ahmed elshahat1 the language of accounting. ahmed elshahat2 1. the language of accounting accounting...

TRANSCRIPT

Ahmed Elshahat 1

THE LANGUAGE OF ACCOUNTING

Ahmed Elshahat 2

1. THE LANGUAGE OF ACCOUNTING

ACCOUNTING DEFINED WHO USES ACCOUNTING?TYPES OF ACCOUNTING

INFORMATION ACCOUNTING PRINCIPLES,

ASSUMPTIONS / CONCEPTS FORMS OF BUSINESS ORGANIZATION FINANCIAL STATEMENTS TYPES OF ACCOUNTS

Ahmed Elshahat 3

TYPES OF ACCOUNTING INFORMATION

Financial: Used by management and external

users... Ex. financial statements

Internal Auditing: Evaluating system of internal

control... reports are accurate and reliable

(Income) Tax Accounting: Must pay Uncle

Sammy

Management (cost) Accounting: Internal

use... (CMA)

Ahmed Elshahat 4

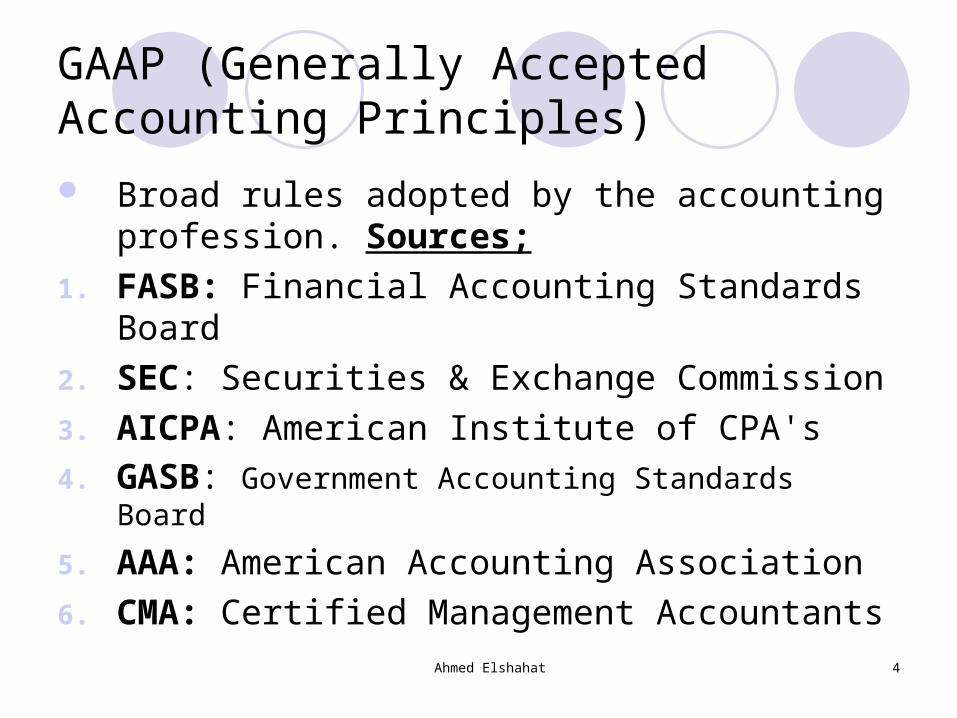

GAAP (Generally Accepted Accounting Principles)

Broad rules adopted by the accounting profession. Sources;

1. FASB: Financial Accounting Standards Board

2. SEC: Securities & Exchange Commission

3. AICPA: American Institute of CPA's

4. GASB: Government Accounting Standards Board

5. AAA: American Accounting Association

6. CMA: Certified Management Accountants

Ahmed Elshahat 5

ACCOUNTING PRINCIPLES, ASSUMPTIONS / CONCEPTS

Cost principle Ongoing concern concept Business entity concept Objectivity principle Stable-dollar concept Realization principle Monetary unit assumption

Ahmed Elshahat 6

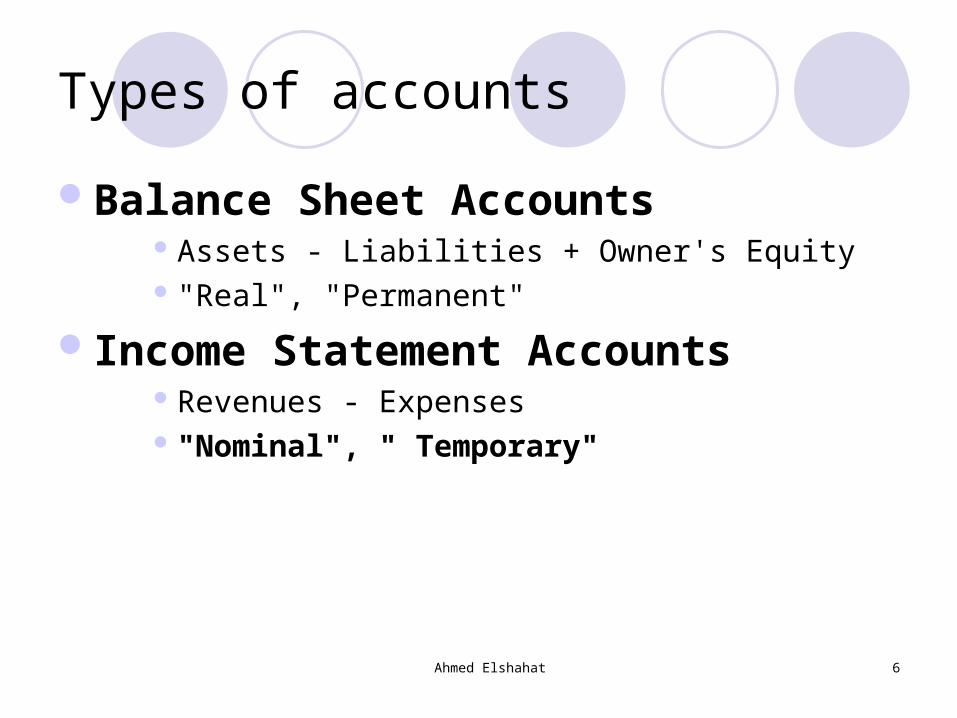

Types of accounts

Balance Sheet Accounts Assets - Liabilities + Owner's Equity "Real", "Permanent"

Income Statement Accounts Revenues - Expenses "Nominal", " Temporary"

Ahmed Elshahat 7

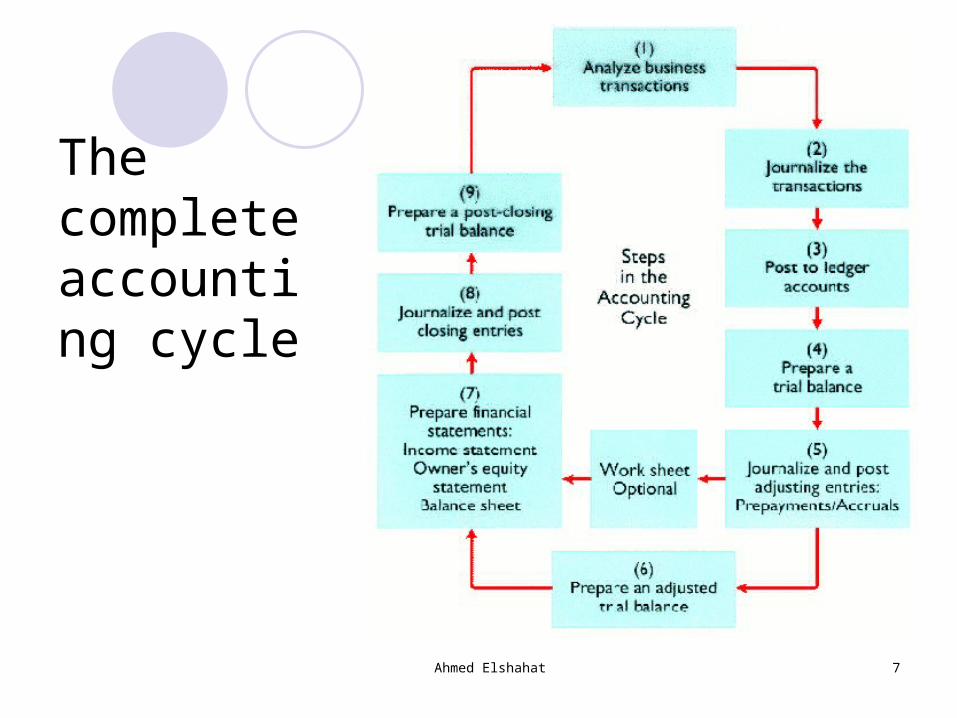

The complete accounting cycle

Ahmed Elshahat 8

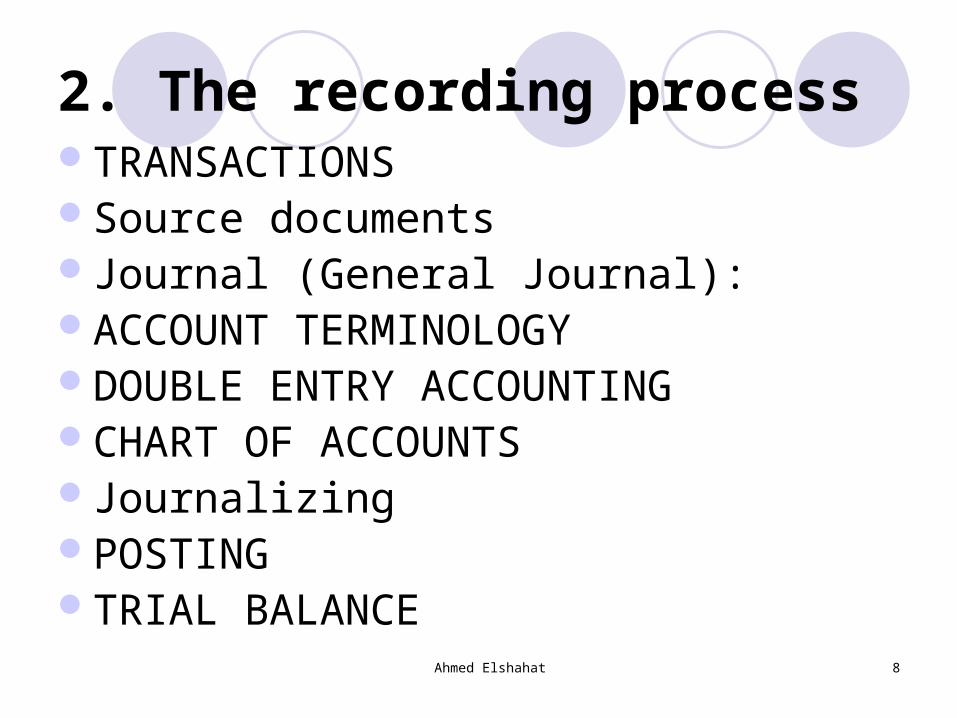

2. The recording processTRANSACTIONS Source documents Journal (General Journal):ACCOUNT TERMINOLOGY DOUBLE ENTRY ACCOUNTING CHART OF ACCOUNTS JournalizingPOSTING TRIAL BALANCE

Ahmed Elshahat 9

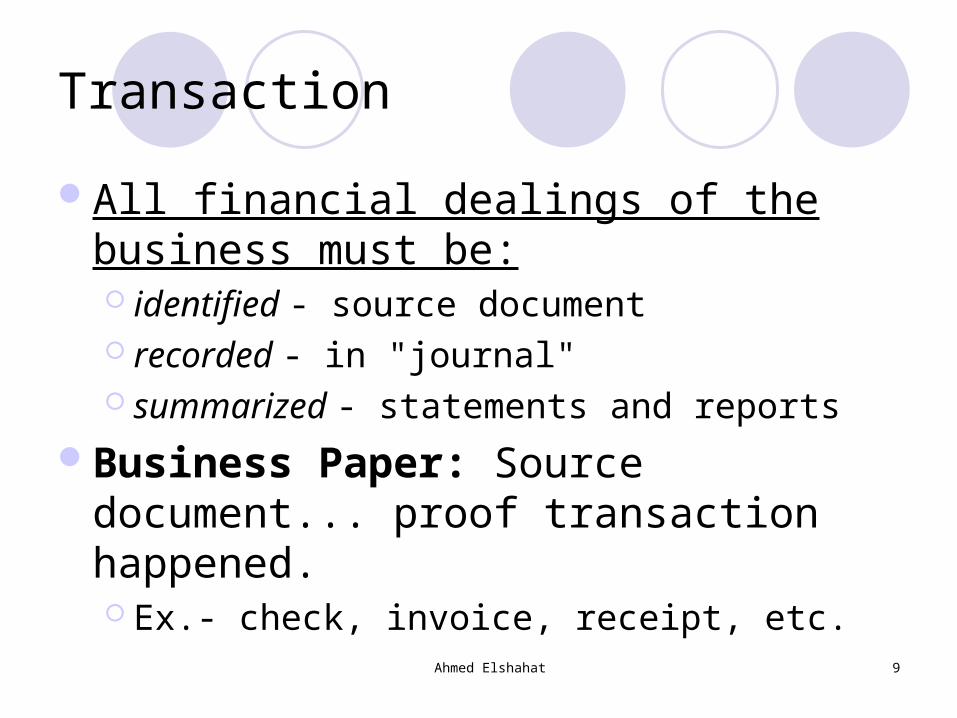

Transaction

All financial dealings of the business must be: identified - source document recorded - in "journal" summarized - statements and reports

Business Paper: Source document... proof transaction happened. Ex.- check, invoice, receipt, etc.

Ahmed Elshahat 10

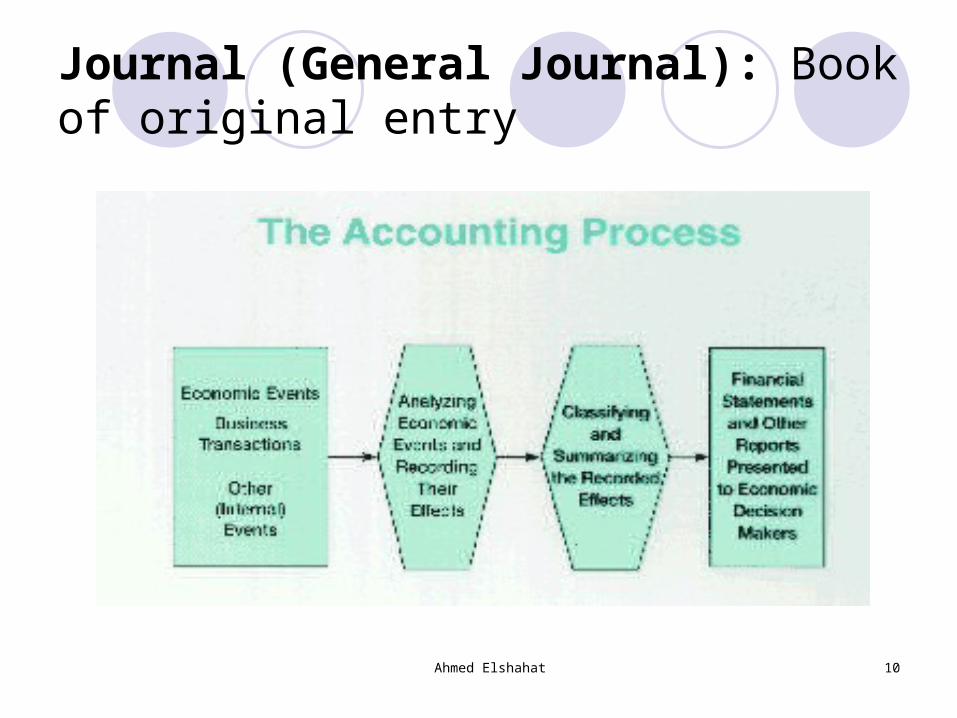

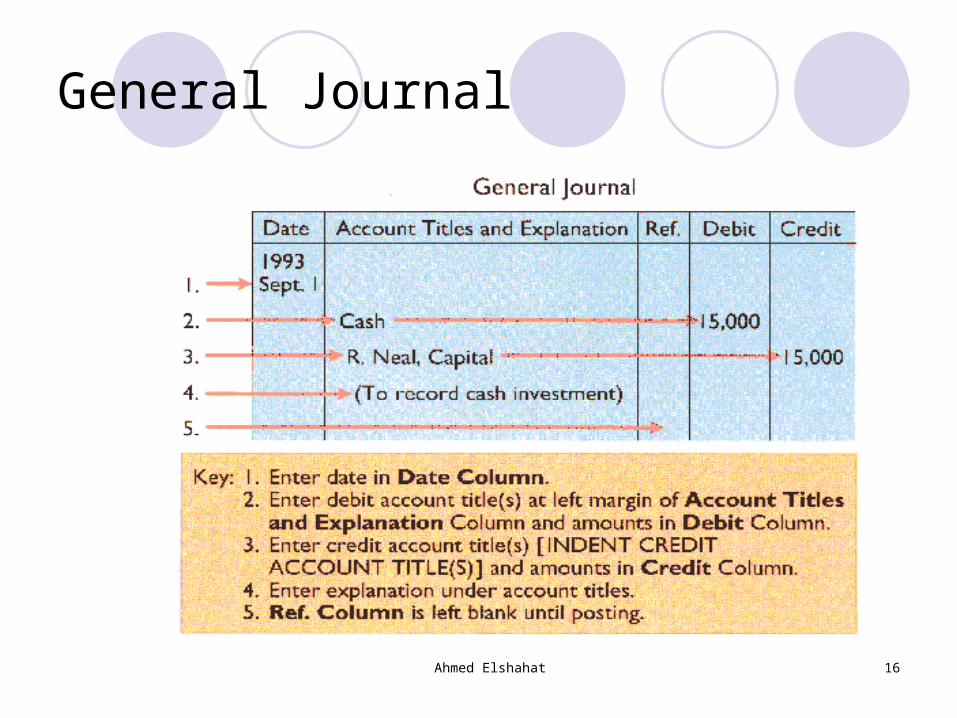

Journal (General Journal): Book of original entry

Ahmed Elshahat 11

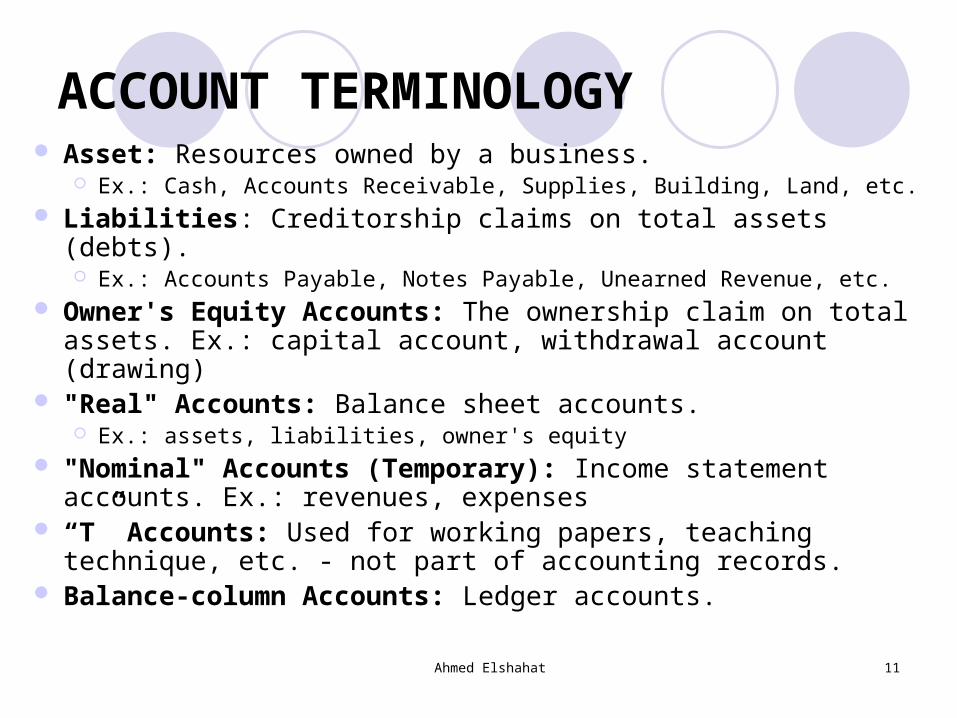

ACCOUNT TERMINOLOGY Asset: Resources owned by a business.

Ex.: Cash, Accounts Receivable, Supplies, Building, Land, etc. Liabilities: Creditorship claims on total assets (debts).

Ex.: Accounts Payable, Notes Payable, Unearned Revenue, etc. Owner's Equity Accounts: The ownership claim on total

assets. Ex.: capital account, withdrawal account (drawing) "Real" Accounts: Balance sheet accounts.

Ex.: assets, liabilities, owner's equity "Nominal" Accounts (Temporary): Income statement

accounts. Ex.: revenues, expenses “T” Accounts: Used for working papers, teaching

technique, etc. - not part of accounting records. Balance-column Accounts: Ledger accounts.

Ahmed Elshahat 12

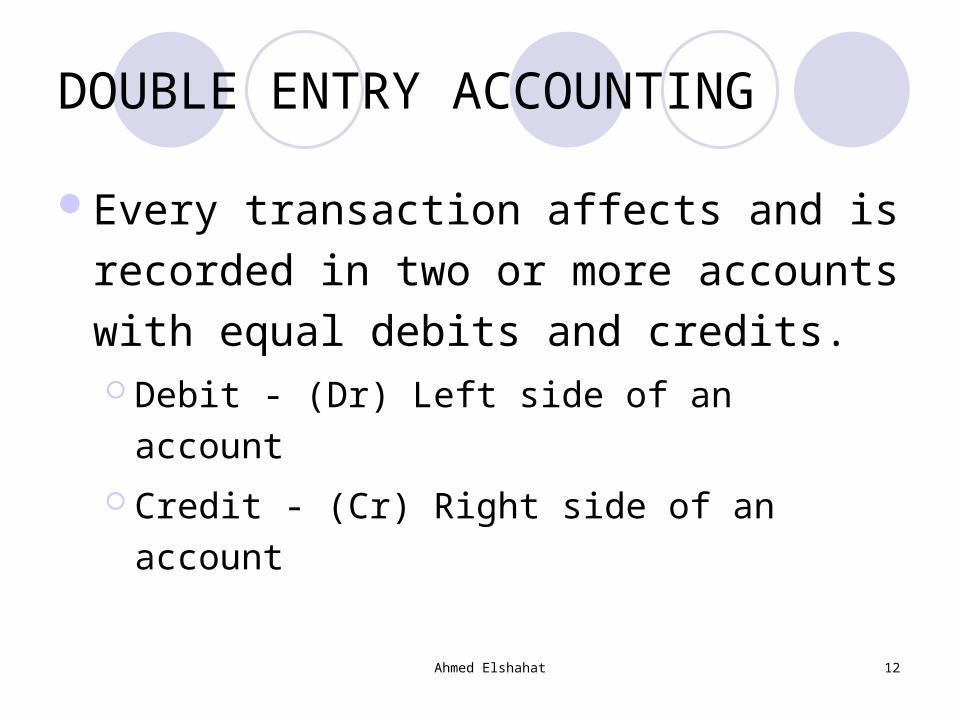

DOUBLE ENTRY ACCOUNTING

Every transaction affects and is recorded

in two or more accounts with equal debits

and credits. Debit - (Dr) Left side of an account

Credit - (Cr) Right side of an account

Ahmed Elshahat 13

JOU

RN

ALI

ZIN

G

Ahmed Elshahat 14

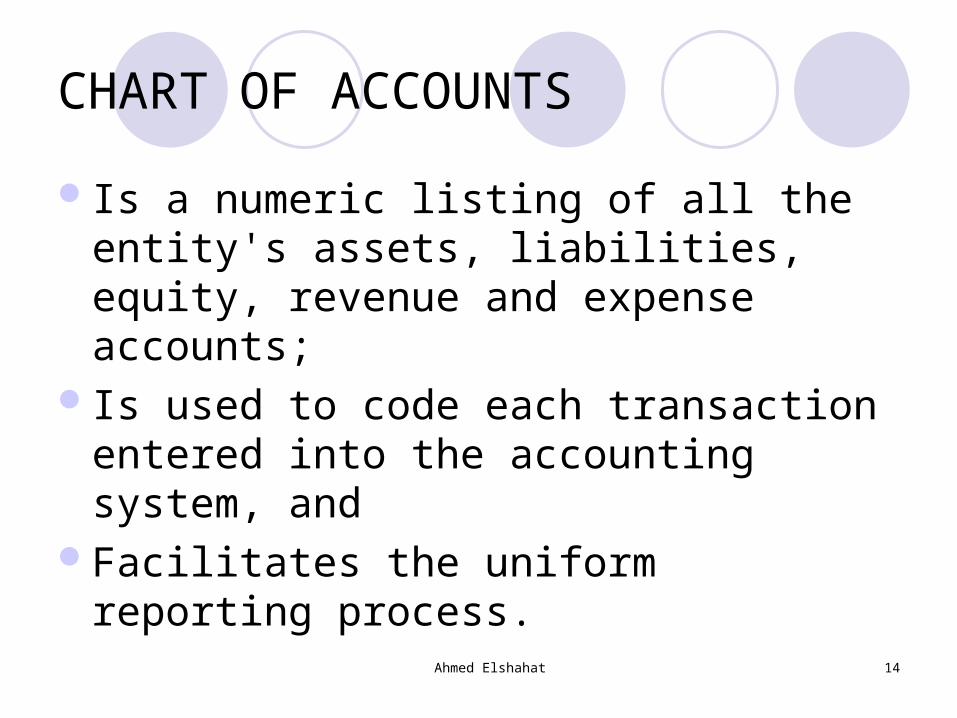

CHART OF ACCOUNTS

Is a numeric listing of all the entity's assets, liabilities, equity, revenue and expense accounts;

Is used to code each transaction entered into the accounting system, and

Facilitates the uniform reporting process.

Ahmed Elshahat 15

CHART OF ACCOUNTS

Ahmed Elshahat 16

General Journal

Ahmed Elshahat 17

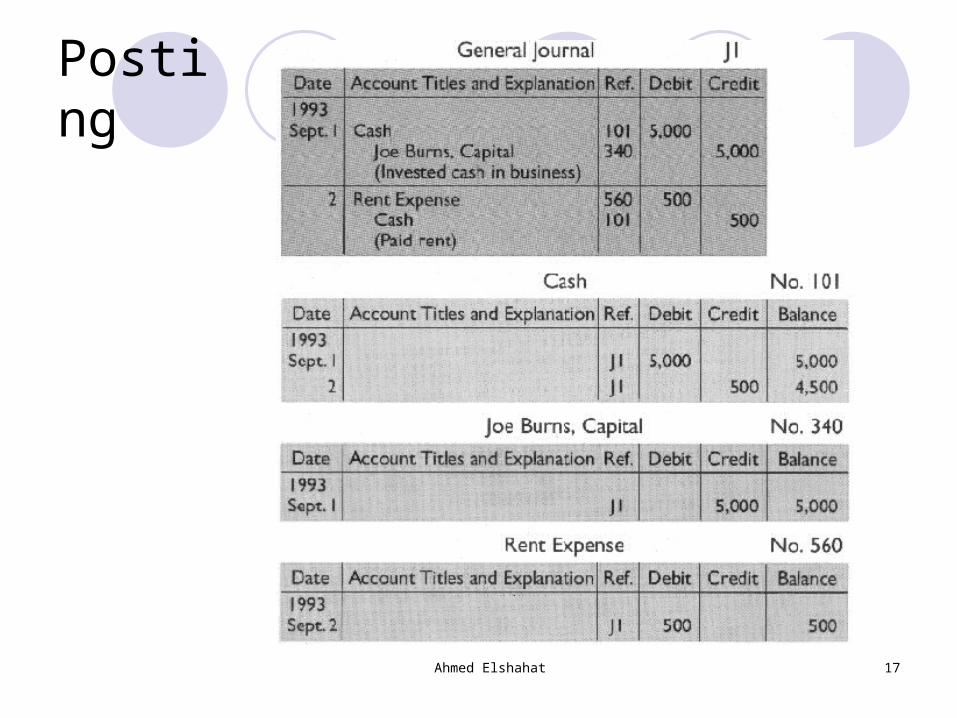

Posting

Ahmed Elshahat 18

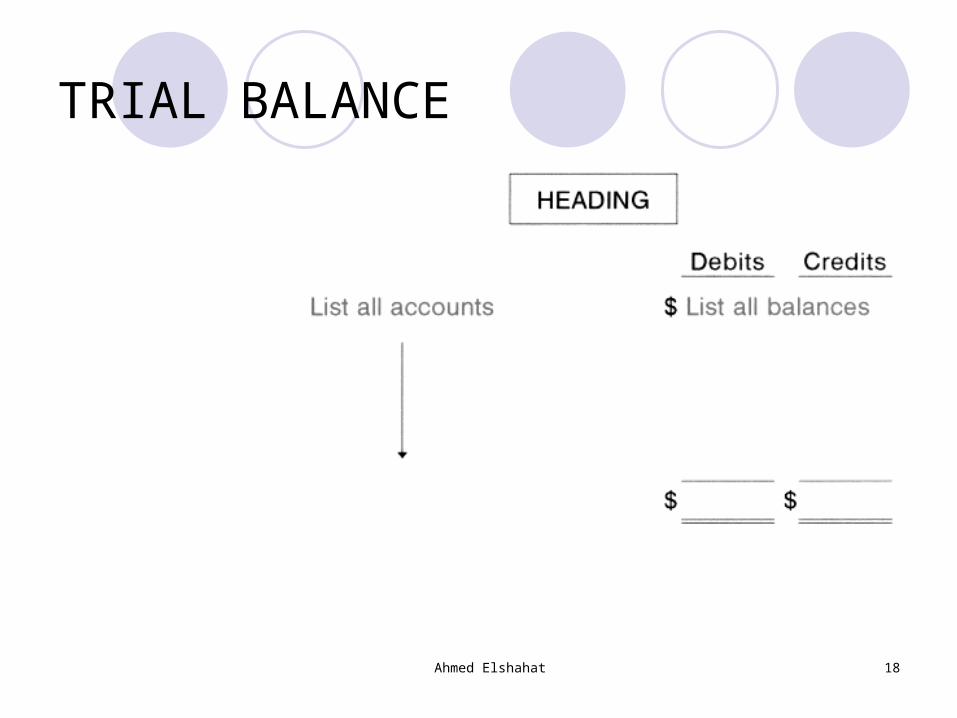

TRIAL BALANCE

Ahmed Elshahat 19

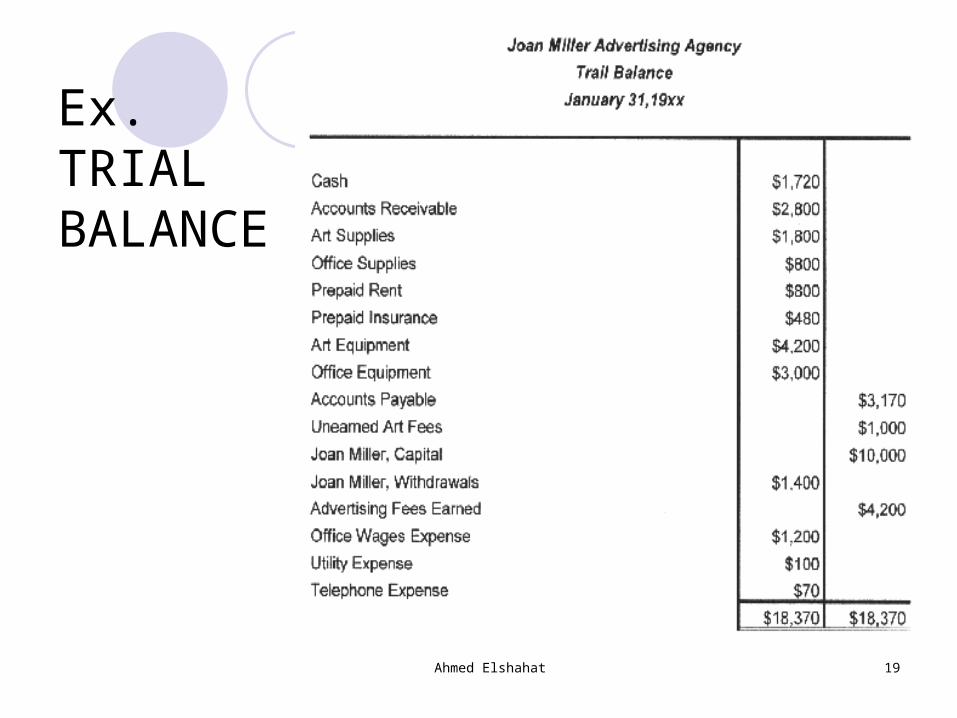

Ex. TRIAL BALANCE

Ahmed Elshahat 20

3. ADJUSTING AND CLOSING ENTRIES

WHAT ACCOUNTS ARE ADJUSTED? WHY ADJUST? Depreciation Accrual Relationships Types of Entries INCOME STATEMENT PREPARATION BALANCE SHEET PREPARATIONClosing Entries

Ahmed Elshahat 21

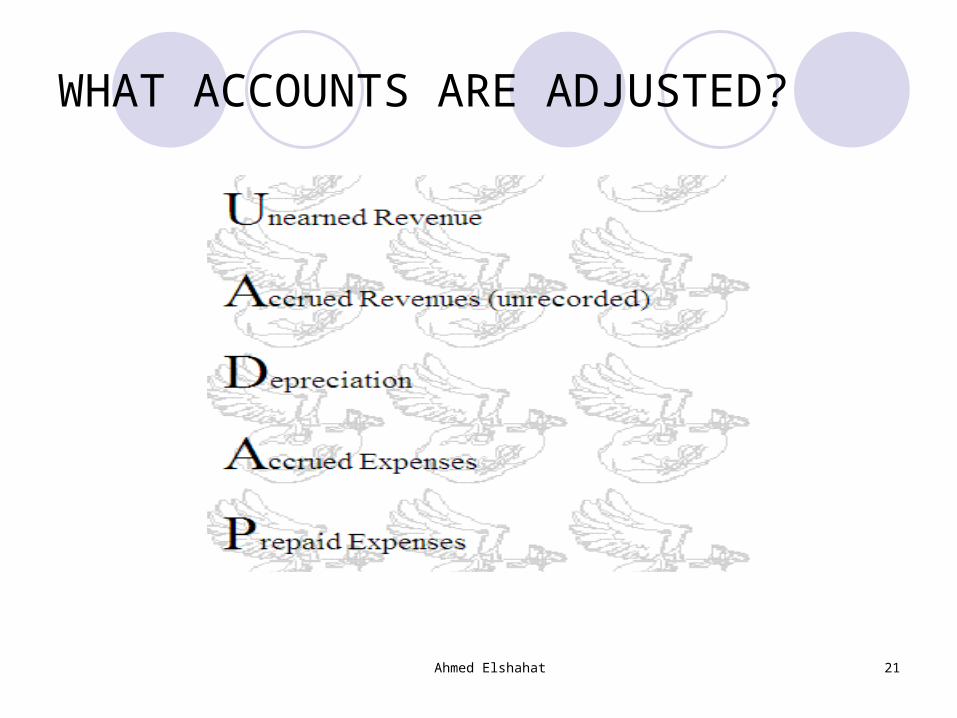

WHAT ACCOUNTS ARE ADJUSTED?

Ahmed Elshahat 22

WHY ADJUST?

Time Period Concept/Periodicity: The idea that the life of a business is

divisible into time periods of equal length. Ex: monthly, quarterly, annual... financial reports;

1. fiscal year

2. calendar year

3. natural business year

Ahmed Elshahat 23

WHY ADJUST? (Cont.)

Realization Principle requires that revenue be assigned to the accounting period in which it is earned, rather than to the period it is collected in cash (this is the basis for accrual accounting)

Matching Principle requires that revenues and expenses be matched; all expenses incurred in earning a revenue must be deducted from the revenue in determining net income

"True picture" -- accuracy

Ahmed Elshahat 24

Depreciation

Ahmed Elshahat 25

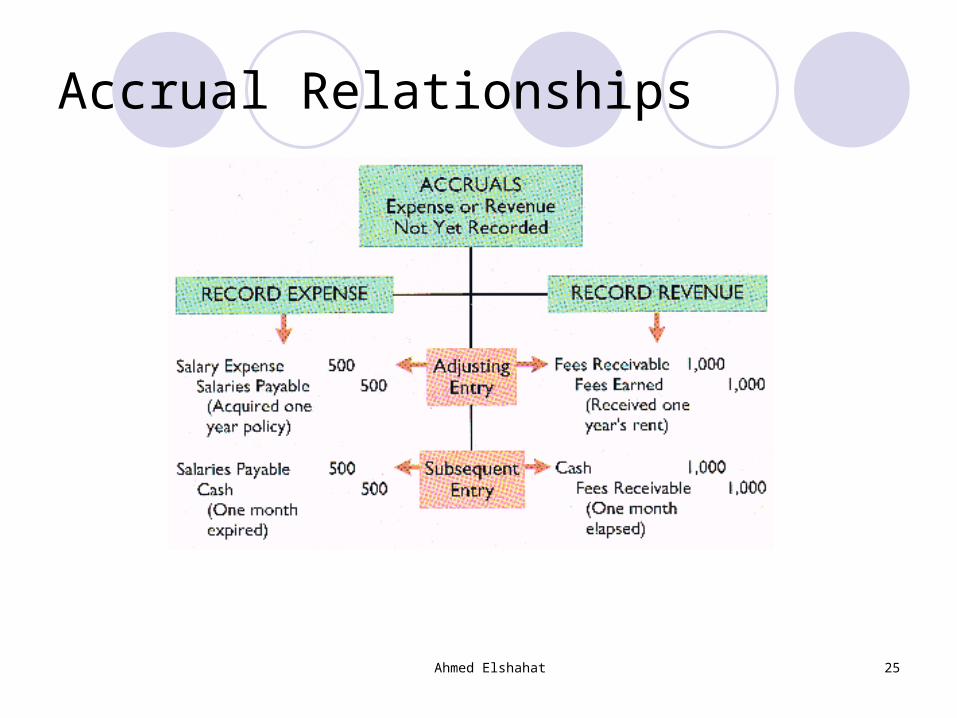

Accrual Relationships

Ahmed Elshahat 26

Types of Entries

Ahmed Elshahat 27

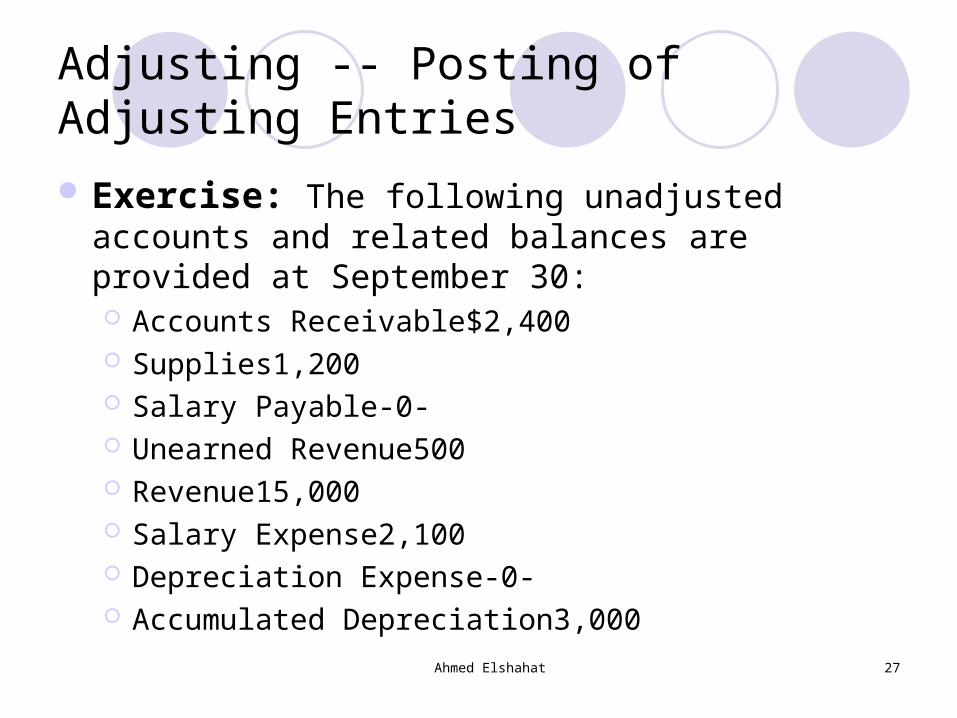

Adjusting -- Posting of Adjusting Entries

Exercise: The following unadjusted accounts and related balances are provided at September 30: Accounts Receivable$2,400 Supplies1,200 Salary Payable-0- Unearned Revenue500 Revenue15,000 Salary Expense2,100 Depreciation Expense-0- Accumulated Depreciation3,000

Ahmed Elshahat 28

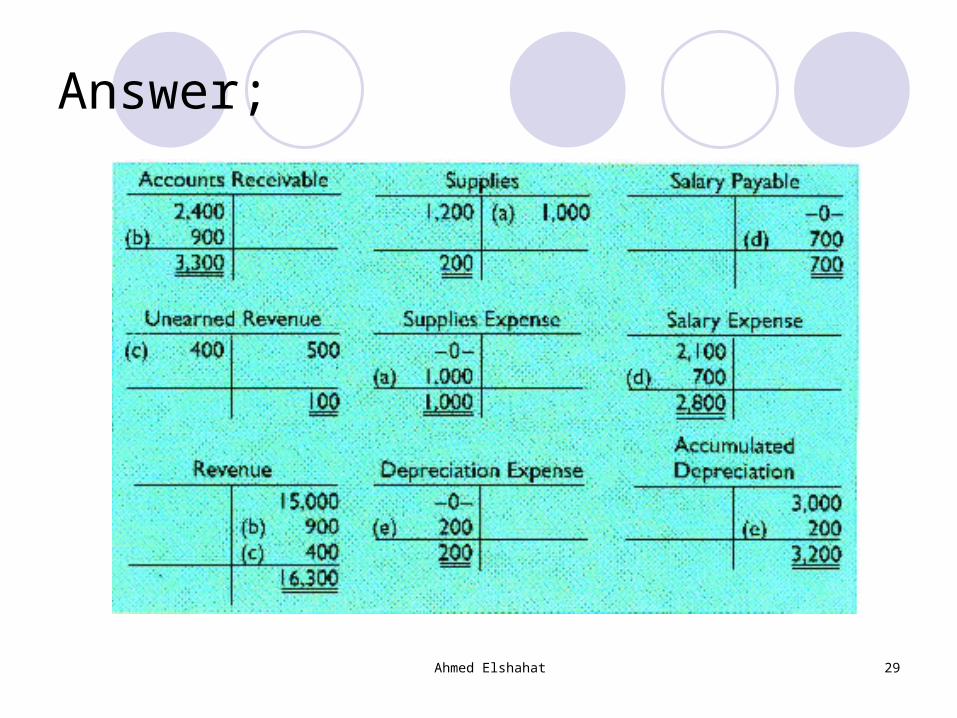

Instructions:

Open T-accounts and post the adjusting entries indicated from the following data:

(a) Supplies on hand, $200

(b) Revenue earned but not accrued, $900

(c) Unearned revenue earned but not recorded, $400

(d) Salary owed to employees, $700

(e) Depreciation of $200 is recognized.

Ahmed Elshahat 29

Answer;

Ahmed Elshahat 30

Summary

Ahmed Elshahat 31

Closing Entries

PURPOSE OF CLOSING ENTRIES

WHAT ACCOUNTS ARE CLOSED?

STEPS IN MAKING CLOSING ENTRIES

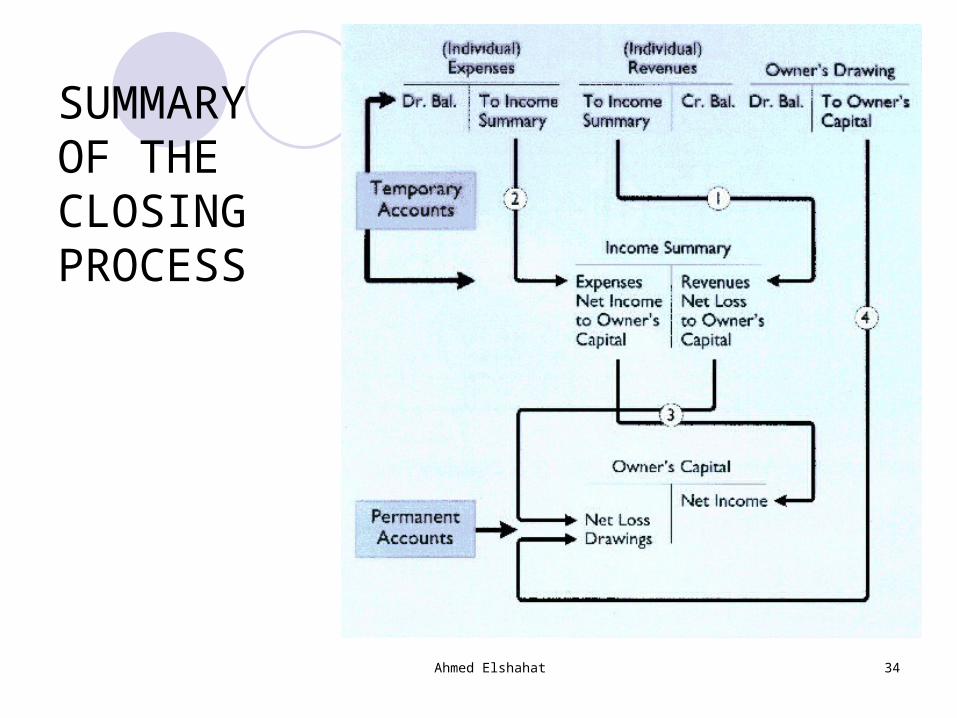

SUMMARY OF THE CLOSING

PROCESS

Ahmed Elshahat 32

PURPOSE OF CLOSING ENTRIES

Closing Entries are made to clear and close nominal accounts (Revenue and Expense) and to transfer the amount of net income or loss to capital accounts (i.e. Owner's Equity).

Accounts to be closed are; Revenues, expenses, drawings, income.

Ahmed Elshahat 33

STEPS IN MAKING CLOSING ENTRIES

Transfer credit balances from income statement to Income Summary

Transfer the debit balances from income statement to Income Summary

Transfer the Income Summary balance to the Capital account

Transfer the Withdrawals account balance to the Capital account

Ahmed Elshahat 34

SUMMARY OF THE CLOSING PROCESS