actuaries club of the southwest southeastern actuaries ... · sales results, despite continued...

TRANSCRIPT

Actuaries Club of the SouthwestSoutheastern Actuaries Conference

Worksite Products in Today’s Market

November 16, 2011,

Presented by:yMilliman, Inc.

Tampa, FLTampa, FL

Outline• Overview of the Worksite Market

Michael Weilant, FSA, MAAA

• Life Worksite Products: What's Working• Life Worksite Products: What s WorkingSanjeev Chaudhuri, FSA, MAAA

• Critical Illness: A Core Product in Today's PortfolioJ if (O'B i ) H d ASAJennifer (O'Brien) Howard, ASA

• Accident Insurance: An Essential Product Nate Sandrowicz, ASA

• Short Term Disability: Where is it Headed? Joshua Weber, FSA, MAAA

• Limited Benefit Medical: PPACA is a Game Changer Darrell Spell, FSA, MAAA

• Reinsurance: Small Coverage Providing Big Value

2 November 17, 2011

Reinsurance: Small Coverage Providing Big Value Clark Himmelberger, FSA, MAAA

Important NoticeThe information in this presentation is general in nature. It is

t i t d d t t th ti ti f

Important Notice

not intended to represent the actions or assumptions of aspecific company and the information is not appropriate forpricing, reserving, reviewing, or performing any other functionspecific to a single carrierspecific to a single carrier.

This presentation was prepared for the specific purpose ofThis presentation was prepared for the specific purpose ofproviding a general overview of the worksite market andproducts typically sold in that market. It is not appropriate forany other purpose. Milliman does not intend to benefit any thirdy p p yparty recipient of its work product.

3 November 17, 2011

Overview of the Worksite Market

4 November 17, 2011

Characteristics of Worksite InsuranceCharacteristics of Worksite Insurance Life and health insurance products

Sold at the worksite

100% employee paid through payroll deduction

Can be filed on an individual on group chassischassis

Can be called “worksite” or “voluntary”

5

y

November 17, 2011

Worksite New Business Annualized PremiumWorksite New Business Annualized Premium(in $ billions)

$6.0

4.0 4.1 4.24.4

4.75.0

5.25.4

5.2

$5.0

2 2

2.6

3.1

3.5

$3.0

$4.0

2.02.2

$1.0

$2.0

$0.01997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: Eastbridge Consulting

6 November 17, 2011

g g

Worksite Takeovers as % of New %Business Premium

45%

38%

41%

35%

40%

29%

20%

25%

30%

12%

17%

10%

15%

0%

0%

5%

2006 2007 2008 2009 2010

7 November 17, 2011

Source: Eastbridge Consulting

Worksite In Force PremiumWorksite In Force Premium(in $ billions)

$30 0

19 520.7

22.924.7 24.6

$25.0

$30.0

Low Estimate High Estimate

13 414.8

15.717.4

18.8 18.7

10 3

13.315.0

16.617.7

19.5

$15.0

$20.0

5.2 5.86.7 7.3

8.510.0

11.312.5

13.4

6.27.0

8.08.8

10.3

$5.0

$10.0

Source: Eastbridge Consulting

$0.01997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

8 November 17, 2011

g g

Worksite Market Share byWorksite Market Share by Distribution Type

2%9%

Benefit Brokers

52%

15%Career Agents

Classics52%

Specialists

23% Occassional

9 November 17, 2011

Source: Eastbridge Consulting

Worksite Group vs IndividualWorksite Group vs. Individual Products

100%

59% 58% 57% 57% 57% 54% 52% 51% 50%70%

80%

90%

59% 58% 5 % 5 % 5 %

50%

60%

70%

Individual

Group

41% 42% 43% 43% 43% 46% 48% 49% 50%20%

30%

40%Group

0%

10%

2002 2003 2004 2005 2006 2007 2008 2009 2010

10 November 17, 2011

Source: Eastbridge Consulting

Worksite Mix of Sales by Product LineWorksite Mix of Sales by Product Line8%

25%10% Life

DI

HI/Supp Med

12%

HI/Supp Med

Cancer/CI

Accident

20%12%

Dental

Other

Source: Eastbridge Consulting

13%

11 November 17, 2011

g g

AflacAflac “With about 90% of our accounts being small businesses with fewer

than 100 employees, our primary market is the slice of America than 100 employees, our primary market is the slice of America that’s been hit the hardest by the economic turmoil over the last two years. As such, we were challenged in our U.S. sales growth…”Source: Aflac 2010 Year In Review

“We were also pleased that Aflac U.S. continued to generate strong sales results, despite continued weakness in the U.S. economy…On the product side, sales have benefited significantly from the addition of group products to our Aflac U.S. product portfolio and strategic, coordinated sales and marketing efforts. On the distribution side, Aflac U.S. has continued to generate significant recruiting gains, which we believe benefited from targeted activities that promote the Aflac sales opportunity.”

12

Source: Aflac 2011 Quarterly Report, Third Quarter

November 17, 2011

Allstate BenefitsAllstate Benefits

“Allstate Benefits continued to grow, with premiums increasing 33% in 2010, putting us in the number two market share position in the U.S. workplace voluntary benefits.”

“To fulfill its purpose, Allstate Financial’s primary objectives are to…dramatically expand Allstate Benefits (our workplace distribution business)…”business)…

“Total premiums and contract charges increased 10.7% in 2010 d t 2009 i il d t hi h l f id t d h lthcompared to 2009 primarily due to higher sales of accident and health

insurance through Allstate Benefits, with a significant portion of the increase resulting from sales to employees of one large company…”

13 November 17, 2011

Source: Allstate 2010 Annual Report

Unum / ColonialUnum / Colonial Market Share: 2nd in voluntary insurance

S htt // /Ab tU /Source: http://unum.com/AboutUs/

2010 2009 2008 2007Unum US Voluntary Benefits Segment - Benefit Ratios 55.1% 56.0% 58.0% 60.1%

“D i 2011 i h b d l i

Colonial Life Segment - Benefit Ratios 49.7% 47.3% 47.5% 48.3%Colonial Life Segment - Before-Tax Operating Ratios 26.2% 27.7% 27.4% 27.1%Source: Unum 2009 & 2010 Annual Reports

“During 2011, we expect premium growth to be modest relative to our long-term outlook. We believe that strong profit margins will continue, although we expect our overall benefit ratio to be slightly higher…We b li i th ill l t th i dbelieve premium growth will reaccelerate as the economy improves and employment growth resumes”Source: Unum 2010 Annual Report – Colonial Life – Segment Outlook

14 November 17, 2011

Life Worksite Products: What's WorkingWhat s Working

15 November 17, 2011

Market SizeMarket SizeBureau of Labor Statistics, October 2011

Establishment Survey Data (private sector)

– Number of employees: 109.5 millionp y

– Average weekly hours: 34.4

A h l i $23 2– Average hourly earnings: $23.2

– Average weekly earnings: $795.42

16 November 17, 2011

Worksite Life Product PortfolioWorksite Life Product Portfolio Term Whole Life Excess Interest Whole Life Universal Life ART/YRT ROP Term Supplement to Group Life

17 November 17, 2011

New Business Premiums

5 406.00

3 504.03 4.10 4.22 4.37

4.725.04 5.23 5.40 5.24

4.00

5.00

3.103.50

1 332.00

3.00

0.66 0.77 0.89 1.09 0.98 1.04 1.01 0.95 1.15 1.31 1.33

0.00

1.00

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10Worksite - Total Worksite - Life

18

Source: Eastbridge US Worksite Study

New Business Premiums: Term v.s. UL/WL

0 941 00

0 65 0 65

0.78

0.94 0.93

0 700.800.901.00

0 330.44

0.59 0.570.65 0.65

0.60

0 400.500.600.70

0.33

0.45 0.45 0.50 0.41 0.40 0.37 0.36 0.37 0.37 0.400.100.200.300.40

0.00'01 '02 '03 '04 '05 '06 '07 '08 '09 '10

Worksite - Term Worksite - UL/WL

19

Source: Eastbridge US Worksite Study

Worksite Pricing IssuesWorksite Pricing Issues

Persistency

Mortality

Expenses

20 November 17, 2011

U.S. Individual Life Persistency yUpdate

21

Worksite PersistencyWorksite Persistency Types of Lapse Other Considerations

– Normal Lapses– Group Lapses

– Product– Group Sizep p

– Job Change Lapsesp

– Market– Industry

22 November 17, 2011

Worksite Mortality AssumptionsWorksite Mortality Assumptions

Market penetration CompetitorspParticipation within

groups

p Issue limitsPersistencygroups

DemographicsAge/Gender

Persistency Level of underwriting

Age/Gender

23 November 17, 2011

Worksite UnderwritingWorksite UnderwritingActively at work Limited Enrollment PeriodParticipationParticipationUnderwriting Questions

Polic and Case Si ePolicy and Case Size Industry

24 November 17, 2011

Worksite UnderwritingWorksite UnderwritingActively at work

– Minimum number of hours per week required

Limited Enrollment Period Limited Enrollment Period– Two to three weeks typically

Participation– Industry standard is 20%– May waive for preferred enrollers

25 November 17, 2011

Worksite UnderwritinggEffect of Participation

Guaranteed Issue Participationqx % 100% 20%

Declines 2000% 25 10Declines 2000% 25 10Substandard 300% 150 50Standard 100% 825 140

Total 1 000 200Total 1,000 200Avg class 178% 245%Avg table 3 6% td 82 5% 70 0%% std 82.5% 70.0%

26

Worksite UnderwritingWorksite UnderwritingUnderwriting Questions

Simplified underwriting– Simplified underwriting– Knock-out questions

Policy and Case Size– Policy maximums and minimiums– Guarantee Issue maximums– Larger the case sizes the better

Industry– Unacceptable and non-standard industries

27

Unacceptable and non standard industries

November 17, 2011

ExpensesExpenses Lower underwriting & issue expenses

Commission structures

Cost of policy maintenance

28 November 17, 2011

Experience ManagementExperience ManagementMortality study

Persistency study

Expense study

S l d k ti l iSales and marketing analysis

29 November 17, 2011

Critical Illness: A Core Product i T d ' P tf liin Today's Portfolio

30 November 17, 2011

Critical Illness - A Brief OverviewC t ca ess e O e eA “Typical” Critical Illness Policy

$ Cancer (optional)$ if Heart Attack

St kLumpSum

Stroke

Kidney Failure

Major Organ Transplant

31 November 17, 2011

Critical Illness - A Brief Overview

Lump Sum Benefits are “Free” Cash

$Medical ExpensesExperimental T t t$ Can Be

Used

Treatment

Travel

LumpSum

for... Debt Restructure

Specific Expenses

Other

32 November 17, 2011

Possible Benefit Options$ Full benefits payable for

additional illnesses• Paralysis• Blindness• Occupational HIV

$ Partial benefits for less severe conditions• CABG - 25%• Carcinoma in situ - 25%• Alzheimers - 25%• Parkinsons - 25%

• Wellness Benefit - $50$

33 November 17, 2011

Wellness Benefit - $50$

Keys to Success in Worksite MarketKeys to Success in Worksite Market

Keep product offerings simple

Take a “portfolio view” of your product design

Address specific needs of your (multiple) clientsclients

34 November 17, 2011

Keep Product Offerings SimpleKeep Product Offerings Simple

Don’t try to include everything

58 Conditions

Multiple Payment Options

Extensive $$ Options

35 November 17, 2011

Keep Product Offerings SimpleKeep Product Offerings Simple

Avoid design features that only a genius can understand

Expansive Severity Levels

Illogical Definitions

Complex Triggers

36 November 17, 2011

Illogical Definitions

T k P tf li Vi f YTake a Portfolio View of Your Product Design

Be certain that your product design does not “clash” with other product’s featuresclash with other product s features.

Cancer Disabilit

Remember some things just don’t go together

Cancer Disability

Remember…some things just don t go together very well!

37 November 17, 2011

Critical Illness Design ConsiderationsThree “Key” Types of Customers:

BuyersyBusiness ownerHR DirectorEmployeep yEmployee’s spouse

Sellers (Agents)CommissionCommissionAcquisition expensesClaims expenses

ManagementManagementProfitRisk

38 November 17, 2011

Environment for Growth in U S ?Environment for Growth in U.S.?

Key Statistic

S Ob ti

Key Statistic– Near doubling of in force count in 2010

Some Observations– Increased interest by HR leaders

G i b di t ib t– Growing awareness by distributors– Lessons learned from previous market entry

failuresfailures– Improved product design consideration– Interest increased due to PPACA

39 November 17, 2011

Key Current Marketers in USKey Current Marketers in US Aetna Allstate Workplace Division

Guardian Life HM Life Insurancep

American Fidelity Assurant Employee Benefits

John Hancock Kanawha / Humana

Colonial Life and Accident Combined Insurance Co. Conseco

Lincoln Financial Starmount Life Symetra Conseco

Continental American Dearborn National

Symetra Transamerica Trustmark

Fairmont Specialty Group Great American

United Healthcare UNUM/Provident

40 November 17, 2011

Three Approaches to CIThree Approaches to CI

Stand-Alone Policy

Accelerated Rider to Life Policy

Combination Product

41 November 17, 2011

Stand Alone PolicyStand Alone Policy

Very flexible Very flexible

Attractive risk features

Best approach for several key markets

E i t i Easier to price

More expensive (e.g. more benefits)

Regulatory obstacles

42 November 17, 2011

Flexible Product DesignFlexible Product Design(stand alone)

Contract can be sold alone or packaged with other coverage

Contract can be “removed” alone

Only covers critical illnessy

Benefits can be tailored to the needs of target market.

43 November 17, 2011

More ExpensiveMore Expensive(stand alone)

N ff t f lif i b fit No offset for life insurance benefits

Usually (but not always) assume “supplemental health insurance” style underwritinghealth insurance style underwriting– Simpler

Less selective– Less selective

Policy expenses vs. lower rider expense

44 November 17, 2011

Accelerated Rider to Life PolicyAccelerated Rider to Life Policy

Best approach for coordinating with life coverpp g

Eliminates “survival period” issue

Limited by base policy Limited by base policy

Best approach for “high-end” market

More difficult to price (offset for coordination with life)

Less expensive (e.g. less benefits)

45 November 17, 2011

Typical Primary Worksite Triggers

Heart Attack

Stroke

Cancer

Renal Failure

Major Organ Transplant

46 November 17, 2011

Typical Secondary Worksite TriggersTypical Secondary Worksite Triggers CABG (25%)

B Burns

Cancer in situ (25%)

Blindness/Deafness/Paralysis Blindness/Deafness/Paralysis

Brain Tumor

Occupational HIV Occupational HIV

Parkinsons (25%)

ComaComa

Alzheimers (25%)

Wellness ($50, $75, or $100)

47

Wellness ($50, $75, or $100)

November 17, 2011

P t ti l R ti V i blPotential Rating Variables Plan DesignPlan Design

Age (or composite rate)

Family Tier Family Tier

Tobacco Status

Occupation Occupation

Employer contribution

G d Gender

Area

48 November 17, 2011

Risk CharacteristicsRisk Characteristics

Some “Disease Diversification”Some “Disease Diversification”

Average morbidity by 4 primary diseasesAverage morbidity by 4 primary diseases

Cancer

Heart Attack

Stroke

Kidney Failure

49 November 17, 2011

L R tLapse Rate

Similar to other worksite products.

S t b tt i t *Some report better persistency.*

*Worksite Critical Illness Products 2005Eastbridge Consulting Group

50 November 17, 2011

Eastbridge Consulting Group

Limited Data SourcesLimited Data Sources

G d i d li d t i t i Good insured lives data in some countries (U.K., Australia, Canada, South Africa)

Population data is available in most countries

Data in one country not transferable to another (without adjustment)( j )

51 November 17, 2011

Data SourcesData Sources American Heart Association (heart attack / stroke)

Surveillance Epidemiology and End Results (SEER)

United States Renal Disease System United States Renal Disease System

United Network for Organ Sharing

State hospital databases

Medstat, HCGs databases

52 November 17, 2011

Anti selection ProtectionAnti-selection Protection

Eligibility Criteria Eligibility Criteria- Actively at work- Employed 90 days

Survival Period –- none

Pre-ex PeriodPre ex Period- Standard Pre-ex – 12/12

53 November 17, 2011

Underwriting Guaranteed IssueUnderwriting – Guaranteed Issue Personal Health

- tobacco use (smoker / non-smoker rating)

Financial Limits- Generally limited: $10,000, $15,000 or $20,000

Participation Requirements- Vary by group size

• 200-999 20%• 1000-4999 15%• 5000+ 10%

54 November 17, 2011

Regulatory Issues in U SRegulatory Issues in U.S.

Product approval still difficult in a few statesProduct approval still difficult in a few states Some states object to certain provisions

– Pre-ex variations– Other coverage– Family history questions (Maryland)

Cover those who had breast cancer 2 yrs treatment free– Cover those who had breast cancer 2 yrs treatment free (Florida)

Loss Ratio requirements vary by state

55 November 17, 2011

Q ti ?Questions?

Accident Insurance: An Essential ProductEssential Product

57 November 17, 2011

What is Accident Insurance?

Covers losses due to injuries onlyj y No illnesses are covered Coverage may supplement other g y pp

insurance

58

Accident Death and Dismemberment

Accidental Death Dismemberment Paralysisy Loss of Use (speech, hearing, sight)

59

Accident Only Indemnity Benefitsy y

– Daily Hospital ConfinementInitial Hospitalization

– SurgeryPhysical Therapy and– Initial Hospitalization

– Intensive Care Unit– Dislocations and Fractures

– Physical Therapy and Rehabilitation

– Blood and plasma

– Ambulance– Diagnostic (x-ray, CAT Scan,

MRI)

– Physician follow-up visits– Accident monthly disability

MRI)– Emergency Room– Transportation

C f b– Coverage for burns– Lacerations

60

Accident Only Medical Expense y pCoverage

Full coverage for all medical expenses if due to an accidentS bj t t d d tibl i d i Subject to deductible, coinsurance, and maximum benefit

Maximum benefit equal to deductible on medical planMaximum benefit equal to deductible on medical plan Often sold in conjunction with high deductible plans

61

Travel Accident Coverageg

Covers accident death while travelling for business

May cover injury and provide accident medical expense benefit

62

Underwritingg

Hard to select against accident coverage

Limited or no underwriting– Actively at work– Not engaged in any hazardous avocationsNot engaged in any hazardous avocations– Restrict by industry or occupation– Off the job coverage vs. 24 hour coverage

63

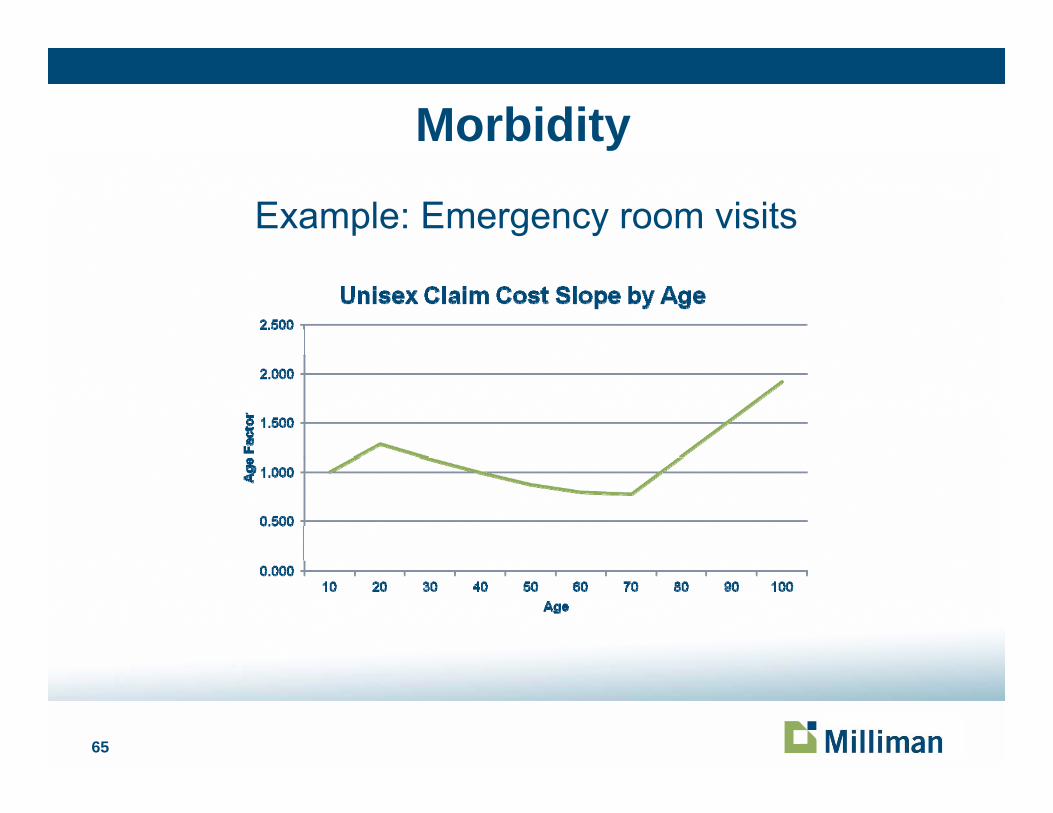

Morbidityy

U-shaped claim slope by age– High for teens early twenties lower in middle ages higher inHigh for teens, early twenties, lower in middle ages, higher in

older/retirement ages

Priced using level claims. Benefit reductions at older ages.Littl ti lif– Little or no active life reserves

Indemnity benefits are not inflation sensitive

64

Morbidityy

Example: Emergency room visits

65

Morbidityy

5

Accidental Deaths per 1,000

4

0

2

3

Dea

ths

per 1

,000

1

02 7 12 17 22 27 32 37 42 47 52 57 62 67 72 77 82 87 92 97

Age

66

Morbidityy

Sources: Accidental Death Accidental Death

- National Safety Council Injury Facts- SOA Reports: Group Life Insurance Experience Committee

> Contains A/E for AD&D by industry categoryy y g y- US Department of Labor – Bureau of Labor Statistics

> Fatal occupational injuries by occupation

Other Benefits – typically priced benefit by benefit usingOther Benefits typically priced benefit by benefit using research, company experience, or proprietary data- National Safety Council Injury Facts- CDC NCHS – Nation Health Survey- CDC’s National Health Statistics Reports- Milliman’s Health Cost Guidelines

67

Other Considerations Expenses

- Claim administration is less than other products.Varies by type of product Adjudicating accidental death vs- Varies by type of product. Adjudicating accidental death vs.

accident disability

CommissionsL R t Lapse Rates- High in payroll markets.

• Limited or no underwriting• Supplemental nature of coveragepp g

Claims Volatility – Varies by size of block- Low incidence- Potentially high claimsPotentially high claims- Low premium

Renewability – most group contracts are optionally renewable

68

renewable

Short Term Disability:Where is it Headed?Where is it Headed?

69 November 17, 2011

Worksite Total Sales (in millions) andWorksite Total Sales (in millions) andWorksite STD as % of Worksite Total

70 November 17, 2011

AgendaAgenda

Why?Why?

What?

Who?

Where?

71 November 17, 2011

Why?Why?1 out of 4

64% / 2% / 30%

44% / 60%

50%

76%76%

72 November 17, 2011

Wh t?What?

73 November 17, 2011

What?What?

D fi itiDefinition

Requirementsequ e e s

WP

BP

Replacement Ratio

74 November 17, 2011

Who?Who?

2010 Group STD Inforce Results2010 Group STD Inforce Results

The Hartford 17.9%Unum 12.6%Lincoln Financial Group 7.9%MetLife 7.6%CIGNA 6 5%CIGNA 6.5%Prudential 5.6%Sun Life Financial 5.5%The Standard 5 4%The Standard 5.4%Guardian Life 4.4%Aetna 4.1%

75 November 17, 2011

Who?Who?

2010 Group STD Sales Resultsp

Unum 11.6%The Hartford 10.4%Lincoln Financial Group 9.8%CIGNA 9.2%Sun Life Financial 6 9%Sun Life Financial 6.9%The Standard 6.5%MetLife 5.0%Liberty Mutual 5 0%Liberty Mutual 5.0%Reliance Standard 4.8%Mutual of Omaha 4.6%

76 November 17, 2011

Wh h it b ?Where….has it been?

77 November 17, 2011

Estimated Worksite STD SalesEstimated Worksite STD Sales (in millions)

78 November 17, 2011

Worksite Group STD Sales as a % ofWorksite Group STD Sales as a % ofEstimated Worksite STD Sales

79 November 17, 2011

Worksite Group STDWorksite Group STD New Sales Increase

80 November 17, 2011

Worksite Group STDWorksite Group STDImputed Termination Rates

81 November 17, 2011

Where….is it headed?

½ of the employers show an interest in replacing l id ith l id b fitemployer-paid with employee paid benefits

82 November 17, 2011

Worksite Group STD as a % ofWorksite Group STD as a % ofGroup STD for New Sales

83 November 17, 2011

Where….is it headed?

Health Promotion Programsg

StrategiesIntegrated Packages- Integrated Packages

- Women- Age Groups

84 November 17, 2011

Agenda

Limited Benefit Medical: PPACA is a Game ChangerPPACA is a Game Changer

85

The Need• Affordable coverage for

Part Time

The Need

– Part Time, – Hourly, – Seasonal, – Waiting Period and – other employees not eligible for Employer Sponsored and

Subsidized Major Medical Coveragej g

• Insureds tend to be lower income• Insureds tend to have higher turnoverInsureds tend to have higher turnover

86

The NeedThe Need

The bottom line….– Need low cost coverage– Need easy access– Need practical, first (or early) dollar

coverage– Need coverage that improves access to

carecare– Need coverage that improves health

87

One Potential Solution

Limited Benefit Medical Plans

One Potential Solution

Affordability for Lower Income = Limited benefits Voluntary Typically minimal or no employer contribution Employer Sponsor Role

Open Enrollment and New Hire Enrollment- Open Enrollment and New Hire Enrollment- Payroll deduction- Sometime Employer Contribution

Benefits to Employer Sponsor- Attract and Retain Employees

M di t bl h lth i t

88

- More predictable health insurance costs

Variations of the SolutionThree Key Approaches to Limited Benefit Plans Scheduled Benefits

Variations of the Solution

- Most common approach- More complicated administratively (tracking of internal limits)- Greater risk transfer for small claims- “Feels” more like hospital indemnity coverage- Typically exempt from HIPAA

Expense Reimbursement Expense Reimbursement- More recent approach- Similar to major medical administration

Less risk transfer for small claims- Less risk transfer for small claims- “Feels” more like major medical- Subject to HIPAA requirements

89

Accident Only

Example: Scheduled Benefits

Inpatient Hospital: $1,200/day

Example: Scheduled Benefits

p p y ICU: $2,400/day Surgical: $2,500 annual max, per scheduleg p Office Dr Visit: $50/visit, up to 6/year Emergency: $100/visit, up to 3/yearg y , p y X-ray & Lab: $50/visit, up to 6/year Wellness: $75/visit, up to 2/year$ , p y

90

Example: Scheduled Benefits

Scheduled Benefits – Other Benefits

Example: Scheduled Benefits

Scheduled Benefits – Other Benefits– Hospital Admission Lump Sum– Outpatient Benefits– Scheduled Surgical Benefits– Anesthesia Benefit– Skilled NursingSkilled Nursing– Transportation– Prescription Drugs

91

Example: Expense Reimbursement

Inpatient Hospital: up to $1,200/day, to

Example: Expense Reimbursement

p p p y$10,000/confinement and $30,000/yr ICU: no additional Surgical: 100% up to $2,500 Office Dr Visit: up to $50/visit, up to 6/year Emergency: up to $100/visit, up to 3/year X-ray & Lab: 100%, up to $200/year Wellness: Annual Checkup qualifies for Dr. Visit

92

Product Variations

Other Key Possibilities

Product Variations

y May have PPO available Benefits may be on a “per cause” basis Varied Limits

- Lifetime Limits- Calendar Year Limits- Benefit Year Limits- Internal Limits (by type of service)( y yp )- Combinations of above- Limits on frequency of use

93

Example: Accident Only

Accident Only Medical

Example: Accident Only

Accident Only Medical Full coverage for all medical expenses if due to an

accident Maximum benefit equal to deductible on medical

planOft ld i j ti ith hi h d d tibl Often sold in conjunction with high deductible plans

94

Access

Simplified Access

Access

p Simplified Rating and Limited Underwriting

- Often Guaranteed Issue with actively at work requirement

Low required participation Pooled rates

95

Expense StructureExpenses (General and Administrative, G&A)

S hi h it t

Expense Structure

Same or higher unit costs Applied against lower claims costs Customer Service Customer Service

- First insurance for many. Lots of questions.

Low (Voluntary) Participation( y) p- Many enrollment kits per actual enrollee

High Turnover- Shorter duration of coverage

MBR 60% or lower60% in line with minimum for Individual (Voluntary)

96

- 60% in line with minimum for Individual (Voluntary)

First (or Early) Dollar Coverage

Question: If you can only afford half the benefits,

First (or Early) Dollar Coverage

which half is better? “First dollar” coverage (low deductibles and copays) with

no catastrophic coverage?no catastrophic coverage?- Covers most expenses for most members.- Not catastrophic- If PPO NetworkIf PPO Network

> Access to healthcare - Insurance Card> Network discount

High deductible catastrophic? High deductible catastrophic?- Benefits very few- They still have to fund high deductibles ($2K-$10k?) out of pocket

97

pocket.

PPACA’s Influence onLimited Benefit Mini-Medical

Plan designs in the market vary between “expense reimbursement”and “fixed indemnity” benefits

Expense reimbursement products will be held to PPACA requirementsExpense reimbursement products will be held to PPACA requirements‒ PPACA bans annual and lifetime limits‒ In the near-term, this would likely wipe out this niche product

Final rules to implement the provision could be written to allow limited‒ Final rules to implement the provision could be written to allow limitedbenefit plans until 2014 when insurance exchanges are set up and taxcredits become available for low wage workers

Fixed indemnity products are “excepted” under the PHSA Fixed indemnity products are excepted under the PHSA‒ 300gg-91(c) Excepted Benefits (3) Benefits not subject to requirements if

offered as independent, non-coordinated benefits(B) Hospital indemnity or other fixed indemnity insurance

98

(B) Hospital indemnity or other fixed indemnity insurance

Limited Benefit Mini-MedicalLimited Benefit Mini Medical Plan designs in the market vary between “expense reimbursement” and

“fixed indemnity” benefitsfixed indemnity benefits

Fixed indemnity products are “excepted” under the PHSA‒ 300gg-91(c) Excepted Benefits (3) Benefits not subject to requirements if300gg 91(c) Excepted Benefits (3) Benefits not subject to requirements if

offered as independent, non-coordinated benefits(B) Hospital indemnity or other fixed indemnity insurance

Expense reimbursement products will be held to PPACA requirements‒ PPACA bans annual and lifetime limits‒ In the near-term, this would likely wipe out this niche product‒ Final rules to implement the provision could be written to allow limited benefit plans

until 2014 when insurance exchanges are set up and tax credits become availablefor low wage workers

99

Limited Benefit Mini-MedicalLimited Benefit Mini Medical

HHS set up a process to provide waivers from requirements of thep p p qAffordable Care Act. This provided “mini-med” providers a means ofrequesting exceptions from the act.

HHS announced the first round of waivers. Recipients included:- Businesses: McDonald’s, Jack in the Box, Inc.- Unions: United Federation of Teachers, Intl Union of Painters…- Insurers: Aetna, Cigna, Mega Life and Health- A total of 1,578 waivers approved as of 7/22/2011.

Waivers are for one year renewal can be requested Requests must Waivers are for one year – renewal can be requested. Requests musthave been filed by September 22, 2011.

100

Reinsurance: Small Coverage Providing Big ValueProviding Big Value

101 November 17, 2011

Why I Love WorksiteWhy I Love Worksite…

102

5-Year Mortality under Existing U/Wy g

1600

1800

1200

1400

1600

Population

800

1000PopulationSuper PNTStd NTGroup

200

400

600 Worksite NTSimp. Iss. NT

0Male Age 45 Deaths per

100,000

103

Mortality and Morbidity Results y yImpacted by…

The population segment you’re drawing from

The underwriting filter used to measure risk

A Si lifi d I I t t I t t A Simplified Issue or Instant Issue program must create a combination of market segment and underwriting filter that produces acceptable mortalityp p y

104

Why You May Not Love WorksiteWhy You May Not Love Worksite…

Don’t like all the mortality and/or morbidity risks Don’t have the capital to support growth Don’t have the expertise to enter the market Don’t have the technology to enter the market

105

Reinsurers Willing to Help…g p

There are reinsurers out there who do love the mortality and morbidity risk on worksite.

There are reinsurers out there with the technology, expertise and capital to help support worksite carriersexpertise and capital to help support worksite carriers.

106

Consultants Willing to Help…g p

There are consultants out there who do know the mortality and morbidity risk on worksite.

There are consultants out there with the tools, expertise and human capital to help support worksite carriersand human capital to help support worksite carriers.

107

Intelliscript Prescription Histories Database

Underwriting Tool Utilizing Red / Yellow / Green Classification

Every drug mapped to an underwriting significance• Significant (e g Coumadin)• Significant (e.g. Coumadin)

• Potentially Significant (e.g. Norvasc)

• Likely Not Significant (e.g. Amoxicillin)

Separate mappings for Life / Health / LTC Client may use mappings “out of the box” or customize Valuable in worksite limited underwriting environment

108

108

Valuable in worksite limited underwriting environment

In Conclusion…

There are many roadblocks to overcome before an insurance carrier chooses to enter or grow in the worksite

k tmarket.

Reinsurers are an excellent resource for overcoming Reinsurers are an excellent resource for overcoming specific insurance risk aversion (CI, DI, SI, GI), technology, expertise, and capital constraints that you are faced with.

109