advanced issues in international grantmaking

TRANSCRIPT

Advanced Issues in International Grantmaking

IITChicago‐KentCollegeofLawConferenceonNot‐For‐ProfitOrganizations

June4,2015

Presented by:

Norah L. Jones & Corbin J. MorrisQuarles & Brady LLP

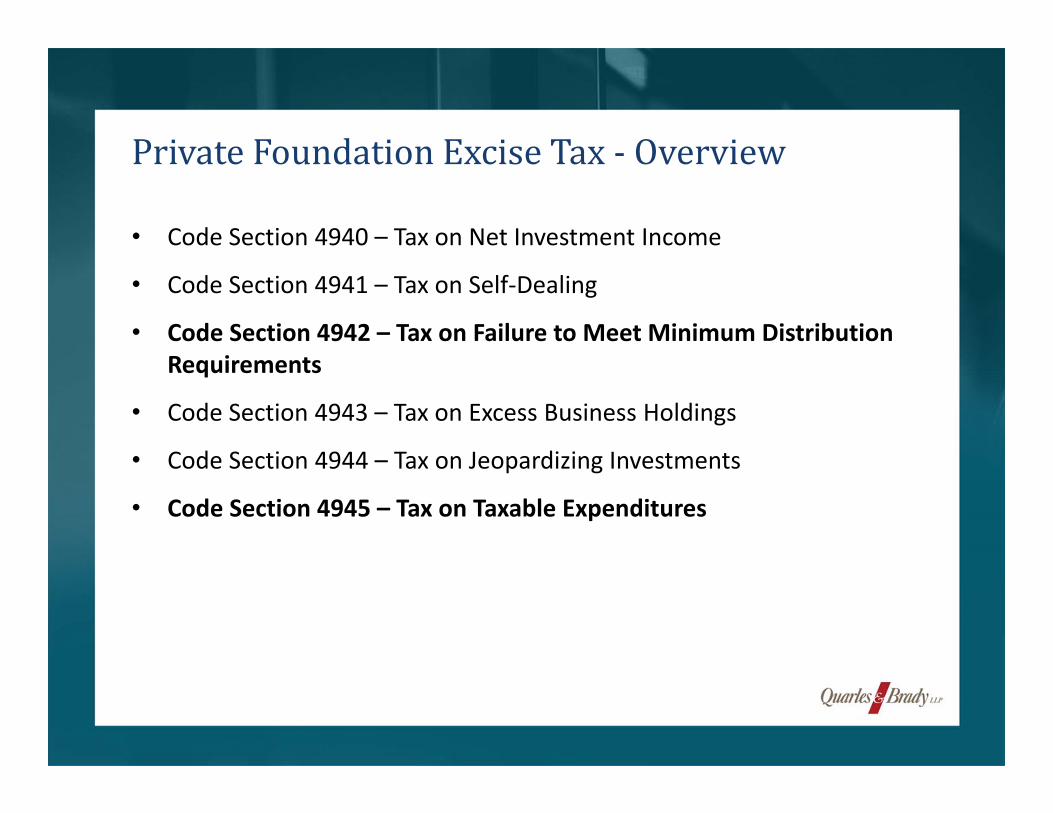

• Code Section 4940 – Tax on Net Investment Income

• Code Section 4941 – Tax on Self‐Dealing

• Code Section 4942 – Tax on Failure to Meet Minimum Distribution Requirements

• Code Section 4943 – Tax on Excess Business Holdings

• Code Section 4944 – Tax on Jeopardizing Investments

• Code Section 4945 – Tax on Taxable Expenditures

PrivateFoundationExciseTax‐ Overview

• Section 4942(a) imposes an excise tax on the “undistributed income” of a private foundation for any taxable year if it has not been distributed by a specific time.

• “Undistributed Income”, with respect to any taxable year, is the amount by which the “distributable amount” for the taxable year exceeds “qualifying distributions” made out of the distributable amount.

• In general, in order to avoid the Section 4942 excise tax, a foundation must make “qualifying distributions” in an amount that is at least equal to 5% of the value of its non‐charitable use assets (i.e., investment assets).

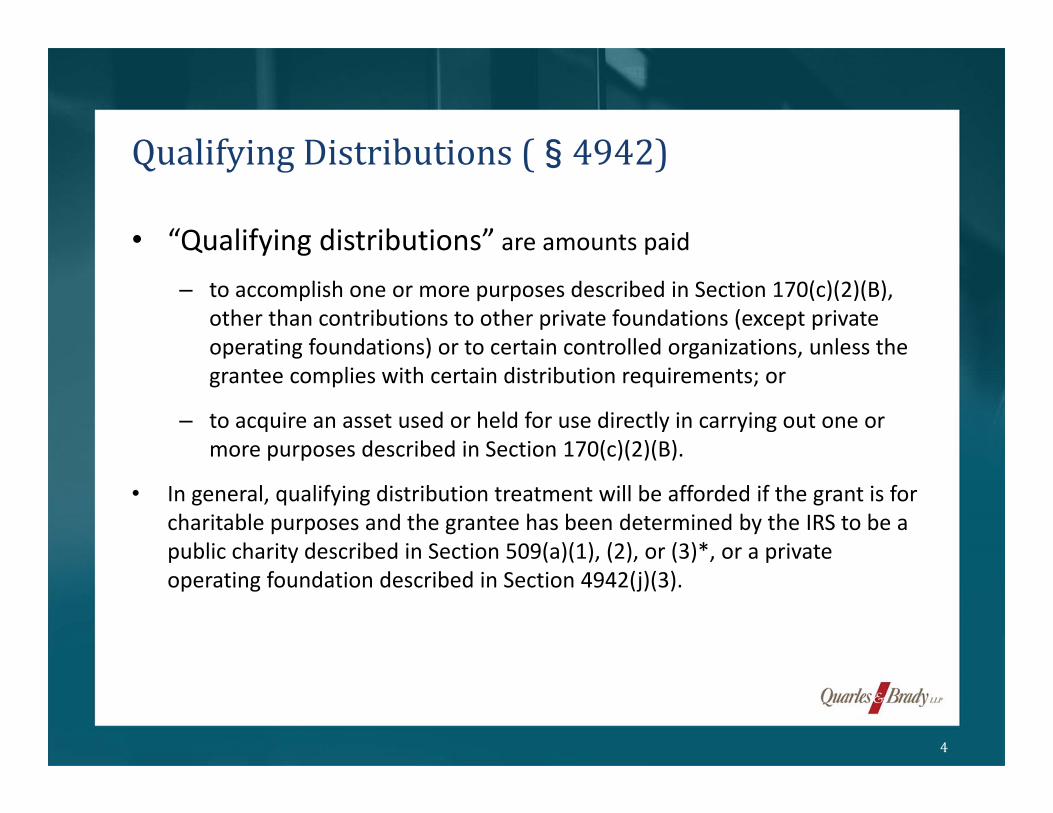

QualifyingDistributions(§4942)

3

• “Qualifying distributions” are amounts paid

– to accomplish one or more purposes described in Section 170(c)(2)(B), other than contributions to other private foundations (except private operating foundations) or to certain controlled organizations, unless the grantee complies with certain distribution requirements; or

– to acquire an asset used or held for use directly in carrying out one or more purposes described in Section 170(c)(2)(B).

• In general, qualifying distribution treatment will be afforded if the grant is for charitable purposes and the grantee has been determined by the IRS to be a public charity described in Section 509(a)(1), (2), or (3)*, or a private operating foundation described in Section 4942(j)(3).

QualifyingDistributions(§4942)

4

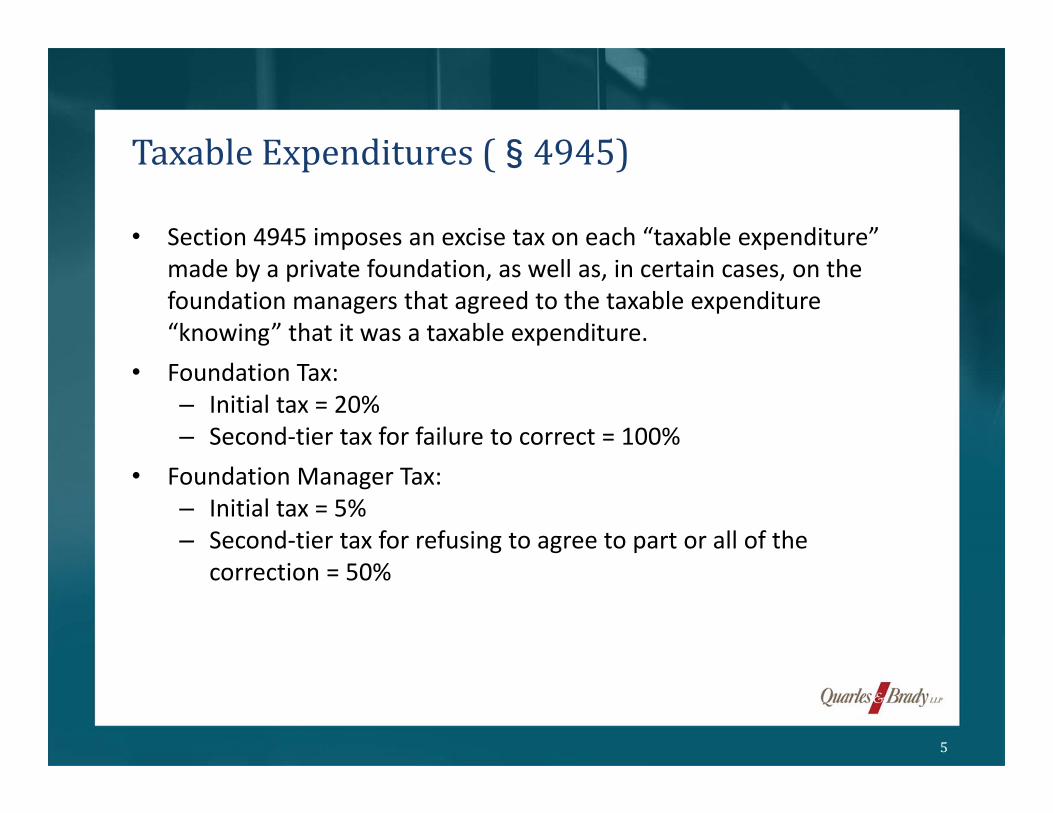

• Section 4945 imposes an excise tax on each “taxable expenditure” made by a private foundation, as well as, in certain cases, on the foundation managers that agreed to the taxable expenditure “knowing” that it was a taxable expenditure.

• Foundation Tax: – Initial tax = 20%– Second‐tier tax for failure to correct = 100%

• Foundation Manager Tax:– Initial tax = 5%– Second‐tier tax for refusing to agree to part or all of the

correction = 50%

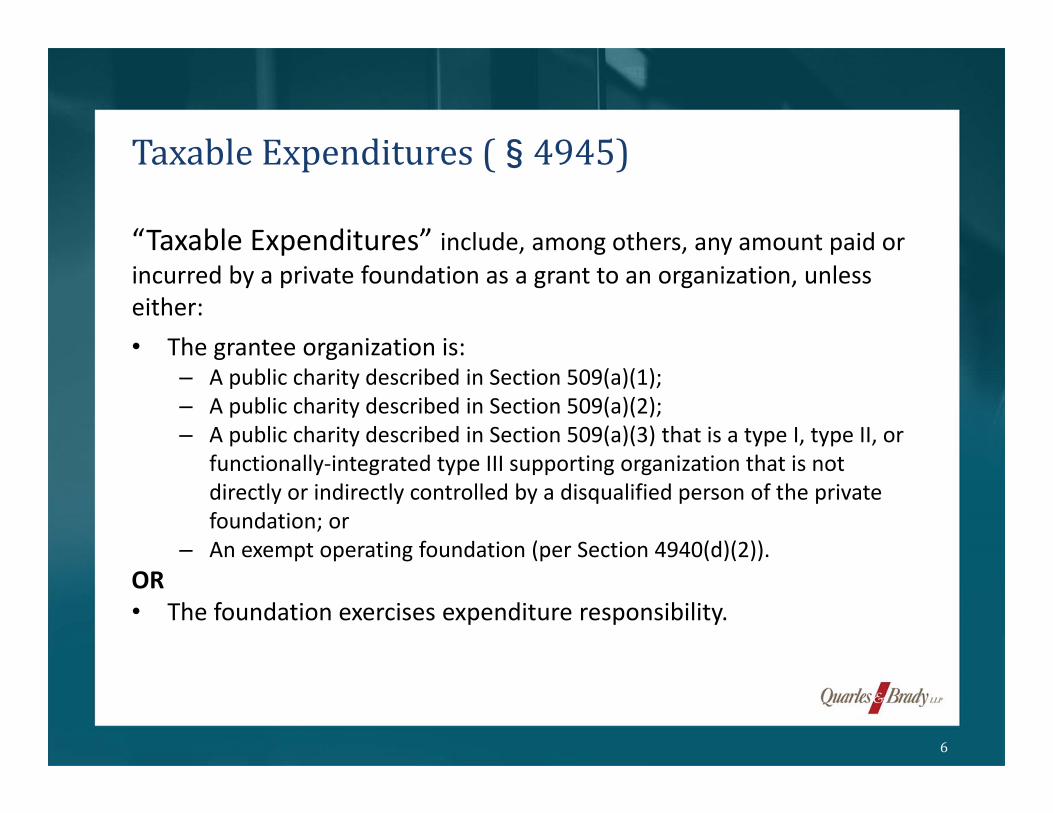

TaxableExpenditures(§4945)

5

“Taxable Expenditures” include, among others, any amount paid or incurred by a private foundation as a grant to an organization, unless either:• The grantee organization is:

– A public charity described in Section 509(a)(1); – A public charity described in Section 509(a)(2);– A public charity described in Section 509(a)(3) that is a type I, type II, or

functionally‐integrated type III supporting organization that is not directly or indirectly controlled by a disqualified person of the private foundation; or

– An exempt operating foundation (per Section 4940(d)(2)). OR• The foundation exercises expenditure responsibility.

TaxableExpenditures(§4945)

6

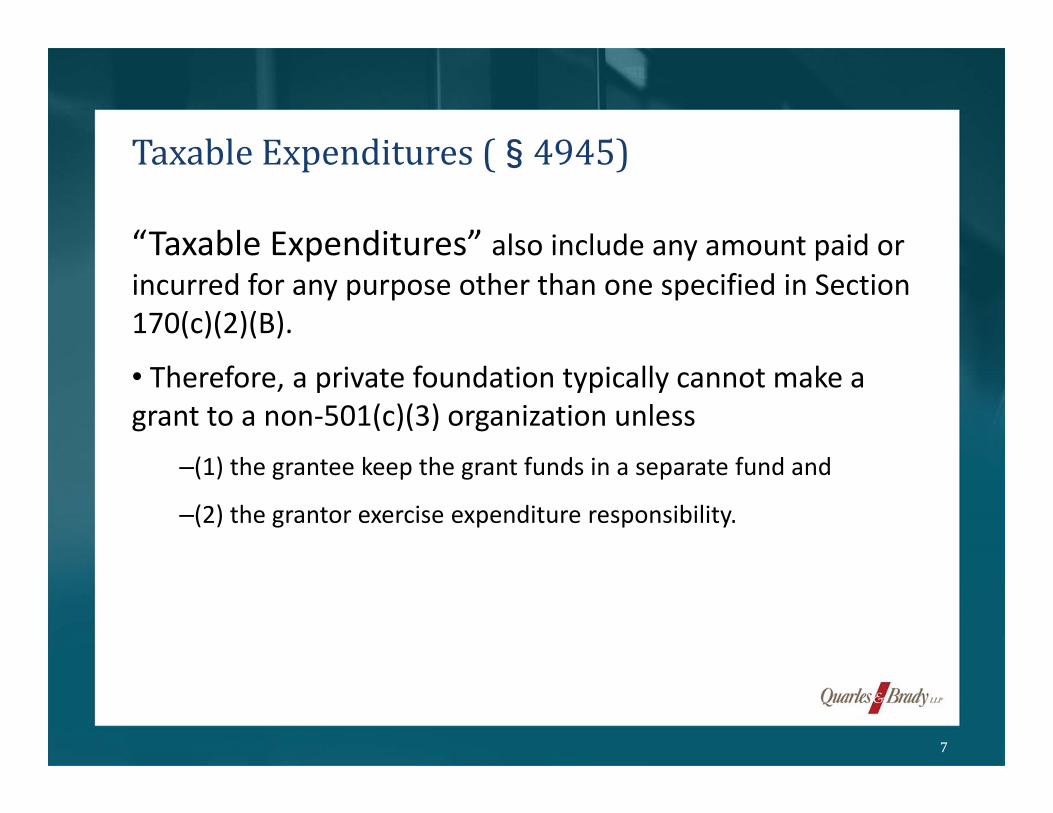

“Taxable Expenditures” also include any amount paid or incurred for any purpose other than one specified in Section 170(c)(2)(B).

• Therefore, a private foundation typically cannot make a grant to a non‐501(c)(3) organization unless

–(1) the grantee keep the grant funds in a separate fund and

–(2) the grantor exercise expenditure responsibility.

TaxableExpenditures(§4945)

7

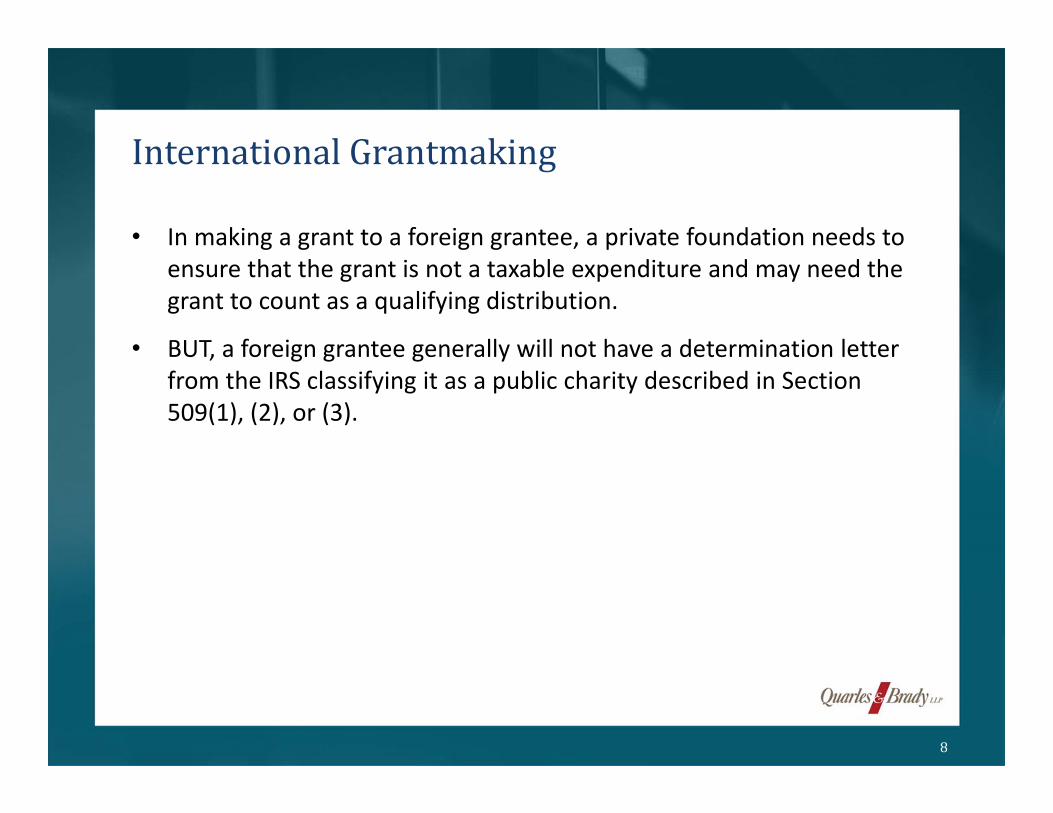

• In making a grant to a foreign grantee, a private foundation needs to ensure that the grant is not a taxable expenditure and may need the grant to count as a qualifying distribution.

• BUT, a foreign grantee generally will not have a determination letter from the IRS classifying it as a public charity described in Section 509(1), (2), or (3).

InternationalGrantmaking

8

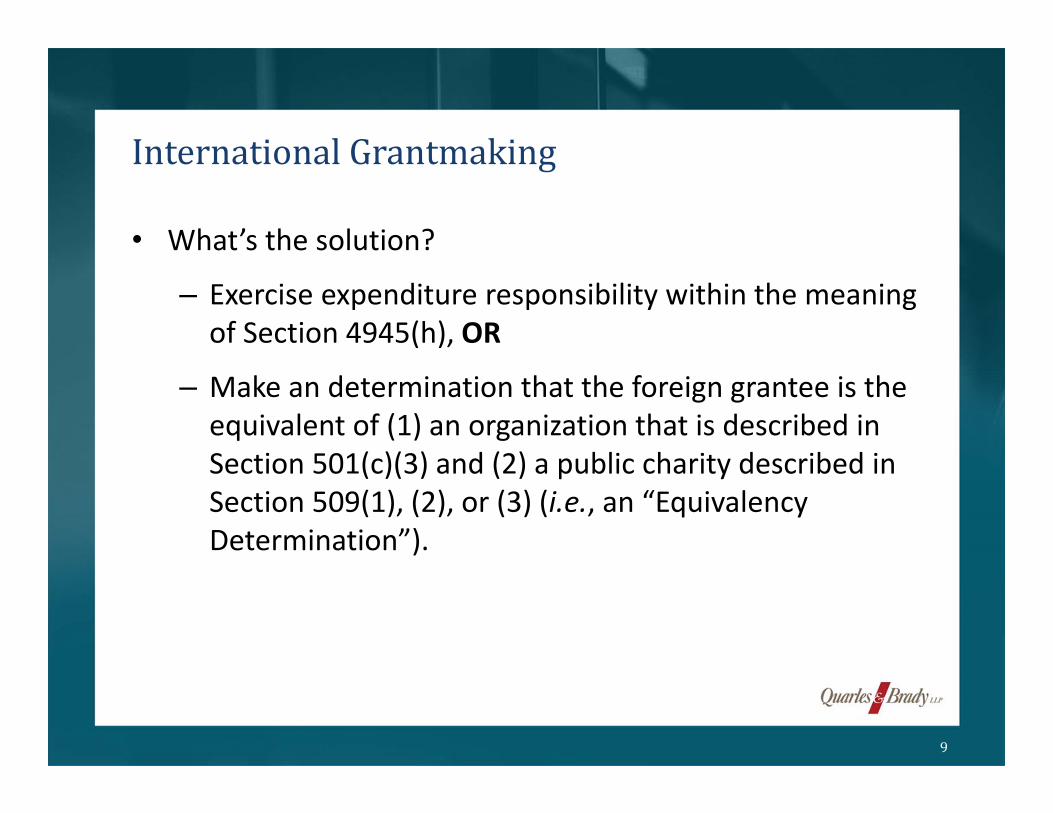

• What’s the solution?

– Exercise expenditure responsibility within the meaning of Section 4945(h), OR

– Make an determination that the foreign grantee is the equivalent of (1) an organization that is described in Section 501(c)(3) and (2) a public charity described in Section 509(1), (2), or (3) (i.e., an “Equivalency Determination”).

InternationalGrantmaking

9

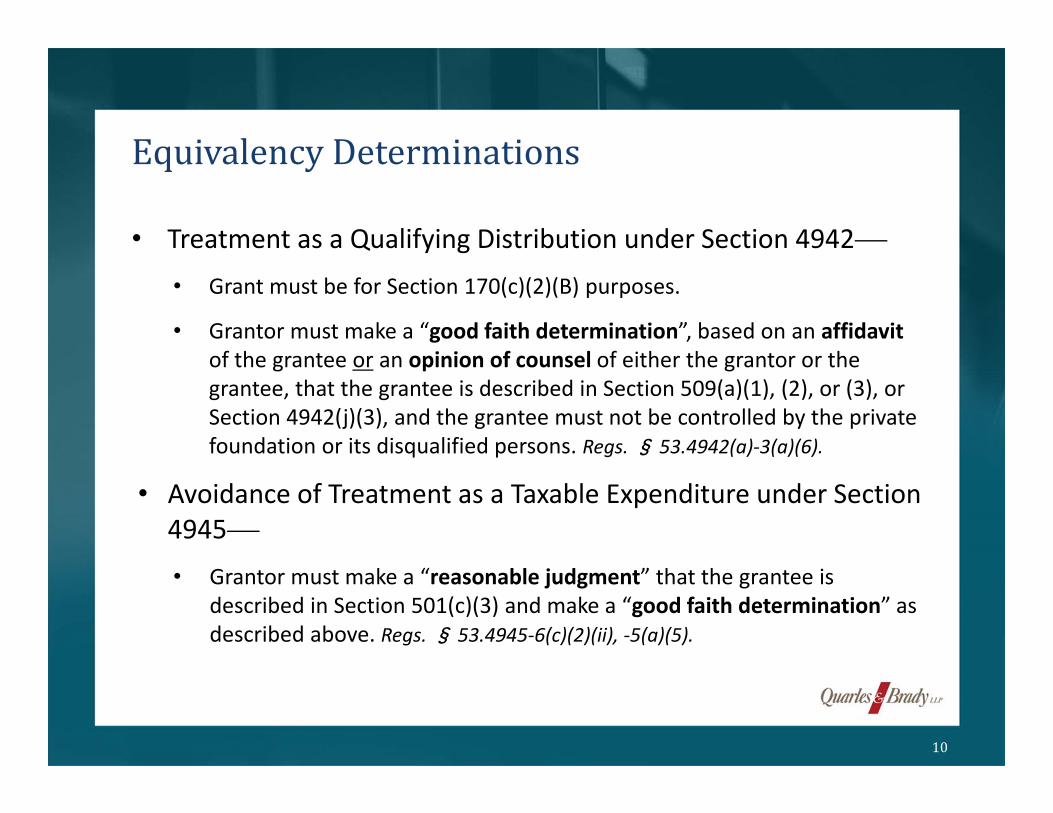

• Treatment as a Qualifying Distribution under Section 4942

• Grant must be for Section 170(c)(2)(B) purposes.

• Grantor must make a “good faith determination”, based on an affidavitof the grantee or an opinion of counsel of either the grantor or the grantee, that the grantee is described in Section 509(a)(1), (2), or (3), or Section 4942(j)(3), and the grantee must not be controlled by the private foundation or its disqualified persons. Regs. § 53.4942(a)‐3(a)(6).

• Avoidance of Treatment as a Taxable Expenditure under Section 4945

• Grantor must make a “reasonable judgment” that the grantee is described in Section 501(c)(3) and make a “good faith determination” as described above. Regs. § 53.4945‐6(c)(2)(ii), ‐5(a)(5).

EquivalencyDeterminations

10

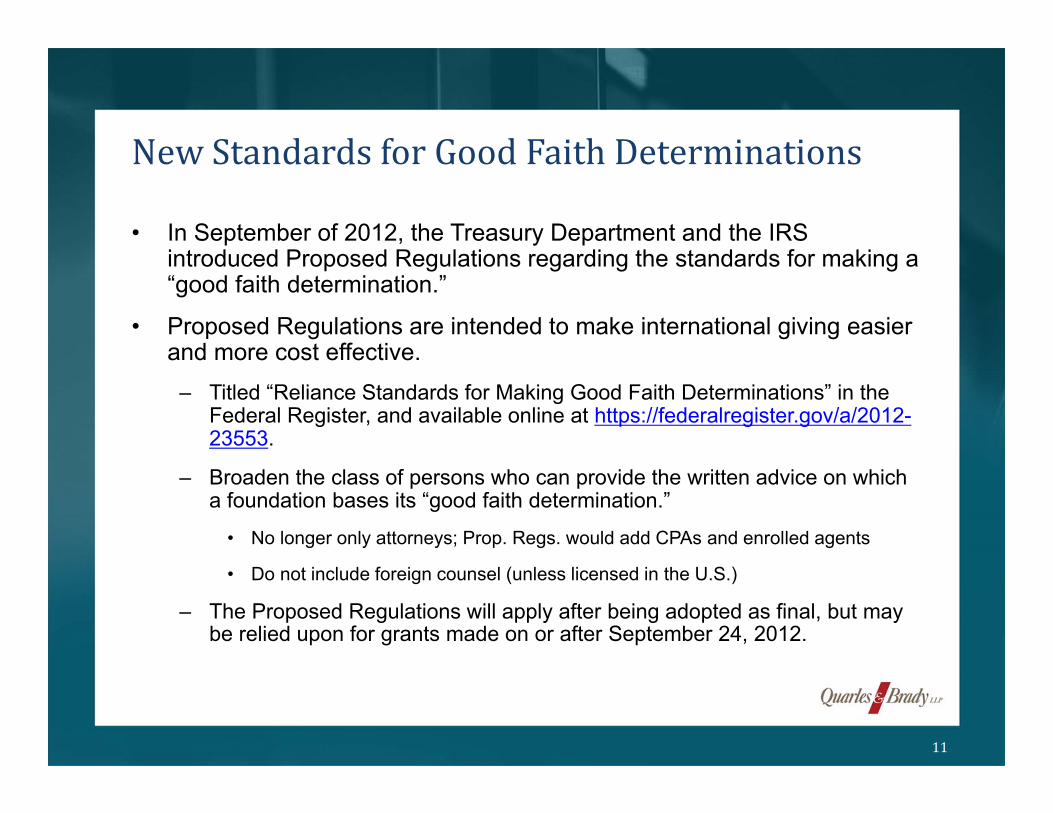

• In September of 2012, the Treasury Department and the IRS introduced Proposed Regulations regarding the standards for making a “good faith determination.”

• Proposed Regulations are intended to make international giving easier and more cost effective.

– Titled “Reliance Standards for Making Good Faith Determinations” in the Federal Register, and available online at https://federalregister.gov/a/2012-23553.

– Broaden the class of persons who can provide the written advice on which a foundation bases its “good faith determination.”

• No longer only attorneys; Prop. Regs. would add CPAs and enrolled agents

• Do not include foreign counsel (unless licensed in the U.S.)

– The Proposed Regulations will apply after being adopted as final, but may be relied upon for grants made on or after September 24, 2012.

NewStandardsforGoodFaithDeterminations

11

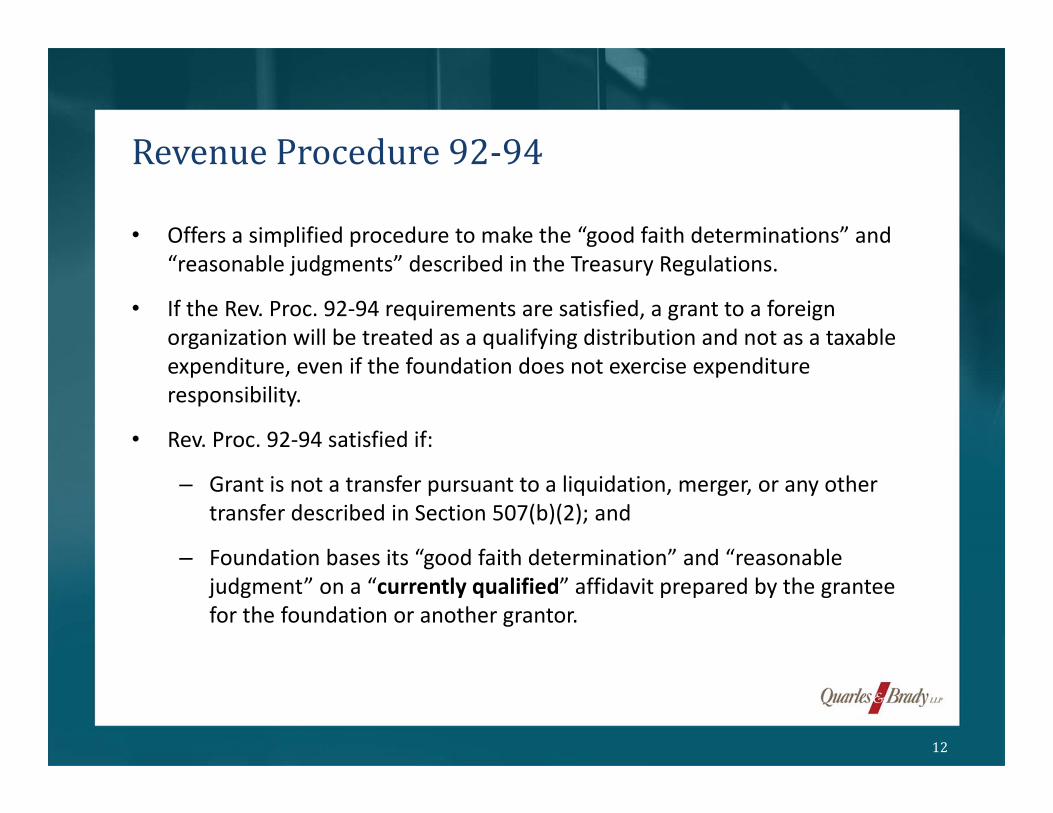

• Offers a simplified procedure to make the “good faith determinations” and “reasonable judgments” described in the Treasury Regulations.

• If the Rev. Proc. 92‐94 requirements are satisfied, a grant to a foreign organization will be treated as a qualifying distribution and not as a taxable expenditure, even if the foundation does not exercise expenditure responsibility.

• Rev. Proc. 92‐94 satisfied if:

– Grant is not a transfer pursuant to a liquidation, merger, or any other transfer described in Section 507(b)(2); and

– Foundation bases its “good faith determination” and “reasonable judgment” on a “currently qualified” affidavit prepared by the grantee for the foundation or another grantor.

RevenueProcedure92‐94

12

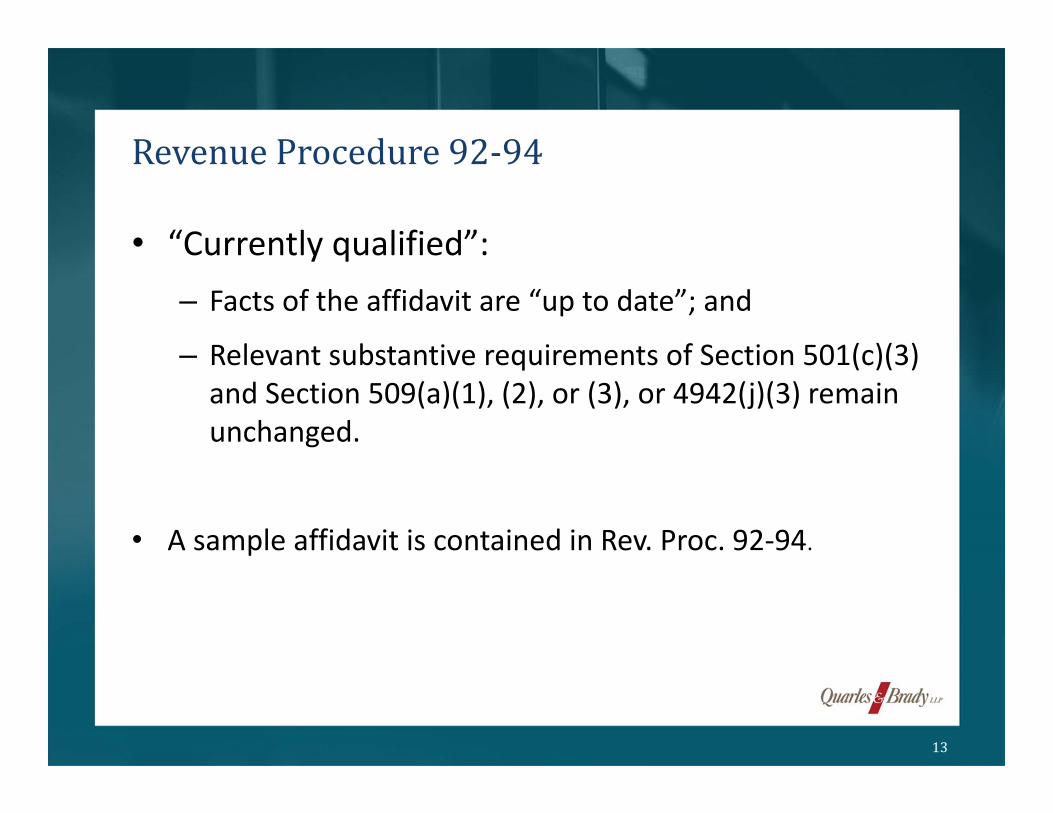

• “Currently qualified”:– Facts of the affidavit are “up to date”; and

– Relevant substantive requirements of Section 501(c)(3) and Section 509(a)(1), (2), or (3), or 4942(j)(3) remain unchanged.

• A sample affidavit is contained in Rev. Proc. 92‐94.

RevenueProcedure92‐94

13

Facts are “up to date” if they reflect the grantee’s latest complete accounting year or the affidavit is updated to reflect the grantee’s current data.

Updating Affidavits:

• If grantee’s exempt status does not depend on financial support (e.g., a school or church), the affidavit may be updated by having the grantee amend any facts in the original that have changed or attest that no facts have changed.

• If grantee’s exempt status depends on financial support (e.g., a grantee that is equivalent to a 509(a)(2) organization), the grantee must provide an attested statement containing enough financial data to establish that it continues to meet the requirements of the applicable Code section.

RevenueProcedure92‐94

14

Affidavit Requirements (regardless of format):

• Must be written in English, and English translations must be provided for copies of supporting documents.

• Must be attested to by a principal officer of the grantee.

• If the grantee claims to be a school described in Section 170(b)(1)(A)(ii), it must provide a statement that it has adopted and operates pursuant to a racially nondiscriminatory policy as to students (per Rev. Rul. 71‐447 and Rev. Rul. 75‐231), and explain any basis for the grantee’s failure to comply with one or more of the provisions of Rev. Proc. 75‐50.

• Must include a declaration in English that states that the purpose of the affidavit is to assist the grant‐making foundation in determining whether the foreign organization is the equivalent of a public charity described in Section 509(a)(1), (2), or (3), or a private operating foundation described in Section 4942(j)(3).

RevenueProcedure92‐94

15

Affidavit Requirements (continued):

• Identify the statute, charter, or other document that created the grantee and state that it is operated exclusively for one or more purposes described in Section 170(c)(2)(B).

• Describe the past, current, and future activities and operations of the grantee.

• Attach English copies of the grantee’s governing documents.

• State that the laws and customs applicable to the grantee do not permit any of its income or assets to be distributed to, or applied for the benefit of, a private person or non‐charitable organization other than pursuant to the conduct of the grantee’s charitable activities, as payment of reasonable compensation for services rendered, or as fair market value for purchased property.

• State that the grantee has no shareholders or members who have a proprietary interest in the income or assets of the grantee.

RevenueProcedure92‐94

16

Affidavit Requirements (continued):

• State that, in the event of dissolution, all of the grantee’s assets would be distributed to another not‐for‐profit organization for charitable, religious, scientific, literary, or educational purposes, or to a governmental instrumentality. Copies in English of the statutory law or provisions in the governing documents must be attached.

• State that the laws and customs applicable to the grantee do not permit the grantee, other than as an insubstantial part of its activities, (A) to engage in any non‐charitable activities or (B) to attempt to influence legislation.

• State that that laws and customs applicable to the grantee do not permit it directly or indirectly to participate or intervene in any political campaign on behalf of, or in opposition to, any candidate for public office.

• State whether and how the grantee is controlled by or operated in connection with any other organization.

RevenueProcedure92‐94

17

Financial Records Requirements:

• Rev. Proc. 92‐94 requires a financial schedule showing the organization’s support for the four most recently completed taxable years. The four‐year period is based on a prior version of the Regulations that required only a four‐year period to determine whether an organization was publicly supported.

• The current Regulations, which became final in 2011, require an examination of the taxable year in question and the four taxable years immediately preceding that taxable year (i.e., five total years).

• Accordingly, it may be reasonable to conclude that, in order to satisfy the requirements of Rev. Proc. 92‐94 for taxable years beginning with 2011, grantors should obtain grantee affidavits that include financial schedules for the current taxable year and the four immediately preceding taxable years.

RevenueProcedure92‐94

18

Requirements Relating to Specific Organizations

• Schools:

– Must normally maintain a regular faculty and curriculum and normally have an enrolled body of students in attendance at the place where their educational activities are regularly carried on.

– Must adopt and operate pursuant to a racially nondiscriminatory policy as to students as set forth in Rev. Rul. 71‐447, Rev. Rul. 75‐231, and as implemented in Rev. Proc. 75‐50.

• Churches:

– “Church” not defined in 170(b)(1)(A)(i). IRS and the courts have developed fourteen identifying features of a church.

– A private foundation may reasonably conclude that a foreign organization is equivalent of a public charity if can demonstrate the presence of the features. See PLR 200209055.

• Hospitals: satisfaction of Section 501(r) requirements?

RevenueProcedure92‐94

19

“Expenditure Responsibility”, which is described in Section 4945(h), requires the foundation to make all reasonable efforts and establish procedures to:

– See that grant is spent solely for the purpose for which made;

– Obtain full and complete reports from the grantee on how funds were spent; and

– Make full and detailed reports with respect to such grants to the IRS on the foundation’s Forms 990‐PF.

Alternatives:ExpenditureResponsibility

20

Expenditure responsibility grant must be made pursuant to a written grant agreement, signed by an officer of the grantee, that requires the grantee to:

– repay any portion not used for grant purposes;

– submit full and complete annual reports;

– maintain records of receipts and expenditures;

– not use funds for (1) propaganda, (2) attempting to influence legislation, (3) influencing the outcome of public elections, (4) carrying on voter registration drives, (5) undertaking activity not specified in section 170(c)(2)(B), or (6) activity otherwise constituting a taxable expenditure.

– + Additional requirements for program‐related investments & non‐501(c)(3) recipients.

Alternatives:ExpenditureResponsibility

21

Private foundation must:– require its grantee to report annually to the foundation for each year

until the grant is expended in full or the grant is otherwise terminated.

– report specified information to the IRS on the foundation’s annual Form 990‐PF with respect to (1) each expenditure responsibility grant made during the tax year and (2) each expenditure responsibility grant upon which any amount or grantee report is outstanding at any time during the foundation's tax year.

– maintain a copy of the agreement covering each expenditure responsibility grant, a copy of each report received from grantee during the taxable year, and a copy of each report made by the grantor’s personnel during the taxable year.

Alternatives:ExpenditureResponsibility

22

A “friends of” organization typically is a 501(c)(3) organized and operated as a U.S. nonprofit corporation primarily to raise funds for the support of a foreign entity.

Alternatives:“Friendsof”Organization

23

To avoid equivalency determination or expenditure responsibility, the private foundation must verify that the “friends of” organization:– Has been determined by the IRS to be described in Section 501(c)(3) of

the Code;

– Has been determined by the IRS to be a public charity described in one of Sections 509(a)(1) or 509(a)(2) of the Code (or to be a supporting organization other than a non‐functionally integrated Type III supporting organization); and

– Has control and discretion with respect to the funds to be granted.

Alternatives:“Friendsof”Organization

24

Avoid earmarking (Treas. Reg. 53.4945‐5(a)(5),(6)):– The “friends of” organization must retain discretion and control with

respect to the funds granted.

– The organization must not be absolutely required to transfer the funds to the foreign entity.

– A private foundation may make grants to specific projects of a “friends of” organization that have been approved in advance by the organization.

– See Rev. Rul. 63‐252, 1963‐2 C.B. 101; Rev. Rul. 66‐79, 1966‐1 C.B. 48 (each in the context of the deductibility of individual contributions).

Alternatives:“Friendsof”Organizations

25

• A venture called “NGOsource” (http://www.ngosource.org/Home) hopes to further simplify the equivalency determination process by creating a repository for U.S. grant‐making organizations and foreign grantees.

– NGOsource is a joint project of the Council on Foundations and TechSoupGlobal – both of which are public charities.

– NGOsource applied to Treasury and the IRS seeking clarification and modification of the Proposed Regulations on equivalency determinations.

• The Proposed Regulations do not specifically address equivalency determination repositories.

NGOsource

26

The IRS considers it a best practice to obtain the following from a foreign grantee:

• Organization’s legal name in English, and in the language of origin, and any acronym or other names used to identify the organization;

• Certified copies of all organizational/governing documents and any amendments thereto;

• Statement of whether the organization is exempt from taxation under the laws of its country;

• Information regarding where the organization maintains a physical presence and the address and telephone number for each place of business;

• Organization description/history (e.g., information to substantiate the identity and integrity of the organization);

• Program/Project Description:

– If grant is for general operating support, obtain information regarding staff size and overall budget,

– If grant is for specific program/project, obtain information regarding program budget, timeline, goals/outcomes, and staff involved.

International Grant‐making Due Diligence Best Practices

27

The IRS considers it a best practice to obtain the following from a foreign grantee:

• Current list of board members, key employees, and senior management, including company affiliations, as well as information regarding their nationality, citizenship, current country of residence, and place and date of birth;

• Most current audited financial statements, if any;

• The names and addresses of individuals and organizations that receive, or will receive, funding, services, or material support from the organization to the extent such information is "reasonably discoverable";

• The names and addresses of any subcontracting organizations utilized by the organization;

• Copies of any public filings or releases made by the organization (such as official registry documents, annual reports, and annual filings); and

• Information regarding the organization’s sources of income, such as official grants, private endowments, and commercial activities.

International Grant‐making Due Diligence Best Practices

28

The IRS considers it a best practice to check the following before making a grant to a foreign grantee:

• Department of the Treasury’s List of Specially Designated Nationals (http://www.treas.gov/offices/enforcement/ofac/sdn).

• Department of State’s List of Designated Foreign Terrorist Organizations (http://www.state.gov/j/ct/rls/other/des/).

International Grant‐making Due Diligence Best Practices

29

© 2015 Quarles & Brady LLP ‐ This document provides information of a general nature. None of the information contained herein is intended as legal advice or opinion relative to specific matters, facts, situations or issues. Additional facts and information or future developments may affect the subjects addressed in this document. You should consult with a lawyer about your particular circumstances before acting on any of this information because it may not be applicable to you or your situation.

Questions?

30