acquisition of rugby architectural building products · acquisition of rugby architectural building...

TRANSCRIPT

Acquisition of Rugby Architectural

Building Products

“Creating the leading diversified hardwood lumber, panel and interior

architectural building materials distributor in North America”

Investor Presentation

June 13, 2016

Prospectus Information PROSPECTUS INFORMATION A preliminary short form prospectus containing important information relating to the securities described in this document has not yet been filed with the securities regulatory authorities in each of the provinces of Canada (other than Quebec). A

copy of the preliminary short form prospectus is required to be delivered to any investor that received this document and expressed an interest in acquiring the securities.

There will not be any sale or any acceptance of an offer to buy the securities until a receipt for the final short form prospectus has been issued.

This document does not provide full disclosure of all material facts relating to the securities offered. Investors should read the preliminary short form prospectus, final short form prospectus and any amendment, for disclosure of those facts,

especially risk factors relating to the securities offered, before making an investment decision.

The short form prospectus will constitute a public offering of the securities described therein and herein only in those jurisdictions where they may be lawfully offered for sale and therein only by persons authorized to sell such securities. The

securities which will be offered by the short form prospectus have not been and will not be registered under the United States Securities Act of 1933, as amended (the "1933 Act"), or any state securities laws and may not be offered or sold in

the United States, except in transactions exempt from the registration requirements of the 1933 Act and any applicable state securities laws. This presentation does not and the short form prospectus will not constitute an offer to sell or a

solicitation of an offer to buy any of these securities within the United States.

1

Forward Looking Statements

2

FORWARD LOOKING STATEMENTS Certain statements in this presentation may constitute “forward-looking information” or “financial outlook” within the meaning of applicable securities laws that involve known and unknown risks, uncertainties and other factors that may cause

actual results, performance or achievements or industry results to be materially different from any future results, performance or achievements or industry results expressed or implied by such forward-looking information or financial outlook.

Forward-looking information and financial outlook are identified by the use of terms and phrases such as “anticipate”, “believe”, “could”, “estimate”, “expect”, “intend”, “may”, “plan”, “predict”, “project”, “will”, “would”, and similar terms and

phrases, including references to assumptions. Such information may involve, but is not limited to, comments with respect to strategies, expectations, planned operations or future actions. Forward-looking information in this presentation

includes, without limitation, statements with respect to: Hardwoods’ anticipated business prospects; Hardwoods’ financial and operational performance, including the performance of its subsidiaries; the planned acquisition, including the

expected terms and closing thereof; plans regarding financing for the acquisition; contingent consideration for the acquisition; expectations or projections about strategies and goals for growth and expansion; expectations regarding realization

of synergies and accretion following the acquisition, and the timing thereof; expected impacts of the acquisition on EBITDA, Adjusted EBITDA, Pro Forma Adjusted EBITDA, sales, Adjusted Sales, Pro Forma Sales, earnings, cash flow, Payout

Ratio, Pro Forma Payout Ratio and dividend growth, as well as on Hardwoods’ future ability to reduce leverage levels; Rugby’s employees; planned changes in Hardwoods’ business, including the addition of new lines of business; expected

operating and financial results; and expected industry, market and economic conditions.

The forecasts and projections that make up the forward-looking information and financial outlook in this presentation are based on management’s expectations and assumptions regarding historical trends, current conditions and expected

future developments, which include, but are not limited to: the satisfactory timing and receipt of regulatory approval with respect to the acquisition and all related transactions; the completion of the acquisition; Hardwoods realizing the expected

benefits and synergies of the acquisition; no undisclosed liabilities associated with the acquisition; no material adverse changes occur in respect of the assets to be acquired before the completion of the acquisition; Hardwoods can comply with

the restrictive conditions required by the debt financing to be completed for the acquisition; there are no material exchange rate fluctuations between the Canadian and US dollar that affect Hardwoods’ performance; the general state of the

economy does not worsen.

The forward-looking information and financial outlook in this presentation is subject to risks, uncertainties and other factors that could cause actual results to differ materially from historical results or results anticipated by the forward-looking

information. The factors which could cause results to differ from current expectations include, but are not limited to: failure to raise the funds necessary to complete the acquisition; failure to close the acquisition; failure to realize the expected

returns and synergies of the acquisition; potential undisclosed liabilities associated with the acquisition; no control by Hardwoods over the assets to be acquired until completion of the acquisition; the acquisition debt financing will be subject to

certain restrictive conditions that limit the discretion of management; Hardwoods’ high dependency on the assets and business acquired from the vendors, if the acquisition closes; exchange rate fluctuations between the Canadian and US

dollar could affect Hardwoods’ performance; Hardwoods’ results are dependent upon the general state of the economy. More information about the risks and uncertainties affecting Hardwoods’ business can be found in the “Risk Factors”

section of its Annual Information Form dated March 11, 2016 which is available under Hardwoods’ profile on SEDAR at www.sedar.com.

To the extent any forward-looking information or statements in this presentation constitute a “financial outlook” within the meaning of securities laws, such information is being provided to demonstrate the potential benefits of the transaction and

management’s estimate of the future financial performance of Rugby, and readers are cautioned that this information may not be appropriate for any other purpose and that they should not place undue reliance on such information.

Although Hardwoods has attempted to identify factors that would cause actual actions, events or results to differ materially from those disclosed in the forward-looking statements or information or financial outlook, there may be other factors

that cause actions, events or results not to be as anticipated, estimated or intended. Also, many of the factors are beyond the control of Hardwoods. Accordingly, readers should not place undue reliance on forward-looking statements or

information. The forward-looking information is made as of the date of this presentation (or in the case of information contained in a document incorporated by reference herein, as of the date of such document), and Hardwoods assumes no

obligation to publicly update or revise such forward-looking information to reflect new information, subsequent or otherwise, except as may be required by applicable securities law. The forward-looking information contained herein is expressly

qualified in its entirety by this cautionary statement.

For the last twelve months (“LTM”) period ended March 31, 2016 all dollar amounts converted from US dollars to Canadian dollars using an average exchange rate of US$1.00 = C$1.3114.

See Appendix A, B and C to this presentation for non-IFRS and non-U.S. GAAP reconciliations.

Non-IFRS and Non-U.S. GAAP Measures

3

NON-IFRS AND NON-U.S. GAAP MEASURES This presentation makes reference to certain non-IFRS financial measures, in the case of the Company, or non-U.S. GAAP financial measures, in the case of Rugby. These non-IFRS and non-U.S. GAAP financial measures are not recognized

measures under IFRS and U.S. GAAP, as applicable, do not have a standardized meaning prescribed by IFRS or U.S. GAAP, as appl icable, and are therefore unlikely to be comparable to similar measures presented by other publicly traded

companies, and should not be construed as an alternative to other financial measures determined in accordance with IFRS and U.S. GAAP, as applicable. Rather, these financial measures are provided as additional information to complement

IFRS and U.S. GAAP financial measures by providing further understanding of operations from management’s perspective. Accordingly, non-IFRS and non-U.S. GAAP financial measures should never be considered in isolation nor as a

substitute to using net income as a measure of profitability or as an alternative to the IFRS consolidated statements of income or other IFRS or U.S. GAAP statements. Management presents non-IFRS and non-U.S. GAAP financial measures,

specifically Adjusted Sales, EBITDA, Adjusted EBITDA, Pro Forma Adjusted EBITDA, Payout Ratio and Pro Forma Payout Ratio as i t believes these supplementary disclosures provide useful additional information related to the operating

results and financial condition of the Company and uses these measures of financial performance and financial condition as a supplement to the consolidated statements of income and statements of financial position of the Company and

Rugby.

The definitions of the non-IFRS and non-U.S. GAAP measures contained in this presentation are as follows: (i) “Adjusted Sales” means sales including the full year results from acquisitions completed during the period and elimination of sales

from locations closed during the period; (ii) “EBITDA” means earnings before interest, taxes, depreciation and amortization; (iii) “Adjusted EBITDA” means earnings before interest, taxes, depreciation and amortization with adjustments for

owner costs and one-time expenses, adjustment to reflect full-year results from acquisitions completed during the period and elimination of results from locations closed during the period, as well as anticipated net benefits from ongoing

initiatives; (iv) “Pro Forma Adjusted EBITDA” means Rugby’s Adjusted EBITDA combined with Hardwoods’ EBITDA; (v) “Payout Ratio” means total dividends paid for the period divided by cash flow from operations before changes to working

capital and less maintenance capital expenditures for the period; and (v) “Pro Forma Payout Ratio” means Pro Forma total dividends paid for the period divided by Pro Forma cash flow from operations before changes to working capital less

maintenance capital expenditures for the period.

For the LTM period ended March 31, 2016 all dollar amounts converted from US dollars to Canadian dollars using an average exchange rate of US$1.00 = C$1.3114.

See Appendix A, B and C to this presentation for non-IFRS and non-U.S. GAAP reconciliations, as well as management’s discussion and analysis of Hardwoods dated May 12, 2016 for the three month period ended March 31, 2016 and

management’s discussion and analysis of Hardwoods dated March 11, 2016 for the year ended December 31, 2015.

Transaction Highlights

4

• Significantly enhances the financial scale of Hardwoods

• Increases Hardwoods’ presence in the commercial end-market, a key strategic objective for the

Company

• Positions Hardwoods for further US expansion and growth

• Establishes Hardwoods as the number one North American distributor of hardwood lumber, panel

and interior architectural building materials

• Diversifies Hardwoods’ customer and product concentration

• Expands Hardwoods’ US geographic footprint with significantly increased presence in the Eastern

US

• Aligned and incentivized management, and accretive earn-out structure

(1) “Payout Ratio”, “Pro Forma Payout Ratio” and “Pro Forma Adjusted EBITDA” are Non-IFRS and Non-U.S. GAAP

measures, see “Non-IFRS and Non-U.S. GAAP measures”

(2) See “Appendix C – Payout Ratio Buildup”

(3) See “Appendix B – Adjusted EBITDA Buildup”

• Enables a ~14% increase to the annual dividend while reducing the Q1 2016 Payout Ratio(1)(2) from

20.3% to a Pro Forma Payout Ratio(1)(2) of 17.8%

• Efficient use of Hardwoods’ debt capacity; debt to LTM Pro Forma Adjusted EBITDA(1)(3) of 2.3x

• Immediately accretive with further upside from expected synergies

1

2

3

4

5

6

7

8

9

10

Transaction Overview

5

Purchase Price Purchase of 100% of the assets of Rugby(1) for US$107 MM

- Additional consideration through earn-out of up to US$13 MM based on achieving certain

performance targets above internal budgets over a two year period after closing

Form of

Consideration

US$100 MM cash consideration, subject to traditional purchase price adjustments

US$7 MM equity subject to contractual restrictions on transfer

Up to an additional US$13 MM in cash or equity, with the amount to be determined and paid upon

achievement of certain performance targets

Financial

Impact

Expected to be accretive to both earnings per share (“EPS”) and cash flow per share (“CFPS”) prior to

any synergies

Identified synergies, include operational, structural and revenue efficiencies

Dividend increase(2) to $0.25 / year (~14% increase) while reducing the Q1 2016 Payout Ratio(3)(4) from

20.3% to a Pro Forma Payout Ratio(3)(4) of 17.8% (~12% reduction)

Transaction

Financing

Combined debt / Pro Forma Adjusted EBITDA(3)(5) of 2.3x

US$107 MM in fully committed financing with the acquisition; ~US$65 MM via increased debt facility,

~US$35 MM equity raise, US$7 MM equity to Rugby

Conditions and

Timing

Subject to third-party approvals, including approval of the TSX and US antitrust approval

Anticipated closing – July 2016

(1) “Rugby” means Rugby Acquisition, LLC and its subsidiaries, collectively doing business as

Rugby Architectural Building Products

(2) Expected to be effective for Q3 2016 dividend, subject to closing of the Transaction

(3) “Payout Ratio”, “Pro Forma Payout Ratio” and “Pro Forma Adjusted EBITDA” are Non-IFRS

and Non-U.S. GAAP measures, see “Non-IFRS and Non-U.S. GAAP Measures”

(4) See “Appendix C – Payout Ratio Buildup”

(5) See “Appendix B – Adjusted EBITDA Buildup”

Overview of Rugby Nationally-recognized industry leader in the one-step distribution of non-structural,

architectural-grade interior building products

6

One-Step Distribution Model Positioned as a critical link between customers

and suppliers

Leading Market Position 31 locations in the US

- 15 on the East coast

Full Product Offering Offers ~30,000 stocking SKUs

- ~6,000 non-stock SKUs

Diversified Customer / Supplier Base Approx. 800 suppliers and 22,000 customers

Strong Financial Performance US$282 MM in LTM(1) Adjusted Sales(2)(3) and

US$12.5 MM in LTM Adjusted EBITDA(2)(4)

Proven M&A Strategy 17 completed acquisitions since 2009

Track record of effective integration

(1) “LTM” means last twelve months ended March 31, 2016

(2) “Adjusted Sales” and “Adjusted EBITDA” are Non-IFRS and Non-U.S. GAAP measures, see “Non-IFRS and Non-U.S. GAAP Measures”

(3) See “Appendix A – Adjusted Sales Buildup”

(4) See “Appendix B – Adjusted EBITDA Buildup”

History of Rugby Through various initiatives, current management of Rugby has transformed their business

into a leading distributor of building products in the U.S.

7

2005

2009

2015

Spun out from

RMC plc

following MBO

Acquires 2

Facilities

Acquires

Northern

Pacific Group

2012 2013

2014

2010

2011

Acquired by

Current

Management

Acquires 11

Facilities

Leading Ridge

Invests

Acquires 13

Facilities

Acquires

Walden’s

Distributing

2016

Acquires 4

Facilities

Note: Acquisitions prior to closures

6%4%

5%

85%

Top 10 11-25 26-50 Others

46%

18%

14%

22%

Top 10 11-25 26-50 Others

Supply Chain

8

• Approximately 800 supplier

relationships

• Average tenure of ~12 years

across top 10 suppliers

• Supplies branded and non-

branded products

• Approximately 22,000 customer

relationships

• Average tenure of ~20 years

across top 10 customers

• Customers include: contractors,

retailers, manufacturers, etc.

Like Hardwoods, Rugby’s distribution model positions the Company as a critical link

connecting suppliers and customers for the distribution of building materials

Suppliers Customers

Supplier Concentration(1) Customer Concentration(1)

(1) Rugby Management estimate for the LTM period ended March 31, 2016

Products Offered

9

LTM Contribution(1)

US$168 million of Adjusted Sales(2)

~60% of total sales

~24% gross margin

Key Products

• Doors • Plywood

• Components • Lumber

• Hardware • Panels

LTM Contribution(1)

US$53 million of Adjusted Sales(2)

~19% of total sales

~19% gross margin

Key Products

• Interior Doors • Door Jambs

• Exterior Doors • Hardware

• Mouldings • Lights

LTM Contribution(1)

US$60 million of Adjusted Sales(2)

~21% of total sales

~26% gross margin

Key Products

• Laminate • Sinks / Faucets

• Countertops • Solid Surfacing

• Panels • Adhesives

Rugby offers a full line of non-structural, architectural-grade building products

Cabinets & Casework Decorative Surfacing Doors & Millwork

(1) Rugby Management estimate for the LTM period ended March 31, 2016

(2) “Adjusted Sales” is a Non-IFRS and Non-U.S. GAAP measure, see “Non-IFRS and Non-U.S. GAAP Measures”;

See “Appendix A – Adjusted Sales Buildup”

Note: Differences in Adjusted Sales to Appendix A are due to rounding

Key Benefits

10

Establishes a Leading

North American Distributor

Enhances Financial

Scale

Immediately Accretive

Increase to Dividend

1

2

3

4

Results in expanded national footprint with the addition of 31 facilities

Improves Balance Sheet

Efficiency

Increased Eastern US

Presence

5

6

(1) “Adjusted Sales”, “Adjusted EBITDA”, “EBITDA”, “Pro Forma Payout Ratio” and “Payout Ratio” are Non-IFRS and

Non-U.S. GAAP measures, see “Non-IFRS and Non-U.S. GAAP Measures”

(2) See “Appendix A – Adjusted Sales Buildup”

(3) See “Appendix B – Adjusted EBITDA Buildup”

(4) See “Appendix C – Payout Ratio Buildup”

Diversifies Platform

Aligned Management

Positioned for Further

Growth

7

8

9 Rugby has completed and integrated 17 acquisitions since 2009 and

has a robust acquisition pipeline

Earned US$282 MM in LTM Adjusted Sales(1)(2) and US$12.5 MM in

LTM Adjusted EBITDA(1)(3) – management is targeting EBITDA(1) for

Rugby of between US$13 MM and US$14 MM for 2016

Expected to be immediately accretive to EPS and CFPS pre-synergies

A ~14% increase to the annual dividend while reducing the Q1 2016

Payout Ratio(1)(4) from 20.3% to a Pro Forma Payout Ratio(1)(4) of 17.8%

Approximately 60% funded with debt; combined debt to LTM Pro Forma

Adjusted EBITDA(1) of 2.3x

~40% of Rugby’s LTM sales and 15 of Rugby’s locations are in the US

Northeast and Southeast markets

Increases presence in the commercial end market and adds

approximately 22,000 customers, diversifying Hardwoods’ customer

and product concentration

Management team has an established track record; CEO and COO will

own Hardwoods’ shares and participate in earn-out

11

Expanded National Footprint More than doubles the existing US branch location footprint, including significant East coast

presence, with minimal geographic overlap with Hardwoods existing locations

Northeastern and Southern

markets represent ~60%(1) of

total housing starts

Hardwoods Facility

Rugby Facility

(1) Per National Association of Home Builders, as at April 29, 2016

Triples number of locations in

these regions

13%

31%

27%

30%

48%

23%

29%24%

15%

30%

30%

Enhances Diversification

12

Geographic Concentration(1)

End Market Concentration(2)

61%

39%

20%

60%

20% 20%

60%

20%

Commercial Residential Other

36%

52%

12%

22%

17%33%

28%

Canada East U.S. West U.S. Central U.S.

(1) By number of branches

(2) By sales, for the LTM period ended March 31, 2016

52%38%

10%

Complementary Product Additions

13

Product Concentration(1)

Acquisition significantly broadens and diversifies Hardwoods’ product offering

Interior Doors Catches Hardware Faucets

40%

26%

12%

8%

7%6%

40%

26%

12%

8%

7%

6%

Sheets Lumber Other Casework Surfacing Doors & Millwork Other

Cabinets Coating

(1) For the LTM period ended March 31, 2016; based on Adjusted Sales; “Adjusted Sales” is a Non-IFRS and Non-

U.S. GAAP measure, see “Non-IFRS and Non-U.S. GAAP Measures”; See “Appendix A – Adjusted Sales Buildup”

Exterior Doors

20%

8%

31%

21%

19%

Sheets Lumber

14

Acquisition increases Hardwoods’ exposure to the improving U.S. housing market

Housing Starts (000s)(1)

Spending on Non-Residential Construction (US$B)(2)

Positioned for Further Growth

1,569 1,6031,705

1,8481,956

2,068

1,801

1,355

906

554 587 609781

925 1,0031,112 1,175

1,353

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

Long-Term Avg: ~1,450

$342 $347 $319 $309 $324 $346$390

$463$500

$437

$348 $337 $355 $360$389

$450$483 $510

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

(1) Per National Association of Home Builders, as at April 29, 2016

(2) Per FMI Consulting; FMI's Construction Outlook First Quarter Report (2016)

$594

$370

$964

$0

$500

$1,000

$1,500

Sale

s (

C$)

$37

$16

$53

$0

$25

$50

$75

EB

ITD

A (

C$)

15

Acquisition significantly enhances Hardwoods’ financial profile

Pro Forma Financials (C$)

LTM Pro Forma Sales(1)(2)(4)

LTM Pro Forma Adjusted EBITDA(1)(2)(5)

Financial Leverage(3)

Current Debt ~C$35 MM

Acquisition Debt ~C$85 MM

Pro Forma Total Debt ~C$120 MM

~2.3x Combined Debt to LTM Pro Forma Adjusted EBITDA(1)

(1) “Pro Forma Sales” and “Pro Forma Adjusted EBITDA” are Non-IFRS and Non-U.S. GAAP

measures, see “Non-IFRS and Non-U.S. GAAP Measures”

(2) Utilizes an average USD / CAD exchange rate of ~$1.31

(3) Utilizes a USD / CAD exchange rate of ~$1.30 (March 31, 2016)

(4) See “Appendix A – Adjusted Sales Buildup”

(5) See “Appendix B – Adjusted EBITDA Buildup”

16

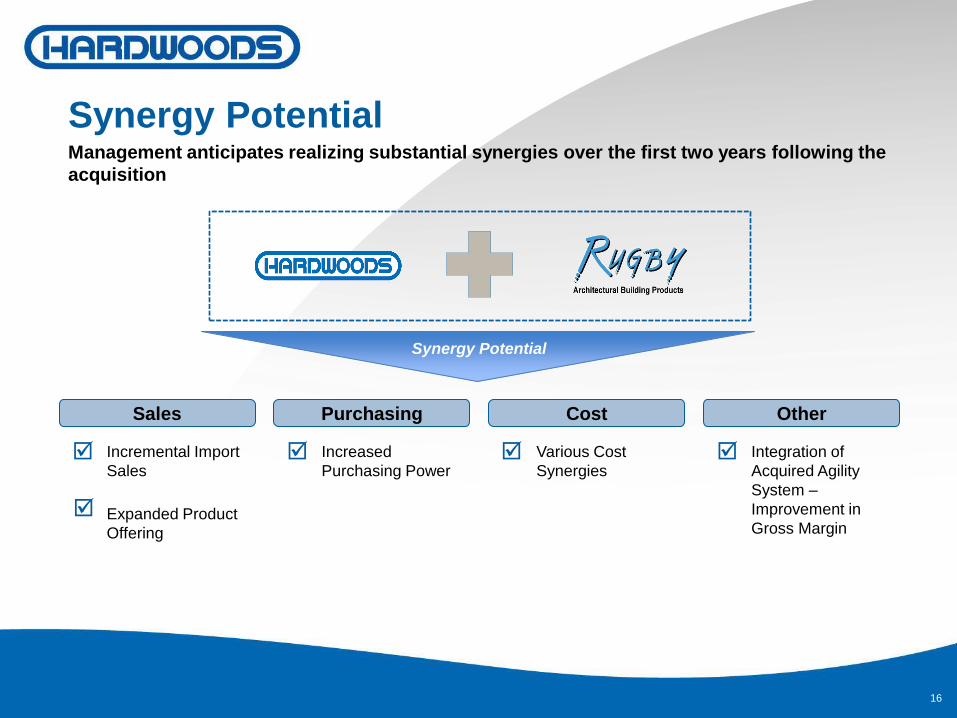

Synergy Potential

Sales

Synergy Potential Management anticipates realizing substantial synergies over the first two years following the

acquisition

Purchasing Cost Other

Incremental Import

Sales

Expanded Product

Offering

Increased

Purchasing Power

Various Cost

Synergies

Integration of

Acquired Agility

System –

Improvement in

Gross Margin

17

Financing and Capital Markets Impact

Equity

~C$50 MM bought deal financing led by Cormark Securities

US$7 MM of equity issued as partial consideration

- Float expected to increase by ~30%(1)

Debt U.S. chartered bank to fund US$65 MM debt requirement

- 5 year term at competitive rates

Positioning

Pro forma market capitalization and enterprise value of ~C$303 MM(2) and ~C$424 MM(2),

respectively

Expected to be accretive to EPS and CFPS before operating and structural synergies

Annual dividend increase to $0.25 / share (~14% increase) from $0.22 / share

Payout Ratio(3)(4) reduces from 20.3% to a Pro Forma Payout Ratio(3)(4) of 17.8% (Q1 2016

basis)

Clean balance sheet and current financing environment provides an opportunity to secure

favourable financing terms

(1) Float calculated as total shares outstanding less insider holdings

(2) Market capitalization based on a C$14.50 Hardwoods’ share price and includes the dilutive securities from

Hardwoods’ long-term incentive plan; enterprise value utilizes pro forma balance sheet items as of March 31, 2016

(3) “Payout Ratio” and “Pro Forma Payout Ratio” are Non-IFRS measures, see “Non-IFRS and Non-U.S. GAAP

measures”

(4) See “Appendix C – Payout Ratio Buildup”

18

Pro Forma Summary

Op

era

tio

nal

Facilities 33 31 64

Customers 10,000 22,000 32,000

Fin

an

cia

l LTM Adjusted

Sales(2) C$594 MM C$370 MM C$964 MM

LTM Adjusted

EBITDA(2) C$37 MM C$16 MM C$53 MM

Sc

ale

Market Cap(5) C$245 MM C$58 MM C$303 MM

Enterprise(5)

Value C$281 MM C$142 MM C$424 MM

(1)

(3)

(4)

(1) Market capitalization based on a C$14.50 Hardwoods’ share price and includes the dilutive securities from Hardwoods’ long-term incentive plan; enterprise value utilizes pro forma balance sheet items as of March 31, 2016

(1) LTM Sales and EBITDA converted utilizing an average USD / CAD exchange rate

of ~$1.31; any debt outstanding converted at a USD / CAD FX rate of $1.30

(2) “Adjusted Sales” and “Adjusted EBITDA” are Non-IFRS and Non-U.S. GAAP

measures, see “Non-IFRS and Non-U.S. GAAP Measures”

(3) See “Appendix A – Adjusted Sales Buildup”

(4) See “Appendix B – Adjusted EBITDA Buildup”

(5)

(3)

(4)

19

Summary

• Adds LTM Adjusted EBITDA(1)(2)(3) of US$12.5 million, bringing LTM Pro Forma

Adjusted EBITDA(1)(2)(3) to C$53 million

• ~14% increase to dividend while reducing Payout Ratio(2)(4) by 12%

• Establishes Hardwoods as the leading North American hardwood distribution

company

• Expected to be immediately accretive to both CFPS and EPS

• Adds 31 new US locations, more than doubling the existing US branch

location footprint, including significant East coast presence

(1) LTM Sales and EBITDA and any debt outstanding converted at a USD / CAD FX rate of $1.31 (March 31, 2016)

(2) “Adjusted EBITDA”, “Pro Forma Adjusted EBITDA” and “Payout Ratio” are Non-IFRS and Non-U.S. GAAP

measures, see “Non-IFRS and Non-U.S. GAAP Measures”

(3) See “Appendix B – Adjusted EBITDA Buildup”

(4) See “Appendix C – Payout Ratio Buildup”

20

Appendix A – Adjusted Sales Buildup

Sales Reconciliation

(Year Ended December 31) (Quarter Ended March 31) (Year Ended March 31)

(US$MM, unless otherwise specified) 2015 Q1/15 Q1/16 LTM

Rugby Sales $271.6 $65.5 $68.2 $274.3

Net Facility Increase (Acquisitions) $6.8 $1.0 $2.3 $8.0

Rugby Adjusted Sales $278.3 $66.5 $70.4 $282.3

FX Rate (C$ / US$) $1.2787 $1.2412 $1.3732 $1.3114

Rugby Adjusted Sales (C$) $355.9 $82.5 $96.7 $370.2

Hardwoods’ Sales (C$) $571.6 $135.1 $157.4 $593.9

Pro Forma Sales (C$) $927.5 $217.6 $254.1 $964.1

Note: Differences due to rounding

21

Appendix B – Adjusted EBITDA Buildup

(Year Ended December 31) (Quarter Ended March 31) (Year Ended March 31)

(US$MM, unless specified otherwise) 2015 Q1/15 Q1/16 LTM

Rugby Net Earnings $3.1 $0.6 $1.6 $4.2

Provision for Income Taxes $0.9 $0.2 $0.0 $0.7

Interest Expense $1.3 $0.4 $0.3 $1.2

Depreciation and Amortization $2.9 $0.7 $0.7 $2.9

Amortization of Loan Origination Costs $0.1 $0.0 $0.0 $0.1

Miscellaneous and Other Income ($0.2) $0.0 ($0.1) ($0.3)

Rugby EBITDA $8.1 $1.9 $2.6 $8.8

Normalizations

Net Facility Increase (Acquisitions) $1.6 $0.4 $0.3 $1.6

Owner Costs and One-Time Expenses $1.1 $0.3 $0.3 $1.1

Ongoing Initiatives $1.4 $0.4 $0.0 $1.0

Rugby Adjusted EBITDA $12.2 $3.0 $3.3 $12.5

FX Rate (C$ / US$) $1.2787 $1.2412 $1.3732 $1.3114

Rugby Adjusted EBITDA (C$) $15.6 $3.7 $4.5 $16.4

Hardwoods EBITDA (C$) $34.8 $7.6 $9.4 $36.6

Pro Forma Adjusted EBITDA (C$) $50.4 $11.3 $13.9 $53.0

EBITDA Reconciliation

Note: Differences due to rounding

22

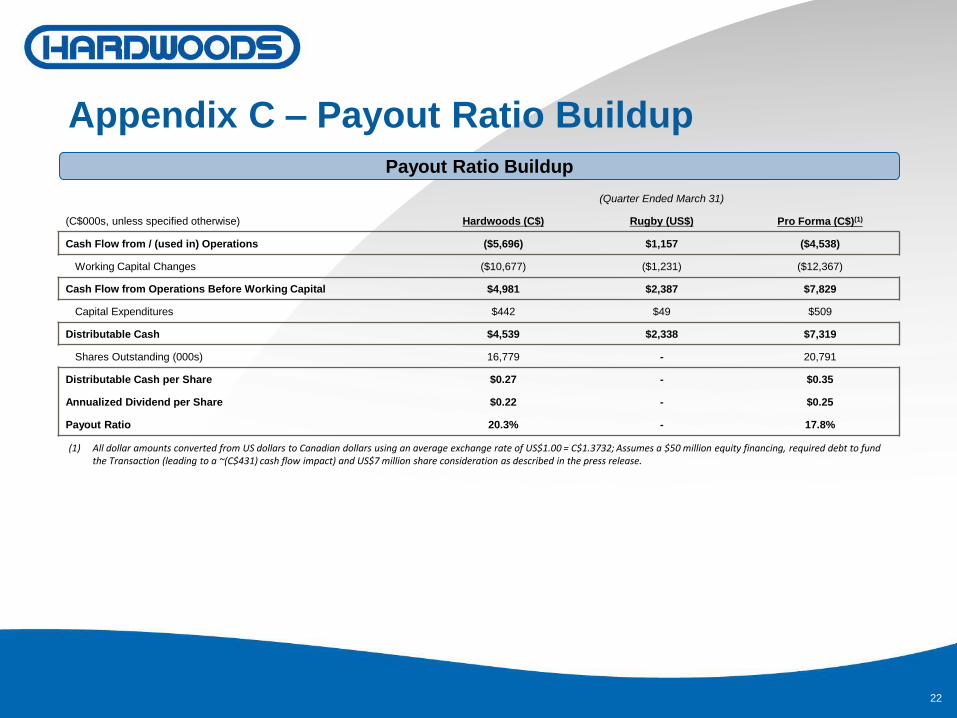

Appendix C – Payout Ratio Buildup

Payout Ratio Buildup

(Quarter Ended March 31)

(C$000s, unless specified otherwise) Hardwoods (C$) Rugby (US$) Pro Forma (C$)(1)

Cash Flow from / (used in) Operations ($5,696) $1,157 ($4,538)

Working Capital Changes ($10,677) ($1,231) ($12,367)

Cash Flow from Operations Before Working Capital $4,981 $2,387 $7,829

Capital Expenditures $442 $49 $509

Distributable Cash $4,539 $2,338 $7,319

Shares Outstanding (000s) 16,779 - 20,791

Distributable Cash per Share $0.27 - $0.35

Annualized Dividend per Share $0.22 - $0.25

Payout Ratio 20.3% - 17.8%

(1) All dollar amounts converted from US dollars to Canadian dollars using an average exchange rate of US$1.00 = C$1.3732; Assumes a $50 million equity financing, required debt to fund the Transaction (leading to a ~(C$431) cash flow impact) and US$7 million share consideration as described in the press release.