administered prices and inflation targeting in thailand · pdf fileadministered prices and...

TRANSCRIPT

Administered Prices and Inflation Targeting in Thailand

Presentation at Bank of ThailandNovember 19, 2015

1

Kanin Peerawattanachart

-6

-4

-2

0

2

4

6

8

10

12

Jan

-96

Oct

-96

Jul-

97

Ap

r-9

8

Jan

-99

Oct

-99

Jul-

00

Ap

r-0

1

Jan

-02

Oct

-02

Jul-

03

Ap

r-0

4

Jan

-05

Oct

-05

Jul-

06

Ap

r-0

7

Jan

-08

Oct

-08

Jul-

09

Ap

r-1

0

Jan

-11

Oct

-11

Jul-

12

Ap

r-1

3

Jan

-14

Oct

-14

Headline Inflation

Core Inflation

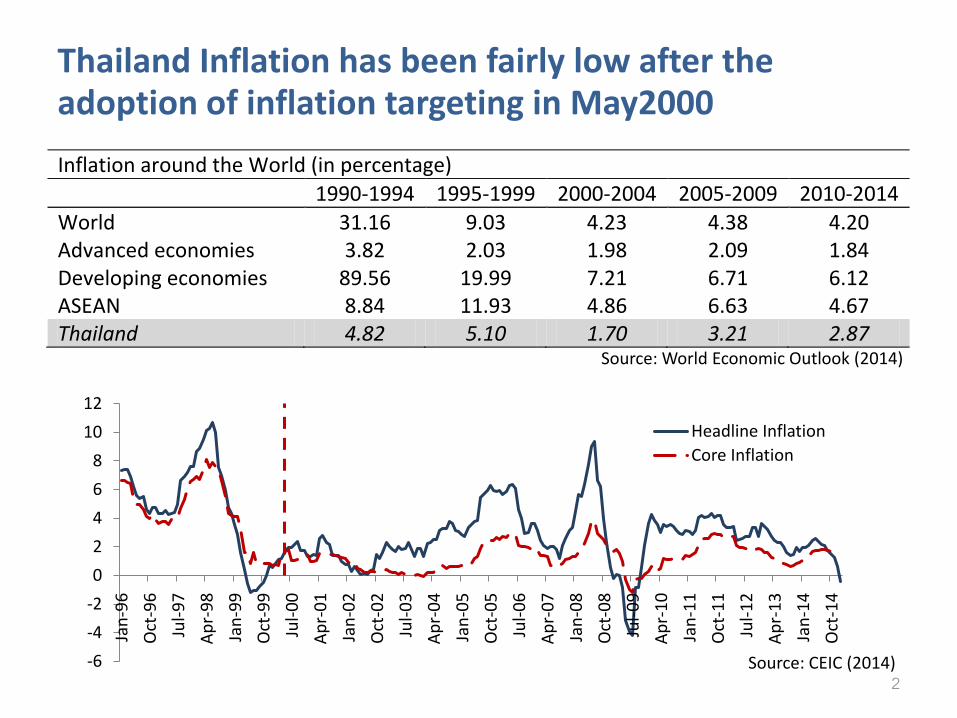

Thailand Inflation has been fairly low after the adoption of inflation targeting in May2000

2

Source: World Economic Outlook (2014)

Inflation around the World (in percentage)

1990-1994 1995-1999 2000-2004 2005-2009 2010-2014

World 31.16 9.03 4.23 4.38 4.20 Advanced economies 3.82 2.03 1.98 2.09 1.84 Developing economies 89.56 19.99 7.21 6.71 6.12 ASEAN 8.84 11.93 4.86 6.63 4.67 Thailand 4.82 5.10 1.70 3.21 2.87

Source: CEIC (2014)

BoT shifted from core inflation targeting at 0.5-3% to headline inflation targeting at 2.5% ± 1.5%

3

Switching of Inflation Targeting Regime

Core Inflation

Headline Inflation

Band Point

Reasons

Easier communication: more attentive to general public

Better anchoring: one target point

Core inflation lost ability to track underlying inflationary pressure. Thailand was the last country that use core inflation as a policy target

Administered Prices

4

Thailand’s share of administered price has always been high above 30% of the CPI Basket

Among inflation targeting countries, Thailand has the largest degree of price subsidies…

…with 135 items, they accounted for around 35% of 2011 CPI Basket

Source: BIS (2009)

5

5%

9% 10% 10%

16% 16% 17% 18% 19%21%

30%

38%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Average : 17%

30.04

38.3437.1

34.6

25.45

31.98

31.627.2

62

77

119

135

0

20

40

60

80

100

120

140

160

0

5

10

15

20

25

30

35

40

45

1998 2002 2007 2011

Weight in Headline Weight in Core Number of Items

Source: Bank of Thailand (2014)

Share of administered prices in CPI Basket Development of Administered Prices in Thailand

How could the sizable share of administered prices impact monetary policy under inflation targeting?

6

High degree of price controls

Maintaining people cost of living

Limiting prices fluctuation and provide short term relief

Coping with temporary shock when monetary policy cannot

accommodate

Distort market mechanism and do not provide long term alleviation

As control is altered, the surprising shock would drive up inflation greatly

Market does not reflect the real pricing, and inflict costs on the

economy

A consistently high proportion of government price control since 2002 could be considered as a special challenge for inflation targeting framework

• “Administered prices also set a special challenge for the inflation targeting framework. The extra measures introduced in 2009 were the main reason for the inflation target being missed in that year. Administered prices also make it harder for the BoT to assess the current state of demand. By keeping prices down, pressures on the index may be suppressed, but at the same time holding prices down gives the public more to spend on other things.”

- Grenville and Ito (2010, p.44)• Controls do not provide long term relief from inflation and do inflict costs on

the economy by distorting the pricing system. - Daniel (1975)

• Large portion of administered items in CPI of emerging economies have substantial impact on inflation volatility in the short term.

- Masson et al. (1998) and Debelle, (2001) • Price controls caused inflation to diverge from normal trend.

- Mallikamas and Ponsaparn (2005)

7

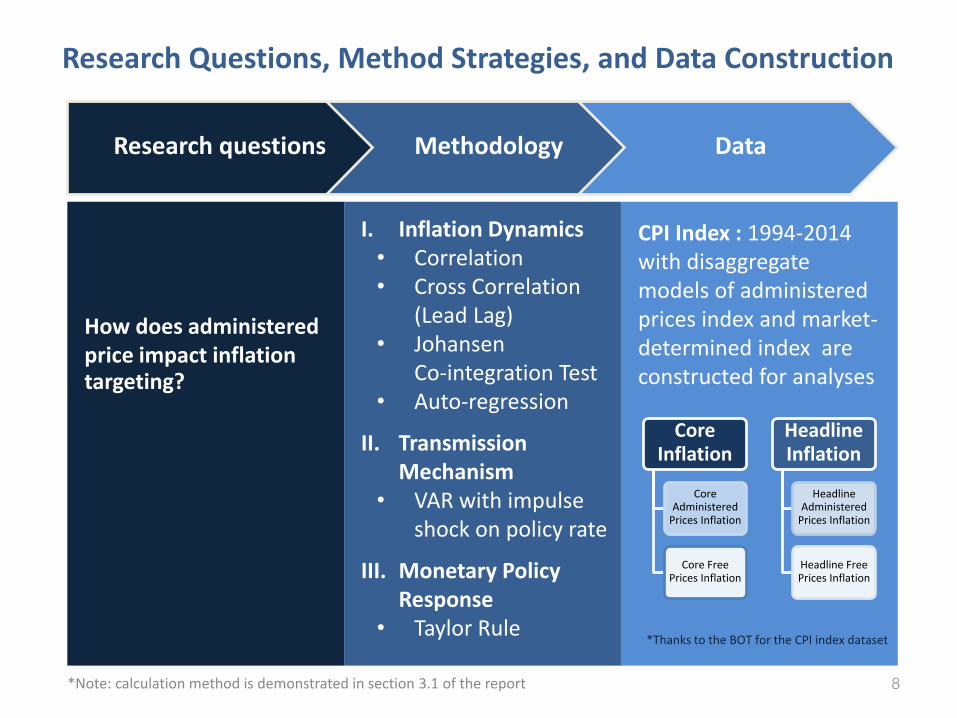

8

Research questions Methodology Data

How does administered price impact inflation targeting?

I. Inflation Dynamics• Correlation• Cross Correlation

(Lead Lag)• Johansen

Co-integration Test• Auto-regression

II. Transmission Mechanism

• VAR with impulse shock on policy rate

III. Monetary Policy Response

• Taylor Rule

CPI Index : 1994-2014 with disaggregate models of administered prices index and market-determined index are constructed for analyses

*Note: calculation method is demonstrated in section 3.1 of the report

Research Questions, Method Strategies, and Data Construction

Core Inflation

Core Administered

Prices Inflation

Core Free Prices Inflation

Headline Inflation

Headline Administered

Prices Inflation

Headline Free Prices Inflation

*Thanks to the BOT for the CPI index dataset

-15

-10

-5

0

5

10

15

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Headline Inflation

Headline admin

Headline free

Asian Financial Crisis

Global Financial Crisis

Euro Crisis

Oil shock

Containing large proportion of administered prices items, headline inflation is more volatile

Source: Bank of Thailand (2014)

9

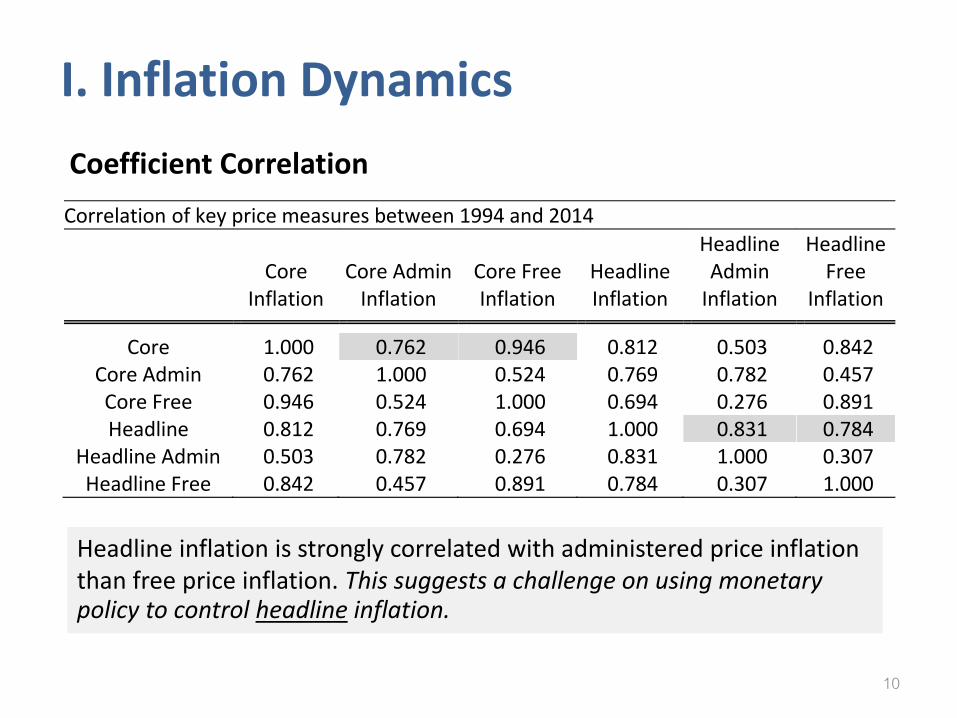

10

Correlation of key price measures between 1994 and 2014

Core

Inflation Core Admin

Inflation Core Free Inflation

Headline Inflation

Headline Admin

Inflation

Headline Free

Inflation Core 1.000 0.762 0.946 0.812 0.503 0.842

Core Admin 0.762 1.000 0.524 0.769 0.782 0.457 Core Free 0.946 0.524 1.000 0.694 0.276 0.891 Headline 0.812 0.769 0.694 1.000 0.831 0.784

Headline Admin 0.503 0.782 0.276 0.831 1.000 0.307 Headline Free 0.842 0.457 0.891 0.784 0.307 1.000

Headline inflation is strongly correlated with administered price inflation than free price inflation. This suggests a challenge on using monetary policy to control headline inflation.

Coefficient Correlation

I. Inflation Dynamics

11

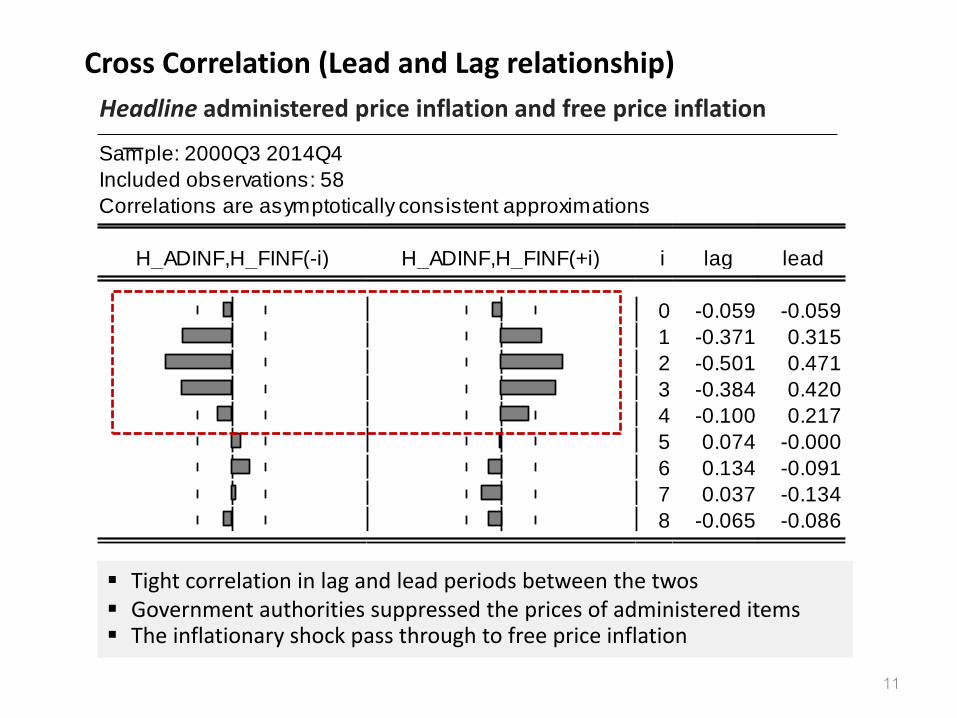

Cross Correlation (Lead and Lag relationship)

Sample: 2000Q3 2014Q4

Included observations: 58

Correlations are asymptotically consistent approximations

H_ADINF,H_FINF(-i) H_ADINF,H_FINF(+i) i lag lead

0 -0.059 -0.059

1 -0.371 0.315

2 -0.501 0.471

3 -0.384 0.420

4 -0.100 0.217

5 0.074 -0.000

6 0.134 -0.091

7 0.037 -0.134

8 -0.065 -0.086

Tight correlation in lag and lead periods between the twos Government authorities suppressed the prices of administered items The inflationary shock pass through to free price inflation

Headline administered price inflation and free price inflation

12

Johansen Co-Integration Test

Inflation Persistency (Auto-regression)

Administered prices do not have significant effect on comprehensiveness and do not reflect the underlying cost of living in the long term

Estimates of persistence in disaggregate inflation

𝜌 coefficient Prob.

Core Inflation 0.490 0.001 Core Admin Inflation 0.523 0.000 Core Free Inflation 0.771 0.000

Headline Inflation 0.297 0.021 Headline Admin Inflation 0.352 0.006 Headline Free Inflation 0.041 0.767

Given lower persistence in headline inflation, BoT has higher ability to anchor inflation expectation

𝜋𝑡 = 𝜇 + 𝜌𝜋𝑡−1 + 𝜀𝑡

*Note: Quarterly Data (%QoQ)

𝜋𝑡 = (1− 𝛾)𝜋𝑡−1 + 𝛾𝐸𝑡 𝜋𝑡+1 + 𝑣𝑡

13

II. Monetary Transmission Mechanism

Vector Auto-Regression Model

-.4

-.3

-.2

-.1

.0

.1

.2

.3

.4

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Response of headline inflation to policy rate

-.4

-.3

-.2

-.1

.0

.1

.2

.3

.4

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Response of headline free prices inflation to policy rate

Given impulse shock on policy rate, headline inflation as well as core inflation tend to adjust faster to interest rate shock than the market-determined price inflation does

Bank of Thailand should even be more forward looking as monetary policy likely takes longer horizon than expect

Note: *Model already taken into account of exogenous oil price, price puzzle still exist

10 quarters

8 quarters

Response of headline inflation to policy rate

Response of free price inflation to policy rate

14

Taylor Equation Estimation Results

Sample period (2003Q1-2014Q4)

Normal Equation Estimated by GMM

Smoothing Equation Estimated by GMM

Regression

regression

recovered

constant 𝛼 = 𝑟𝑓 + 𝜋∗ 2.948

(0.214)** 𝛼

0.929 (0.224)**

𝑟𝑓 + 𝜋∗ 2.921

output gap 𝛽2 = 𝛽𝑦 0.124

(0.116) 𝛽2

0.085 (0.049)*

𝛽𝑦 0.267

inflation gap 𝛽1 1.029

(0.187)** 𝛽1

0.327 (0.101)**

𝛽𝜋 1.028

lagged policy

𝜌 0.682

(0.079)** 𝜌 0.682

R-squared

0.555

0.914

Notes: Brackets are standard errors. “**” denotes significance level at 5%

Coefficients of inflation deviation in both equation are consistent with the Taylor principle (i.e. optimal monetary policy).

𝑖𝑡 = 𝛼 + 𝛽1 𝜋𝑡 − 𝜋∗ + 𝛽2 𝑦𝑡 − 𝑦∗ + 𝜌𝑖𝑡−1 + 𝜀𝑡

III. Monetary Policy Response

15

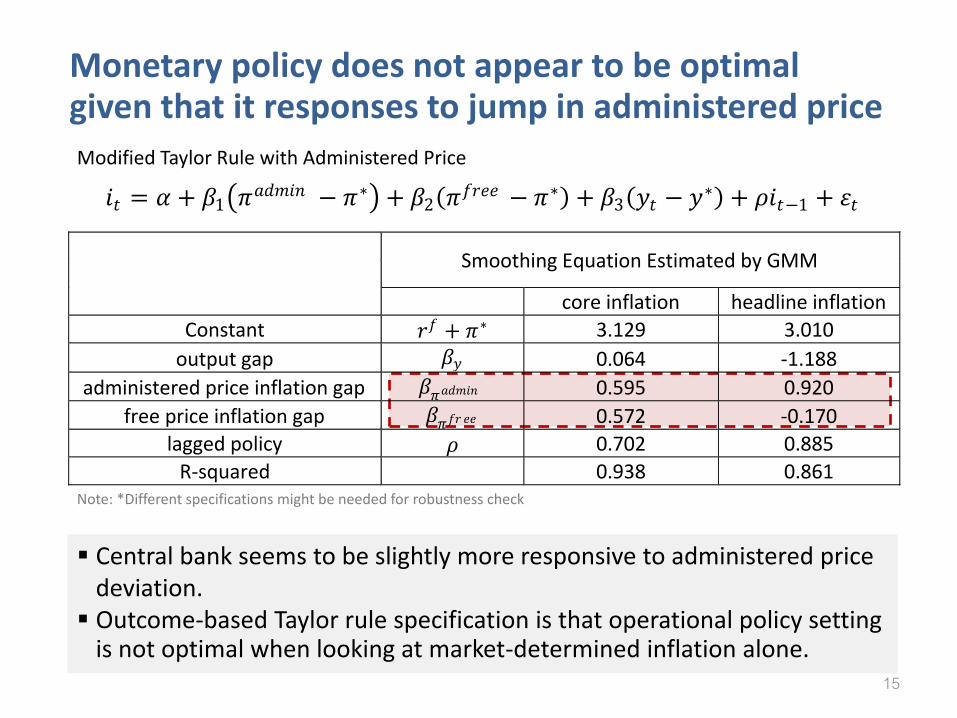

Smoothing Equation Estimated by GMM

core inflation headline inflation

Constant 𝑟𝑓 + 𝜋∗ 3.129 3.010

output gap 𝛽𝑦 0.064 -1.188

administered price inflation gap 𝛽𝜋𝑎𝑑𝑚𝑖𝑛 0.595 0.920

free price inflation gap 𝛽𝜋𝑓𝑟 𝑒𝑒 0.572 -0.170

lagged policy 𝜌 0.702 0.885

R-squared

0.938 0.861

Modified Taylor Rule with Administered Price

Central bank seems to be slightly more responsive to administered price deviation. Outcome-based Taylor rule specification is that operational policy setting

is not optimal when looking at market-determined inflation alone.

Monetary policy does not appear to be optimal given that it responses to jump in administered price

Note: *Different specifications might be needed for robustness check

𝑖𝑡 = 𝛼 + 𝛽1 𝜋𝑎𝑑𝑚𝑖𝑛 − 𝜋∗ + 𝛽2 𝜋

𝑓𝑟𝑒𝑒 − 𝜋∗ + 𝛽3 𝑦𝑡 − 𝑦∗ + 𝜌𝑖𝑡−1 + 𝜀𝑡

Conclusion

16

Price controls raise concern on controllability of Monetary Policy

Inflation process has largely been influenced by price controls Strong correlation with administered prices sector Complicated lead and lag relationship No long-term relationship between price controls and inflation Headline inflation is less persistent; better anchor expectation

Takes longer time for Monetary Policy to become fully effective

Free prices sector has slower transmission process than aggregate headline inflation with over 2 years

Optimality of Monetary Policy depends crucially on the measures of inflation

Taylor Rule holds when aggregate inflation is used to estimate Reaction function seems to exhibit higher degree of response

to deviation in administered price sector

Evolving Process of Inflation

Dynamics

1

Transmission Mechanism

2

Monetary Policy

Response

3

Coordination between Bank of Thailand and Ministry of Commerce is necessary required

17

Key Takeaways

Price controls set special challenges for monetary policy and central bank should incorporate this fact

1

Bank of Thailand should be even more forward looking in setting appropriate monetary policy

2

3

Further study: Welfare analysis on the optimal threshold for the degree of government price control (c.f. Safouane et.al. 2012)

4

THANK YOU.

18