter / Appliances

• Solar / Wind inverters

• Solar / Wind Power

DC distribution

• Power Storage

• UPS

• UPS

• Industrial machines

• Building

• Mining, oil, gas power

generation

• Shipping/Rail

SiC

Power Switching

30V 600V 1.2 kV ≥2kV

Volume segment Niche segment

Compound Semiconductors – MOCVD System Generations

• Extendibility: Extensive choice of configurations and enhancements

• Scalability: Multiple technologies on one platform

• Productivity: Highest throughput, best yield, fastest growth rates

Two Reactor Technologies Planetary Reactor® & Close Coupled Showerhead® (CCS)

AIXTRON TECHNOLOGIES AND PRODUCTS

15

Year of Introduction Technology Chambers

2002 • G3 Planetary

• 19x2” CCS

• 24x2”, 8x4”

• 19x2”

2006 • G4 HT Planetary

• CRIUS® CCS

• 42x2”, 11x4”, 6x6”

• 31x2”, 12x3”, 7x4”, 3x6”, 1x12”

2010/ 2011 • G5 HT Planetary

• CRIUS® II-eXL CCS

• 56x2”, 14x4”, 8x6’’, 5x8’’

• 75x2”, 19x4”

2012 • G5+ HT Planetary • 5x8” GaN-on-Si Technology

2014 • G5 WW

• AIX R6

• 12x4”, 8x6”

• 121x2”, 31x4”, 12x6”

Compound Semiconductors – MOCVD

• Addressing multiple industries

• Established industry standard & market leading

• Configurable, extendable common platform

• Introduced the latest MOCVD technology - AIX R6

Two Reactor Technologies Planetary Reactor® & Close Coupled Showerhead® (CCS)

AIXTRON TECHNOLOGIES AND PRODUCTS 16

Planetary Reactor®

AIX G5+, 5x8 Close Coupled Showerhead®

AIX R6, 31x4”

• Unique Planetary reactor design

• Horizontal reactor type

• Patented CCS Technology

• Vertical reactor design

Organic Electronics – OVPD® + Encapsulation

AIXTRON TECHNOLOGIES AND PRODUCTS 17

Source: DisplaySearch, AIXTRON

Front-end Array process equipment

Front-end Cell process equipment

Coating

Etching

Stripping

Test and repair

ITO deposition

Cleaning

Organic material deposition

Encapsulation

Cathode deposition

Cleaning Glass cutting

Bonding

Aging

Final test

Back-end Module process equipment

Targeted technology

OLED manufacturing process

Organic Electronics – Front-end Process Equipment

AIXTRON TECHNOLOGIES AND PRODUCTS

18

Cleaning Deposition Cathode

deposition Encapsulation Module

preparation Automation

5%

40%

10% 20%

5%

20%

Cumulative Capex

45%

55%

75%

80%

100%

Focus Activities

Key competency: Thin-film deposition

Value creation: 60%

Source: IHS; AIXTRON internal estimates

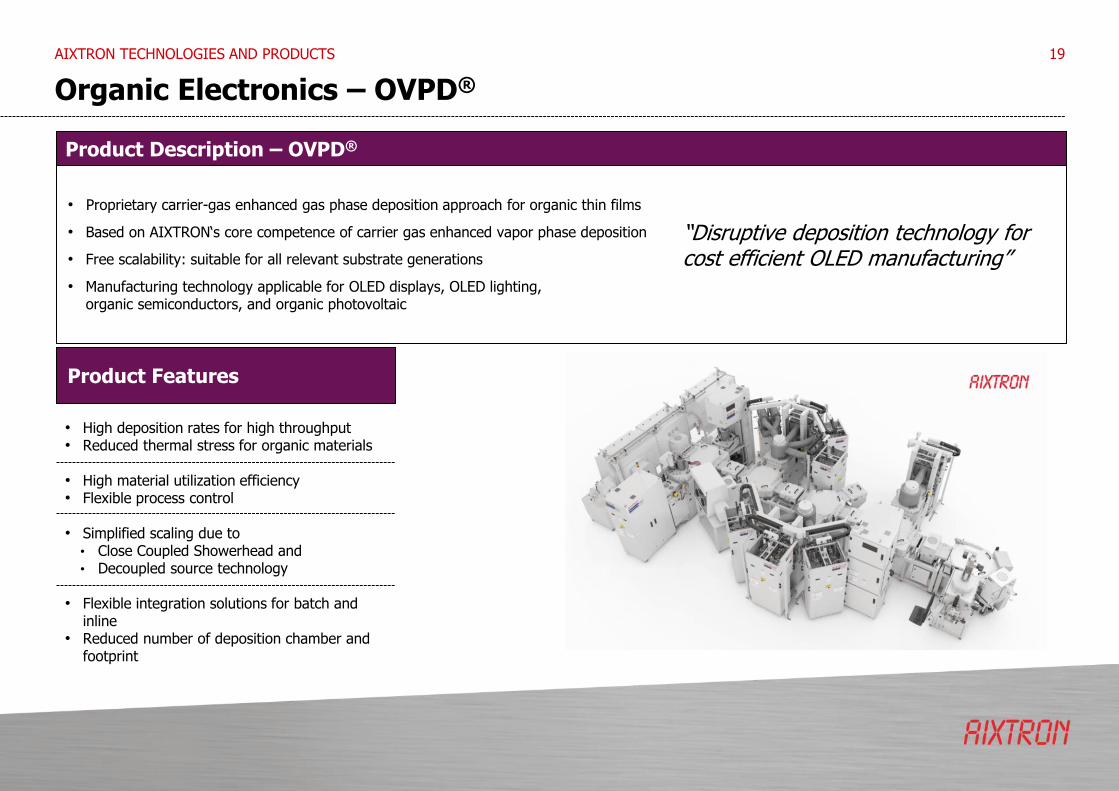

Organic Electronics – OVPD®

19

• Proprietary carrier-gas enhanced gas phase deposition approach for organic thin films

• Based on AIXTRON‘s core competence of carrier gas enhanced vapor phase deposition

• Free scalability: suitable for all relevant substrate generations

• Manufacturing technology applicable for OLED displays, OLED lighting, organic semiconductors, and organic photovoltaic

• High deposition rates for high throughput • Reduced thermal stress for organic materials

• High material utilization efficiency • Flexible process control

• Simplified scaling due to

• Close Coupled Showerhead and • Decoupled source technology

• Flexible integration solutions for batch and inline

• Reduced number of deposition chamber and footprint

Product Description – OVPD®

Product Features

“Disruptive deposition technology for cost efficient OLED manufacturing”

AIXTRON TECHNOLOGIES AND PRODUCTS

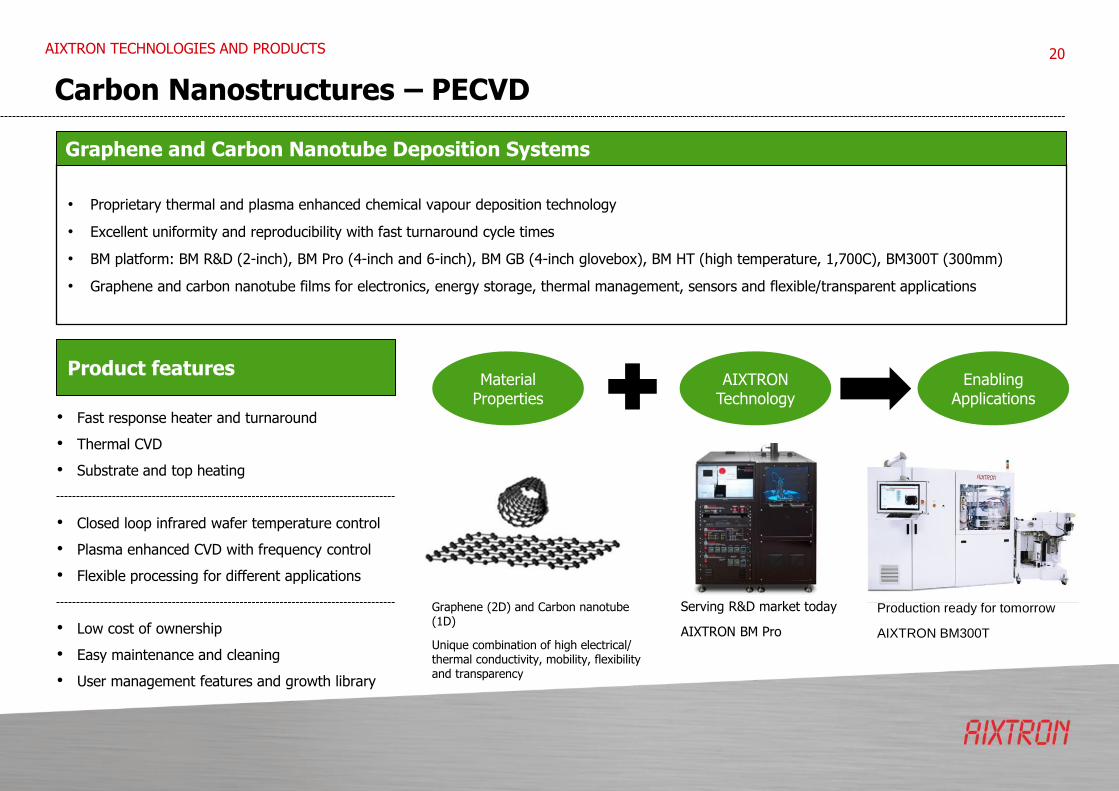

Carbon Nanostructures – PECVD

20

Product features

• Proprietary thermal and plasma enhanced chemical vapour deposition technology

• Excellent uniformity and reproducibility with fast turnaround cycle times

• BM platform: BM R&D (2-inch), BM Pro (4-inch and 6-inch), BM GB (4-inch glovebox), BM HT (high temperature, 1,700C), BM300T (300mm)

• Graphene and carbon nanotube films for electronics, energy storage, thermal management, sensors and flexible/transparent applications

Graphene and Carbon Nanotube Deposition Systems

• Fast response heater and turnaround

• Thermal CVD

• Substrate and top heating

• Closed loop infrared wafer temperature control

• Plasma enhanced CVD with frequency control

• Flexible processing for different applications

• Low cost of ownership

• Easy maintenance and cleaning

• User management features and growth library

Graphene (2D) and Carbon nanotube (1D)

Unique combination of high electrical/ thermal conductivity, mobility, flexibility and transparency

Serving R&D market today

AIXTRON BM Pro

Production ready for tomorrow

AIXTRON BM300T

Material Properties

AIXTRON Technology

Enabling Applications

AIXTRON TECHNOLOGIES AND PRODUCTS

Silicon Semiconductors – ALD

21

Product Description – ALD

• Up to 3 patented TriJet vaporizers

• Small volume confined process space ensure short ALD cycle time

• > 40 % less precursor consumption • Efficient purge

• Isolated multi wafer processing with

> 40% higher throughput

• Close Coupled Showerhead for uniform distribution

• Flexibility and ease of maintenance

• 300mm ALD Technology

• QXP-8300 Mini-batch system

• High throughput : 2 Process Chambers – 8 stations

• Up to 3 vaporizers and one bubbler

• Applications : DRAM, Logic and Flash High k Dielectric Metal electrode : ReRAM and PCRAM Active elements

• Proven in HVM with >40% lower CoO and >90% Uptime in DRAM and Flash Fabs

“Best-in class technology, state of the art deposition system, lowest CoO”

AIXTRON TECHNOLOGIES AND PRODUCTS

Product Features

Silicon Semiconductors – ALD and MOCVD

22

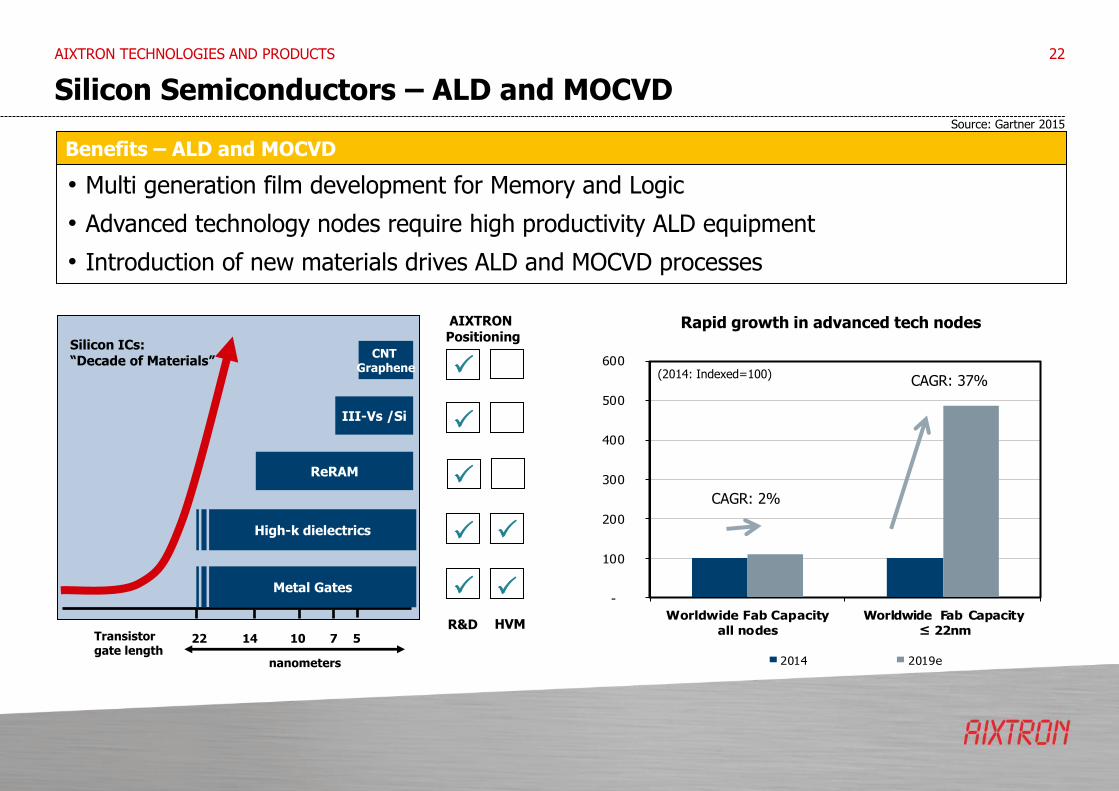

Benefits – ALD and MOCVD

• Multi generation film development for Memory and Logic

• Advanced technology nodes require high productivity ALD equipment

• Introduction of new materials drives ALD and MOCVD processes

AIXTRON TECHNOLOGIES AND PRODUCTS

-

100

200

300

400

500

600

Worldwide Fab Capacity

all nodes

Worldwide Fab Capacity

≤ 22nm

2014 2019e

ReRAM

III-Vs /Si

nanometers

22 Transistor gate length

10

CNT Graphene

14 7

Silicon ICs: “Decade of Materials”

R&D HVM

AIXTRON Positioning

Source: Gartner 2015

(2014: Indexed=100) CAGR: 37%

CAGR: 2%

Rapid growth in advanced tech nodes

5

Metal Gates

High-k dielectrics

Revenue Analysis

OPERATIONS 23

H1/2015: by region

H1/2015: by equipment & spares

72%

28%

Spares

Equipment

H1/2015: by end application

(equipment only)

24%

32%

19%

14%

11%

79%

11%

10%

Americas

Europe

Asia

Power Electronics

Silicon

LED

Optoelectronics

Others

Consolidated Income Statement*

24

(€ million) H1/15 H1/14

Restated +/- Q2/15 Q1/15 +/-

Revenues 80.7 90.1 -10% 40.4 40.3 0%

Cost of sales 68.3 67.61 1% 36.8 31.5 17%

Gross profit 12.4 22.61 -45% 3.6 8.8 -59%

Gross Margin 15% 25%1 -10 pp 9% 22% -13 pp

Selling expenses 6.3 6.41 -2% 3.0 3.3 -9%

General & admin expenses 8.5 9.6 -11% 4.2 4.3 -2%

R&D 27.6 29.2 -6% 14.6 12.9 13%

Net other op.(income)/expenses -3.3 -1.3 -154% -0.3 -3.0 -90%

EBITDA -21.8 -13.4 -63% -15.3 -6.4 -139%

EBIT -26.7 -21.5 -24% -17.9 -8.8 -103%

EBIT Margin -33% -24% -9 pp -44% -22% -22 pp

Result before tax -26.2 -20.8 -26% -17.7 -8.5 -108%

Pre-Tax Margin -33% -23% -10 pp -44% -21% -23 pp

Net result -27.6 -23.4 -18% -18.1 -9.5 -91%

Net Return on Sales -34% -26% -8 pp -45% -23% -22 pp

FINANCIALS

*) rounded figures; may not add up 1) Restated; please refer to “Accounting Policies” in H1-Report

Consolidated Statement of Financial Position*

25

(€ million) 30/6/15 31/12/14 30/6/14

Property, plant & equipment 80.6 77.3 78.3

Goodwill 77.1 64.8 64.5

Other intangible assets 5.7 2.5 2.7

Others 4.8 4.6 5.8

Non-current assets 168.2 149.2 151.3

Inventories, WIP & Finished Goods 85.8 81.7 72.7

Trade receivables 23.5 26.3 30.3

Others 9.4 8.3 9.3

Cash & Cash Equivalents incl. CD 255.4 268.1 275.6

Current Assets 374.1 384.4 387.8

Shareholders' equity 398.6 415.7 443.6

Non-current liabilities 3.8 1.3 2.0

Trade payables 12.6 16.4 14.4

Advance payments from customers 95.1 66.9 51.1

Others 32.2 33.2 28.1

Current liabilities 139.9 116.5 93.7

Balance Sheet total 542.3 533.5 539.2

Financials

*) rounded figures; may not add up

Consolidated Statement of Cash Flows*

26

(€ million) H1/15 H1/14 Q2/15 Q1/15

Cash Flow from operating activities -6.4 -25.1 3.7 -10.1

Cash Flow from investing activities 8.9 -19.9 -2.4 11.3

Cash Flow from financing activities -0.2 -0.2 -0.2 0.0

Exchange rate changes 5.2 0.6 -1.0 6.2

Net change in Cash & Cash Equivalents 7.5 -44.6 0.1 7.4

Cash & Cash Equivalents (beginning of period) 116.6 167.5 124.0 116.6

Cash & Cash Equivalents (end of period) 124.1 122.8 124.1 124.0

Change in Cash deposits -22.5 13.8 -7.6 -14.8

Free Cash Flow1 -12.3 -31.3 -0.1 -12.1

Capex -7.4 -6.2 -3.8 -3.5

FINANCIALS

*) rounded figures; may not add up 1) Operating CF + Investing CF + Changes in Cash Deposits, adjusted for acquisition effects (upfront payments and loan)

AIXTRON SE Dornkaulstr. 2 52134 Herzogenrath Germany Phone +49 (2407) 9030-0 Fax +49 (2407) 9030-40 E-Mail [email protected]

Thank you very much for your attention.