accounting bellwork 3 rd hour: what goes in the post reference column of the following: 1.general...

TRANSCRIPT

Accounting BellworkAccounting Bellwork

3rd Hour: What goes in the post reference column of the following:

1. General ledger

2. General journal

3. General ledger with a balance brought forward

Susan RuckerApril 19, 2023

Bellwork

1. General ledger• G for general journal and the page # of the

journal.

2. General journal• The account # of the ledger entry.

3. General ledger with a balance brought forward

• A checkmark

Section 3Preparing a Trial Balance

Section 3Preparing a Trial Balance

What You’ll Learn

The purpose of a trial balance.

How to prepare a trial balance.

How to identify and locate trial

balance errors.

What You’ll Learn

The purpose of a trial balance.

How to prepare a trial balance.

How to identify and locate trial

balance errors.

Why It’s ImportantTo present accurate financial

statements, the accounts must be in balance. The purpose of a trial balance is to prove that the general ledger is in balance.

Why It’s ImportantTo present accurate financial

statements, the accounts must be in balance. The purpose of a trial balance is to prove that the general ledger is in balance.

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

Key Terms

proving the ledger

trial balance

transposition error

Key Terms

proving the ledger

trial balance

transposition error

slide error

correcting entry

slide error

correcting entry

The Fifth Step in the Accounting Cycle: The Trial BalanceThe Fifth Step in the Accounting Cycle: The Trial Balance

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

Adding all the debit and credit balances, then comparing the two totals to see whether they are equal is call proving the ledger.

A formal way to prove that debits equal credits is to prepare a trial balance.

Prepared on two-column accounting stationery.

Account numbers are listed in the far left column.

Adding all the debit and credit balances, then comparing the two totals to see whether they are equal is call proving the ledger.

A formal way to prove that debits equal credits is to prepare a trial balance.

Prepared on two-column accounting stationery.

Account numbers are listed in the far left column.

The Fifth Step in the Accounting Cycle: The Trial Balance (con’t.)

The Fifth Step in the Accounting Cycle: The Trial Balance (con’t.)

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

Account names are listed in the

next column.

Debit balances are entered in the

first amount column.

Credit balances are entered in the

second amount column.

Account names are listed in the

next column.

Debit balances are entered in the

first amount column.

Credit balances are entered in the

second amount column.

The Fifth Step in the Accounting Cycle: The Trial Balance (con’t.)The Fifth Step in the Accounting Cycle: The Trial Balance (con’t.)

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

WhoWhat

When

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

Finding ErrorsFinding Errors

1. Add the debit and credit columns again. There may be an adding error.

2. If the difference between columns is 10, 100, or 1000 and so on, you probably made an addition error.

3. If the amount you are out of balance is evenly divisible by 9, you may have a transposition error or a slide error.

1. Add the debit and credit columns again. There may be an adding error.

2. If the difference between columns is 10, 100, or 1000 and so on, you probably made an addition error.

3. If the amount you are out of balance is evenly divisible by 9, you may have a transposition error or a slide error.

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

Finding Errors cont.Finding Errors cont.

Transposition Error:

Occurs when two digits within an amount are accidentally reversed, or transposed.

ie. The amount $325 may have been written as $352.

Transposition Error:

Occurs when two digits within an amount are accidentally reversed, or transposed.

ie. The amount $325 may have been written as $352.

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

Finding Errors cont.Finding Errors cont.

Slide Error:

Occurs when a decimal point is moved by mistake.

ie. The amount $1800 is written as $180 or $18,000.

Slide Error:

Occurs when a decimal point is moved by mistake.

ie. The amount $1800 is written as $180 or $18,000.

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

Correcting EntriesCorrecting Entries

There are three types of errors:

1. Error in a journal entry that is not posted.

2. Error in posting to the ledger when the journal entry is correct.

3. Error in a journal entry that is posted.

There are three types of errors:

1. Error in a journal entry that is not posted.

2. Error in posting to the ledger when the journal entry is correct.

3. Error in a journal entry that is posted.

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

When an error in a journal entry is

discovered after posting, make a

correcting entry to fix the error.

When an error in a journal entry is

discovered after posting, make a

correcting entry to fix the error.

Correcting Entries cont.Correcting Entries cont.

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)

Finding Errors cont.Finding Errors cont.

4. Make sure that you have included all of the general ledger accounts in the trial balance.

5. Make sure the amounts are recorded in the correct column.

6. You may have an error in the ledger.

7. Check the general ledger to verify the correct amounts are posted from the journal entries.

4. Make sure that you have included all of the general ledger accounts in the trial balance.

5. Make sure the amounts are recorded in the correct column.

6. You may have an error in the ledger.

7. Check the general ledger to verify the correct amounts are posted from the journal entries.

Demonstration Problems7-4 through 7-6

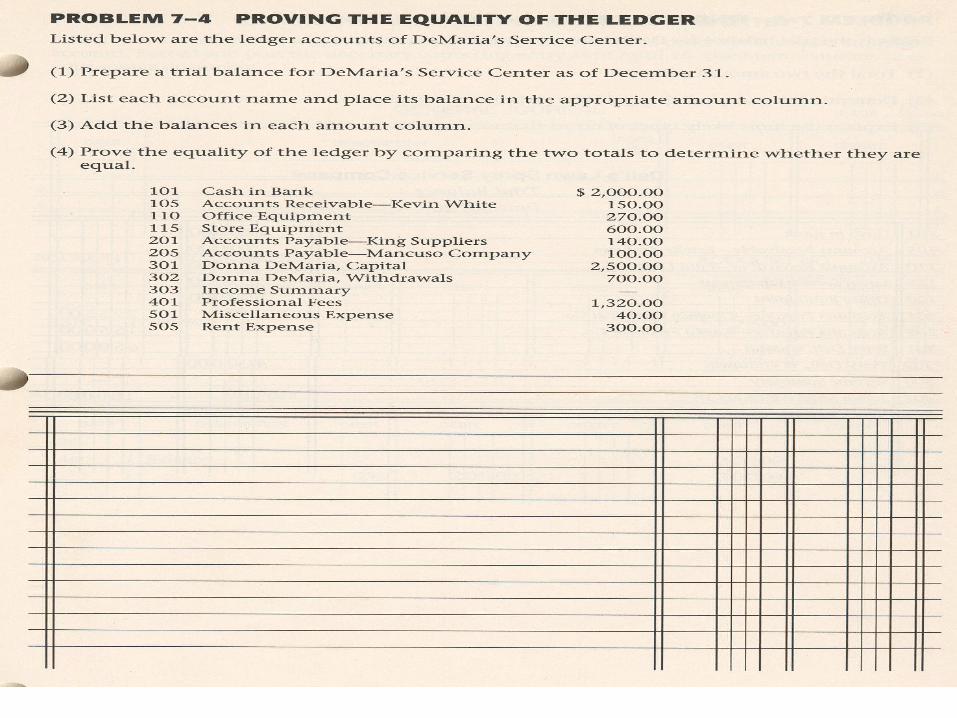

Problem 7-4

DeMaria’s Service CenterTrial Balance

December 31, 20--

101 Cash in Bank 2000--105 Accounts Receivable – Kevin White 150--110 Office Equipment 270--115 Store Equipment 600--201 Accounts Payable – King Suppliers 140--205 Accounts Payable – Mancuso Company 100--301 Donna DeMaria, Capital 2500--302 Donna DeMaria, Withdrawals 700--303 Income Summary ----401 Professional Fees 1320--501 Miscellaneous Expense 40--505 Rent Expense 300--

4060--TOTAL 4060--

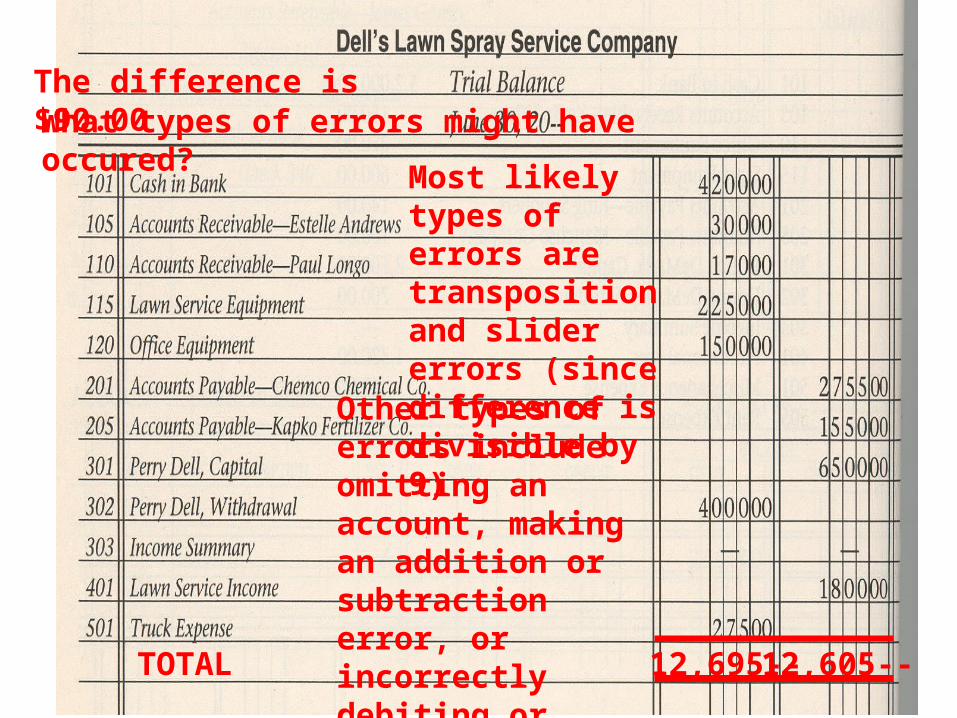

Problem 7-5

TOTAL 12,695--12,605--

The difference is $90.00What types of errors might have occured?

Most likely types of errors are transposition and slider errors (since difference is divisible by 9)

Other types of errors include omitting an account, making an addition or subtraction error, or incorrectly debiting or crediting records.

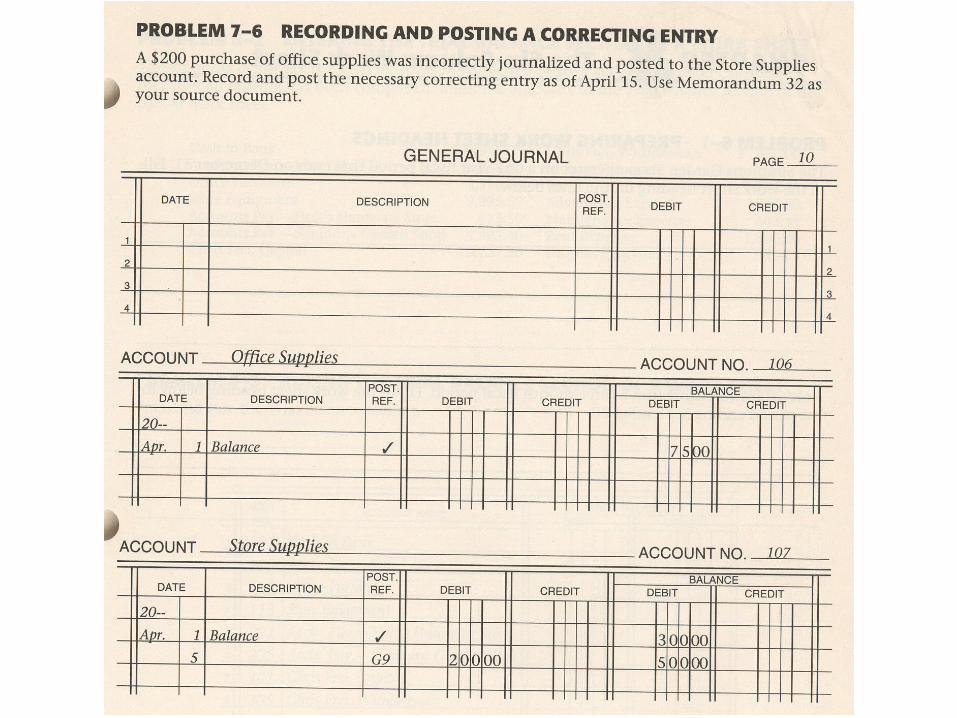

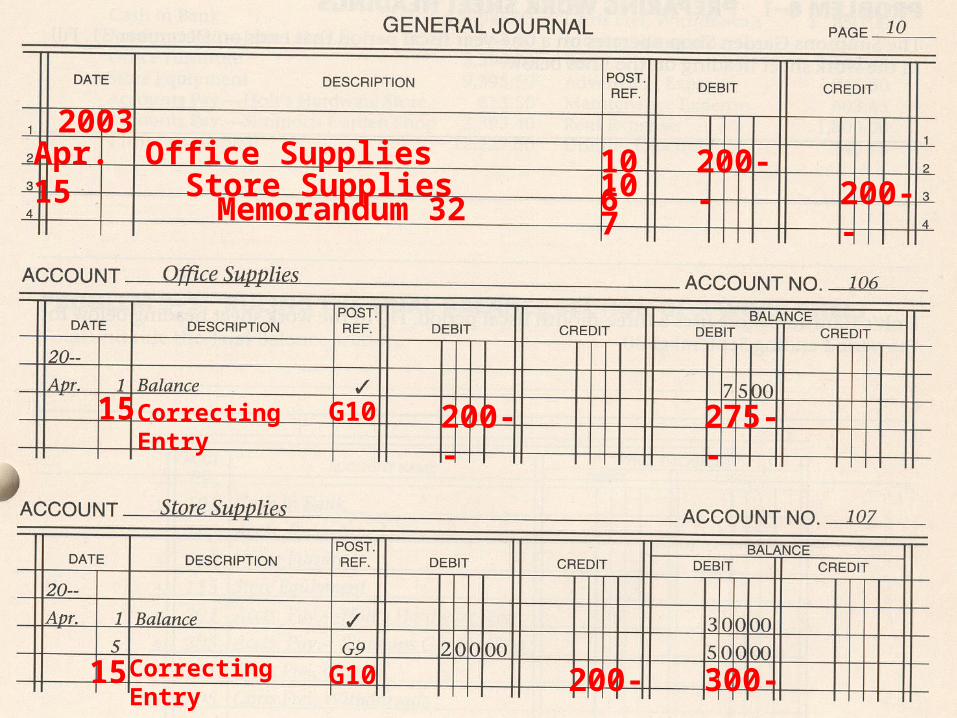

2003Apr. 15 Office Supplies 200--

Store Supplies 200--Memorandum 32

15 Correcting Entry 200--G10 275--

106

15 Correcting Entry 200--G10 300--

107

Check Your Understanding p170 Check Your Understanding p170

Thinking Critically 1&2

Problems 7-3 and 7-4

Thinking Critically 1&2

Problems 7-3 and 7-4

Section 3 Preparing a Trial Balance (con’t.)Section 3 Preparing a Trial Balance (con’t.)