advisor guide sun long term care insurance · advisor guide sun long term care insurance advisor...

TRANSCRIPT

HEALTH INSURANCE | Long term care

Sun LTCI overview:

Productdetails

Additionaloptions

Glossaryofterms

ADVISOR GUIDE

SUN LONG TERM CARE INSURANCE

ADVISOR USE ONLY

Life’s brighter under the sun

1SUN LONG TERM CARE INSURANCE

WithSunLifeFinancial,you’reworkingwithCanada’sleadingLTCIproductandamarketleaderwithexperiencepayingover$36.9millioninclaimsasofDecember2013.2

Asyoubuildandreviewretirementincomeplansforclients,it’simportanttohelpthemrecognizeandconsidertheirfuturehealthcareneedsandtheimpacttheirchoicesandexpectationswillhaveontheirplans.Longtermcareinsurancecanhelpwithfinancialprotectionfortheirplansandthemeanstopayforthelevelofcaretheywantandexpect.

Why include long term care insurance (LTCI) in your portfolio of product solutions?

It’s easy to take our ability to perform day-to-day activities for granted, but this can change, especially as we age.

Fortunately, most of these changes aren’t dramatically different from one day to the next – it’s more of a gradual process.

The level of health care and personal assistance we need, and the cost to meet these needs, will increase with age with the average Canadian experiencing nine to 14 of the final years of their life in diminished health.1

At birth...

theaveragelifeexpectancyofaCanadianmaleis78years.Overnineofthoseyearsareexpectedtobewithadiminishedqualityoflife.1

theaveragelifeexpectancyofaCanadianfemaleis83years.Justover14ofthoseareexpectedtobewithadiminishedqualityoflife.1

0 20 40 60 80 100

Male

Onset of health impairment

Age

Female

1 StatisticsCanada,20122 LifeInsuranceMarketingResearchAssociation(LIMRA),December2013;SunLifeFinancial,December2013.

What is the LTCI target market?

TheLTCIsolutioncanfitwithinthefinancialplanofanumberofdifferenttargetmarkets.Thesearebestsegmentedbythefollowinglifestages:

Planningforretirement Closetoretirement Retirees

TheLTCIproductoptionsavailablewillbedifferentforeachmarketandfitintotheirplanningdifferently.

This guide contains the information you need to:

understandSunLongTermCareInsurance(SunLTCI),

successfullyselltherightplan,and

helpclientsmanagetheirpolicy.

ProductinformationinthisguidereferstopoliciessoldafterDecember6,2013(2013series),unlessotherwiseindicated.

Inthisguide,the symbolisusedtoidentifyaSunLifeFinancialcompetitiveadvantage.Pleaserefertopage39forasummaryofthesecompetitiveadvantages.

2SUN LONG TERM CARE INSURANCE

Product at a glance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Product details . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Issueages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7Howwedeterminedependency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7DEFINITION:Activitiesofdailyliving. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8DEFINITION:Assistivedevices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9

Plan details . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Benefittype. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Weeklybenefitamount . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Waitingperiod. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Benefitperiod. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Additional options that may be applied for . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Inflationprotection. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Returnofpremiumondeath(ROPD). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12DEFINITION:Returnablepremiumamount. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Plan features that are automatically included . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Waiverofpremium(whenaclaimisapproved). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Spousalwaiver. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13DEFINITION:Spouse . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Firstpaymentbonus. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Extendedterminsurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Planofcare. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

LifestageCare™ service . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Applying for a Sun LTCI policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Residencyrequirements. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18Backdating. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Ownershiprules. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20Whoreceivespayment. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Completingtheapplication. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Payments. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Underwritingevidencerequirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22Riskclasses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23Typesofunderwritingdecisions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23Financialunderwriting. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .23

CONTENTS

3SUN LONG TERM CARE INSURANCE

Premium details . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Premiumfrequency–monthlyorannually. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .24Withdrawablepremiumfund. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Premiumpaymentoptions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Premiumguarantee. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .25Whenwewaivepremiums. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26Non-forfeitureprovision..............................................................26

Issuing a Sun LTCI policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Policydate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26Whentheinsurancecomesintoeffect. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .26

Plan changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Changingcoverageoptions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Terminatinganoption. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Conversions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Internalreplacements. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27Reinstatements. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .28Reinstatementrulesataglance. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29

Making a claim for Sun Long Term Care Insurance benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29Whentomakeaclaim. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .29Howtomakeaclaim. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .30Exclusionsandlimitations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31Tipsforanefficientclaimsprocess. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Product history . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34ClaricaLTCIpoliciesdatedDecember,2000-December,2003. . . . . . . . . . . . . . . . . . . . . . . . . . .34ClaricaLTCIpoliciesdatedDecember2003-September2005. . . . . . . . . . . . . . . . . . . . . . . . . . .36SunLTCIpoliciesdatedSeptember,2005–December,2013 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .38

Competitive advantages – summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Where to go for more information? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .40

4SUN LONG TERM CARE INSURANCE

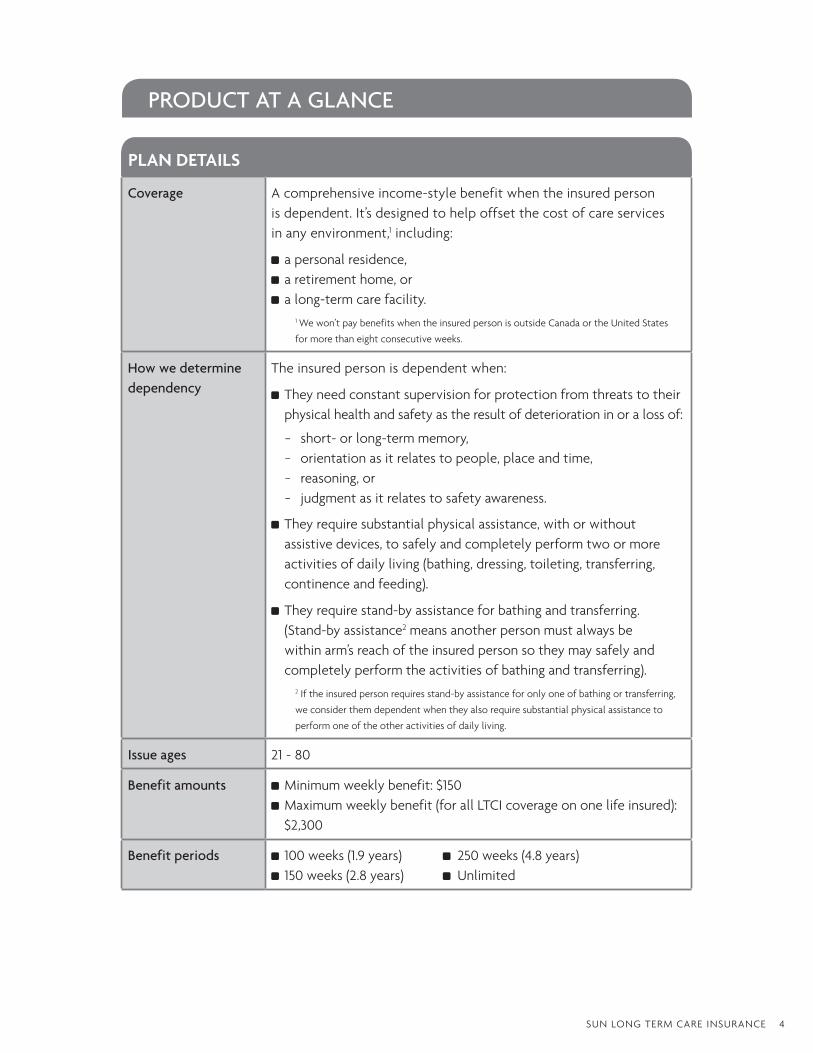

PRODUCT AT A GLANCE

PLAN DETAILS

Coverage Acomprehensiveincome-stylebenefitwhentheinsuredpersonisdependent.It’sdesignedtohelpoffsetthecostofcareservicesinanyenvironment,1including:

apersonalresidence, aretirementhome,or along-termcarefacility.

1Wewon’tpaybenefitswhentheinsuredpersonisoutsideCanadaortheUnitedStates

formorethaneightconsecutiveweeks.

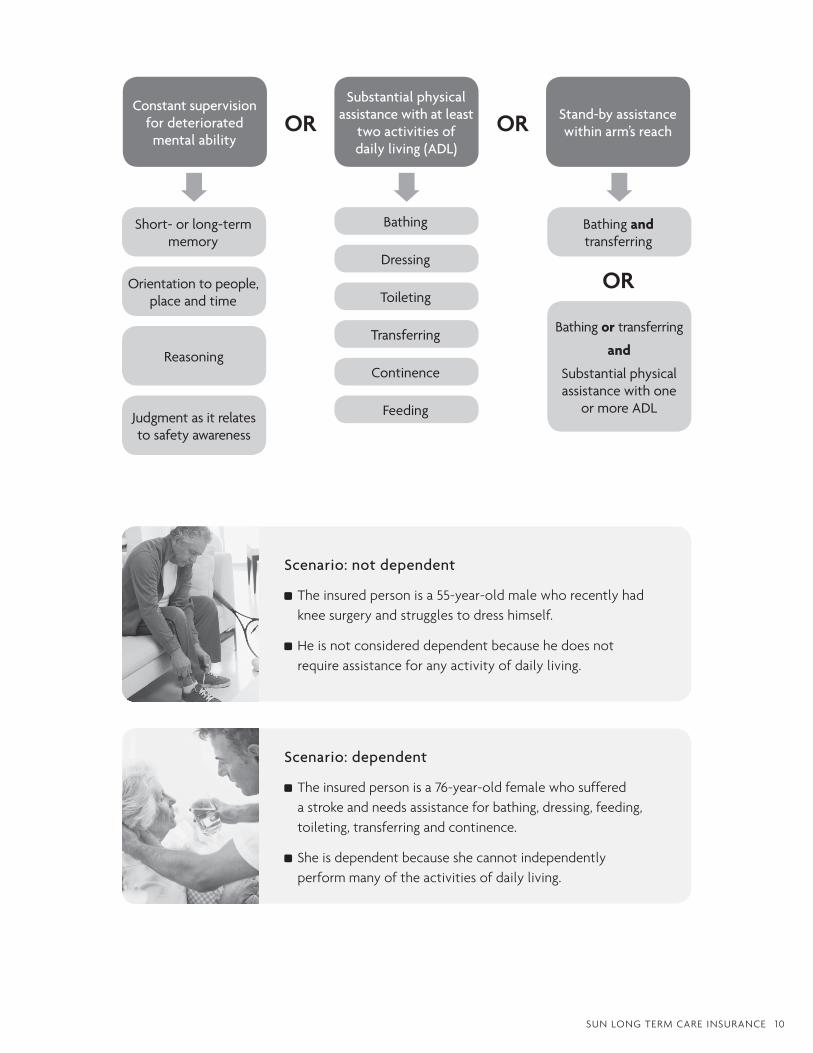

How we determine dependency

Theinsuredpersonisdependentwhen:

Theyneedconstantsupervisionforprotectionfromthreatstotheirphysicalhealthandsafetyastheresultofdeteriorationinoralossof:

− short-orlong-termmemory,− orientationasitrelatestopeople,placeandtime,− reasoning,or− judgmentasitrelatestosafetyawareness.

Theyrequiresubstantialphysicalassistance,withorwithoutassistivedevices,tosafelyandcompletelyperformtwoormoreactivitiesofdailyliving(bathing,dressing,toileting,transferring,continenceandfeeding).

Theyrequirestand-byassistanceforbathingandtransferring.(Stand-byassistance2meansanotherpersonmustalwaysbewithinarm’sreachoftheinsuredpersonsotheymaysafelyandcompletelyperformtheactivitiesofbathingandtransferring).

2Iftheinsuredpersonrequiresstand-byassistanceforonlyoneofbathingortransferring,

weconsiderthemdependentwhentheyalsorequiresubstantialphysicalassistanceto

performoneoftheotheractivitiesofdailyliving.

Issue ages 21-80

Benefit amounts Minimumweeklybenefit:$150 Maximumweeklybenefit(forallLTCIcoverageononelifeinsured):$2,300

Benefit periods 100weeks(1.9years) 250weeks(4.8years) 150weeks(2.8years) Unlimited

5SUN LONG TERM CARE INSURANCE

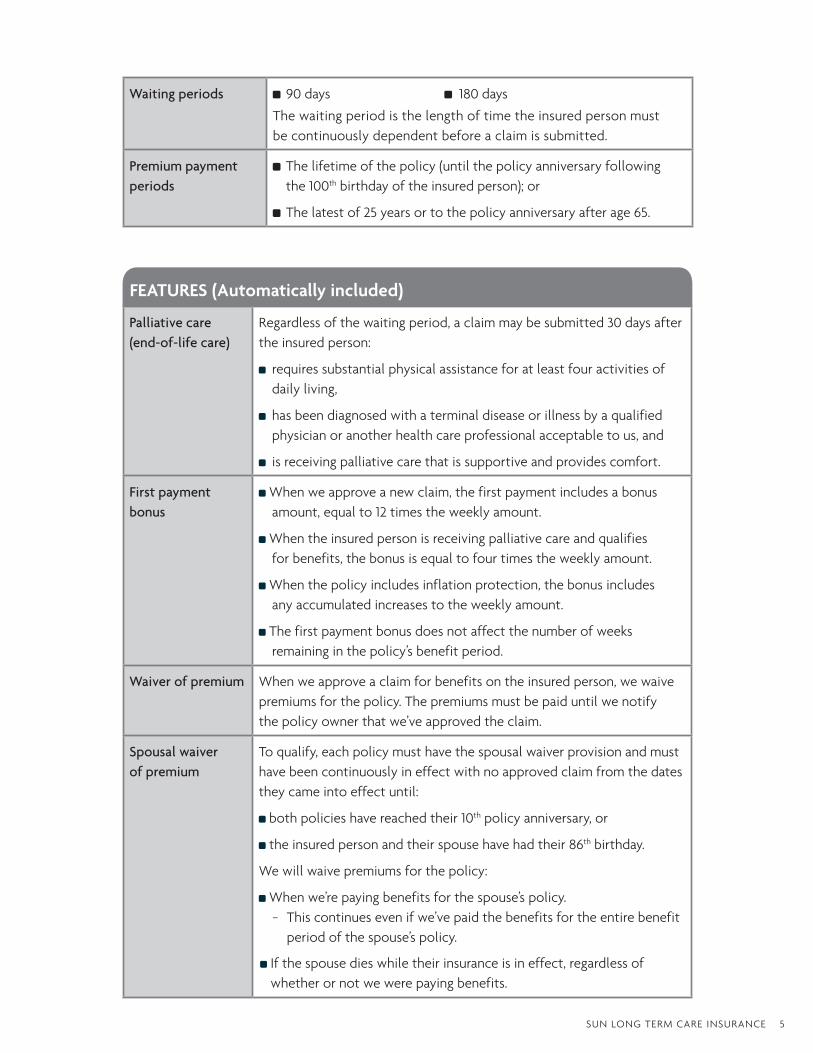

Palliative care (end-of-life care)

Regardlessofthewaitingperiod,aclaimmaybesubmitted30daysaftertheinsuredperson:

requiressubstantialphysicalassistanceforatleastfouractivitiesofdailyliving,

hasbeendiagnosedwithaterminaldiseaseorillnessbyaqualifiedphysicianoranotherhealthcareprofessionalacceptabletous,and

isreceivingpalliativecarethatissupportiveandprovidescomfort.

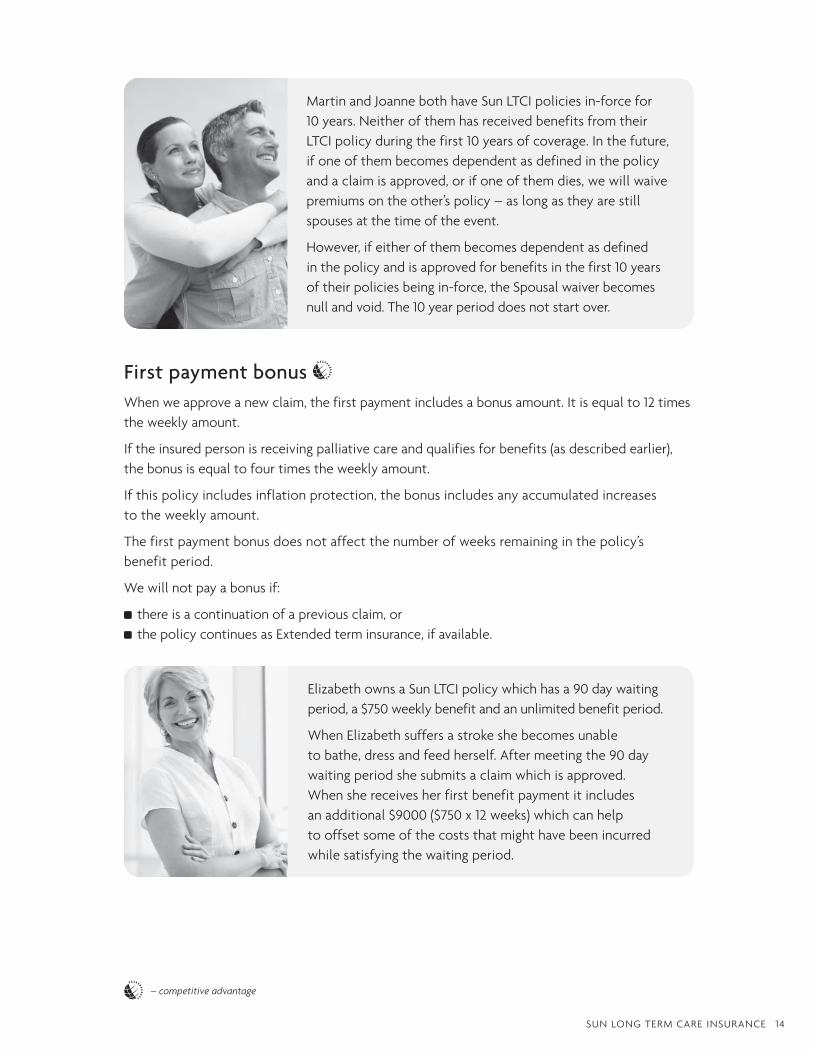

First payment bonus

Whenweapproveanewclaim,thefirstpaymentincludesabonusamount,equalto12timestheweeklyamount.

Whentheinsuredpersonisreceivingpalliativecareandqualifiesforbenefits,thebonusisequaltofourtimestheweeklyamount.

Whenthepolicyincludesinflationprotection,thebonusincludesanyaccumulatedincreasestotheweeklyamount.

Thefirstpaymentbonusdoesnotaffectthenumberofweeksremaininginthepolicy’sbenefitperiod.

Waiver of premium Whenweapproveaclaimforbenefitsontheinsuredperson,wewaivepremiumsforthepolicy.Thepremiumsmustbepaiduntilwenotifythepolicyownerthatwe’veapprovedtheclaim.

Spousal waiver of premium

Toqualify,eachpolicymusthavethespousalwaiverprovisionandmusthavebeencontinuouslyineffectwithnoapprovedclaimfromthedatestheycameintoeffectuntil:

bothpolicieshavereachedtheir10thpolicyanniversary,or

theinsuredpersonandtheirspousehavehadtheir86thbirthday.

Wewillwaivepremiumsforthepolicy:

Whenwe’repayingbenefitsforthespouse’spolicy.− Thiscontinuesevenifwe’vepaidthebenefitsfortheentirebenefit

periodofthespouse’spolicy.

Ifthespousedieswhiletheirinsuranceisineffect,regardlessofwhetherornotwewerepayingbenefits.

FEATURES (Automatically included)

Waiting periods 90days 180days

Thewaitingperiodisthelengthoftimetheinsuredpersonmustbecontinuouslydependentbeforeaclaimissubmitted.

Premium payment periods

Thelifetimeofthepolicy(untilthepolicyanniversaryfollowingthe100thbirthdayoftheinsuredperson);or

Thelatestof25yearsortothepolicyanniversaryafterage65.

6SUN LONG TERM CARE INSURANCE

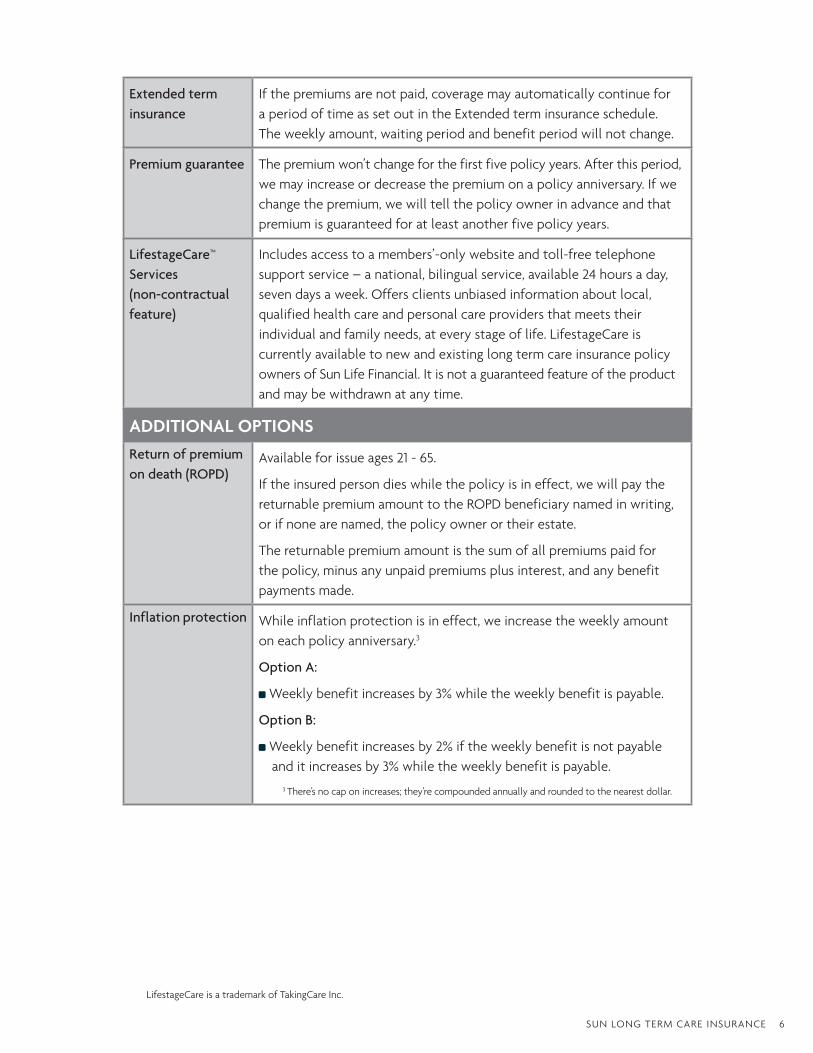

Extended term insurance

Ifthepremiumsarenotpaid,coveragemayautomaticallycontinueforaperiodoftimeassetoutintheExtendedterminsuranceschedule.Theweeklyamount,waitingperiodandbenefitperiodwillnotchange.

Premium guarantee Thepremiumwon’tchangeforthefirstfivepolicyyears.Afterthisperiod,wemayincreaseordecreasethepremiumonapolicyanniversary.Ifwechangethepremium,wewilltellthepolicyownerinadvanceandthatpremiumisguaranteedforatleastanotherfivepolicyyears.

LifestageCare™

Services (non-contractual feature)

Includesaccesstoamembers’-onlywebsiteandtoll-freetelephonesupportservice–anational,bilingualservice,available24hoursaday,sevendaysaweek.Offersclientsunbiasedinformationaboutlocal,qualifiedhealthcareandpersonalcareprovidersthatmeetstheirindividualandfamilyneeds,ateverystageoflife.LifestageCareiscurrentlyavailabletonewandexistinglongtermcareinsurancepolicyownersofSunLifeFinancial.Itisnotaguaranteedfeatureoftheproductandmaybewithdrawnatanytime.

ADDITIONAL OPTIONSReturn of premium on death (ROPD)

Availableforissueages21-65.

Iftheinsuredpersondieswhilethepolicyisineffect,wewillpaythereturnablepremiumamounttotheROPDbeneficiarynamedinwriting,orifnonearenamed,thepolicyownerortheirestate.

Thereturnablepremiumamountisthesumofallpremiumspaidforthepolicy,minusanyunpaidpremiumsplusinterest,andanybenefitpaymentsmade.

Inflation protection Whileinflationprotectionisineffect,weincreasetheweeklyamountoneachpolicyanniversary.3

Option A:

Weeklybenefitincreasesby3%whiletheweeklybenefitispayable.

Option B:

Weeklybenefitincreasesby2%iftheweeklybenefitisnotpayableanditincreasesby3%whiletheweeklybenefitispayable.

3There’snocaponincreases;they’recompoundedannuallyandroundedtothenearestdollar.

LifestageCareisatrademarkofTakingCareInc.

7SUN LONG TERM CARE INSURANCE

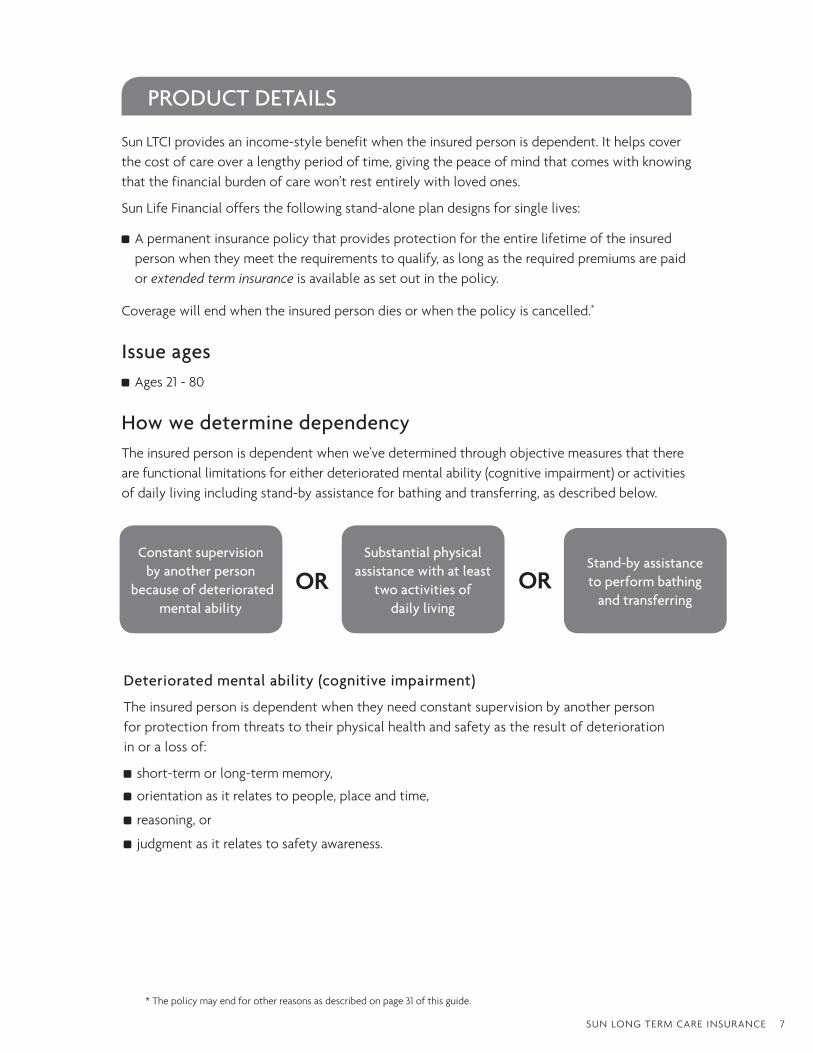

SunLTCIprovidesanincome-stylebenefitwhentheinsuredpersonisdependent.Ithelpscoverthecostofcareoveralengthyperiodoftime,givingthepeaceofmindthatcomeswithknowingthatthefinancialburdenofcarewon’trestentirelywithlovedones.

SunLifeFinancialoffersthefollowingstand-aloneplandesignsforsinglelives:

Apermanentinsurancepolicythatprovidesprotectionfortheentirelifetimeoftheinsuredpersonwhentheymeettherequirementstoqualify,aslongastherequiredpremiumsarepaidorextendedterminsuranceisavailableassetoutinthepolicy.

Coveragewillendwhentheinsuredpersondiesorwhenthepolicyiscancelled.*

Issue ages Ages21-80

How we determine dependency Theinsuredpersonisdependentwhenwe’vedeterminedthroughobjectivemeasuresthattherearefunctionallimitationsforeitherdeterioratedmentalability(cognitiveimpairment)oractivitiesofdailylivingincludingstand-byassistanceforbathingandtransferring,asdescribedbelow.

PRODUCT DETAILS

*Thepolicymayendforotherreasonsasdescribedonpage31ofthisguide.

Deteriorated mental ability (cognitive impairment)

Theinsuredpersonisdependentwhentheyneedconstantsupervisionbyanotherpersonforprotectionfromthreatstotheirphysicalhealthandsafetyastheresultofdeteriorationinoralossof:

short-termorlong-termmemory,

orientationasitrelatestopeople,placeandtime,

reasoning,or

judgmentasitrelatestosafetyawareness.

Constant supervision by another person

because of deteriorated mental ability

Substantial physical assistance with at least

two activities of daily living

Stand-by assistance to perform bathing

and transferringOR OR

8SUN LONG TERM CARE INSURANCE

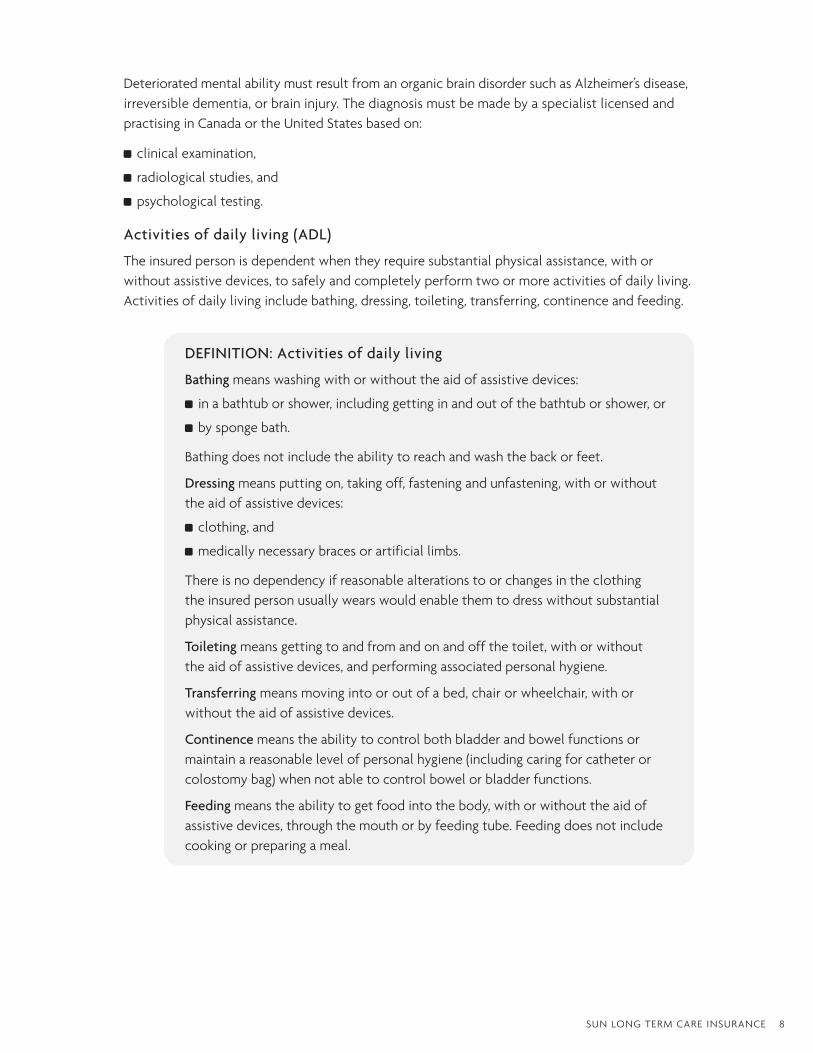

DeterioratedmentalabilitymustresultfromanorganicbraindisordersuchasAlzheimer’sdisease,irreversibledementia,orbraininjury.ThediagnosismustbemadebyaspecialistlicensedandpractisinginCanadaortheUnitedStatesbasedon:

clinicalexamination,

radiologicalstudies,and

psychologicaltesting.

Activities of daily living (ADL)

Theinsuredpersonisdependentwhentheyrequiresubstantialphysicalassistance,withorwithoutassistivedevices,tosafelyandcompletelyperformtwoormoreactivitiesofdailyliving.Activitiesofdailylivingincludebathing,dressing,toileting,transferring,continenceandfeeding.

DEFINITION: Activities of daily living

Bathingmeanswashingwithorwithouttheaidofassistivedevices:

inabathtuborshower,includinggettinginandoutofthebathtuborshower,or

byspongebath.

Bathingdoesnotincludetheabilitytoreachandwashthebackorfeet.

Dressingmeansputtingon,takingoff,fasteningandunfastening,withorwithouttheaidofassistivedevices:

clothing,and

medicallynecessarybracesorartificiallimbs.

Thereisnodependencyifreasonablealterationstoorchangesintheclothingtheinsuredpersonusuallywearswouldenablethemtodresswithoutsubstantialphysicalassistance.

Toiletingmeansgettingtoandfromandonandoffthetoilet,withorwithouttheaidofassistivedevices,andperformingassociatedpersonalhygiene.

Transferringmeansmovingintooroutofabed,chairorwheelchair,withorwithouttheaidofassistivedevices.

Continencemeanstheabilitytocontrolbothbladderandbowelfunctionsormaintainareasonablelevelofpersonalhygiene(includingcaringforcatheterorcolostomybag)whennotabletocontrolbowelorbladderfunctions.

Feedingmeanstheabilitytogetfoodintothebody,withorwithouttheaidofassistivedevices,throughthemouthorbyfeedingtube.Feedingdoesnotincludecookingorpreparingameal.

9SUN LONG TERM CARE INSURANCE

Stand-by assistance for bathing and transferring

Theinsuredpersonisalsodependentwhentheyrequirestand-byassistanceforbathingandtransferring.Stand-byassistancemeansanotherpersonmustalwaysbewithinarm’sreachoftheinsuredpersonsotheymaysafelyandcompletelyperformtheactivitiesofbathingandtransferring.

Iftheinsuredpersonrequiresstand-byassistanceforonlyoneofbathingortransferring,weconsiderthemdependentwhentheyalsorequiresubstantialphysicalassistancetoperformoneoftheotherADLs.

DEFINITION: Assistive devices

Assistivedevicesareaidsthatwedeterminecouldbeusedtoimprovetheinsuredperson’sfunctioning.Theseincludeadjustablebeds,buttonhooks,canes,crutches,grabbars,handheldshowerheads,bathbrushes,seatlifts,transferbenches,walkersandwheelchairs.IfusinganassistivedeviceallowstheinsuredpersontoperformanADLsafelyandcompletely,theinsuredpersonisnotdependentforthatactivity.

Palliative care (end-of-life care)

Regardlessofthewaitingperiod,aclaimmaybesubmitted30daysaftertheinsuredperson:

requiressubstantialphysicalassistanceforatleastfouractivitiesofdailyliving,

hasbeendiagnosedwithaterminaldiseaseorillnessbyaqualifiedphysicianoranotherhealthcareprofessionalacceptabletous,and

isreceivingpalliativecarethatissupportiveandprovidescomfort.

–competitiveadvantage

10SUN LONG TERM CARE INSURANCE

Scenario: not dependent

Theinsuredpersonisa55-year-oldmalewhorecentlyhadkneesurgeryandstrugglestodresshimself.

Heisnotconsidereddependentbecausehedoesnotrequireassistanceforanyactivityofdailyliving.

Scenario: dependent

Theinsuredpersonisa76-year-oldfemalewhosufferedastrokeandneedsassistanceforbathing,dressing,feeding,toileting,transferringandcontinence.

Sheisdependentbecauseshecannotindependentlyperformmanyoftheactivitiesofdailyliving.

Bathing

Dressing

Toileting

Transferring

Continence

Feeding

Constant supervision for deteriorated

mental ability

Substantial physical assistance with at least

two activities of daily living (ADL)

Stand-by assistance within arm’s reachOR OR

OR

Short- or long-term memory

Bathing and transferring

Bathing or transferring

and

Substantial physical assistance with one

or more ADL

Orientation to people, place and time

Reasoning

Judgment as it relates to safety awareness

11SUN LONG TERM CARE INSURANCE

PLAN DETAILS

Benefit type Wepayaweeklyincome-stylebenefittothepolicyownerwhentheinsuredpersonqualifiesforit.Theclaimantdoesn’tneedtosubmitreceiptsforservicestoreceivethebenefitoncetheinsuredpersonqualifiesforthebenefit.Thepolicyownercanusethemoneyhowevertheychoose.

Weekly benefit amount Thebenefitiscalculatedweeklyandpaidmonthly.

Minimum weekly benefit amount: $150

Maximum weekly benefit amount (for all LTCI coverage on one insured person):$2,300

Waiting periodThewaitingperiodisthelengthoftimetheinsuredpersonmustbecontinuouslydependentbeforeaclaimissubmitted.

ItstartsonthedatetheyfirstrequireassistancefortwoormoreADLsorthedatetheyfirstrequirecontinualsupervision.Therearetwooptionstochoosefrom:

90days 180days

Benefit period Thebenefitperiodisthelengthoftimewemaypayaclaim.

100weeks(1.9years) 250weeks(4.8years) 150weeks(2.8years) Unlimited

Ifthebenefitperiodislimitedtoamaximumnumberofweeks,eachpaymentwemakereducesthenumberofweekseligibletobepaid.Thenumberofweeksinthebenefitperioddoesnotstartoverwithanewclaim.

Ifthebenefitperiodisunlimited,it’snotaffectedbythepaymentswemake.

–competitiveadvantage

12SUN LONG TERM CARE INSURANCE

Therearenocapsonincreases.

Ifanapplicantwishestoobtaincoverageformorethanthemaximumweeklybenefitamountof$2,300,thiscanbeachievedbyselectingInflationprotectionoptionB.Withthisoption,theinitialcoverageamountwilldoubleinapproximately35years.

Return of premium on death (ROPD) Iftheinsuredpersondieswhilethepolicyisineffect,wewillpaythereturnablepremiumamount,asdescribedbelow,totheROPDbeneficiarynamedinwriting,orifnonearenamed,thepolicyownerortheirestate.

DEFINITION: Returnable premium amount

Thereturnablepremiumamountisthesumofallpremiumspaidforthepolicy,minus:

anyunpaidpremiumsplusinterest,and anybenefitpaymentsmade.

Inflation protection Whileinflationprotectionisineffect,weincreasetheweeklyamountoneachpolicyanniversary,asdescribedbelow.Increasesarecompoundedannuallyandroundedtothenearestdollarandtherearenocapsonincreases.

Atthetimeofpurchase,theclientmayselectoneofthefollowingoptions.

Option A:

Whileinflationprotectionisineffect,weincreasetheweeklybenefitamountbythreepercentoneachpolicyanniversarywhenbenefitsarepayable.Increaseswillbecompoundedannuallyandroundedtothenearestdollarandtherearenocapsonincreases.

Ifbenefitsarenolongerpayableonapolicyanniversary,theweeklybenefitamountwillnotincrease.Anyaccumulatedincreaseremainsineffect.

Option B:

Whileinflationprotectionisineffect,weincreasetheweeklybenefitamountoneachpolicyanniversary.Theincreaseweapplyis:

Twopercentifwearenotpayingbenefitsonthepolicyanniversarydateor Threepercentifwearepayingbenefitsonthepolicyanniversarydate.

ADDITIONAL OPTIONS THAT MAY BE APPLIED FOR

–competitiveadvantage

13SUN LONG TERM CARE INSURANCE

DEFINITION: Spouse

Spousemeansthepersonwhoismarriedtotheinsuredperson,isinacivilunionwiththeinsuredperson,orthepersonwholiveswiththeinsuredpersoninaconjugalrelationshipforatleast12consecutivemonthsbeforethedateaclaimissubmittedforthespouse.

Torequestpremiumsbewaived,thepolicynumbermustbeincludedonthespouse’sclaimform.Wemayaskforproofofthespouse’srelationshiptotheinsuredperson.

Wewillwaivepremiumsforthepolicywhenwe’repayingbenefitsforthespouse’spolicy.Wewillcontinuetowaivepremiumsforthepolicyevenafterwe’vepaidbenefitsfortheentirebenefitperiodfortheirpolicy.

Wewillalsowaivepremiumsforthepolicyifthespousedieswhiletheirinsuranceisineffect,whetherornotwewerepayingbenefitsatthetimetheydie.Wewillrequireproofofthespouse’sdeath.

Thepremiumsforthepolicymustbepaiduntilwenotifytheclientthattherequestisapproved.

Anyexcesspremiumspaidwillbedepositedtothepolicy’swithdrawablepremiumfund.

Waiver of premium (when a claim is approved)Whenweapproveaclaimforbenefitsontheinsuredperson,wewaivepremiumsforthepolicy.Thepremiumsmustbepaiduntilwenotifythepolicyownerthatwe’veapprovedtheclaim.

Spousal waiver Ifwe’veissuedalongtermcareinsurancepolicyontheinsuredperson’sspouseandapprovedaclaimforbenefitsonthatpolicy,wemaywaivepremiumsfortheinsuredperson’spolicy.

Tohavepremiumswaived,bothpoliciesmusthaveSpousalwaiver.Eachpolicymusthavebeencontinuouslyineffectwithnoapprovedclaim,fromthedatestheycameintoeffectuntil:

bothpolicieshavereachedtheir10thpolicyanniversary,or theinsuredpersonandtheirspousehavehadtheir86thbirthday.

PLAN FEATURES THAT ARE AUTOMATICALLY INCLUDED

–competitiveadvantage

14SUN LONG TERM CARE INSURANCE

ElizabethownsaSunLTCIpolicywhichhasa90daywaitingperiod,a$750weeklybenefitandanunlimitedbenefitperiod.

WhenElizabethsuffersastrokeshebecomesunabletobathe,dressandfeedherself.Aftermeetingthe90daywaitingperiodshesubmitsaclaimwhichisapproved.Whenshereceivesherfirstbenefitpaymentitincludesanadditional$9000($750x12weeks)whichcanhelptooffsetsomeofthecoststhatmighthavebeenincurredwhilesatisfyingthewaitingperiod.

First payment bonus Whenweapproveanewclaim,thefirstpaymentincludesabonusamount.Itisequalto12timestheweeklyamount.

Iftheinsuredpersonisreceivingpalliativecareandqualifiesforbenefits(asdescribedearlier),thebonusisequaltofourtimestheweeklyamount.

Ifthispolicyincludesinflationprotection,thebonusincludesanyaccumulatedincreasestotheweeklyamount.

Thefirstpaymentbonusdoesnotaffectthenumberofweeksremaininginthepolicy’sbenefitperiod.

Wewillnotpayabonusif:

thereisacontinuationofapreviousclaim,or thepolicycontinuesasExtendedterminsurance,ifavailable.

MartinandJoannebothhaveSunLTCIpoliciesin-forcefor10years.NeitherofthemhasreceivedbenefitsfromtheirLTCIpolicyduringthefirst10yearsofcoverage.Inthefuture,ifoneofthembecomesdependentasdefinedinthepolicyandaclaimisapproved,orifoneofthemdies,wewillwaivepremiumsontheother’spolicy–aslongastheyarestillspousesatthetimeoftheevent.

However,ifeitherofthembecomesdependentasdefinedinthepolicyandisapprovedforbenefitsinthefirst10yearsoftheirpoliciesbeingin-force,theSpousalwaiverbecomesnullandvoid.The10yearperioddoesnotstartover.

–competitiveadvantage

15SUN LONG TERM CARE INSURANCE

Extended term insurance IfpremiumsarenotpaidandthepolicyhasbeenineffectforthenumberofyearssetoutintheExtendedterminsurancescheduleinthepolicy,thepolicywillautomaticallycontinueforaperiodoftime.Attheendofthatperiod,thepolicyends.

Thepolicycontinuesineffectif:

wedonotreceivetherequiredpremiumwithin31daysafteritisdue, thereisnotenoughmoneyinthewithdrawablepremiumfundtopaytherequiredpremium,and extendedterminsuranceisavailable.

Theweeklyamount,waitingperiodandbenefitperiodwillnotchange.

Whilethepolicycontinuesasextendedterminsurance:

thepolicyownermaynotpaypremiums, thepolicyownermaynotputmoneyintothewithdrawablepremiumfund, wewillnotpayafirstpaymentbonus, Returnofpremiumondeathends,ifincludedinthepolicy,and Inflationprotectionends,ifincludedinthepolicy.(Anyaccumulatedincreasetotheweeklyamountremainsineffect).

Ifweapproveaclaimwhileextendedterminsuranceisineffect,thepolicycontinuesassetoutintheschedule.Ifwestoppayingaclaimbeforetheendofthelastavailableyearshownintheschedule,thepolicycontinuesasextendedterminsurance.

Ifwe’restillpayingbenefitsattheendofthelastavailableyearshownintheschedule,wewillcontinuetopaybenefitswhiletheinsuredpersonqualifies.Onthedatetheynolongerqualify,thepolicyends.

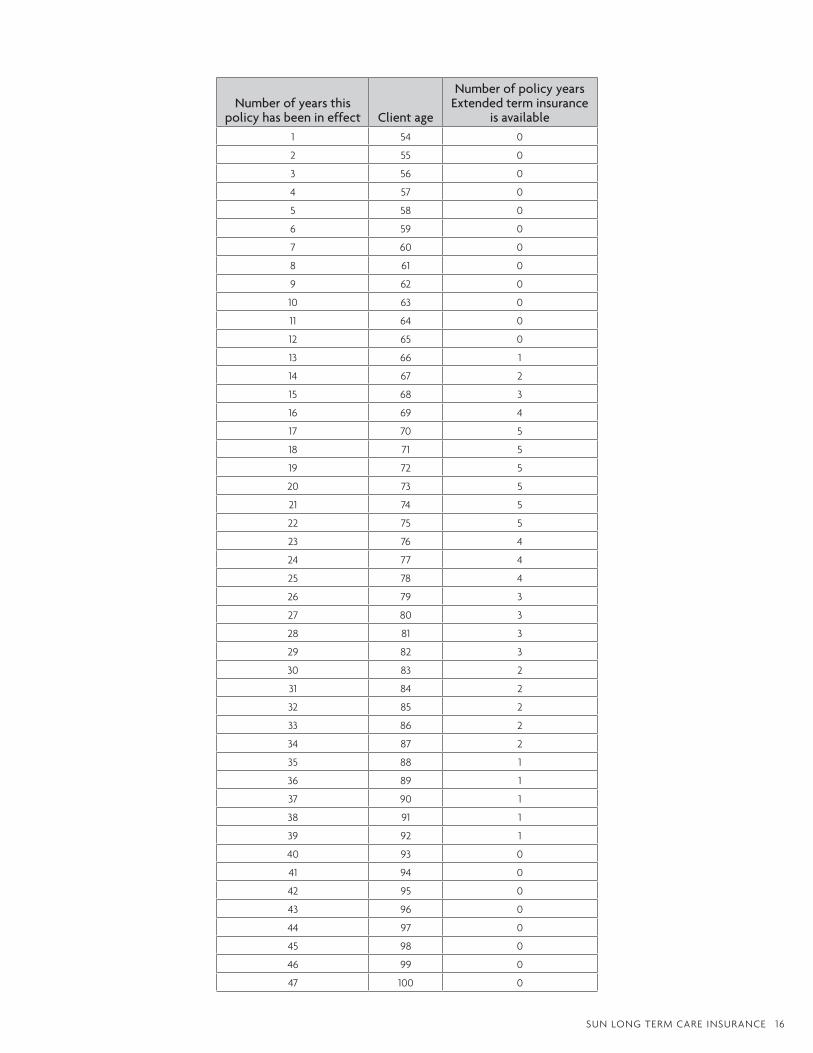

ThetablepresentedonthefollowingpageisanexampleofanExtendedterminsuranceschedulebasedona53yearoldfemale,whohaspurchasedthefollowingpolicy:

$650WeeklyBenefit UnlimitedBenefitperiod 90dayWaitingPeriod Withoutadditionaloption Paidforannuallyonalifetimebasis(untiltheanniversaryafterage100)

–competitiveadvantage

16SUN LONG TERM CARE INSURANCE

Number of years this policy has been in effect Client age

Number of policy years Extended term insurance

is available1 54 0

2 55 0

3 56 0

4 57 0

5 58 0

6 59 0

7 60 0

8 61 0

9 62 0

10 63 0

11 64 0

12 65 0

13 66 1

14 67 2

15 68 3

16 69 4

17 70 5

18 71 5

19 72 5

20 73 5

21 74 5

22 75 5

23 76 4

24 77 4

25 78 4

26 79 3

27 80 3

28 81 3

29 82 3

30 83 2

31 84 2

32 85 2

33 86 2

34 87 2

35 88 1

36 89 1

37 90 1

38 91 1

39 92 1

40 93 0

41 94 0

42 95 0

43 96 0

44 97 0

45 98 0

46 99 0

47 100 0

17SUN LONG TERM CARE INSURANCE

Reversing Extended term insurance

Thepolicyownercanapplytoreverseextendedterminsuranceandresumepayingpremiumsforthispolicyiftheinsuredpersonisalive.

Toreverseextendedterminsurance:

applywithintwoyearsofthedatetherequiredpremiumwasnotpaid, giveusnewevidenceofinsurabilitythatweconsidersatisfactory,and makeapaymentequaltothereinstatementchargeweset.

Ifwedon’tapprovetheapplication,werefundanyamountpaidwhentherequestwassubmitted.

Plan of careTheinsuredpersonisentitledtoonefreeplanofcare.Arequestforaplanofcarecanbemadeafteraclaimhasbeenapprovedandwhiletheinsuredpersonisdependent.

Theplanofcarewilloutlinethetypeandamountofcaretheinsuredpersonrequires.Itwillalsoexplainhowcarecanbeprovidedandifgovernmentprogramsareavailable.

Fromthemomentthepolicyisissuedandaslongasitremainsinforce,thepolicyownerhasimmediateandunlimitedaccesstothevaluableresourcesprovidedthroughLifestageCareservices.

LifestageCareiscurrentlyavailabletonewandexistinglongtermcareinsurancepolicyownersofSunLifeFinancial.Itisnotaguaranteedfeatureoftheproductandmaybewithdrawnatanytime.

Accessing LifestageCare

Thepolicyownercanaccessthisuniqueserviceimmediatelyafterthepolicyisissuedandwithouthavingtomakeaclaim,aslongasthepolicyremainsinforce.LifestageCareservicesareforthepolicyowner’spersonalusebutcanalsobeusedtohelpanyfamilymember.

AccessingLifestageCareiseasy–logintotheLifestageCarewebsiteorcallthetoll-freenumber.TheLTCIpolicynumberistheclientidentifier.TheclientcanstartusingLifestageCareservicesimmediately:

www.sunlife.mylifestagecare.ca 1877-301-1515

Helping families help themselves

Theserviceprovidesunlimitedaccesstoinformationaboutlocal,qualifiedhealthcareandpersonalcareproviderscloselymatchingindividualandfamilyneeds,ateverystageoflife.

Seniors–foraging,retirementresidences,nursinghomes,homecare,andcommunitycare

Self-care–forpersonaladviceandwell-being,addictiontreatment,budgetandcreditcounseling,andphysicalrehabilitation

Children and teens –forparenting,childcare,andspecialneedsservices

–competitiveadvantage

LIFESTAGECARE™ SERVICE

18SUN LONG TERM CARE INSURANCE

APPLYING FOR A SUN LTCI POLICY

Residency requirements

Non-residents

WeconsiderresidentsofCanadatobeindividualswhoresideinCanadaforsixmonthsormoreeachyear.SunLifeFinancialproductsarepricedforindividualslivinginCanada.WedonotacceptapplicationsforindividualswhodonotliveinCanada.

Permanent residents of Canada

Iftheindividualhaspermanentresidentstatus,theycanbeconsidered.However,iftheyliveinCanadalessthan12monthsperyear,wewillrequireaparamedicalandbloodprofile.

Expert advice. Specific information. Confidential service.

LifestageCareisamembers’-onlywebsite,andtoll-freetelephonesupportserviceisavailabletolongtermcareinsurancepolicyownerswithSunLifeFinancial.

Expert–expertagentsareavailable24hoursaday,7daysaweektoanswerquestionsbyphoneoremail

Specific–helpsplanandmanagefamilycareresponsibilitiesandfindresourcesbasedonspecificrequirementsandpostalcode.Theinformationreceivedismatchedspecificallytotheindividual’sneeds

Confidential–acomplete,unbiasedservice;anyinformationprovidediskeptstrictlyconfidential

Care resources for the policy owner and their family

LifestageCarefocusesontheinformationandsupportneededtoprovidethebestcareforthewholefamily.Theserviceallowsthepolicyownerandtheirfamilytoquicklyandeasily:

Findacompleterangeofqualifiedlocalprofessionals,carefacilitiesandhealthcareresourcesanywhereinCanada.

Determinewhathomecare,rehabilitationtreatment,educationalandresidentialserviceswillcost.

Obtainprofessionaladviceongeriatriccareandcareforteensandchildrenincludingresourcesforspecialneeds.

Readsimpleexplanationsoftreatmentoptions.

Findtherightquestionstoaskwhenchoosingaprofessionalcaregiver.

Stayinformedaboutmultiplegovernmentfinancialassistanceprograms.

LifestageCareisatrademarkofTakingCareInc.

19SUN LONG TERM CARE INSURANCE

Non-landed immigrants

Generallyspeaking,non-landedimmigrantsarenoteligibletoapplyforlongtermcareinsurance.However,exceptionsmaybemadefordoctors,professionals,investors,entrepreneursandotherindividualsapprovedunderaprovincialnomineeprogram(withtheexceptionofrefugees).Inthesecaseswewillrequireacopyoftheiremploymentcontractandworkvisaorprovincialnomineeacceptanceletter.

Ifthereismedicalhistoryrequiringtreatmentorfollow-up,weexpecttheproposedinsuredpersontohaveamedicaldoctorinCanadabeforewecanconsiderthem.

MaximumLTCIcoverageof$1,000perweekmaybeconsidered.

IftheyhaveresidedinCanadalessthan12months,wewillrequireaparamedicalandbloodprofile.

Temporary work visa

LTCIisgenerallynotavailable.

Exception:TheproposedinsuredpersonmustbearesidentofCanadaforaminimumofoneyearbeforeapplication.Theymustprovideacopyoftheiremploymentcontractandworkvisaandconfirmtheyintendtoapplyfortheirpermanentresidentstatuswheneligible.

Ifthereismedicalhistoryrequiringtreatmentorfollow-up,weexpecttheclienttohaveamedicaldoctorinCanadabeforewecouldcanthem.

MaximumLTCIcoverageof$750perweekmaybeconsidered.

Other temporary residents (includingthoseonastudentvisa)

LTCIisnotavailable.

BackdatingWepermitbackdatingtosaveageuptoamaximumofthreemonths.

Backdatingisonlypermittedtoreducepremiumsasaresultofthelowerissueage.Apolicycannotbebackdatedinordertoapplyforcoveragethatwouldotherwisebeunavailable.

Forexample,wecannotbackdatetoage80toapplyforaSunLTCIpolicy.

Ifapolicyisbackdatedtoretainage,evidencerequirementsarebasedontheproposedinsuredperson’sactualageatthetimetheapplicationissubmitted.Forexample,iftheclientturned70inthelastthreemonths,theycanbackdatetoretainage69ratesbuttheevidencerequirementswouldbebasedontheiractualageof70.

20SUN LONG TERM CARE INSURANCE

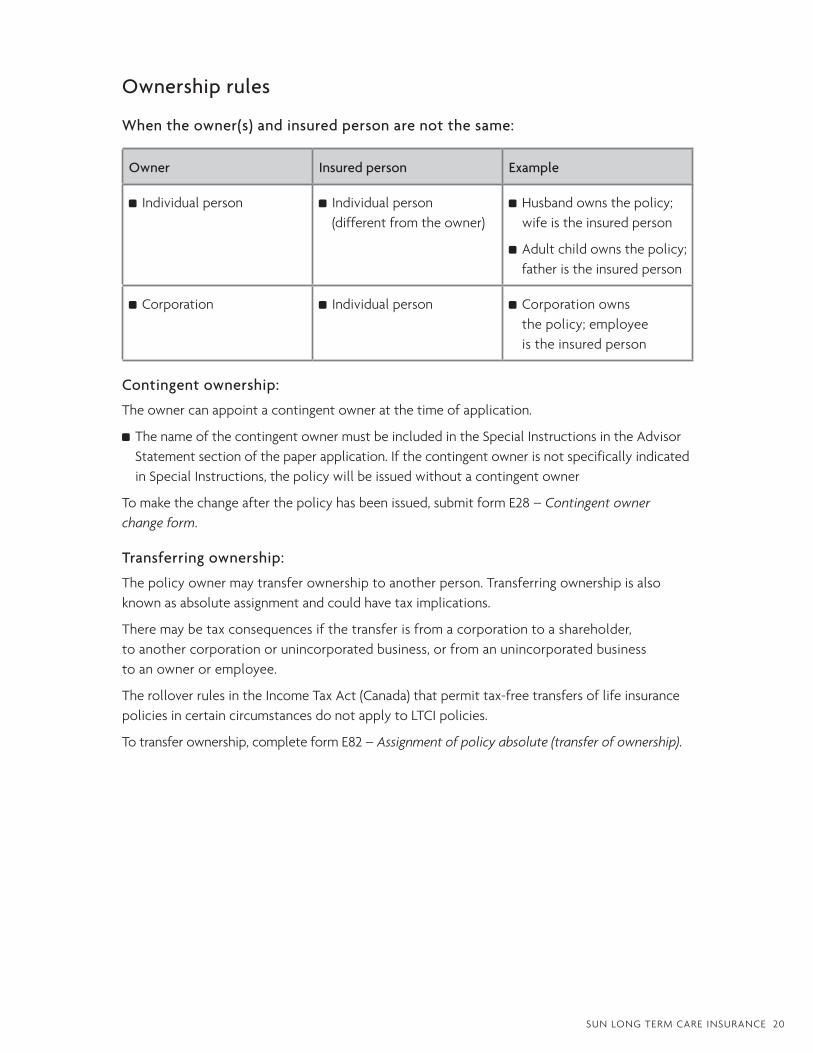

Ownership rules

When the owner(s) and insured person are not the same:

Owner Insured person Example

Individualperson Individualperson(differentfromtheowner)

Husbandownsthepolicy;wifeistheinsuredperson

Adultchildownsthepolicy;fatheristheinsuredperson

Corporation Individualperson Corporationownsthepolicy;employeeistheinsuredperson

Contingent ownership:

Theownercanappointacontingentowneratthetimeofapplication.

ThenameofthecontingentownermustbeincludedintheSpecialInstructionsintheAdvisorStatementsectionofthepaperapplication.IfthecontingentownerisnotspecificallyindicatedinSpecialInstructions,thepolicywillbeissuedwithoutacontingentowner

Tomakethechangeafterthepolicyhasbeenissued,submitformE28–Contingentownerchangeform.

Transferring ownership:

Thepolicyownermaytransferownershiptoanotherperson.Transferringownershipisalsoknownasabsoluteassignmentandcouldhavetaximplications.

Theremaybetaxconsequencesifthetransferisfromacorporationtoashareholder,toanothercorporationorunincorporatedbusiness,orfromanunincorporatedbusinesstoanowneroremployee.

TherolloverrulesintheIncomeTaxAct(Canada)thatpermittax-freetransfersoflifeinsurancepoliciesincertaincircumstancesdonotapplytoLTCIpolicies.

Totransferownership,completeformE82–Assignmentofpolicyabsolute(transferofownership).

21SUN LONG TERM CARE INSURANCE

Who receives payment

Claim payment

Theweeklybenefitispaidtothepolicyownerorthepolicyowner’sestate.

Return of premium on death (ROPD)

TheROPDbeneficiarypayeecanbedesignatedwhencompletingtheapplication.ThenameofthebeneficiarymustbeincludedintheSpecialInstructionssectionofthepaperapplication.Indicatethefullname(s)oftheROPDbeneficiary(ies)(withapercentage,ifapplicable),therelationshiptotheinsuredpersonforCommonlawpolicies(orpolicyownerforQuebec),andifnamingaspouse,indicatewhethertheappointmentisrevocableorirrevocable.Ifthisisnotspecifiedontheapplication,theROPDbeneficiarywillbetheownerorestateoftheowner.

FuturechangescanbesubmittedinwritingtoSunLifeFinancial’sheadoffice.Therequestmustincludethepolicyowner’sname,policynameandnumberandnewbeneficiaryappointment(asabove).Therequestmustbesignedanddatedbythepolicyowner.Ifthebeneficiarywasirrevocable,theymustalsosigngivingtheirconsenttochange.

Completing the applicationCompletetheSunLifeFinancialpaperapplication,form810-3523(English)or820-3523(French),availableonwww.sunlife.ca/advisororfromyourRegionalSalesDirector.Pleaserefertotheinstructionsonthefrontcoveroftheapplication.

PleasesubmittheoriginalcopytoSunLifeFinancialthroughyourMGAorNationalAccountofficeorbackoffice.

Supportingdocumentsyoumaywishtoincludeare:

illustration, coveringletterormemowithdetailsofthesale,and completedunderwritingquestionnaire,ifapplicable

Oncetheapplicationisreceived,itwillbeassignedtoanunderwriter.Applicationstatuscanbecheckedonwww.sunlife.ca/advisor.Ifyouneedassistance,pleasecallourAdvisorServiceCentreat1800-800-4SUN(4786).

PaymentsDependingonthepremiumfrequencychosenbytheclient,paymentscanbemadeonamonthlybasisthroughourpre-authorizedchequing(PAC)processorannuallybycheque.

IfPACischosen,monthlypaymentsaredeductedautomaticallyfromthepayor’sbankaccountandappliedtothepremiumowing.Monthlypremiumsarecalculatedbymultiplyingtheannualpremium(includingthe$150policyfee)by0.09(themodalfactor).

Forexample,aSunLTCIpolicywithanannualpremiumof$3,000willhaveamonthlypremiumof$270.

Monthlypremium:$3,000x.09=$270

Ifthepolicyownerchoosestopayannuallybycheque,paymentscanberemittedtoourheadofficebeforethepolicyanniversarydate.Anannualstatementissenttotheownerapproximatelythreeweeksbeforethepolicyanniversary,remindingthemthattheirannualpremiumisdue.

22SUN LONG TERM CARE INSURANCE

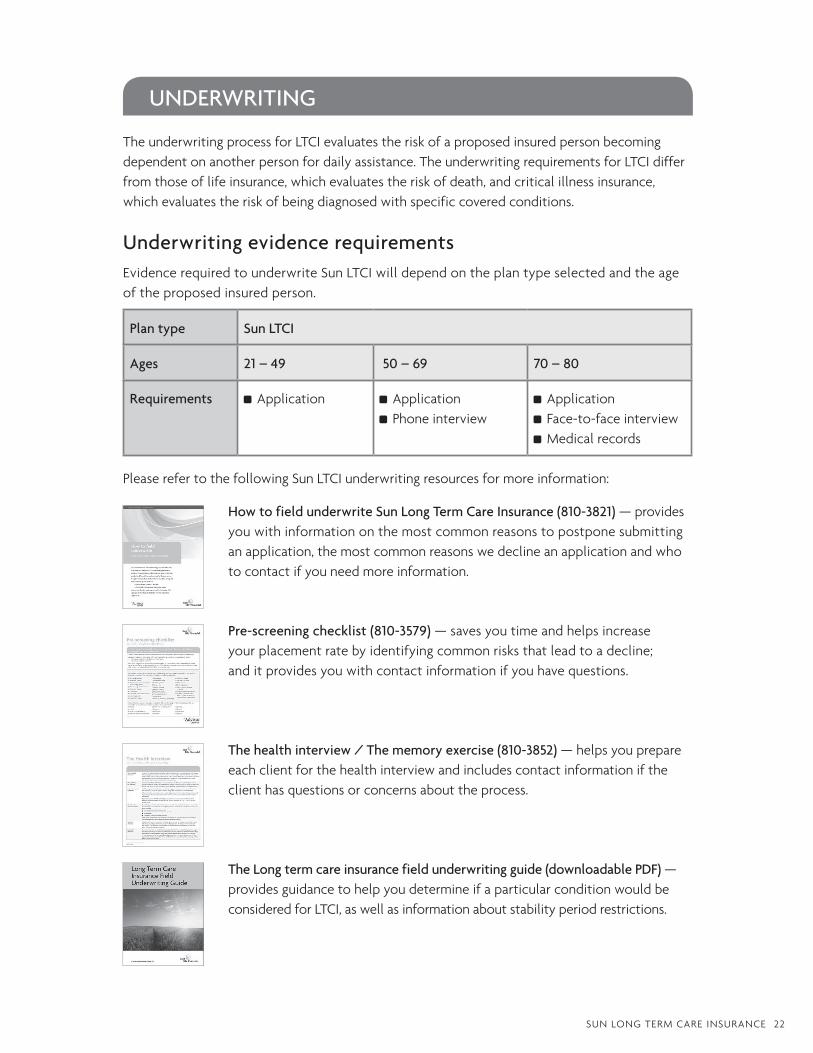

TheunderwritingprocessforLTCIevaluatestheriskofaproposedinsuredpersonbecomingdependentonanotherpersonfordailyassistance.TheunderwritingrequirementsforLTCIdifferfromthoseoflifeinsurance,whichevaluatestheriskofdeath,andcriticalillnessinsurance,whichevaluatestheriskofbeingdiagnosedwithspecificcoveredconditions.

Underwriting evidence requirementsEvidencerequiredtounderwriteSunLTCIwilldependontheplantypeselectedandtheageoftheproposedinsuredperson.

Plan type Sun LTCI

Ages 21 – 49 50 – 69 70 – 80

Requirements Application Application Phoneinterview

Application Face-to-faceinterview Medicalrecords

PleaserefertothefollowingSunLTCIunderwritingresourcesformoreinformation:

UNDERWRITING

How to field underwrite Sun Long Term Care Insurance (810-3821)—providesyouwithinformationonthemostcommonreasonstopostponesubmittinganapplication,themostcommonreasonswedeclineanapplicationandwhotocontactifyouneedmoreinformation.

Pre-screening checklist (810-3579)—savesyoutimeandhelpsincreaseyourplacementratebyidentifyingcommonrisksthatleadtoadecline;anditprovidesyouwithcontactinformationifyouhavequestions.

The health interview / The memory exercise (810-3852)—helpsyouprepareeachclientforthehealthinterviewandincludescontactinformationiftheclienthasquestionsorconcernsabouttheprocess.

The Long term care insurance field underwriting guide (downloadable PDF) —providesguidancetohelpyoudetermineifaparticularconditionwouldbeconsideredforLTCI,aswellasinformationaboutstabilityperiodrestrictions.

23SUN LONG TERM CARE INSURANCE

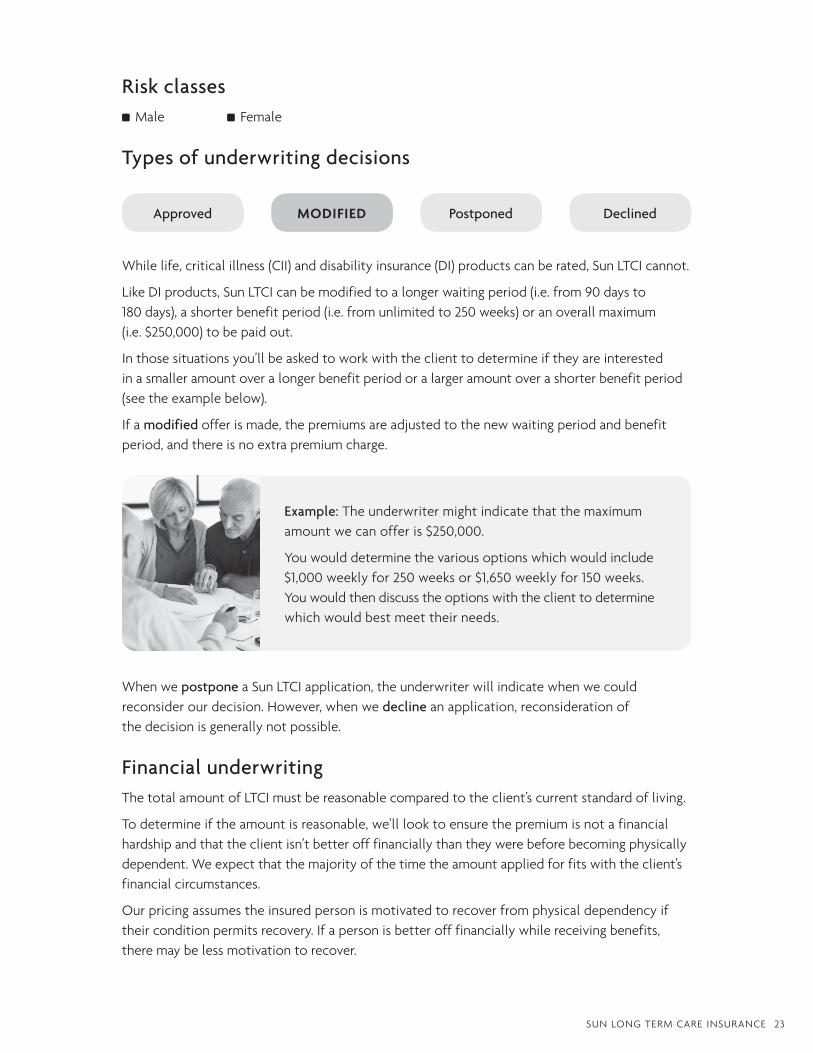

Risk classes Male Female

Types of underwriting decisions

Whilelife,criticalillness(CII)anddisabilityinsurance(DI)productscanberated,SunLTCIcannot.

LikeDIproducts,SunLTCIcanbemodifiedtoalongerwaitingperiod(i.e.from90daysto180days),ashorterbenefitperiod(i.e.fromunlimitedto250weeks)oranoverallmaximum(i.e.$250,000)tobepaidout.

Inthosesituationsyou’llbeaskedtoworkwiththeclienttodetermineiftheyareinterestedinasmalleramountoveralongerbenefitperiodoralargeramountoverashorterbenefitperiod(seetheexamplebelow).

Ifamodifiedofferismade,thepremiumsareadjustedtothenewwaitingperiodandbenefitperiod,andthereisnoextrapremiumcharge.

Approved MODIFIED Postponed Declined

Example:Theunderwritermightindicatethatthemaximumamountwecanofferis$250,000.

Youwoulddeterminethevariousoptionswhichwouldinclude$1,000weeklyfor250weeksor$1,650weeklyfor150weeks.Youwouldthendiscusstheoptionswiththeclienttodeterminewhichwouldbestmeettheirneeds.

WhenwepostponeaSunLTCIapplication,theunderwriterwillindicatewhenwecouldreconsiderourdecision.However,whenwedeclineanapplication,reconsiderationofthedecisionisgenerallynotpossible.

Financial underwritingThetotalamountofLTCImustbereasonablecomparedtotheclient’scurrentstandardofliving.

Todetermineiftheamountisreasonable,we’lllooktoensurethepremiumisnotafinancialhardshipandthattheclientisn’tbetterofffinanciallythantheywerebeforebecomingphysicallydependent.Weexpectthatthemajorityofthetimetheamountappliedforfitswiththeclient’sfinancialcircumstances.

Ourpricingassumestheinsuredpersonismotivatedtorecoverfromphysicaldependencyiftheirconditionpermitsrecovery.Ifapersonisbetterofffinanciallywhilereceivingbenefits,theremaybelessmotivationtorecover.

24SUN LONG TERM CARE INSURANCE

Whencompletinganapplication,youwillbeaskedforthetotalannualincomeandnetworthfortheproposedinsuredpersonandtheirspouse/partner,ifapplicable.Makingsuretheamountappliedforisalignedwiththeclient’sfinancialsituationwillhelpyousubmitqualitybusinessandmaintainyourreferralrelationships.

Bankruptcy (personal/business bankruptcy, current not yet discharged)

Inthissituation,thefollowingfactorsaretakenintoaccountwhenconsideringeligibility:

Stableemployment

Aminimumgrossannualsalaryof$30,000

Ifself-employedusegrossincomelessbusinessexpenses

Ifapplicationsarereceivedonbothspouses,onewithbankruptcynotyetdischargedandtheothernotworking,aminimumgrossannualsalaryof$60,000

Maximumweeklybenefitamountof$500forallapplicants

Unlimitedbenefits,ifallisfavourable;otherwise,wemayconsiderareducedbenefitamount

AllpremiumsmustbepaidinCanadianfundsanddrawnfromanaccountataCanadianfinancialinstitution.

Premium frequency – monthly or annually

Monthly payments

Ifthepolicyownerchoosestopaymonthlybypre-authorizedchequing(PAC),monthlypaymentsaredeductedautomaticallyfromthepayor’sbankaccountandappliedtothepremiumowing.Monthlypremiumsarecalculatedbymultiplyingtheannualpremium(includinga$150policyfee)by0.09(themodalfactor).

PREMIUM DETAILS

Example:ASunLongTermCareInsurancepolicywithanannualpremiumof$3,000.00willhaveamonthlypremiumof$270.00.

25SUN LONG TERM CARE INSURANCE

Annual payment

Ifthepolicyownerchoosestopayannuallybycheque,paymentscanberemittedtoSunLifeFinancial’sheadofficebeforethepolicyanniversarydate.Anannualstatementissenttothepolicyownerapproximatelythreeweeksbeforethepolicyanniversarytoremindthemthattheirannualpremiumisdue.

Withdrawable premium fundIfwereceivemoremoneythanisowedinpremiums,wewillholdtheexcessamountinthewithdrawablepremiumfund.Wemaysetamaximumamountthatcanbeinthefund.Thisfundcanbeusedtopaypremiumsatanytime.

Theamountinthewithdrawablepremiumfundwillearninterestdaily.Wesettheinterestrateeachdaybasedonshort-terminterestrates.Interestearnedonthepremiumfundistaxable.

Themoneyfromthisfundcanbewithdrawnatanytime.Theremaybelimitsonwithdrawalamountsandwemaychargeafeeforthesewithdrawals.You’llbeinformedofanyrulesandlimitationswhenyousubmitawithdrawalrequest.

PleasecalltheAdvisorServiceCentreat1800-800-4SUN(4786)fordetails.

Premium payment options Theapplicantmustselectoneofthefollowing:

Premiumsarepayableforthelifetimeofthepolicy(untilthepolicyanniversaryfollowingthe100thbirthdayoftheinsuredperson,or

Premiumsarepayabletothelatestof25yearsortothepolicyanniversaryafterage65.

Premium guarantee ThepremiumshownonthePolicysummarywon’tchangeforthefirstfivepolicyyears.Afterthisperiod,wemayincreasethepremiumonapolicyanniversary.Ifwechangethepremium,wewilltellthepolicyownerinadvanceandthatpremiumisguaranteedforatleastanotherfivepolicyyears.

Anypremiumchangeisbasedontheinsuredperson’sageonthepolicydate.Wedonotconsidertheinsuredperson’shealthwhenwemakeapremiumchange.

Inthisscenario,thepurchasedateofthepolicywasJanuary20,2013.

2010 2015 2020 2025 2030

Premium

Year

After the 2018 (five year) policy anniversary: option to increase premium, but no

increase is applied at this point in time2022: premium increase occurs;

rates locked in for the next five years

Cycle can repeat2013: policy purchased

26SUN LONG TERM CARE INSURANCE

When we waive premiumsWhenweapproveaclaimforbenefits,wewaivepremiumsforthepolicy.Thepremiumsmustbepaiduntilwenotifythepolicyownerthatwe’veapprovedtheclaim.

Non-forfeiture provision (Extended term insurance)IfpremiumsarenotpaidandthepolicyhasbeenineffectforthenumberofyearssetoutintheExtendedterminsurancescheduleinthepolicy,thepolicywillautomaticallycontinueforaperiodoftime.Attheendofthatperiod,thepolicyends.

FormoredetailsaboutthisprovisionpleaseseeExtendedTermInsuranceonpage15.

Policy dateThepolicydateindicatedinthepolicyisthestartdateofthatpolicy.

Thepolicydateisthedatethepolicyisissued,ortheretainedagedateifrequested.

Pleaserefertotheadvisorsiteformoredetailsonpolicydeliveryrequirements.

When the insurance comes into effectThesepoliciescomeintoeffectwhenallsettlerequirementsarereceivedandapproved.

ISSUING A SUN LTCI POLICY

27SUN LONG TERM CARE INSURANCE

Changing coverage options Thereareavarietyofchangespossibleincluding:

decreasingtheweeklybenefitamount, decreasingthebenefitperiod, lengtheningthewaitingperiod, changingtheinflationprotectionoptionfromtwopercent/threepercenttozeropercent/threepercent,

decreasingthebenefitamountattributedtoinflationprotectionincreases,and changingthepremiumpaymentfrequency.

TorequestanyofthesechangesuseformE220–Changeform–Longtermcareinsurance.

Wedeterminetheminimumbenefitamountthatmustremainineffect.

Terminating an optionItispossibletoterminateanoption,suchas:

Inflationprotection,or OptionalReturnofpremiumondeath.

TorequestthisuseformE220–Changeform–Longtermcareinsurance.

ConversionsSunLongTermCareInsurancedoesn’thaveanyconversionoptions.

Internal replacementsAninternalreplacementallowsforaplanchangeoutsideofthecontractualright.Undermostcircumstances,evidenceofinsurabilitymustbesubmittedforinternalreplacements.Anewapplicationisalwaysrequired.Quebecspecific-InQuebec,advisorsmustfollowthereplacementprocedure.

Examplesofinternalreplacementsinclude:

increasingthebenefitamount, increasingthebenefitperiod, shorteningthewaitingperiod, addingoptionalReturnofpremiumondeath(ROPD), addingInflationprotection, changingInflationprotectionbenefitfromzeropercent/threepercentwhilereceivingbenefitstotwopercent/threepercentwhilereceivingbenefits,and

lengtheningpremiumpaymentperiod.

PLAN CHANGES

28SUN LONG TERM CARE INSURANCE

Note:Becausethisisnotacontractualright,therulesforinternalreplacementsmaychange.

Exception–AninternalreplacementwithoutevidenceispossibleforSunLTCIinthefollowingscenarios:

Ifthenewapplicationisexactlythesameastheoldoneexcepttheclientwishesto:

a)Shortenthepremiumpaymentperiod.

b)Shortenthepremiumpaymentperiodincombinationwithanyofthefollowing:

− Iftheoriginalpolicy(eitherClaricaorSunLife)hasROPD,nounderwritingisrequiredtohaveROPDonthenewpolicy.

− IftheoriginalpolicyisaSunLifeFinancialplanwithInflationprotection,nounderwritingisrequiredtohaveInflationprotectiononthenewpolicy.

− Iftheoriginalpolicy(eitherClaricaorSunLife)hasaccumulatedInflationprotectionamountsandtheclientselectsaplanamounttotallingtheexistingbasebenefitplusanyaccumulatedamountsforthenewpolicy,nounderwritingisrequired.(Example:Theexistingpolicyhasa$500basebenefitwith$75.00add-inInflationprotectionaccumulation,thenewplancanhave$575.00withnounderwritingrequired).

ReinstatementsTherequiredpremiumsforthepolicymustbepaidbytheduedate.Ifpremiumsarenotpaidwhendue,wewillwithdrawtheunpaidpremiumfromthewithdrawablepremiumfundifithassufficientfunds.

Thepolicywillendif:

premiumsarenotreceivedbeforetheendofthe31stdayaftertheyaredue, thereareinsufficientfundsinthewithdrawablepremiumfund,and extendedterminsuranceisnotavailable.

Ifthepolicyendsthisway,itiscalledalapse.Ifthepolicyendedbecauseitlapsed,thepolicyownercanapplytohaveitputbackintoeffect(reinstated)iftheinsuredpersonisalive.

Toreinstatethepolicy,thepolicyownermust:

applywithintwoyearsofthedatethepolicyended, providenewevidenceofinsurabilitythatweconsidersatisfactory,and makeapaymentequaltothereinstatementchargeweset.

Ifwedon’tapprovetheapplication,werefundtheamountpaidtoputthepolicybackintoeffect.

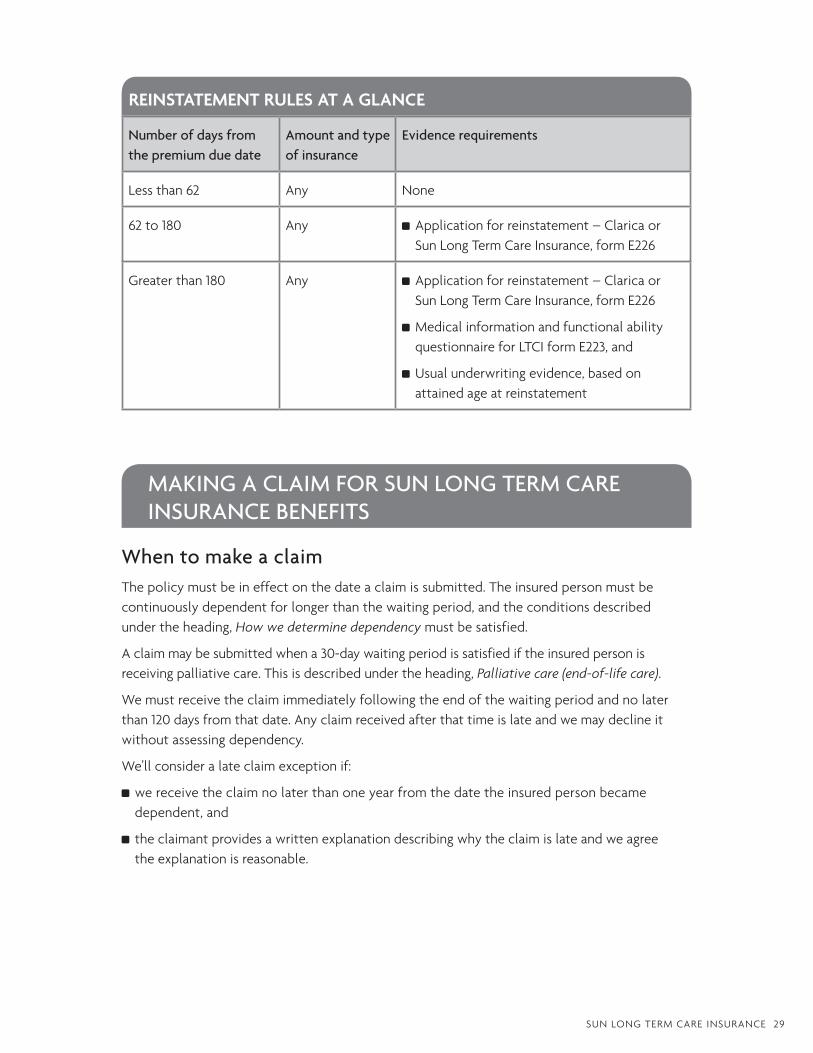

29SUN LONG TERM CARE INSURANCE

Number of days from the premium due date

Amount and type of insurance

Evidence requirements

Lessthan62 Any None

62to180 Any Applicationforreinstatement–ClaricaorSunLongTermCareInsurance,formE226

Greaterthan180 Any Applicationforreinstatement–ClaricaorSunLongTermCareInsurance,formE226

MedicalinformationandfunctionalabilityquestionnaireforLTCIformE223,and

Usualunderwritingevidence,basedonattainedageatreinstatement

REINSTATEMENT RULES AT A GLANCE

MAKING A CLAIM FOR SUN LONG TERM CARE INSURANCE BENEFITS

When to make a claimThepolicymustbeineffectonthedateaclaimissubmitted.Theinsuredpersonmustbecontinuouslydependentforlongerthanthewaitingperiod,andtheconditionsdescribedundertheheading,Howwedeterminedependencymustbesatisfied.

Aclaimmaybesubmittedwhena30-daywaitingperiodissatisfiediftheinsuredpersonisreceivingpalliativecare.Thisisdescribedundertheheading,Palliativecare(end-of-lifecare).

Wemustreceivetheclaimimmediatelyfollowingtheendofthewaitingperiodandnolaterthan120daysfromthatdate.Anyclaimreceivedafterthattimeislateandwemaydeclineitwithoutassessingdependency.

We’llconsideralateclaimexceptionif:

wereceivetheclaimnolaterthanoneyearfromthedatetheinsuredpersonbecamedependent,and

theclaimantprovidesawrittenexplanationdescribingwhytheclaimislateandweagreetheexplanationisreasonable.

30SUN LONG TERM CARE INSURANCE

How to make a claim

Step 1: Notify us

Contact us–Tomakeaclaim,theclaimantshouldcontactSunLifeFinancialusingthetollfreenumberlistedintheirpolicy.Thisnumberis1877-SUN-LIFE(786-5433).Wewillthensendtheappropriateclaimformtobecompleted.YoucancallIndividualClaimsServicestollfreeat1800-800-4SUN(4786)[email protected].

Form–Thepersonmakingtheclaimmustcompletetheform(s)andgiveustheinformationweneedtoassesstheclaim.

TheinsuredpersonmustbeinCanadaortheUnitedStatesatthetimeaclaimismade.Iftheyarenot,theymustreturntobeassessedbyaphysicianlicensedandpractisinginCanadaortheUnitedStates.

Beforeweapprovetheclaim,theinsuredperson’sdateofbirthmustbeverified.Ifthedateofbirthgivenontheapplicationisincorrect,we’lladjusttheamountwepaytoreflecttheinsuredperson’scorrectage.

Pay premiums–Policypremiumsmustcontinuetobepaiduntilweadvisethatwe’veapprovedtheclaim.

Send forms–Theform(s)andinformationmustbesentto:

IndividualClaimsServicesSunLifeAssuranceCompanyofCanada227KingStS,POBox1601,StnWaterlooWaterlooONCanadaN2J4C5

Fees–Physiciansmaychargeafeetocompletecertainforms.Thepersonmakingtheclaimisresponsibleforanyfeesforthisinformation.

Step 2: Collection of medical information

Information we need–Theclaimantmustgiveustheinformationweneedtoassesstheclaim.Thisincludesourformwhichmustbecompletedbyaphysicianoranotherhealthcareprofessionalacceptabletous.Thephysicianmustdescribetheinsuredperson’smedicalcondition,limitationsandfunctionalabilitiesandprovideobjectivemedicalinformationabouttheirdependence.

Additional information–We’lladviseifweneedanyotherinformationtoassesstheclaim.Thiscouldincludemedicalrecords,clinicaltests,physiotherapyreports,psychologicaltestsandanyotherobjectivemedicalinformationthatsupportstheclaim.

Fees–Anyfeeschargedbyphysicianstocompleteformsorprovideinformationaretheclaimant’sresponsibility.

31SUN LONG TERM CARE INSURANCE

Doctors–Physicians,specialistsorhealthcarepractitionerswhoprovideinformationtousmustbelicensedandpractisinginCanadaortheUnitedStates.Theymaynotbethepolicyowner,insuredperson,anyoneentitledtomakeaclaimunderthispolicy,oranyrelativeorbusinessassociateofthesepeople.

Documentation by us–Wemayrequiretheinsuredpersontobeexaminedbyanyhealthcarepractitionersthatweappoint.Thesemaybelicensedphysicians,physiotherapists,occupationaltherapists,psychiatrists,psychologistsorothers.Wepayfortheseexaminations.

Wemayalsorequiretheinsuredpersontoauthorizeustogatheranduseinformationfromotherinsurersorgovernmentagencies.

Step 3: Making the claims decision

Oncewereceiveallinformationwerequire,wewillassesstheinformationandmakeadecision.Wecommunicatethisdecisionandpaythebenefittothepolicyownerortheestate,ifapplicable.

Ifwedenyaclaim,wesendaletterexplainingthedecisiontothepolicyowner.Ifthepolicyownerandtheinsuredpersonarenotthesameperson,wewillsendtwodeclineletters:

onelettertotheclaimant,fullyexplainingourpolicydecision,and asecondlettertothepolicyowner,confirmingourdenialoftheclaim.Nomedicalinformationisgiventothepolicyownerforprivacyreasons.

TocontacttheIndividualClaimsServicesdepartment,use:

Email:[email protected]:1800-800-4SUN(4786)Fax:1866-487-4745

Exclusions and limitationsThepolicyendsandbenefitsarenotpayableiftheinsuredperson’sdependencystartedbeforethelaterof:

themostrecentdateanapplicationforthispolicywassigned, thepolicydateshownundertheheadingPolicysummary,or themostrecentdatethispolicywasputbackintoeffect,ifthepolicyhasbeenreinstated.

Wewon’tpaybenefitswhentheinsuredpersonisoutsideCanadaortheUnitedStatesformorethaneightconsecutiveweeks.Ifwe’vepaidbeyondtheeightconsecutiveweeklimitation,wehavetherighttodeducttheoverpaymentfromanyfuturebenefits.

Wewon’tpaybenefitsiftheinsuredperson’sdependencyisdirectlyorindirectlycausedbyorassociatedwiththeinsuredpersonoperatingavehiclewhiletheirbloodalcohollevelismorethan80milligramsofalcoholper100millilitresofblood.Avehicleincludesanyformofground,airormarinetransportationthatcanbeputintomotionbyanymeans,includingmuscularpower.Wedonottakeintoaccountwhetherornotthevehicleisinmotion.

–competitiveadvantage

32SUN LONG TERM CARE INSURANCE

Wewon’tpaybenefitsiftheinsuredperson’sdependencyisdirectlyorindirectlycausedbyorassociatedwiththeinsuredperson:

committingorattemptingtocommitacriminaloffence,

attemptingtotaketheirownlife,regardlessofwhethertheinsuredpersonhasamentalillnessorunderstandsorintendstheconsequencesoftheiraction(s),

causingthemselfbodilyinjury,regardlessofwhethertheinsuredpersonhasamentalillnessorunderstandsorintendstheconsequencesoftheiraction(s),

intentionallytakinganydrugotherthanasprescribedbyalicensedmedicalpractitionerandinaccordancewiththeinstructionsgiven,and/or

intentionallytakinganyintoxicant,narcoticorpoisonoussubstance.Thisdoesnotincludesmokingcigarettes,cigarillos,cigars,chewingtobaccooroccasionaluseofalcohol.

Wewon’tpaybenefitsiftheinsuredperson’sdependencyisdirectlyorindirectlycausedbyorassociatedwithcivildisorderorwar,whetherdeclaredornot.

Tips for an efficient claims process Makesureyouunderstandtheclaimtriggersandthattheinsuredpersonmeetsthedefinitionofdependenceasdefinedbythecontract.Thiswillhelpreduceineligibleclaims,setbetterexpectationsfortheinsuredpersonandreducepotentialexpenses.

Verifythewaitingperiodsetoutinthepolicy.Afterthewaitingperiodhasbeenmet,completeandsubmittheclaimform.

Makesuretheformiscomplete,signedanddatedbeforeyousubmitit.Youneedtoinclude:

− thefulladdress(includingpostalcode)ofalldoctorstheinsuredpersonhasconsulted,and− thephonenumberofalldoctorstheinsuredpersonhasconsulted.

Verifytheinsuredperson’sdateofbirthandcheckitagainstthatshowninthepolicy.

Itisimportantthatweobtainallmedicalreportsfromthephysiciantosupporttheclaim.Ifthereportsarenotsenttous,wecannotdoafullevaluationandthiswillcausedelays.

33SUN LONG TERM CARE INSURANCE

TAXATION

TherearenospecifictaxlawsgoverningLTCIpolicies.

BasedoncurrenttaxlawsandguidancefromtheCanadaRevenueAgency,weexpectthat:

Premiumspaidforalongtermcareinsurancepolicyownedbyanindividualorindividualswillnotbetaxdeductible.

Anycashbenefitspaidfromalongtermcareinsurancepolicywillbetax-freewhenthepolicyownerandbenefitpayeearethesame.

Ifthepolicyisownedbyacorporation,differenttaxlawsmayapplytosomecircumstances:

Premiumspaidforalongtermcareinsurancepolicyownedbyacorporationwillnotbetaxdeductible,exceptinstrictlylimitedcircumstancesthatarebeyondthescopeofthisguide.

Anycashbenefitspaidfromalongtermcareinsurancepolicywillbetax-freewhenthepolicyownerandbenefitpayeearethesame.

Paymentofanypartofthecashbenefitfromthecorporationoranunincorporatedbusinesstoanemployeeorshareholdercouldproducetaxconsequencesfortherecipient.

Sincelongtermcareinsuranceisnotlifeinsurance,nopartofthelongtermcareinsurancebenefitthatacorporationreceivescanbepaidtoitsshareholdersasatax-freecapitaldividend.

Ifthecorporationtransfersownershipofalongtermcareinsurancepolicytooneofitsshareholdersoremployees,theremaybetaxconsequencesfortherecipient.

Theforegoingisonlyageneralsummary.Ataxprofessionalshouldbeconsultedformoreinformation.FormoreinformationconsulttheCanadianHealthInsuranceTaxGuide:www.sunlife.ca/advisor/HealthTaxGuide

34SUN LONG TERM CARE INSURANCE

Clarica Long Term Care Insurance (Dec. 4, 2000 to Dec. 11, 2003)

Issue ages 31–80

Coverage type Comprehensive

Whentheinsuredpersonqualifiesforthisincome-stylebenefit,wepayitnomatterwheretheyliveorreceivecarewithinCanadaortheUnitedStates.

Withincome-stylebenefits,clientsdonotneedtosubmitreceiptstoreceivetheirweeklybenefit;theycanusethemoneyhowevertheychoose.

Claim triggers Aclaimispaidwhentheinsuredperson:

alwaysneedssubstantialphysicalassistancefromanotherpersontocompletetwoormoreoftheactivitiesofdailyliving(bathing,dressing,toileting,movingtoorfromabedorchair,continence,andfeeding),or

hasdeterioratedmentalability.

Weekly benefit amounts

Minimum$150 Maximum$2,000

Waiting periods 30days 90days 180days

Benefit periods 100weeks 150weeks

250weeks 500weeks Unlimited

Payment period options

15years 20years Lifetime

Return of premium on death (ROPD)

Thereturnableamountisbasedonhowlongthepolicyhasbeeninforce.

Claimsaresubtractedfromthereturnableamount.

Thereisnoreturnofpremiumifthepolicyisonextendedtermcoverage.

PLAN DETAILS

PRODUCT HISTORY

Inforceproductnolongersold

35SUN LONG TERM CARE INSURANCE

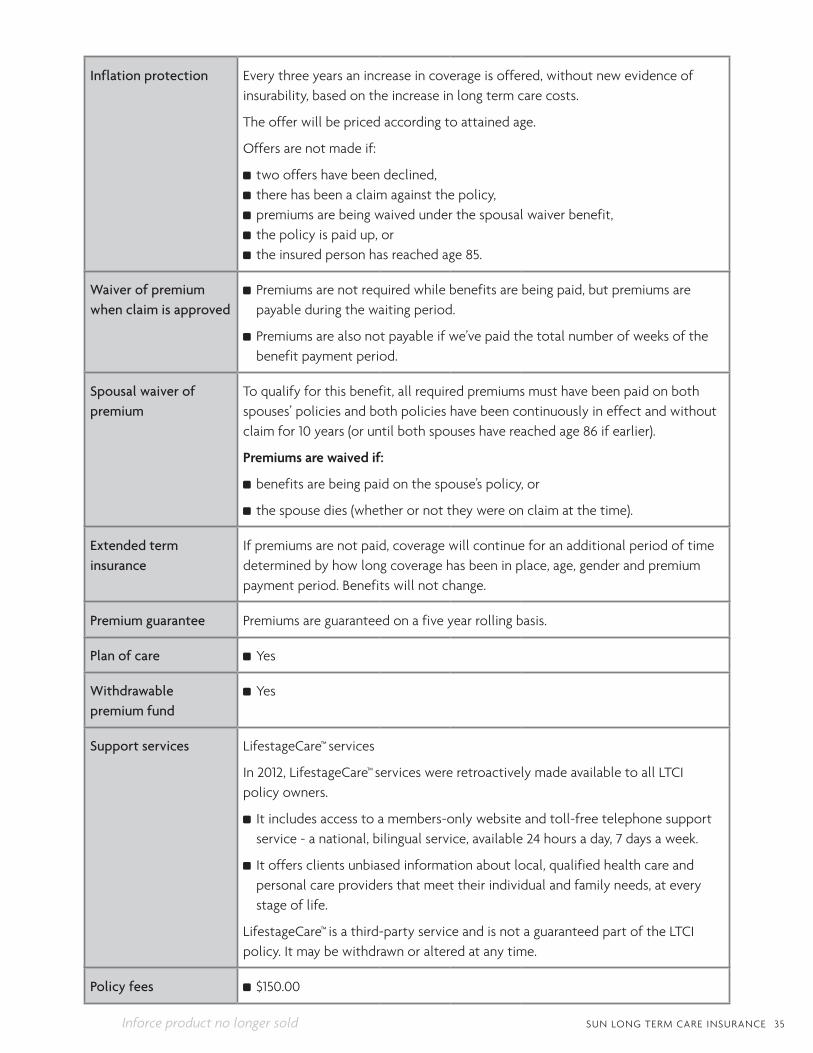

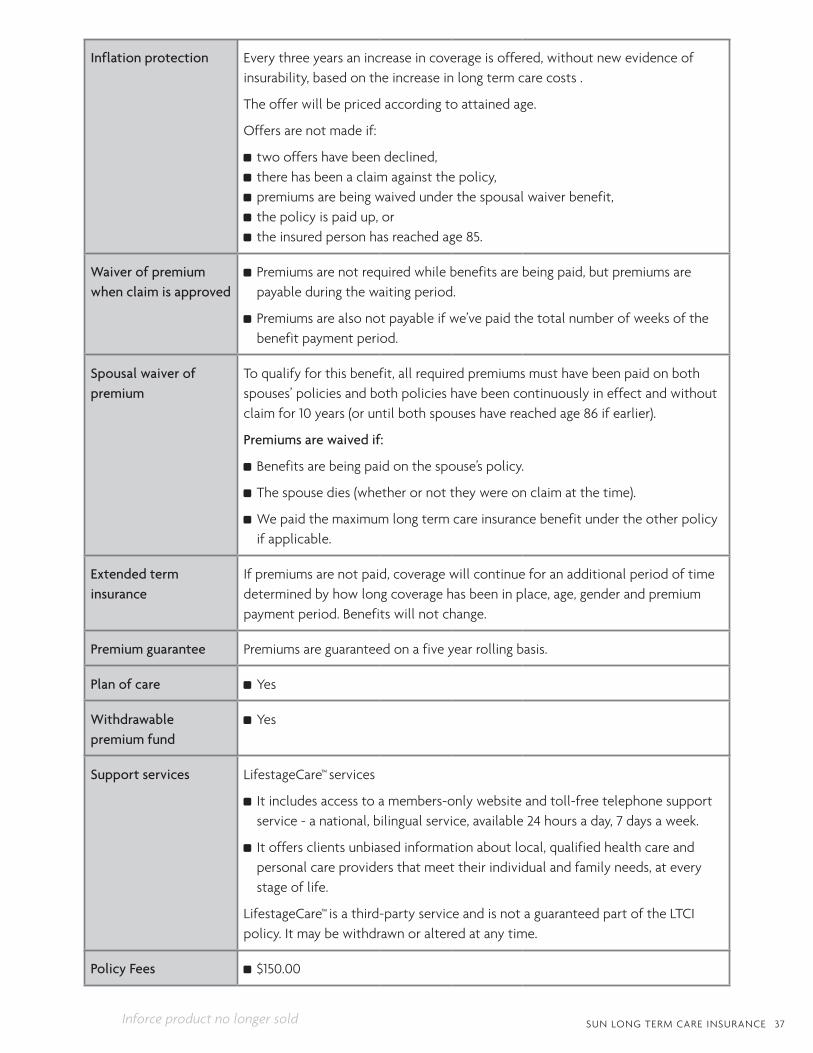

Inflation protection Everythreeyearsanincreaseincoverageisoffered,withoutnewevidenceofinsurability,basedontheincreaseinlongtermcarecosts.

Theofferwillbepricedaccordingtoattainedage.

Offersarenotmadeif:

twooffershavebeendeclined, therehasbeenaclaimagainstthepolicy, premiumsarebeingwaivedunderthespousalwaiverbenefit, thepolicyispaidup,or theinsuredpersonhasreachedage85.

Waiver of premium when claim is approved

Premiumsarenotrequiredwhilebenefitsarebeingpaid,butpremiumsarepayableduringthewaitingperiod.

Premiumsarealsonotpayableifwe’vepaidthetotalnumberofweeksofthebenefitpaymentperiod.

Spousal waiver of premium

Toqualifyforthisbenefit,allrequiredpremiumsmusthavebeenpaidonbothspouses’policiesandbothpolicieshavebeencontinuouslyineffectandwithoutclaimfor10years(oruntilbothspouseshavereachedage86ifearlier).

Premiums are waived if:

benefitsarebeingpaidonthespouse’spolicy,or

thespousedies(whetherornottheywereonclaimatthetime).

Extended term insurance

Ifpremiumsarenotpaid,coveragewillcontinueforanadditionalperiodoftimedeterminedbyhowlongcoveragehasbeeninplace,age,genderandpremiumpaymentperiod.Benefitswillnotchange.

Premium guarantee Premiumsareguaranteedonafiveyearrollingbasis.

Plan of care Yes

Withdrawable premium fund

Yes

Support services LifestageCare™services

In2012,LifestageCare™serviceswereretroactivelymadeavailabletoallLTCIpolicyowners.

Itincludesaccesstoamembers-onlywebsiteandtoll-freetelephonesupportservice-anational,bilingualservice,available24hoursaday,7daysaweek.

Itoffersclientsunbiasedinformationaboutlocal,qualifiedhealthcareandpersonalcareprovidersthatmeettheirindividualandfamilyneeds,ateverystageoflife.

LifestageCare™isathird-partyserviceandisnotaguaranteedpartoftheLTCIpolicy.Itmaybewithdrawnoralteredatanytime.

Policy fees $150.00

Inforceproductnolongersold

36SUN LONG TERM CARE INSURANCE

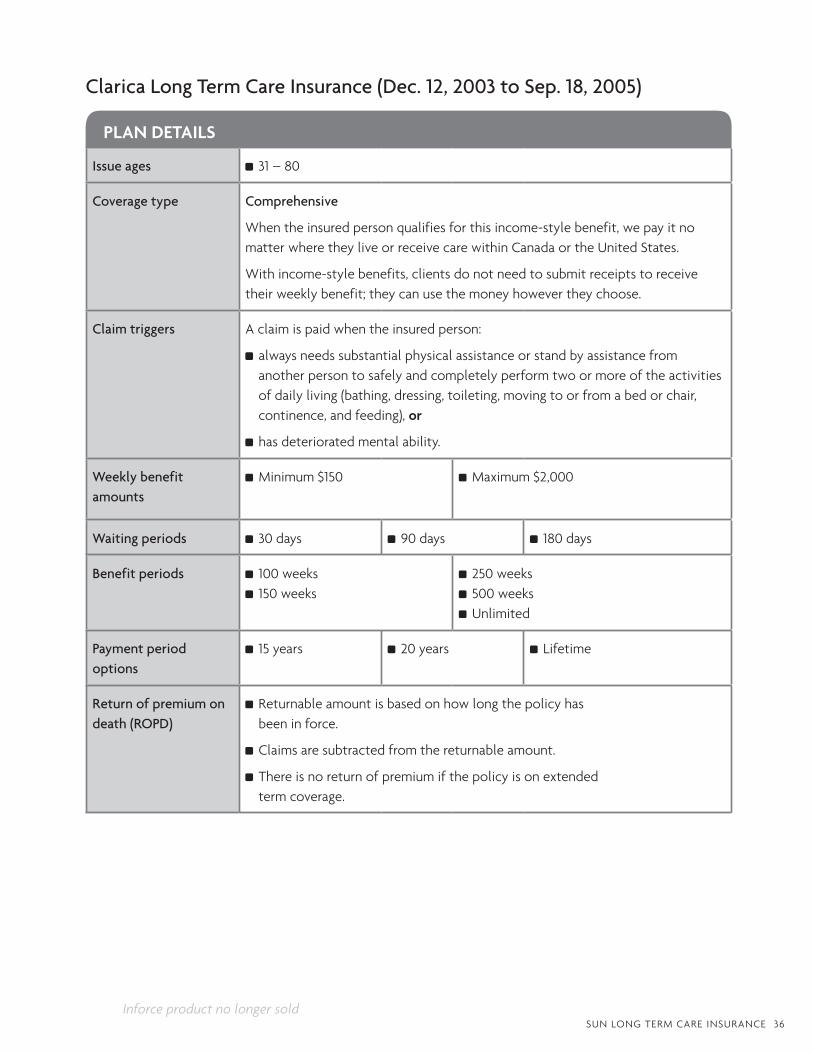

Clarica Long Term Care Insurance (Dec. 12, 2003 to Sep. 18, 2005)

Issue ages 31–80

Coverage type Comprehensive

Whentheinsuredpersonqualifiesforthisincome-stylebenefit,wepayitnomatterwheretheyliveorreceivecarewithinCanadaortheUnitedStates.

Withincome-stylebenefits,clientsdonotneedtosubmitreceiptstoreceivetheirweeklybenefit;theycanusethemoneyhowevertheychoose.

Claim triggers Aclaimispaidwhentheinsuredperson:

alwaysneedssubstantialphysicalassistanceorstandbyassistancefromanotherpersontosafelyandcompletelyperformtwoormoreoftheactivitiesofdailyliving(bathing,dressing,toileting,movingtoorfromabedorchair,continence,andfeeding),or

hasdeterioratedmentalability.

Weekly benefit amounts

Minimum$150 Maximum$2,000

Waiting periods 30days 90days 180days

Benefit periods 100weeks 150weeks

250weeks 500weeks Unlimited

Payment period options

15years 20years Lifetime

Return of premium on death (ROPD)

Returnableamountisbasedonhowlongthepolicyhasbeeninforce.

Claimsaresubtractedfromthereturnableamount.

Thereisnoreturnofpremiumifthepolicyisonextendedtermcoverage.

Inforceproductnolongersold

PLAN DETAILS

37SUN LONG TERM CARE INSURANCE

Inflation protection Everythreeyearsanincreaseincoverageisoffered,withoutnewevidenceofinsurability,basedontheincreaseinlongtermcarecosts.

Theofferwillbepricedaccordingtoattainedage.

Offersarenotmadeif:

twooffershavebeendeclined, therehasbeenaclaimagainstthepolicy, premiumsarebeingwaivedunderthespousalwaiverbenefit, thepolicyispaidup,or theinsuredpersonhasreachedage85.

Waiver of premium when claim is approved

Premiumsarenotrequiredwhilebenefitsarebeingpaid,butpremiumsarepayableduringthewaitingperiod.

Premiumsarealsonotpayableifwe’vepaidthetotalnumberofweeksofthebenefitpaymentperiod.

Spousal waiver of premium

Toqualifyforthisbenefit,allrequiredpremiumsmusthavebeenpaidonbothspouses’policiesandbothpolicieshavebeencontinuouslyineffectandwithoutclaimfor10years(oruntilbothspouseshavereachedage86ifearlier).

Premiums are waived if:

Benefitsarebeingpaidonthespouse’spolicy.

Thespousedies(whetherornottheywereonclaimatthetime).

Wepaidthemaximumlongtermcareinsurancebenefitundertheotherpolicyifapplicable.

Extended term insurance

Ifpremiumsarenotpaid,coveragewillcontinueforanadditionalperiodoftimedeterminedbyhowlongcoveragehasbeeninplace,age,genderandpremiumpaymentperiod.Benefitswillnotchange.

Premium guarantee Premiumsareguaranteedonafiveyearrollingbasis.

Plan of care Yes

Withdrawable premium fund

Yes

Support services LifestageCare™services

Itincludesaccesstoamembers-onlywebsiteandtoll-freetelephonesupportservice-anational,bilingualservice,available24hoursaday,7daysaweek.

Itoffersclientsunbiasedinformationaboutlocal,qualifiedhealthcareandpersonalcareprovidersthatmeettheirindividualandfamilyneeds,ateverystageoflife.

LifestageCare™isathird-partyserviceandisnotaguaranteedpartoftheLTCIpolicy.Itmaybewithdrawnoralteredatanytime.

Policy Fees $150.00

Inforceproductnolongersold

38SUN LONG TERM CARE INSURANCE

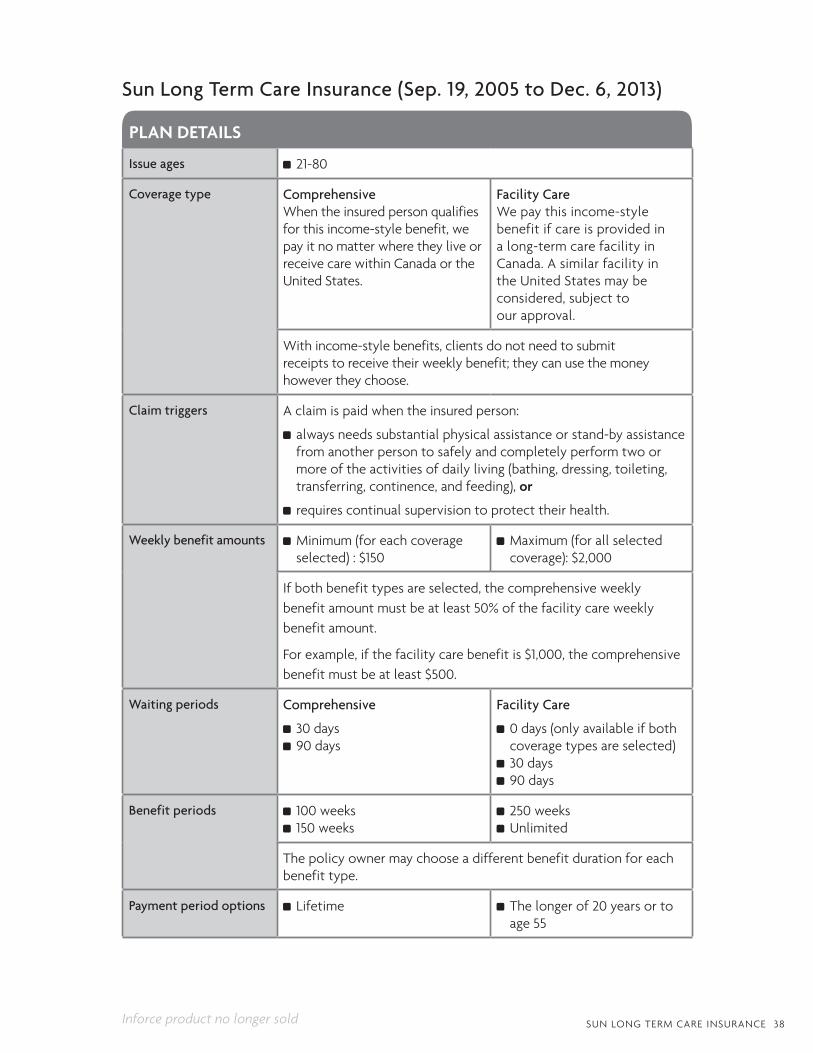

Sun Long Term Care Insurance (Sep. 19, 2005 to Dec. 6, 2013)

Issue ages 21-80

Coverage type ComprehensiveWhentheinsuredpersonqualifiesforthisincome-stylebenefit,wepayitnomatterwheretheyliveorreceivecarewithinCanadaortheUnitedStates.

Facility Care Wepaythisincome-stylebenefitifcareisprovidedinalong-termcarefacilityinCanada.AsimilarfacilityintheUnitedStatesmaybeconsidered,subjecttoourapproval.

Withincome-stylebenefits,clientsdonotneedtosubmitreceiptstoreceivetheirweeklybenefit;theycanusethemoneyhowevertheychoose.

Claim triggers Aclaimispaidwhentheinsuredperson:

alwaysneedssubstantialphysicalassistanceorstand-byassistancefromanotherpersontosafelyandcompletelyperformtwoormoreoftheactivitiesofdailyliving(bathing,dressing,toileting,transferring,continence,andfeeding),or

requirescontinualsupervisiontoprotecttheirhealth.

Weekly benefit amounts Minimum(foreachcoverageselected):$150

Maximum(forallselectedcoverage):$2,000

Ifbothbenefittypesareselected,thecomprehensiveweeklybenefitamountmustbeatleast50%ofthefacilitycareweeklybenefitamount.

Forexample,ifthefacilitycarebenefitis$1,000,thecomprehensivebenefitmustbeatleast$500.

Waiting periods Comprehensive

30days 90days

Facility Care

0days(onlyavailableifbothcoveragetypesareselected)

30days 90days

Benefit periods 100weeks 150weeks

250weeks Unlimited

Thepolicyownermaychooseadifferentbenefitdurationforeachbenefittype.

Payment period options Lifetime Thelongerof20yearsortoage55

Inforceproductnolongersold

PLAN DETAILS

39SUN LONG TERM CARE INSURANCE

Return of premium on death (ROPD)

Thisoptionalbenefitreturnsaportionofpremiumstotheownerofthepolicy(ortheowner’sestate)iftheinsuredpersondies.

Returnableamountisbasedonhowlongthepolicyhasbeeninforce.

Calculatedseparatelyforeachbenefittype.

Claimsaresubtractedfromthereturnableamount.

Doesnotincludepremiumsforinflationprotectionbenefit.

Ifbothbenefittypesareselected,thisoptionappliestoboth.

Inflation protection Option A

− Weeklybenefitincreasesby3%eachpolicyanniversary-thedatethepolicybecameeffective-whiletheweeklybenefitispayable.

Option B

− Weeklybenefitincreasesby2%eachpolicyanniversaryiftheweeklybenefitisnotpayable.

− Weeklybenefitincreasesby3%eachpolicyanniversarywhiletheweeklybenefitispayable.

Thesameoptionmustbechosenforbothbenefittypesbutitworksindependentlyforeach.

Increasesarecompoundedannually.

Nocaponincreases.

Benefitmaximummayexceed$2,000perweekduetoinflationprotectionincreases.

Waiver of premium when claim is approved

Premiumsarenotrequiredwhilebenefitsarebeingpaid,butpremiumsarepayableduringthewaitingperiod.

Premiumsarealsonotpayableifwe’vepaidthetotalnumberofweeksineitherthecomprehensiveorfacilitycarebenefitperiod.

Spousal waiver of premium

Toqualifyforthisbenefit,allrequiredpremiumsmusthavebeenpaidonbothspouses’policiesandbothpolicieshavebeencontinuouslyineffectandwithoutclaimfor10years(oruntilbothspouseshavereachedage86ifearlier).

Premiums are waived if:

Benefitsarebeingpaidonthespouse’spolicy.

We’vepaidthetotalnumberofweeksinthecomprehensiveorfacilitycarebenefitperiodforthespouse’spolicy.

Thespousedies(whetherornottheywereonclaimatthetime).

Inforceproductnolongersold

40SUN LONG TERM CARE INSURANCE

Extended term insurance Ifpremiumsarenotpaid,coveragemaycontinueforalimitedtimebasedon:

Basebenefittype(comprehensiveorfacilitycare) Ageatpurchase Gender Premiumpaymentperiod Thenumberofyearsthepolicyhasbeeninforce

Whileextendedterminsuranceisineffect:

Noreturnofpremiumondeathbenefitispaid Noinflationprotectionincreasesaremade

Premium guarantee Premiumsareguaranteedonafiveyearrollingbasis.

Plan of care Yes

Withdrawable premium fund

Yes

Support services LifestageCare™services

Itincludesaccesstoamembers-onlywebsiteandtoll-freetelephonesupportservice-anational,bilingualservice,available24hoursaday,7daysaweek.

Itoffersclientsunbiasedinformationaboutlocal,qualifiedhealthcareandpersonalcareprovidersthatmeettheirindividualandfamilyneeds,ateverystageoflife.

LifestageCare™isathird-partyserviceandisnotaguaranteedpartoftheLTCIpolicy.Itmaybewithdrawnoralteredatanytime.

Policy fees $150.00

Inforceproductnolongersold

41SUN LONG TERM CARE INSURANCE

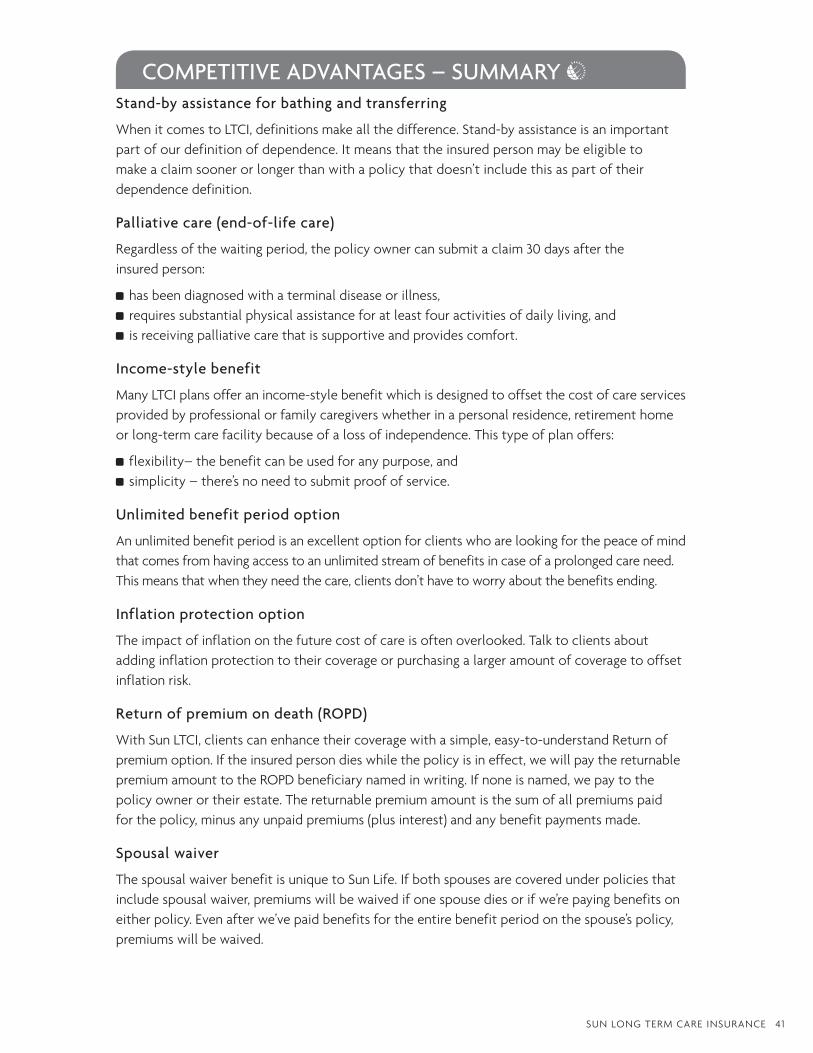

Stand-by assistance for bathing and transferring

WhenitcomestoLTCI,definitionsmakeallthedifference.Stand-byassistanceisanimportantpartofourdefinitionofdependence.Itmeansthattheinsuredpersonmaybeeligibletomakeaclaimsoonerorlongerthanwithapolicythatdoesn’tincludethisaspartoftheirdependencedefinition.

Palliative care (end-of-life care)

Regardlessofthewaitingperiod,thepolicyownercansubmitaclaim30daysaftertheinsuredperson:

hasbeendiagnosedwithaterminaldiseaseorillness, requiressubstantialphysicalassistanceforatleastfouractivitiesofdailyliving,and isreceivingpalliativecarethatissupportiveandprovidescomfort.

Income-style benefit

ManyLTCIplansofferanincome-stylebenefitwhichisdesignedtooffsetthecostofcareservicesprovidedbyprofessionalorfamilycaregiverswhetherinapersonalresidence,retirementhomeorlong-termcarefacilitybecauseofalossofindependence.Thistypeofplanoffers:

flexibility–thebenefitcanbeusedforanypurpose,and simplicity–there’snoneedtosubmitproofofservice.

Unlimited benefit period option

Anunlimitedbenefitperiodisanexcellentoptionforclientswhoarelookingforthepeaceofmindthatcomesfromhavingaccesstoanunlimitedstreamofbenefitsincaseofaprolongedcareneed.Thismeansthatwhentheyneedthecare,clientsdon’thavetoworryaboutthebenefitsending.

Inflation protection option

Theimpactofinflationonthefuturecostofcareisoftenoverlooked.Talktoclientsaboutaddinginflationprotectiontotheircoverageorpurchasingalargeramountofcoveragetooffsetinflationrisk.

Return of premium on death (ROPD)

WithSunLTCI,clientscanenhancetheircoveragewithasimple,easy-to-understandReturnofpremiumoption.Iftheinsuredpersondieswhilethepolicyisineffect,wewillpaythereturnablepremiumamounttotheROPDbeneficiarynamedinwriting.Ifnoneisnamed,wepaytothepolicyownerortheirestate.Thereturnablepremiumamountisthesumofallpremiumspaidforthepolicy,minusanyunpaidpremiums(plusinterest)andanybenefitpaymentsmade.

Spousal waiver

ThespousalwaiverbenefitisuniquetoSunLife.Ifbothspousesarecoveredunderpoliciesthatincludespousalwaiver,premiumswillbewaivedifonespousediesorifwe’repayingbenefitsoneitherpolicy.Evenafterwe’vepaidbenefitsfortheentirebenefitperiodonthespouse’spolicy,premiumswillbewaived.

COMPETITIVE ADVANTAGES – SUMMARY

42SUN LONG TERM CARE INSURANCE

Toqualifyforthebenefit,eachspousemusthaveapolicythathasbeencontinuouslyineffectwithnoapprovedclaimfromthedatestheycameintoeffectuntil:

bothpolicieshavereachedtheir10thpolicyanniversaries,or bothspouseshavehadtheir86thbirthdays.

First Payment bonus

Whenweapproveanewclaim,thefirstpaymentincludesabonusamountequalto12timestheweeklyamount.Iftheinsuredpersonisreceivingpalliativecareandqualifiesforbenefits,thebonusisequaltofourtimestheweeklyamount.Thisbonuscanhelpoffsetsomeofthecoststhatmighthavebeenincurredwhilesatisfyingthewaitingperiod.

Extended term insurance

WithSunLTCI,iftheclientcan’tpaythepremiums,extendedterminsurancemayhelp.Ifthisprovisionapplies,thepolicymaystayinforceforaspecifiedtime,andthebenefitamount,benefitperiodandwaitingperioddon’tchange.

LifestageCare™ services

ThepolicyownerhasimmediateandunlimitedaccesstoLifestageCare–anational,bilingualinformationserviceavailable24hoursaday,sevendaysaweek–oncethepolicyisissuedandaslongasit’sinforce.

Clientsgetaccesstounbiasedinformationaboutlocal,qualifiedhealthandpersonalcareprovidersthatmeetstheirindividualandfamilyneedsateverystageoflife.ThepolicyownercanuseLifestageCareservicestohelpanyfamilymember.

Premium guarantee

Allinsurersguaranteetheirratesforthefirstfivepolicyyears.However,manymaychangetheirratesanytimeafterward.AtSunLifeFinancial,ifwechangeourrates,wewon’tchangethemagainforatleastanotherfiveyears.

Coverage extended outside of Canada and the United States

Mostinsurersdon’tprovidecoverageforanyamountoftimespentoutsideofCanadaortheUnitedStates.SunLTCIprovidescoverageforeightconsecutiveweekswhentheinsuredpersontravelsoutsideeithercountry.

WHERE TO GO FOR MORE INFORMATION?ContactyourRegionalSalesDirectorortheSalesSupportteamformoreinformationonlongtermcareinsuranceproducts.

Telephone:1800-800-4SUN(4786)Email:[email protected]

It’simportanttomeetwithclientsregularlytoreviewtheircoverageandhelpthemwithanycontractualconversionsorrenewalstoensuretheyhavetheprotectionthatmeetstheirneeds.

SunLifeAssuranceCompanyofCanadaisamemberoftheSunLifeFinancialgroupofcompanies.

©SunLifeAssuranceCompanyofCanada,2017.

810-3352-Digital-07-17

Life’s brighter under the sun