advanced methods of insurance lecture 3. exotic options: tools pay-off –digital, chooser, compound...

TRANSCRIPT

Advanced methods of insurance

Lecture 3

Exotic options: tools

• Pay-off– Digital, chooser, compound

• Barriers– Up/Down-In/Out, parigine

• Path dependent– Asian, look-back, ladder, shout

• Investment period– Forward start, ratchet.

• Early exercize– Bermuda, American

• Multivariate– Basket, rainbow, exchange

• Foreign exchange– Quantos, compos

Pay-off

• Chooser: at an intermediate date can be chosen to be call or put

• Digital: fixed pay-off if a trigger condition, i.e. underlying price above some threshold, zero otherwise

• Compound options: underlying is an option

Chooser options

• At date the holder of the option may be call or put. If the strike is the same the option is called “simple”

• At time the chooser will nechooser() = max(call(S,;K,T), put(S,;K,T))

= call(S,;K,T) + max(KP(,T) – S(),0)• To avoid arbitrage, at time t the value of the

chooser must bechooser(t) = call(S,t;K,T) + put(S,t;KP(,T),)

Digital…Digital CoN

0

0,2

0,4

0,6

0,8

1

1,2

48 48,5 49 49,5 50 50,5 51 51,5 52

Digital CoN

…and vertical spreads (super-replication)Spread verticali e opzioni digitali

0

0.2

0.4

0.6

0.8

1

1.2

48 48.5 49 49.5 50 50.5 51 51.5 52

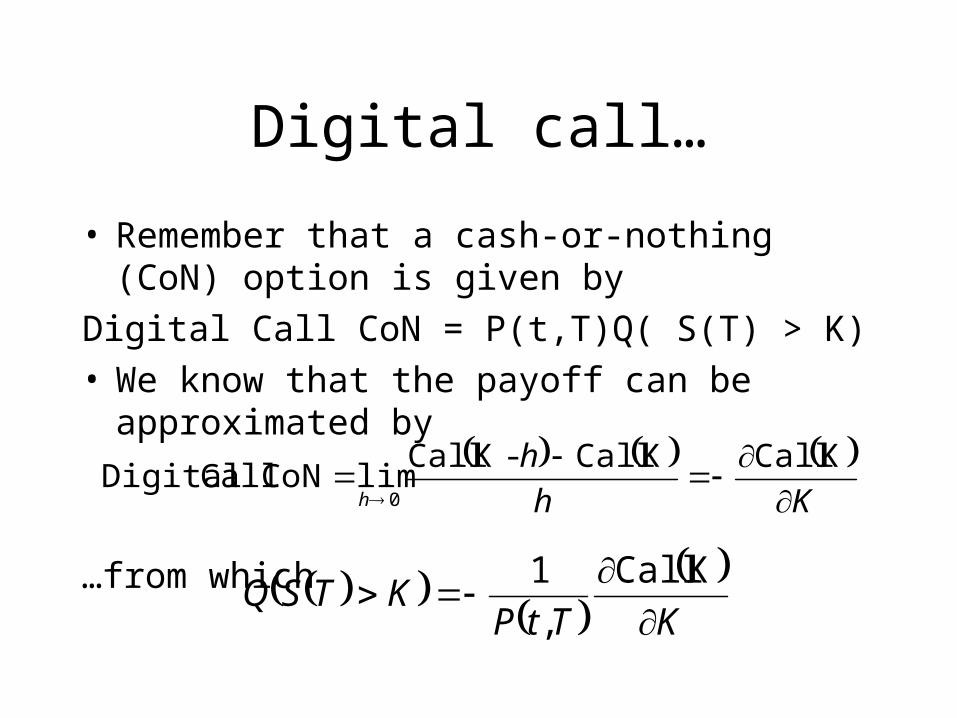

Digital call…

• Remember that a cash-or-nothing (CoN) option is given by

Digital Call CoN = P(t,T)Q( S(T) > K)• We know that the payoff can be approximated by

…from which

Kh

hh

KCall

KCall-KCalllim CoN Call Digital

0

KTtPKTSQ

KCall

,

1

…and put

• Sama analysis for a digital put paying one unit of cash if S(T) K

Digital Put CoN = P(t,T)Q( S(T) K)• Same approximation

…from which

Kh

hh

KPut

-KPutKPutlim CoNPut Digitale

0

KTtPKTSQ

KPut

,

1

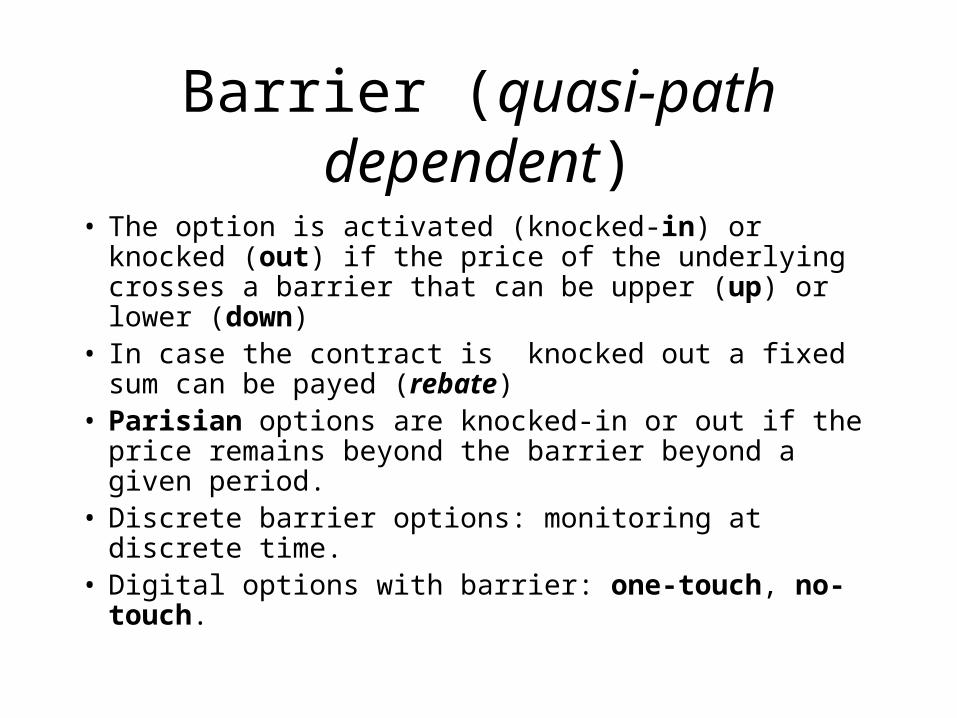

Barrier (quasi-path dependent)

• The option is activated (knocked-in) or knocked (out) if the price of the underlying crosses a barrier that can be upper (up) or lower (down)

• In case the contract is knocked out a fixed sum can be payed (rebate)

• Parisian options are knocked-in or out if the price remains beyond the barrier beyond a given period.

• Discrete barrier options: monitoring at discrete time.

• Digital options with barrier: one-touch, no-touch.

Simmetry of barrier options

• It is immediate to verify that to exclude arbitrage opportunities

Plain vanilla option =

Down(Up)-and-in(H) + Down(Up)-and-out(H) • Every option with barrier can be represented with

– A long position in a plain vanilla option– A short position in the symmetric barrier option

Path-dependent

• The value of the reference price or of the strike to be used for the pay-off depends on the prices of the underlying asset in a period of time.

• Asian: use the average of the underlying as reference rate (average rate) or strike (average rate).

• Lookback: the strike is set at the maximum/minimum on a reference period

• Ladder: the strike is updated on a grid of values, whenever the underlying crosses the value.

Asian options

• The problem of most Asian options is that they are written on arithmetic averages.

• In the Black and Scholes model, in which prices are log-normal, the sum of them is not log-normale.

• Evaluation techniques:– Moment matching (Turnbull e Wakeman): the

distributon is approximated by a log-normal distribution

– Monte Carlo: pay-offs generated for every path and averaged

Ladder options

• In ladder options the strike is set at a level H if the underlying during the life of the option crosses the value H. Each of these levels H represents a step of a stairs (ladder).

• Ladder options allow to reset the strike accroding to movements of the market.

• In the extreme case of a continuous grid we get a lookback.

Ladder options: evalutation

• Take a single step H.

• Assume an option with strike price K and date T. We have that:

Ladder (K, H) =

Down(Up)-and-Out(K,H)

+ Down(Up)-and-In(H,H)

Forward start options

• Assume that at time the strike is K = S().The value of the option at time will be

B & S(S(); S(),T–) • Notice that given a constant c we have

B & S(S(); S(),T – ) =c B & S(S()/c; S()/c ,T – ) • Setting c = S()/S(t) we have

B & S(S(); S(),T–)= S() B & S(S(t); S(t),T – )/S(t)• The value of the forward start option is equivalent to buying N = B &

S(S(t); cS(t),T–)/S(t) units of the underlying at time t. At time we have

B & S(S(); S(),T–) = S() N• At time t we compute

Forward Start =exp(– r( – t) EQ[S()]N = exp(– r( – t))S(t) exp((r –d)( – t))N

= exp(– d( – t)) B & S(S(t); S(t),T – )

Multivariate options

• Basket: the value of the underlying is computed as a weighted average of a basket of stocks

• Rainbow: use different aggregating functions:– Options on maximum or minimum of a basket of stocks

(option on the max/min) – Options to exchange a financial asset with another

(exchange option), – Options written on the price difference of assets (spread

option), – Options with different strikes for every stock in the

basket (multi-strike).

Reverse convertible• Period: 1° Febbraio-1° settembre 2000

• Fixed coupon 22%, paid 01/09/2000

• Repayment of principal in cash or Telecom stocks if the following conditions occur– On 25/08/2000 Telecom is below 16.77 Euro– Between 28/01/2000 and 25/08/2000 the price

of Telecom stock touches 13.416 Euro

• Reverse convertible = ZCB – put

(with barrier)

Index-Linked Bond

• Period: July 31 2000 – July 31 2004• Coupon and principal: paid at maturity• Coupon defined as the maximum between 6% and

the average growth of end of quarter equally weighted portfolio of : Nikkei 225, Eurostoxx 50 e S&P 500.

• Index-Linked Bond = zero coupon + option (Asian basket call)

Quanto structured note

• Period 13 March 2000 - 10 October 2000• Fixed coupon 23% paid at maturity• Principal repaid in cash at maturity if the pound

value of Vodaphone stock is not below 3.775 on 3/10/2003; alternatively Vodaphone stocks are delivered

• Quanto structured note = zero coupon bond -quanto put

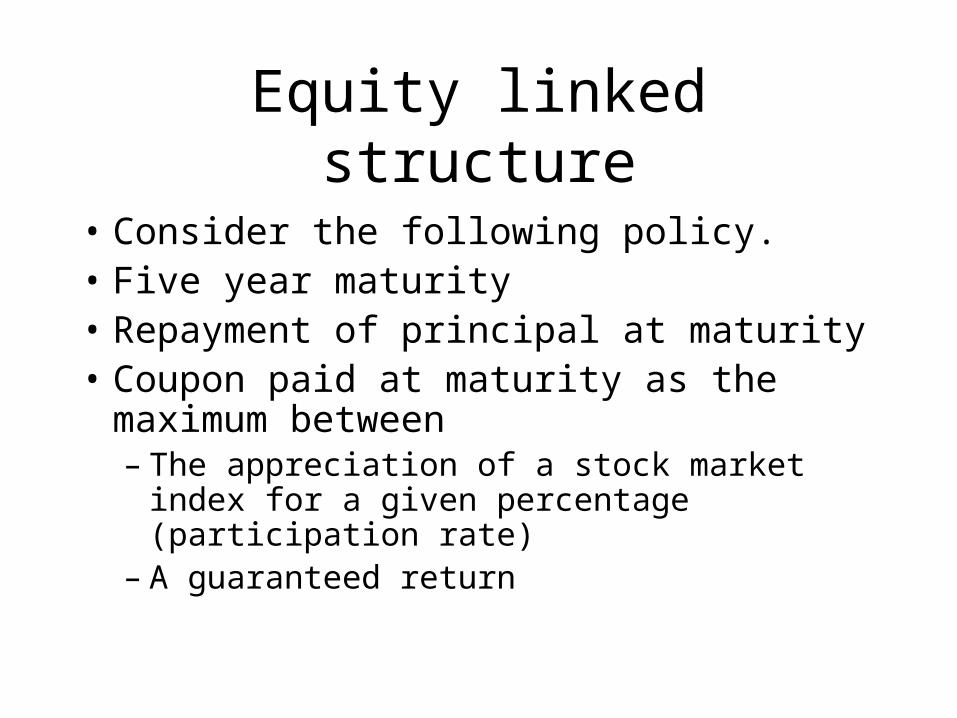

Equity linked structure

• Consider the following policy.• Five year maturity• Repayment of principal at maturity• Coupon paid at maturity as the maximum

between– The appreciation of a stock market index for a

given percentage (participation rate)– A guaranteed return

Structuring choices• How to make the product less riskhy? If the product is considered

much too risky, the speculative content can be reduced in two ways– Reducing leverage– Reducing volatility

• Risk can be reduced by increasing the strike price (the guaranteed return) or reducing the participation rate

• Volatility can be reduced choosing an Asian option for the investment on the index:– Reduced risk for the investor: smoothing– Reduced dependence on long term volatility

Crash protection• The investment horizon of a product like this

could be considered too long. If the market decreases by a relevant amount, the vlaue of the option can decrease to zero, and the investor remains locked in a low return investment.

• For this, we may consider a crash protection clause. Under this clause, if the value falls below a percentage h of the initial value the new strike is set at that level.

Crash protection: evaluation• The value of the product is determined as

ZCB + Call Ladder (S(t)/S(0), t; 1, h)• We can isolate the value of the crash protection clause using

– The replicating portfolio of the latter option – The symmetry of in and out options.

• We compute ZCB + Call(S(t)/S(0), t; 1, h) +

Down-and-In(S(t)/S(0), t;h, h) – Down-and-In(S(t)/S(0), t; 1, h)

• The value of the crash protection clause is then given by the difference between a Down-and-In with strike equal to the barrier and that with the initial strike.

Callability/putability

• A callable bond at time can be decomposed in terms of a exchangeable compund option.

• Payoff exampleMax[1, S(T)/S(0)] =

= 1 + max[S(T)/S(0) – 1,0] callable at time at par. At time the value isMin[1,P(,T) +Call(S()/S(0);1,T)] =

= P(,T) +Call(S()/S(0);1,T) – max[Call(S()/S(0);1,T) – (1 – P(,T)), 0]

A different product

• Assume that investors prefer a product giving a stream of payments indexed to equity.

• We can think of a sequence of coupons of the kind

Coupon (t + i) = max[S(t + i)/S(t + i – 1 ) – 1,0] • This way the product produces the cash flows that

an investor would earn by investing every year on the stock market, while being protected by losses.

Ratchet index-linked

• The new product can be represented as a coupon bond whose flow of interest is represented by a sequence of forward start options, which define what is called a rachet or cliquet option.

• This amounts, if we rule out dividends, to N one year options.

Ratchet index-linked

• If we consider a constant dividend yield q we have

Coupons = (1 – vN )/(1 – v)AtM Call

with

v = exp(– q )

Vega bond

• Assume a product that in N years pay a coupon defined as

Coupon = max[0, D + imin(S(t+i)/S(t+i–1) – 1,0)]• In other terms, the coupon is given by an initial

endowment D, expressed in percentage of the initial principal, from which negative movements of the market are subtracted.

Vega bond

• Rewrite the pay-off as,

Coupon = max[0,D – imax(1 – S(t+i)/S(t+i–1),0)]

• Interest payment is a put option written on a ratchet put.

Multivariatedigital notes(Altiplano)

• Assume a coupon defined (reset date) and paid at time tj. • Assume a basket of n stocks, whose prices are Sn(tj).• Denote Sn(t0) the reference prices, typically taken at the

beginning of the contracts and used as strike price.• Denote Ij indicator function taking value 1 if Sn(tj)/Sn(t0) > 1 and

0 otherwise for all the securities. • The coupon is a multivariate option, and, given the coupon rate

c

jc*ICedola

Altiplano with memory• Assume a coupon defined (reset date) and paid at

time tj, and a sequence of dates {t0,t1,t2,…,tj – 1}.

• Assumiame a basket of n = 1,2,…N assets, whose prices are Sn(ti).

• Denote B a barrier and Ii an indicator function taking value 1 if Sn(ti)/ S(t0) > B and zero otherwise.

• The memory feature implies that the first time ti when the indicator function is taking value 1 all coupons up to ti are paid.

Everest• Assume a coupon defined and paid at time T.• Assume a basket of n = 1,2,…N bonds, whose prices are

Sn(T).• Denote Sn(t0) the reference prices, typically recoorded at

the origin of the contract and used as strike prices• The coupon of an Everest is

max[min(Sn(T)/Sn(0),1+k] = = (1 + k) + max[min(Sn(T)/Sn(0) – (1+k),0]

with n = 1,2,…,N and a guaranteed return equal to k.

Equity-linked bond• Assume a coupon defined and paid at time T.• Assume a basket n = 1,2,…N stocks, whose prices are

Sn(T).• Denote Sn(t0) the reference prices, typically recorded at

the origin of the contract, and used as strike prices.• The coupon of the basket option is

max[Average(Sn(T)/Sn(0),1+k] = = (1 + k) + max[Average(Sn(T)/Sn(0) – (1+k),0]

with n = 1,2,…,N and minimum guaranteed return k.

Long/short correlation

• For a multivariate option it is crucial to determine the sign of exposure to changes in correlation.

• The sign of the exposure to correlation is linked to the presence of AND or OR in the contract.

• Example: a call on min is long correlation, while a a call on max is short.