agfunder agrifood tech investing report 2017 the global food and agriculture industry. as with all...

TRANSCRIPT

I N V E S T I N G R E P O R T

AgFunder AgriFood Tech

Y E A R I N R E V I E W

AgFunder is an online Venture Capital Platform investing in

the bold and exceptional entrepreneurs

transforming our food and agriculture system

Are you a Corporate, Startup, or Investor? Learn how AgFunder can help you https://agfunder.com

As a Venture Capital Platform we build our own technology to invest globally and at

scale, to make better investment decisions, and to support our portfolio companies.

Through media and research AgFunder has built a community of over 50,000 members

and subscribers, giving us the largest and most powerful network in the industry.

See our portfolio companies: https://agfunder.com/listings

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 3

INTRODUCTION

AgriFood Tech:

2017 in ReviewAfter a relatively subdued 2016, we looked to 2017 to

be the year when agrifood tech investing got back on

track, and resumed the upward trend of previous years

with new players entering the market. This was easily

achieved with a new record level of venture investment,

characterized by a 29% increase in year-over-year

funding for agrifood technologies.

Food ecommerce continued to dominate the

downstream investment landscape, as the allure of the

more established players and their broader consumer

market access proved too much for venture capital to

resist.

In upstream technologies, 2017 was a fascinating year

from an investment perspective. We saw the creation of

two new agtech unicorns, as well as an ambitious

vertical farming startup with no revenue achieve a $200

million Series B round, led by the largest venture fund

ever created. It looks like farm tech has finally gone

mainstream.

The growing concern with the lack of notable exists in

the farm tech space also subsided in 2017, as the ag

majors began to throw off the shackles of recent

mergers and make strategic acquisitions to bolster their

technology and talent.

But these laudable developments occurred against a

backdrop of declining early stage investment. Seed

stage funding dollars dropped by 27% in 2017, along

with a 28% decline in number of companies funded.

Whilst we applaud the maturing of the market and the

larger investment levels coming in for later stage deals,

this trend could indicate a weakening pipeline ahead.

With a growing number of accelerators and seed stage

funds coming online globally, it appears to be a

transient concern as we anticipate good early stage

investment volumes in the burgeoning agrifood tech

markets like South America and Asia Pacific.

Michael Dean CIO, & The AgFunder Team

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 4

What is AgriFood Tech?

WHAT IS AGRIFOOD TECH?

Agrifood tech is the small but growing segment of the startup and venture capital universe that’s aiming to improve or disrupt the global food and agriculture industry.

As with all industries, technology plays a key role in the operation of the agrifood sector, a $7.8 trillion industry, responsible for feeding the planet and employing well over 40% of the global population. The pace of innovation has not kept up with other industries and today agriculture remains the least digitized of all major industries, according to McKinsey.

The industrial agrifood sector of today is also largely inefficient compared to other industries, with an increasing number of demands and constraints being placed on it. These pressures include a growing global population set to reach 9 billion by 2050; climate change and global warming; environmental degradation; changing consumer demands; limited natural resources; food waste; consumer health issues and chronic disease.

The need for agrifood tech innovation is greater than ever. This creates many opportunities for entrepreneurs and technologists to disrupt the industry and create new efficiencies at various points in the supply chain. Broadly speaking, agrifood tech startups are primarily aiming to solve the following challenges: food waste, Co2 emissions, chemical residues and run-off, drought, labor shortages,

health and sugar consumption, opaque supply chains and distribution inefficiencies, food safety and traceability, farm efficiency and profitability, and unsustainable meat production.

There are many ways to categorize agrifood tech startups highlighting the complexity of the industry. See page 5 for our categorization system, which we developed in consultation with venture capitalists, entrepreneurs, and other industry experts.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 5

AgriFood Tech Category Definitions

Farm Robotics, Mechanization & Equipment

On-farm machinery, automation, drone manufacturers, grow equipment

Novel Farming Systems

Indoor farms, aquaculture, insect, & algae production

In-Store Retail & Restaurant Tech

Shelf-stacking robots, 3D food printers, POS systems, food waste monitoring IoT

Home & Cooking Tech

Smart kitchen appliances, nutrition technologies, food testing devices

Supply Chain Technologies

Food safety & traceability tech, logistics & transport, processing tech

Bioenergy & Biomaterials

Non-food extraction & processing, feedstock technology, cannabis pharmaceuticals

Restaurant Marketplaces

Online tech platforms delivering food from a wide range of vendors

Farm Management Software, Sensing & IoT

Ag data capturing devices, decision support software, big data analytics

Ag Biotechnology

On-farm inputs for crop & animal ag including genetics, microbiome, breeding, animal health

eGrocery

Online stores and marketplaces for sale & delivery of processed & un-processed ag products to consumer.

WHAT IS AGRIFOOD TECH?

Agribusiness Marketplaces

Online Restaurants and Meal Kits

Startups offering culinary meals and sending pre-portioned ingredients to cook at home

Innovative Food

Cultured meat, novel ingredients, plant-based proteins,

Commodities trading platforms, online input procurement, equipment leasing

MiscellaneousUpstream

Downstream

Upstream+Downstream

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 6

Sources & Methodology

SOURCES

Data Sources & Curation

Utilizing new advanced machine-learning algorithms and

artificial intelligence to help identify and categorize agrifood

tech startups, our database has grown to over 11,000

companies, with new startups and historical data being

added each day.

The raw data for the AgriFood Tech Funding Report comes

from Crunchbase, which gathers publicly available

information such as press releases and US Securities and

Exchange Filings, as well as crowdsourcing directly from the

industry. AgFunder contributes a significant portion of raw

data through its own data collection methods that include

private communications with investors and companies.

The raw data is then heavily curated by the AgFunder team

to ensure that it is relevant, accurate, up-to-date, complete,

and categorized according to AgFunder’s proprietary

tagging system for inclusion in our report.

We believe our database represents the most

comprehensive and curated database of agrifood tech

companies globally.

While we are happy to share our findings, we reserve all

rights with respect to AgFunder research and this report, and

require it to be fully and accurately cited when any of the

data is used.

Because non-US companies are not required to publicly file

financings with their regulator, there may be many financings

absent from our analysis.

Undisclosed Financings

Of the 994 financings in our curated data set, 267 had

undisclosed financings, which could not be determined

through research or direct sources. We excluded

undisclosed financings when computing averages and

median values. In some cases, we were able to confidentially

obtain financing figures directly from the the investors, on the

condition that they only be included in the aggregate figures.

Multiple Financings

In some cases, CrunchBase displayed multiple financings for

the same company in the same year. In the case of distinct

funding rounds (Seed, A, B,…) or asset classes (debt v.

equity), we counted these as separate rounds. Where a

company raised capital two or more times within two months,

we aggregated the total into one round.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 7

Sources & Methodology

SOURCES

CategorizationAgFunder’s categorization system is designed to capture broad

themes in the agrifood technology landscape (see page 5 for a

list of categories). As the categories progress through the value

chain from farm inputs to the consumer, the mapping becomes

complex. The agrifood sector has a wide supply chain spanning

industrials, farming, logistics, wholesale distribution, processing,

retail distribution, and the consumer. In many cases,

technologies such as marketplaces connect different links in the

supply chain and so in this report we’ve chosen to focus on

high-level themes. To assist with the categorization and to avoid

subjectivity, AgFunder first employs over 150 machine learning

and artificial intelligence models to suggest category placement

and to help tag the company according to the technology and

its place in the supply chain. Finally, the AgFunder team

manually reviews the suggestions for each company, often with

significant research and debate among our team.

TimelinesIn most cases, the details of a funding are recorded within a few

days of its first public announcement. However, there are times

when these details are only shared months or even years after

the deal has officially closed. With new historical data constantly

coming into our system, it makes it difficult to make an apples-

to-apples comparison between years.

For the purposes of this report, covering deals closing on Jan 1 -

Dec 31, we give a 15-day grace period between the

announcement and the record date. Any new data not recorded

before Jan 15, will not be included in the report. Overall, we

estimate about 20% of additional funding rounds are eventually

reported after the cut-off date, but because most deals are

announced and reported at the same time, especially large

deals, this only represents about 5% in additional investment.

Since we are always incorporating more historical data, funding

totals for past years may not match past AgFunder reports.

Thank you to all of our data partners across the globe!

(see page 8)

Special Acknowledgement

Special thanks to Tim Li and the rest of the Crunchbase team for

their support and assistance.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 8

SOURCES

Our International Data PartnersIn addition to our partnership with CrunchBase, we’ve partnered with several groups from around the world to help us

collect more international data from a local level to ensure we can present the most comprehensive data set in the

industry. Our partners for the 2017 report include Start-up Nation Central in Israel, SP Ventures in Brazil, the BitsxBites

Accelerator in China, and the SproutX Accelerator in Australia.

ChinaIsrael

South America Australia

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 9

Year End Overview 2017

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 10

Co-Investment Fund

Co-invest with AgFunder and other leading venture capitalists in the next generation of agrifood technology startups

Now Open for InvestmentClosing by March 25, 2018

Accredited Investors only. Spots are limited. Investors admitted on a first-come basis.

https://agfunder.com/managed-fund

This does not constitute an offer to sell or a solicitation of an offer to buy any securities.

AgriFood Tech Funding Breakdown 2017

UpstreamAgBiotech,FarmManagementSW,FarmRobotics&Equipment,

Bioenergy&Biomaterials,NovelFarming,

AgribusinessMarketplaces,Midstream,InnovativeFood

DownstreamIn-storeRestaurant&Retail,OnlineRestaurants,eGrocery,

RestaurantMarketplaces,Home&Cooking

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 12

Notable Exits

YEAR IN REVIEW

By any account, 2017 was a good year for agrifood tech exits. That was not only because exciting exits in agrifood tech have

been few and far between for the last few years, but also because a couple of the major ag players — Deere & Company and

DowDuPont — made acquisitions. No longer distracted by consolidation and ensuing M&A transactions, this could be a signal

that the large strategic players will have more time, and money, to pursue more exits in 2018.

DowDuPont’s acquisition of farm management software

startup Granular for $300 million in August ticked many

boxes for a successful exit including a good investor

return and participation from an ag strategic. Granular

raised just $25 million in two rounds from some high

profile investors including Andreessen Horowitz, Khosla

Ventures, and GV (Google Ventures), along with

agriculture investor Fall Line Capital.

John Deere acquired ag robotics startup Blue River

Technology for $305 million in September. An obvious

match and route for Deere to build out its artificial

intelligence capabilities, the deal also provided a good

return for investors reaching 4x the valuation of the last

round. Investors included Khosla Ventures, Pontifax

Agtech, as well as ag industry giants Monsanto and

Syngenta. The company raised just over $30 million in

total since its founding.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 13

YEAR IN REVIEW

Key Insights for 20171. Jumbo Deals Bring Late Stage Investors

• Large deals characterized 2017 funding for agrifood tech

startups as the sector continued to mature and some large,

international investors placed bets.

• Perhaps the most high profile deal was the $200 million Series

B close from Plenty, the Californian indoor farming company.

The round attracted investment from Japan’s SoftBank via its

$100 billion Vision Fund. An early stage business, yet to post

any revenue, it broke records for farm tech funding when the

deal was announced in July.

• Plenty was soon overtaken by Indigo Agriculture, the

microbial seed coating company with an innovative business

model, as it raised $203 million in Series D funding after

attracting Dubai’s sovereign wealth fund. The round values

Indigo at over $1 billion, taking it to unicorn status.

• The year closed out with another agrifood tech unicorn in

Ginkgo Bioworks raising a whopping $275 million in Series D

funding involving private equity firm General Atlantic, Bill

Gates and Y Combinator’s Continuity Fund.

• The size of these rounds and the nature of the investors --

which include private equity capital -- indicate the intention of

some of these startups to build stand-alone businesses with

no plans for acquisition by the majors.

2. Strategics Shift Gear with M&A

• Monsanto’s purchase of The Climate Corporation for $1

billion in 2013 was the last major exit for an farm tech startup

until 2017, creating impatience and even concern in the

sector’s VC community. But the narrative changed when John

Deere and DowDuPont both made acquisitions of around

$300 million. Deere acquired ag robotics startup Blue River

Technology for $305 million and DowDuPont acquired

Granular for $300 million. Both acquisitions were motivated

by the corporates’ desire for both technology and personnel.

• While experts have long posited that agriculture was headed

for the “pharma model” of innovation, where large

entrenched players use acquisition as the primary mode of

obtaining new technologies, the large agribusinesses have

been distracted by consolidation and the ensuing M&A. Now,

the large strategic players could have more time, and money,

to pursue more exits in 2018.

• Indigo Agriculture and Farmers Business Network are two

startups that have confirmed they plan to list on a public

exchange instead of seeking acquisition as an exit.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 14

YEAR IN REVIEW

3. Seed Stage Slips as Sector Matures

• While total seed funding dropped by 28% year-over-year,

funding at every other stage increased with Series D deals

posting the greatest increase in total value: +108% year-over-

year to $2.3 billion.

• Consistent with global trends, the number of agrifood tech

funding deals dropped 17% in 2017, compared to a 27%

drop globally, according to Venture Pulse report.

• Most of this contraction came at the seed stage where activity

dropped 29% year-over-year compared to just a 4%

contraction between 2015 and 2016.

• Though having a greater share of deals at the later stage

shows a maturing in the sector, loss of activity at the seed

stage doesn’t bode well for years to come. It is also somewhat

surprising considering the large number of accelerator

programs and early-stage resources dedicated to agrifood

tech across the globe.

4. New Geographies Start to Rise

• Though seed stage deals are down worldwide, suggesting a

potential dip in future innovation, several developing

countries are stoking early stage innovation through new

accelerators and funds.

• Latin America, with some of the world’s largest agriculture

industries, is starting to catch up with its overseas

counterparts, particularly in Brazil and Argentina where SP

Ventures and NXTP Labs were among the most active farm

tech investors in 2017. Brazil’s SP Ventures made six

investments while Argentina’s NXTP Labs, an accelerator VC,

made eight. This trend moved in line with overall venture

capital figures; VenturePulse indicated Brazil’s VC ecosystem

grew 47% in 2017 to close $575 million in investment overall,

with strong activity in fintech.

• Agrifood tech investments can be slow to mimic global

venture trends, but we anticipate fintech and agrifood tech to

combine in future Brazilian agrifood tech deals. A stronger

connection between China and Latin America may also be

beneficial to agrifood tech startups.

• Israel, Australia, and Ireland are other countries on an upward

trajectory in terms of deal count as early stage resources get

going.

Key Insights for 2017 (Continued)

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 15

YEAR IN REVIEW

In 2017 agrifood tech financing increased by

29% year-over-year, which is consistent with

global trends. Agrifood tech investment has

certainly recovered from the 9% dip in

funding that occurred in 2016. That dip

reflected a 10% drop in the overall global

venture capital markets in that year.

Financing | $Billions

$3.0

$2.3

$5.1

$8.6

$7.8

$10.1

2012 2013 2014 2015 2016 2017

Annual Financings 2012-2017

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 16

Annual Financings 2012-2017 (Upstream)

YEAR IN REVIEW

Financing | $Billions

$2.4

$1.6

$2.5

$3.0

$3.4

$4.2

2012 2013 2014 2015 2016 2017

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 17

$0.6$0.8

$2.6

$5.5

$4.4

$5.9

2012 2013 2014 2015 2016 2017

Annual Financings 2012-2017 (Downstream)

YEAR IN REVIEW

Financing | $Billions

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 18

$7

88

$1

,20

1

$1

,56

8

$1

,56

2

$2

,45

9

$1

,80

3

$2

,67

3

$1

,63

0

$1

,78

6

$2

,87

0

$1

,65

4

$1

,49

9

$1

,87

1

$3

,00

1

$2

,98

7

$2

,25

2

184

209222

203

316 315

337

283

314 312

284 287 293 287

237

177

2014-Q1 2014-Q2 2014-Q3 2014-Q4 2015-Q1 2015-Q2 2015-Q3 2015-Q4 2016-Q1 2016-Q2 2016-Q3 2016-Q4 2017-Q1 2017-Q2 2017-Q3 2017-Q4

YEAR IN REVIEW

# Deals

Financing | $Millions

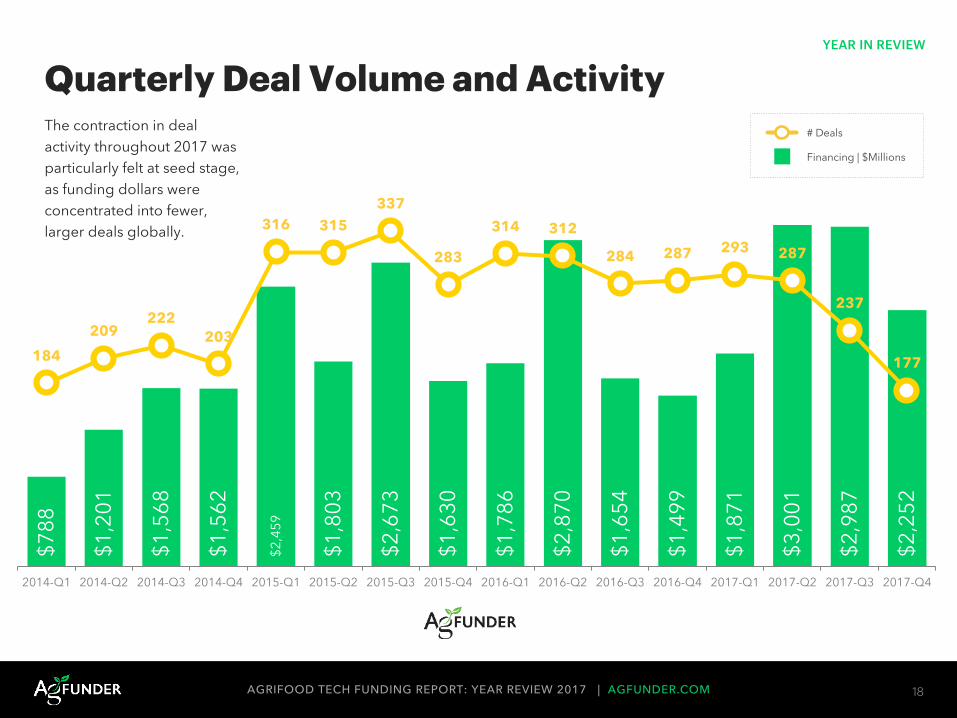

The contraction in deal

activity throughout 2017 was

particularly felt at seed stage,

as funding dollars were

concentrated into fewer,

larger deals globally.

Quarterly Deal Volume and Activity

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 19

$5

32

$5

03

$6

08

$8

91

$6

60

$6

34

$9

58

$7

71

$7

41

$9

27

$8

70

$8

76

$8

80

$9

43

$1

,12

6

$1

,23

6

106

127123 119

172

153

143135

168162

172

144

163171

126

110

2014-Q1 2014-Q2 2014-Q3 2014-Q4 2015-Q1 2015-Q2 2015-Q3 2015-Q4 2016-Q1 2016-Q2 2016-Q3 2016-Q4 2017-Q1 2017-Q2 2017-Q3 2017-Q4

Quarterly Deal Volume and Activity (Upstream)

YEAR IN REVIEW

# Deals

Financing | $Millions

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 20

$2

57

$6

99

$9

60

$6

71

$1

,79

8

$1

,16

9

$1

,71

4

$8

59

$1

,04

5

$1

,94

3

$7

83

$6

23

$9

91

$2

,05

8

$1

,86

1

$9

97

78 82

99

84

144

162

194

148 146 150

112

143

130

116111

66

2014-Q1 2014-Q2 2014-Q3 2014-Q4 2015-Q1 2015-Q2 2015-Q3 2015-Q4 2016-Q1 2016-Q2 2016-Q3 2016-Q4 2017-Q1 2017-Q2 2017-Q3 2017-Q4

YEAR IN REVIEW

# Deals

Financing | $Millions

Quarterly Deal Volume and Activity (Downstream)

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 21

Innovation Services

Setting up your own Corporate Innovation Center here in Silicon Valley can cost well over $1 million annually. By accessing our

investment infrastructure, AgFunder Innovation Services can get you there faster and at a fraction of the cost. Whether you need

help setting up your own Corporate Venture Capital unit, or want a team in Silicon Valley to help support your Business Development

or Partnerships teams. We can help.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 22

Deals by Category

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 23

Key Insights - Category

DEALS BY CATEGORY

1. eGrocery startups raised 96% more funding in 2017 than

2016, driven largely by international deals that

demonstrate investors’ continued interest in the space

despite multiple VC-backed failures.

2. While Restaurant Marketplaces seemed to continue to

dominate funding in the Mid Year report, by the end of

2017 the category represented a smaller portion of the

agrifood tech funding than in the past with 21% of the pie.

However overall, funding for the category still increased

14% year-over-year.

3. Midstream Technologies became the third best-funded

category in 2017 with 9% of total funding and 89 startups

raising $924 million. Growth in Midstream Technologies

funding volume is largely based on the $275 million Series

D round for microbe manufacturing company Ginkgo

Bioworks, which represents 30% of funding in that

category.

4. Novel Farming Systems had a big year in 2017 raising

$652 million across 57 deals, a 233% increase on 2016.

This growing category doubled its share of agrifood tech

dollars to represent 6% of total funding in 2017. Plenty’s

$200 million Series B was by far the largest contributor to

this category. Without this record-breaking deal, Novel

Farming Systems would drop four places in the ranking

behind Agribusiness Marketplaces, Online Restaurants

and Meal Kits, and Farm Management Software, Sensing,

& IoT.

5. Ag Biotechnology continues to decrease in both

investment and share of the total agrifood tech pie,

dropping by 11% in total funding year-over-year in 2017

despite two deals bringing in $100 million or more. While

showing signs that investor appetite for ag biotechnology

may be slowing down, this category also demonstrates

that $100+ million rounds are becoming more common

across all categories whether technically “hot” or not.

Restaurant Marketplaces, eGrocery, Midstream

Technologies, Ag Biotechnology, Novel Farming Systems,

In-store Retail & Restaurant Tech, and Agribusiness

Marketplaces all saw deals over $100 million.

6. Funding volume for Innovative Food startups stayed

virtually the same year-over-year raising $411 million in

2017. However, deal count in this category dropped by

23% to 50 deals keeping with the trend of fewer, larger

deals overall.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 24

2017 AgriFood Tech InvestmentDEALS BY CATEGORY

24%

21%

9%

8%

7%

6%

5%

5%

5%

4% 2%

1% 1% 1% eGrocer

Restaurant Marketplaces

Midstream Technologies

In-Store Retail & Restaurant

Ag Biotechnology

Novel Farming Systems

Agribusiness Marketplaces

Online Restaurants

Farm Mgmt SW, Sensing & IoT

Innovative Food

Bioenergy & Biomaterials

Robotics, Mech. & Farm Eq

Home & Cooking

Miscellaneous

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 25

$2,398

$2,110

$924

$826

$696

$652

$541

$487

$464

$411

$238

$209

$85

$71

eGrocer

Restaurant Marketplaces

Midstream Technologies

In-Store Retail & Restaurant Tech

Ag Biotechnology

Novel Farming Systems

Agribusiness Marketplaces

Online Restaurants & Mealkits

Farm Mgmt SW, Sensing & IoT

Innovative Food

Bioenergy & Biomaterials

Robotics, Mechanization & Other …

Home & Cooking

Miscellaneous

59

89

154

67

57

49

74

134

49

49

59

32

35

Deal Volume and Activity by Category

DEALS BY CATEGORY

104• Though the number of eGrocery deals

declined 33% year-over-year, dollar

financing in this category increased 96%,

overtaking Restaurant Marketplaces, the

best-funded category in 2016. Seven

eGrocery startups raised more than $100

million including Chinese eGrocer

MissFresh’s $500 million and Instacart’s

$400 million Series D rounds.

• Other categories, such as Online

Restaurants and Midstream Technologies,

also saw this drop in deal count with a

bump in total dollar funding highlighting

the overall trend for larger deals as the

sector matures.

• Funding for Home and Cooking startups,

which include consumer appliances for

growing and preparing food, contracted

by 58% while deal count virtually stayed

the same year-over-year.

Financing | $Millions

Upstream Financing

Downstream Financing

Upstream+Downstream

# Deals

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 26

0bn

1bn

2bn

3bn

4bn

5bneGrocer

Robotics, Mechanization & Farm Eq

Restaurant Marketplaces

Online Restaurants & Mealkits

Novel Farming Systems

Miscellaneous

Midstream Technologies

Innovative Food

In-Store Retail & Restaurant Tech

Home & Cooking

Farm Mgmt SW, Sensing & IoT

Bioenergy & Biomaterials

Agribusiness Marketplaces

Ag Biotechnology

Investment by Category 2014-2017

DEALS BY CATEGORY

2014-H1 2014-H2 2015-H1 2015-H2 2016-H1 2016-H2 2017-H1 2017-H2

• Investment grew year-over-year in

11 categories including eGrocery

(96% to $2.4bn), Restaurant

Marketplaces (14% to $2.1bn), In-

store Retail & Restaurant Tech (3%

to $826m), Midstream

Technologies (29% to $924m),

Innovative Food (5% to $411m),

Farm Management Software,

Sensing, & IoT (27% to $464m),

Online Restaurants (54% to $487m),

Agribusiness Marketplaces (73% to

$541m), Novel Farming Systems

(233% to $652m), Robotics

Mechanization & Farm Equipment

(17% to $209m) .

• Categories that experienced a drop

in funding were Ag Biotech (-11%),

Bioenergy & Biomaterials (-33%),

Home and Cooking (-58%), and

Miscellaneous (-38%).

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 27

$4

.5

$2

.8

$2

.0

$1

.1

$1

.5

$1

.7

$1

.6

$4

.6

$2

.7

$2

.3

$3

.2

$2

.1

$1

.1

$2

.0

Median Deal Size by Category

DEALS BY CATEGORY

Median overall: $2.0m

Financing | $Millions

Upstream Financing

Downstream Financing

Up+Down Financing

• Overall, the median size of agrifood

deals increased by 67% year-over-

year to $2 million from $1.2 million.

As in 2016, Ag Biotechnology

posted the highest median as a

capital intensive category.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 28

Top 15 eGrocery Deals

DEALS BY STAGE

$500.0

$400.0

$300.0

$293.1

$230.0

$108.5

$100.0

$45.0

$44.4

$40.0

$35.0

$35.0

$27.0

$21.0

$18.1

MissFresh

Instacart

Yiguo.com

Bigbasket.com

MissFresh

Picnic

MissFresh

Bigbasket.com

FreshMarket

Shipt

Brandless

Sugarfina

Eaze

Cornershop

Mathem Financing | $Millions

• eGrocery startups raised $2.4 billion in 2017 – up

96% from 2016. As consumers around the world

become accustomed to buying food online,

ecommerce continues to be a prominent force in

agrifood tech investment despite having more

startup casualties than most.

• Chinese eGrocers dominate this list not only in

funding, but in number. MissFresh, Yiguo, and

FreshMarket are all Chinese startups. Other

countries outside the US represented are India

(BigBasket), The Netherlands (Picnic), and

Sweden (Mathem).

• Brandless is the youngest company within the top

eGrocery deals. The San Francisco-based startup,

which sells only private-label products, has raised

two rounds of funding since its founding in 2016.

• Eaze is a San Francisco-based cannabis delivery

service. The company raised a $27 million Series

B round in 2017 in part, in order to get ready for

the legalization of recreational cannabis in

California, which went into effect in January 2018.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 29

Top 15 Ag Biotechnology Deals

DEALS BY CATEGORY

Financing | $Millions

$203.0

$100.0

$40.0

$29.0

$25.0

$24.5

$24.0

$23.0

$21.0

$19.3

$15.4

$15.0

$13.2

$12.5

$12.3

Indigo

Bayer–Gingko Fertilizer Partnership

Calysta Energy

Inocucor Technologies

AquaBounty Technologies

Two Pore Guys, Inc.

Newleaf Symbiotics

Muse bio

Provivi

Cool Planet Energy Systems

Agrisoma

Phytelligence

DNA Script

Roslin Technologies

Asilomar Bio

• Ag biotechnology financing contracted

11% year-over-year to reach $670

million, yet it contains some of the

largest deals of the year.

• The leading ag biotech deals

demonstrate the diversity within this

category that goes far beyond crop

inputs and seeds to genetically

modified seafood (AquaBounty) and

animal feed (Calysta and Roslin Tech).

• Indigo Agriculture, the Boston-based

microbial crop technology startup,

closed its Series D funding round on

$203 million: the largest fundraising

effort by a farm tech company to date.

• Other biological crop input startups

Inocucor Technologies, Newleaf

Symbiotics, Provivi, and the yet

unnamed Bayer - Ginkgo Bioworks

joint venture, also made the top 10 ag

biotech deals.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 30

Top 15 Novel Farming Systems Deals

DEALS BY CATEGORY

Financing | $Millions

$200.0

$73.6

$52.5

$50.4

$40.0

$32.0

$26.5

$25.0

$24.0

$20.0

$13.6

$10.0

$8.1

$7.5

$7.3

Plenty Inc.

Aphria

TerrAscend

Protix Biosystems

AeroFarms

Cronos Group

MPX Bioceutical

Aphria

Cannabco Pharmaceutical Corp

Bowery Farming Inc

Cronos Group

MGC Pharmaceuticals

Holistic Industries

Bowery Farming Inc

Freight Farms

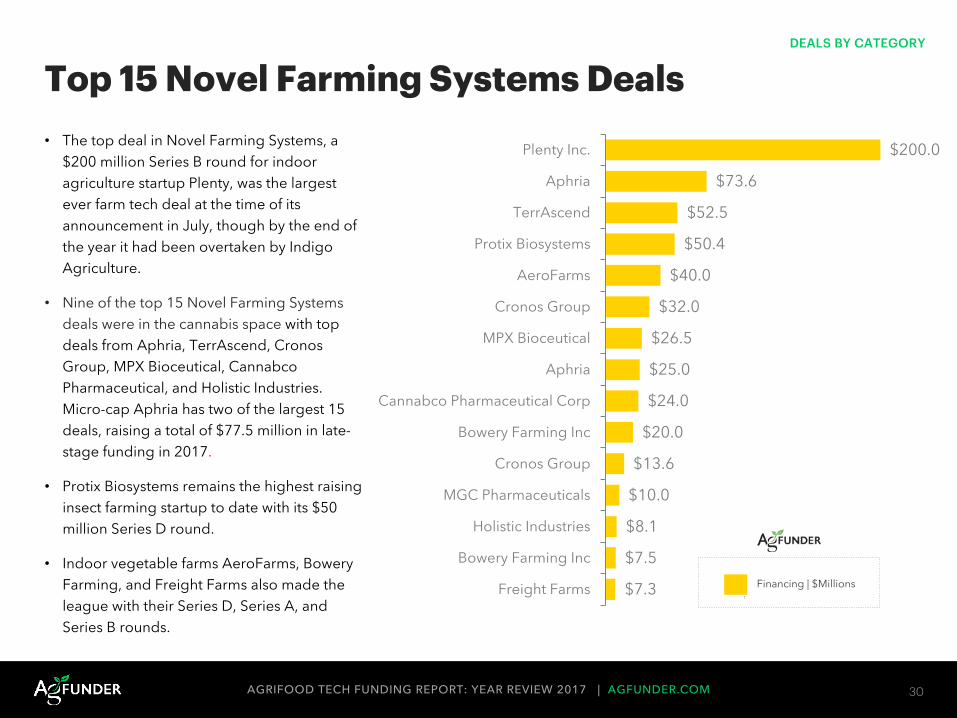

• The top deal in Novel Farming Systems, a

$200 million Series B round for indoor

agriculture startup Plenty, was the largest

ever farm tech deal at the time of its

announcement in July, though by the end of

the year it had been overtaken by Indigo

Agriculture.

• Nine of the top 15 Novel Farming Systems

deals were in the cannabis space with top

deals from Aphria, TerrAscend, Cronos

Group, MPX Bioceutical, Cannabco

Pharmaceutical, and Holistic Industries.

Micro-cap Aphria has two of the largest 15

deals, raising a total of $77.5 million in late-

stage funding in 2017.

• Protix Biosystems remains the highest raising

insect farming startup to date with its $50

million Series D round.

• Indoor vegetable farms AeroFarms, Bowery

Farming, and Freight Farms also made the

league with their Series D, Series A, and

Series B rounds.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 31

Top 15 Midstream Deals

DEALS BY CATEGORY

Financing | $Millions

$275.0

$68.0

$62.0

$45.0

$42.0

$40.0

$30.4

$30.0

$21.5

$21.0

$17.5

$17.2

$16.0

$15.5

$15.4

Ginkgo Bioworks

Inagora

Convoy

Vayyar

Transfix

Samsara Networks Inc

Mesh Korea

rfXcel

Mesh Korea

Label Insight, Inc

Intralytix

Starship Technologies

Flirtey

icix

Cobot

• Increasing demand for transparency,

traceability, efficiency and safe food drives

much of the innovation taking place in the

midstream category (post farm gate/pre-

consumer).

• Investment in Midstream Technologies startups

increased 29% year-over-year to $924 million.

• Ginkgo Bioworks, a Boston startup genetically

engineering microbes for the flavor, fragrance,

agriculture, and food industries, closed out

2017 with a $275 million Series D round,

bringing the company’s total funding to $429

million. Ginkgo is also partnering with Bayer on

a yet-unnamed $100 million ag biotech joint

venture.

• Prominent midstream startups are often multi-

industrial. Convoy, for example, is a service that

matches loads with available contract truck

drivers. The service has been particularly

valuable for growers of produce with a short

season and short shelf-life.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 32

Top 15 In-Store Retail & Restaurant Deals

DEALS BY CATEGORY

• In-store Retail & Restaurant Tech saw

modest growth in 2017 growing 3% to

$826 million.

• The top-raising startups were both point of

sale systems with Canada’s Lightspeed POS

and Boston-based Toast.

• In-restaurant robotics remains a slow-

growing sector of agrifood tech, but two

robotics startups made the top 15.

Momentum Machines, the creator of the

burger-making robot, raised a $18.4 million

Series A from GV (Google Ventures), and

Khosla Ventures among others. And Bossa

Nova raised a $17.5 million Series B round

involving Intel Capital. Bossa Nova robots

scan shelves in order to count inventory

and find misplaced items while dodging

obstacles like stray shopping carts.

Financing | $Millions

$166.0

$101.0

$55.0

$42.9

$35.0

$22.4

$20.0

$20.0

$18.4

$17.5

$15.0

$15.0

$14.7

$13.3

$13.0

Lightspeed POS

Toast

Gather Technologies

Ritual

Revel Systems

Keruyun Technology

Seasoned.co

ChowNow

Momentum Machines

Bossa Nova Robotics Inc.

Dajialai

Slice

Bingobox

Chope Group

Resy

$2.6bnINVESTED

UNIQUE INVESTORS

625 $203mBIGGEST DEAL

-9%DEAL GROWTHDEALS

345

+32%INVESTMENT GROWTH

Farm Tech Spotlight 2017

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 34

Key Insights – Farm Technology

FARM TECH SPOTLIGHT

1. Farm technology is an important subset of the agrifood

tech landscape, and is often what’s intended when people

refer to the more inclusive definition of ‘agtech.’ By our

definition, farm tech exclusively captures the companies

with technologies in use on farms. For edge cases, we’ve

erred toward a more exclusive definition. See the full list of

categories within farm tech on the next page. Some of

these category names are identical to those within the full

agrifood tech context but in this section, the startups within

them are restricted to those used on the farm.

2. Farm tech investment represented 26% of total agrifood

tech funding volume in 2017, reaching $2.6 billion. The

farm tech funding total represents a 32% year-over-year

increase, while deal activity actually decreased by 9% as

larger and later stage deals pushed up the investment

total.

3. Farm tech saw some exciting exits in 2017 with John Deere

acquiring robotics company Blue River Technology for

$305 million, and DowDuPont acquiring farm management

software platform Granular for $300 million. Both exits

were applauded by investors as large agricultural

corporates look to acquire the innovation they find difficult

to foster in-house. Likewise, international fertilizer giant

Yara acquired nitrogen modeling platform Adapt-N from

Agronomic Technology Corp for an undisclosed amount.

4. Agribusiness Marketplaces are quickly becoming the

category to watch within farm tech as Farmers Business

Network (FBN) in the US and Maihuolang in China became

some of the best-funded farm tech startups. The category

raised $511 million in 2017 representing 77% growth year-

over-year, which included two rounds from FBN totaling

$150 million.

5. Novel Farming Systems also raised eye-catching rounds in

2017, including indoor vegetable farming startup Plenty’s

$200 million Series B from Japan’s Softbank, insect farming

company Protix Biosystems’ $50 million round, and

AeroFarms’ $40 million Series D round. Cannabis growers

also posted big raises pushing funding in this category to

increase by 243% to $652 million.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 35

Farm Tech Category Definitions

FARM TECH SPOTLIGHT

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 36

Farm Tech Financing 2014-2017

FARM TECH SPOTLIGHT

• Farm tech funding volumes increased 32% year-over-year, but deal activity declined 9% as

larger and later stage deals dominated the space in 2017. As more 2017 historical data is

released we can expect to see an increase in the total number of (typically small) companies

funded without greatly affecting the total funding dollars.

Financing | $Millions

# Deals

$608

$878

$844

$901

$990

$893

$1,348

$1,255

149 152

215

155

197

183

209

136

2014-H1 2014-H2 2015-H1 2015-H2 2016-H1 2016-H2 2017-H1 2017-H2

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 37

Farm Tech Deal Volume & Activity by Category

FARM TECH SPOTLIGHT

• Farm tech investments increased year-

over-year in five farm tech categories:

Novel Farming Systems (243%),

Agribusiness Marketplaces (77%), Farm

Management Software, Sensing & IoT

(37%), Robotics, Mechanization &

Other Farm Equipment (16%), and

Bioenergy & Biomaterials (500%).

• On the other hand, Ag Biotechnology

(-11%) and Farm-to-Consumer

eGrocery (-33%) experienced

contractions in funding.

• Keeping with the theme of fewer,

larger deals in 2017, deal count

decreased in almost every category

within farm tech, though not as

dramatically as in the whole of agrifood

tech. Ag Biotechnology (-30%) and

eGrocery (-50%) saw the steepest

drops in deal count. No other category

saw deal count changed more than

10% year-over-year.

Financing | $Millions

# Deals

$670

$586

$511

$461

$209

$42

$41

$24

$60

Ag Biotechnology

Novel Farming Systems

Agribusiness Marketplaces

Farm Mgmt SW, Sensing & IoT

Robotics, Mechanization & Farm Eq

Bioenergy & Biomaterials

Midstream Technologies

Farm-to-Consumer eGrocery

Miscellaneous

39

37

131

38

6

8

5

18

62

Financing | $Millions

Upstream Financing

Downstream Financing

Up+Down Financing

# Deals

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 38

Farm Technology Category Breakdown

FARM TECH SPOTLIGHT

26%

22%

20%

18%

8%

2% 1%

2% Ag Biotechnology

Novel Farming Systems

Agribusiness Marketplaces

Farm Mgmt SW, Sensing &

IoT

Robotics, Mechanization &

Farm Eq

Bioenergy & Biomaterials

Midstream Technologies

Farm-to-Consumer

eGrocery

Miscellaneous

• In 2017, Novel Farming

Systems jumped over

Agribusiness

Marketplaces and Farm

Management Software,

Sensing & IoT to

become the second

best-financed category

within farm tech. Since

many of these

businesses have high

overhead costs, we

expect more large

rounds to come in this

category with the caveat

that investors may want

to see clear results from

existing players before

funding new ones.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 39

Top 20 Farm Tech Deals

FARM TECH SPOTLIGHT

• There is perhaps no more visible marker of the

maturing of the farm tech startup ecosystem than the

growing values of the top farm tech deals. In 2016

only two top deals were valued at more than $50

million, but in 2017, half of the top 20 deals

exceeded $50 million.

• The Top 20 deals for startups operating at the farm

level were wide-ranging, including Novel Farming

Systems, Ag Biotechnology, Agribusiness

Marketplaces, and Farm Management Software,

Sensing, & IoT.

• The first sign that 2017 would be a big year for farm

tech was the $150 million Series A for Chinese

Agribusiness Marketplace Maihuolang, followed by

indoor farm Plenty’s $200 million Series A. These

large, early rounds set a new tone for farm tech deals.

• European insect farming group Protix raised the

largest insect farming deal on record with a $50

million round. Though excitement around insect

farming persists, it has not yet been matched with

equivalent funding.

$203.0

$200.0

$150.0

$110.0

$100.0

$73.6

$70.0

$70.0

$53.0

$50.4

$50.0

$40.0

$40.0

$40.0

$34.0

$33.0

$32.0

$30.0

$29.0

$29.0

Indigo

Plenty Inc.

Maihuolang

Farmers Business Network

Bayer–Gingko Partnership

Aphria

Spire

ProducePay

3D Robotics

Protix Biosystems

Orbital Insight Inc.

Calysta Energy

Farmers Business Network

AeroFarms

Swift Navigation

Kespry

Cronos Group

Descartes Labs

Dafengshou

Inocucor Technologies Financing | $Millions

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 40

Most Active Farm Tech Investors

FARM TECH SPOTLIGHT

• In what can likely be taken as a sign of the

gradual mainstreaming of farm tech

investing, the two most active investors

are not sector-focused.

• SOSV, the “accelerator VC”, tops both the

farm tech and overall agrifood tech

investor leagues.

• Sector-focused accelerators across the

globe were also active investors including

SVG Partners, manager of California’s

THRIVE Agtech accelerator, NXTP Labs,

the Latin American accelerator, and

SproutX, Australia’s first agtech

accelerator.

• Syngenta Ventures was the most active

strategic corporate VC in the fam tech

space making five investments in 2017.

Monsanto Growth Ventures (4), Maumee

Ventures (3), BASF Venture Capital (3),

Taylor Farms Ventures (2), and Cargill (1)

also participated in deals.

INVESTOR LOCATION#

INVESTMENTS

SOSV Princeton, NJ 12

Y Combinator Mountain View, CA 10

SVG Partners Los Gatos, CA 9

NXTP Labs Buenos Aires, Argentina 8

SproutX Melbourne, Australia 6

SP Ventures Sao Paulo, Brazil 6

Fall Line Capital San Mateo, CA 5

GV Mountain View, CA 5

Syngenta Ventures Basel, Switzerland 5

Lewis & Clark Ventures St. Louis, MO 5

Deals by Stage

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 42

Key Insights – by Stage

DEALS BY STAGE

1. Overall agrifood tech deal count dropped by 17% to

994 deals in 2017 and most of that considerable drop

was at the seed stage. Seed stage deal activity fell by

27% with a much more obvious drop in the second half

of 2017. The average size of seed stage deals increased

by 60% however, suggesting the presence of outliers at

this early stage. Indeed Starship Technologies, a land-

based delivery robot startup, raised a $17.2 million seed

round – the largest agrifood tech seed stage deal on

record, according to AgFunder data going back to

2012.

2. Growth in agrifood tech funding was largest at Series D

stage where it increased 108% to reach $2.3 billion.

Among the largest Series D rounds in 2017 were

Chinese eGrocer MissFresh ($500m), US eGrocer

Instacart ($400m), Chinese eGrocer Yiguo ($300m), US

midstream company Ginkgo Bioworks ($275m), and US

ag biotechnology startup Indigo Agriculture ($203m).

All of these companies are part of a global trend for

venture-backed companies to stay independent longer,

holding out for larger valuations. This is made possible

by investors that seem to be maintaining an appetite for

these mature startups. For example, Indigo Agriculture

has already told AgFunderNews that the company will

likely remain privately held until it lists publicly.

3. The median deal size for Series D rounds grew 52% to

$35 million, which is mirrored in global VC markets and

suggests that investors have a healthy appetite for big

swings that have undergone some level of market

testing.

4. Funding at Series A stage increased by 46% totaling

$1.3 billion – the largest funding total for the stage in

any year on AgFunder record. Although the total was

partly driven by Chinese Agribusiness Marketplace

Maihuolang ($150m) and the unnamed ag

biotechnology joint venture between Bayer and Ginkgo

Bioworks ($100m), the median deal size at Series A

stage increased by 67% with the average deal size right

behind (up 60%) . This suggests that despite a few large

deals, the growth in this stage is authentic and not

dependent on outliers.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 43

Deal Volume and Activity by Stage

DEALS BY STAGE

# Deals

Financing | $Millions

Startups matured beyond Series D in nearly every

category within agrifood tech in 2017. Food ecommerce

outliers ele.me, Delivery Hero, Deliveroo, and Big Basket

together make up 71% of 2017 late-stage funding.

$335

$1,364

$1,775

$1,258

$2,330

$125

$2,923556

204

104

34 26 2050

Seed A B C D Debt Late

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 44

Upstream: Deal Volume and Activity by Stage

DEALS BY STAGE

# Deals

Financing | $Millions

$194

$921

$1,101

$492

$813

$109

$554

305

124

66

18 1312

32

Seed A B C D Debt Late

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 45

Downstream: Deal Volume and Activity by Stage

DEALS BY STAGE

# Deals

Financing | $Millions

$141

$423

$674$766

$1,517

$16

$2,369

251

7938

16 13

8

18

Seed A B C D Debt Late

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 46

Deal Average and Median by Stage

DEALS BY STAGE

Median | $Millions

Average | $Millions

• Large differences between the average and

median indicate the presence of very large

outliers. This divergence is most acute at Late

Stage (beyond Series D).

$1.3$7.8

$17

$33

$59

$25

$115

$0.5$4.3

$10

$23

$34

$4

$25

Seed A B C D Debt Late

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 47

$17.2

$7.5

$7.5

$6.7

$6.0

$5.7

$5.0

$5.0

$5.0

$5.0

$4.6

$4.5

$4.5

$4.1

$4.0

Starship Technologies

Bowery Farming Inc

Koia

Platterz

Basket

Farmwise

Grow Food

Cafe X Technologies

LifeFuels

Minibar Delivery

Utkal Tubers

Pure Harvest

Pure Harvest Smart Farms

Yumi

Milklane

Top 15 Seed Deals

DEALS BY STAGE

Financing | $Millions

Upstream Financing

Downstream Financing

Up+Down Financing

# Deals

• Seed stage funding contracted by 28% to

$335 million in 2017 from $464 million in

2016, while the number of deals

dropped by 27% to 556. This trend is

consistent with on overall drop in funding

at the seed stage across all sectors of

venture capital, according to

VenturePulse.

• Autonomous delivery startups raised

some of the largest seed stage deals

including Starship Technologies, Yumi,

and Platterz.

• Vegetable harvesting robot Farmwise

and automated café Café X Technologies

also raised large seed deals.

• New York-based indoor farm group

Bowery and animal diagnostics startup TL

Biolabs raised seed funding from high

profile general tech VCs such as GV

(Google Ventures) and Andreesen

Horowitz.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 48

$150.0

$100.0

$24.5

$24.0

$21.0

$20.5

$20.0

$20.0

$19.0

$18.4

$17.8

$17.0

$16.8

$16.7

$16.0

Maihuolang

Bayer–Gingko Partnership

Two Pore Guys, Inc.

Cannabco Pharmaceutical Corp

Hyliion

Perfect Day Foods

Bowery Farming Inc

Seasoned.co

Nuritas

Momentum Machines

Kolonial

Memphis Meats

Fenfenzhong

Astro Digital

Flirtey

Top 15 Series A Deals

DEALS BY STAGE

• Series A stage funding increased

by 48% in 2017 to $1.36 billion

from $919 million, while the deal

count only increased by 10% to.

• The Bayer-Ginkgo Bioworks

partnership is the first round of

funding for this yet-unnamed ag

biotech startup, which will be co-

located with Ginkgo in Boston.

• Two cellular agriculture startups

raised top Series A deals in 2017.

Perfect Day Foods is creating

animal-free dairy products and

Memphis Meats is working on

cultured meat. Both companies

are American.

• Animal diagnostics device startup

Two Pore Guys raised funding

from Khosla Ventures.

Financing | $Millions

Upstream Financing

Downstream Financing

Up+Down Financing

# Deals

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 49

$200.0

$108.5

$62.0

$50.4

$50.0

$50.0

$48.0

$43.0

$42.9

$42.0

$40.0

$35.0

$34.0

$33.7

$30.0

Plenty Inc.

Picnic

Convoy

Protix Biosystems

Brandless

Soylent

ZUME Pizza

Daily Harvest

Ritual

MycoTechnology

Shipt

BEFORE Brands

Swift Navigation

Frichti

Descartes Labs

Top 15 Series B Deals

DEALS BY STAGE

• Series B funding grew by 19% year-

over-year in 2017 growing to $1.8

billion from $1.5 billion, while the deal

count at this stage saw almost no

change. Almost all of this growth can

be attributed to indoor farming

company Plenty’s $200 million Series B

round led by SoftBank. Without this

record-breaking round, the stage

would have grown by just 5% in terms

of deal volume.

• Though the top Series B deals display

much of the diversity within agrifood

tech, consumer-facing startups such as

Brandless, Soylent, Daily Harvest and

Picnic are dominant.

• Grocery delivery startup Shipt raised its

$40 million Series B round in June 2017

and was acquired by retail giant Target

in December 2017.

Financing | $Millions

Upstream Financing

Downstream Financing

Up+Down Financing

# Deals

Deals by Geography

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 51

Key insights – by Geography

DEALS BY GEOGRAPHY

1. Agrifood startups raised funding in 59 countries globally.

The United States continues to dominate the overall deal

count with 42% of deal activity and 45% of deal volume.

This is unsurprising with a robust startup ecosystem and

an increasing amount of early stage support for

AgriFood entrepreneurs in the form of accelerators,

incubators, pitch competitions and more. However, the

US is not immune to global trends and the country’s deal

count decreased by 26% even despite a 34% jump in

deal volume.

2. Deal flow is increasing internationally as countries such as

Argentina, Brazil, Australia, and Ireland are gradually

building up their agrifood tech startup ecosystems with

early-stage support from incubators and accelerators.

Though this growth has not yet been met with a

significantly increased share of total agrifood financing,

deal activity in Brazil, Israel, Australia, Ireland, Sweden,

Singapore, Malaysia, Argentina, Turkey, South Korea,

Denmark, South Africa, Norway, and Egypt increased in

2017 despite the sector’s overall trend for the reverse.

4. Ireland doubled its deal count year-over-year, likely a

result of the country’s recent investment in the agrifood

tech sector through government and private actors.

5. Though China’s agrifood tech deals are consistently

breaking records in terms of their size, the country saw a

20% contraction in deal flow. Chinese deals have

historically centered around China’s growing internet

economy and consumer technologies, but 2017 saw a

diversification of deals. China’s 28 deals represented

Novel Farming Systems, In-store Retail & Restaurant

Tech, eGrocery, Innovative Food, Midstream

Technologies, Agribusiness Marketplaces, Restaurant

Marketplaces, Online Restaurants, and Robotics,

Mechanization & Farm Equipment.

6. Australia posted notable growth, with deal count

increasing 76% and dollars invested growing as well by

46% year-over-year. With 91% of its 32 deals at seed

stage, we expect Australia to continue to gain share of

the overall agrifood tech pie as these companies mature.

Half of these seed stage deals were in the Farm

Management Software, Sensing & IoT category

suggesting that Australia may play a larger role in farm

tech in coming years.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 52

Global Investment: Number of Deals per Country

DEALS BY GEOGRAPHY

4160

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 53

$1,000.0

$500.0

$421.3

$385.0

$300.0

$293.1

$230.0

$166.0

$150.0

$108.5

$100.0

$80.0

$73.6

$68.0

$52.5

$51.0

$50.4

$45.0

$45.0

$44.4

Ele.me

MissFresh e-commerce

Delivery Hero

Deliveroo

Yiguo.com

Bigbasket.com

MissFresh e-commerce

Lightspeed POS

Maihuolang

Picnic

MissFresh e-commerce

Swiggy

Aphria

Inagora

TerrAscend

Uhuru Energy

Protix Biosystems

Bigbasket.com

Vayyar

FreshMarket

Top 20 Non-U.S. Deals

DEALS BY GEOGRAPHY

Financing | $Millions

Upstream Financing

Downstream Financing

• China continues to exert dominance

over international deal volume, mostly

on the downstream side of the value

chain. Both the Series C and D rounds

for Chinese eGrocer MissFresh made

it into the top 20.

• As farm tech slowly matures outside

the US, we expect the share of top

deals to swing gradually away from

food commerce, but this is not yet the

case with 70% of the top 20

international deals from food

ecommerce startups.

• The largest agrifood tech deal for both

2016 and 2017 went to the same

Chinese company: food ecommerce

giant ele.me, which raised a $1 billion

late stage round in June 2017.

• Cannabis companies continue to

bring in some of the largest deals of

the year with Canada’s TerrAscend

and Aphria.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 54

Top 20 US Venture Deals

DEALS BY GEOGRAPHY

$400

$275

$203

$200

$118

$110

$101

$100

$77

$70

$70

$62

$55

$55

$53

$50

$50

$50

$48

$43

Instacart

Ginkgo Bioworks

Indigo

Plenty Inc.

Snap Kitchen

Farmers Business Network

Toast

Bayer–Gingko Partnership

Freshly

ProducePay

Spire

Convoy

Gather Technologies

Beyond Meat

3D Robotics

Soylent

Brandless

Orbital Insight Inc.

ZUME Pizza

Daily Harvest

Financing | $Millions

Upstream Financing

Downstream Financing

• The top five US deals are a clear

demonstration of the variety in agrifood

tech startups in the US, and how the sector

is maturing including eGrocery, Midstream

Tech, Ag Biotech, Novel Farming Systems,

and Online Restaurants.

• Other categories in the top 20 include

Agribusiness Marketplaces, Innovative

Food, In-store Retail & Restaurant Tech, and

Farm Management Software, Sensing, & IoT.

• Bayer and Ginkgo Bioworks’ joint venture

has yet to announce its name or any team

members. Ginkgo Bioworks’ own Series D

round was the largest Farm Tech deal of

2017, breaking Plenty’s record from earlier

in the year.

• Zume Pizza’s Series B round marked a

turning point for restaurant robotics. The

pizza delivery restaurant with a robotic chef

breathed life into this sleepy space with

investment from AME Cloud Ventures.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 55

U.S. Investment: Number of Deals by State

DEALS BY GEOGRAPHY

1580

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 56

$2,206

$817

$344

$133$120$118$79$70$69$68$55$55$51$40$40

CAMANYCOTXWANJPAILMOGAMNVAALNC

U.S. Investment: Value of Deals by State

DEALS BY GEOGRAPHY

• California continues to lead in agrifood tech deal

volume in the US, making up 48% of total US

financing and 38% of US deal flow. Forty-two

percent of California’s deals were on-farm

technologies.

• The runner up for the past several years, New York,

fell to third place in 2017 financings, with

Massachusetts taking the second slot in dollars

raised, though not in deal count. Large deals (four

over $100 million) pushed deal volume up for this

biotech hub.

• Florida ranks fifth in deal count and 16th in total

financing, suggesting that the state may jump up in

prominence in the US if these small deals lead to

larger rounds.

Investor Activity

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 58

Key insights – Investor Activity

INVESTOR ACTIVITY

1. The number of unique investors participating in

agrifood tech deals more than doubled year-over-year

in 2017 increasing to 1487 from 670 in 2016 -- a figure

that has steadily increased every year since AgFunder

records began, demonstrating the increasing interest in

the agrifood tech space. The group is diversifying and

looking more and more in line with more traditional tech

investing as generalist VCs catch on to the potential of

agrifood tech. Though not even close to the accelerator

boom of 2016 when sixteen new accelerators launched

across the globe, nine new accelerators launched in

2017 in Australia, the US, India, Brazil, Vietnam, and

Germany.

2. The most active agrifood tech investors in 2017 were

“accelerator VC” SOSV and Y Combinator with 41 and

24 deals respectively. SOSV’s participation varied,

covering Bioenergy & Biomaterials, Innovative Food,

Novel Farming Systems, Ag Biotechnology, Farm Mgmt

SW, Sensing & IoT, and In- Store Retail & Restaurant

Tech.

3. Silicon Valley VCs GV (Google Ventures), Sequoia

Capital, Khosla Ventures and Andreesen Horowitz

among others showed an increased interest in agrifood

tech investments in 2017. GV alone participated in nine

deals.

4. In 2017 we saw an uptick in participation from notable

sovereign wealth funds and mega-funds from outside

the US. Singapore’s Temasek made further agrifood

investments in 2017 along with the Investment

Corporation of Dubai, Meraas, the investment vehicle of

Sheikh Mohammed bin Rashid, of Dubai, Softbank’s

Vision Fund, and Japanese trading house Mitsui & co.

Private equity groups like ADM Capital, global asset

management firms like Alliance Bernstein, and even a

pension fund in the Municipal Employee Retirement

System of Michigan are also getting involved.

5. Agrifood strategics stepped up the pace a bit as

Syngenta Ventures (5), Monsanto Growth Ventures (4),

Maumee Ventures (3) BASF Venture Capital (3), Taylor

Farms Ventures (2), Wilbur-Ellis’s Cavallo Ventures (2),

Cargill (1), and Tate & Lyle Ventures (1) all made

investments.

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 59

1,214

18036 29 8 5

2 8 1 2 1 1 1x1 x2 x3 x4 x5 x6 x7 x8 x9 x10 x11 x24 x41

Number of Deals by Investors & Accelerators

INVESTOR ACTIVITYN

UM

BE

R O

F I

NV

ES

TO

RS

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 60

Most Active Venture Funds

INVESTOR ACTIVITY

RANK INVESTOR LOCATION # INVESTMENTS

1 SOSV Princeton, NJ 41

2 Y Combinator Mountain View, CA 24

3 SVG Partners Los Gatos, CA 10

4 GV (Google Ventures) Mountain View, CA 9

5 Bessemer Venture Partners Menlo Park, CA 8

5 GGV Capital Menlo Park, CA 8

5 500 Startups Mountain View, CA 8

5 SP Ventures Sao Paulo, Brazil 8

5 Khosla Ventures Menlo Park, CA 8

5 Accel Partners Palo Alto, CA 8

5 SproutX Melbourne, Australia 8

5 NXTP Labs Buenos Aires, Argentina 8

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 61

Agtech Funds 2006 - Present

INVESTOR ACTIVITY

(Year Fund Announced Final Close)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Cultivian Fund I ($34M)

Anterra Capital Fund I

( $125M)

Avrio Ventures Fund III

($110M)

New Crop Capital ($25M)

Cultivian Sandbox Fund II ($115M)

Closed Loop Capital (Evergreen)

Omnivore Partners Fund I ($40M)

Avrio Ventures LP II ($92M)

Greensoil Agro & Food I ($12M)

CapAgro Innovation Fund

( $147M)

Seed to Growth

Ventures

($125M)Middleland Capital (family office backed)

Fall Line Farms Fund I ( $127M)

Greensoil Agro & Food II

($19M)

Lewis & Clark Ventures ($20M)

PowerPlant Ventures ($42M)

Finistere Fund I ($32M)

Avrio Ventures LP I ($75M)

2 1 2 5 3

Pontifax Agtech Fund I

( $105M)

ADM Capital Cibus Fund

( $105M)

1 4 1 1

Finistere Ventures

Ireland Agtech Fund

( $24M)

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 62

New Agtech Accelerators’& Resources

INVESTOR ACTIVITY

Jan Feb March April May June July Aug Sept Oct Nov Dec

IMPACT Growth(remote)

SparkLabs Cultiv8

( Australia)

Pulse(Brazil)

Agro Innovation Lab(Germany)

GSF Accelerator

(India)

Land O’Lakes Dairy Accelerator

( Minnesota, US)AgSprint Accelerator(New Mexico, US)

IowaAgriTech

Accelerator

(Iowa, US)

11 1

Mekong Agriculture

Technology Challenge

Startup Accelerator

( Vietnam)

1 2 21

M & A

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 64

Mergers & Acquisitions (1 of 3)AGTECH EXITS

Target Target Country Acquirer Targets Category

Bioline Ltd UK InVivo Group Ag Biotechnology

BUG Agentes Biológicos Brazil Koppert Ag Biotechnology

Ceres USA Land O' Lakes Ag Biotechnology

Ekompany Netherlands Kingenta Ag Biotechnology

EnviroFlight USA Interexon Ag Biotechnology

Gen9 USA Ginkgo Bioworks Ag Biotechnology

Edeniq USA Aemetis Bioenergy & Biomaterials

BIOMAR Microbial Technologies Spain 4d pharma Bioenergy & Biomaterials

Extrakt Chemie Germany Frutarom Bioenergy & Biomaterials

Segetis United States GFBiochemicals Bioenergy & Biomaterials

Granular USA DowDupont Farm Mgmt Software, Sensing & IoT

Agam Advanced Agronomy Israel Rivulis Irrigation Farm Mgmt Software, Sensing & IoT

Precision Planting USA AGCO Farm Mgmt Software, Sensing & IoT

Focus Technology Group USA AGDATA Farm Mgmt Software, Sensing & IoT

proPlant Germany Bayer Farm Mgmt Software, Sensing & IoT

Silent Herdsman UK Afimilk Farm Mgmt Software, Sensing & IoT

Oso Technologies USA Scott's Miracle Grow Farm Mgmt Software, Sensing & IoT

Blossom USA Scott's Miracle Grow Farm Mgmt Software, Sensing & IoT

SupraSensor USA The Climate Corp Farm Mgmt Software, Sensing & IoT

VitalFields Estonia The Climate Corp Farm Mgmt Software, Sensing & IoT

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 65

Mergers & Acquisitions (2 of 3)AGTECH EXITS

Target Target Country Acquirer Targets Category

AXIO-NET Germany Trimble Farm Mgmt Software, Sensing & IoT

Farmeron USA Virtus Nutrition Farm Mgmt Software, Sensing & IoT

GrowCameras.com USA GreenGro Technologies Farm Mgmt Software, Sensing & IoT

AgSolver USA EFC Systems Farm Mgmt Software, Sensing & IoT

Adapt-N USA Yara Farm Mgmt Software, Sensing & IoT

Abe's Market USA Direct Eats Food Marketplace/E-commerce

EatOnGo India InnerChef Food Marketplace/E-commerce

Flavor Labs India InnerChef Food Marketplace/E-commerce

Place of Origin India Craftsvilla Food Marketplace/E-commerce

TinyOwl India Roadrunnr Food Marketplace/E-commerce

CookNook USA Homemade Food Marketplace/E-commerce

SpoonRocket USA iFood Food Marketplace/E-commerce

FarmBox USA GrubMarket Food Marketplace/E-commerce

Urban Acres USA Greenling Food Marketplace/E-commerce

Foodinho Italy Glovo Food Marketplace/E-commerce

The Fresh Diet USA New Fresh Food Marketplace/E-commerce

Eat24 USA GrubHub Food Marketplace/E-commerce

Baidu Delivery China ele.me Food Marketplace/E-commerce

Runnr India Zomato Food Marketplace/E-commerce

Anova USA Electrolux Home & Cooking

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 66

Mergers & Acquisitions (3 of 3)AGTECH EXITS

Target Target Country Acquirer Targets Category

Innophos Holdings Inc USA Novel Ingredients Innovative Food

Daiya Foods Canada Otsuka Innovative Food

Canada Blockchain Hosting Corp USA Calyx Bioventures Midstream Technologies

Ozone International USA Wheatsheaf Group Midstream Technologies

Parcel USA Walmart Midstream Technologies

Food Genius USA US Foods Midstream Technologies

Undisclosed USA CropLogic Miscellaneous

Pantry USA Byte Miscellaneous

Calagri USA Pacific Ag Miscellaneous

Botanicare USA Scott's Miracle Grow Novel Farm Systems

Gavita Holland Netherlands Scott's Miracle Grow Novel Farm Systems

AeroGrow USA Scott's Miracle Grow Novel Farm Systems

Backyard Farms USA Mastronardi Novel Farm Systems

Fair Insects USA Protix Biosystems Novel Farm Systems

Radish USA Tovala Online Restaurants & Mealkits

Skyward USA Verizon Robotics & Other Farm Eq

Netafim Israel Mexichem Robotics & Other Farm Eq

AerWay Canada Salford Group Robotics & Other Farm Eq

Blue River Technologies USA John Deere Robotics & Other Farm Eq

Hagie Manufacturing USA John Deere Robotics & Other Farm Eq

Keenan Ireland Alltech Robotics & Other Farm Eq

AGRIFOOD TECH FUNDING REPORT: YEAR REVIEW 2017 | AGFUNDER.COM 67

Are We Missing Your Data?Don’t forget to send it to us!