accounting basics study_material_0

TRANSCRIPT

Accounting Basics

Prepared for First Year MBA

Overview

S No Particulars

01 Introduction to Accounting

02 Accounting Equation

03 Types of Transactions

04 Purchase and Sales

05 Types of Accounts

06 Golden Rules of Accounting

07 Journal ; Step by Step Procedure of Writing a Journal

08 Ledger ; Procedure for Posting a Ledger

09 Trail Balance along with illustration

10 Introduction to Trading account, P&L A/C and Balance Sheets

11 References

1. Introduction to Accounting

1.1 Definition

“The process of identifying, measuring and communicating economic information topermit informed judgment and decision by users of the information”.

‐ American Accounting Association

1.2 Objectives of Accounting

i. to maintain accounting records.ii. to calculate the result of operations.iii. to ascertain the financial position.

iv. to communicate the information to users.

1. Introduction to Accounting

1.3 Debtors ‐ Definition

A company or individual who owes money. If the debt is in the form of a loan from afinancial institution, the debtor is referred to as a borrower. If the debt is in the form ofsecurities, such as bonds, the debtor is referred to as an issuer.

Debtors can be entities, companies or people of a legal nature that owe money tosomeone else – such as your business for example.

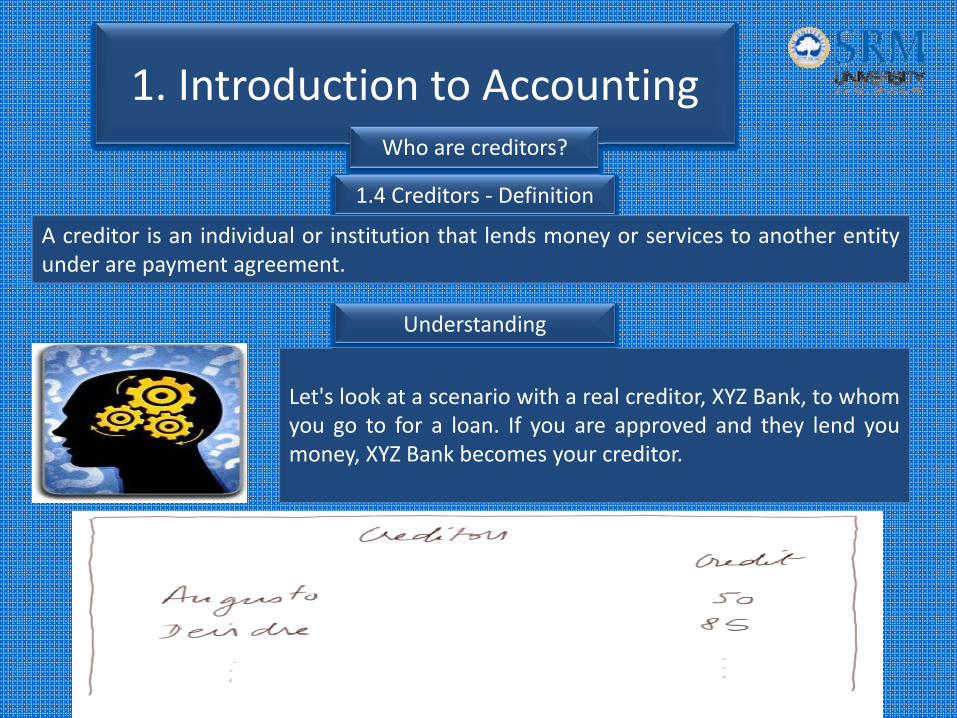

1.4 Creditors ‐ Definition

A creditor is an individual or institution that lends money or services to another entityunder are payment agreement.

1. Introduction to AccountingWho are creditors?

Let's look at a scenario with a real creditor, XYZ Bank, to whomyou go to for a loan. If you are approved and they lend youmoney, XYZ Bank becomes your creditor.

Understanding

Relationship between Debtors and Creditors

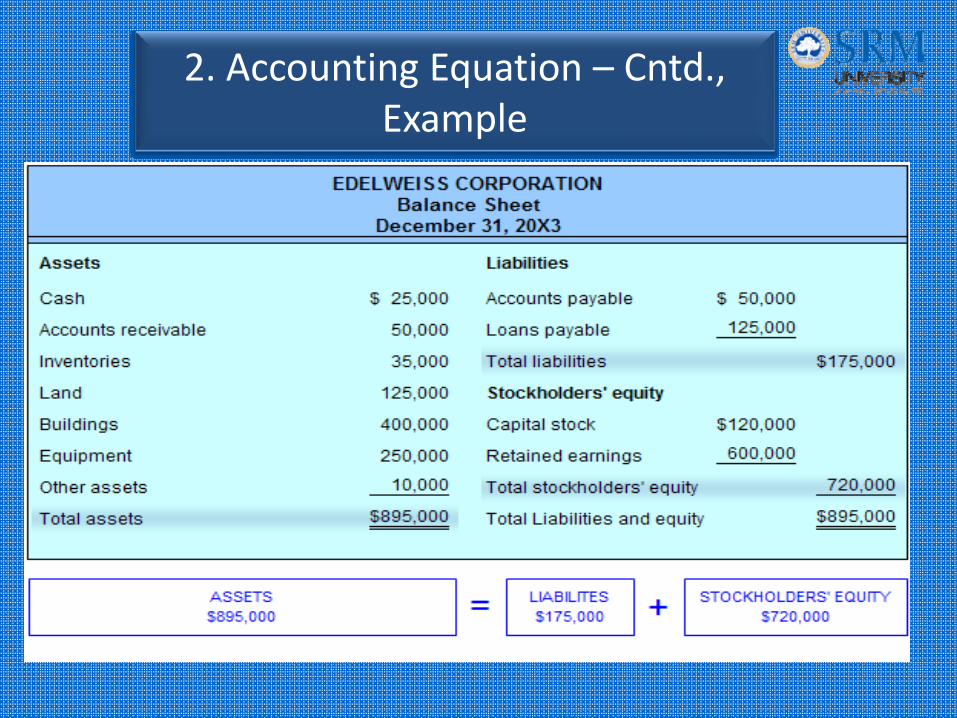

2. Accounting Equation

The financial position of a company is measured by the following items:

1. Assets (what it owns)2. Liabilities (what it owes to others)

3. Owner’s Equity (the difference between assets and liabilities)

The accounting equation (or basic accounting equation) offers us a simple way tounderstand how these three amounts relate to each other. The accounting equation fora sole proprietorship is:

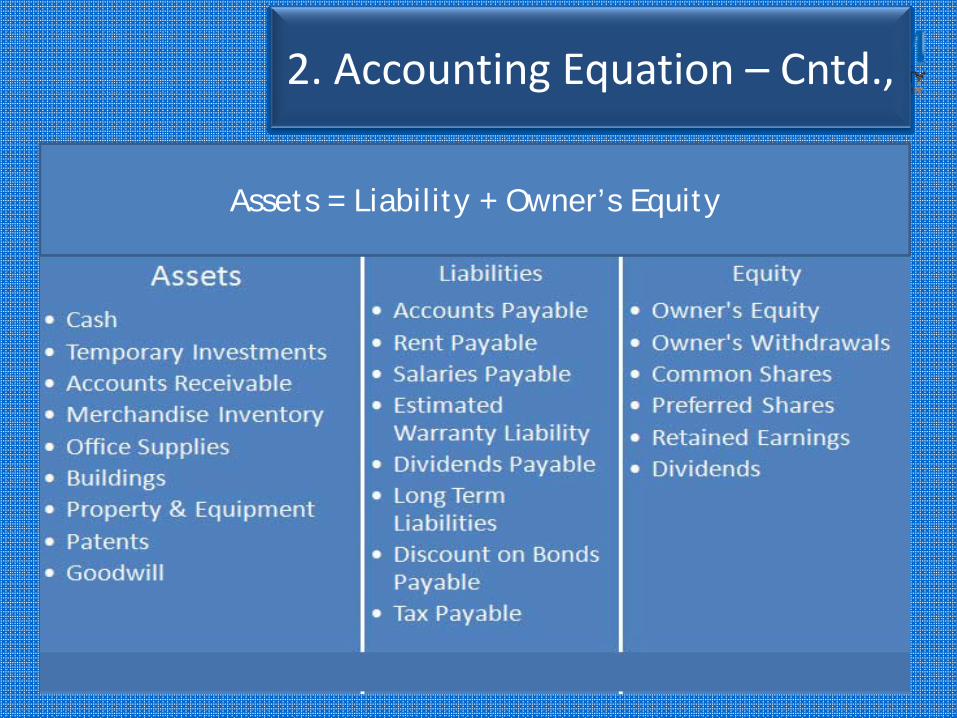

Assets = Liabilities + Owner’s Equity

Assets Liabilities Owners Equity

2. Accounting Equation

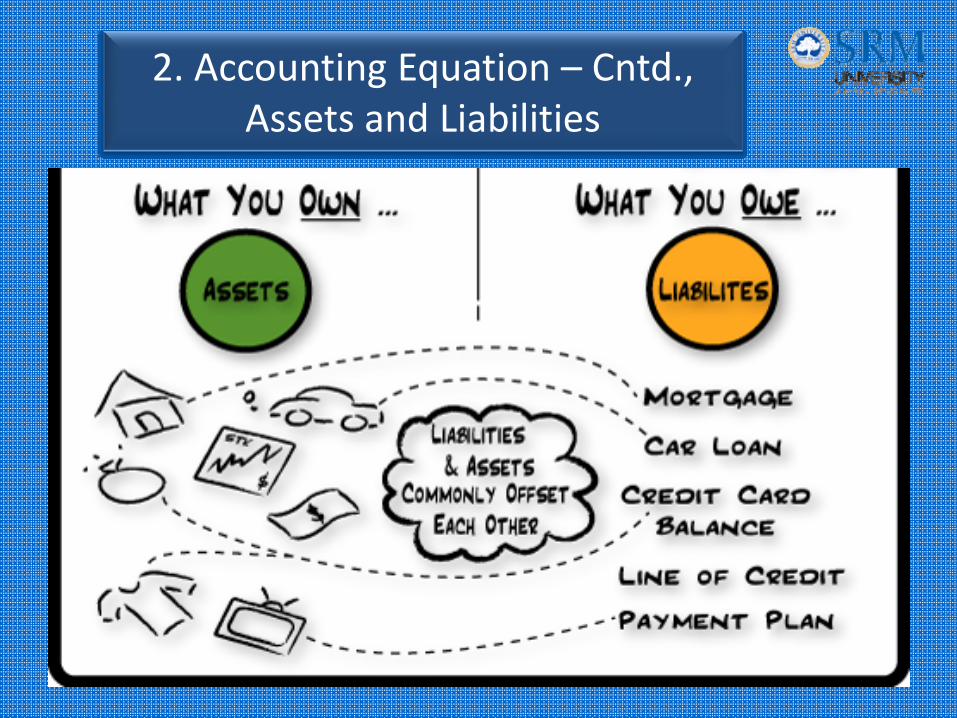

2.1 Assets : Assets are a company’s resources—things the company owns. Examples of assets include cash, accounts receivable, inventory, prepaid insurance, investments, land, buildings, equipment, and goodwill. From the accounting equation, we see that the amount of assets must equal the combined amount of liabilities plus owner’s (or stockholders’) equity.

2.2 Liability : Liabilities are a company’s obligations—amounts the company owes.Examples of liabilities include notes or loans payable, accounts payable, salaries andwages payable, interest payable, and income taxes payable (if the company is a regularcorporation). Liabilities can be viewed in two ways:

(1) as claims by creditors against the company’s assets, and(2) a source—along with owner or stockholder equity—of the company’s assets.

2.3 Owners Equity : Owner’s equity or stockholders’ equity is the amount left over after liabilities are deducted from assets:

Assets – Liabilities = Owner’s (or Stockholders’) Equity.Owner’s or stockholders’ equity also reports the amounts invested into the company bythe owners plus the cumulative net income of the company that has not beenwithdrawn or distributed to the owners.

2. Accounting Equation – Cntd.,Assets and Liabilities

2. Accounting Equation – Cntd.,Terms

2.4 Double‐entry Book Keeping System

A double‐entry bookkeeping system is a set of rules for recording financial information ina financial accounting system in which every transaction or event changes at least twodifferent nominal ledger accounts.

2.5 Credit

An accounting notation that increases liability, equity, and expense accounts. Creditsdecrease asset and expense accounts.

2.6 Debit

In bookkeeping, an entry in the left hand column of an account to record a debt. Debitsincrease asset and expense accounts. Debits decrease liability, income, and equityaccounts.

2. Accounting Equation – Cntd.,

Assets = Liability + Owner’s Equity

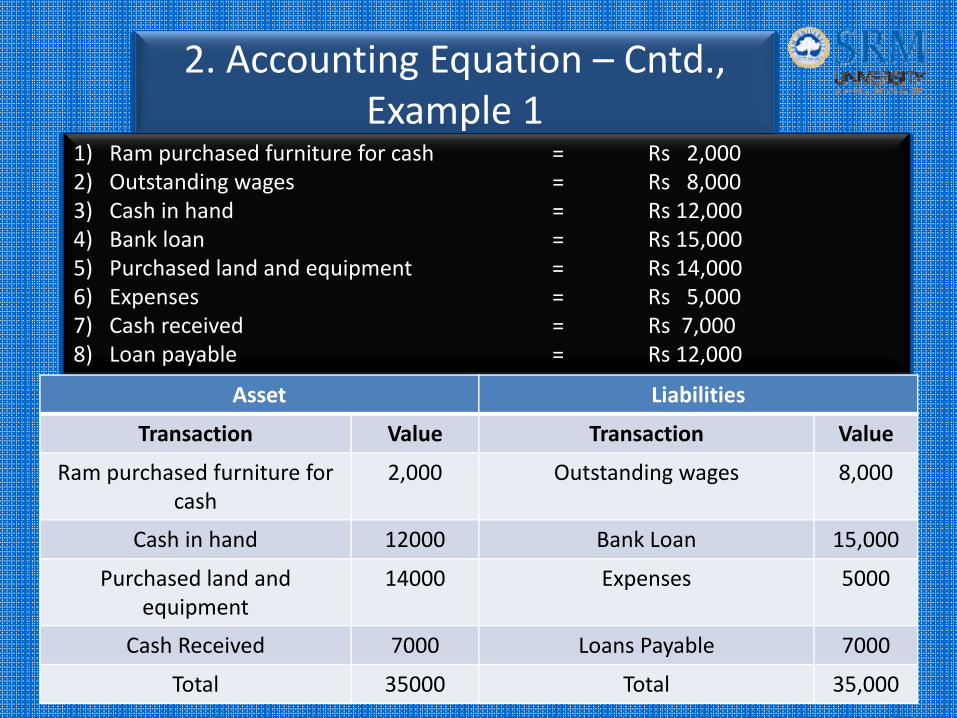

2. Accounting Equation – Cntd.,Example 1

1) Ram purchased furniture for cash = Rs 2,0002) Outstanding wages = Rs 8,0003) Cash in hand = Rs 12,0004) Bank loan = Rs 15,0005) Purchased land and equipment = Rs 14,0006) Expenses = Rs 5,0007) Cash received = Rs 7,0008) Loan payable = Rs 12,000

Asset Liabilities

Transaction Value Transaction Value

Ram purchased furniture for cash

2,000 Outstanding wages 8,000

Cash in hand 12000 Bank Loan 15,000

Purchased land andequipment

14000 Expenses 5000

Cash Received 7000 Loans Payable 7000

Total 35000 Total 35,000

2. Accounting Equation – Cntd.,Example

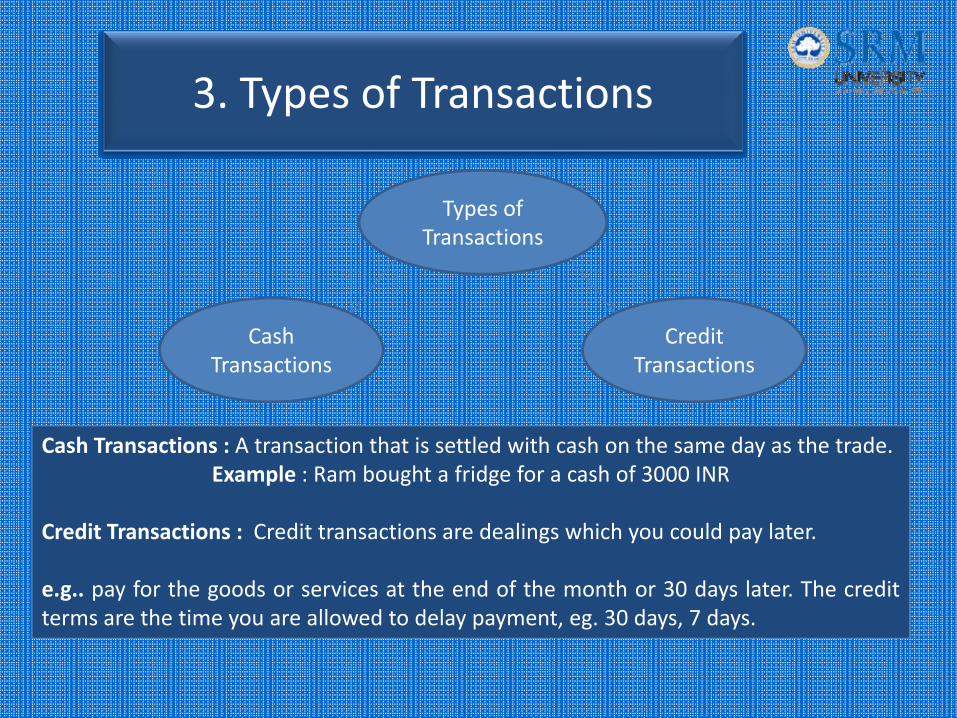

3. Types of Transactions

Types of Transactions

Cash Transactions

Credit Transactions

Cash Transactions : A transaction that is settled with cash on the same day as the trade.Example : Ram bought a fridge for a cash of 3000 INR

Credit Transactions : Credit transactions are dealings which you could pay later.

e.g.. pay for the goods or services at the end of the month or 30 days later. The creditterms are the time you are allowed to delay payment, eg. 30 days, 7 days.

4.1 PurchasesPurchases Account : A temporary account used in the periodic inventory system torecord the purchases of merchandise for resale. (Purchases of equipment or suppliesare not recorded in the purchases account.) This account reports the gross amount ofpurchases of merchandise. Net purchases is the amount of purchases minus purchasesreturns, purchases allowances, and purchases discounts.

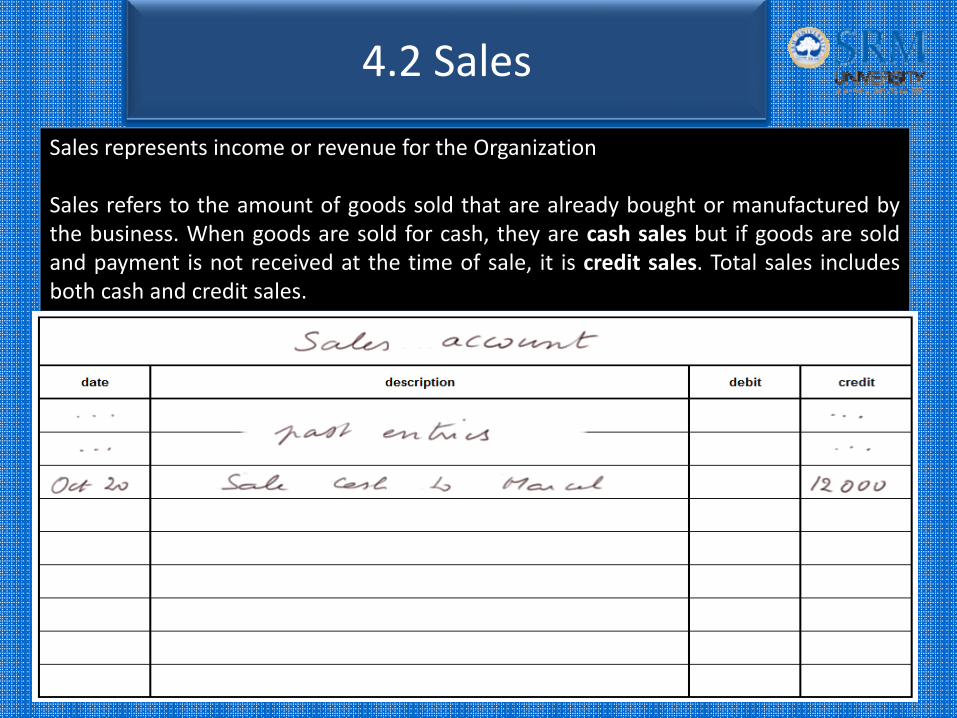

Sales represents income or revenue for the Organization

Sales refers to the amount of goods sold that are already bought or manufactured bythe business. When goods are sold for cash, they are cash sales but if goods are soldand payment is not received at the time of sale, it is credit sales. Total sales includesboth cash and credit sales.

4.2 Sales

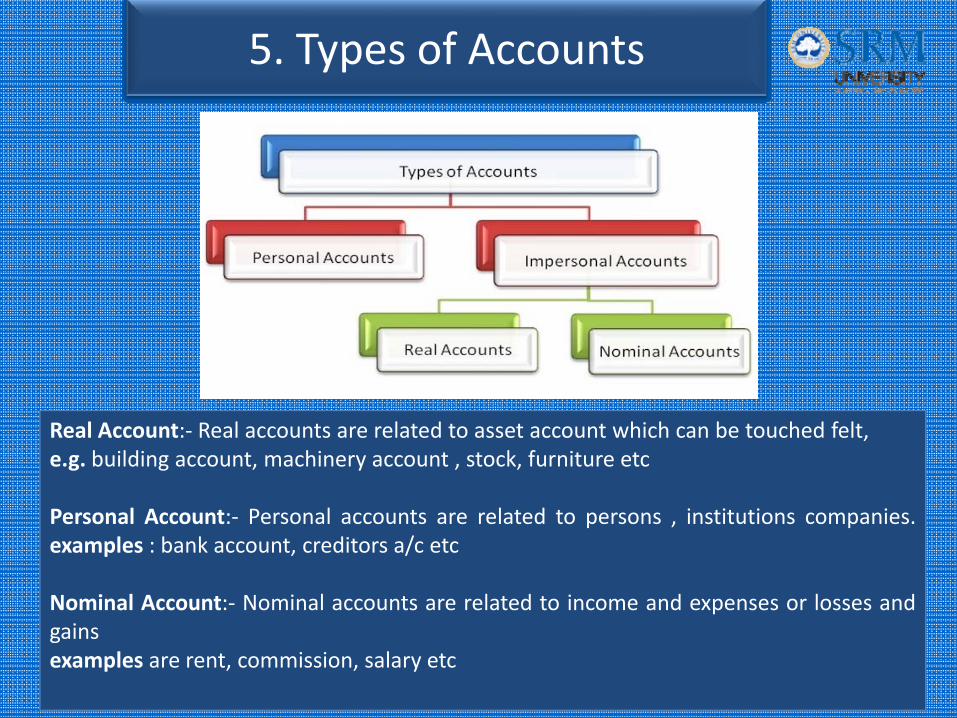

5. Types of Accounts

Real Account:‐ Real accounts are related to asset account which can be touched felt,e.g. building account, machinery account , stock, furniture etc

Personal Account:‐ Personal accounts are related to persons , institutions companies.examples : bank account, creditors a/c etc

Nominal Account:‐ Nominal accounts are related to income and expenses or losses andgainsexamples are rent, commission, salary etc

6. Golden Rules of AccountingDebit The Receiver, Credit The Giver

This principle is used in the case of personal accounts. When a person gives something to theorganization, it becomes an inflow and therefore the person must be credit in the books ofaccounts. The converse of this is also true, which is why the receiver needs to be debited.

Debit What Comes In, Credit What Goes OutThis principle is applied in case of real accounts. Real accounts involve machinery, land andbuilding etc. They have a debit balance by default. Thus when you debit what comes in, you areadding to the existing account balance. This is exactly what needs to be done. Similarly when youcredit what goes out, you are reducing the account balance when a tangible asset goes out of theorganization.

Debit All Expenses And Losses, Credit All Incomes And GainsThis rule is applied when the account in question is a nominal account. The capital of thecompany is a liability. Therefore it has a default credit balance. When you credit all incomes andgains, you increase the capital and by debiting expenses and losses, you decrease the capital. Thisis exactly what needs to be done for the system to stay in balance.

S NO Debit Credit1 The Receiver The Giver

2 What comes in What comes out

3 All expenses and losses All incomes and gains

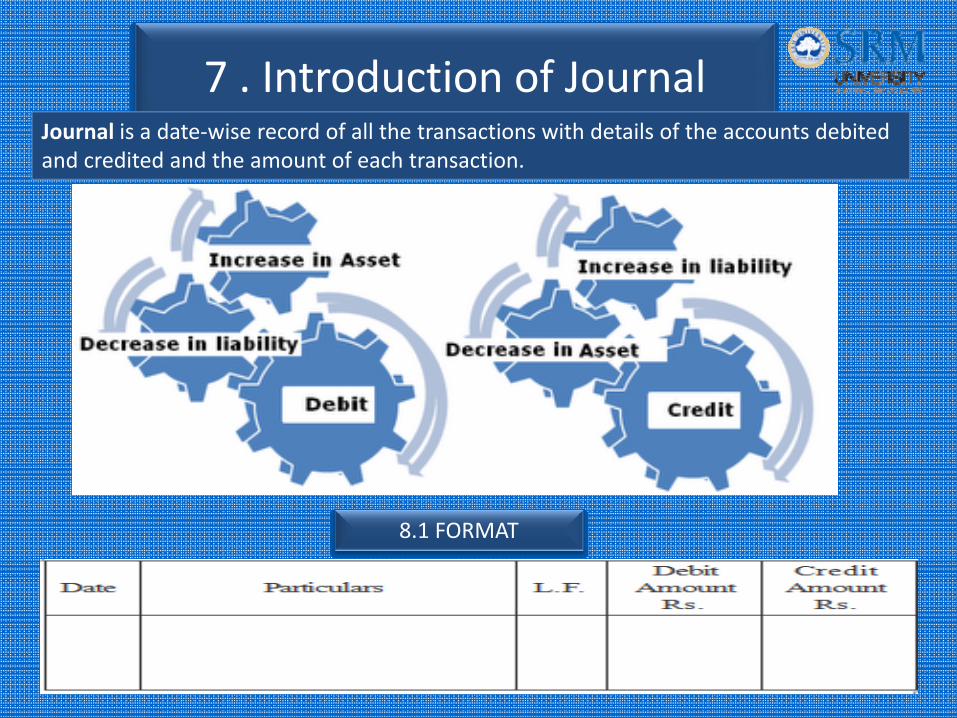

7 . Introduction of JournalJournal is a date‐wise record of all the transactions with details of the accounts debited and credited and the amount of each transaction.

8.1 FORMAT

7. Introduction of Journal – Cntd.,

Step No. Process

1 Determine the two accounts which are involved in the transaction

2 Classify the above two accounts under Personal, Real or Nominal

3 Find out the rules of debit and credit for the above two accounts

4 Identify which account is to be debited and which account is to be credited

5 Record the date of transaction in the date column. The year and month is written once,till they change. The sequence of the dates and months should be strictly maintained

6 Enter the name of the account to be debited in the particulars column very close to theleft hand side of the particulars column followed by the abbreviation Dr. in the sameline. Against this, the amount to be debited is written in the debit amount column in thesame line

7 Write the name of the account to be credited in the second line starts with the word‘To’ a few space away from the margin in the particulars column. Against this, theamount to be credited is written in the credit amount column in the same line.

8 Write the narration within brackets in the next line in the particulars column.

9 Draw a line across the entire particulars column to separate one journal entry from theother.

7 . Introduction of Journal – Cntd.,Illustration

January 1, 2004 – Saravanan started business with Rs. 1,00,000

8.1 Analysis of Transaction

8.1 Analysis of Transaction

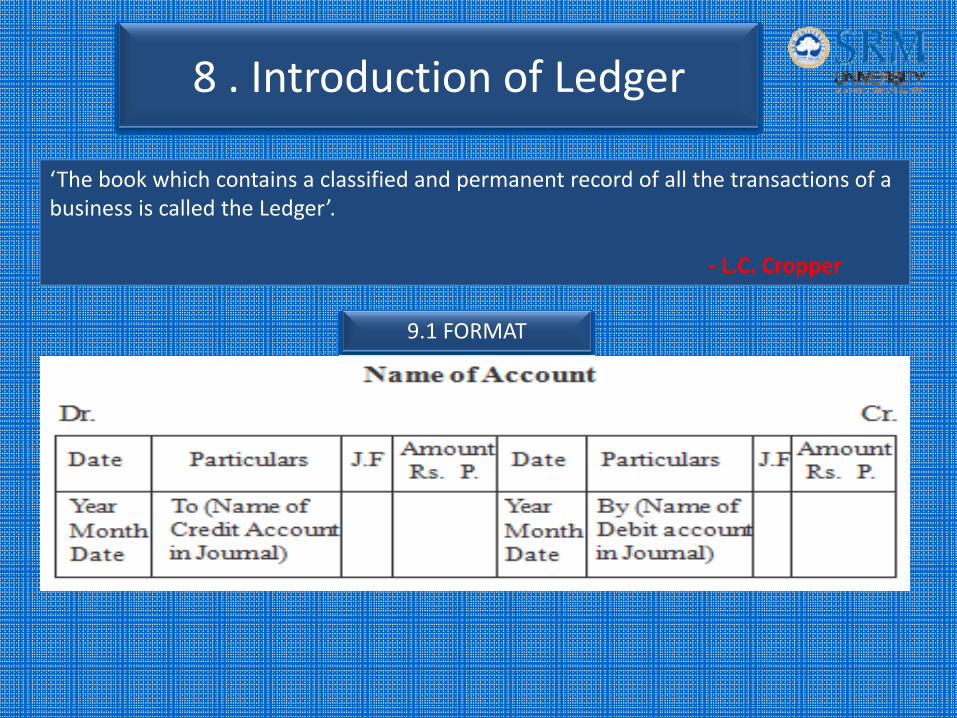

8 . Introduction of Ledger

‘The book which contains a classified and permanent record of all the transactions of a business is called the Ledger’.

‐ L.C. Cropper

9.1 FORMAT

8 . Posting in Ledger

Procedure of posting for an Account which has been debited in the journal entry.

S No. Particulars

1 Locate in the ledger, the account to be debited and enter the date of the transaction inthe date column on the debit side.

2 Record the name of the account credited in the Journal in the particular columns of thedebit side as “To..... (name of the account credited)”.

3 Record the page number of the Journal in the J.F column on the debit side and in theJournal, write the page number of the ledger on which a particular account appears in theL.F. column.

4 Enter the relevant amount in the amount column on the debit side

Procedure of posting for an Account which has been credited in the journal entry

1 Locate in the ledger the account to be credited and enter the date of the transaction inthe date column on the credit side.

2 Record the name of the account debited in the Journal in the particulars column on thecredit side as “By...... (name of the account debited)”

3 Record the page number of the Journal in the J.F column on the credit side and in theJournal, write the page number of the ledger on which a particular account appears in theL.F. column

4 Enter the relevant amount in the amount column on the credit side.

8. Introduction of Ledger– Cntd.,Illustration

Mr. Ram started business with cash Rs. 5,00,000 on 1stJune 2003.

Solution : The above transaction will appear in Journal and Ledger as under

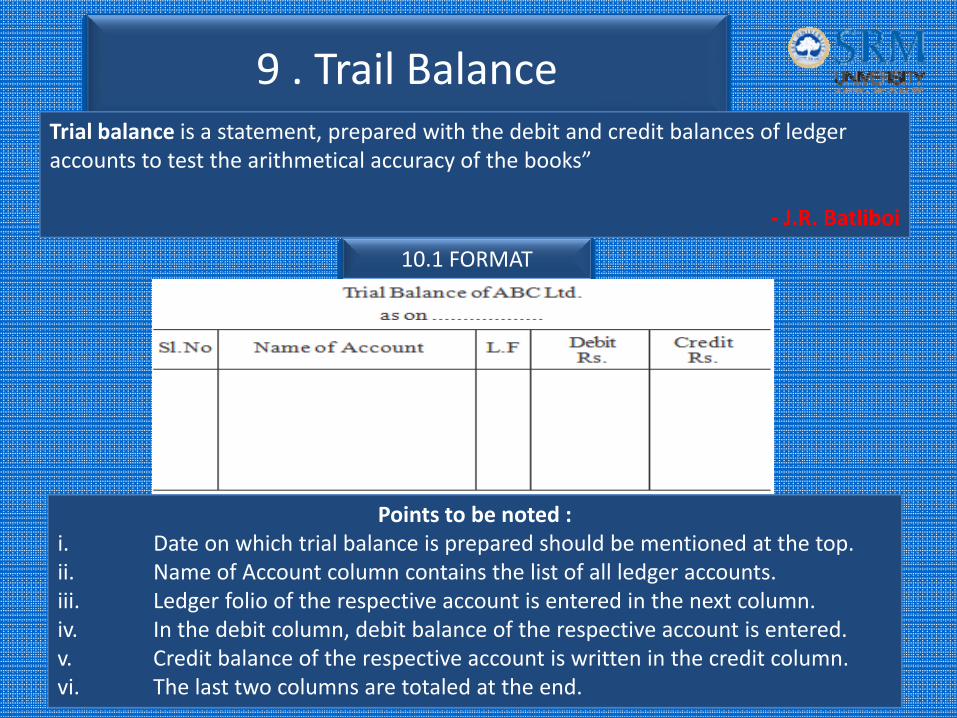

9 . Trail BalanceTrial balance is a statement, prepared with the debit and credit balances of ledger accounts to test the arithmetical accuracy of the books”

‐ J.R. Batliboi

10.1 FORMAT

Points to be noted :i. Date on which trial balance is prepared should be mentioned at the top.ii. Name of Account column contains the list of all ledger accounts.iii. Ledger folio of the respective account is entered in the next column.iv. In the debit column, debit balance of the respective account is entered.v. Credit balance of the respective account is written in the credit column.vi. The last two columns are totaled at the end.

9 Trail Balance ‐ Illustration

The following balances were extracted from the ledger of Rahul on 31st March, 2003.You are requested to prepare a trial balance as on that date in the proper form.

9 . Trail Balance – IllustrationSolution

10. Final Accounts

Final Accounts

Trading, Profit and

Loss Account

Balance Sheet

Parts of Final Accounts

The first part is Trading and Profit and Loss Account. This is prepared to find out the netresult of the business. The second part is Balance Sheet which is prepared to know thefinancial position of the business.

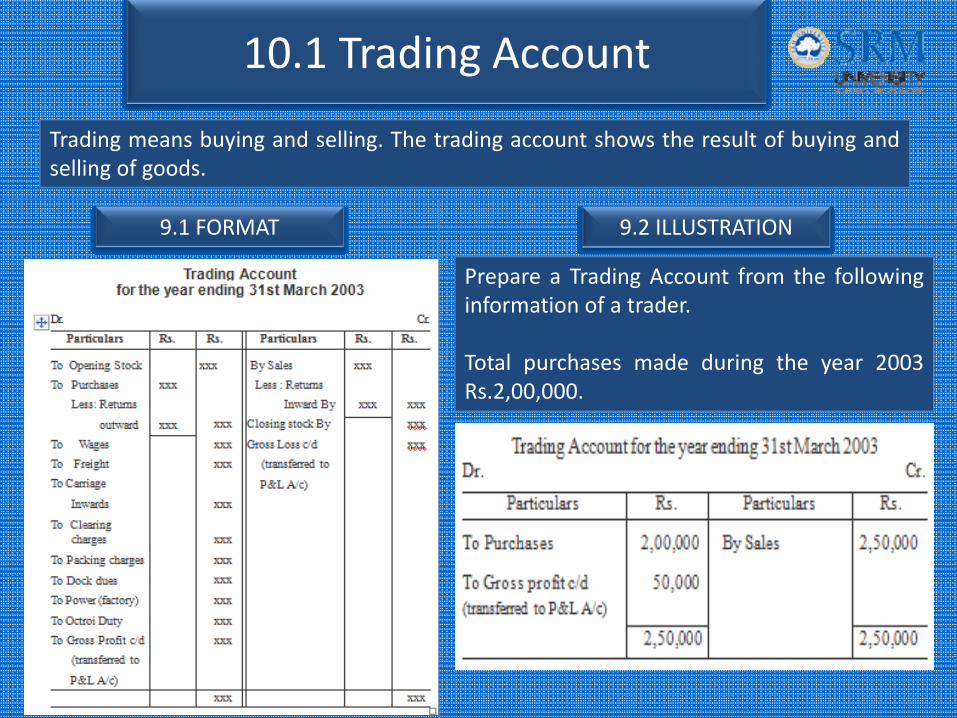

10.1 Trading Account

Trading means buying and selling. The trading account shows the result of buying andselling of goods.

9.1 FORMAT 9.2 ILLUSTRATION

Prepare a Trading Account from the followinginformation of a trader.

Total purchases made during the year 2003Rs.2,00,000.

10.2 Profit and Loss A/C

After calculating the gross profit or grossloss the next step is to prepare the profitand loss account. To earn net profit a traderhas to incur many expenses apart fromthose spent for purchases andmanufacturing of goods. If such expensesare less than gross profit, the result will benet profit. When total of all these expensesare more than gross profit the result will benet loss.

Need

Format

The aim of profit and loss account is toascertain the net profit earned or net losssuffered during a particular period

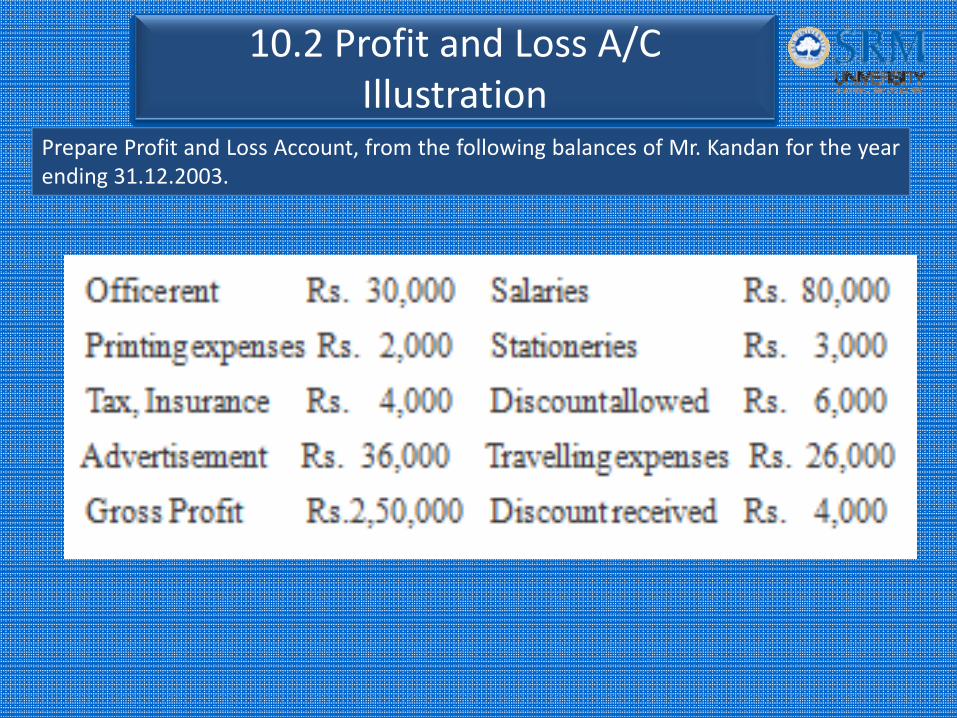

10.2 Profit and Loss A/CIllustration

Prepare Profit and Loss Account, from the following balances of Mr. Kandan for the yearending 31.12.2003.

10.2 Profit and Loss A/CIllustration ‐ Solution

10.3 Balance SheetDefinition

‘A statement which sets out the assets and liabilities of a business firm and which serves to ascertain the financial position of the same on any particular date’

Format

10.3 Balance Sheet Illustration

Question

From the following Trial Balance of M/s. Ram & Sons, prepare trading and profit andloss account for the year ending on 31st March 2002 and the balance sheet as on thedate

10.3 Balance Sheet Illustration ‐ Solution

11.References

1. Higher Secondary Accountancy book published by Tamil Nadu Text Book Corporation

2. T.S.Grewal – Double Entry Book Keeping.3. R.L.Gupta, Radha Swamy – Financial Accounting.4. Institute of Company Secretaries of India – Principle of Accountancy.5. P.C.Tulsian, S.D.Tulsian – ISC Accountancy for Class XI6. Accounting Text and Cases – Robert Anthony, Tata McGraw‐Hill Publications7. www.icai.org8. Education.svtution.org9. www.investpedia.com10. www.lapasserelle.com