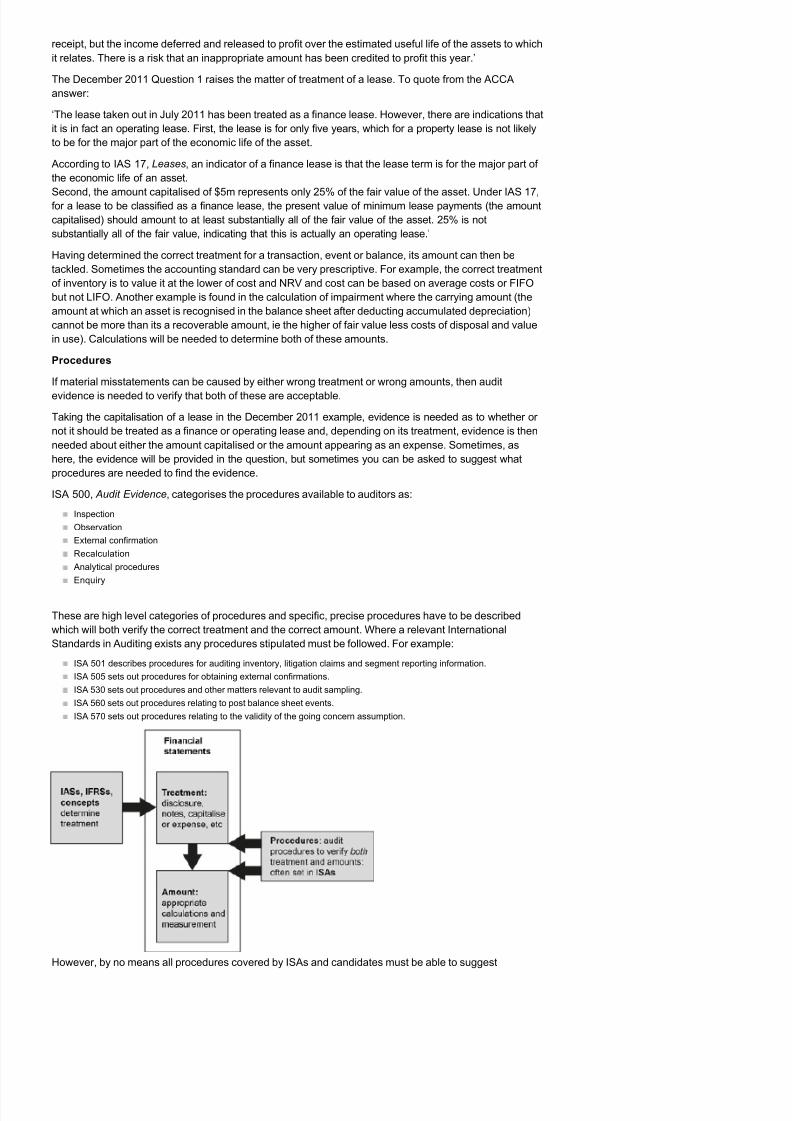

Home >Students >Exam resources >Professional level >P7 Advanced Audit and Assurance>Technical articles ACCOUNTING ISSUES My ACCA Search RELATED LINKS Student Accountant hub page TAP into Paper P7 A very common theme in Paper P7 questions is to pr esent you with information that embodies an accounting issue. Sometimes the information is presented as a standalone requirement but is often, forexample, included in a set of notes of a conversation with an audit client’s finance director. For example: December 2012 Question 1 contains: Work has recently started on a new production line which will ensure that Grohl Co meets new regulatory requirements prohibiting the use of certain chemicals, which come into force in March 2013. In July 2012, a loan of $30m with an interest rate of 4% was negotiated with Grohl Co’s bank, the main purpose of the loan being to fund the capital expenditure necessary for the new production line. June 2012 Question 1 contains: Starling Co received a grant of $35mon 1 March 2012in relation to redevelopment of its main manufacturing site. The government is providing grants to companies for capital expenditure on environmentally friendly assets. Starling Co has spent $25m of the amount received on solar panels which generate electricity, and intends to spend the remaining $10m on upgrading its production and packaging lines. December 2011 Question 1 contains: On 1 July 2011, Oak Co entered into a lease which has been accounted for as a finance lease and capitalised at $5m. The leased property is used as the head office for Oak Co’s new website development and sales division. The lease term is for five years and the fair value of the property at the inception of the lease was $20m. Typically the question requirements will then be something along the lines of: Evaluate the business risks faced by X Co. Identify and explain the risks of material misstatement to be considered in planning the audit of X Co. In respect of the risks of material misstatement, suggest suitable audit procedures. Business risks Remember that when you are describing business risks, you should say nothing about potential misstatements in the financial statements. Business risks exist quite independently of the financial statements and they do not depend on audit procedures. Business risk is where the directors make wrong decisions or where events have occurred which threaten the business’s future. Business risks are often classified as: Strategic risks (for example, investing in out-of date technology). Operational risks (for example, manufacturing products which have faults). Regulatory risks (for example, the fines and damages that might be payable as a consequence of breaching health and safety regulations). Financial risks (for example, an inability to pay interest or rent because of poor cash flow). Although drafting financial statements does not affect the business risks, understanding the business risks can give insights into where the financial statements might contain material misstatements. For example, investing in out-of date technology could cause going concern problems and queries about the The global body for professional accountants About us Contact us Wor k for us Technical acti vi ti es Hel p & support Pakistan