accounting for paralegals. the fees journal kept track of all fees billed to clients a purchase...

TRANSCRIPT

Accounting For Paralegals

The fees journal kept track of all fees billed to clients

A purchase journal recorded all purchased products

A payroll journal recorded all amounts paid to employees

A general journal was used for records of an infrequent nature

A summary of all the records were sorted into different accounts in one big book called a general ledger

Bookkeepers used records called JOURNALS and LEDGERS

Fees journal

Cash Book

Separate books were used for different types of records

Most businesses now use computers

• In today's modern times, a business has the choice of using computers instead of manual books

• They save significant amounts of time• Save costs• Very efficient• Garbage in = garbage out• It is therefore important for you to first

understand how the accounting function works using manual records

A paralegal practice must maintain two separate sets of accounts:

1. those of the practice

2. trust accounts

Transferring funds between the two is tightly controlled under By-Law 9

Failing to comply with the laws pertaining to the maintenance of trust accounts can result in losing your license to practice

Two sets of accounts

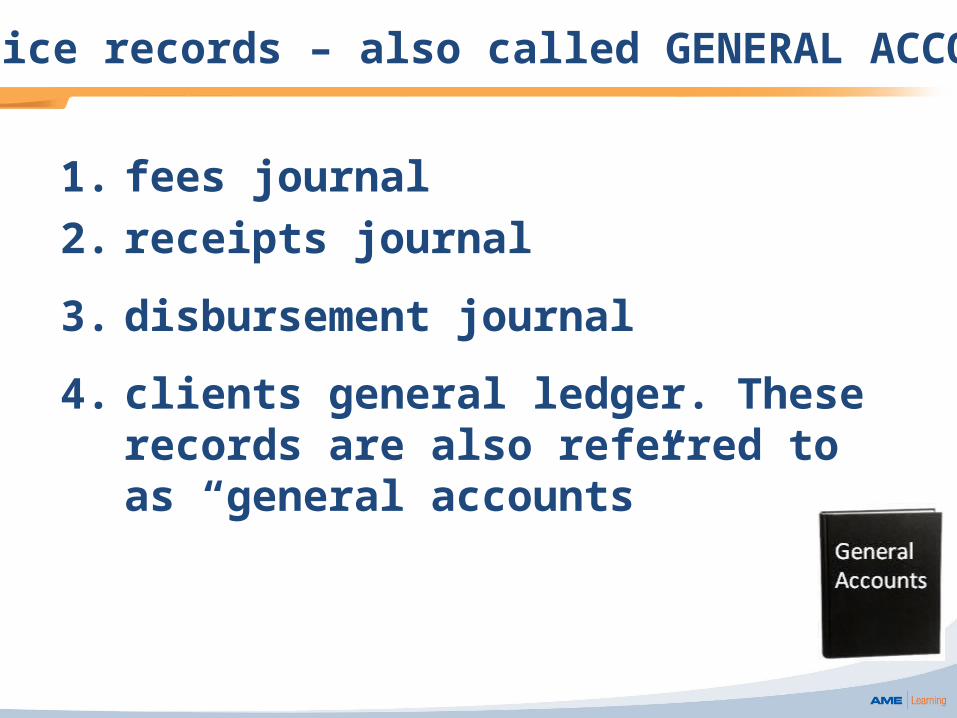

1. fees journal 2. receipts journal

3. disbursement journal

4. clients general ledger. These records are also referred to as “general accounts”

Practice records – also called GENERAL ACCOUNTS

Ref # Date Invoice # Client Fees billedDisbursements

billed GST billed Total amount billed

Carol HiltebeitelFEES JOURNAL

The FEES journal records all service fees and disbursements

Ref # DateReceived from

(source of funds) Amount Method of payment & details

Carol HiltebeitelGENERAL RECEIPTS JOURNAL – PRACTICE ACCOUNT

The RECEIPTS journal records all amounts received into the practice e.g. fees paid directly from clients, money received from the trust, loans received etc.

The DISBURSEMENT journal records all amounts paid from the practice e.g. rent, wages, insurance fees, client refunds etc.

Ref. # Date Paid to Use of funds Amount Method of payment & details

Carol HiltebeitelParalegal

GENERAL DISBURSEMENTS JOURNAL – PRACTICE ACCOUNT

Ref. # Date Particulars Invoice #

Fees & disburesments

billed

Payments from client

(including tax)Balance owed

by client

Ref. # Date Particulars Invoice #

Fees & disbursements

billed

Payments from client

(including tax)Balance owed

by client

Account: NAME OF CLIENT

Carol HiltebeitelCLIENT GENERAL LEDGER – PRACTICE ACCOUNT

Account: NAME OF CLIENT

The CLIENTS ledger account maintains all the amounts billed and paid in a separate record for each client and keeps track of amounts owing. This is an important control but not required under By-Law 9

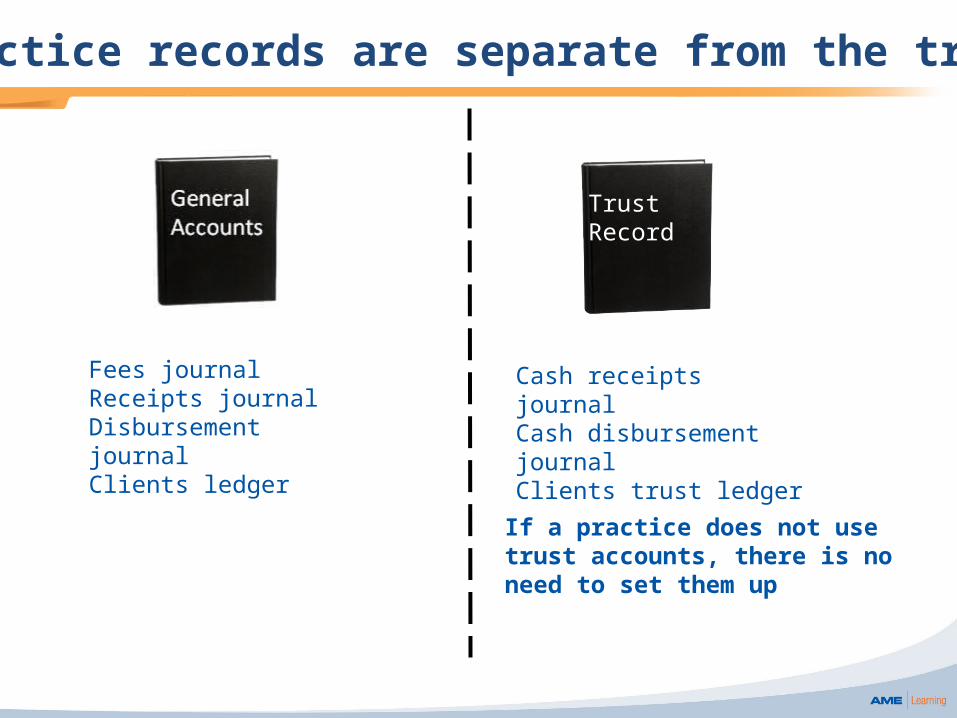

Practice records are separate from the trust

TrustRecord

Fees journalReceipts journalDisbursement journalClients ledger

Cash receipts journalCash disbursement journalClients trust ledger

If a practice does not use trust accounts, there is no need to set them up

1. for funds that belong to a client

2. to be paid to another party on behalf of a client

3. by the practice for future legal fees and disbursements still be billed

4. as directed by your client

5. for expenses to be reimbursed to your practice by the client

The funds of a trust account are used:

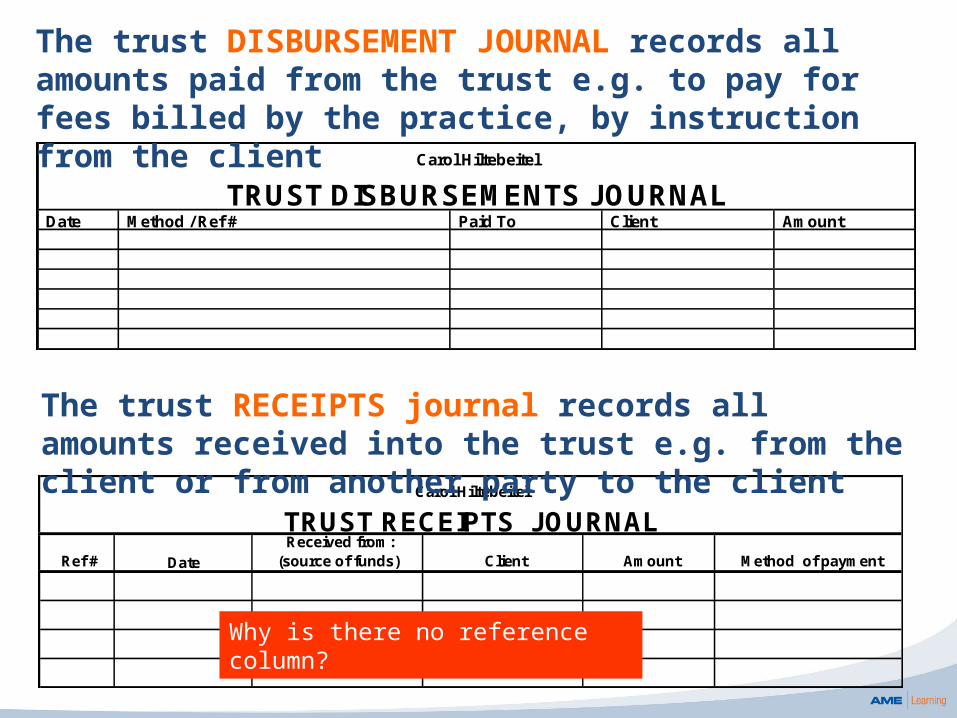

Date Paid To Client Amount

Carol Hiltebeitel

TRUST DISBURSEMENTS JOURNALMethod / Ref #

Ref # Date Received from:

(source of funds) Client Amount Method of payment

TRUST RECEIPTS JOURNALCarol Hiltebeitel

Why is there no reference column?

The trust DISBURSEMENT JOURNAL records all amounts paid from the trust e.g. to pay for fees billed by the practice, by instruction from the client

The trust RECEIPTS journal records all amounts received into the trust e.g. from the client or from another party to the client

Ref. # Date Particulars Receipts

Disbursements Balance in

account

Ref. # Date Particulars Receipts Disbursments Balance in

account

Account: CLIENT NAME

Carol HiltebeitelParalegal

CLIENT TRUST LEDGER

Account: CLIENT NAME

The trust MIXED TRUST records each individuals records relating to all amounts received and disbursed and the amount left in the trust. All interest received and bank fees are not recorded in the mixed trust. (There is no way accurate way of allocating them to each account)

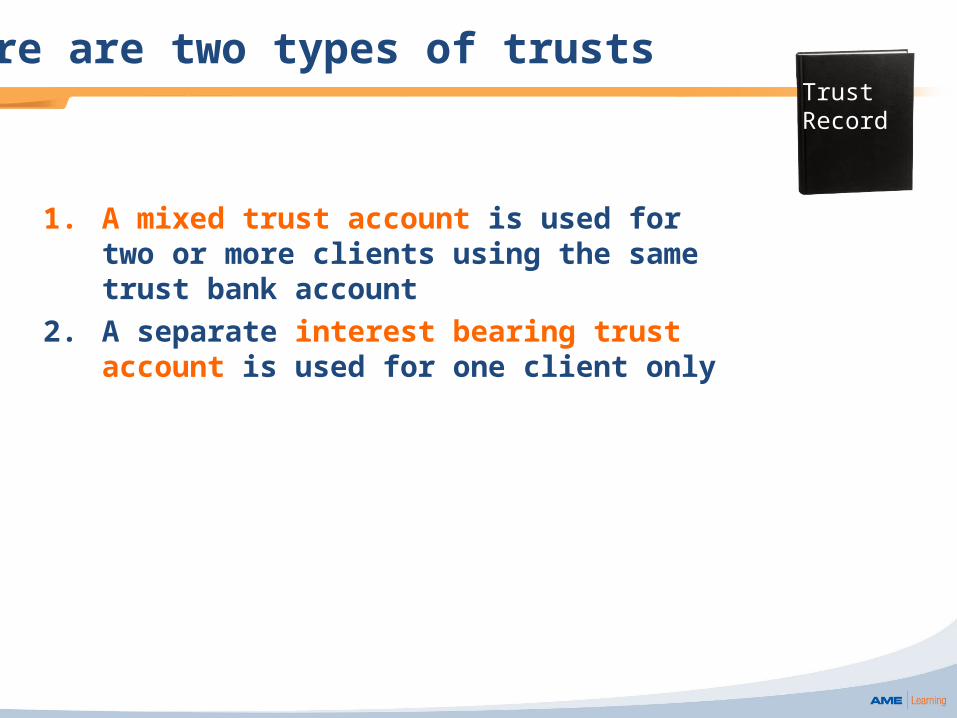

1. A mixed trust account is used for two or more clients using the same trust bank account

2. A separate interest bearing trust account is used for one client only

There are two types of trustsTrustRecord

a) The mixed account may not receive any interest earned. Interest must be paid directly to the Law Foundation

b) The mixed account may not pay any bank fees – these are paid directly by the practice

c) An interest bearing account may receive interest and pay bank charges. A surplus must be paid to the client or by way of their instruction

Trust records

The primary difference between the two accounts are:

The sequence in which records are maintained is CRUCIAL