acct 2302 fundamentals of accounting ii spring 2011 lecture 12 professor jeff yu

DESCRIPTION

ACCT 2302 Fundamentals of Accounting II Spring 2011 Lecture 12 Professor Jeff Yu. Review:. Budgeted R.M. Purchase in units = budgeted Production in Units * R.M. needed for each unit + desired ending R.M. inventory – beginning R.M. Inventory - PowerPoint PPT PresentationTRANSCRIPT

ACCT 2302

Fundamentals of Accounting II

Spring 2011

Lecture 12

Professor Jeff Yu

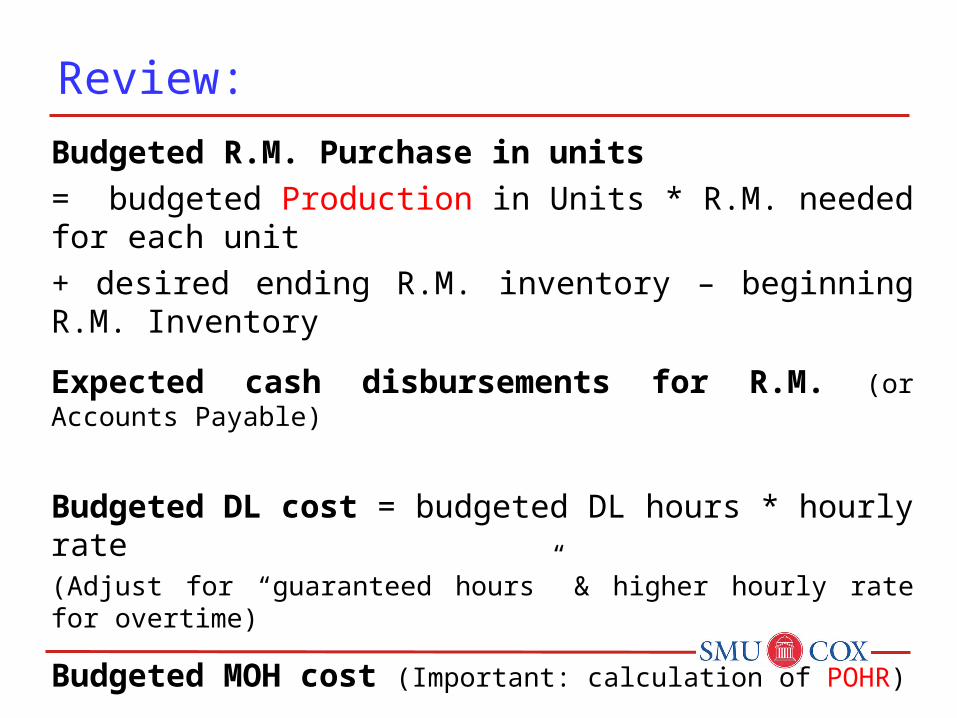

Budgeted R.M. Purchase in units

= budgeted Production in Units * R.M. needed for each unit + desired ending R.M. inventory – beginning R.M. Inventory

Expected cash disbursements for R.M. (or Accounts Payable)

Budgeted DL cost = budgeted DL hours * hourly rate(Adjust for “guaranteed hours” & higher hourly rate for overtime)

Budgeted MOH cost (Important: calculation of POHR)

Budgeted S&A expense

Budgeted ending F.G. Inventory

Review:

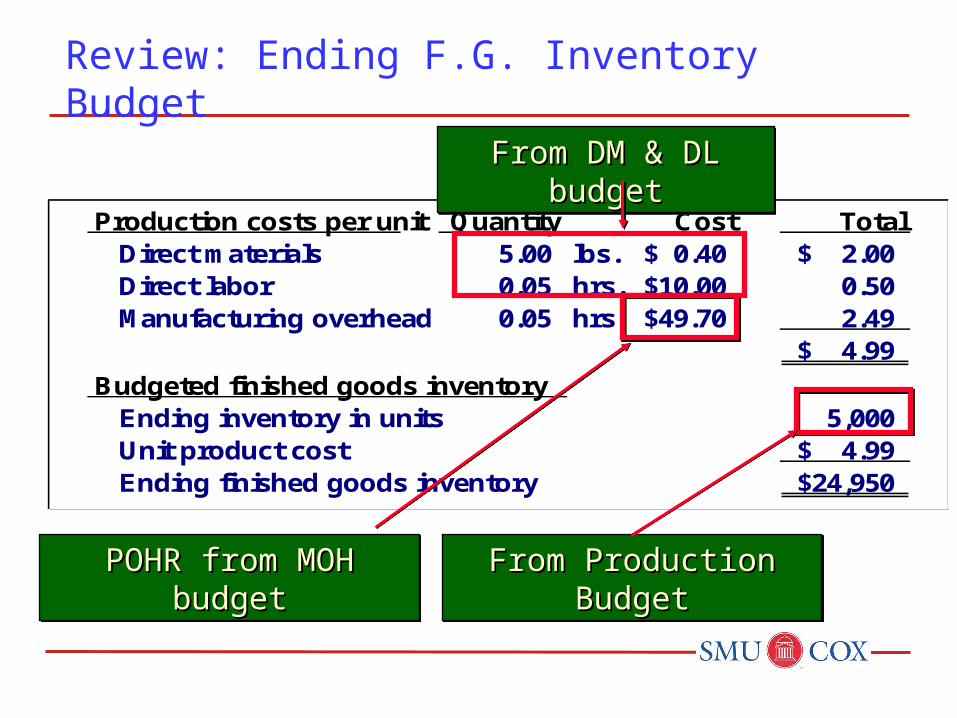

Production costs per unit Quantity Cost Total Direct materials 5.00 lbs. 0.40$ 2.00$ Direct labor 0.05 hrs. 10.00$ 0.50 Manufacturing overhead 0.05 hrs. 49.70$ 2.49

4.99$

Budgeted finished goods inventory Ending inventory in units 5,000 Unit product cost 4.99$ Ending finished goods inventory 24,950$

From Production BudgetFrom Production BudgetFrom Production BudgetFrom Production BudgetPOHR from MOH budgetPOHR from MOH budgetPOHR from MOH budgetPOHR from MOH budget

Review: Ending F.G. Inventory Budget

From DM & DL From DM & DL budgetbudget

From DM & DL From DM & DL budgetbudget

Tonga toys makes Playclay. The desired ending F.G. inventory is 30% of the next month’s sales. Each unit of Playclay sells for $10, requires 2 pounds of raw materials at $0.2 per pound, and consumes 0.25 direct labor hour at $10 per hour. POHR is $0.4 per direct labor hour. Based on historical data, Tonga estimated a cost function for total S&A expenses as Y=60,000+2X.

July August Sept. Oct.Budgeted sales in units 40,000 50,000 70,000 35,000

Q: (1) what is the budgeted cost of ending F.G. inventory in August? (2) what is the budgeted cost of goods sold in August? (3) what is the budgeted total S&A expenses in August? (4) what is the budgeted net operating income in August?

Practice Problem

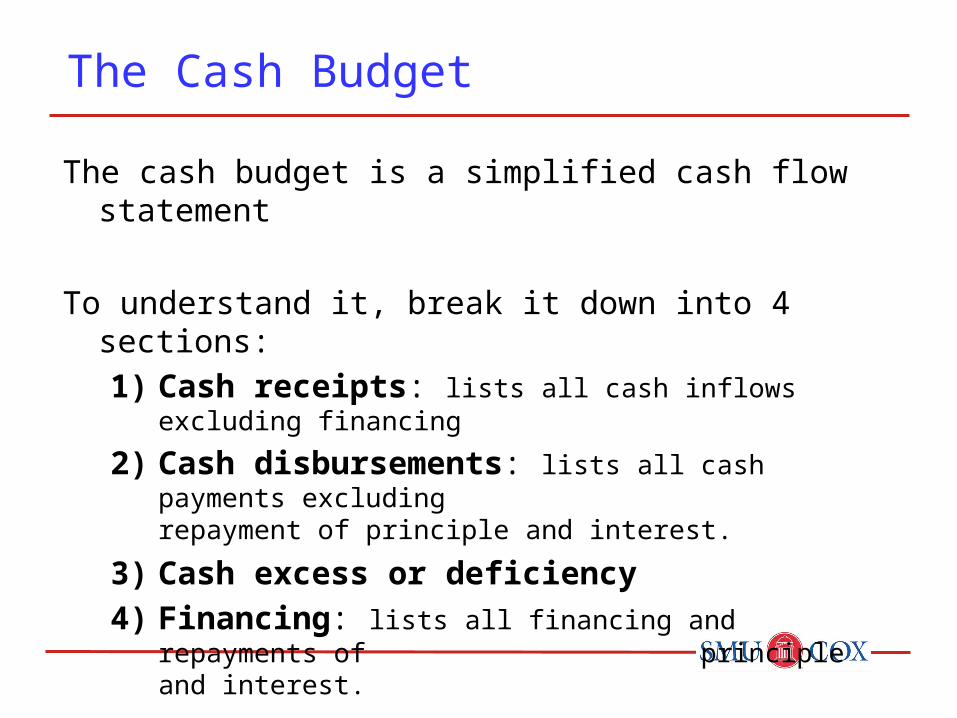

The cash budget is a simplified cash flow statement

To understand it, break it down into 4 sections:

1) Cash receipts: lists all cash inflows excluding financing

2) Cash disbursements: lists all cash payments excluding repayment of principle and

interest.

3) Cash excess or deficiency

4) Financing: lists all financing and repayments of principle and interest.

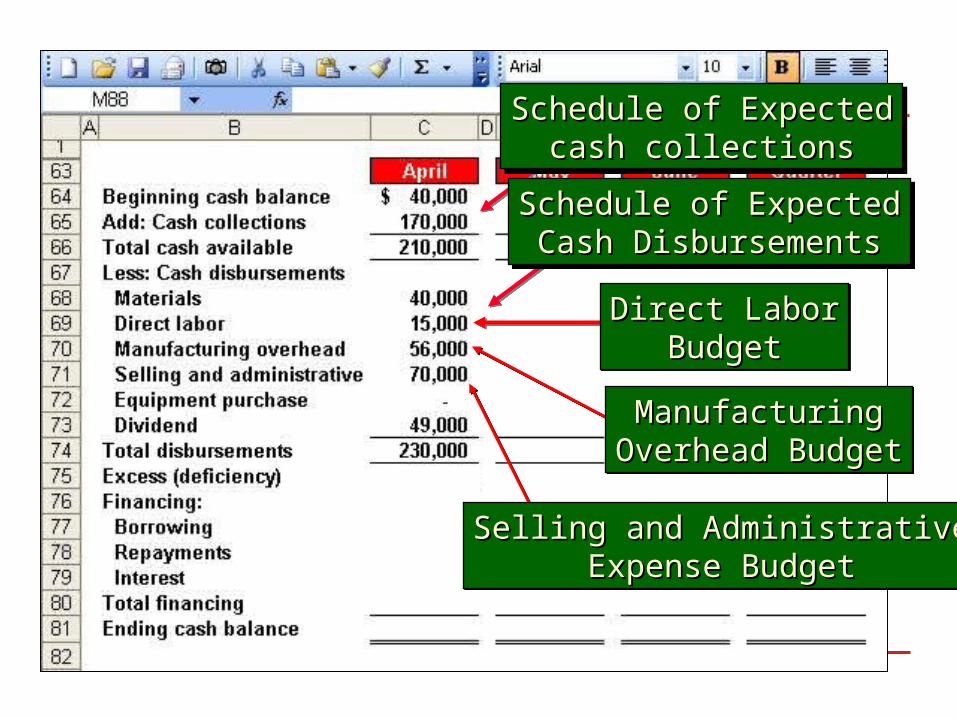

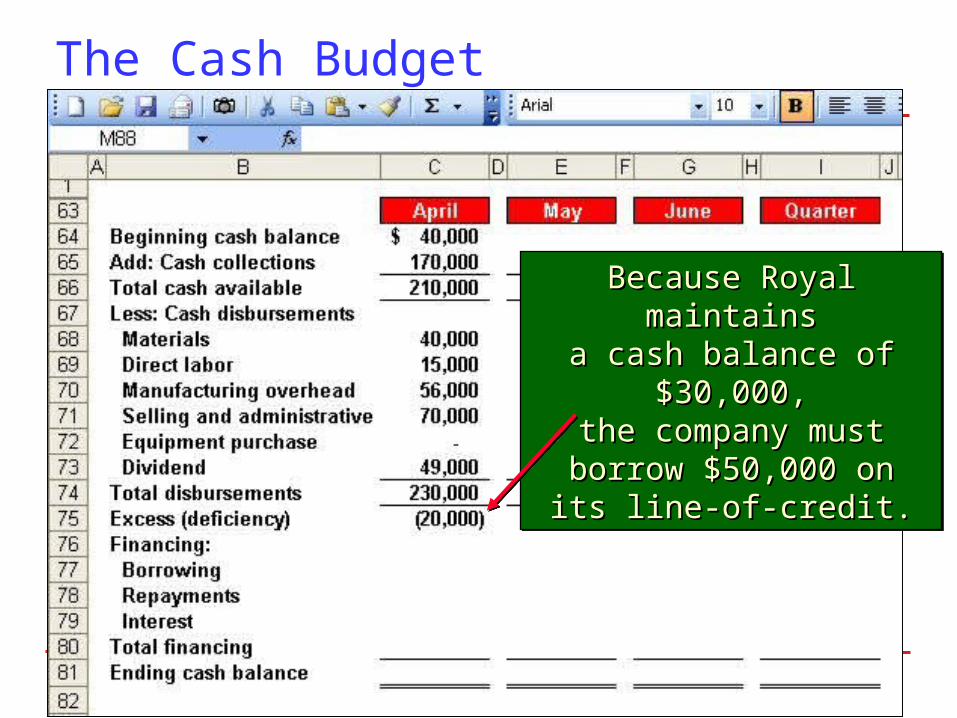

The Cash Budget

Example: Cash Budget

Royal Inc.: Has an April 1 cash balance of $40,000 Pays a cash dividend of $49,000 in April Maintains a minimum cash balance of $30,000 Maintains a 16% open line of credit for $75,000 Borrows on the first day of the month and repays loans on the

last day of the quarter (assume interest is not compounded for simplicity).

Purchases $143,700 of equipment in May and $48,300 in June (both purchases paid in cash)

Direct LaborDirect LaborBudgetBudget

Direct LaborDirect LaborBudgetBudget

ManufacturingManufacturingOverhead BudgetOverhead Budget

ManufacturingManufacturingOverhead BudgetOverhead Budget

Selling and AdministrativeSelling and AdministrativeExpense BudgetExpense Budget

Selling and AdministrativeSelling and AdministrativeExpense BudgetExpense Budget

Schedule of ExpectedSchedule of Expectedcash collectionscash collections

Schedule of ExpectedSchedule of Expectedcash collectionscash collections

Schedule of ExpectedSchedule of ExpectedCash DisbursementsCash Disbursements

Schedule of ExpectedSchedule of ExpectedCash DisbursementsCash Disbursements

The Cash Budget

Because Royal Because Royal maintainsmaintains

a cash balance of a cash balance of $30,000,$30,000,

the company must the company must borrow $50,000 on its borrow $50,000 on its

line-of-credit.line-of-credit.

Because Royal Because Royal maintainsmaintains

a cash balance of a cash balance of $30,000,$30,000,

the company must the company must borrow $50,000 on its borrow $50,000 on its

line-of-credit.line-of-credit.

The Cash Budget

$50,000 × 16% × 3/12 = $50,000 × 16% × 3/12 = $2,000$2,000

Borrowings on April 1 andBorrowings on April 1 andrepayment on June 30.repayment on June 30.

$50,000 × 16% × 3/12 = $50,000 × 16% × 3/12 = $2,000$2,000

Borrowings on April 1 andBorrowings on April 1 andrepayment on June 30.repayment on June 30.

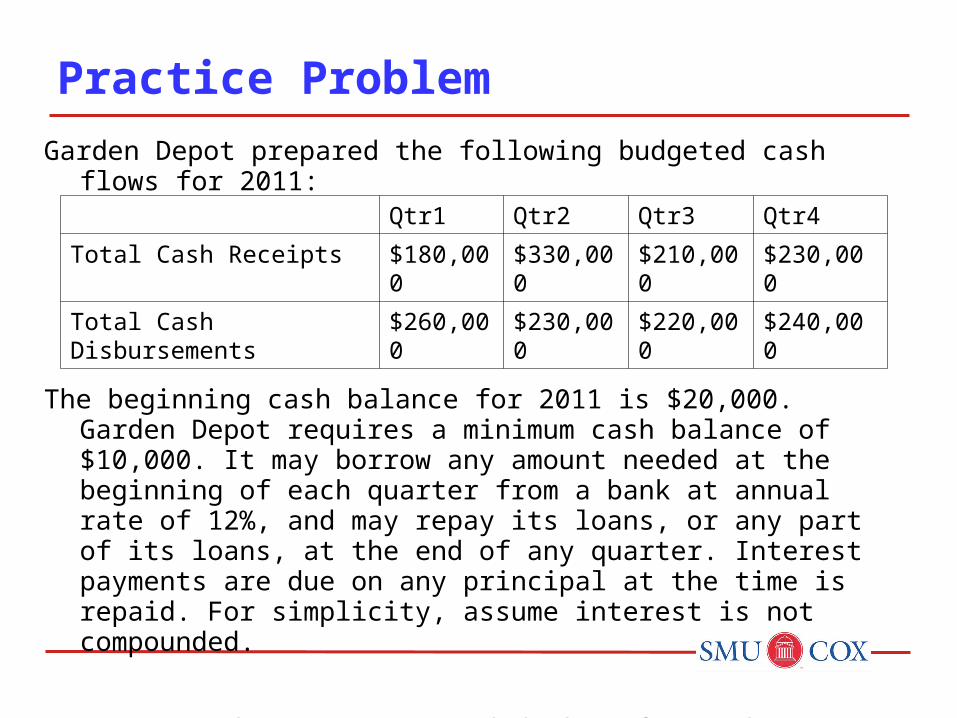

Garden Depot prepared the following budgeted cash flows for 2011:

The beginning cash balance for 2011 is $20,000. Garden Depot requires a minimum cash balance of $10,000. It may borrow any amount needed at the beginning of each quarter from a bank at annual rate of 12%, and may repay its loans, or any part of its loans, at the end of any quarter. Interest payments are due on any principal at the time is repaid. For simplicity, assume interest is not compounded.

Q: Prepare the company’s cash budget for each quarter & year 2011.

Practice Problem

Qtr1 Qtr2 Qtr3 Qtr4

Total Cash Receipts $180,000 $330,000 $210,000 $230,000

Total Cash Disbursements $260,000 $230,000 $220,000 $240,000

Shilow Co. maintains a minimum cash balance of at least $4,000 at the end of each month and can draw down a credit line of $20,000 at annual interest rate of 12% (assume interest is not compounded for simplicity). The budgeted cash balance on August 1, 2011 is $8,000. The cash budget for 2011 shows expected cash receipts of $56,000 and expected cash disbursements of $65,000 for August.

Q: (1) Will Shilow Co. have a cash excess or deficiency in August?

(2) Assume Shilow Co. expects the cash shortage in August and plans to draw down the minimum required fund on August 1, 2011 from the credit line and pay back the principle and interest on December 31, 2011. What is the budgeted interest expense?

Practice Problem

Royal CompanyBudgeted Balance Sheet

June 30

Current assets Cash 43,000$ Accounts receivable 75,000 Raw materials inventory 4,600 Finished goods inventory 24,950 Total current assets 147,550 Property and equipment Land 50,000 Equipment 367,000 Total property and equipment 417,000 Total assets 564,550$

Accounts payable 28,400$ Common stock 200,000 Retained earnings 336,150 Total liabilities and equities 564,550$

DM budgetDM budgetDM budgetDM budget

Ending FG Ending FG InventoryInventoryBudgetBudget

Ending FG Ending FG InventoryInventoryBudgetBudget

Schedule of Schedule of Cash paymentsCash paymentsSchedule of Schedule of

Cash paymentsCash payments

Schedule of cashSchedule of cashcollectionscollections

Schedule of cashSchedule of cashcollectionscollections

Example: Budgeted Balance Sheet

Cash BudgetCash BudgetCash BudgetCash Budget

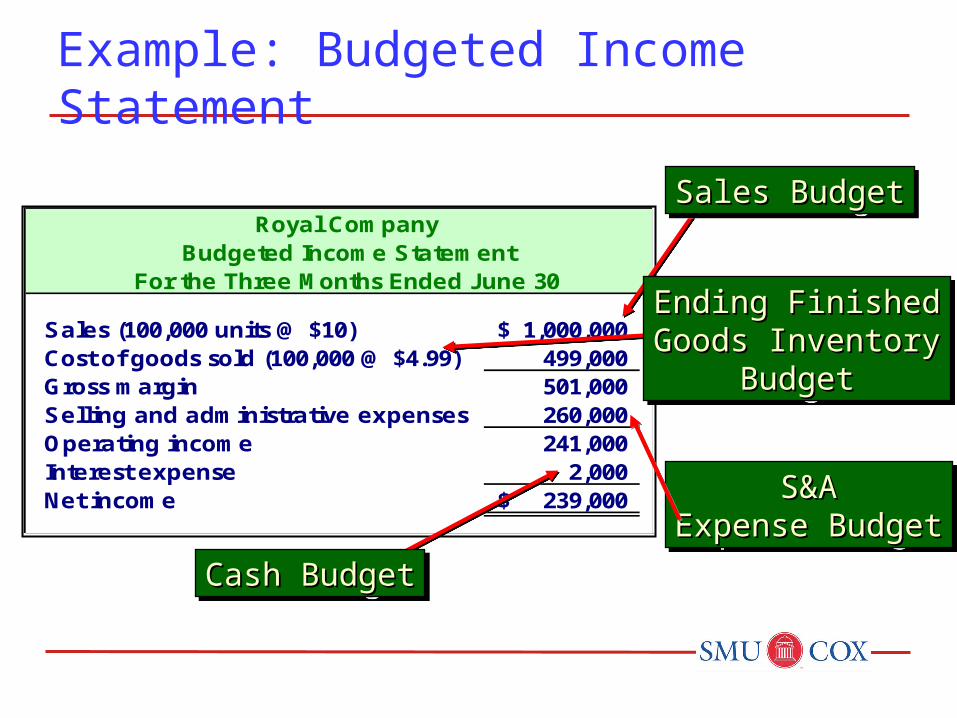

Example: Budgeted Income Statement

Royal CompanyBudgeted Income Statement

For the Three Months Ended June 30

Sales (100,000 units @ $10) 1,000,000$ Cost of goods sold (100,000 @ $4.99) 499,000 Gross margin 501,000 Selling and administrative expenses 260,000 Operating income 241,000 Interest expense 2,000 Net income 239,000$

Sales BudgetSales BudgetSales BudgetSales Budget

Ending FinishedEnding FinishedGoods InventoryGoods Inventory

BudgetBudget

Ending FinishedEnding FinishedGoods InventoryGoods Inventory

BudgetBudget

S&AS&AExpense BudgetExpense Budget

S&AS&AExpense BudgetExpense Budget

Cash BudgetCash BudgetCash BudgetCash Budget

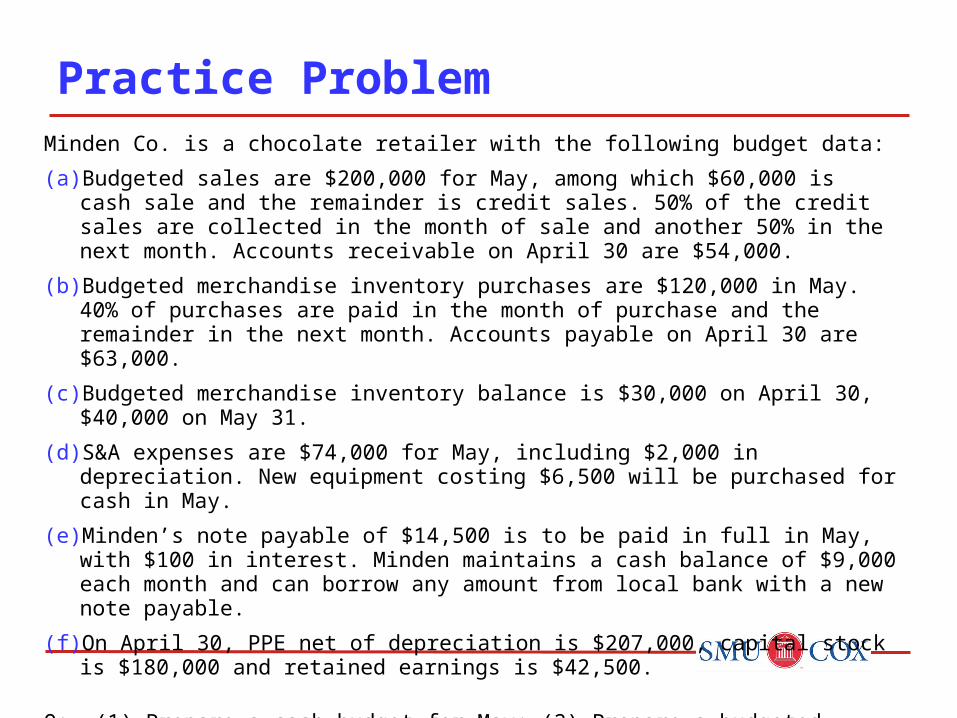

Minden Co. is a chocolate retailer with the following budget data:

(a) Budgeted sales are $200,000 for May, among which $60,000 is cash sale and the remainder is credit sales. 50% of the credit sales are collected in the month of sale and another 50% in the next month. Accounts receivable on April 30 are $54,000.

(b) Budgeted merchandise inventory purchases are $120,000 in May. 40% of purchases are paid in the month of purchase and the remainder in the next month. Accounts payable on April 30 are $63,000.

(c) Budgeted merchandise inventory balance is $30,000 on April 30, $40,000 on May 31.

(d) S&A expenses are $74,000 for May, including $2,000 in depreciation. New equipment costing $6,500 will be purchased for cash in May.

(e) Minden’s note payable of $14,500 is to be paid in full in May, with $100 in interest. Minden maintains a cash balance of $9,000 each month and can borrow any amount from local bank with a new note payable.

(f) On April 30, PPE net of depreciation is $207,000, capital stock is $180,000 and retained earnings is $42,500.

Q: (1) Prepare a cash budget for May; (2) Prepare a budgeted income statement for May;

(3) Prepare a budgeted balance sheet as of May 31.

Practice Problem

Chapter 10: Flexible Budget

The master budgets discussed in Chapter 9 could also be called STATIC budgets because they are prepared based on a fixed level of future activity.

A static budget is suitable for planning, but is inadequate for evaluating cost control.

Static Budget and Performance Analysis

Static budgets are prepared for

a single, planned level of activity.

Performance evaluation is difficult when actual activity

level differs from the planned activity level.

Hmm! Comparingstatic budgets withactual costs is likecomparing apples

and oranges.

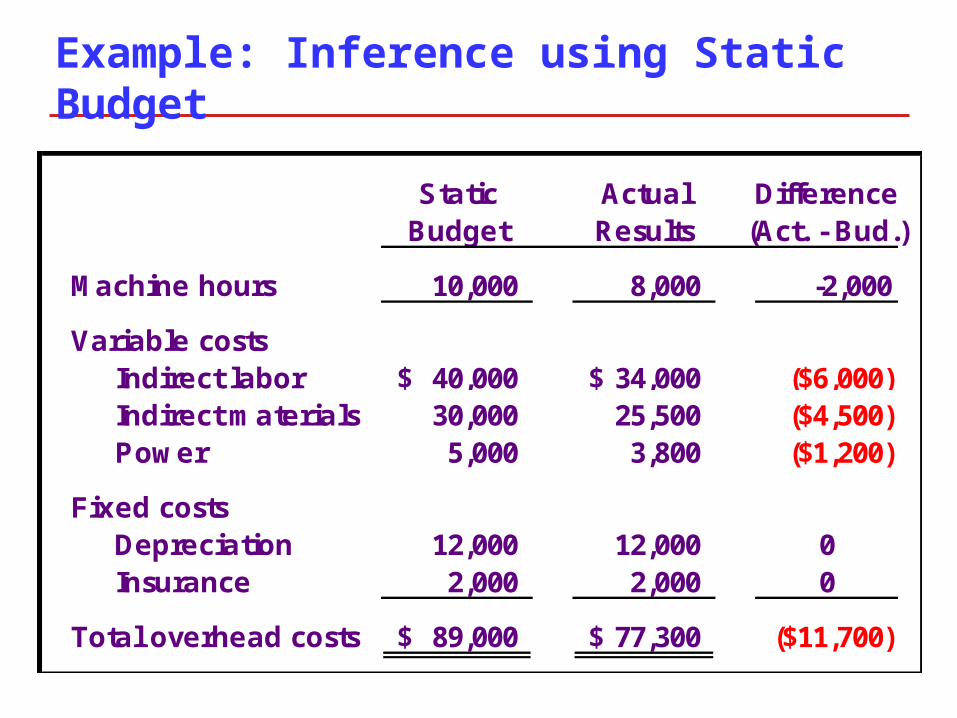

Static Actual DifferenceBudget Results (Act. - Bud.)

Machine hours 10,000 8,000 -2,000

Variable costs Indirect labor 40,000$ 34,000$ ($6,000) Indirect materials 30,000 25,500 ($4,500) Power 5,000 3,800 ($1,200)

Fixed costs Depreciation 12,000 12,000 0 Insurance 2,000 2,000 0

Total overhead costs 89,000$ 77,300$ ($11,700)

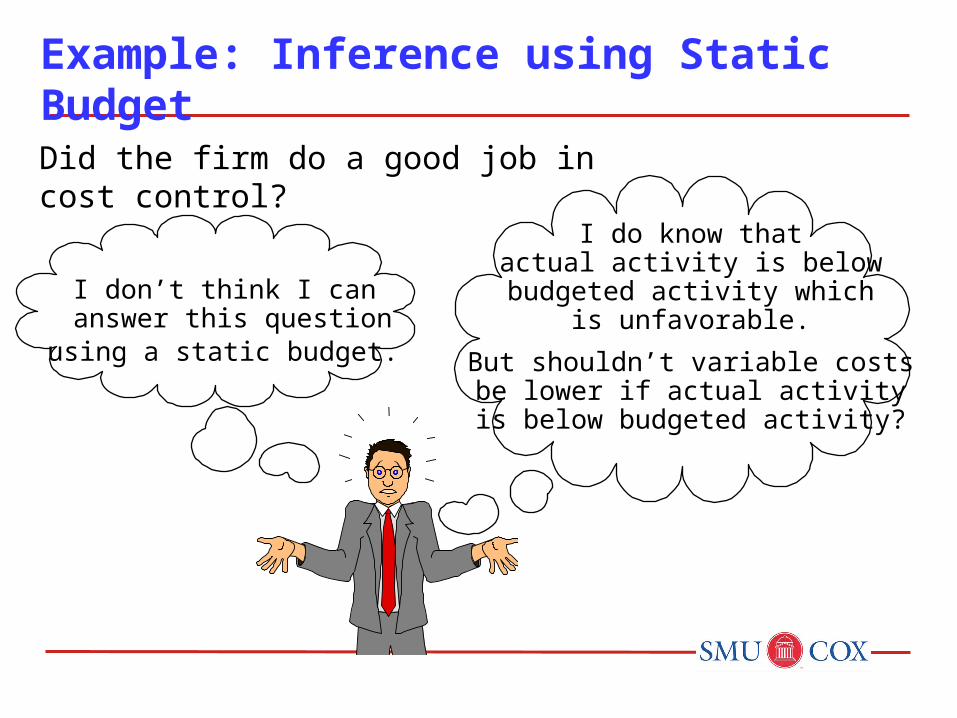

Example: Inference using Static Budget

I don’t think I can answer this question

using a static budget.

I do know thatactual activity is belowbudgeted activity which

is unfavorable.

But shouldn’t variable costsbe lower if actual activity

is below budgeted activity?

Did the firm do a good job in cost control?

Example: Inference using Static Budget

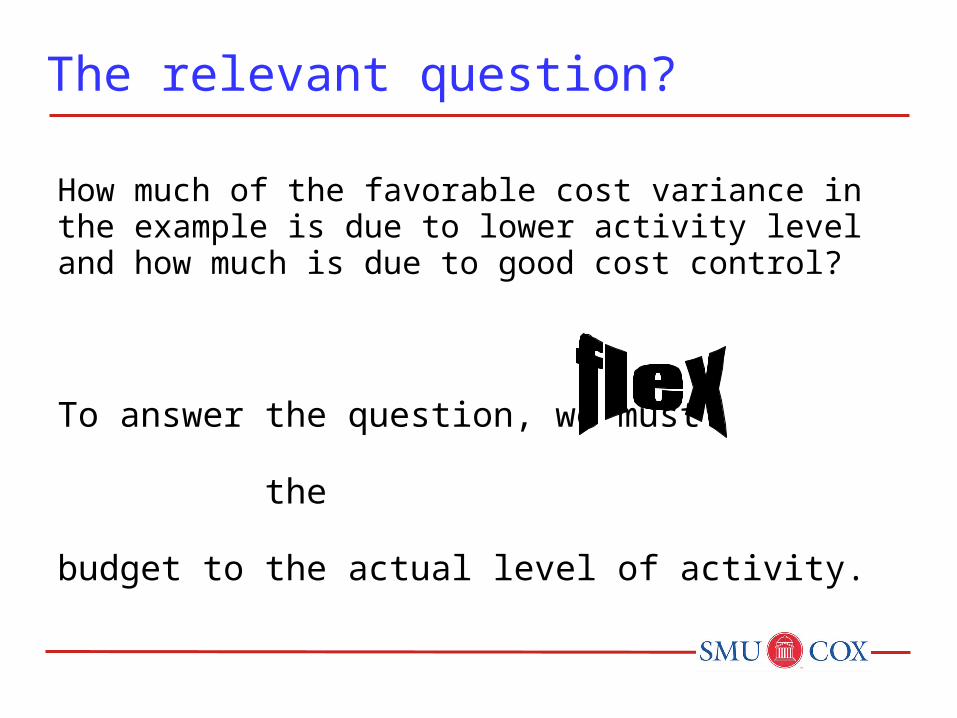

How much of the favorable cost variance in the example is due to lower activity level and how much is due to good cost control?

To answer the question, we must the

budget to the actual level of activity.

The relevant question?

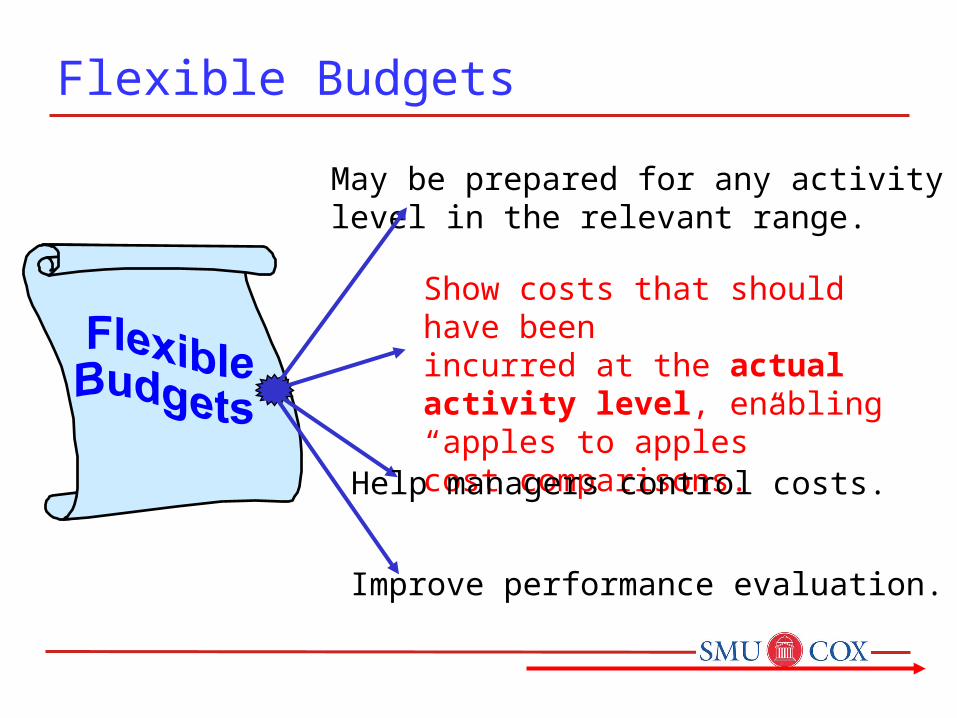

Flexible Budgets

Improve performance evaluation.

May be prepared for any activity level in the relevant range.

Show costs that should have beenincurred at the actual activity level, enabling “apples to apples”cost comparisons.Help managers control costs.

For Next Class

Finish chapter 10. Attempt the assigned HW problem.

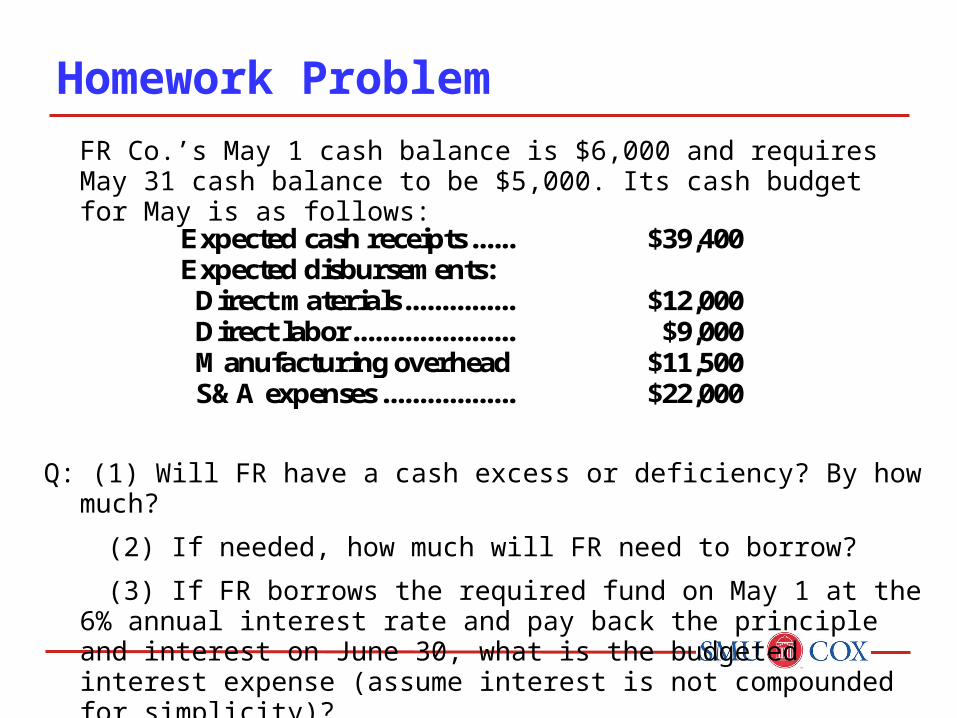

FR Co.’s May 1 cash balance is $6,000 and requires May 31 cash balance to be $5,000. Its cash budget for May is as follows:

Q: (1) Will FR have a cash excess or deficiency? By how much?

(2) If needed, how much will FR need to borrow?

(3) If FR borrows the required fund on May 1 at the 6% annual interest rate and pay back the principle and interest on June 30, what is the budgeted interest expense (assume interest is not compounded for simplicity)?

Homework Problem

Expected cash receipts ...... $39,400 Expected disbursements:

Direct materials ............... $12,000 Direct labor ...................... $9,000 Manufacturing overhead $11,500 S&A expenses .................. $22,000