africa – an opportunity for pharma and patients

TRANSCRIPT

Africa – an opportunity for Pharma and Patients

UNIDO2018

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

McKinsey & Company | 1

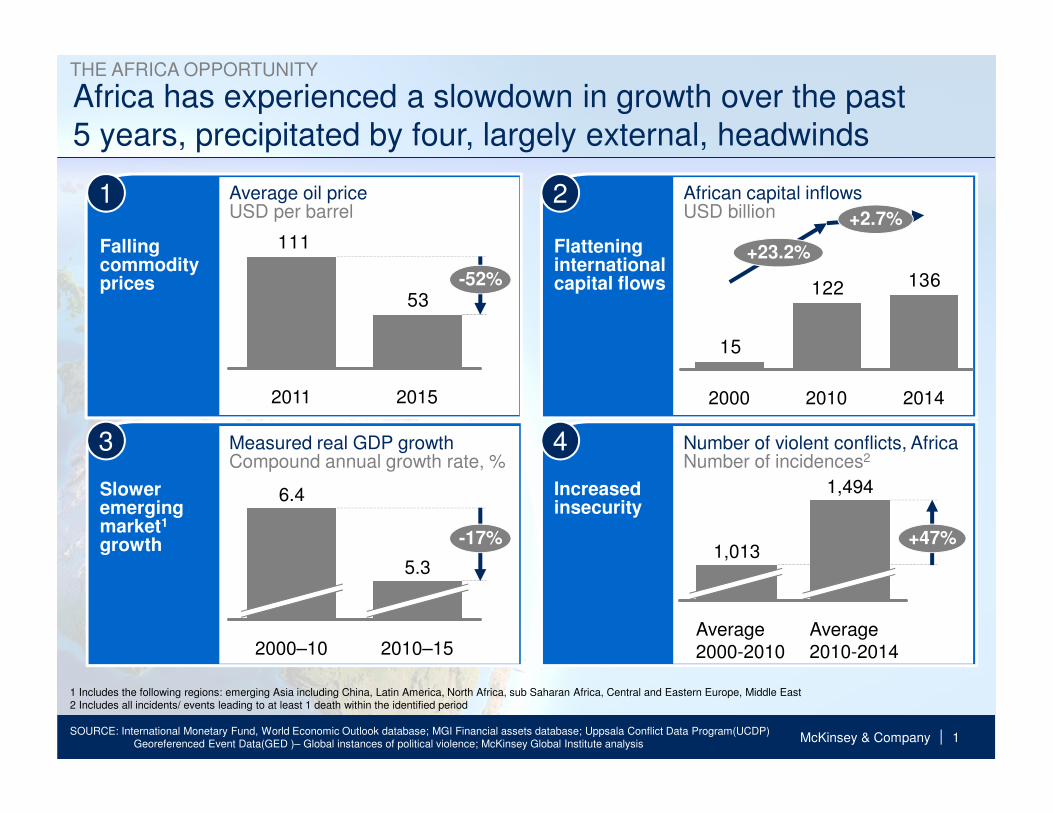

Africa has experienced a slowdown in growth over the past 5 years, precipitated by four, largely external, headwinds

SOURCE: International Monetary Fund, World Economic Outlook database; MGI Financial assets database; Uppsala Conflict Data Program(UCDP) Georeferenced Event Data(GED )– Global instances of political violence; McKinsey Global Institute analysis

1 2

3 4

Falling commodity prices

Slower emerging market1

growth

Flatteninginternationalcapital flows

Increasedinsecurity

53

111

-52%

2011 2015

Average oil priceUSD per barrel

136122

15

+2.7%

2000

+23.2%

20142010

African capital inflowsUSD billion

-17%

2000–10

5.3

2010–15

6.4

1,013

1,494

Average2000-2010

+47%

Average2010-2014

Measured real GDP growthCompound annual growth rate, %

Number of violent conflicts, AfricaNumber of incidences2

1 Includes the following regions: emerging Asia including China, Latin America, North Africa, sub Saharan Africa, Central and Eastern Europe, Middle East2 Includes all incidents/ events leading to at least 1 death within the identified period

THE AFRICA OPPORTUNITY

McKinsey & Company | 2

We believe Africa’s long-term growth prospects are still positive

SOURCE: Findex World Bank 2014; Euromonitor; press search; McKinsey Global Institute analysis

▪ Working age population to be world’s largest by 2034 at 1.1bn

▪ Stable jobs now growing faster than the labourforce

▪ Africa is urbanizing faster than any other region: Another ~190 million moving to urban regions by 2025

▪ Urban areas have 2.5x higher productivity than rural areas

▪ Africa has a significant share of global resource reserves e.g. 10% of global oil exports

▪ These reserves can competitively meet continued global demand for these resources

Technology creating opportunities to leapfrog in key sectors e.g.,

▪ Financial services

▪ Education

▪ Healthcare

▪ Retail/Wholesale

Technology

A B

C D

Growing workforce Rapid urbanisation

Natural resource endowments

THE AFRICA OPPORTUNITY

McKinsey & Company | 3

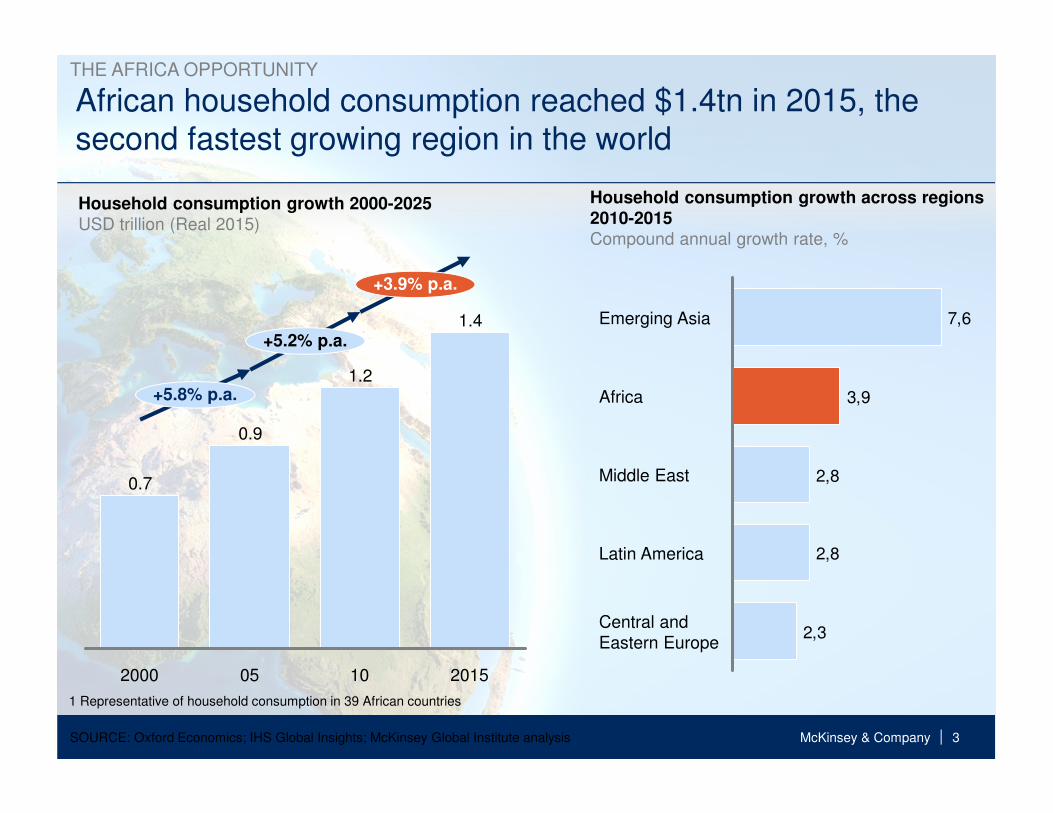

African household consumption reached $1.4tn in 2015, the second fastest growing region in the world

SOURCE: Oxford Economics; IHS Global Insights; McKinsey Global Institute analysis

+5.8% p.a.

+3.9% p.a.

+5.2% p.a.

0.9

1.4

1.2

1005 20152000

0.7

1 Representative of household consumption in 39 African countries

2,3

2,8

2,8

3,9

7,6

Central andEastern Europe

Middle East

Emerging Asia

Latin America

Africa

Household consumption growth across regions 2010-2015Compound annual growth rate, %

Household consumption growth 2000-2025USD trillion (Real 2015)

THE AFRICA OPPORTUNITY

McKinsey & Company | 4

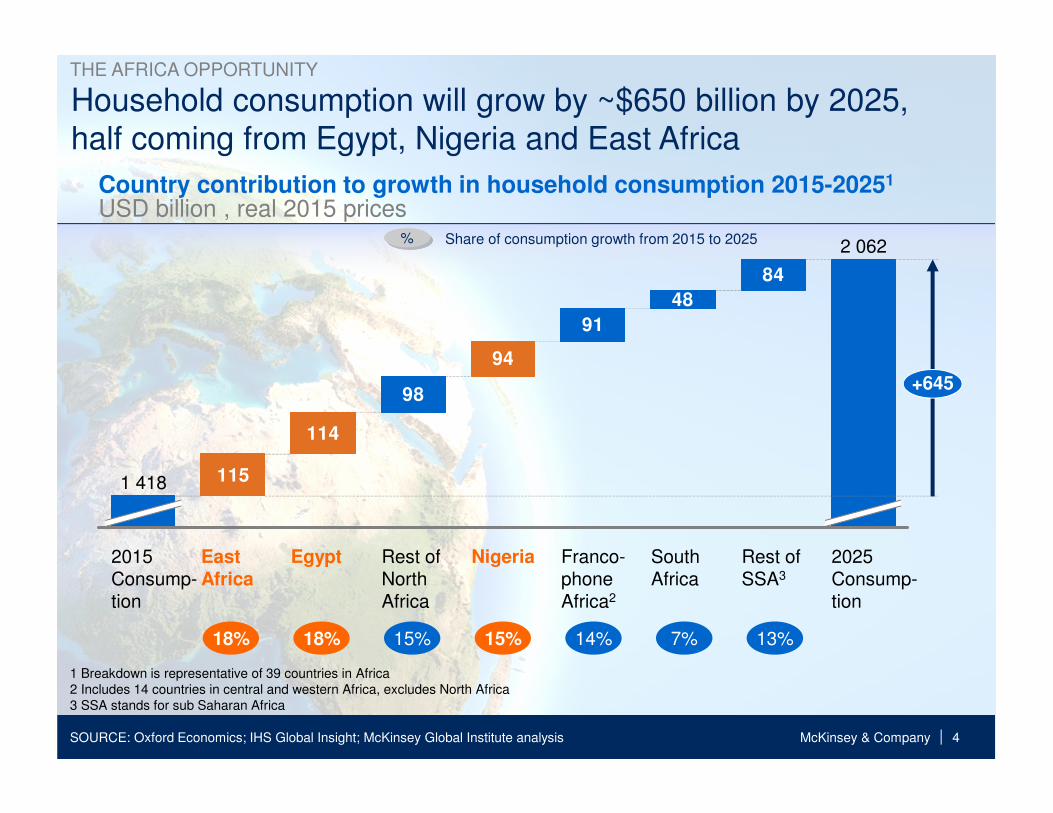

Country contribution to growth in household consumption 2015-20251

USD billion , real 2015 prices

Household consumption will grow by ~$650 billion by 2025, half coming from Egypt, Nigeria and East Africa

SOURCE: Oxford Economics; IHS Global Insight; McKinsey Global Institute analysis

115

98

94

91

48

84

114

+645

NigeriaRest of North Africa

2 062

Rest of SSA3

South Africa

Franco-phone Africa2

2025 Consump-tion

2015 Consump-tion

1 418

East Africa

Egypt

15%18%18% 15% 14% 7% 13%

1 Breakdown is representative of 39 countries in Africa2 Includes 14 countries in central and western Africa, excludes North Africa3 SSA stands for sub Saharan Africa

Share of consumption growth from 2015 to 2025%

THE AFRICA OPPORTUNITY

McKinsey & Company | 5

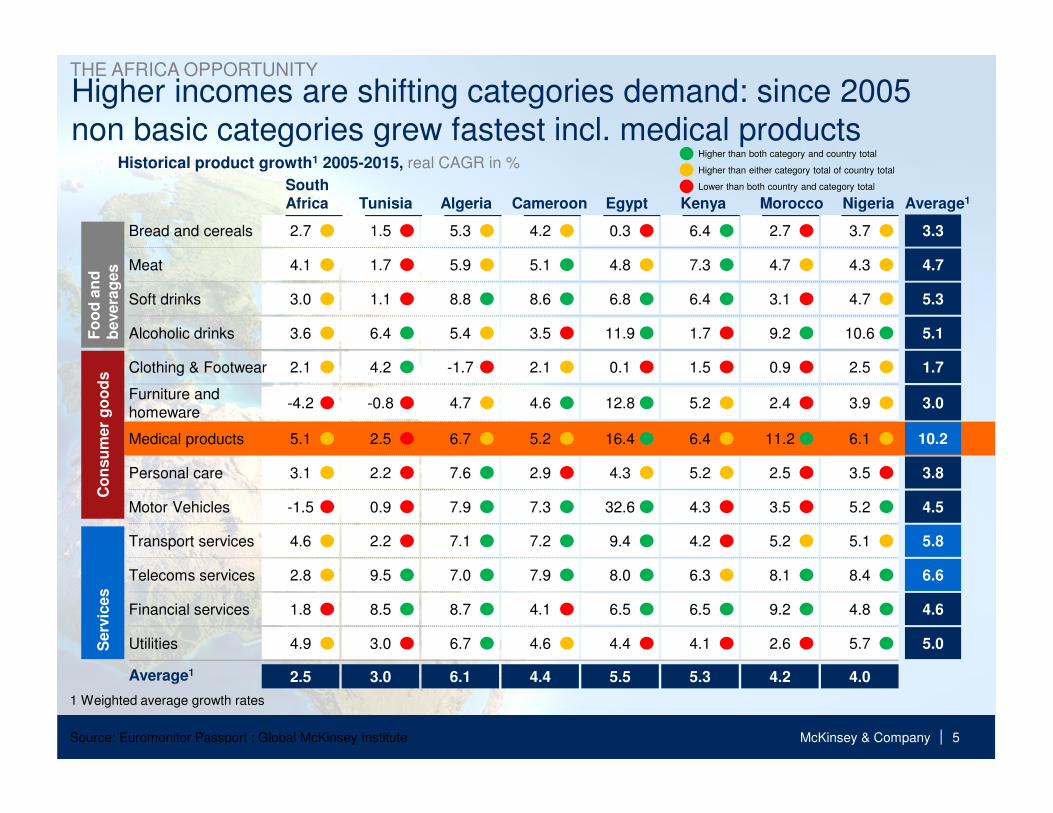

Higher incomes are shifting categories demand: since 2005 non basic categories grew fastest incl. medical products

Source: Euromonitor Passport ; Global McKinsey Institute

Historical product growth1 2005-2015, real CAGR in %

South Africa Tunisia Algeria Cameroon Egypt Kenya Morocco Average1

2.5 3.0 6.1 4.4 5.5 5.3 4.2 4.0

Nigeria

1.5 5.3 4.2 0.3 6.4 2.7 3.7 3.32.7Bread and cereals

1.7 5.9 5.1 4.8 7.3 4.7 4.3 4.74.1Meat

1.1 8.8 8.6 6.8 6.4 3.1 4.7 5.33.0Soft drinks

6.4 5.4 3.5 11.9 1.7 9.2 10.6 5.13.6Alcoholic drinks

4.2 -1.7 2.1 0.1 1.5 0.9 2.5 1.72.1Clothing & Footwear

-0.8 4.7 4.6 12.8 5.2 2.4 3.9 3.0-4.2Furniture and homeware

2.2 7.6 2.9 4.3 5.2 2.5 3.5 3.83.1Personal care

0.9 7.9 7.3 32.6 4.3 3.5 5.2 4.5-1.5Motor Vehicles

2.2 7.1 7.2 9.4 4.2 5.2 5.1 5.84.6Transport services

9.5 7.0 7.9 8.0 6.3 8.1 8.4 6.62.8Telecoms services

8.5 8.7 4.1 6.5 6.5 9.2 4.8 4.61.8Financial services

5.03.0 6.7 4.6 4.4 4.1 2.6 5.74.9Utilities

Average1

Fo

od

an

d

bevera

ges

Co

nsu

mer

go

od

s

1 Weighted average growth rates

Higher than either category total of country total

Higher than both category and country total

Lower than both country and category total

Serv

ices

2.5 6.7 5.2 16.4 6.4 11.2 6.1 10.25.1Medical products

THE AFRICA OPPORTUNITY

McKinsey & Company | 6

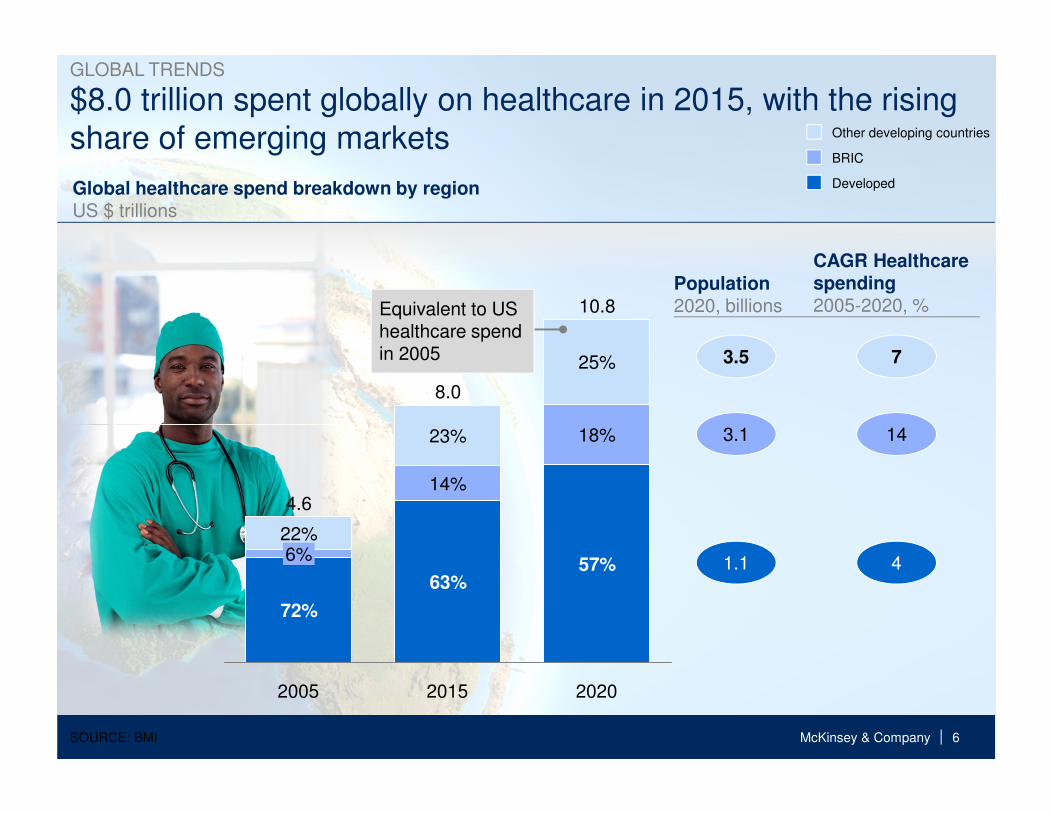

$8.0 trillion spent globally on healthcare in 2015, with the rising share of emerging markets

6%22%

10.8

18%

57%

25%

20202015

8.0

63%

14%

23%

2005

4.6

72%

Global healthcare spend breakdown by regionUS $ trillions

3.5

3.1

1.1

Other developing countries

Developed

BRIC

7

14

4

Population2020, billions

CAGR Healthcare spending2005-2020, %

SOURCE: BMI

GLOBAL TRENDS

Equivalent to US healthcare spend in 2005

McKinsey & Company | 7

+9% CAGR

The pharmaceutical and medical products market experienced strong growth in recent years

SOURCE: BMI; World Bank; McKinsey analysis

1 OTC, Patented, Generics split extrapolated from data available for 60% of pharmaceutical sales

29.4

20142010

20.6

African pharmaceutical and medical products marketUSD billions1

AFRICA OPPORTUNITY

McKinsey & Company | 8

2020Realistic

14.5

3.0

58.7

2020Optimistic

45.1

7.1

52.2

66.5

7.8

2020Base

37.6

2010

6.5

17.5

44.2

Fast growth expected for Africa in the next years

SOURCE: WHO; World Bank; IMF; African Development Bank; BMI; McKinsey Africa Pharma 2020 Model

17.4 35.4 41.8 53.3

Africa salesper capita

USD

Africa pharmaceutical market forecastUSD billions

14%

12%

9%

Top 151

1 South Africa, Egypt, Algeria, Nigeria, Morocco, Angola, Tunisia, Libya, Ethiopia, Sudan, Ghana, Kenya, Cameroon, Tanzania, Uganda

AFRICA OPPORTUNITY

McKinsey & Company | 9

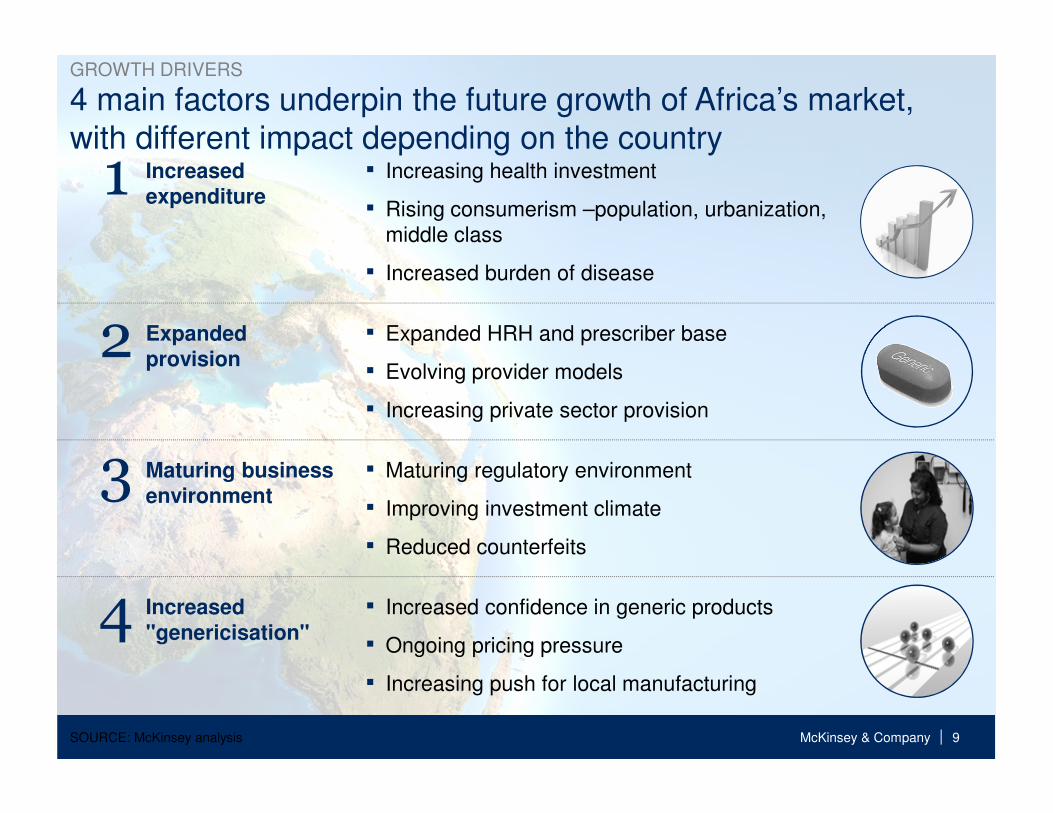

4 main factors underpin the future growth of Africa’s market, with different impact depending on the country

SOURCE: McKinsey analysis

Increased "genericisation"

2

3

4

1

GROWTH DRIVERS

Increased expenditure

▪ Increasing health investment

▪ Rising consumerism –population, urbanization, middle class

▪ Increased burden of disease

Expanded provision

▪ Expanded HRH and prescriber base

▪ Evolving provider models

▪ Increasing private sector provision

Maturing business environment

▪ Maturing regulatory environment

▪ Improving investment climate

▪ Reduced counterfeits

▪ Increased confidence in generic products

▪ Ongoing pricing pressure

▪ Increasing push for local manufacturing

McKinsey & Company | 10

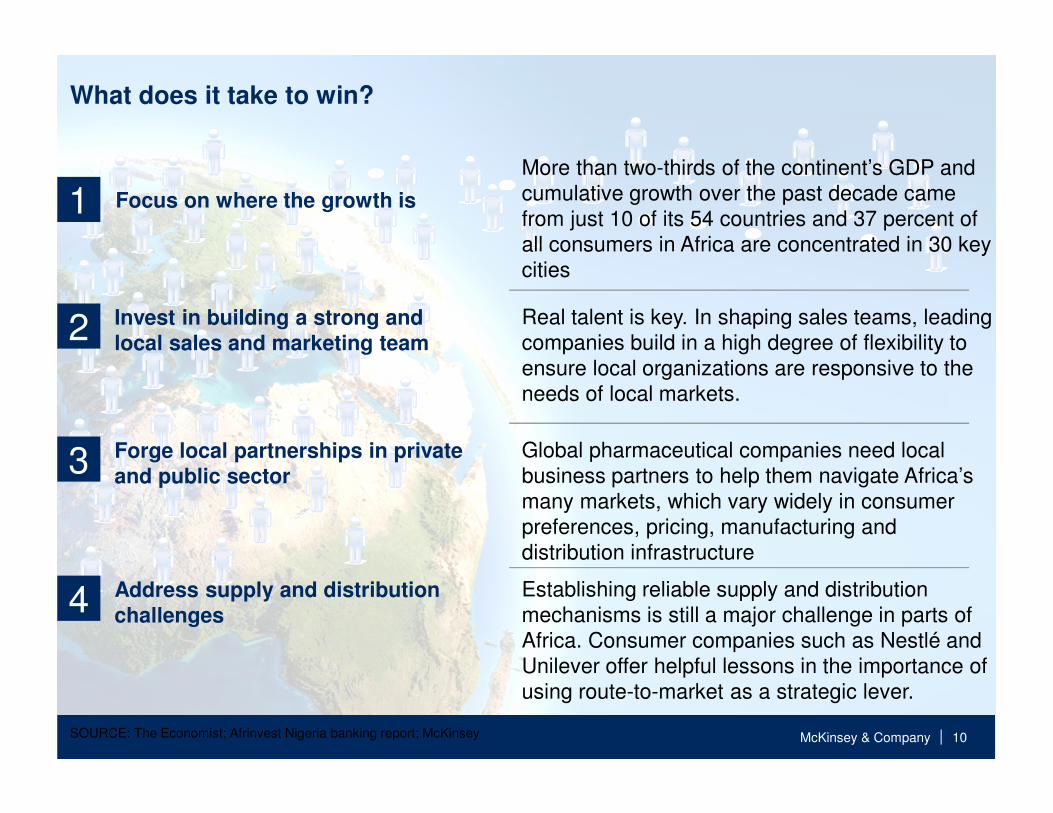

What does it take to win?

SOURCE: The Economist; Afrinvest Nigeria banking report; McKinsey

Focus on where the growth is1More than two-thirds of the continent’s GDP and cumulative growth over the past decade came from just 10 of its 54 countries and 37 percent of all consumers in Africa are concentrated in 30 key cities

Address supply and distribution challenges4 Establishing reliable supply and distribution

mechanisms is still a major challenge in parts of Africa. Consumer companies such as Nestlé and Unilever offer helpful lessons in the importance of using route-to-market as a strategic lever.

Global pharmaceutical companies need local business partners to help them navigate Africa’s many markets, which vary widely in consumer preferences, pricing, manufacturing and distribution infrastructure

Forge local partnerships in private and public sector3

2 Invest in building a strong and local sales and marketing team

Real talent is key. In shaping sales teams, leading companies build in a high degree of flexibility to ensure local organizations are responsive to the needs of local markets.

McKinsey & Company | 11

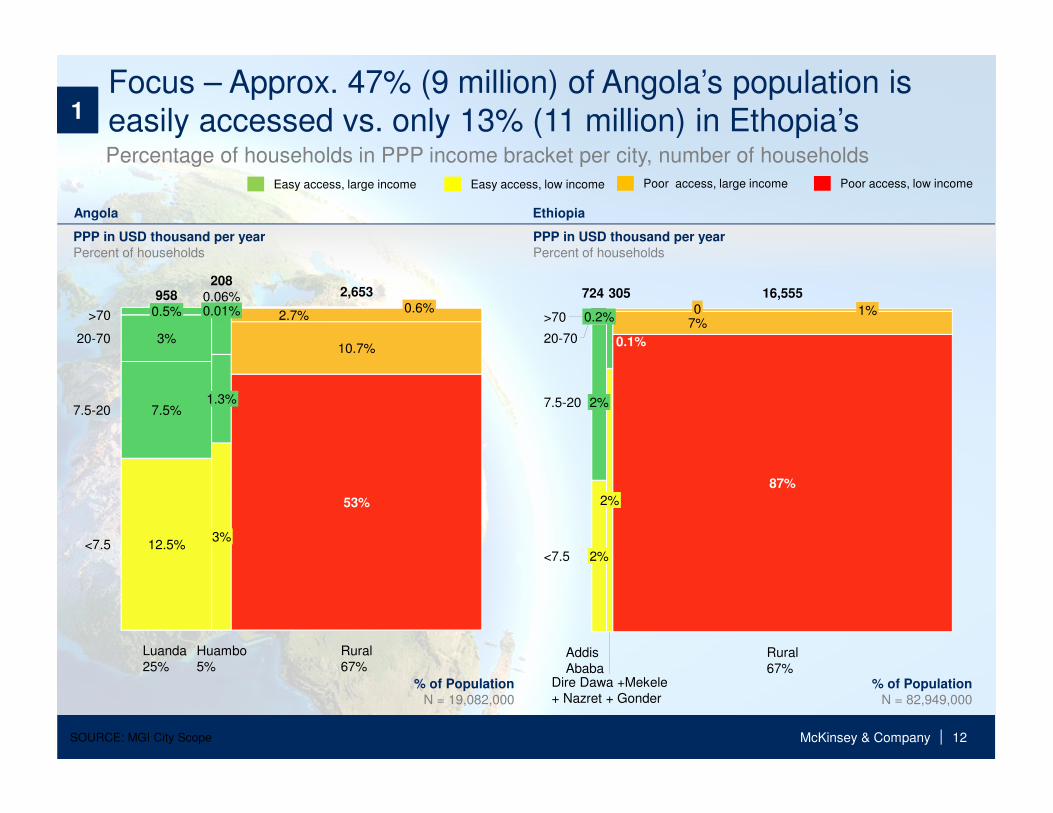

Nigeria Mozambique

Rwanda

SOURCE: McKinsey CityScope; team analysis

1 Only cities with more than 1 million inhabitants are shown on the maps

▪ Total population: 158m (2010) / 230m (2025)▪ Total number of households: 34m / 61m▪ Number of households > 7,5k income: 3.3m / 9.7m

▪ Total population: 23m (2010) / 32m (2025)▪ Total number of households: 6m / 10m▪ Number of households > 7,5k income: 0.4m / 1.6m

▪ Total population: 11m (2010) / 16m (2025)▪ Total number of households: 2m / 4m▪ Number of households > 7,5k income: 0.8m / 2.6m

Maputo: 72 / 279

Lagos: 735 /2.476 Port Harcourt: 160 / 496

Ibadan: 219 / 665

Benin City: 68 / 240

Abuja: 138 / 490

Kano: 88 / 314

Ogbomosho: 80 / 249

Kaduna: 56 / 205

Kigali: 77 / 269

Focus – Focusing on additional cities1 can be more powerful and rewarding than focusing on opening new countries

Number of households with an income superior to 7.5K USD, ‘000 City: XX / XX 2010 2025

Focus on cities: penetrate large countries (e.g., Nigeria) city-by-city and be clear on trade-off when entering smaller markets

1

McKinsey & Company | 12SOURCE: MGI City Scope

0.6%

20-70

53%

1.3%7.5-20

<7.5

958

Rural67%

>70

2,653

Huambo5%

208

3%

0.01%

Luanda 25%

0.06%

7.5%

3%

0.5% 2.7%

12.5%

10.7%

% of Population

N = 19,082,000

PPP in USD thousand per year

Percent of households

Easy access, large income Easy access, low income Poor access, large income Poor access, low income

20-70

87%

016,555

<7.5

>70

7.5-20

0.1%

AddisAbaba

Dire Dawa +Mekele+ Nazret + Gonder

305

2%

1%0.2%

2%

2%

724

Rural67%

7%

% of Population

N = 82,949,000

PPP in USD thousand per year

Percent of households

EthiopiaAngola

Percentage of households in PPP income bracket per city, number of households

Focus – Approx. 47% (9 million) of Angola’s population is easily accessed vs. only 13% (11 million) in Ethopia’s1

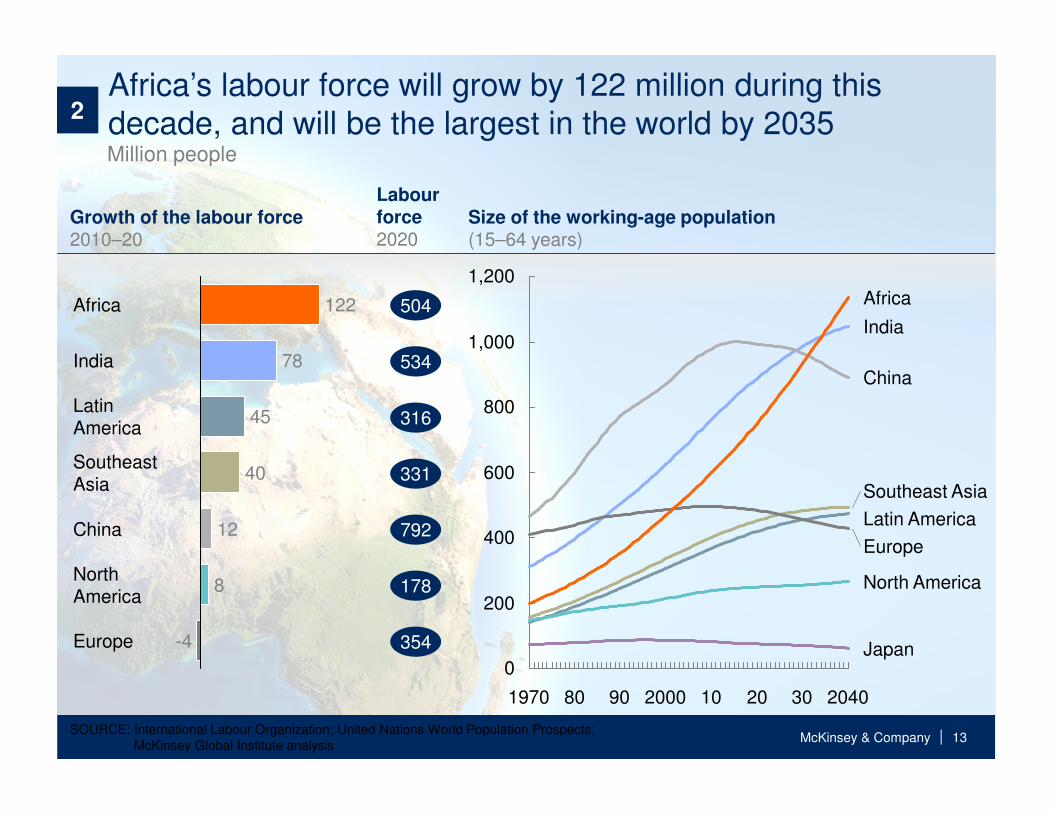

McKinsey & Company | 13SOURCE: International Labour Organization; United Nations World Population Prospects;

McKinsey Global Institute analysis

Africa’s labour force will grow by 122 million during this decade, and will be the largest in the world by 2035

8

SoutheastAsia

LatinAmerica

India

China

Europe -4

NorthAmerica

12

40

45

78

122Africa 504

354

178

792

331

316

534

1,200

1,000

800

0

600

400

200

Southeast Asia

Europe

Latin America

China

30

Japan

India

80

North America

101970 20

Africa

2040200090

Growth of the labour force2010–20

Size of the working-age population(15–64 years)

Million people

Labour force 2020

2

McKinsey & Company | 14

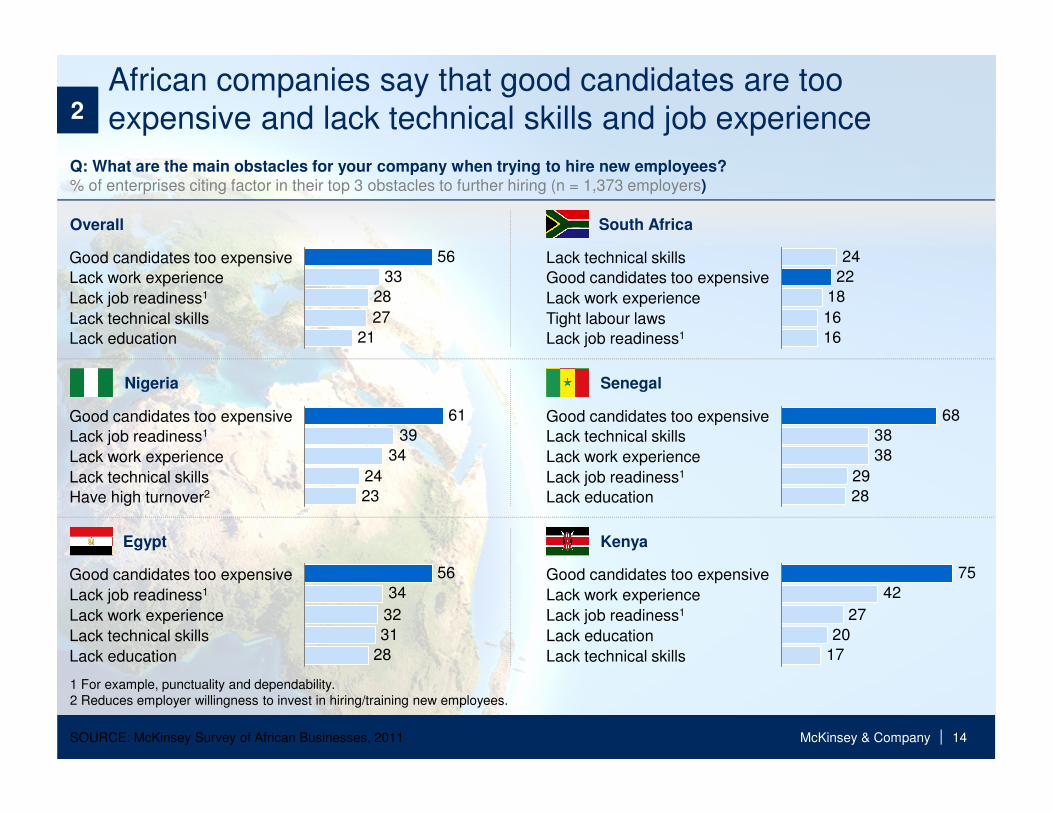

African companies say that good candidates are too expensive and lack technical skills and job experience

SOURCE: McKinsey Survey of African Businesses, 2011

Q: What are the main obstacles for your company when trying to hire new employees?% of enterprises citing factor in their top 3 obstacles to further hiring (n = 1,373 employers)

21

27

28

33

56

Lack technical skills

Lack education

Lack work experience

Good candidates too expensive

Lack job readiness1

1 For example, punctuality and dependability.2 Reduces employer willingness to invest in hiring/training new employees.

Overall South Africa

Nigeria Senegal

Egypt Kenya

16

16

18

22

24Lack technical skills

Lack work experience

Lack job readiness1

Good candidates too expensive

Tight labour laws

17

20

27

42

75

Lack job readiness1

Lack technical skills

Lack education

Lack work experience

Good candidates too expensive

23

24

34

39

61

Have high turnover2

Lack work experience

Lack job readiness1

Lack technical skills

Good candidates too expensive

28

31

32

34

56

Lack technical skills

Lack work experience

Lack job readiness1

Good candidates too expensive

Lack education

28

29

38

38

68

Lack work experience

Lack job readiness1

Good candidates too expensive

Lack education

Lack technical skills

2

McKinsey & Company | 15

Multiple barriers for NCDs at healthcare system level

Infrastructure gap ▪ Poor quantity and quality of diagnostic and treatment centers (e.g., no radiotherapy machines in Côte d’Ivoire)

Human resources scarcity

▪ Limited number of specialists (e.g., no medical oncologist in Nigeria)

Supply chain challenges

▪ Complex supply chain leading to high mark-ups, availability issues and poor cold chain quality assurance

Absence of data ▪ Limited epidemiology data: few registries for NCDs (e.g. no registries of cancer in Gabon)

Policy, regulation and stakeholders inefficiencies

▪ Limited knowledge of NCDs, hence low political priority given to them (e.g. policy development)

▪ Limited knowledge of regulation of Biologics

Funding issues ▪ Limited coverage of NCDs by public and private health insurance

NON-COMMUNICABLE DISEASES

SUB-SAHARAN AFRICA3

McKinsey & Company | 16

Unlock private sector through partnerships in funding and infrastructure

3 types of partnerships

Partnerships with private insurers

▪ Design Private Health insurance package to cover NCDs and related products (incl. innovative micro-insurance)

▪ Provide regional risk pooling through deals with Re-insurance companies (to improve economics)

Partnerships for infrastructure

▪ Develop centers of excellence with international hospital chains (to reduce medical tourism)

▪ Partner with medical device makers to bridge infrastructure gaps

Partnerships with banks for patient credit funding

▪ Develop innovative patient credit productswith banks

3

McKinsey & Company | 17SOURCE: McKinsey in-store visits

In >20% of the visits products were not available Always available1

Partly available

Not available

Product 4

Product 1

Product 2

Product 3

Product 5

Product 6

Product 7

Product 8

Product 9

DISGUISED CLIENT EXAMPLE

1 Available in all pharmacies visited in city2 No availability in at least 1 pharmacy3 No availability in any visited pharmacy

4

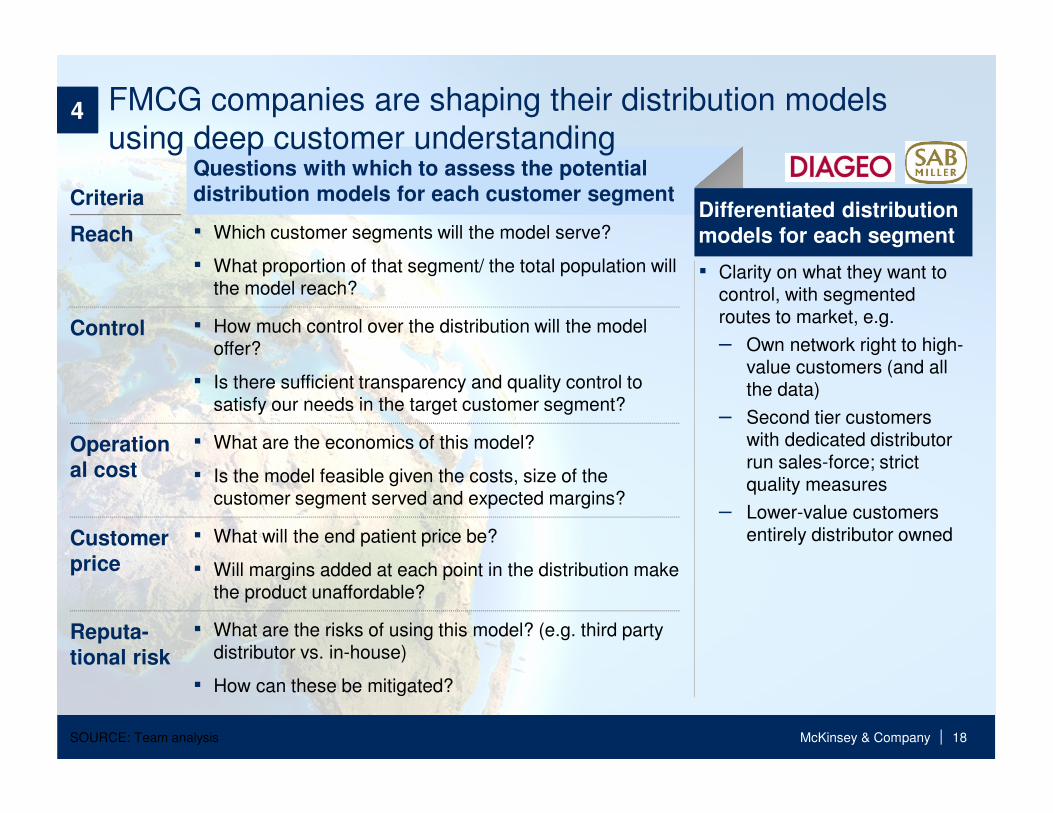

McKinsey & Company | 18SOURCE: Team analysis

Questions with which to assess the potential distribution models for each customer segment

Differentiated distribution models for each segment

▪ Clarity on what they want to control, with segmented routes to market, e.g.

– Own network right to high-value customers (and all the data)

– Second tier customers with dedicated distributor run sales-force; strict quality measures

– Lower-value customers entirely distributor owned

Criteria

▪ Which customer segments will the model serve?

▪ What proportion of that segment/ the total population will the model reach?

▪ How much control over the distribution will the model offer?

▪ Is there sufficient transparency and quality control to satisfy our needs in the target customer segment?

▪ What are the economics of this model?

▪ Is the model feasible given the costs, size of the customer segment served and expected margins?

▪ What will the end patient price be?

▪ Will margins added at each point in the distribution make the product unaffordable?

▪ What are the risks of using this model? (e.g. third party distributor vs. in-house)

▪ How can these be mitigated?

Reach

Control

Operational cost

Customer price

Reputa-tional risk

FMCG companies are shaping their distribution models using deep customer understanding

4