accountability and regulation - reporting · pdf fileaccountability and regulation - reporting...

TRANSCRIPT

PROCEEDINGS 27

ACCOUNTABILITY AND REGULATION - REPORTING PERFORMANCE

Cemil AltinRob BaldwinStan Chaplin

Mark CourtneyCarl Hetherington

Jim MarshallIan Rowson

Jean Spencer Peter Vass

Phil Wynn Owen

ACCOUNTABILITY AND REGULATION - REPORTING

PERFORMANCE

Proceedings of a CRI Conference

held on 7th March 2001 at

One Great George Street, London

Chaired by Professor Ralph Turvey

Edited by Peter Vass

Desktop published by Jan Marchant

© The University of Bath All Rights Reserved ISBN

iii

PREFACE The CRI is pleased to publish the papers from its conference on Accountability and Regulation - Reporting Performance, as its 27th set of Proceedings. Regulation benefits from having a coherent and explicit framework of objectives which can be a reference point for judging the performance of the system and holding the regulators, and the regulated, to account. The government has been taking significant steps in recent years to ensure that regulation is cost-effective and meets the principles of ‘better regulation’, set out by bodies such as the Better Regulation Task Force and, internationally, by the OECD. We hope that the CRI conference, and its set of Proceedings, will contribute to the debate. In that respect, we are indebted to the authors and presenters at the conference for their contributions. The CRI would welcome comments on these Proceedings and further analytical work in the area. The CRI publishes work on regulation by a wide variety of authors, and covering a range of regulatory topics and disciplines, in its International, Occasional and Technical Paper series. The purpose is to promote debate and better understanding about the regulatory framework and the processes of decision making and accountability. The views of authors are their own, and do not necessarily represent those of the CRI. Comments, enquiries or manuscripts to be considered for publication should be addressed to: Peter Vass, Director-CRI, School of Management, University of Bath, Bath, BA2 7AY. Peter Vass Director, CRI August 2001

iv

v

CONTENTS Preface

iii

1 The policy framework for ‘better regulation’ Phil Wynn Owen and Mark Courtney

1

2 The role of regulatory accounts: the joint regulators’ consultation document Peter Vass

17

3 Ofgem’s information and incentives project Cemil Altin

31

4 Regulatory accounts in the gas and electricity industries Carl Hetherington

39

5 Regulatory accounts: a multi-utility framework Stan Chaplin

47

6 Integration of periodic reviews and regulatory accounting: lessons from the transport sector Ian Rowson

59

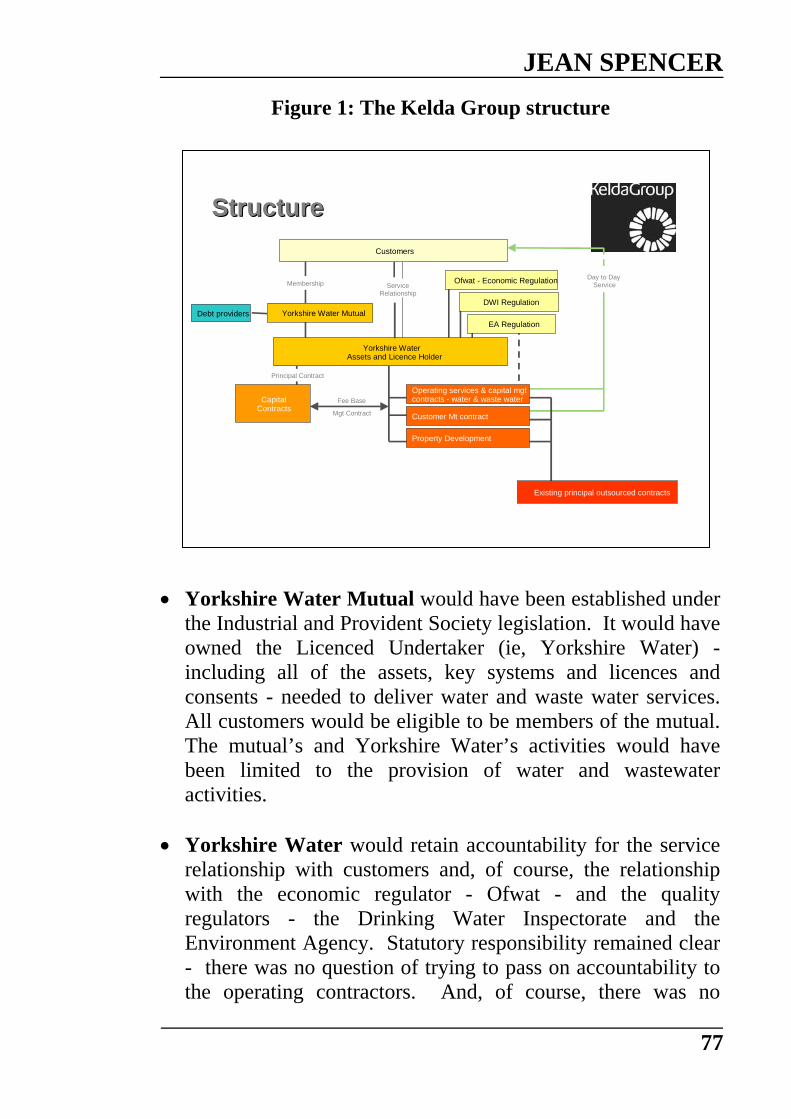

7 Accountability with customer ownership: the Kelda proposals for restructuring Jean Spencer

73

8 The accountability of regulators: international aspects Jim Marshall

83

9 A risk framework for regulatory accountability Robert Baldwin

91

vi

Phil Wynn Owen, Director Mark Courtney, Deputy Director Regulatory Impact Unit, The Cabinet Office

1

1 THE POLICY FRAMEWORK FOR ‘BETTER REGULATION’ Phil Wynn Owen and Mark Courtney

Working to change the regulatory approach in Whitehall and Brussels Introduction Phil Wynn Owen set out his view of the importance of better regulation and what its key elements were, and described the UK and European experience of regulatory reform. The coverage of this part of his talk was similar to the recent paper by Mark Courtney of the Regulatory Impact Unit, which is reprinted below from the CRI Regulatory Review 2000/2001, updated for recent developments. Phil Wynn Owen also described the terms of reference of the Better Regulation Task Force’s current review of the economic regulators and its progress to date. The development of this review has been tracked on the Regulatory Impact Unit’s website.∗ The report was published in July 2001, entitled Economic Regulators (BRTF, Cabinet Office, London). The executive summary of the report includes the following five recommendations:

∗ see www.cabinet-office.gov.uk/regulation/taskforce/programme0001.htm

BETTER REGULATION

2

• Regulators’ objectives - to address the problems which can arise from statutory objectives that “can be contradictory and it is difficult for companies to judge how regulators will prioritise between them”,

Recommendation 1 Regulators’ annual business plans should include a clear explanation of how they will prioritise their different objectives. Regulators should also explain how the decisions they take relate to their objectives. • Costs and benefits - because “the costs of regulation are rising

despite the development of competition, and contrary to the original assumption that this would lead to a reduction in regulation”,

Recommendation 2 Economic regulators should be required to produce assessments of costs and benefits for proposals with a significant impact on business activity. • Individual or board? - “regulatory regimes should be

consistent and predictable” and “to suppport the trend away from individual regulators”,

Recommendation 3 The boards of regulatory bodies should include both executive and non-executive members. They should be appointed for their expertise rather than to represent stakeholder groups. • Consultation - in order that “the experience and expertise of

stakeholders should be used to shape proposals from an early stage”,

P. WYNN OWEN AND M. COURTNEY

3

Recommendation 4 Regulators should include in their work plans proposals to encourage an innovative approach to consultation, allow a real dialogue between different stakeholders and demonstrate how proposals have been amended following consultation. • Withdrawal from competitive markets - given “clear exit

strategies should be implemented and regulators should justify the need for any continued regulation where competition has developed”,

Recommendation 5 Regulators should set out a programme in their annual work plans to review market sectors for lifting price controls and the removal of outdated licence conditions. Companies should be able to challenge failure to complete these programmes.

The remainder of this chapter is the paper by Mark Courtney.∗

BETTER REGULATION: PRINCIPLES AND PRACTICE The need for better regulation There are two conflicting pressures which account for the increasing attention which is being paid to the quality of regulation - not only in Britain but in many countries. On the one hand, there is the frequent demand for increased regulation. There are two reasons for this:

∗ First published as Chapter 8 of the Regulatory Review 2000/2001 - Millennium edition, pp 149-162, CRI, University of Bath, 2001, but updated for recent developments.

BETTER REGULATION

4

• With greater prosperity there is an understandable demand for more regulation to provide greater protection against involuntary risks. For example, levels of death on the roads or industrial injuries that were acceptable a generation ago would not be tolerated now, requiring more stringent regulation of vehicle safety and workplace practices.

• Scientific and technical advances have brought enormous

benefits but have also created new risks, and thus have created the need for new regulations. In addition, we now have increased knowledge about long-standing hazards, such as asbestos and global warming, and increased technical competence to do something about them.

Set against the demand for increased regulation is the growing recognition that, while each individual regulation may be justifiable, there is a danger that their cumulative effect may be to stifle freedom of initiative in both businesses and citizens. A similar effect was recognised earlier in the field of fiscal policy, where it came to be seen that, no matter what the desirability of public expenditure, there is a limit to the proportion of national income that can be taken in taxation or used in public expenditure before the incentives to the private creation of wealth are weakened excessively. Indeed, the tightening of fiscal discipline in recent years in almost all of the industrial countries has been one of the reasons for the increased pressure on regulation. Since governments are unable to increase public expenditure to achieve policy goals, there is greater pressure on them to turn to regulation of private activity to achieve the same effect. While the analogy between fiscal and regulatory burdens is not exact, and the methods that can be used in measuring or controlling them are quite different, there is general agreement that some of the rigour that is customarily applied in the fiscal area needs to be brought to bear on the continued growth in government regulation. The net effect of these two forces - greater demand for regulation and a recognition of the cumulative burden of regulation - has been to put a premium on

P. WYNN OWEN AND M. COURTNEY

5

better regulation. There are two aspects to this: first, to make sure that new regulations are cost-effective in the sense that they bring the greatest social benefits for the least costs imposed on business, consumers and the government. Secondly, to have a procedure whereby laws and regulations that have become obsolete, duplicative or unnecessary can be weeded out. Modernising government - the regulatory impact assessment In the United Kingdom, part of the response to the pressure for better regulation has been to set up more or less independent regulators for the public utilities and for financial services. The extremely important role that they play is not the theme of this chapter, but is covered, in large part, elsewhere in this edition of the Regulatory Review. For the main bulk of government regulation not covered by the independent regulators, the process of reform started in the 1980s with the requirement that regulations should be accompanied by an assessment of the compliance cost that they imposed on business, and was continued with the passage of the Deregulation and Contracting Out Act in 1994, which, by introducing a new kind of amendable secondary legislation, made it easier to repeal obsolete regulations, some of which might be contained in Acts of Parliament. The new Labour Government elected in May 1997 broadened this process and made better regulation an integral part of its Modernising Government programme, where it fits naturally into their overall theme of making government policy evidence-based and responsive to people’s needs. As from August 1998, new legislation or regulation which has a significant effect on business, charities or the voluntary sector has had to be accompanied by a regulatory impact assessment which should set out not only the expected costs to business,

BETTER REGULATION

6

consumers and government but also the expected benefits. These should, as far as possible, be quantified and expressed in monetary terms. This assessment has to be available in the form of a partial (that is, a provisional or preliminary) regulatory impact assessment when collective Ministerial agreement is being sought to the principle of legislation or regulation in a particular area, and when public consultation is being carried out. Special attention should be paid to any burden placed on small businesses. As from October 2000, if the proposals affect small businesses, then the Small Business Service (which was set up in April 2000) must be consulted. It will help in organising consultation with small firms and representative associations and it has the right to have its views recorded in the regulatory impact assessment. Subsequently, a full regulatory impact assessment is developed to include the results of public consultation and is the basis on which Ministers decide on action. As from October 2000, the responsible Minister must sign a declaration that, having read the regulatory impact assessment, he is satisfied that the benefits justify the costs. The final regulatory impact assessment should then be placed in the libraries of the House of Commons and House of Lords when the regulation or legislation is presented to Parliament.1 Modernising regulation - principles and practice The previous section described the mechanics of producing a regulatory impact assessment, a process overseen at the centre by the Regulatory Impact Unit (RIU) within the Cabinet Office,

1 Cabinet Office, Good Policy Making: A Guide to Regulatory Impact Assessment, August 2000. The general principles of cost-benefit analysis to be used in a regulatory impact assessment are those in HM Treasury, Appraisal and Evaluation in Central Government, ‘The Green Book’, 1997, HMSO.

P. WYNN OWEN AND M. COURTNEY

7

working with departmental RIUs within each government department. But the process only produces better regulation when it is used at an early stage in the formulation of policy to identify all the options – including non-regulatory options – that might help achieve the policy objective under consideration, and then to choose the most cost-effective form of action. It also needs to work closely with other aspects of good policy-making, including, where appropriate, environmental assessments and the input from scientific advisory committees.2

In the nature of things, the successes in the early stages of this process are not often visible, since they consist of the weeding out of costly or cumbersome proposals that might initially have been a preferred course of action, and their replacement by cheaper, more effective or non-regulatory alternatives. But there are some clear examples of the sort of improvements that have been made later on in the process, when initial proposals that had already been published were subsequently modified: • National minimum wage: reporting requirements were

reduced – eg, there was no longer a requirement to put the national minimum wage on pay slips or to keep detailed records.

• Stakeholder pensions: an exemption was introduced whereby

employers with four or fewer employees would not be required to provide access to stakeholder pensions or deduct pension contributions.

• Working time: revised regulations removed many of the

administrative burdens for businesses, including reduced record keeping in respect of those who opt out of the protection of the regulations and those who essentially determine their own working hours, subject to a minimum.

2 Consultation on a Code of Practice for Scientific Advisory Committees, DTI, July 2000.

BETTER REGULATION

8

• Food Standards Agency: an initial proposal to fund the Agency by a separate levy on all food shops was replaced by funding through taxation.

Good regulation requires not just effective regulation in particular areas, but an ability to take the overall effect of government regulation into account. One reason the Government is paying particular attention to getting early estimates of the impact of proposed legislative and regulatory measures is to enable a more balanced legislative programme to be constructed, taking forward those measures which contribute most effectively to the Government’s overall aims. In addition, the Panel for Regulatory Accountability was established in November 1999, to allow departmental Ministers to explain to it what initiatives they are taking to modernise regulation.3

Regulatory reform Besides an improvement in formulating new regulation, there needs to be a system for reviewing existing regulations to see whether they are still necessary or if they should be amended. Sometimes such a review can be anticipated at the time a regulation is introduced. For example, the government has given a commitment that the operation of the student loan recovery system will be reviewed after one year to establish whether routing repayments through the payroll system places too heavy a burden on small businesses.

3 Current membership is: Minister for the Cabinet Office (chair), Secretary of State for Trade and Industry, Chief Secretary to the Treasury, Parliamentary Secretary in the Cabinet Office, Chairman of the Better Regulation Task Force, Chief Executive of the Small Business Service. For a general guide to the operation of Cabinet Committees see: cabinet- office.gov.uk/cabsec/2000/guide/index.htm.

P. WYNN OWEN AND M. COURTNEY

9

But there is also a need to examine the body of existing regulation. This is one of the principal aims of the Better Regulation Task Force, whose independent, unpaid members come from large and small businesses, citizen and consumer groups, the trade unions and the voluntary sector, and which has been chaired, since it was established in September 1997, by Lord Haskins. This task force can examine any area of legislation and regulation as it affects particular sectors or particular aspects of doing business, publish reports and make recommendations. Recent reports have covered:4

• payroll review; • helping small firms cope with regulation – exemptions and

other approaches; • red tape affecting head teachers; • tackling the impact of increasing regulation – a case study of

hotels and restaurants; • alternatives to state regulation; • protecting vulnerable people. The government has committed itself to responding to the reports of the Better Regulation Task Force within sixty days, and has most often accepted their recommendations. Examples from earlier reports include: • Licensing Hours: The government’s White Paper included

three proposals which had been recommended by the Better Regulation Task Force: more flexible opening hours balanced against the needs of local residents; the development of a personal licence scheme; and the transfer of responsibility of liquor licensing to local authorities.

• Funding for the Voluntary Sector: The Better Regulation

Task Force persuaded the government to simplify the rules in order to avoid discrimination against small voluntary groups.

4 Better Regulation Task Force, Annual Report 1999-2000, Cabinet Office, October 2000.

BETTER REGULATION

10

• Long Term Care: The Better Regulation Task Force helped to get agreement to a new approach based on national rules, ensuring that council homes are inspected to the same standard as private homes.

A second strand in the government’s programme of regulatory reform is the action taken to improve the order-making power under the Deregulation and Contracting Out Act 1994 to make it easier to remove regulatory burdens from businesses, the voluntary sector, charities, the wider public sector and citizens. The Regulatory Reform Act 2001 provides a much wider reforming power than in the 1994 Act, which has mostly been used for quite small changes.5 In particular, it allows the reform of an entire regulatory regime, involving the repeal and replacement of one or more Acts, together with their subordinate legislation. This will allow Ministers to propose reform, for example, in cases where a burden stems from overlapping, out-dated or over-complex legislation. Regulatory Reform Orders, in the process of re-balancing regulatory regimes, will be able to impose burdens as well as remove them, so as to ensure that regulatory burdens are distributed fairly. These wider powers are balanced by stricter safeguards, such that the desirability of making an order depends on the extent to which it reduces burdens. Any necessary protection must be maintained, and no order should prevent anyone from exercising an existing right or freedom which they might reasonably expect to continue to exercise. And any new burdens imposed must be proportionate and must strike a fair balance between the public interest and the interests of the persons affected. The mandatory requirements for thorough public consultation and rigorous Parliamentary scrutiny remain: draft orders must be considered twice by both the Deregulation Committee in the

5 Publication of the draft Regulatory Reform Bill, Cm 4713, April 2000. Further details on the Bill are at: http://www.cabinet-office.gov.uk/regulation/index/bill.htm.

P. WYNN OWEN AND M. COURTNEY

11

House of Commons and the Delegated Powers and Deregulation Committee in the House of Lords before the Committee reports are voted on by the relevant House (this is sometimes called the ‘super-affirmative’ procedure). In addition, Ministers bringing forward regulatory reform orders will be required to present more explanatory information to Parliament than they did with deregulation orders, explaining the burdens that are being removed or reduced; how the tests of the continued exercise of existing rights and the restrictions on any new burdens are being met; and the consultation carried out on the draft order. Examples of the sort of regulatory reform which could be undertaken under the order-making power are: • reform of fire safety legislation (currently enshrined in

approximately 120 Acts of Parliament and a similar number of statutory instruments);

• removal of the duplicative accounting for charitable funds by

NHS bodies, whereby they must currently submit accounts of charitable funds to the Charity Commission under charity law and also to the National Audit Office under health legislation;

• allow school governing bodies to provide after-school

childcare. European regulation By most measures, around half of new regulations taking effect in the UK have their origin in EU initiatives. A better regulatory climate must, therefore, involve improving these measures too. There are two stages to this: improving the transposition and implementation in the UK of European Directives and improving the quality of European Directives themselves.

BETTER REGULATION

12

In transposing European Directives into UK law, a broadly similar process of impact assessment must be made as for regulations introduced on a domestic UK initiative.6 But there are, of course, additional considerations. In transposing European Directives into domestic legislation, one should neither introduce stricter provisions than necessary (over-implementation) nor leave out essential elements (under-implementation). In contrast to the perception of over-assiduous implementation, the UK is in the middle of the European pack in terms of the overall timeliness and completeness of its transposition of European legislation. But it is always necessary to strive for better quality implementation. Rules should be as clear as possible, even if the original Directive is not, but without introducing prescriptions that do not necessarily follow from the Directive (there can be occasions when there are benefits to exceeding some minimum standard in a European directive but, if so, that should be a conscious and not an inadvertent result). We should avoid simply adding EU-based regulations to existing regulations in a particular area – a process known as double-banking. Within the existing system, obtaining better European legislation in the first place is the outcome of making an early assessment of possible measures, lobbying the Commission, Council, European Parliament and other Member States, and negotiating to try to make sure that any piece of legislation represents a proportionate response to the policy need and that it contains sufficient flexibility to allow its implementation to make a positive contribution to welfare in each member country (especially, from our own point of view, in the UK). The European Commission has its own business impact assessment system, known as the fiche d’impact. This applies, however, only to proposals thought to have a significant effect on business and, it would be fair to say, is usually produced only towards the end of the policy-making process, and therefore has

6 Cabinet Office, The Guide to Better European Regulation, 1999.

P. WYNN OWEN AND M. COURTNEY

13

less impact on its formation. There is also a system for review of legislation at EU level known as Simpler Legislation for the Internal Market (SLIM). It has, for example, simplified the rules governing agreement to the Recognition of Diplomas in certain sectors, making it easier for these professional qualifications to be recognised across the EU. The European Council meeting in Lisbon in March 2000, realising the need to improve European competitiveness, gave a very significant push towards better European regulation when it asked:

“…the Commission, the Council and the Member States, each in accordance with their respective powers…to set out by 2001 a strategy for further co-ordinated action to simplify the regulatory environment, including the performance of public administration, at both national and Community level”.7

This aim was reaffirmed at the Stockholm Council in March 2001 where the elements of regulatory reform were further defined. The Commission is now committed to bringing forward a regulatory reform strategy for the Laeken Council in December 2001, which will include consultation on proposed regulation, assessment of the impact of regulations, as well as the introduction of schemes for codification and recasting of European legislation and legislation review systems. The public sector Apart from legislation which affects society at large, there is an enormous body of internal regulation and procedures which affects the ability of the public sector to deliver front line

7 Paragraph 17, Presidency Conclusions, Lisbon European Council, 23 and 24 March 2000, ue.eu.int/newsroom/main.cfm

BETTER REGULATION

14

services. Originally designed to ensure accountability or specify standards of service to the public, it can, like other regulation, grow unchecked and, cumulatively, have a stifling effect on efficiency. Many departments have, as part of the Modernising Government programme, undertaken reviews to look for more efficient ways of serving the public. One focus of this work was the establishment, in November 1999, of the Public Sector Team within the Regulatory Impact Unit in the Cabinet Office. Its first report, the result of close collaboration with the Home Office and the police forces in England and Wales, resulted in agreed recommendations for the reduction of police paperwork which will result in time savings equivalent to the work of ninety policemen every year.8 The second report, with DfEE, resulted in 4.5 million hours saved across the school system. The third report dealt with paperwork burdens on General Practitioners: the overall estimated annual savings for GPs directly resulting from the outcomes achieved are around 7.2 million appointments plus 750,000 hours. In all its work, the team aims not just to produce reports but to facilitate outcomes and get agreement on action that will make a real difference on the ground. Enforcement Good regulation does not consist only in having well-drafted legislation in place, but also in having it respected and enforced in an effective but sympathetic and flexible way. This Government has adopted an approach based on co-operation between enforcers and those subject to enforcement, by developing an Enforcement Concordat with the close involvement of representatives of business, the voluntary sector,

8 Public Sector Team, Regulatory Impact Unit, Making a Difference, Reducing Police Paperwork, Cabinet Office, April 2000; Reducing School Paperwork, December 2000; and Reducing General Practitioner Paperwork, March 2001.

P. WYNN OWEN AND M. COURTNEY

15

the enforcement community and consumer groups.9 The Concordat is a non-statutory code that describes for businesses and others what they can expect from enforcement officers, with the emphasis on helping businesses to comply, on the basis that prevention is better than cure. Central and local government enforcement bodies commit themselves voluntarily to its principles and procedures. By June 2001 the Concordat had been adopted by over 90% of the local authorities in England and Wales (including all County Councils), by all the local authorities in Scotland and by the vast majority of central government agencies. The principles of the Enforcement Concordat can be summarised as follows: • standards: service standards that business can expect from

local authority enforcers will be published annually with performance against them;

• openness: information will be given in plain language and advice will be disseminated widely;

• helpfulness: staff will work on the basis that prevention is better than cure;

• complaints procedures: well publicised and timely; • proportionality: any action required will be proportionate to

the risks; • consistency: arrangements will be in place to ensure that

different enforcers treat businesses in the same way. The Concordat also sets out procedures, including: • a business will be told what is good advice and what is a legal

requirement; • as far as possible in the circumstances, there will be discussion

before formal action is taken;

9 Cabinet Office, Enforcement Concordat, March 1998. Also available at www.cabinet-office.gov.uk/regulation/1998/enforce.htm

BETTER REGULATION

16

• if action does have to be taken for urgent reasons, this will be followed by a prompt written explanation of the reasons.

Enforcement authorities adopting the Concordat commit themselves to production of an implementation plan setting out any changes that are needed to their procedures or officer training to ensure compliance with the Concordat. Adopting authorities are also required to produce an annual report on their performance against the Concordat. The Regulatory Impact Unit in the Cabinet Office is co-ordinating the adoption of the Concordat, and intends to commission independent research into its effectiveness on the ground. Conclusion Better regulation is a continuing process. Initiatives taken over recent years should ensure that individual regulations and legislation are introduced and enforced with better knowledge of whom they will affect and in what way, and that they will have a better balance between costs and benefits as a result. In a society of increasing technical complexity, where fewer activities are undertaken by the public sector and more by the regulated private sector, it is unlikely that the cumulative volume of regulation will ever actually decrease. But timely reassessment of old regulations and rigorous scrutiny of new ones should minimise the burden of regulation and ensure that it contributes as effectively as possible to the goals that society sets itself.

Peter Vass, Director, CRI and Senior Lecturer, University of Bath School of Management

17

2 THE ROLE OF REGULATORY ACCOUNTS: THE JOINT REGULATORS’ CONSULTATION DOCUMENT Peter Vass Introduction Regulation is for a purpose; not for its own sake. To achieve good regulation there must be a framework of objectives to inform regulatory action, and criteria which are demonstrably appropriate to judging the performance of regulation, including both the regulator and the regulated. The list of questions to be asked includes issues such as: • is the focus of regulation on outcomes, rather than just inputs? • are the incentive properties of the regulatory system good, or

mis-aligned, leading to perverse or unintended outcomes? • is the regulatory system consistent, for example, as between

its treatment of competition and public service obligations? • has the cost-benefit test been applied, both to the setting of

quality and service standards, and by the regulator in costing the effect of regulatory action on all parties?

• are the rewards of out-performance equitably divided between

stakeholders and, in particular, do the rewards reflect management effort?

THE ACCOUNTING FRAMEWORK

18

Harmonisation of regulatory accounts Regulatory accounts are important for the accountability of the regulator and the regulated, and help answer questions such as those listed above. This is because they are prepared regularly; reflect the ambit of regulatory action and, in the series of accounted profits and costs, reflect the outcomes of the incentive based, RPI-X price control system (to be compared with the forecast outcomes made at the time of the regulator’s periodic review of price controls). It was, therefore, a welcome policy development arising from the Labour Government’s ‘review of utility regulation’ which emphasised the fact that harmonisation and consistency of regulatory practice across sectors was to be an important further development in promoting public confidence and understanding of the generic regulatory system that applies to all of our (mostly privatised) utilities and network industries. One practical outcome was the Joint Regulators’ Working Group, set up to address in a more formal way common regulatory issues and procedures. Since 1999 it has reported annually, and therefore has particular potential as a catalyst for change, cross-sectoral harmonisation and debate. The question is whether it will be used positively to find further common ground - or whether it will more often than not be used to approve the perpetuation of different approaches, albeit to like issues. The form of regulatory accounts is an ideal topic to test the new, cross-sectoral approach - in part because the spotlight has often been on the high theory of the economics of regulation, and accounting for regulation has been seen as a detail to be left to the ‘bean-counters’; in part because, in practice, the substantive impact of regulation is to be found and discussed in terms of accounts, but the conventions of accounting and their apparent ‘flexibility’ makes for suspicion and uncertainty as to what is being measured and how it should be interpreted.

PETER VASS

19

Joint ownership? The regulators and the regulated have a joint interest in regulatory accounts, and this reflects the fact that each periodic review is underpinned (even if the general public is not made aware of it) by forecast regulatory accounts based on the regulator’s calculations and assumptions for setting the price controls. As these reflect the regulator’s decisions, then they are ‘owned’ by the regulator, and could be used to show, for example, that the price controls set are consistent with the company earning a normal rate of return (which will demonstrate the key role of the regulatory asset base in consistently allowing, through the rolling forward method, a return on investment until the return of investment). Other practical aspects of regulation, such as the treatment of any discount on assets purchased at privatisation (and the allocation of that discount between regulated and unregulated assets), clawback of disallowed revenues or carry-over of out-performance into the next period’s allowed revenue in order to enhance incentives, could equally well be reflected in the format and presentation of the forecast regulatory accounts (and different methods of presentation of carry-over could be developed, based either on enhancing asset value (‘goodwill’) or showing a higher than normal allowed rate of return). The regulated companies, however, prepare, and hence ‘own’, the outturn accounts. These outturn accounts will show the companies actual capital (CAPEX) and operational expenditure (OPEX). It is the comparison between the forecast and the outturn accounts which provides the insights into the performance of the regulatory system. Fair comparisons, however, require ‘like for like’ comparisons, and there needs to be flexibility to consider what regulatory adjustments might be necessary to ensure that. Whilst it would be helpful to achieve consensus that both are prepared on a consistent, like-for-like, methodology, there may be legitimate reasons for differences between the approach of the regulator and regulated in reporting

THE ACCOUNTING FRAMEWORK

20

results. So it is necessary to conclude that the regulator has to be responsible for the ‘integrity’ of a set of published, outturn accounts which can be fairly compared with the regulator’s forecast accounts (which might, for reasons of commercial confidentiality at the time of each periodic review, only be published - in full or in part - at the next periodic review as part of the retrospective comparison with the outturns in order to judge performance). This issue has surfaced quite interestingly with Ofgem’s proposal that each company should publish its own estimate of its regulatory book value.1 Prima facie, it would be expected that the regulator should be the guardian of a properly constructed, rolled forward regulatory asset base which took account of allowed acquisitions in the period and deducted allowed depreciation consistent with the methodology of the periodic review. This is illustrated in a number of responses to Ofgem’s consultation paper:

“we have some reservations about the value of the company’s view of its regulatory asset value (RAV), since in the past there has always been a difference in view between the regulator and regulated about the regulatory asset value”.

British Gas Trading

“Ofgem suggests that regulated businesses should include their own interpretation of their asset value in their regulatory accounts. This implies that Ofgem is unwilling to agree accounting principles for determining regulatory asset values”.

Transco In anticipation of possible similar proposals from the water regulator, a water industry commentator prepared a draft response as follows:

1 Ofgem (August 2000), Regulatory accounts - consultation paper.

PETER VASS

21

“any published regulatory capital value (RCV) should be one that is recognised and agreed (with Ofwat) - it would be misleading and unhelpful for companies to report their estimate of the RCV, taking account of, for example, discretionary expenditure if Ofwat subsequently take a different view of the allowability of investment, or indeed change the rules retrospectively”.

Timing: sectoral and joint consultations The regulators published their joint consultation paper in October 2000.2 The publication by Ofgem in August 2000 of its own regulatory accounts consultation paper has been noted above, and it might have been expected that Ofgem’s final proposals would await the final conclusions from the inter-regulatory working group, following their consultation, before issuing its own final proposals. However, Ofgem published its own final proposals in November 2000, reaching broadly the same conclusions as their August 2000 document (and the final proposals from the joint regulators had not been published by the time of the CRI conference in March 2001, of which this is the Proceedings - it was published in April 2001 under the same title as its consultation document but with the by-line, final proposals paper). Whilst there were important timing reasons for the development of the Ofgem proposals, including the requirement of the Utilities Act 2000 to separate distribution from supply licences in electricity, and the progress of Ofgem’s Information and Incentives Project [see in particular the chapters by Carl Hetherington and Cemil Altin which follow], it has to be said that the timing has been unfortunate in undermining, to some

2 Ofgem, Oftel, Ofwat, Ofreg, ORR, CAA, Postcomm (October 2000), The role of regulatory accounts in regulated industries, consultation paper, inter-regulatory working group, Ofgem.

THE ACCOUNTING FRAMEWORK

22

extent, belief in the integrity of the consultation process, for what should be seen as an important ‘top-level’ framework document aimed at harmonising practice. The cynic has been left with the view that the final inter-regulatory proposals, when published, will accommodate whatever sectoral practice is in place. This is regrettable, but was perhaps inevitable because Ofgem’s own consultation document showed clearly the tensions between the aim of reporting to reflect the objectives of regulation and reporting consistently with generally accepted accounting practice (GAAP). This could be termed a ‘developing debate’. Ofgem fully recognised a problem with the existing regulatory accounts, as shown from the following extracts (August 2000 consultation document):

“at present regulatory accounts do not include the information necessary to make proper comparisons between actual performance and the assumptions underlying network price controls”,

and

“these factors suggest that the primary purpose of regulatory accounts should be to support the regulation of monopoly businesses subject to on-going price control”,

but concluded that the regulatory accounts should be:

“prepared on the basis of historical cost accounting principles (HCA) but with disclosure of each company’s estimate of its regulatory asset value”,

even though they were to be:

PETER VASS

23

“presented in such a way so that they can be reconciled in a reasonably straightforward way with the assumptions underlying the price controls and the statutory accounts”.

One reason for the emphasis on historical cost accounts being comparative practice:

“however, at present it is not clear to what extent companies in general will move toward modified historical cost accounting (MHCA) principles and so the case for HCA principles remains compelling”,

and “the financial modelling, which is used during the price control review to inform judgements about the financial viability of network businesses, uses HCA principles, as this is broadly consistent with the approach adopted by the credit rating agencies”.

But does this miss the point? We should note too that it is generally accepted accounting practice that any form of modified historical cost accounts should include a reconciliation to historical cost profit in accordance with Financial Reporting Standard (FRS) 3, Reporting Financial Performance. An accounting digression The conflict reflected in the above Ofgem statements arises because price controls are not specified in terms of historical acquisition costs. The regulatory system is based on financial capital maintenance, whereby an indexed asset base is used to provide a real rate of return. This conflict over the price base can be summed up as follows:

THE ACCOUNTING FRAMEWORK

24

A key accounting principle

• Revenues are ‘matched’ with expenses for the year to determine profit or loss

• Properly defined to include the cost of • opex • capital consumption (depreciation) • capital finance (cost of capital)

then we have ‘economic’ profit (or loss) for the year.

• But Revenue = Price x output (P.Q) and Expenses = Cost x output (C.Q)

so not comparing ‘like with like’ if P and C are not on the same price base.

The importance of preparing regulatory accounts which are consistent with regulatory objectives and price control procedures was certainly recognised by respondents to the Ofgem consultation paper, some of which follow:

“we believe that current cost accounting (CCA) concepts are important to an understanding of the performance of the business with long lived assets such as ours, and should therefore be an integral part of the price review process”,

and went on to note comparatively:

“since Ofwat, Oftel and ORR require current cost regulatory accounts, the replacement of CCA by HCA by Ofgem would be a step away from consistency”.

United Utilities

“the primary purpose of the regulatory accounts is to enable stakeholders to compare actual performance to

PETER VASS

25

the assumptions underlying the price control. This requires that the regulatory accounts reflect the basis of price controls”,

so that Transco:

“firmly rejects Ofgem’s proposal that regulatory accounts should be prepared on a historical cost basis on a number of grounds, including that such accounts would not reflect the basis of the price controls and so would not be consistent with the primary purpose”.

Transco

The joint regulators’ proposals The joint regulators’ proposals reflect the same tensions. They state the usefulness of regulatory accounts as follows:

“some of the practical applications of regulatory accounts can include:

• monitoring performance against the assumptions

underlying the current price control; • informing future price control reviews; • assisting in the detection of certain anti-competitive

behaviour, such as unfair cross - subsidisation and undue discrimination;

• assisting comparative competition; • assisting in monitoring financial health;

THE ACCOUNTING FRAMEWORK

26

• improving transparency in the regulatory process (regulatory accounts are the main source of regular, published and audited information about regulated companies)”,

but then give precedence to sectoral practice and explicit authority for reporting standards to each regulator. This is well reflected in the following extracts, which represent a pot pourri rather than harmonisation:

“the proposed common regulatory accounting framework will provide a structure for the preparation of regulatory accounts”,

but propose that:

“regulatory accounts will be prepared and audited using either the regulatory accounting guidelines (RAGs) for the industry or, where a RAG does not cover the issue, UK GAAP. Where there is any conflict between RAGs and UK GAAP, then the RAGs will take precedence”,

going on to reinforce the use of sectoral discretion based on existing differences as follows:

“nevertheless, the approach adopted by each regulator reflects the specific circumstances of the industry concerned”,

with the result that:

“given this diversity of valuation methods it is not possible to achieve consistency in the basis of preparation of regulatory accounts”.

PETER VASS

27

Diversity of accounting practice It is true that there is diversity of regulatory practice, which will be reflected in different series of accounting numbers, but each is consistent with the regulatory objectives in the sector for profiling revenue, and reflects an underlying financial capital maintenance system, that is, none of them are historical cost. The three main models are: • acquisition cost accounting, with acquisition costs updated by

the RPI; • replacement cost accounting, with uprating by the RPI: a

regulatory hybrid which allows for current depreciation charges to reflect replacement cost but with an abated regulatory book value to avoid windfall gains to shareholders where there was a substantial discount at privatisation (the Competition Commission, and it predecessor body, the Monopolies and Mergers Commission, dealt with the problem by applying a market to asset ratio (MAR) adjustment which in effect applied the acquisition cost model);

• renewals accounting, with future cash flows met by an annual

repairs and renewals provision, and with acquisition costs (Capex) at privatisation, or for improved levels of service, capitalised as non-depreciable assets on which a rate of return is earned.

The importance of current cost values is reinforced by the approach adopted by the Competition Commission with respect to Mid-Trent Water, which is referred to explicitly by United Utilities in their response because its report shows that, first:

THE ACCOUNTING FRAMEWORK

28

“the Competition Commission therefore regards current cost depreciation as more significant than HC depreciation for water companies, and by extension to other network industries with long life assets, such as electricity distribution”,

second,

“the replacement cost of a network in a current cost balance sheet provides valuable information on the annual cost of maintaining that network”,

and, thirdly:

“for a regulator to include less than the forecast maintenance expenditure in price limits would be unfair to future generations since it would mean that today’s customers were paying insufficient to maintain the asset base and future customers would have to make up the deficit in higher bills”.

The audit statement The joint regulators’ proposals include the need for reconciliation to the underlying regulatory objectives:

“The published regulatory accounts should also include a comparison between the actual performance of the company and the assumptions underlying its price control”,

which is very welcome, but is undermined, not only by the sectoral discretion, but by the weakening of the audit opinion, as follows:

PETER VASS

29

“reflecting the fact that RAGs may take precedence over the UK GAAP in the preparation of regulatory accounts, then it may no longer be appropriate to use “true and fair view” in the audit opinion”,

therefore proposing “ presents fairly in accordance with”,

which fails to emphasise that there is a set of objectives for regulation, and fails to put an additional onus on regulators to issue accounting guidelines which properly reflect the underlying objectives, spirit and approach of regulation. Conclusions • disappointment [at this stage] that the opportunity has not

been taken by the joint regulators’ working group to put regulatory accounting and reporting centre stage - and to recognise the direct link between the periodic review methodology and the primary regulatory accounts - something which is essential to providing accountability and public understanding;

• it is not too late for the joint regulators’ final proposals to

reconsider, and to surprise us; • but then, even if it doesn’t, the regulatory accounts will

develop because they are important to the evolution of the RPI-X system. For example, if we are to extend the review period from five to perhaps ten years then that might have to be associated with some form of profit sharing and we would need to account for profit correctly;

THE ACCOUNTING FRAMEWORK

30

• the practical reality of financial capital maintenance being the basis of the regulatory system (which takes account of changing prices) will remain the underlying driver for regulatory accountability and, hence, reporting, even if it is partially obscured by historical cost accounting.

Cemil Altin, Project Manager, IIP, Office of Gas and Electricity Markets (Ofgem)

31

3 OFGEM’S INFORMATION AND INCENTIVES PROJECT Cemil Altin Introduction I intend to concentrate on the information side of the Information and Incentives Project (IIP), which has been the focus of our work so far. I will also talk a little about the next stage of the project which will be about translating the information that we collect into an incentive scheme to strengthen the incentives on companies to deliver the appropriate quality of supply. 1999 DPCR review The commitment to undertake the IIP was born out of the last distribution price control review (DPCR) of public electricity suppliers (PESs), undertaken in 1999. From that process it was recognised by all sides that there were problems in the way in which price controls were reviewed and implemented - problems that could be avoided. This work has built on the foundations of RPI-X price controls which have demonstrated strong incentives on companies to reduce costs.

Some problems with RPI-X Quality and accuracy of information - it was clear from the last price control review that the quality and accuracy of information that the companies were providing to the regulator was not of a satisfactory level. A significant amount of time during the price review was spent cleaning up cost data to make it more

OFGEM’S IIP

32

consistent - little work was done on the side of quality. It was recognised that this was an untenable position, therefore the current work of regulatory accounts (on costs) and IIP (on quality) has sought to improve the information that we collect from companies. Concerns about company behaviour - There are incentives on companies to game the regulator at the time of the price review, rather than continually focusing on beating objectively set targets. There is also a distortion with respect to the incentives on companies to reduce costs - associated both with the periodicity of the price control process and the way in which operating and capital expenditure are treated. At the last review not enough was known about the relationship between operating and capital expenditure to set a total cost price control…this may change in the future. The search for more competitive solutions - One way of overcoming some of the problems associated with the periodicity of price controls, and for improving incentives on companies, is to introduce an increased element of competitive solutions, or greater use of comparative assessment. What happened in 2000 The focus for the IIP has been on the fourteen electricity distribution businesses of the public electricity suppliers. However, some of the principles identified during the IIP could be applicable to other network regulated businesses. For example, the ongoing review of Transco’s price control has identified the need to have a greater focus on outputs and on improving the quality of information that the company provides to the regulator. Ofgem also intends to introduce stronger incentives on Transco to deliver quality of service to its customers - using guaranteed and overall standards of performance and a new incentive scheme. The incentive scheme

CEMIL ALTIN

33

is analogous to the IIP scheme but in eventuality it may differ in its framework for a variety of reasons, including a different industry structure. The work on the IIP so far has focused on improving the quality and accuracy of information about quality of service provided by companies to the regulator. We found that up to 30 per cent of the differences between companies on quality of supply performance could be due to different degrees of accuracy in the measurement systems used by companies and different definitions. It would not be possible to base the incentive scheme on this information. Therefore steps have been taken to improve the situation. We now require that the companies report to a specified level of accuracy for the number and duration of interruptions to supply (as set out in the licence condition) and using consistent definitions as set out in the Regulatory Instructions and Guidance (RIGs). The new requirement specifies that companies must report to a 95 per cent accuracy level, at high voltage (HV) level and 90 per cent at the low voltage (LV) level for the number and duration of interruptions to supply. We published our initial thoughts on how companies would be assessed against these accuracy requirements in the covering letter to the February version of the RIGs. Taking this forward is an important part of the work this year. The RIGs, which set out consistent definitions and related instructions and guidance for all IIP information, will also improve matters. If companies fail to meet the required levels of accuracy Ofgem will need to consider what action is necessary. This could include the imposition of financial penalties under the Utilities Act 2000. We have also specified the information that companies must report to Ofgem on the medium term performance of their networks - this is covered by IIP. This information will help improve the understanding of the impact of decisions on the medium term performance of the network - both involving

OFGEM’S IIP

34

expenditure by the companies and regulatory decisions. The information that must be provided covers two broad areas - a detailed analysis of fault trends and their causes and an explanation of the asset management strategy that companies are pursuing. Reporting and audit We published a ‘final’ version of the RIGs in February 2001. This was to provide the companies with a degree of comfort that Ofgem would not change the reporting requirements ahead of them accepting the IIP licence condition. Going forward there is an explicit change process for both the RIGs and the licence condition which sets out how, and in what circumstances, there can be changes. We anticipate that there will be a need for changes to the RIGs as our, and the industry’s, understanding of the IIP output measures improves. In this respect the change will not be bad thing, although it will be necessary to consider the timing for making changes so as not to burden overmuch the companies or Ofgem with the associated consultation process. Once the licence condition has been agreed it will be included in Section C of the new standard distribution licence.1

Ofgem intends to appoint an auditor to help develop the audit framework and undertake the audit. We intend to appoint one set of auditors as this will help to ensure consistency of approach and help identify any differences across companies. This will be different to the arrangements in the water industry where there are company appointed reporters who owe a duty of care to the regulator. However, the circumstances are also different. We are concerned about improving consistency as soon as possible and appointing a single auditor will give this process further impetus. There may be changes in the future. For example, the

1 Since the CRI conference in March all the companies have accepted the IIP licence condition and it is now in the standard distribution licence, which must be determined by the Secretary of State.

CEMIL ALTIN

35

water model may become appropriate or companies could have responsibility for auditing each other, given that they will all have an interest in each other’s data! As part of this year’s work we are also looking at how IIP reporting relates to other reporting requirements on the distribution businesses, which includes guaranteed and overall standards of performance; quality of supply reports, condition 6 reports on network performance and new requirements, such as the proposed long term development statement (as required by the Utilities Act 2000). It will be important to remove any unnecessary duplication and ensure consistency in definitions and approach where appropriate. We also need to think about how Ofgem reports on companies’ performance under the IIP and how this relates to other areas, such as reporting on regulatory accounts and guaranteed and overall standards of performance. In particular, we may need to think about whether there are advantages in having a more overall type of report which covers a number of areas, or whether this may actually reduce transparency. The incentive scheme - context One of the main aspects of the IIP this year will be on developing the incentive scheme which will apply to the fourteen distribution businesses from April 2002. We have explicitly stated that the IIP is not meant to re-open the existing price control and this commitment will guide us in how we develop the detail of the framework. It is also important to think about the other incentives applying to distribution businesses in developing the IIP arrangements. These include: the incentives delivered by the main price control; the Utilities Act 2000; environmental and social guidance;

OFGEM’S IIP

36

NETA; and embedded generation. It will be important to ensure that companies are not provided unclear or distorted incentives. IIP in 2001/2 - key principles There are two main principles or objectives for the incentive scheme - reinforcing existing quality of supply targets and injecting more comparative assessment. The IIP January document set out two broad models for the incentive scheme. The first of these is about strengthening the incentives on companies to deliver the price control commitments on quality which they agreed with the regulator (the absolute model). This relates to the relationship between a company and its own customers, and therefore any transactions regarding failure or success against these targets should take place between these two parties. For example, if a company fails to meet its target it could be required to reduce its prices to its customers. The second model was at the other extreme and was based on a company’s performance being assessed relative to that of its peers. This will help in overcoming problems associated with the periodicity of the price control and, more importantly, provide an ongoing incentive on companies to continually focus on the delivery of quality of service to its customers, ie, help to encourage ‘frontier’ behaviour. This relates to the relationship between companies, as it should be expected that those companies that are out-performers should earn a higher rate of return relative to under-performing companies. This suggests that it should be funded by some form of transaction between companies rather than between a company and its customers. However, work has only just begun in this area and the consultation process has just got underway. In any event, the two models outlined in the January document probably reflect the two extremes of possible outcomes.

CEMIL ALTIN

37

IIP in 2002 - application issues The work on IIP has suggested that changes need to be made to targets to make them more robust and to reflect changed circumstances. These changes fall into three main categories: changes for new definitions; changes for improved measurement systems; and changes to take account of inherent (topographic and demographic factors) and inherited factors which are outside the control of companies and impact on network performance. In deciding how much revenue to put at risk to the incentive scheme, and to each output measure, it will be important to consider a number of factors, including: the quality of information that is collected; the views of customers; and the need to avoid creating perverse incentives if companies expect a different amount of revenue to be subsequently put at risk to the IIP. We also need to think about how companies’ performance will be measured. For example, should there be an end target or a normalised starting point, and should performance be assessed on an annual or rolling basis. These are all important issues which will be occupying our minds over the coming months. IIP timetable The timetable in Table 1 is reasonably self-explanatory, and things are still on track to begin the incentive scheme in April 2002.2

2 Since the CRI conference in March 2001, Ofgem has published its update paper (May 2001) which sets out in more detail the work programme on the IIP over the next 18 months.

OFGEM’S IIP

38

Table 1: IIP Timetable September 2000 Final information proposals January 2001 Consultation - RIGs,

Incentives, initial thoughts February - March 2001 Information licence modification April 2001 Update, including work programme June 2001 Initial proposals December 2001 Final proposals April 2002 Implementation 2003/2004 Next distribution price control review

(DPCR)

Carl Hetherington, Head of Regulatory Accounts, Ofgem39

4 REGULATORY ACCOUNTS IN THE GAS AND ELECTRICITY INDUSTRIES Carl Hetherington Overview Offer first published a consultation paper on regulatory accounting in the electricity industry in October 1998. Ofgem expanded the review to include the gas industry. A consultation paper was published in August 2000 and a final proposals paper was published in November 2000. It is intended that the changes to regulatory accounting in the gas and electricity industries will be effective from April 2001. The provision of high quality regulatory information is important in ensuring that the regulatory process is as efficient as possible. Regulatory accounts are the primary source of regular, audited financial information about the businesses regulated by Ofgem. Improving the quality and relevance of information that companies provide to Ofgem has been the main focus of this review of regulatory accounts. This is also the focus of other important areas of work, such as the Information and Incentives Project (IIP). An inter-regulatory regulatory accounts working group is also examining regulatory accounting issues for gas, electricity, telecommunications, water and sewerage, rail, airport and air traffic control services and postal services. It published a consultation paper on cross-industry issues in October 2000 and a final proposals paper will be published in April 2001 (now published). Ofgem’s proposals in the gas and electricity industry are consistent with the proposals of the working group.

OFGEM - REGULATORY ACCOUNTS

40

The main regulatory accounting issues in the gas and electricity industries that have been identified by Ofgem are that regulatory accounts should be: • prepared only by those separate licensed businesses subject to

price control; • prepared on the basis of historical cost accounting principles

but with disclosure of each company’s estimate of its regulatory asset value and its return on that basis;

• presented in such a way that they can be reconciled in a

reasonably straightforward way with the assumptions underlying price controls and also with the statutory accounts;

• subject to a more rigorous audit process; • published annually on a timely basis and that they will include

more information and narrative. Main issues This section of the paper will provide a summary of the main issues involved in the review of regulatory accounts in the gas and electricity industries. Further information about these issues can be found in the publications identified below. Inter-regulatory working group An inter-regulatory regulatory accounts working group was set up to identify and develop areas of consistency within published regulatory accounts. The group meets on a regular basis to discuss regulatory accounting issues. The working group published a consultation paper in October 2000 and a final proposals paper will be published in April 2001 (now published).

CARL HETHERINGTON

41

Price control For Ofgem, the main purpose of regulatory accounts will be to inform future price control reviews and monitor actual performance against current price controls. As a result of the focus on price controlled businesses, Ofgem is removing the requirement for most of the supply or generation licensees that currently prepare regulatory accounts to prepare them in the future. At the same time, Ofgem is strengthening the requirements on price controlled companies. There will also be more disclosures about the regulatory asset value (RAV). In particular, the notes to the regulatory accounts will set out the regulated company’s estimate of its RAV, how the RAV was determined, the return on the RAV, where appropriate, the return on the price control basis, and other performance indicators. Regulatory accounting guidelines (RAGs) The working group identified a common regulatory framework under which regulatory accounts should be prepared. As part of this framework Ofgem will develop RAGs for the following businesses: • electricity distribution businesses; • NGC and the Scottish transmission businesses; • Transco. In most cases the RAGs will comply with UK GAAP. Where the RAGs do not cover an accounting issue then UK GAAP will be used. If the RAGs do not comply with UK GAAP, then the RAGs will take precedence. It is hoped that a paper on the RAGs for the electricity distribution businesses will be published in April 2001 and that the new arrangements will be effective

OFGEM - REGULATORY ACCOUNTS

42

from April 2001. Working papers on the RAGs for NGC and the Scottish transmission businesses and for Transco should be published in September 2001, proposals will be published in December 2001 and it is hoped that the new arrangements will be effective from April 2002. It is hoped that a working paper on the RAGs for Transco will be published in 2001 or 2002. Basis of preparation Ofgem’s November 2000 regulatory accounts proposals paper, and the working group’s April 2001 proposals paper on the role of regulatory accounts in regulated industries, both discuss the issue of the basis of preparation in some detail. The approach adopted by each regulator to the basis of preparation reflects the specific circumstances of the industry concerned. Given the different methods used by the regulators to value regulated assets it is not possible to achieve consistency in the basis of preparation of regulatory accounts. Each regulator will use the basis of preparation that is most appropriate for its industry. Nevertheless it is possible to identify some of the main considerations governing the choice of the basis of preparation by each regulator. These include: • transparency; • the method used to set price controls; • how the RAV is determined; • consistency within the industry concerned; • consistency with the statutory accounts of the companies

concerned; • views of consumers; • nature of the industry concerned; • the extent of competition within that industry. Other important points to consider when discussing the basis of preparation issue are:

CARL HETHERINGTON

43

• There is no one correct valuation of a company; whether or not a valuation is appropriate depends on the specific circumstances of the company and the user of the regulatory accounts.

• An important aspect of the discussion on the basis of

preparation is that the transparency of the regulatory accounts should be improved by including in the regulatory accounts a note setting out a detailed disclosure of the basis of preparation of the regulatory accounts, the regulated company’s estimate of its RAV, how the RAV was determined and the return on the RAV. The vast majority of the respondents to Ofgem’s regulatory accounts consultation paper from the gas and electricity industries supported the use of HCA as the basis of preparation of the regulatory accounts, with disclosure of information about the RAV.

• Most companies in the gas and electricity industries that will

prepare regulatory accounts in the future, at present prepare their statutory accounts using HCA as the basis of preparation.

• Companies can always include additional financial

information, based on other bases of preparation, in their regulatory accounts.

Audit The main issues involve: • appointment of auditors: Ofgem has proposed a number of

reserve powers which will allow it to appoint another auditor if the audit of the regulatory accounts is unsatisfactory or there is a requirement for another auditor to be involved;

• duty of care: the auditor should owe Ofgem a duty of care for

the audit of the regulatory accounts;

OFGEM - REGULATORY ACCOUNTS

44

• materiality: Ofgem will have a reserve power to set the approach to materiality for the audit of the regulatory accounts if it is unhappy with the current arrangements;

• audit opinion: the audit opinion in the regulatory accounts will

be ‘presents fairly in accordance with’; • engagement letter: an engagement letter for the regulatory

accounts will be agreed between the regulated company, the regulator and the auditor.

Publication The regulatory accounts will either be published as a stand-alone document or in the company’s statutory accounts. The main issue is ensuring that regulatory accounting disclosures are transparent to the users of the regulatory accounts. It is also important to decide how much of the information provided to the regulator should be included in the published regulatory accounts. The main issue concerns what information a monopoly price controlled business should be allowed to regard as being commercially sensitive.

CARL HETHERINGTON

45

Useful publications 1. Offer’s October 1998 regulatory accounts consultation paper. 2. Ofgem’s August 2000 regulatory accounts consultation paper. 3. Ofgem’s November 2000 regulatory accounts final proposals paper. 4. Ofgem’s April 2001 working paper on electricity distribution businesses regulatory accounting guidelines. 5. Inter-regulatory regulatory accounts working group’s October 2000 consultation paper on the role of regulatory accounts in regulated industries. 6. Inter-regulatory regulatory accounts working group’s April 2001 final proposals paper on the role of regulatory accounts in regulated industries.

OFGEM - REGULATORY ACCOUNTS

46

Stan Chaplin, Finance Director, North West Water

5 REGULATORY ACCOUNTS: A MULTI-UTILITY PERSPECTIVE Stan Chaplin Introduction Before looking at regulatory accounts from a multi-utility perspective, an introduction to the ‘new look’ United Utilities. The main subsidiaries of United Utilities are shown in Figure 1.

Service Delivery Customer Sales Contract Solutions Vertex Norweb Telecom

United Utilities Group PLC

The managementand operation ofWater,Wastewater andElectricityDistribution assetsin the North West

The managementof sales of waterand otherservices tocustomers

The managementand operation ofother people’sassets in the UKand internationally

The provision ofbusiness processoutsourcingservices,specialising incustomerrelationshipmanagement

The provision ofvoice and datatelecommunicationssolutions for smalland medium-sizedenterprises

New businesses

Figure 1: New business structure

• Service Delivery - a new business including the regulated

networks in the North West; a multi-utility operation. • Customer Sales - the equivalent of energy supply for water

and wastewater services. This business uses Vertex as its agent in managing the interface with customers.

47

MULTI-UTILITY PERSPECTIVE

48

The restructuring is preparing us for changes in the market place - utility management and competition. All three new businesses identified in Figure 1 can respond to this and are dealt with in more detail below. Vertex is now much less dependent on internal customers, and is winning new external contracts regularly. Table 1 sets out our main purpose behind the restructuring.

Table 1: United Utilities

United Utilities is a multi-utility with a focused strategy to: - improve the efficiency of its regulated

businesses - maximise multi-utility synergies - develop its non-regulated businesses using

its core skills of asset management and customer relationship management

Service delivery Large efficiency savings are required following the regulatory reviews in water and electricity. There is considerable focus on this in the service delivery business, as shown in Table 2. Further multi-utility synergies are being achieved. Note the large investment programme; £3.1 billion of which is on water over the five years to 2004/5. £1 out of every £4 of UK environmental capex is spent in the North West.

STAN CHAPLIN

49

Table 2: Service delivery

The service delivery business: - brings together the management and operation

of licensed water and electricity distribution assets to secure more multi-utility synergies

- delivers the programme of £400 million cost reductions required from the regulators’ price reviews of the businesses

- delivers a regulated capital programme of £3.6 billion over the five years

- holds the stewardship of regulated asset bases Customer sales Setting up trading arrangements between service delivery and customer sales (see Table 3) gives us two market leading opportunities: • learning about the complexities of competition; • influencing the regulatory position, and the development of

competition in water. This includes developing pricing arrangements between service delivery and customer sales which reflect the regulators’ aspirations of a low risk networks business.

Table 3: Customer sales The customer sales business: - was created from United Utilities water business - exploits different skills to asset management - actively participates in the emerging and

competitive water market - is a new business, selling water and wastewater

services within and outside the North West and enhancing the value of our relationship with our existing and new customers

- sells new products and services

MULTI-UTILITY PERSPECTIVE

50

Contract solutions Contract solutions as set out in Table 4 will be our vehicle for entering the utility market place, other than on North West regulated assets. The recent acquisition of Hyder industrial is worth noting. Also the contract won to operate assets and facilities for Welsh Water.

Table 4: Contract solutions

The contract solutions business: - builds on our core asset management skills - manages third party assets throughout the UK

and selected areas overseas - responds to increased outsourcing by utilities

and others in the UK - includes renewable generation, metering and

connections businesses Regulatory accounts I start with a reflection from Edmund Burke.

“The objects of a financier are, then, to secure an ample revenue; to impose it with judgement and equality; to employ it economically; and when necessity obliges him to make use of credit, to secure its foundations in that instance, and for ever, by the clearness and candor of his proceedings, the exactness of his calculations, and the solidity of his funds”.

Edmund Burke An apt quotation for the session on accountability and regulation!

STAN CHAPLIN

51

Objectives The objectives (in Table 5) were set out by Keith Mason (Ofwat) in a paper to the Centre for the study Regulated Industries (CRI) two years ago. These are still relevant issues and I will cover each of these in the presentation, and show how well these are covered by the present arrangements.

Table 5: Tests for regulatory accounts

- consistency? - comparability? - monitoring and informing price reviews? - transparency?

Context First of all it is important for us to put the process of regulatory accounts in context, as set out in Table 6.

Table 6: Context of regulatory accounts

- different information for various stakeholders - current cost accounts

• cost of maintaining the asset base • sustainability of dividends • costs faced by new entrants

- historical cost accounts • relevance to debt markets and equity

investors • key indicators such as interest cover and

gearing - what about regulatory asset value? - all the above are relevant and can co-exist

MULTI-UTILITY PERSPECTIVE

52

There are different informational requirements by different groups of stakeholders as referred to below: • CCA - important in setting price limits for long-lived asset

bases and therefore should be retained as the key basis - this is also an indication of the costs faced by new entrants which is important for the competitive market.

• HCA - important for issues relating to access to funding, a