adirondack mountain club, inc. financial … · adirondack mountain club, inc. ... carol a....

TRANSCRIPT

ADIRONDACK MOUNTAIN CLUB, INC.

FINANCIAL REPORT

DECEMBER 31, 2016

ADIRONDACK MOUNTAIN CLUB, INC.

TABLE OF CONTENTS

PAGE

INDEPENDENT AUDITOR’S REPORT 1-2

STATEMENTS OF FINANCIAL POSITION 3

STATEMENTS OF ACTIVITIES 4

STATEMENTS OF CASH FLOWS 5

NOTES TO FINANCIAL STATEMENTS 6-17

SCHEDULE OF FUNCTIONAL EXPENSES 18

1.

INDEPENDENT AUDITOR’S REPORT

To the Board of Directors

Adirondack Mountain Club, Inc.

Report on the Financial Statements

We have audited the accompanying financial statements of Adirondack Mountain

Club, Inc. (the Club), which comprise the statements of financial position as of

December 31, 2016 and 2015, and the related statements of activities and cash

flows for the years then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these

financial statements in accordance with accounting principles generally accepted in

the United States of America; this includes the design, implementation, and

maintenance of internal control relevant to the preparation and fair presentation of

financial statements that are free from material misstatement, whether due to fraud

or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on

our audits. We conducted our audits in accordance with auditing standards

generally accepted in the United States of America. Those standards require that we

plan and perform the audit to obtain reasonable assurance about whether the

financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the

amounts and disclosures in the financial statements. The procedures selected

depend on the auditor’s judgment, including the assessment of the risks of material

misstatement of the financial statements, whether due to fraud or error. In making

those risk assessments, the auditor considers internal control relevant to the entity’s

preparation and fair presentation of the financial statements in order to design audit

procedures that are appropriate in the circumstances, but not for the purpose of

expressing an opinion on the effectiveness of the entity’s internal control.

Accordingly, we express no such opinion. An audit also includes evaluating the

appropriateness of accounting policies used and the reasonableness of significant

accounting estimates made by management, as well as evaluating the overall

presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to

provide a basis for our audit opinion.

11 British American Blvd. Latham, New York 12110-1405 | P: 518-785-0134 | F: 518-785-0299

111 Everts Ave. Queensbury, NY 12804 | P: 518-792-6595 | F: 518-792-6635

www.marvincpa.com

Kevin J. McCoy, CPA

Thomas W. Donovan, CPA

Frank S. Venezia, CPA

James E. Amell, CPA

Carol A. Hausamann, CPA

Daniel J. Litz, CPA

Karl F. Newton, CPA

Kevin P. O’Leary, CPA

Heather R. Lewis, CPA

Heather D. Patten, CPA

An Independent Member of the BDO Alliance USA

2.

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the

financial position of Adirondack Mountain Club, Inc. as of December 31, 2016 and 2015, and the changes

in its net assets and its cash flows for the years then ended in accordance with accounting principles

generally accepted in the United States of America.

Report on Supplementary Information

Our audits were conducted for the purpose of forming an opinion on the financial statements as a whole.

The schedule of functional expenses on page 18 is presented for purposes of additional analysis and is

not a required part of the financial statements. Such information is the responsibility of management and

was derived from and relates directly to the underlying accounting and other records used to prepare the

financial statements. The information has been subjected to the auditing procedures applied in the audit

of the financial statements and certain additional procedures, including comparing and reconciling such

information directly to the underlying accounting and other records used to prepare the financial

statements or to the financial statements themselves, and other additional procedures in accordance with

auditing standards generally accepted in the United States of America. In our opinion, the information is

fairly stated in all material respects in relation to the financial statements as a whole.

Marvin and Company, P.C.

Latham, NY

March 30, 2017

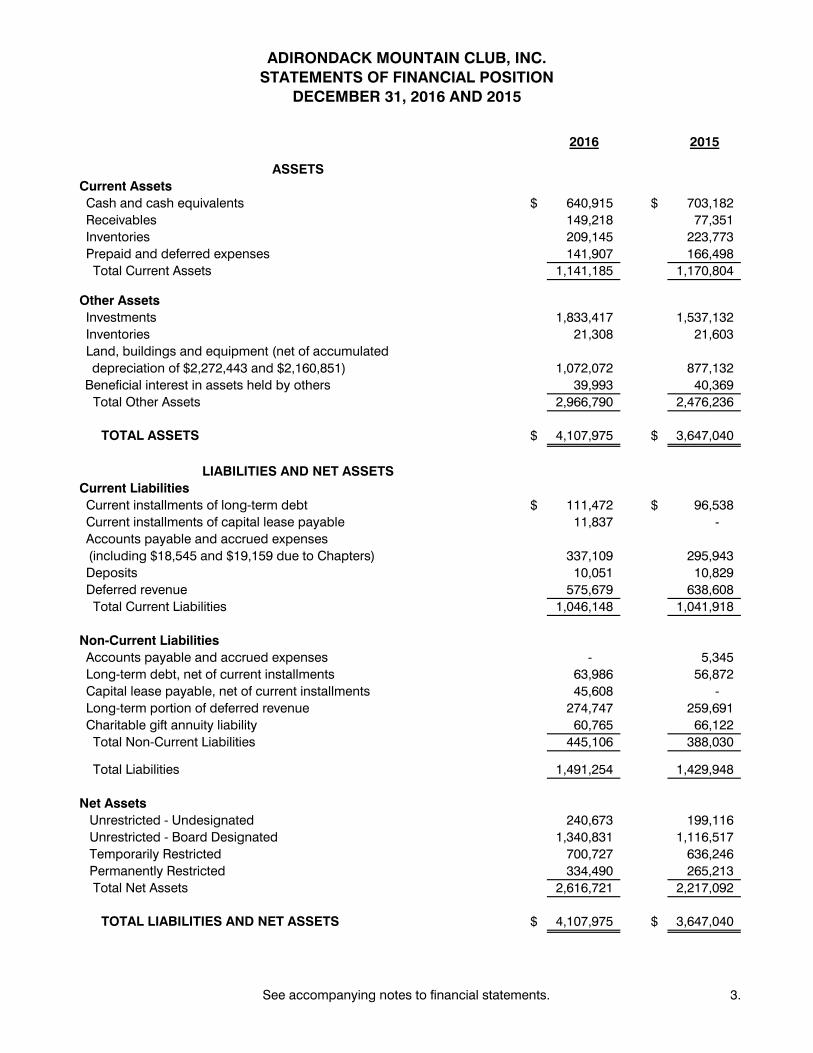

2016 2015

ASSETS

Current Assets

Cash and cash equivalents $ 640,915 $ 703,182

Receivables 149,218 77,351

Inventories 209,145 223,773

Prepaid and deferred expenses 141,907 166,498

Total Current Assets 1,141,185 1,170,804

Other Assets

Investments 1,833,417 1,537,132

Inventories 21,308 21,603

Land, buildings and equipment (net of accumulated

depreciation of $2,272,443 and $2,160,851) 1,072,072 877,132

Beneficial interest in assets held by others 39,993 40,369

Total Other Assets 2,966,790 2,476,236

TOTAL ASSETS $ 4,107,975 $ 3,647,040

LIABILITIES AND NET ASSETS

Current Liabilities

Current installments of long-term debt $ 111,472 $ 96,538

Current installments of capital lease payable 11,837 -

Accounts payable and accrued expenses

(including $18,545 and $19,159 due to Chapters) 337,109 295,943

Deposits 10,051 10,829

Deferred revenue 575,679 638,608

Total Current Liabilities 1,046,148 1,041,918

Non-Current Liabilities

Accounts payable and accrued expenses - 5,345

Long-term debt, net of current installments 63,986 56,872

Capital lease payable, net of current installments 45,608 -

Long-term portion of deferred revenue 274,747 259,691

Charitable gift annuity liability 60,765 66,122

Total Non-Current Liabilities 445,106 388,030

Total Liabilities 1,491,254 1,429,948

Net Assets

Unrestricted - Undesignated 240,673 199,116

Unrestricted - Board Designated 1,340,831 1,116,517

Temporarily Restricted 700,727 636,246

Permanently Restricted 334,490 265,213

Total Net Assets 2,616,721 2,217,092

TOTAL LIABILITIES AND NET ASSETS $ 4,107,975 $ 3,647,040

DECEMBER 31, 2016 AND 2015

STATEMENTS OF FINANCIAL POSITION

ADIRONDACK MOUNTAIN CLUB, INC.

See accompanying notes to financial statements. 3.

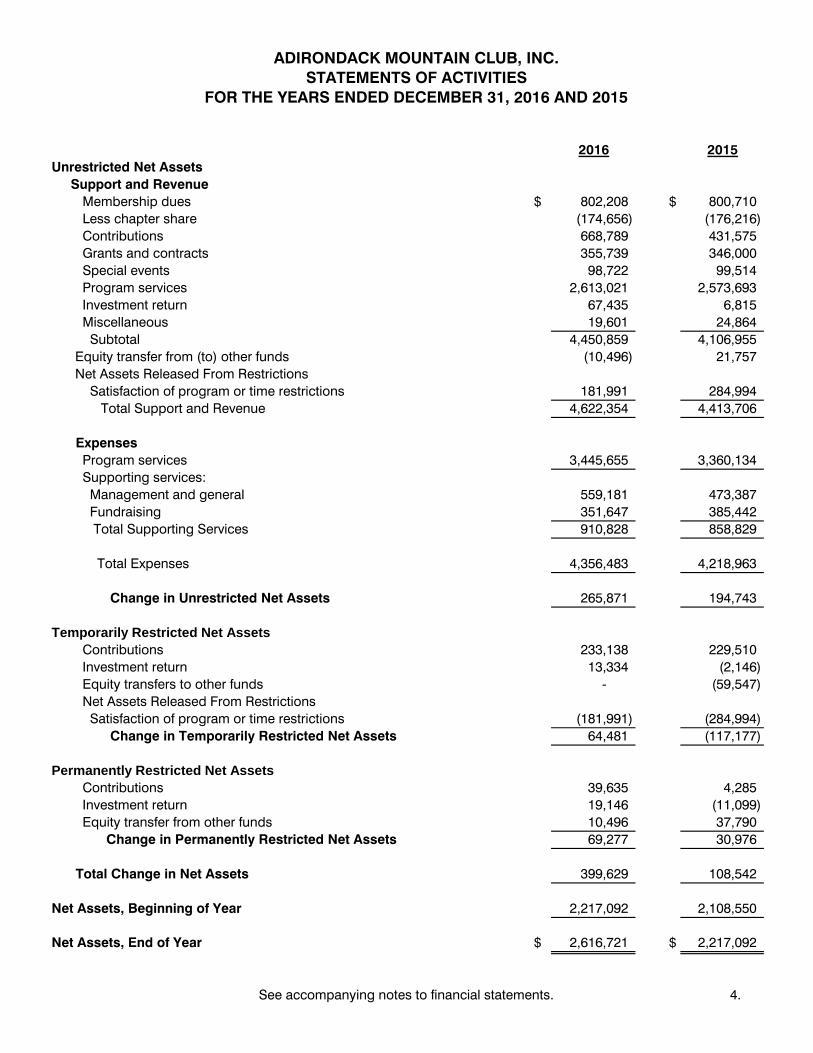

2016 2015

Unrestricted Net Assets

Support and Revenue

Membership dues $ 802,208 $ 800,710

Less chapter share (174,656) (176,216)

Contributions 668,789 431,575

Grants and contracts 355,739 346,000

Special events 98,722 99,514

Program services 2,613,021 2,573,693

Investment return 67,435 6,815

Miscellaneous 19,601 24,864

Subtotal 4,450,859 4,106,955

Equity transfer from (to) other funds (10,496) 21,757

Net Assets Released From Restrictions

Satisfaction of program or time restrictions 181,991 284,994

Total Support and Revenue 4,622,354 4,413,706

Expenses

Program services 3,445,655 3,360,134

Supporting services:

Management and general 559,181 473,387

Fundraising 351,647 385,442

Total Supporting Services 910,828 858,829

Total Expenses 4,356,483 4,218,963

Change in Unrestricted Net Assets 265,871 194,743

Temporarily Restricted Net Assets

Contributions 233,138 229,510

Investment return 13,334 (2,146)

Equity transfers to other funds - (59,547)

Net Assets Released From Restrictions

Satisfaction of program or time restrictions (181,991) (284,994)

Change in Temporarily Restricted Net Assets 64,481 (117,177)

Permanently Restricted Net Assets

Contributions 39,635 4,285

Investment return 19,146 (11,099)

Equity transfer from other funds 10,496 37,790

Change in Permanently Restricted Net Assets 69,277 30,976

Total Change in Net Assets 399,629 108,542

Net Assets, Beginning of Year 2,217,092 2,108,550

Net Assets, End of Year $ 2,616,721 $ 2,217,092

ADIRONDACK MOUNTAIN CLUB, INC.

STATEMENTS OF ACTIVITIES

FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015

See accompanying notes to financial statements. 4.

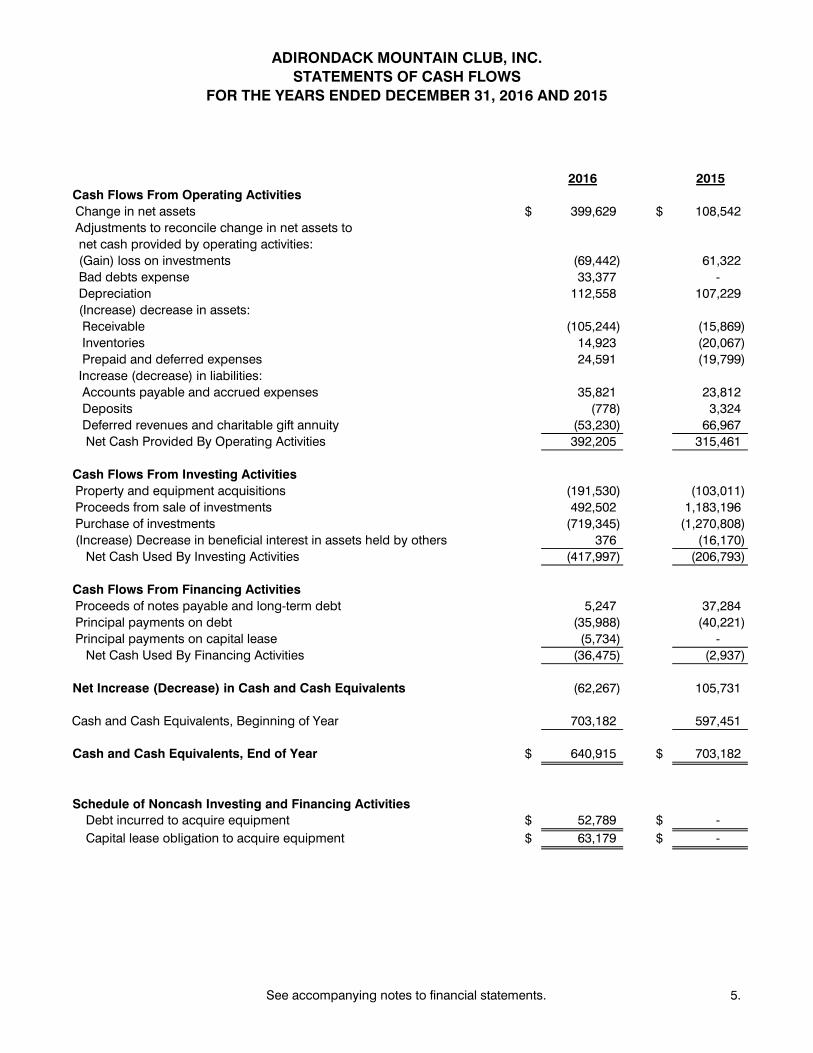

2016 2015

Cash Flows From Operating Activities

Change in net assets $ 399,629 $ 108,542

Adjustments to reconcile change in net assets to

net cash provided by operating activities:

(Gain) loss on investments (69,442) 61,322

Bad debts expense 33,377 -

Depreciation 112,558 107,229

(Increase) decrease in assets:

Receivable (105,244) (15,869)

Inventories 14,923 (20,067)

Prepaid and deferred expenses 24,591 (19,799)

Increase (decrease) in liabilities:

Accounts payable and accrued expenses 35,821 23,812

Deposits (778) 3,324

Deferred revenues and charitable gift annuity (53,230) 66,967

Net Cash Provided By Operating Activities 392,205 315,461

Cash Flows From Investing Activities

Property and equipment acquisitions (191,530) (103,011)

Proceeds from sale of investments 492,502 1,183,196

Purchase of investments (719,345) (1,270,808)

(Increase) Decrease in beneficial interest in assets held by others 376 (16,170)

Net Cash Used By Investing Activities (417,997) (206,793)

Cash Flows From Financing Activities

Proceeds of notes payable and long-term debt 5,247 37,284

Principal payments on debt (35,988) (40,221)

Principal payments on capital lease (5,734) -

Net Cash Used By Financing Activities (36,475) (2,937)

Net Increase (Decrease) in Cash and Cash Equivalents (62,267) 105,731

Cash and Cash Equivalents, Beginning of Year 703,182 597,451

Cash and Cash Equivalents, End of Year $ 640,915 $ 703,182

Schedule of Noncash Investing and Financing Activities

Debt incurred to acquire equipment $ 52,789 $ -

Capital lease obligation to acquire equipment $ 63,179 $ -

ADIRONDACK MOUNTAIN CLUB, INC.

STATEMENTS OF CASH FLOWS

FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015

See accompanying notes to financial statements. 5.

6.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

The Adirondack Mountain Club, Inc., (the Club) founded in 1922, is a nonprofit, membership-

supported conservation, recreation and educational organization devoted to promoting the

protection and enlightened use of the Forest Preserve of New York State and of the Adirondack

and Catskill Parks.

Basis of Presentation

The Club reports information regarding its financial position and activities according to three

classes of net assets: unrestricted net assets, temporarily restricted net assets, and permanently

restricted net assets, see Notes 12, 13 and 14.

In addition, the Club reports unrestricted net assets as follows:

Undesignated and Board Designated - operating funds, which include unrestricted, and

board designated resources, represent the portion of expendable funds that are available

for support of Club operations.

Cash and Cash Equivalents

The Club considers all highly liquid investments with an initial maturity of three months or less to

be cash equivalents.

Investments

The Club records investments at fair value. Fair value is determined based on quoted prices in

active markets. The Club's policy is to invest in diversified mutual funds to minimize risk and

obtain an adequate return. For internal purposes, earnings are transferred to operations based

on a reasonable rate of return, determined annually. The Club used a rate of return of 4% for

2016 and 2015; $42,971 and $43,963 were considered investment earnings available for

operations for 2016 and 2015, respectively.

Inventories

Inventories consist of publications, merchandise for resale and food and are carried at the lower

of weighted average cost or market, principally on the first-in, first-out method. The Club is also

including certain labor costs related to new editions of self-published books in inventory. During

2016 and 2015, approximately $12,100 and $14,400 of salaries and related costs were

capitalized into inventory, respectively.

7.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Land, Buildings and Equipment

Land, buildings and equipment are carried at cost or, if donated, at the approximate fair value at

the date of donation. Repairs and maintenance are charged to expense as incurred.

Depreciation of buildings and equipment is provided on a straight-line basis over the following

estimated useful lives:

Years

Buildings and Improvements 10-31

Equipment and Furniture 3-10

Vehicles 3-5

Revenue Recognition

Program Service Income

Program service income includes lodging, workshops and seminars, and outings. Revenue is

recognized when the activity takes place. Deposits received in advance are recorded as deferred

revenue.

Sales

The Club receives revenue from the sale of publications and merchandise. Sales are recognized

when shipped to or picked up by the customer.

Membership Dues

The unearned portion of membership dues is classified as deferred revenue. Life membership

dues received during the year are recorded as deferred revenue and recognized over 20-25

years.

Contributions

All contributions are considered available for the Club’s general programs unless specifically

restricted by the donor. Amounts received that are designated for future periods or restricted by

the donor are reported as temporarily or permanently restricted support and increase the

respective class of net assets. Dividend and interest income that is limited to specific uses by

donor restrictions is reported as increases in restricted net assets.

Pledges receivable in the accompanying statements of financial position, if any, consist of

unconditional promises to give, which are recorded at their net realizable value at the time the

promises are received. These promises to give are reflected as either current or long-term

receivables on the statement of financial position. There were no pledges receivable at

December 31, 2016 and 2015.

8.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Bad Debts

The Club uses the direct write-off method of accounting for bad debts, which approximates the

allowance method.

Income Taxes

The Club is exempt from federal income tax under Section 501(c)(3) of the Internal Revenue

Code, except for net income derived from unrelated business activities. Under Accounting

Standards Codification (ASC) Section 740, the tax status of tax-exempt entities is an uncertain tax

position since events could potentially occur that jeopardize tax-exempt status. Management is

not aware of any events that could jeopardize the Club’s tax-exempt status. The Club has

advertising revenue which is subject to tax on unrelated business income, but has no net income

from advertising activities and therefore has not recorded a tax liability. The Club believes that it

has appropriate support for any tax positions taken, and as such, does not have any uncertain

tax positions that are material to the financial statements.

In addition, the Club qualifies for the charitable contribution deduction under Section 170(b)(1)(A)

and has been classified as an organization other than a private foundation under Section

509(a)(2).

The Club is subject to routine audits by the taxing authorities until the expiration of the related

statutes of limitations. There are currently no examinations of the Club’s tax returns in progress.

Statement of Cash Flows

Cash paid for interest on debt was $5,908 in 2016 and $5,597 in 2015.

Use of Estimates

Management uses estimates and assumptions in preparing financial statements. Those

estimates and assumptions affect the reported amounts of assets and liabilities, the disclosure of

contingent assets and liabilities, and the reported revenues and expenses. Actual results could

differ from those estimates.

Related Entity

ADK Mountain Club Foundation, Inc. (the Foundation) is tax exempt under Section 501(c)(3) of

the Internal Revenue Code. The primary purpose of the Foundation is to raise funds for the

support of the charitable, conservation of natural resources, outdoor recreation and educational

programs and activities of the Club. The Foundation and the Club share certain Board members.

When the Foundation begins activity it will be consolidated into the Club financial statements.

There have been no significant transactions between the Foundation and the Club during 2016

and 2015.

9.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

2. RECEIVABLES

Receivables are as follows:

2016 2015

Publications sales $ 19,220 $ 57,215

Grants and other 129,998 20,136

Total Receivables $ 149,218 $ 77,351

3. INVENTORIES

Inventories are as follows:

2016 2015

Publications $ 64,906 $ 74,647

Resale items 158,313 163,582

Food 7,234 7,147

Total Inventories $ 230,453 $ 245,376

Included in publications inventories are books with a cost of $21,308 and $21,603 at December

31, 2016 and 2015, respectively, that are not expected to be sold within the next year.

4. RISKS AND UNCERTAINTIES

The Club invests in various investment securities. Investment securities are exposed to various

risks such as interest rate, market and credit risks. Due to the level of risk associated with certain

investment securities, it is at least reasonably possible that changes in the values of investment

securities will occur in the near-term and that such changes could materially affect account

balances and the amounts reported in the statements of financial position.

5. INVESTMENTS

Investments are recorded at fair value (Level 1) and consist of the following:

2016 2015

Money market funds $ 23,044 $ 34,618

Bond mutual funds 871,382 601,225

Balanced mutual funds 377,081 499,126

Equity mutual funds 558,874 402,163

Stocks 3,036. -

Total Investments $ 1,833,417 $ 1,537,132

At December 31, 2016 and 2015 there were net unrealized gains (losses) on investments of

approximately $57,710 and $(65,284), respectively.

Level 1 valuations are based on quoted prices in active markets for identical assets or liabilities.

Valuation adjustments are not applied to Level 1 instruments. Since valuations are based on

quoted prices that are readily and regularly available in an active market, valuation of these

products does not entail a significant degree of judgment.

10.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

5. INVESTMENTS

Investment return is summarized as follows:

2016 2015

Interest and dividend income $ 30,473 $ 54,892

Net realized and unrealized gains (losses) on investments

carried at fair value

69,442

(61,322)

Total Investment Return $ 99,915 $ (6,430)

Also, see Note 16 for fair value disclosures over the split interest agreements.

6. LAND, BUILDINGS AND EQUIPMENT

2016 2015

Land $ 195,761 $ 195,761

Land improvements 167,725 167,725

Buildings and improvements 1,695,285 1,575,470

Equipment and furniture 1,043,663 911,734

Vehicles 242,081 187,293

Total 3,344,515 3,037,983

Less accumulated depreciation 2,272,443 2,160,851

Net Land, Buildings and Equipment $ 1,072,072 $ 877,132

Depreciation expense was $112,558 and $107,229 for December 31, 2016 and 2015,

respectively.

7. DEFERRED REVENUE

2016 2015

Deferred membership dues $ 236,013 $ 241,747

Life memberships 287,897 273,091

Deposits on future outings 91,608 145,502

Lodging 203,798 205,172

Advertising 405 -

Educational programs 8,936 10,456

Other 21,769 22,331

Total Deferred Revenue 850,426 898,299

Less noncurrent portion of life and multi-year memberships 274,747 259,691

Net Deferred Revenue $ 575,679 $ 638,608

11.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

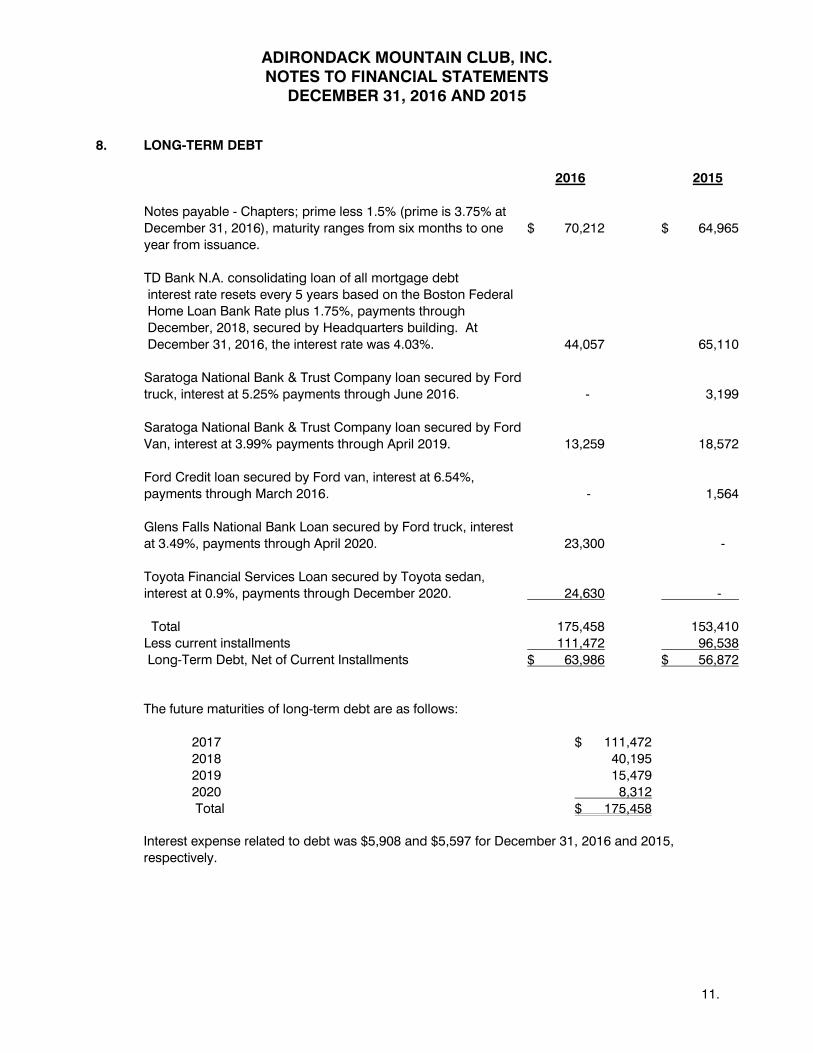

8. LONG-TERM DEBT

2016 2015

Notes payable - Chapters; prime less 1.5% (prime is 3.75% at

December 31, 2016), maturity ranges from six months to one

year from issuance.

$ 70,212

$ 64,965

TD Bank N.A. consolidating loan of all mortgage debt

interest rate resets every 5 years based on the Boston Federal

Home Loan Bank Rate plus 1.75%, payments through

December, 2018, secured by Headquarters building. At

December 31, 2016, the interest rate was 4.03%.

44,057

65,110

Saratoga National Bank & Trust Company loan secured by Ford

truck, interest at 5.25% payments through June 2016.

-

3,199

Saratoga National Bank & Trust Company loan secured by Ford

Van, interest at 3.99% payments through April 2019.

13,259

18,572

Ford Credit loan secured by Ford van, interest at 6.54%,

payments through March 2016.

-

1,564

Glens Falls National Bank Loan secured by Ford truck, interest

at 3.49%, payments through April 2020.

23,300

-

Toyota Financial Services Loan secured by Toyota sedan,

interest at 0.9%, payments through December 2020.

24,630

-

Total 175,458 153,410

Less current installments 111,472 96,538

Long-Term Debt, Net of Current Installments $ 63,986 $ 56,872

The future maturities of long-term debt are as follows:

2017 $ 111,472

2018 40,195

2019 15,479

2020 8,312

Total $ 175,458

Interest expense related to debt was $5,908 and $5,597 for December 31, 2016 and 2015,

respectively.

12.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

9. CAPITAL LEASE

The Club is the lessee of office equipment under a capital lease which expires in 2021. The

assets and liabilities under the lease are recorded at the lower of the present value of the

minimum lease payments or the fair value of the asset. The assets are amortized over their

estimated productive lives. Amortization of assets under capital leases is included in depreciation

expense.

The following is an analysis of the leased assets included in property and equipment:

Equipment $ 63,179

Less: accumulated depreciation 4,063

Total $ 59,116

The following is a schedule of future minimum lease payments under the lease for the years

ending December 31:

2017 $ 14,045

2018 14,045

2019 14,045

2020 14,045

2021 7,022

Total minimum lease payments 63,202

Less: amount representing interest 5,757

Present value of minimum lease payments $ 57,445

10. DONATED MATERIALS AND SERVICES

Donated materials and equipment are recorded in the financial statements at their estimated fair

values at the date of receipt. No amounts have been reflected in the financial statements for

donated services since those services do not meet the criteria for recognition under accounting

principles generally accepted in the United States of America. The Club pays for most services

requiring specific expertise. However, many individuals volunteer their time and perform a variety

of tasks that assist the Club with specific program services and various committee assignments.

11. FUNCTIONAL ALLOCATION OF EXPENSES

The costs of providing program and other activities have been summarized on a functional basis

in the statement of activities. Accordingly, certain costs have been allocated between the

program and supporting services benefited. Labor related costs are allocated based on labor

dollars; occupancy related costs are allocated based on facility usage.

13.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

12. UNRESTRICTED BOARD DESIGNATED NET ASSETS

Unrestricted board designated net assets at December 31 are as follows:

2016 2015

Memorial Fund $ 225,870 $ 215,722

Sean Kelleher Fund 7,289 7,123

Education Fund 39,229 36,330

Sinking Capital/Land Trust Fund 37,449 30,061

Natural History Endowment Fund 28,962 28,303

George B. Duncan Fund 459,005 448,568

Slater Trust Fund 112,434 109,877

Maegan E. Spindler Education Fund (a) - 8,779

Grow ADK Fund 410,306 211,659

Future Capital Outlay Fund 20,287 20,095

Total Board Designated Net Assets $ 1,340,831 $ 1,116,517

The Board invests these funds in a manner similar to endowment funds. See Note 14.

(a) During 2016, this fund was moved to permanently restricted net assets once the balance

reached $10,000.

13. TEMPORARILY RESTRICTED NET ASSETS

Temporarily restricted funds at December 31 are as follows:

2016 2015

Restricted for specific purposes:

Jamieson Fund (conservation easements) $ 67,195 $ 62,894

Education 213,306 179,357

Lecture series 522 583

Membership - 18,244

Johns Brook Lodge 2,050 13,405

Loj 43,345 30,136

Publications 830 830

President’s Library Fund 8,013 8,013

Advocacy 210,776 148,344

Trails 5,009 19,148

Charitable Gift Annuity 72,312 66,122

Wilderness Legal Defense Fund 50,021 37,144

46R#507 Fund - 15,220

Summit Stewards 5,468 -

Other 21,880 36,806

Total Temporarily Restricted Net Assets $ 700,727 $ 636,246

Amounts reported in the statements of financial position as beneficial interest in assets held by

others represent the net cumulative transfers by the Club to the Adirondack Foundation, as well

as earnings thereon. These amounts totaled $39,993 and $40,369 at December 31, 2016 and

2015, respectively. The Foundation holds and invests the funds on behalf of the Club’s

temporarily restricted Wilderness Legal Defense Fund and in 2015, the 46R#507 Fund. The

Foundation has no decision making authority over the funds. Instead, the funds are distributed to

the Club upon request to the Foundation.

14.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

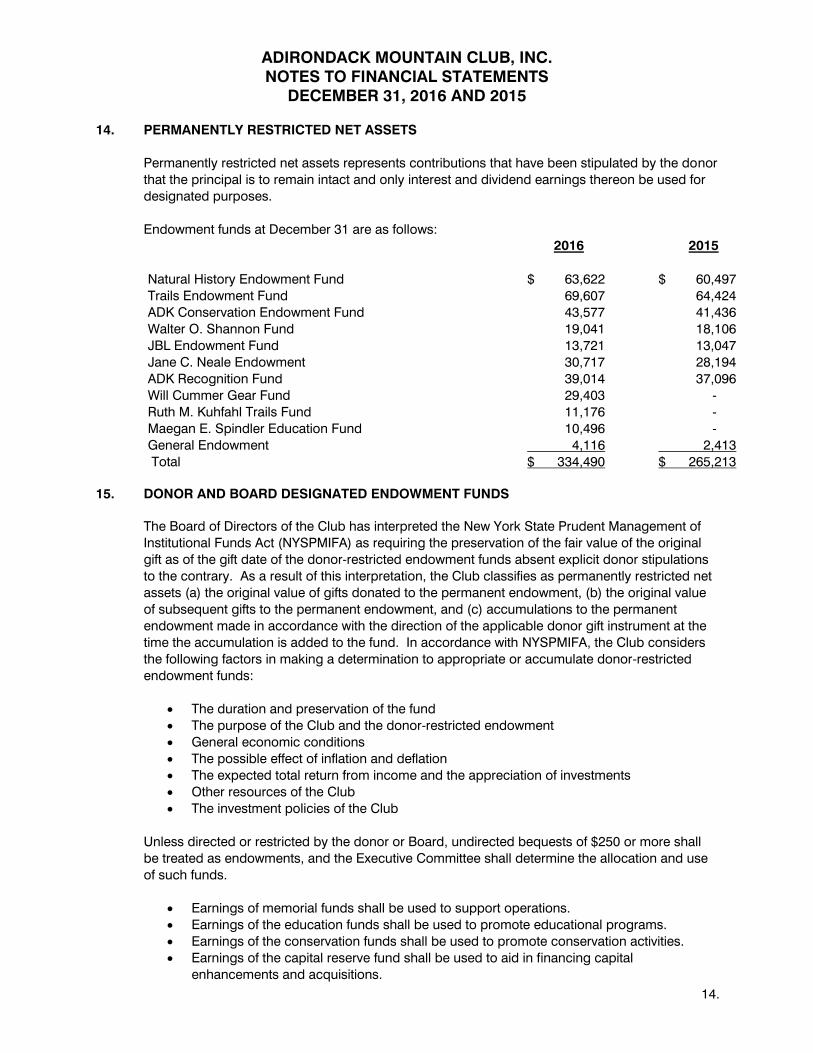

14. PERMANENTLY RESTRICTED NET ASSETS

Permanently restricted net assets represents contributions that have been stipulated by the donor

that the principal is to remain intact and only interest and dividend earnings thereon be used for

designated purposes.

Endowment funds at December 31 are as follows:

2016 2015

Natural History Endowment Fund $ 63,622 $ 60,497

Trails Endowment Fund 69,607 64,424

ADK Conservation Endowment Fund 43,577 41,436

Walter O. Shannon Fund 19,041 18,106

JBL Endowment Fund 13,721 13,047

Jane C. Neale Endowment 30,717 28,194

ADK Recognition Fund 39,014 37,096

Will Cummer Gear Fund 29,403 -

Ruth M. Kuhfahl Trails Fund 11,176 -

Maegan E. Spindler Education Fund 10,496 -

General Endowment 4,116 2,413

Total $ 334,490 $ 265,213

15. DONOR AND BOARD DESIGNATED ENDOWMENT FUNDS

The Board of Directors of the Club has interpreted the New York State Prudent Management of

Institutional Funds Act (NYSPMIFA) as requiring the preservation of the fair value of the original

gift as of the gift date of the donor-restricted endowment funds absent explicit donor stipulations

to the contrary. As a result of this interpretation, the Club classifies as permanently restricted net

assets (a) the original value of gifts donated to the permanent endowment, (b) the original value

of subsequent gifts to the permanent endowment, and (c) accumulations to the permanent

endowment made in accordance with the direction of the applicable donor gift instrument at the

time the accumulation is added to the fund. In accordance with NYSPMIFA, the Club considers

the following factors in making a determination to appropriate or accumulate donor-restricted

endowment funds:

The duration and preservation of the fund

The purpose of the Club and the donor-restricted endowment

General economic conditions

The possible effect of inflation and deflation

The expected total return from income and the appreciation of investments

Other resources of the Club

The investment policies of the Club

Unless directed or restricted by the donor or Board, undirected bequests of $250 or more shall

be treated as endowments, and the Executive Committee shall determine the allocation and use

of such funds.

Earnings of memorial funds shall be used to support operations.

Earnings of the education funds shall be used to promote educational programs.

Earnings of the conservation funds shall be used to promote conservation activities.

Earnings of the capital reserve fund shall be used to aid in financing capital

enhancements and acquisitions.

15.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

15. DONOR AND BOARD DESIGNATED ENDOWMENT FUNDS

Endowment investment policy consists of up to 50% of new non-specified money be invested in

an equity mutual fund, and a minimum 50% be invested in government securities mutual fund for

a maximum of 10 years.

Allocation of Investment Returns

When endowment funds are added to the investment portfolio, they are used to “buy” shares in

the portfolio at the then current value per share (much like purchasing shares in a mutual fund.)

The value of each endowment is tracked by the value of its shares. Endowment shares may

never be sold and the number of shares can never go down. Additional shares may be

purchased if new funds are provided by any source. The investment return of the investment

portfolio increases the value of each share, and withdrawals for annual financial support

decreases the value of each share. The investment return between pay-outs for an individual

endowment may be determined by tracking the value of its shares.

In the year 2016, the Club had the following endowment-related activities:

Board Designated Endowment Total

Endowment net assets, beginning of

year

$ 806,956

$ 265,213

$ 1,072,169

Interest and dividend income 15,926 9,035 24,961

Net realized and unrealized gains

(losses) on investments carried at fair

value

36,292

20,588

56,880

Total investment return 52,218 29,623 81,841

Less: Operating investment return 32,120 10,477 42,597

Nonoperating investment return 20,098 19,146 39,244

Contributions 8,310 39,635 47,945

Amounts appropriated for expenditure - - -

Fund transfers (10,496) 10,496 -

Endowment net assets, end of year $ 824,868 $ 334,490 $ 1,159,358

In the year 2015, the Club had the following endowment-related activities:

Board Designated Endowment Total

Endowment net assets, beginning of

year

$ 829,262

$ 234,237

$ 1,063,499

Interest and dividend income 38,883 11,687 50,570

Net realized and unrealized gains

(losses) on investments carried at fair

value

(45,505)

(13,808)

(59,313)

Total investment return (6,622) (2,121) (8,743)

Less: Operating investment return 33,335 (28,812) 4,523

Nonoperating investment return (39,957) 26,691 (13,266)

Contributions 17,651 4,285 21,936

Amounts appropriated for expenditure - - -

Fund Transfers - - -

Endowment net assets, end of year $ 806,956 $ 265,213 $ 1,072,169

16.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

16. SPLIT-INTEREST AGREEMENTS

The Club administers several charitable gift annuities. A charitable gift annuity provides for the

payment of distributions to the grantor or other designated beneficiaries over a period of time

(usually the designated beneficiary’s lifetime). At the death of the beneficiary, the remaining

assets are available for the Club’s use. The portion of the annuity attributable to the present

value of the future benefits to be received by the Club is recorded in the Statement of Activities as

a contribution in the period the annuity is established. Assets held for the charitable gift annuities

totaled $129,609 at December 31, 2016 and are reported at fair value in investments in the Club’s

statements of financial position. The Club periodically revalues the liability to make distributions

to the designated beneficiaries based on actuarial assumptions. The present value of the

estimated future payments ($60,765 at December 31, 2016) is calculated using the original

discount rate (4%) used in each agreement and the applicable mortality tables.

This is a Level 3 liability as the liability is measured at fair value on a recurring basis using

unobservable inputs. Unobservable inputs include a discount factor and life expectancies:

January 1, 2015 $ 69,186

Total gains/losses and amortization 6,376

Annuitant payments (9,440)

December 31, 2015 66,122

Total gains/losses and amortization 4,083

Annuitant payments (9,440)

December 31, 2016 $ 60,765

The gains/losses noted above are included in temporarily restricted net assets.

17. PENSION PLAN

During 1995, the Club established the Thrift Plan for Employees of Adirondack Mountain Club,

Inc. (the Plan) under Section 403(b) of the IRS Code. This is a defined contribution plan that

covers all employees over age 21 who have completed one year of eligible service. Employer

contributions were 3% of participant compensation; employees may also contribute to the Plan.

Also, employees who contribute at least 1% of their own compensation will receive an additional

1% matching contribution from the Club. Employer contributions are fully vested after six years of

service. The Plan allows forfeitures to be used to reduce the employer contributions. Forfeitures

were utilized in 2016 and 2015 to reduce the Club’s contribution. The Club's contributions to the

Plan for 2016 and 2015 were $37,318 and $54,382, respectively.

18. COMMITMENTS

Leases

The Club was under a non-cancelable lease as of December 31, 2015, which was bought out in

2016 as part of the capital lease agreement described in note 9. Therefore, there are currently no

future payments for non-cancelable leases.

17.

ADIRONDACK MOUNTAIN CLUB, INC.

NOTES TO FINANCIAL STATEMENTS

DECEMBER 31, 2016 AND 2015

19. LINE OF CREDIT

The Club has a revolving line of credit with Glens Falls National Bank in the amount of $250,000.

The line is payable on demand. The interest rate is prime plus .75% (4.50% at December 31,

2016) or a minimum of 4.00% and all interest is payable at the date of expiration. The line of

credit expires upon termination of the account. No amount was outstanding with the line of credit

at December 31, 2016 and 2015. The Club must maintain a minimum debt service coverage ratio

of 1.00, tested annually. The Club met the covenant at the end of 2016.

The credit line is secured by a first blanket lien on all business assets.

20. ADVERTISING COSTS

Advertising costs are expensed as incurred. Advertising costs are included in the schedule of

functional expense under public relations, education and advertising. For the year ended

December 31, 2016 and 2015, costs were $37,083 and $38,069, respectively.

21. CONCENTRATION OF CREDIT RISK

The Club maintains its cash balances with multiple financial institutions. Balances at the financial

institutions are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000. At

December 31, 2016 bank balances in excess of FDIC limits totaled approximately $140,300.

22. RECLASSIFICATION OF PRIOR YEAR’S FINANCIAL STATEMENTS

Certain items in the prior year financial statements have been reclassified to conform to the

current year’s presentation. The reclassifications have no effect on previously reported changes

in net assets or net assets.

23. SUBSEQUENT EVENTS

The Club’s management has evaluated events subsequent to the statement of financial position

date of December 31, 2016 through March 30, 2017, which is the date these financial statements

were issued, and have determined that there are no subsequent events that require recording or

disclosure under accounting principles generally accepted in the United States of America.

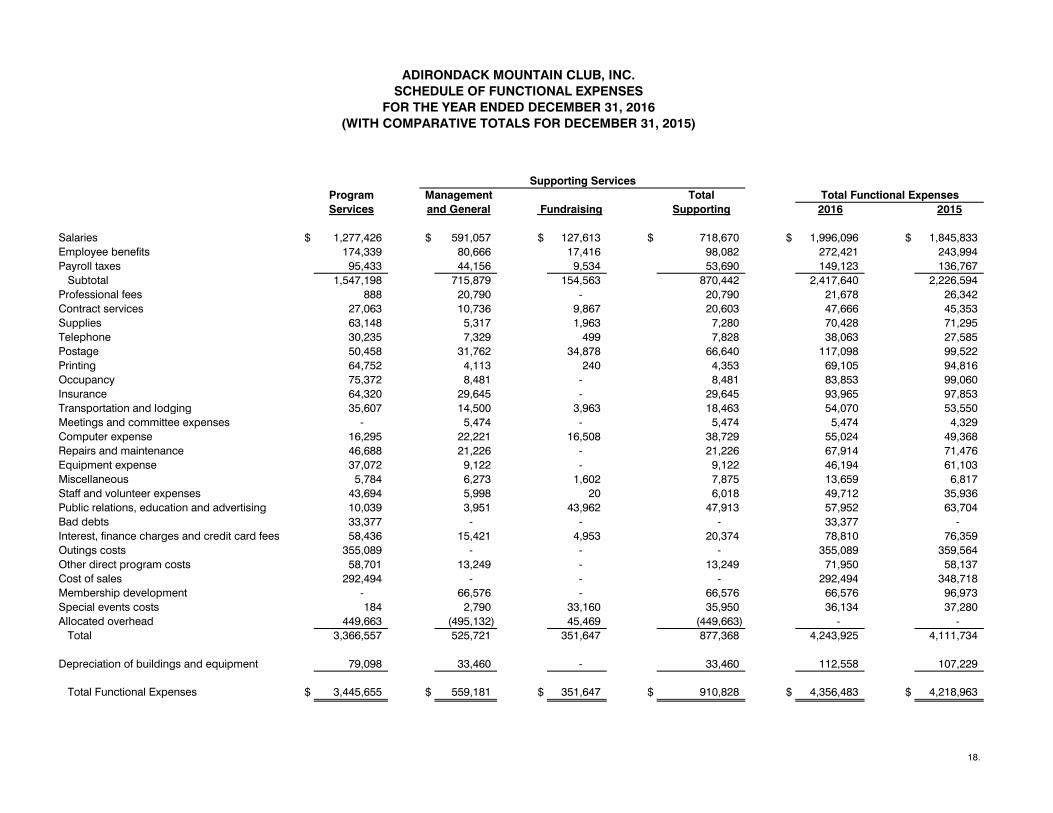

Supporting Services

Program Management Total Total Functional Expenses

Services and General Fundraising Supporting 2016 2015

Salaries $ 1,277,426 $ 591,057 $ 127,613 $ 718,670 $ 1,996,096 $ 1,845,833

Employee benefits 174,339 80,666 17,416 98,082 272,421 243,994

Payroll taxes 95,433 44,156 9,534 53,690 149,123 136,767

Subtotal 1,547,198 715,879 154,563 870,442 2,417,640 2,226,594

Professional fees 888 20,790 - 20,790 21,678 26,342

Contract services 27,063 10,736 9,867 20,603 47,666 45,353

Supplies 63,148 5,317 1,963 7,280 70,428 71,295

Telephone 30,235 7,329 499 7,828 38,063 27,585

Postage 50,458 31,762 34,878 66,640 117,098 99,522

Printing 64,752 4,113 240 4,353 69,105 94,816

Occupancy 75,372 8,481 - 8,481 83,853 99,060

Insurance 64,320 29,645 - 29,645 93,965 97,853

Transportation and lodging 35,607 14,500 3,963 18,463 54,070 53,550

Meetings and committee expenses - 5,474 - 5,474 5,474 4,329

Computer expense 16,295 22,221 16,508 38,729 55,024 49,368

Repairs and maintenance 46,688 21,226 - 21,226 67,914 71,476

Equipment expense 37,072 9,122 - 9,122 46,194 61,103

Miscellaneous 5,784 6,273 1,602 7,875 13,659 6,817

Staff and volunteer expenses 43,694 5,998 20 6,018 49,712 35,936

Public relations, education and advertising 10,039 3,951 43,962 47,913 57,952 63,704

Bad debts 33,377 - - - 33,377 -

Interest, finance charges and credit card fees 58,436 15,421 4,953 20,374 78,810 76,359

Outings costs 355,089 - - - 355,089 359,564

Other direct program costs 58,701 13,249 - 13,249 71,950 58,137

Cost of sales 292,494 - - - 292,494 348,718

Membership development - 66,576 - 66,576 66,576 96,973

Special events costs 184 2,790 33,160 35,950 36,134 37,280

Allocated overhead 449,663 (495,132) 45,469 (449,663) - -

Total 3,366,557 525,721 351,647 877,368 4,243,925 4,111,734

Depreciation of buildings and equipment 79,098 33,460 - 33,460 112,558 107,229

Total Functional Expenses $ 3,445,655 $ 559,181 $ 351,647 $ 910,828 $ 4,356,483 $ 4,218,963

ADIRONDACK MOUNTAIN CLUB, INC.

SCHEDULE OF FUNCTIONAL EXPENSES

FOR THE YEAR ENDED DECEMBER 31, 2016

(WITH COMPARATIVE TOTALS FOR DECEMBER 31, 2015)

18.