agenda - uio.no · agenda • background • model for purchase probability (often reffered to as...

TRANSCRIPT

Agenda

• Background

• Model for purchase probability (often

reffered to as conversion rate)

• Model for renewwal probability

• What is the link between price change,

product mix and churn??

Bakgrunn

• Assume you have developed a new tariff model, using chapter 8,9 and 10 from the book

• Should you implement it «as is»?

• Compare new tariff with the gross tariff that exists today (gross tairff is the tariff used today adjusted for discounts and moderations) and analyze differences

• Evaluate consequences of the tariff used today and reconcile with the differences above:

– How is the conversion rate today?

– How is the renewal rate today?

Logistic regression – the probability that

something is occuring Those with property,

For example insurance

Those without property,

i.e., insurance Client

age

Product

mix

Geo-

graphy

Client

age

Product-

mix

Ge-

ography

• Those having insurance are compared with those that do not have insurance

• If an explanatory variable is statistically significant it will be included in the model that

predicts the probability that a client has an insurance product

• Name this probability p

• Then the modelled link between p and the explanatory variables is:

• This model can be used to score all customers since every customer is assigned a

modelled p

• The idea is to prioritize those with high modelled p that do not possess the insurance

product

nnxxp

p

...

1log 11

Variable 1 can for example be client age Estimated effect of variable 1

Purchase probability (conversion

rate) villa insurance • Model: Purchase probaility for villa insurance using logistic regression

• Database 1 (insurance data) : – Bank clients without insurance products

– Insurance information is used

• Database 2 (bank data): – Bank clients without insurance products

– Bank information is used

• Period: (1.5.2012-30.4.2014)

• Approximately 70 000 bank clients were offered villa insurance

• Approximately 31% accepted

• Model 1 is typically used for consequence analysis in connection with tariff development/assessment

• Model 2 is typically used by the sales department

• It is conceivable that a model 3 using both information sources could be developed. This was attempted but it did not outperform model 2.

• Model 1 and model 2 do both have 6 explanatory variables

Different events require separate

treatment

Sales to new customers • Which factors drive the sales?

• What objects are easily sold?

• Which bank customers

purchase villa insurance?

Event

Renewal • What factors drive the renewal

rate?

• How important is price change

for the renewal rate?

• Is the churn wanted or not?

Cross sales to existing

customers • What factors drive cross sales?

Logistic regression • Offer data

• Bank data and insurance data

• Respons: has purchased villa

insurance (yes/no)

Method and data

Logistic regression • Insurance data

• Respons: has renewed the

policy (yes/no)

Same as sales to new

customers

• Is the company attractive for

strategically important

customers?

• Should the price be adjusted

for specific groups?

Follow up questions

• How does renewal vary with

customer scoring?

• How does price sensitivity vary

with customer scoring?

• Does the cross sales increase

expected customer lifetime?

Purchase probability (conversion

rate) villa insurance

• About the data

• Validation of model

• Explanatory variables in model

• Ranking of explanatory variables

• Interpretation of odds ratio for explanatory

variables

Purchase probability villa insurance

• Model: purchase probability for villa insurance using logistic regression

• Database 1 (insurance data) : – Bank customers without property insurance products

– Insurance data is used

• Database 2 (bankdata): – Bank customers without property insurance products

– Bankdata is used

• Period: (1.5.2012-30.4.2014)

• Approximately 70 000 such customers were offered villa insurance

• Approximately 31% accepted

• Model 1 is typically used for consequence analysis in tariff development

• Model 2 is typically used for sales purposes

• A model 3 combining data from model 1 and 2 is conceivable. This was attempted but it did not outperform model 2 and was therefore discarded.

• Model 1 and model 2 do both have 6 explanatory variables

Validation of model 1(insurance

data)

• The model was calibrated on 90% of the data (ca 63 000)

• The model was validated on the remaining 10% (ca 7 000)

Modelled accept rate per decile

Actual accept rate

Mean actual accept

rate

Explanatory variables model

1(insurancedata)

• Customer age

• Building age

• Building standard

• Use of the building

• Building size in square meters (proxy for

insurable sum)

• Building type

Results model 1 insurancedata

• Wald is defined as (Estimate/sd(estimate))^2

• Wald can be used to rank the importance of the

explanatory variables

• Assume for example, as above, that all explanatory

variables are statistically significant

• The variables customer age and building size have the

highest Wald score

• In other words, The Wald criterion is ranking customer

age and building size as the most important explanatory

variables

Explanatory

variable Wald Significance

Customer age 610 <0.0001

Building size 160 <0.0001

Normal standard 121 <0.0001

Building age 79 <0.0001

Villa (yes/no) 54 <0.0001

Inhabitated by

owner (yes/no) 6 0.0137

Definition of odds ratio

• The odds ratio is the ratio of the odds of an event occuring in one group to the odds of it occuring in another group

• If the probabilities of the event in each of the grous are p1 (first group) and p2 (second group), then the odds ratio is:

• Where qx=1-px.

• An odds ratio of 1 indicates that the event is equally likely to occur in both groups

• An odds ratio greater than 1 indicates that the event is more likely to occur in the first group

• An odds ratio less than 1 indicates that the event is less likely to occur in the first group

12

21

22

11

22

11

/

/

)1/(

)1/(

qp

qp

qp

qp

pp

pp

Results model 1 insurance data

The accept rate for

young customers is

higher than the

accept rate for old

customers

The accept rate for semi-

old is lower than the

accept rate for old

old >= 70 young <30 % change

accept rate 20 % 32 % 60 %

25 % 39 % 56 %

31 % 45 % 45 %

35 % 51 % 44 %

odds ratio 1.9

Purchase probability villa insurance

model 2

• Validation of model

• Explanatory variables model

• Ranking of explanatory variables

• Interpretation of odds ratio for explanatory

variables

Validation of model 2 (bankdata)

• The model was calibrated on 90% of the data (ca 56 000)

• The model was validated on the remaining 10% (ca 6 000)

Modellert tilslag per decil

Actual accept rate

Average actual

accept rate

Explanatory variables model 2

(bankdata)

• Number of products

• Has / has not house loan

• Has / has not a savings account and if yes

what kind

• Has / has not active savings insurance

• Has / has not stake in mutual fund

• Occupational affinity(Academic, Nurse etc)

Results model 2 Bankdata

• Wald is defined as (Estimate/sd(estimate))^2

• Wald can be used to rank the importance of the explanatory

variables

• Wald can also be used to compare models

• Comparing the Wald levels of model 1 and model 2 it is noted

that model 2 seems to have detected much stronger drivers for

accept rate than model 1

• Wald in model 2 is much larger than Wald in model 1

• This was also indicated in the validation of model 2 where

the range in accept rate between high and low deciles was

considerably larger

• Range in accept rate model 1: 22%-45%

• Range in accept rate model 2: 9%-72%

Wald Significance

Number of

products 6374 <0.0001

Mutual fund 1843 <0.0001

Has house loan 1732 <0.0001

Savings account 805 <0.0001

Occupational

affinity 713 <0.0001

Active savings

insurance 630 <0.0001

Resultats model 1 Bankdata

Renewal rate villa insurance

• About the methodology

• About the data

• About the development of the portfolio

• Validation of model

• About the selection of time window

• Price sensitivity villa insurance

• Explanatory variables model

• Ranking of explanatory variables

• Interpretation of odds ratio for explanatory variables

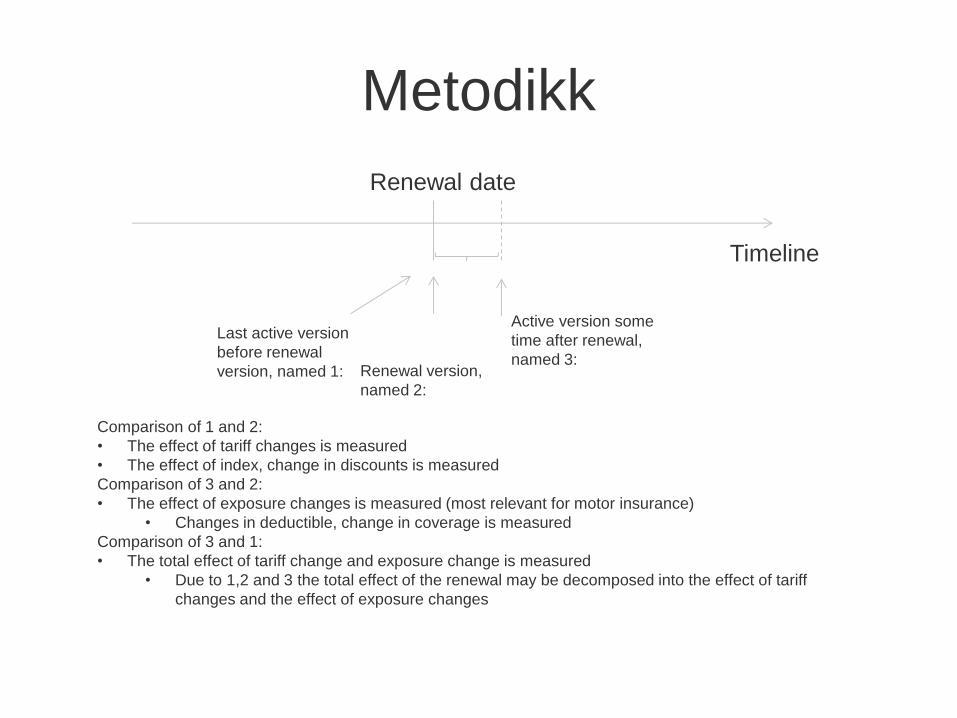

Metodikk

Renewal date

Last active version

before renewal

version, named 1: Renewal version,

named 2:

Active version some

time after renewal,

named 3:

Comparison of 1 and 2:

• The effect of tariff changes is measured

• The effect of index, change in discounts is measured

Comparison of 3 and 2:

• The effect of exposure changes is measured (most relevant for motor insurance)

• Changes in deductible, change in coverage is measured

Comparison of 3 and 1:

• The total effect of tariff change and exposure change is measured

• Due to 1,2 and 3 the total effect of the renewal may be decomposed into the effect of tariff

changes and the effect of exposure changes

Timeline

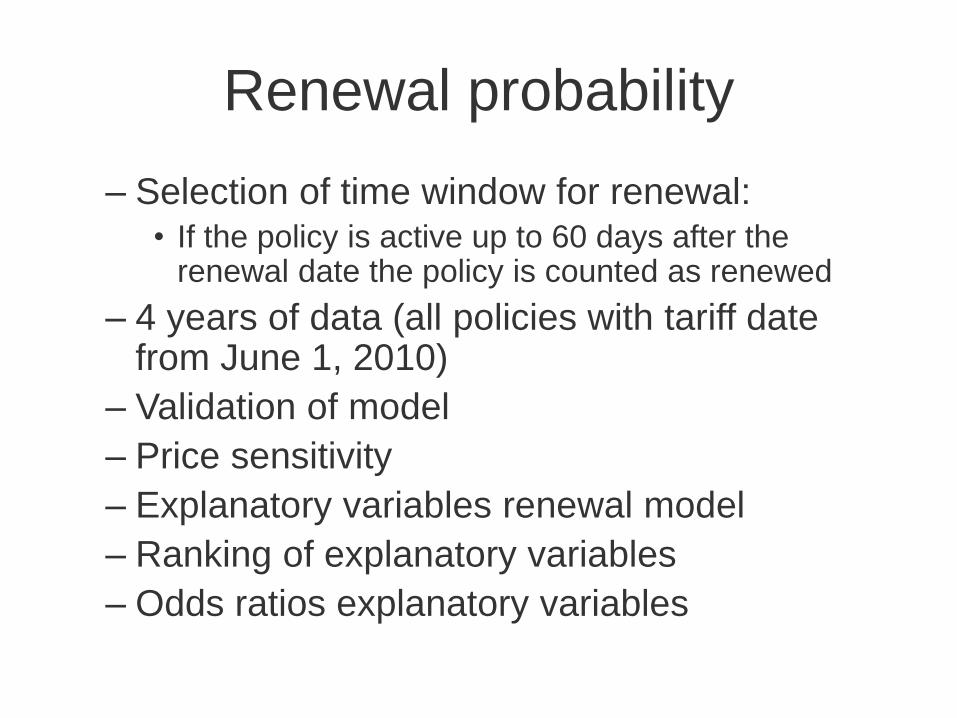

Renewal probability

– Selection of time window for renewal: • If the policy is active up to 60 days after the

renewal date the policy is counted as renewed

– 4 years of data (all policies with tariff date from June 1, 2010)

– Validation of model

– Price sensitivity

– Explanatory variables renewal model

– Ranking of explanatory variables

– Odds ratios explanatory variables

Fornyelsessannlighet villaforsikring

• Modell: Renewal probability for villa

insurance using logistic regression

• Data:

– Villas in the portfolio, active or historic, with

tariff date > May 31, 2010

– Villas with good history (ca 71 000)

Validering av fornyelsesmodell

• Model calibrated on 90% of the data (appr 64 000)

• Model validated on the remaining 10% (ca 7 000)

Persentile in renewal model

Actual renewal rate Average actual

renewal rate

Renewal rate

Selection of time window

• The graph shows the total share not renewed in time after the renewal date for the 4 years period

• The graph shows that the share not renewed is highest in the renewal month and the month after

• The total share not renewed is 32% accumulated for the entire 4 years period

Tid i måneder etter fornyelse

Total share not renewed per month after

renewal

Not renewed

Accumulated not renewed

Price sensitivity villa

• The graph shows renewal rate for different price changes for active and historic villa policies for the

entire 4 years period

• The renewal rate is hardly changed when the price change is between -4% and 2% - reducing the

premium does not reduce the churn in this case

• When the price change is between 2% and 14% the renewal rate is reduced with 0.5% per percent price

increase

• When the price change is above 14% the renewal rate is reduced with 1% per percent price increase

Persentil i fordeling av prisendring i fornyelsen

Average renewal based on 4 years of data using 60 days

window

Estimated renewal rate based on the 4 year period

Results renewal model

• The customer age and price change in renewal are the

most important variables

• Whether the customer has had a claim or not is not so

important compared to the other variables

Explanatory

variable Wald Significance

Customer age 264 <0.0001

Price change in

renewal 230 <0.0001

Building size 108 <0.0001

Has had claim 8 <0.0001

Results model 1

• The renewal is increasing with increasing age

• The renewal is increasing with increasing building size

• The renewal is lowest for those with at least 5% price reduction (who are these?)

• The renewal is highest for those with price increase between 2% and 12%

• The renewal is higher for those that did not have claims (improvement potential in claims

settlement department?)

Do main products like car and villa increase

expected customer lifetime?

How price sensitive is the customer?

tid 1/5-2010 1/5-2011 1/5-2012 1/5-2013 1/5-2014

villa car

Only villa Only car Both villa and car

How many are in

the portfolio here

?

How many are

remaining? And

here?

And

here?

And

here?

Price increase villa

Price increase car Large Very large

Significant Moderate

Significant

Moderate

Negativ

Moderate

The churn is declining with time

and depending on product mix

• The churn is highest for those with villa and not car

• The churn is lowest for customers with villa and car

• The churn is highest the first year after the starting point and declining afterwards

• Are these results robust?

Villa not car

Car not villa

Both villa and car

Yearly churn for different product mix C

hu

rn

Hypothesis: the churn is highest

the first year

• Observe those who are in the portfolio one year later, i.e., 1/5-2011. How many are still in

the portfolio after 1,2 og 3 years?

• The churn is highest for those with villa and no car

• The churn is lowest for customers with villa and car

• The churn is highest the first year and declining aftwerwards

Villa not car

Car not villa

Both villa and car

Yearly churn for different product mix

Chu

rn

Resultats from 3 starting points

avgang villa ikke bil bil ikke villa kunder med villa og bil

1/5-10 - 1/5-11 30,0 % 26,0 % 15,7 %

1/5-11 - 1/5-12 17,0 % 15,0 % 14,2 %

1/5-12 - 1/5-13 11,1 % 10,6 % 10,7 %

1/5-13 - 1/5-14 7,7 % 7,9 % 7,4 %

avgang villa ikke bil bil ikke villa kunder med villa og bil

1/5-11 - 1/5-12 30,7 % 24,3 % 19,8 %

1/5-12 - 1/5-13 16,4 % 15,5 % 14,3 %

1/5-13 - 1/5-14 11,4 % 11,4 % 9,9 %

avgang villa ikke bil bil ikke villa kunder med villa og bil

1/5-12 - 1/5-13 23,1 % 18,7 % 17,0 %

1/5-13 - 1/5-14 17,7 % 17,2 % 13,6 %

Starting point: 1/5 2010

Starting point: 1/5 2011

Starting point: 1/5 2012

Churn villa not car car not villa both villa and car

Churn villa not car car not villa both villa and car

Churn villa not car car not villa both villa and car

Summary churn, product mix and

price change • In periods with severe price increases the churn is higher

• This result is reconcilable with the results from the renewal rate model. This indicates a quite strong link between churn and price change.

• Those with villa and no car have the highest churn, those with car and no villa have medium churn and those with villa and car have the lowest churn.

• Independent of product mix the churn measured in time after starting point seems to be declining. (the churn 1 year after the starting point is highest, 2 years after a little lower etc)

• The difference in churn between the product mix groups is falling as a function of time after the starting point

• The results indicate that customers with both villa and car are less price sensitive than customers with only one main product