addressing diversity in govt health policies n health insurance regulatory frameworks for effective...

TRANSCRIPT

Addressing Diversity in Government Health Policies and Health Insurance Regulatory Frameworks for Effective Business Development

6th Annual Health Insurance Asia, 2012

1

Regulatory Frameworks for Effective Business Development

July 17, 2012

Dr. Milind Sabnis, MD, MBA

Principal Consultant

Healthcare, Asia Pacific

2

Agenda

• INTRODUCTION

• KEY GLOBAL TRENDS IMPACTING HEALTHCARE

• HEALTHCARE SPENDING IN ASIA

• HEALTHCARE INSURANCE

3

• HEALTHCARE INSURANCE

• FUTURE OF HEALTHCARE

KEY GLOBAL TRENDS IMPACTING HEALTHCARE

4

KEY GLOBAL TRENDS IMPACTING HEALTHCARE

Globalization, consumerism, and prosperity are the 3 major trends that will impact healthcare…

Globalization

Globalization:

• World is becoming smaller: cheap air- travel, connectivity,

internet, medical tourism

• Increased healthcare awareness because of multiple media

Consumerism:

• Increased awareness of medical conditions; potential

treatments, best physicians, hospitals to treat these conditions

• Increased decision making in choosing physicians,

hospitals, and insurance plans

1

31

5

ConsumerismProsperity

hospitals, and insurance plans

Prosperity:

• Increasing disposable income, financial independence

leading to exploring more choices

• Increased health awareness has led to consumers spending

more on health prevention

2

2 3

Source: Frost & Sullivan

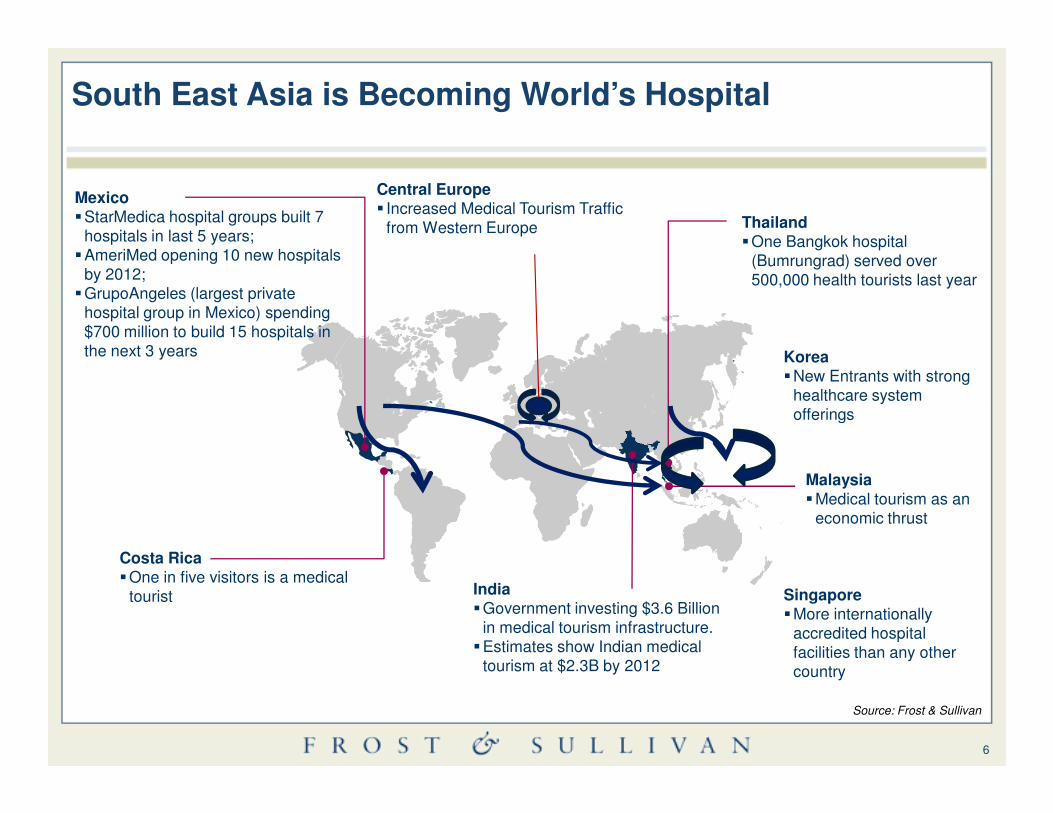

South East Asia is Becoming World’s Hospital

Thailand�One Bangkok hospital

(Bumrungrad) served over 500,000 health tourists last year

Mexico�StarMedica hospital groups built 7

hospitals in last 5 years;�AmeriMed opening 10 new hospitals

by 2012; �GrupoAngeles (largest private

hospital group in Mexico) spending $700 million to build 15 hospitals in the next 3 years

Central Europe� Increased Medical Tourism Traffic

from Western Europe

Korea�New Entrants with strong

healthcare system offerings

6

Costa Rica�One in five visitors is a medical

tourist

Malaysia�Medical tourism as an

economic thrust

India�Government investing $3.6 Billion

in medical tourism infrastructure.�Estimates show Indian medical

tourism at $2.3B by 2012

offerings

Singapore�More internationally

accredited hospital facilities than any other country

Source: Frost & Sullivan

Increased Prosperity and Middle Class Consumption will Fuel Healthcare Expenditure

Other Asia9%

India4%

China2%

Japan8%

EU30%

US21%

Other26%

Middle Class Consumption (2009)

Other Asia14%

India23%

China18%

Japan4%

EU14%

US7%

Other20%

Middle Class Consumption (2030)

7

•Middle class consumption in China and India will surpass that of EU and US by 2030

•APAC will contribute to 59% of global middle class consumption by 2030, rising from 23% in 2009

•Over half of the middle class will be from the APAC region by 2020

•Both factors will be a major growth driver for HC expenditure and the growth of the HC delivery market as demand increases across the region

1810

36

22

28

53

2 26 5

0

20

40

60

80

100

2010 2020

Origins of Global Middle Class (%)

Middle East and North Africa

Sub-Saharan Africa

Asia Pacific

Central and South America

EU

North America

Source: OECD, Smith Barney, Frost & Sullivan

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

Pe

rce

nta

ge

of

Ag

ed

65

an

d A

bo

ve

to

Tota

l Po

pu

lati

on

(%

)

Po

pu

lati

on

(M

illi

on

)By 2020, two-third of the Asia-pacific population over 65 years will have at least one chronic disease

Healthcare Industry: Population Aged 65 and Above, (Asia Pacific), 2009-2020

The Burden of Disease in elderly, Asia Pacific

8

0.0%

2.0%

-

50.0

2010 2015 2020

Pe

rce

nta

ge

of

Ag

ed

65

an

d A

bo

ve

to

Tota

l Po

pu

lati

on

(%

)

Year

Aged 65 and Above (Million)

Percentage of Aged 65 and Above to Total Population (%)

� In 2010, 7.6% (241.7 million) of the Asia Pacific population was aged 65 and above.

� By 2020, this will be more than 9.7% (333.95)

� 65.2% of those aged 65+ have one chronic condition

Source: WHO, Frost & Sullivan

HEALTHCARE SPENDING IN ASIA

9

HEALTHCARE SPENDING IN ASIA

3.9

4.1

4.34.8

5.9

7.2

6.5

8.3

8.5

9.4

16.2

Singapore

Laos

Thailand

MalaysiaCambodia

Vietnam

KoreaJapan

Australia

UKUSA

Total expenditure on health as a % of GDP, 2009

Compared with the developed countries, most Asian countries spend smaller proportion of their GPD on health…

AS

EA

N C

ou

ntr

ies

De

ve

lop

ed

C

ou

ntr

ies

10

2.6

3.4

44.2

4.6

5.5

5.8

2

2.4

2.93.8

3.9

0 2 4 6 8 10 12 14 16 18

PakistanBangladesh

Sri Lanka

IndiaChina

Bhutan

Nepal

Myanmar

Indonesia

Brunei

PhilippinesSingapore

%

Most countries in Asia spend less than 5% of their GDP on healthcare

AS

EA

N C

ou

ntr

ies

Oth

er

As

ian

C

ou

ntr

ies

Source: WHO

7.17.2

7.58.9

9.814

12.317.9

15.118.3

18.7

MalaysiaPhilippinesCambodia

Viet NamSingapore

Thailand

KoreaJapan

UKAustralia

USA

AS

EA

N C

ou

ntr

ies

De

ve

lop

ed

C

ou

ntr

ies

General government expenditure on health as a % of total government expenditure, 2009

Most developed governments spend >15% of their budgets on healthcare, while most Asian governments don’t spend half as much...

11

3.64.1

7.37.9

8.610.3

13.3

0.83.8

6.86.97.1

0 2 4 6 8 10 12 14 16 18 20

PakistanIndia

Sri LankaBangladesh

NepalChina

Bhutan

MyanmarLaos

Brunei IndonesiaMalaysia

AS

EA

N C

ou

ntr

ies

Oth

er

As

ian

C

ou

ntr

ies

%

Most Governments in Asia spend <8% of their budget on healthcare Source: WHO

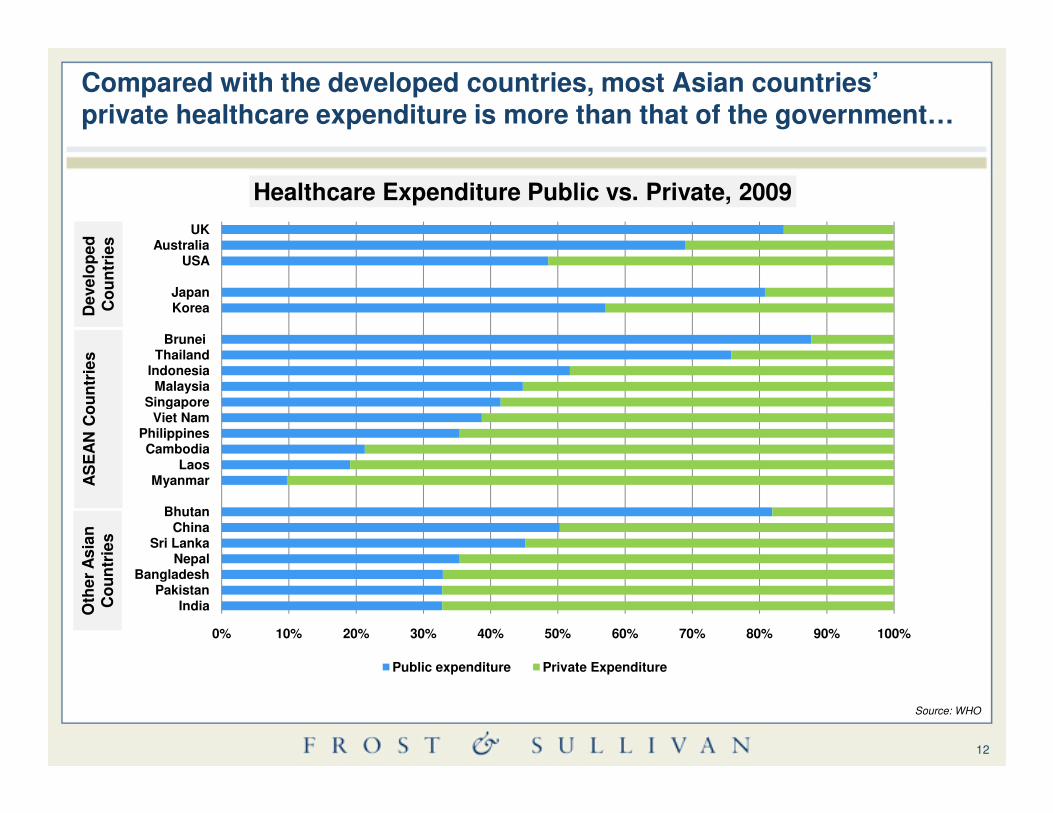

SingaporeMalaysia

IndonesiaThailand

Brunei

KoreaJapan

USAAustralia

UK

Healthcare Expenditure Public vs. Private, 2009

AS

EA

N C

ou

ntr

ies

De

ve

lop

ed

C

ou

ntr

ies

Compared with the developed countries, most Asian countries’ private healthcare expenditure is more than that of the government…

12

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

IndiaPakistan

BangladeshNepal

Sri LankaChina

Bhutan

MyanmarLaos

CambodiaPhilippines

Viet NamSingapore

Public expenditure Private Expenditure

AS

EA

N C

ou

ntr

ies

Oth

er

As

ian

C

ou

ntr

ies

Source: WHO

Viet NamSingaporeIndonesia

PhilippinesMalaysiaThailand

KoreaJapan

UKAustralia

USA

Components of Private Expenditure, 2009

AS

EA

N C

ou

ntr

ies

De

ve

lop

ed

C

ou

ntr

ies

In most Asian countries most people pay for health out-of-pocket; PHI is restricted to certain part of the societies in these countries…

13

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

BhutanPakistan

BangladeshNepalIndia

ChinaSri Lanka

CambodiaMyanmar

LaosBrunei

Viet Nam

PHI OOP Other

OOP=Out of pocket; PHI=Private Health Insurance; Others=charity, aids, etc Source: WHO

AS

EA

N C

ou

ntr

ies

Oth

er

As

ian

C

ou

ntr

ies

There is a huge potential for PHI in the Asian market…

HEALTHCARE INSURANCE

14

HEALTHCARE INSURANCE

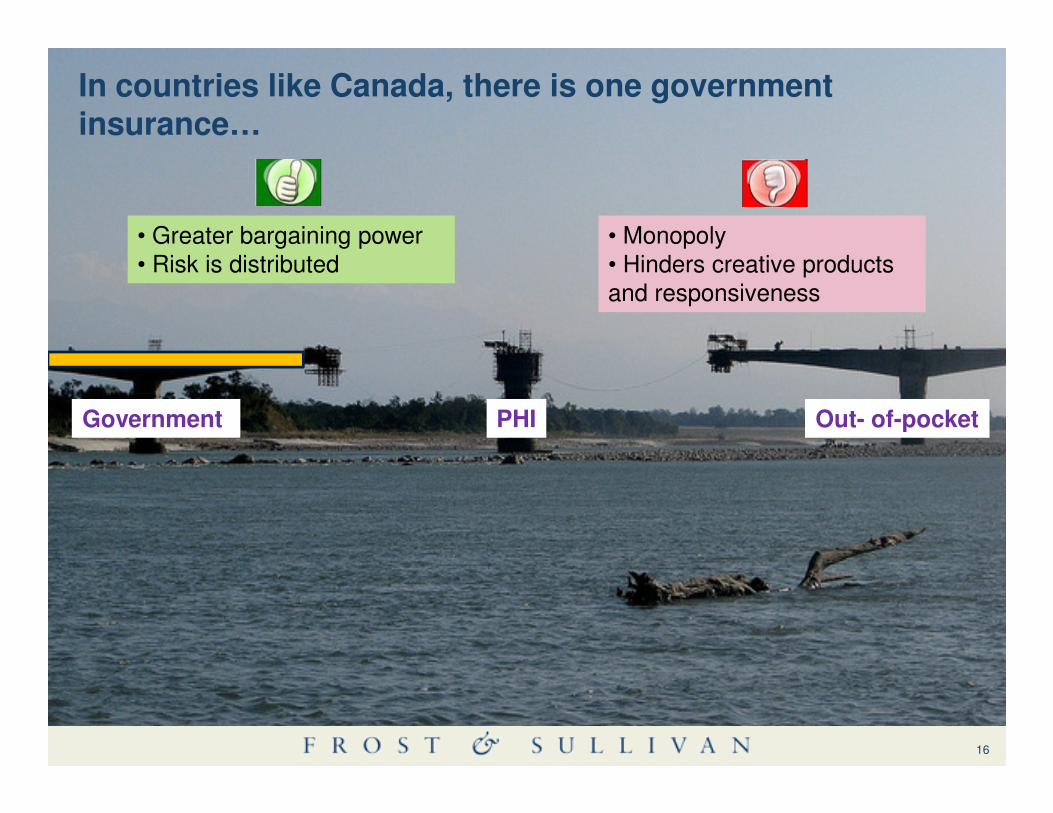

Government PHI Out- of-pocket

15

Government PHI Out- of-pocket

• Greater bargaining power• Risk is distributed

• Monopoly• Hinders creative products and responsiveness

In countries like Canada, there is one government insurance…

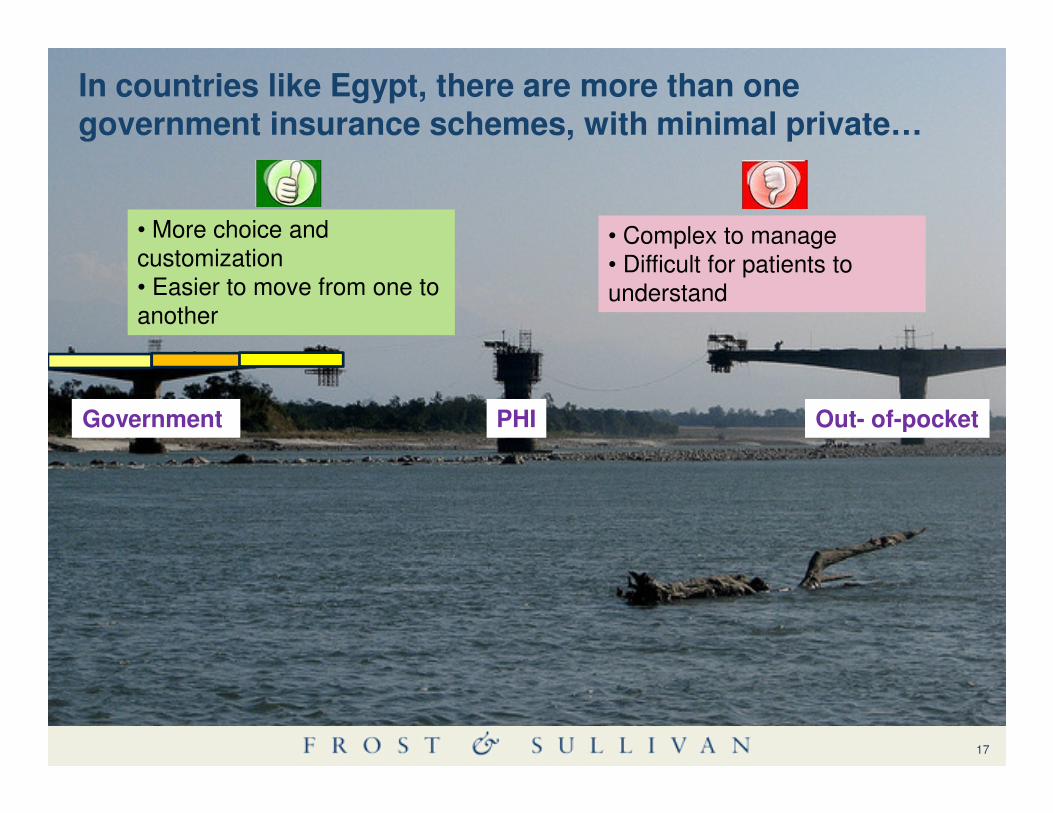

Government PHI Out- of-pocket

16

Government PHI Out- of-pocket

• More choice and customization• Easier to move from one to another

• Complex to manage• Difficult for patients to understand

In countries like Egypt, there are more than one government insurance schemes, with minimal private…

Government PHI Out- of-pocket

17

Government PHI Out- of-pocket

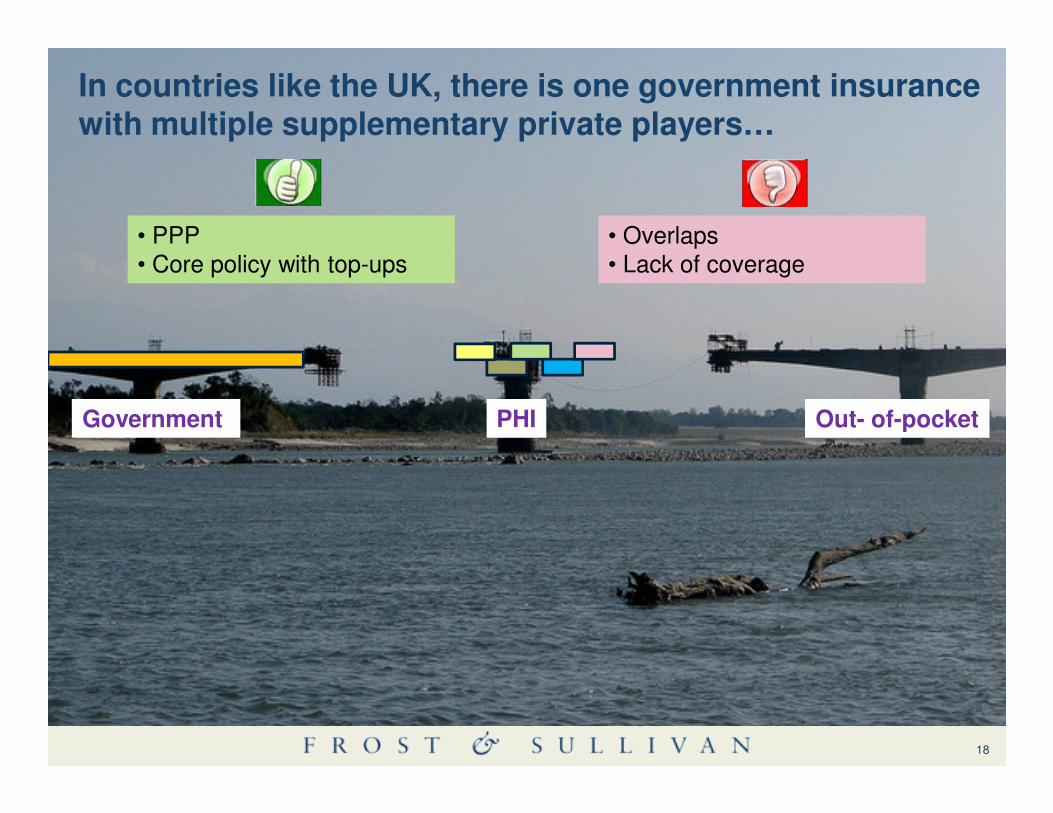

• PPP• Core policy with top-ups

• Overlaps• Lack of coverage

In countries like the UK, there is one government insurance with multiple supplementary private players…

Government PHI Out- of-pocket

18

Government PHI Out- of-pocket

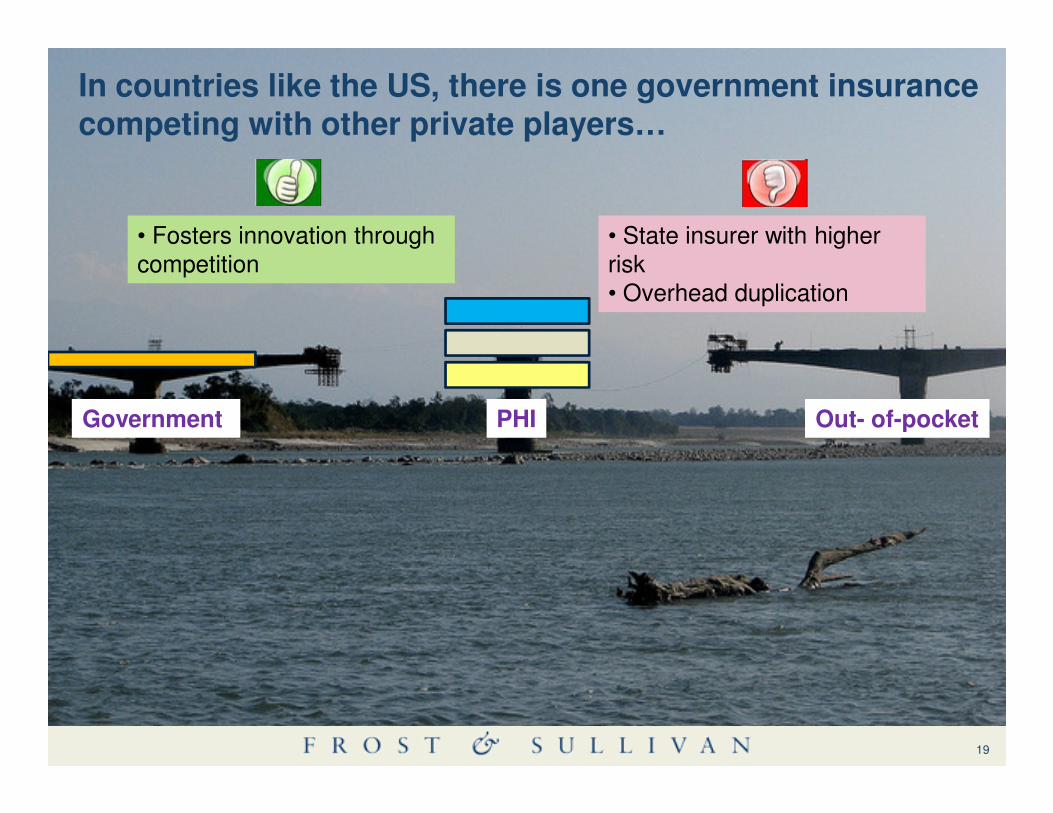

• Fosters innovation through competition

• State insurer with higher risk• Overhead duplication

In countries like the US, there is one government insurance competing with other private players…

Government PHI Out- of-pocket

19

Government PHI Out- of-pocket

• Fosters responsiveness, innovation through competition

• More complex• Overhead duplication• Risk selection (need risk-equalization)

In countries in the West Indies, there are multiple private players, with no government player…

Government PHI Out- of-pocket

20

Government PHI Out- of-pocket

Key Markets Healthcare Insurance Environments in Asia Pacific

India China Indonesia Malaysia Thailand Australia Singapore

Aging Population No Yes No Yes Yes Yes Yes

Dominant Distributer ofPHI

Life/ Non Life/ Health

Life/ Non Life/ Health

Life Life Life Health Life

Tax Incentives for PHI Yes Group No Yes No Yes Yes

Restrictions on PremiumRates

Notify No No No No Yes notify

Guaranteed Renewal Some Some No No No Yes

21

Guaranteed Renewal Some Some No No No Yes

Portability of PHI policy In Discussion No No No No Yes

Group biz as % of totalportfolio

45% 30% >20% 30% 20% <10% 25%

Minimum BenefitsSchedule

YES NO

Medical Underwritingallowed

Yes No Yes

The 3 elements of healthcare: High quality, reasonable cost, and ease of access…

Quality

Cost

Access

Situation Challenges Opportunities

Ac

ce

ss

• Increasing elderly population• Increasing medical travellers• High quality healthcare • Efficient schemes [Medisave, Medical Shield, Medifund, Eldershield]

Access constraint: • Shortage of hospital bed space (2.2/1000, ideal 3/1000)• High cost of healthcare

Improved access: Medisave covers 12 private hospitals in Malaysia; offer international medical insurance• High premium specialized packages that cover eg. BUPA Pregnancy; … preventive

22

Qu

ali

ty

Co

st

• Flat subsidy per patient of US$80 paid to the hospital/doctor regardless on the disease treated• Popular with public

• 39% population covered by government insurance, 5% covered by private; ~56% uninsured

Pregnancy; … preventive

Cost constraints: • Not sustainable as cost incurred by hospitals is higher leading to deteriorating service and quality in overburdened public hospitals• Cost constraints in other part of the world eg. Middle east, Singapore

Cost-effective options:• Packages for middle & high income groups who would prefer to pay for high quality • Opportunities for foreign (ME) insurance companies to lower their reimbursement costs [60-70% cheaper than US, 50% cheaper than Singapore

Quality constraints: • Inadequate quality; wealthy go to Malaysia and Singapore• Middle class relies on private; less pressure on the government to provide good quality healthcare

Improved quality options:•High premium packages that cover medical travel •Packages that incentivize local treatment at JCI accredited hospitals

FUTURE OF HEALTH CARE

23

FUTURE OF HEALTH CARE

From...

Provider Centric Focus Patient Centric

Centralized – Hospital Monitor De-Centralized – Shift to Community

...To

A modern healthcare system is on the horizon, demanding a paradigm shift

Healthcare Paradigm Shift

24

Invasive in general hospitals Treatment Less invasive in specialized hospitals

Treating Sickness Objective Preventing Sickness – “Wellness”

Source: Frost & Sullivan

F

M

T

O

Focus: moving from physicians to patientsF

M

T

O

25

Physician PatientsPatients are becoming:

• Aware of treatment/medicine choices

• Informed decision makers

• Responsible for their own health

Source: Frost & Sullivan

Hospital based careHospital based care Community based careCommunity based care

Innovation in hospital business models: Hospitals go virtual; development of community based care

F

M

T

O

26

Centralized model

Patient overload

Increased costs

Strain on health care resources

Decentralized model

Reduced patient load

Reduced cost

Optimum utilization of health care resources

Source: Frost & Sullivan

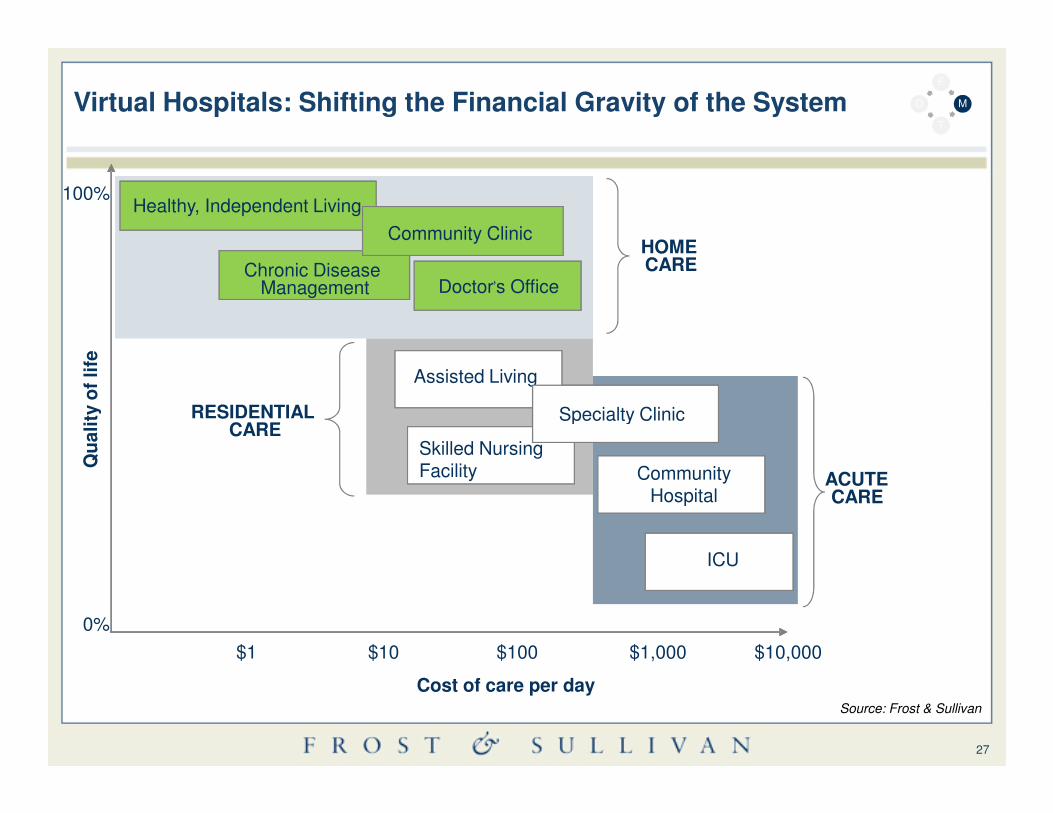

Virtual Hospitals: Shifting the Financial Gravity of the System

Healthy, Independent Living

Chronic Disease Management

Community Clinic

Doctor’s Office

100%

Assisted Living

HOME CARE

RESIDENTIAL

Qu

ali

ty o

f li

fe

Healthy, Independent Living

Chronic Disease Management

Community Clinic

Doctor’s Office

Assisted Living

Specialty Clinic

F

M

T

O

27

Cost of care per day

$1 $10 $100 $1,000 $10,000

0%

Skilled Nursing Facility

Specialty Clinic

Community Hospital

ICU

RESIDENTIAL CARE

Qu

ali

ty o

f li

fe

Skilled Nursing Facility

Specialty Clinic

Community Hospital

ICU

ACUTE CARE

Source: Frost & Sullivan

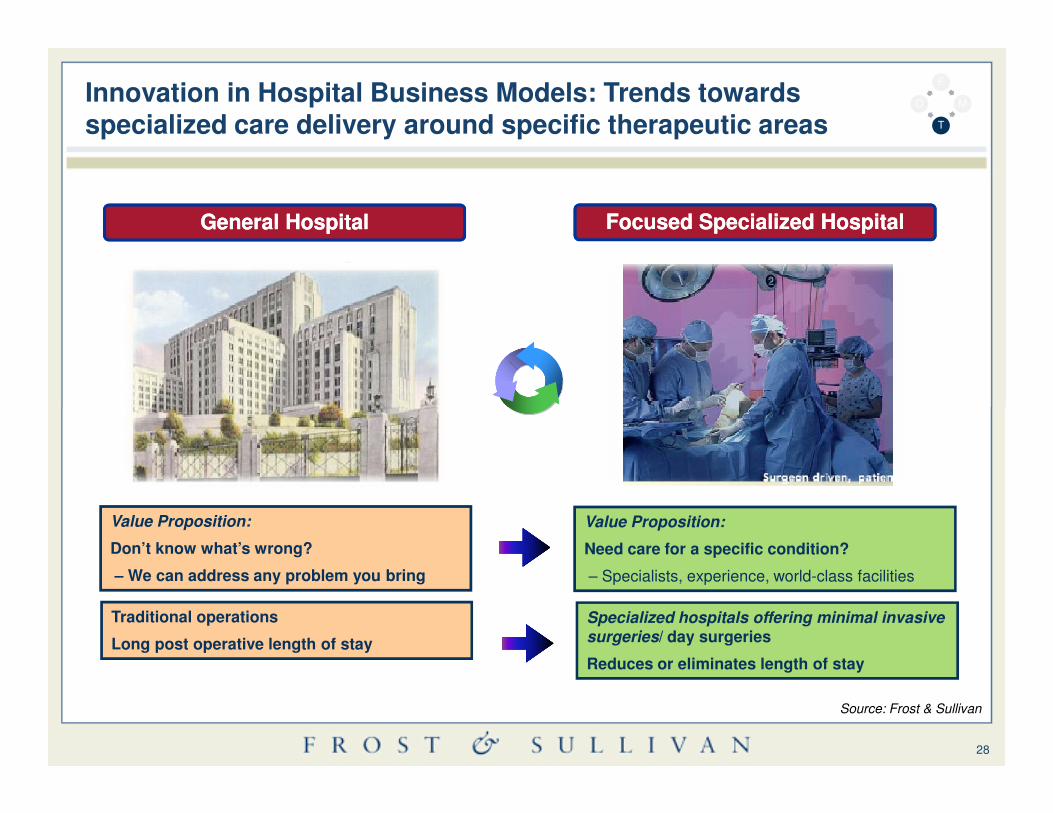

General HospitalGeneral Hospital Focused Focused Specialized HospitalSpecialized Hospital

Innovation in Hospital Business Models: Trends towards specialized care delivery around specific therapeutic areas

F

M

T

O

28

Value Proposition:

Don’t know what’s wrong?

– We can address any problem you bring

Value Proposition:

Need care for a specific condition?

– Specialists, experience, world-class facilities

Traditional operations

Long post operative length of stay

Specialized hospitals offering minimal invasive surgeries/ day surgeries

Reduces or eliminates length of stay

Source: Frost & Sullivan

Wellness of the body, the mind and the soul

Mind

Mood

Stress levels

Mental health

Sense of optimism

Attitude

Security

Safety

F

M

T

O

29

Body SoulPersonal values

Personal fulfilment

Self image / self actualization

Sight / vision

Touch & feel

Smell / breathing

Sound

Temperature

Wellness

Source: Frost & Sullivan

Why Wellness?

50% Percent of all diseases can be avoided and prevented by lifestyle changes

Only 31% of healthcare expenditure in organization is spent on direct medical costs

Medical Costs

Direct = 31%

Medical Costs

Workers

Indirect = 69%

Lost Productivity:- Absenteeism

Employee & Customer Dissatisfaction:

F

M

T

O

30

69% of medical costs are due to productivity loss

50% of all medical costs can be saved with integrated and comprehensive health management.

Workers Compensation

Salary Continuation

Dissatisfaction:- Turnover + Temporary Staffing- Poor Quality

Replacement Workers:- Training Interim Employee- Administrative re-work

75% caused by chronic diseases that are preventable

Source: An Unhealthy America: The Economic Burden of Chronic Disease, The Milken Institute Center for Health Economics

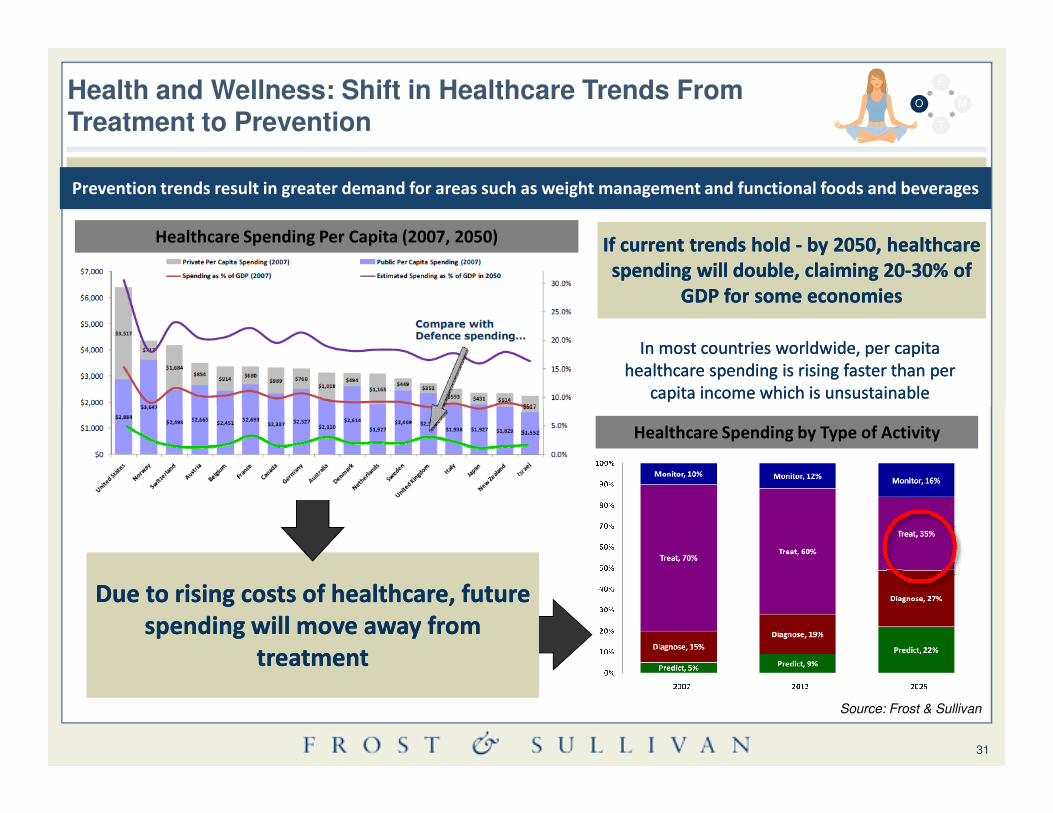

Health and Wellness: Shift in Healthcare Trends From Treatment to Prevention

Healthcare Spending Per Capita (2007, 2050)

In most countries worldwide, per capita In most countries worldwide, per capita

healthcare spending is rising faster than per healthcare spending is rising faster than per

capita income which is unsustainable capita income which is unsustainable

If current trends hold If current trends hold -- by 2050, healthcare by 2050, healthcare

spending will double, claiming 20spending will double, claiming 20--30% of 30% of

GDP for some economies GDP for some economies

Prevention trends result in greater demand for areas such as weight management and functional foods and beverages

F

M

T

O

31

Due to rising costs of healthcare, future Due to rising costs of healthcare, future

spending will move away from spending will move away from

treatment treatment

Healthcare Spending by Type of Activity

Source: Frost & Sullivan

What does that mean for the insurance companies….

From...

Provider Centric Focus Patient Centric

Centralized – Hospital Monitor De-Centralized – Shift to Community

...To

Customized Insurance products

Insurance products incentivising community care

32

Community

Invasive in general hospitals

Treatment Less invasive in specialized hospitals

Treating Sickness Objective Preventing Sickness –“Wellness”

Specialized insurance products that cover less invasive surgeries

Insurance products that cover and incentivize preventive care, regular monitoring, vaccinations, healthy habits…

The key is to manage quality, cost, and access…

Government PHI Out- of-pocket

33

Government PHI Out- of-pocket

Thank you

Dr. Milind Sabnis, MD, MBA

Principal ConsultantHealthcare, Asia [email protected]

Donna Jeremiah

Director Corporate Communications, Asia [email protected]: +61 (02) 8247 8927

34

Jessie Loh

ManagerCorporate Communications, Asia [email protected]. (65) 6890 0942

Carrie Low

ExecutiveCorporate Communications, Asia [email protected]. (603) 6204 5910