adjustments and the ten-column work sheet

DESCRIPTION

Chapter 18. $. Adjustments and the Ten-Column Work Sheet. $. Making Accounting Relevant Financial data must be communicated properly before it can be used effectively. $. $. Discuss the types of communication skills that are important to success in the workplace. Chapter 18. - PowerPoint PPT PresentationTRANSCRIPT

Adjustments and the Ten-Column Work Sheet

Adjustments and the Ten-Column Work SheetMaking Accounting Relevant

Financial data must be communicated

properly before it can be used

effectively.

Making Accounting Relevant

Financial data must be communicated

properly before it can be used

effectively.

Discuss the types of communication skills that are important to success in the workplace.

Section 1Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory

Section 1Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory

What You’ll Learn How to complete the Trial Balance

section of the work sheet. Why certain general ledger accounts

are adjusted. Why Merchandise Inventory is

adjusted. How to calculate and record the

adjustment for Merchandise Inventory.

What You’ll Learn How to complete the Trial Balance

section of the work sheet. Why certain general ledger accounts

are adjusted. Why Merchandise Inventory is

adjusted. How to calculate and record the

adjustment for Merchandise Inventory.

Why It’s ImportantSome general ledger account

balances are adjusted, or updated, so that the general ledger correctly reflects the financial position of the business at the end of the period. This ensures the accuracy of the end-of-period reports and statements.

Why It’s ImportantSome general ledger account

balances are adjusted, or updated, so that the general ledger correctly reflects the financial position of the business at the end of the period. This ensures the accuracy of the end-of-period reports and statements.

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Key Terms adjustment

beginning inventory

Key Terms adjustment

beginning inventory

ending inventory

physical inventory

ending inventory

physical inventory

Completing End-of-Period WorkCompleting End-of-Period Work

to provide information about financial

position of business

worksheet is basis for preparing

financial statements and end-of-period

journal entries

to provide information about financial

position of business

worksheet is basis for preparing

financial statements and end-of-period

journal entries

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

The Ten-Column Work Sheet

Five amount sections:

The Ten-Column Work Sheet

Five amount sections:

Trial Balance Trial Balance

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Adjustments Adjustments

Adjusted Trial Balance Adjusted Trial Balance

Income statement Income statement

Balance Sheet Balance Sheet

Completing Trial Balance Section

Proves Equality of Debits and Credits in General Ledger

Completing Trial Balance Section

Proves Equality of Debits and Credits in General Ledger

enter number and name of each

account

even ones with zero balances

accounts listed in numerical order

enter number and name of each

account

even ones with zero balances

accounts listed in numerical order

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Completing the Trial Balance Section (con’t.)

Completing the Trial Balance Section (con’t.)

enter balance of each account in

appropriate column

Debit and Credit columns are:ruledtotaledproveddouble ruled

enter balance of each account in

appropriate column

Debit and Credit columns are:ruledtotaledproveddouble ruled

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Calculating AdjustmentsCalculating Adjustments

Some account balances change because of:internal operations of the business passage of time

Some account balances change because of:internal operations of the business passage of time

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Calculating AdjustmentsCalculating Adjustments

Adjustment: amount added to or subtracted

from an account balance brings balance up-to-date.

Adjustment: amount added to or subtracted

from an account balance brings balance up-to-date.

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Calculating AdjustmentsCalculating Adjustments

Transfer costs of assets consumed

from permanent asset accounts to

temporary expense accounts

assets are “expensed”

expenses are costs of doing

business

matches expenses with revenues

Transfer costs of assets consumed

from permanent asset accounts to

temporary expense accounts

assets are “expensed”

expenses are costs of doing

business

matches expenses with revenues

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Determining the Adjustments NeededDetermining the Adjustments Needed

If the balance shown for an

account is not up-to-date as of the

last day of the fiscal period, then

that account balance must be

adjusted.

If the balance shown for an

account is not up-to-date as of the

last day of the fiscal period, then

that account balance must be

adjusted.

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Determining the Adjustments NeededDetermining the Adjustments Needed

IS IT ADJUSTED?

Inventory

Supplies

Insurance

Taxes

IS IT ADJUSTED?

Inventory

Supplies

Insurance

Taxes

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Adjusting Merchandise InventoryAdjusting Merchandise Inventory

Merchandise on Hand is

constantly changing

Changes NOT recorded in

Merchandise Inventory

Merchandise on Hand is

constantly changing

Changes NOT recorded in

Merchandise Inventory

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Adjusting Merchandise InventoryAdjusting Merchandise Inventory

Buy Merchandise – Debit Purchases

Sell Merchandise – Credit Sales

Buy Merchandise – Debit Purchases

Sell Merchandise – Credit Sales

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Adjusting Merchandise InventoryAdjusting Merchandise Inventory

Beginning Inventory = $84,921

from general ledger

in Trial Balance

same as last period’s ending

Beginning Inventory = $84,921

from general ledger

in Trial Balance

same as last period’s ending

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Adjusting Merchandise InventoryAdjusting Merchandise Inventory

Compare Beginning to Physical

Physical Inventory = $81,385

Beginning Inventory =$84,921

Merch Inv. went down $3,536

Need to credit Merch Inv.

Debit Income Summary

Compare Beginning to Physical

Physical Inventory = $81,385

Beginning Inventory =$84,921

Merch Inv. went down $3,536

Need to credit Merch Inv.

Debit Income Summary

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Adjusting the Merchandise Inventory Account (con’t.)Adjusting the Merchandise Inventory Account (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

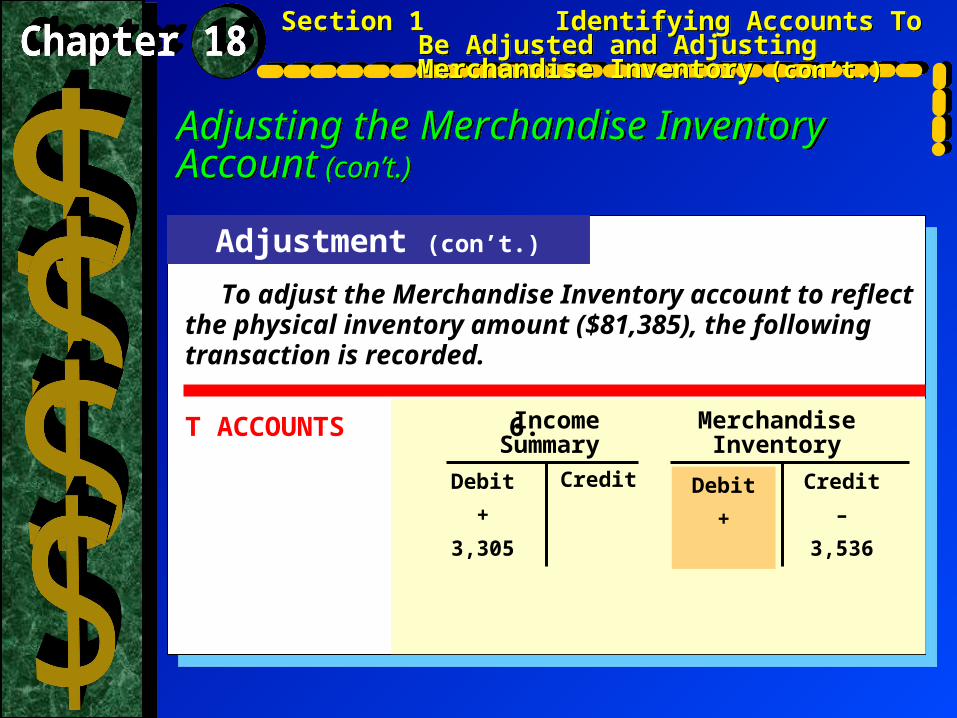

AdjustmentTo adjust the Merchandise Inventory account to reflect

the physical inventory amount ($81,385), the following transaction is recorded.

ANALYSIS Identify 1. The accounts Merchandise Inventory and Income Summary are affected. Classify 2. Merchandise Inventory is an asset account (permanent). Income Summary is a temporary capital account. + / – 3.Merchandise Inventory is decreased by $3,536. This amount is transferred to Income Summary.

Adjusting the Merchandise Inventory Account (con’t.)Adjusting the Merchandise Inventory Account (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Adjustment (con’t.)

To adjust the Merchandise Inventory account to reflect the physical inventory amount ($81,385), the following transaction is recorded.

DEBIT-CREDIT RULE 4. To transfer the decrease in Merchandise Inventory, debit Income Summary for $3,536.

5.Decreases to asset accounts are recorded as credits. Credit Merchandise Inventory for $3,536.

Adjusting the Merchandise Inventory Account (con’t.)Adjusting the Merchandise Inventory Account (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Adjustment (con’t.)

To adjust the Merchandise Inventory account to reflect the physical inventory amount ($81,385), the following transaction is recorded.

T ACCOUNTS 6. Income MerchandiseSummary Inventory

CreditDebit

+

3,305

Credit

–

3,536

Debit

+

Entering the Adjustment for Merchandise Inventory on the Work Sheet

Entering the Adjustment for Merchandise Inventory on the Work Sheet

Adjustments are entered in the

Adjustments columns of the work

sheet. The debit and credit parts of

each adjustment are given a unique

label. The label consists of a small

letter in parentheses and is placed just

above and to the left of the adjustment

amounts.

Adjustments are entered in the

Adjustments columns of the work

sheet. The debit and credit parts of

each adjustment are given a unique

label. The label consists of a small

letter in parentheses and is placed just

above and to the left of the adjustment

amounts.

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Entering the Adjustment for Merchandise Inventory on the Work Sheet (con’t.)

Entering the Adjustment for Merchandise Inventory on the Work Sheet (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Check Your UnderstandingCheck Your Understanding

What would you do if the Debit

and Credit columns of the Trial

Balance section of the work sheet

are not equal?

What would you do if the Debit

and Credit columns of the Trial

Balance section of the work sheet

are not equal?

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory (con’t.)

Section 2Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax

Section 2Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax

What You’ll Learn Why the Supplies, Prepaid Insurance,

and Federal Corporate Income Tax Expense accounts are adjusted.

How to calculate the adjustments for supplies, insurance, and federal corporate income tax.

How to enter the adjustments on the work sheet.

What You’ll Learn Why the Supplies, Prepaid Insurance,

and Federal Corporate Income Tax Expense accounts are adjusted.

How to calculate the adjustments for supplies, insurance, and federal corporate income tax.

How to enter the adjustments on the work sheet.

Why It’s Important

Account balances related to

supplies, insurance, and federal

corporate income tax required

adjustment in order to prepare

accurate financial reports.

Why It’s Important

Account balances related to

supplies, insurance, and federal

corporate income tax required

adjustment in order to prepare

accurate financial reports.

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Adjusting the Supplies AccountAdjusting the Supplies Account

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

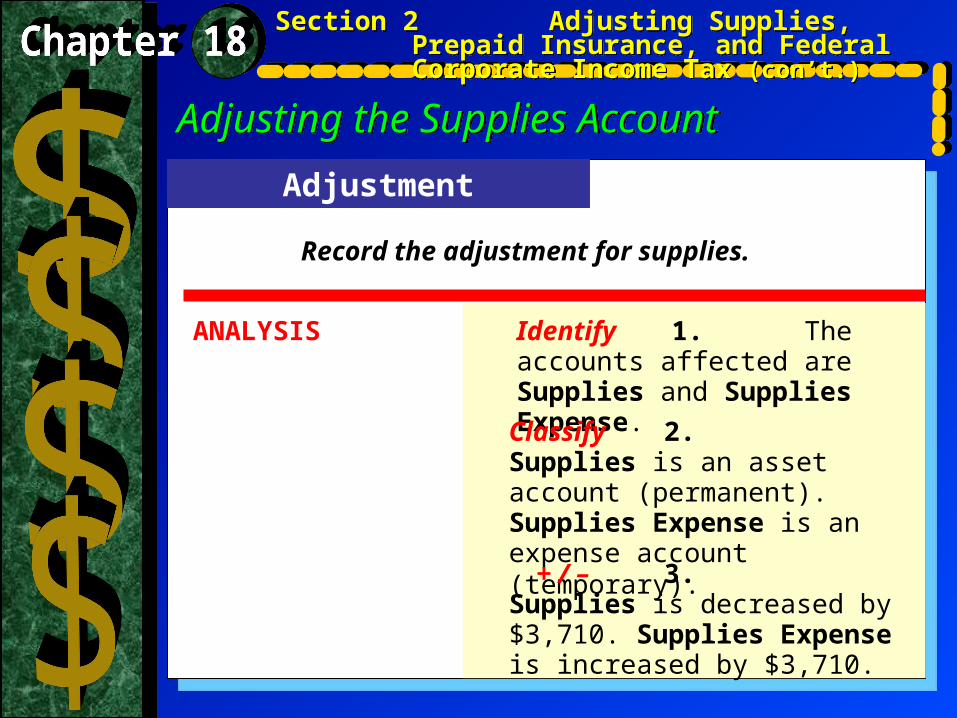

Adjustment

Record the adjustment for supplies.

ANALYSIS Identify 1. The accounts affected are Supplies and Supplies Expense.

Classify 2. Supplies is an asset account (permanent). Supplies Expense is an expense account (temporary). + / – 3.Supplies is decreased by $3,710. Supplies Expense is increased by $3,710.

Adjusting the Supplies Account (con’t.)Adjusting the Supplies Account (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

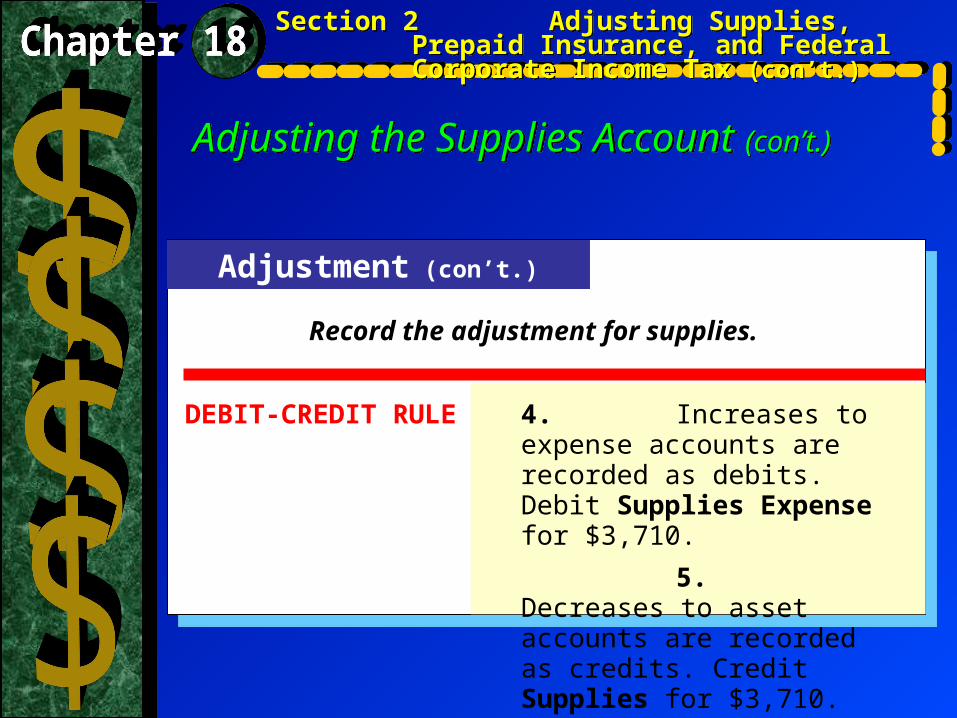

Adjustment (con’t.)

Record the adjustment for supplies.

DEBIT-CREDIT RULE 4. Increases to expense accounts are recorded as debits. Debit Supplies Expense for $3,710.

5.Decreases to asset accounts are recorded as credits. Credit Supplies for $3,710.

Adjusting the Supplies Account (con’t.)Adjusting the Supplies Account (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

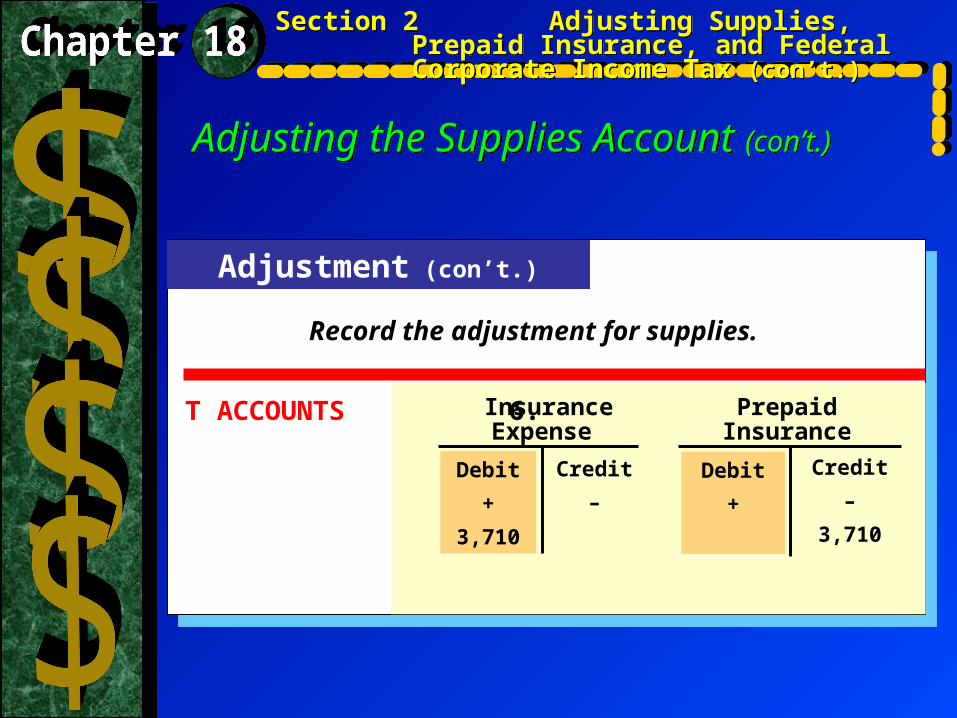

Adjustment (con’t.)

Record the adjustment for supplies.

T ACCOUNTS 6. Insurance PrepaidExpense Insurance

Debit

+

3,710

Debit

+

Credit

–

3,710

Credit

–

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

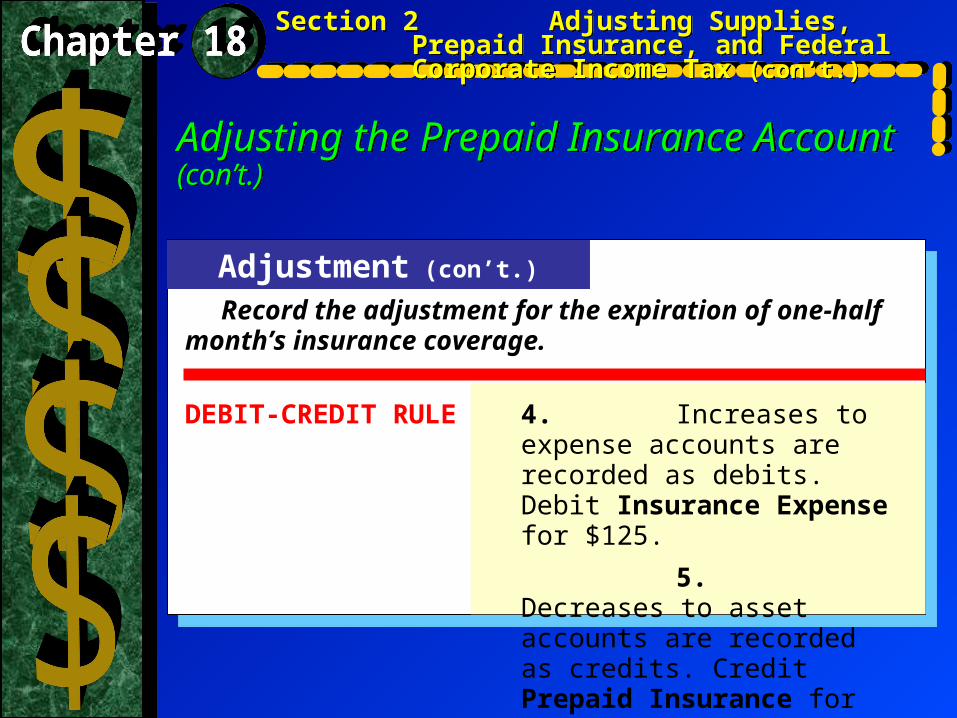

AdjustmentRecord the adjustment for the expiration of one-half

month’s insurance coverage.

ANALYSIS Identify 1. The accounts affected are Insurance Expense and Prepaid Insurance. Classify 2.

Insurance Expense is an expense account (temporary). Prepaid Insurance is an asset account (permanent). + / – 3.Insurance Expense is increased by $125. Prepaid Insurance is decreased by $125.

Adjusting the Prepaid Insurance AccountAdjusting the Prepaid Insurance Account

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Adjustment (con’t.)

DEBIT-CREDIT RULE 4. Increases to expense accounts are recorded as debits. Debit Insurance Expense for $125.

5.Decreases to asset accounts are recorded as credits. Credit Prepaid Insurance for $125.

Adjusting the Prepaid Insurance Account (con’t.)

Adjusting the Prepaid Insurance Account (con’t.)

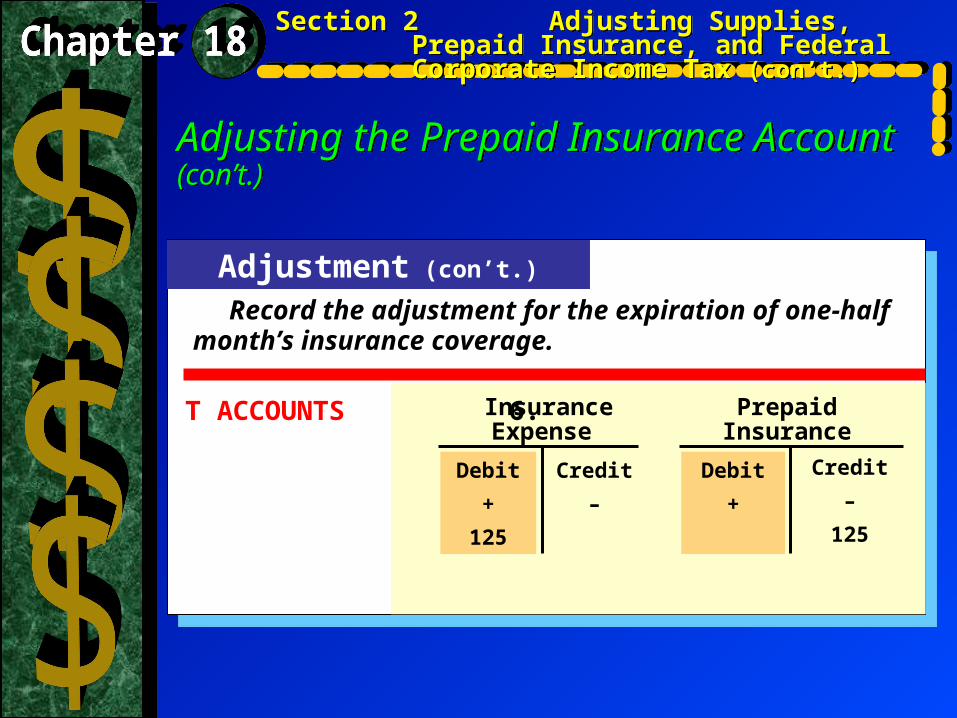

Record the adjustment for the expiration of one-half month’s insurance coverage.

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Adjustment (con’t.)

T ACCOUNTS 6. Insurance PrepaidExpense Insurance

Debit

+

125

Debit

+

Credit

–

125

Credit

–

Adjusting the Prepaid Insurance Account (con’t.)

Adjusting the Prepaid Insurance Account (con’t.)

Record the adjustment for the expiration of one-half month’s insurance coverage.

Check Your UnderstandingCheck Your Understanding

Explain how to make an

adjustment for prepaid

insurance.

Explain how to make an

adjustment for prepaid

insurance.

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax (con’t.)

Section 3Completing the Work Sheet and Journalizing and Posting the Adjusting Entries

Section 3Completing the Work Sheet and Journalizing and Posting the Adjusting EntriesWhat You’ll Learn

How to complete the Adjusted Trial Balance section.

How to extend amounts to the Income Statement and Balance sheet sections.

How to report the net income or net loss for the period.

How to journalize the adjusting entries in the general journal.

How to post the adjusting entries to the general ledger.

What You’ll Learn How to complete the Adjusted Trial

Balance section. How to extend amounts to the Income

Statement and Balance sheet sections. How to report the net income or net loss

for the period. How to journalize the adjusting entries in

the general journal. How to post the adjusting entries to the

general ledger.

Why It’s Important

The work sheet is the source

of information for journalizing the

adjusting entries and preparing

the financial statements.

Why It’s Important

The work sheet is the source

of information for journalizing the

adjusting entries and preparing

the financial statements.

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Completing the Adjusted Trial Balance SectionCompleting the Adjusted Trial Balance Section

Once the adjustments are entered

in the Adjustments section of the work

sheet, it is important to prove that the

accounts are still in balance. This is

done by completing an adjusted trial

balance.

Once the adjustments are entered

in the Adjustments section of the work

sheet, it is important to prove that the

accounts are still in balance. This is

done by completing an adjusted trial

balance.

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Extending Amounts to the Balance Sheet and Income Statement Sections

Extending Amounts to the Balance Sheet and Income Statement Sections

Beginning with line 1, each

account balance in the Adjusted Trial

Balance section is extended to the

appropriate column of either the

Balance Sheet section or the Income

Statement section.

Beginning with line 1, each

account balance in the Adjusted Trial

Balance section is extended to the

appropriate column of either the

Balance Sheet section or the Income

Statement section.

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Completing the Work SheetCompleting the Work Sheet

After all amounts are extended to the

Balance Sheet and Income Statement

sections, a single rule is drawn across

the columns in these sections.

All four columns are then totaled.

The difference between the two

column totals in each section is the

amount of net income (or net loss) for

the period.

After all amounts are extended to the

Balance Sheet and Income Statement

sections, a single rule is drawn across

the columns in these sections.

All four columns are then totaled.

The difference between the two

column totals in each section is the

amount of net income (or net loss) for

the period.

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Completing the Work Sheet (con’t.)Completing the Work Sheet (con’t.)

After the net income (or net loss) is

recorded, the columns in the

Balance Sheet and Income

Statement sections are ruled and

totaled.

A double rule is drawn across all

four columns.

After the net income (or net loss) is

recorded, the columns in the

Balance Sheet and Income

Statement sections are ruled and

totaled.

A double rule is drawn across all

four columns.

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Journalizing AdjustmentsJournalizing Adjustments

The journal entries that update the

general ledger accounts at the end of

a period are called adjusting entries.

The source of information for

journalizing the adjusting entries is

the Adjustments section of the work

sheet.

The journal entries that update the

general ledger accounts at the end of

a period are called adjusting entries.

The source of information for

journalizing the adjusting entries is

the Adjustments section of the work

sheet.

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Journalizing Adjustments (con’t.)Journalizing Adjustments (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Posting Adjusting Entries to the General LedgerPosting Adjusting Entries to the General Ledger

After the adjusting entries are

recorded in the general journal, they

are posted to the general ledger

accounts.

Once the adjusting entries are

posted, the general ledger accounts

are up-to-date.

After the adjusting entries are

recorded in the general journal, they

are posted to the general ledger

accounts.

Once the adjusting entries are

posted, the general ledger accounts

are up-to-date.

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Check Your UnderstandingCheck Your Understanding

Which types of general ledger

accounts appear in the Balance

Sheet section of the work sheet?

Which types of general ledger

accounts appear in the Balance

Sheet section of the work sheet?

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)

Section 3 Completing the Work Sheet & Journalizing & Posting the Adjusting Entries (con’t.)