accessing the u.s. market to raise capital

TRANSCRIPT

Accessing the U.S. Market to Raise Capital

Presentation: March 13, 2013

2

Topics for presentation Capital-raising alternatives, including: • Institutional private placements (Section 4(a)(2) offerings) • Rule 144A offerings • Section 3(a)(2) offerings • Covered bond offerings • Registration process for registered offerings

3

Capital-raising alternatives • Types of issuances

• Senior unsecured debt • Senior secured debt (including covered bonds) • Subordinated debt • Structured debt (e.g., equity-linked and commodity-linked notes) • Hybrid debt / preferred stock • Contingent capital (“coco”) debt • Deposit liabilities

• Issuing entities • Home offices • US branches • Other affiliated entities (e.g., financing SPVs)

4

Financing continuum Private Offering Public Offering

• U.S. private placement (“insurance” or “debt” private placement)

• 144A offering • Tranche from

a EMTN or GMTN

• Standalone 144A

• 144A “program”

• SEC Registration OR • 3(a)(2) Offering

(for banks)

• 3(a)(2) standalone

• 3(a)(2) program

Less Liquid Less time-consuming

Liquid More time-consuming

5

Institutional Private Placements (4(a)(2) Offerings)

6

What is a private placement? •An offering of debt to US investors under Section 4(a)(2) of the US Securities Act of 1933, which permits a “transaction by an issuer not involving any public offering”

•Key factors for qualification include investor sophistication, limited number of offerees and lack of widespread marketing

•Result of qualification: not required to register securities with the US Securities and Exchange Commission (“SEC”) meaning not subject to SEC filing and disclosure rules (other than anti-fraud rules)

•Sometimes referred to as a “Reg D” – which is actually only applicable in the case of a Regulation D filing

7

Who invests in private placements? •Most investors are US financial institutions • Insurance companies are most common •In some cases, non-US (particularly UK) investors may participate •Pool of prospective investors has gotten larger

8

Private placement process •Standardized documentation

• Model X Forms • Most transactions are documented pre-marketing • U.S. governing law (usually NY); English law has become an option • Term sheets vary in detail

• Individual investor decisions – no “agent bank” equivalent • Due diligence – confidentiality preserved given limited number of potential

investors • Bilateral negotiations pre-circle via placement agent(s) • Monitoring of the investment post-closing

9

Role and Benefits of Appointing Specialized Issuer Counsel •Market expectation/desire • Issuer can better control drafting of principal documentation •Provides issuer with objective, current market and legal expectations •Effectively represents the Issuer’s interests during pre-documentation •Smoother, more efficient transaction process

10

Role of Pre-Designated US Investor Counsel •U.S. Special Counsel for Investors

• Experienced U.S. special counsel usually pre-designated by issuer with advice from placement agents and issuer special counsel

• Pre-marketing phase • Reviews term sheet and, sometimes, issuer’s bank facility • Advocates for “the market” on documentation and structural issues • Identifies potential investor resistance points (structure, documentation or

commercial) for the issuer and the placement agent to evaluate before going to the market (“pick your battles”)

•Marketing phase • Responds to inquiries from prospective investors regarding the term sheet, the

proposed Note Purchase Agreement, the issuer’s bank facility and other aspects of the transaction

• Identifies important issues that arose in the pre-marketing documentation phase

•Post-circle phase • Negotiate final changes in documentation (if any)

11

Role of non-US Counsel •Home Jurisdiction Counsel or Other Local Counsel for Investors

• Generally not required if issuer is advised by reputable firms with experience in the cross-border debt markets

12

Laws and Governmental Regulations • Issuer’s jurisdiction of organization

• Withholding taxes and treaties • Registration duties • Legal restrictions on types of securities • Currency and Payment Regulations (if any)

•US • Securities laws

• Securities Act of 1933 • Securities Exchange Act of 1934 • Sarbanes-Oxley Act (not applicable to foreign issuers or their lawyers unless

filing with the SEC)

• Insurance laws and regulations • “Legal investment” requirements • NAIC ratings and reserve requirements

13

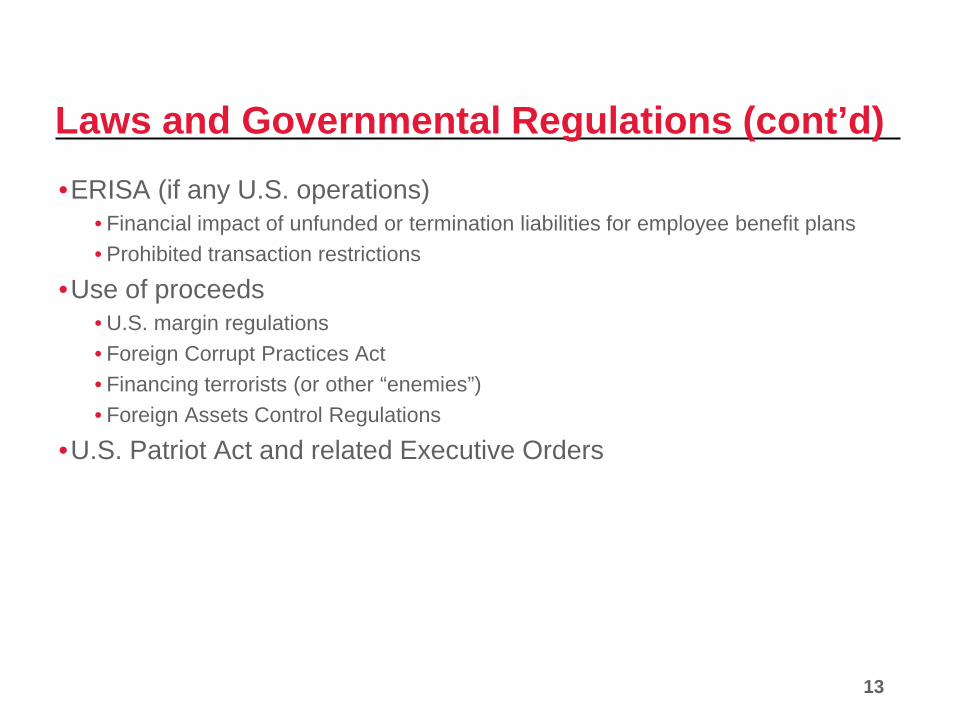

Laws and Governmental Regulations (cont’d) •ERISA (if any U.S. operations)

• Financial impact of unfunded or termination liabilities for employee benefit plans • Prohibited transaction restrictions

•Use of proceeds • U.S. margin regulations • Foreign Corrupt Practices Act • Financing terrorists (or other “enemies”) • Foreign Assets Control Regulations

•U.S. Patriot Act and related Executive Orders

14

Significant covenants •Model X Forms

• Financial information and reasonable access to management and auditors • “Housekeeping” covenants • Maintenance of pari passu ranking of Notes and any guarantees • Change in nature of business • Arms’ length affiliate transactions • Mergers, consolidations, amalgamations

•Other Restrictive Covenants • Financial covenants usually based upon covenant package in existing bank facility

(if any)

•Limitation on “priority debt” (structural subordination) • Subsidiary external borrowings • Secured debt • Sale and leasebacks

15

Significant covenants (cont’d) •Asset dispositions •Emergence of “Most Favored Lender” provisions •Effect of GAAP/IFRS changes

16

Development of Model X Forms •Almost total market acceptance of the Model Forms

• Streamlines documentation process (template) • Investors focus on departures from relevant Model Form and substantive issues

that are outside the form (primarily covenant package)

•Cross-border adaptation of Model Forms • Model X Form adopted in September 2004 • Based upon updated Model Form No. 2 • Surprisingly few changes from domestic version, with particular emphasis on tax-

related issues and certain “hot button topics” such as compliance with new U.S. anti-terrorism regulations

• Easily adaptable to multi-currency transactions and investor swap arrangements re non-USD tranches

• Model Forms X-1 and X-2 adopted in 2006

•Current Ongoing Project to update all Model Forms

17

Key investor objectives •“Buy and Hold”: Notes are expected to be held to maturity •No withholding tax •Secure, predictable return to match portfolio liabilities •“Relationship” investors

18

Transaction chronology •Potential issuer, working with the placement agents, produces an Offering Memorandum (“Memorandum”)

• Memorandum contains Term Sheet and, usually, draft of Note Purchase Agreement

•Deal is marketed to investors, often through a “roadshow” • Issuer and investors agree a final Note Purchase Agreement • Issuer sells Notes to investors

19

Documentation •Note Purchase Agreement •Notes •Guarantee Agreement (Parent) •Guarantee Agreement(s) (Subsidiaries)

20

The Note Purchase Agreement (NPA) •Based on relevant standard “Model X Form” •Model Form created by the Transactions Process Management Committee of the American College of Investment Counsel

21

NPA: Key provisions •Representations and warranties by Issuer, including:

• Due organization/authorization • Financial statements • Compliance with law and regulations (including environmental) • Tax compliance • ERISA compliance • Use of proceeds (important to investors to know where the money is going) • Compliance with anti-terrorism laws (investment cannot legally be made otherwise) • Pari passu

•Purchaser representations (source of funds must also comply with ERISA)

22

NPA: Key provisions (cont’d) • Information requirements

• Financial statements (annual and semi-annual, IFRS or GAAP) • Other reports • Default notices/other notices • Compliance certificate • Inspection rights (Why? Investors have come to expect these of all investments)

•Prepayment • Required prepayments • Prepayment with “make-whole” or “modified make-whole” • Swap breakage (used only if investors are swapping)

•Affirmative Covenants (what issuer will do) • Compliance with law • Insurance, properties • Taxes • Corporate existence • Pari Passu

23

NPA: Key provisions (cont’d) •Negative covenants (what issuer will NOT do)

• Financial covenants (e.g. interest and debt coverage, net worth) • Negative pledge • Sale of assets • Merger or consolidation • Transactions with affiliates • Subsidiary debt

•Events of default • Failure to pay • Covenant breaches • Cross-defaults

•Tax gross-up or interest adjustment • Note payments must be free of withholding tax

24

NPA: Key provisions (cont’d) •Remedies on default •Registration/exchange/substitution of notes •Payments on Notes; Expenses •Amendment and waiver •Governing law and jurisdiction

• Issuer must agree to use New York law and to give New York courts jurisdiction • Appointment of agent for service in New York State • Possible use of English law

•Defined terms (including financial terms)

25

Rule 144A Offerings

26

Why are Rule 144A offerings attractive? • Rule 144A provides a clear safe harbor for offerings to institutional

investors. • Does not require extensive ongoing registration or disclosure

requirements. • Index eligible issuances have good liquidity in the Rule 144A

market.

27

• Rule 144A provides a non-exclusive safe harbor from the registration requirements of Section 5 of the Securities Act for resales of restricted securities to “qualified institutional buyers” (QIBs).

• The rule recognizes that not all investors are in need of the protections of the prospectus requirements of the Securities Act.

• The rule applies to offers made by persons other than the issuer of the securities. (i.e., “resales”).

• The rule applies to securities that are not listed on a U.S. securities exchange or quoted on an automated inter-dealer quotation system.

• A reseller may rely on any applicable exemption from the registration requirements of the Securities Act in connection with the resale of restricted securities (such as Regulation S or Rule 144).

Rule 144A – overview

28

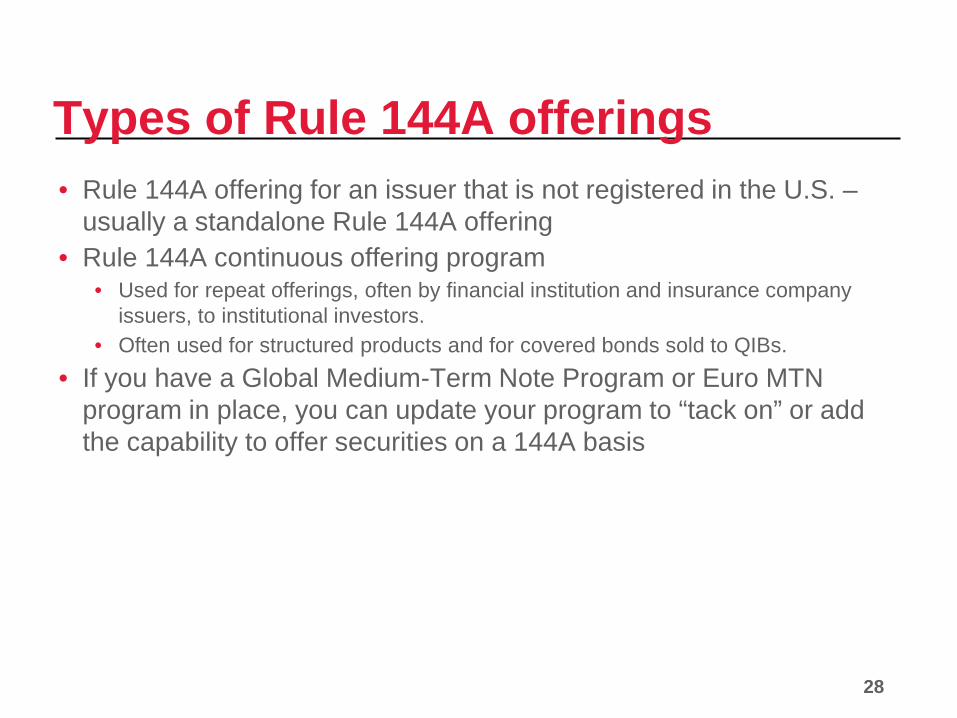

Types of Rule 144A offerings • Rule 144A offering for an issuer that is not registered in the U.S. –

usually a standalone Rule 144A offering • Rule 144A continuous offering program

• Used for repeat offerings, often by financial institution and insurance company issuers, to institutional investors.

• Often used for structured products and for covered bonds sold to QIBs. • If you have a Global Medium-Term Note Program or Euro MTN

program in place, you can update your program to “tack on” or add the capability to offer securities on a 144A basis

29

How are Rule 144A offerings structured? • The issuer initially sells restricted securities to investment bank(s)

as “initial purchasers” in a Section 4(a)(2) or Regulation D private placement.

• The investment bank reoffers and immediately resells the securities to QIBs under Rule 144A.

• Often combined with a Regulation S offering.

30

How are Rule 144A offerings conducted? • Often similar to a registered offering. • “Road show” with a preliminary offering memorandum. • Confirmation of orders with the final offering memorandum.

• The offering memorandum may be delivered electronically. • The purchase agreement is executed at pricing, together with the

delivery of a comfort letter. • Closing on a “T+3” basis, or as otherwise agreed with the investors. • Publicity: generally limited to a Rule 135c compliant press release –

limited information about the offering.

31

Rule 144A Offering Memorandum • May contain similar information to a full “S-1/F-1” prospectus, or may be

much shorter. • If the issuer is a public company, it may incorporate by reference the

issuer’s filings from its home country. • Scope of disclosure (whether included or incorporated by reference) may be

comparable to a public offering, as the initial purchasers/underwriters expect “10b-5” representations from the issuer, and legal opinions from counsel.

• Due diligence by counsel will often be similar to that performed in a public offering.

• For a non-U.S. offering, with a Rule 144A “tranche,” there may be a U.S. “Rule 144A wrapper” attached to the non-U.S. offering document (such as a UKLA or Luxembourg approved prospectus)

32

Documentation for a Rule 144A offering • Offering memorandum or offering circular

• A purchase agreement between the issuer and the initial purchasers/underwriter(s)

• Similar to an underwriting agreement in terms of representations, covenants, closing conditions and indemnities.

• Legal opinions • 10b-5 negative assurance letters • Comfort letters

33

Documentation for a 144A MTN program •Offering memorandum •Program agreement •Agency agreement •Legal opinions, 10b-5 negative assurance letters and comfort letters required at the time program is established and from time to time thereafter

34

The JOBS Act and marketing Rule 144A offerings • The JOBS Act requires the SEC to adopt rules to permit general

solicitations in connection with Rule 144A offerings, provided that sales are made solely to QIBs.

• The SEC issued proposed rules on August 29, 2012 and the comment period ended on October 5, 2012. The SEC has not issued final rules at this time.

• Potential impact: • Use of additional offering modalities to market transactions and disseminate

information. • For example, public websites that describe the offering and press releases.

35

Conditions for Rule 144A offering • Reoffers or resales only to a QIB, or to an offeree or purchaser that

the reseller reasonably believes is a QIB. • Reseller must take steps to ensure that the buyer is aware that the

reseller may rely on Rule 144A in connection with such resale. • The securities reoffered or resold (a) when issued were not of the

same class as securities listed on a U.S. national securities exchange or quoted on a U.S. automated inter-dealer quotation system and (b) are not securities of an open-end investment company, UIT, etc.

• For an issuer that is not an Exchange Act reporting company or exempt from reporting pursuant to Rule 12g3-2(b) under the Exchange Act, the holder and a prospective buyer designated by the holder must have the right to obtain from the issuer, upon the holder’s request, certain reasonably current information.

36

Rule 159: “Time of Sale Information” • Although Rule 159 under the Securities Act is not expressly

applicable to Rule 144A offerings, many investment banks apply the same treatment, in order to help reduce the risk of liability.

• Use of term sheets and offering memoranda supplements, to ensure that all material information is conveyed to investors at the time of pricing.

• Counsel is typically expected to opine as to the “disclosure package,” as in the case of a public offering.

NY2 632073

37

Section 3(a)(2) Offerings

38

Section 3(a)(2) and Offerings by Banks • Section 3(a)(2) of the Securities Act exempts from registration under

the Securities Act any security issued or guaranteed by a bank. • Basis: banks are highly regulated, and provide adequate disclosure

to investors about their finances in the absence of federal securities registration requirements. Banks are also subject to various capital requirements that may increase the likelihood that holders of their debt securities will receive timely payments of principal and interest.

39

What is a “bank”? • Under Section 3(a)(2), the institution must meet both of the following

requirements: • it must be a national bank or any institution supervised by a state banking

commission or similar authority; and • its business must be substantially confined to banking.

• Examples of entities that do not qualify: • Bank holding companies • Finance companies • Investment banks • Foreign banks

40

Guarantees • Another basis for qualification as a bank: securities guaranteed by a

bank. • Not limited to a guaranty in a legal sense, but also includes arrangements in

which the bank agrees to ensure the payment of a security. • The guaranty or assurance of payment, however has to cover the entire

obligation; it cannot be a partial guarantee or promise of payment. • Again, guarantees by foreign banks (other than those of an eligible U.S. branch or

agency) would not qualify for this exception. • The guarantee is a legal requirement to qualify for the exemption; investors will

not be looking to the US branch for payment/credit. Investors will look to the home office.

41

Non-U.S. Banks/U.S. Offices • U.S. branches/agencies of foreign banks are conditionally entitled to

rely on the Section 3(a)(2) exemption. • 1986: the SEC takes the position that a foreign branch/agency will

be deemed to be a “national bank” or a “banking institution organized under the laws of any state” if “the nature and extent of federal and/or state regulation and supervision of that particular branch or agency is substantially equivalent to that applicable to federal or state chartered domestic banks doing business in the same jurisdiction.”

• As a result, U.S. branches/agencies of foreign banks are frequent issuers or guarantors of debt securities in the U.S. Most issuances or guarantees occur through the NY branches of these banks.

42

Examples of Issuing Entities: • U.S. branch as direct issuer: UBS, CS, NAB, CBA and ANZ • U.S. branch as guarantor, headquarters as issuer: BNP, Rabo, SocGen, Svenska

• U.S. branch as guarantor, SPV/Cayman branch as issuer: Fortis, BNP • More banks are using a guarantee structure to allow greater flexibility for use of proceeds.

Which Regulator? • Most U.S. branches of foreign banks have elected the N.Y. State Banking Commissioner as their primary regulator with their secondary regulator the Federal Reserve.

• Some U.S. branches have opted for the Office of the Comptroller of the Currency (“OCC”) as their primary regulator.

Non-U.S. Banks/U.S. Offices (cont’d)

43

OCC Registration/Disclosure • National banks or federally licensed U.S. branches/agencies of foreign

banks regulated by the Office of the Comptroller of the Currency (the “OCC”) are subject to OCC securities offering (Part 16) regulations.

• Part 16 of OCC regulations provides that these banks or banking offices may not offer and sell their securities until a registration statement has been filed and declared effective with the OCC, unless an exemption applies.

• An OCC registration statement is generally comparable in scope and detail to an SEC registration statement; as a result, most bank issuers prefer to rely upon an exemption from the OCC’s registration requirements. Section 16.5 provides a list of exemptions, which includes:

• Regulation D offerings • Rule 144A offerings

44

Part 16.6 of the OCC Regulations • 12 CFR 16.6 provides a separate partial exemption for offerings of

“non-convertible debt” to accredited investors in denominations of $250,000 or more.

• National banks with foreign parents that have shares traded in the US may be able to rely upon this exemption by furnishing the foreign private issuer reports (Forms 20-F, 6-K) filed by foreign issuers.

• Alternatively, Federal branches/agencies may rely on this exemption by furnishing to the OCC parent bank information which is required under Exchange Act Rule 12g3-2(b), and to purchasers the information required under Securities Act Rule 144A(d)(4)(i).

45

Denominations • The 3(a)(2) exemption does not require specific minimum

denominations in order to obtain the exemption. • Many state-chartered branches of foreign banks issue/sell in

denominations of $1000 • However, for a variety of reasons, denominations may at times be

significantly higher than in retail transactions: • Offerings targeted to institutional investors. • Complex securities. • Relationship to 16.6’s requirement of $250,000 minimum denominations.

46

Deposits versus other liabilities • Foreign banks may elect to issue debt instruments in the form of

deposit liabilities as opposed to “pure” debt: • Yankee CDs (US$-denominated deposit liabilities of a foreign bank or its US

branch). • Other types of deposits (e.g., structured deposits).

• What are the legal differences between deposit liabilities and other debt issuances?

• In the case of foreign banks, less than meets the eye. • Foreign banking organization (“FBO”) deposit liabilities are not insured and

generally are issued in large denominations (minimum $100,000 and usually higher).

• For capital equivalency/asset segregation purposes, deposits and non-deposit liabilities generally are treated in the same manner.

47

Blue Sky regulation • Securities issued under Section 3(a)(2) are considered “covered

securities” under Section 18 of the Securities Act. • As a result, blue sky filings are not needed in any state in which the

securities are offered.

48

FINRA requirements • Even though securities offerings under Section 3(a)(2) are exempt

from registration under the Securities Act, public securities offerings conducted by banks must be filed with the Financial Industry Regulatory Authority (“FINRA”) for review under Rule 5110(b)(9), unless an exemption is available.

• Transactions under Section 3(a)(2) must also be reported through FINRA’s Trade Reporting and Compliance Engine (“TRACE”). TRACE eligibility provides greater transparency for investors. Currently, Rule 144A securities are not TRACE reported.

49

Exchange Act reporting • Section 12(i) of the Exchange Act provides that the administration

and enforcement of Exchange Act Sections 12, 13, 14(a), 14(c), 14(d), 14(f), and 16 is vested in the OCC with respect to national banks, the Federal Reserve Board as to member banks of the Federal Reserve System, the FDIC as to all other insured banks, and the OTS as to savings associations.

• As a result, a bank that otherwise would be subject to Exchange Act periodic reporting requirements would submit its reports to the appropriate banking agency, and not to the SEC.

50

Exchange Act reporting (cont’d) • Foreign banks are not Section 3(a)(2) “banks” and therefore are not

subject to Exchange Act Section 12(i), but to the extent they otherwise are required to register under the Exchange Act as issuers, or submit reports as foreign private issuers, they would register and file their reports with the SEC.

• U.S. branches/agencies of foreign banks would not be subject to Exchange Act Section 12(i) requirements solely by virtue of their issuance of debt securities.

51

Section 3(a)(2) offering documentation • The offering documentation for bank notes is similar to that of a

registered offering. • Base offering document, which may be referred to as an “offering

memorandum” or an “offering circular” (instead of a “prospectus”). • The base document is supplemented for a particular offering by one

or more “pricing supplements” and/or “product supplements.” • These offering documents may be supplemented by additional

offering materials, including term sheets and brochures. • A purchase agreement (for a standalone offering), or a program

agreement (for a 3(a)(2) program) • A fiscal and paying agency agreement

52

Comparison of Section 3(a)(2) to Rule 144A Section 3(a)(2) Rule 144A

Required issuer: Need a US state or federal licensed bank as issuer or as guarantor

No specific issuer or guarantor is required

Exemption from the Securities Act:

Section 3(a)(2) Section 4(a)(2) / Rule 144A

FINRA Filing Requirement:

Subject to filing requirement and payment of filing fee Not subject to FINRA filing

Blue Sky: Generally exempt from blue sky regulation Generally exempt from blue sky regulation

Listing on an exchange:

May be listed if issued in compliance with Part 16.6 No

“Restricted” No; considered “public” and therefore eligible for bond indices, TRACE reporting

Yes

53

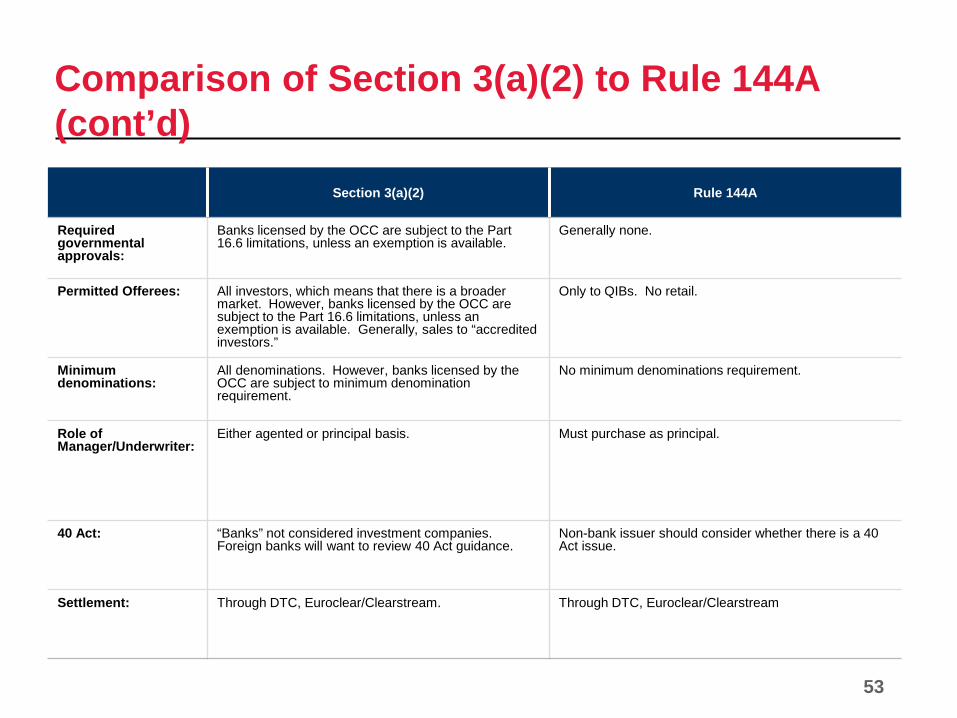

Comparison of Section 3(a)(2) to Rule 144A (cont’d)

Section 3(a)(2) Rule 144A

Required governmental approvals:

Banks licensed by the OCC are subject to the Part 16.6 limitations, unless an exemption is available.

Generally none.

Permitted Offerees: All investors, which means that there is a broader market. However, banks licensed by the OCC are subject to the Part 16.6 limitations, unless an exemption is available. Generally, sales to “accredited investors.”

Only to QIBs. No retail.

Minimum denominations:

All denominations. However, banks licensed by the OCC are subject to minimum denomination requirement.

No minimum denominations requirement.

Role of Manager/Underwriter:

Either agented or principal basis. Must purchase as principal.

40 Act: “Banks” not considered investment companies. Foreign banks will want to review 40 Act guidance.

Non-bank issuer should consider whether there is a 40 Act issue.

Settlement: Through DTC, Euroclear/Clearstream. Through DTC, Euroclear/Clearstream

54

Note: Shading denotes Yankee issuance; list is comprehensive but may not capture every 3(a)(2) issuance in 2011-13; 3(a)(2) issuances are unsecured

3(a)(2) Issuances (2011- 2013) Pricing Date Issuer Ratings (M/S) Coupon (%) Tranche Value (US$mm) Structure Maturity Date Deal Nationality

1/7/2013 1/7/2013

11/8/2012

Intesa SanPaolo Spa (New York) Intesa SanPaolo Spa (New York) American Express Centurion Bank

Baa2/BBB+ Baa2/BBB+

A2/A-

3.125 3.875 0.875

2,000 1,500 750

3YR FXD 5YR FXD 3YR FXD

1/15/2016 1/16/2018 11/13/2015

Italy Italy US

11/8/2012 American Express Centurion Bank A2/A- 3mL+45bp 550 3YR FRN 11/13/2015 US 11/2/2012 Rabobank Nederland Aa2/AA- 3.950 1,500 10YR FXD 11/9/2022 Netherlands 11/2/2012 National Bank of Canada Aa2/A 1.450 750 5YR FXD 11/7/2017 Canada

10/17/2012 PNC Bank NA A3/A- 2.700 1,000 10YR FXD 11/1/2022 US 9/4/2012 Australia & New Zealand Banking Group (New York) Aa2/AA- 1.875 750 5YR FXD 10/6/2017 Australia

8/10/2012 UBS AG (Stamford) -/BBB- 7.625 2,000 10YR FXD 8/17/20222 Switzerland 8/8/2012 National Australia Bank Ltd Aa2/AA- 2.000 13 5YR FXD 8/10/2017 Australia

7/26/2012 National Australia Bank (New York) Aa2/AA- 3mL+113bp 500 3YR FRN 8/7/2015 Australia 7/26/2012 National Australia Bank (New York) Aa2/AA- 1.600 1,250 3YR FXD 8/7/2015 Australia 7/10/2012 Sumitomo Mitsui Banking Corp Aa3/A+ 1.350 1,000 3YR FXD 7/18/2015 Japan 7/10/2012 Sumitomo Mitsui Banking Corp Aa3/A+ 1.800 1,250 5YR FXD 7/18/2017 Japan 7/10/2012 Sumitomo Mitsui Banking Corp Aa3/A+ 3.200 750 10YR FXD 7/18/2022 Japan

6/6/2012 TCF National Bank Baa1/BBB- 6.250 110 10YR FXD 6/8/2022 US 3/28/2012 Svenska Handelsbanken AB Aa3/AA- 2.875 1,250 5YR FXD 4/4/2017 Sweden 3/16/2012 National Australia Bank Ltd Aa2/AA- 3mL+1bp 175 3YR FRN 3/20/2015 Australia

3/5/2012 Commonwealth Bank of Australia (New York) Aa2/AA- 1.950 2,000 3YR FXD 3/16/2015 Australia 3/1/2012 National Australia Bank (New York) Aa2/AA- 2.000 1,500 3YR FXD 3/9/2015 Australia 3/1/2012 National Australia Bank (New York) Aa2/AA- 2.750 1,000 5YR FXD 3/9/2017 Australia 2/1/2012 Rabobank Nederland Aa2/AA- 3.875 3,000 10YR FXD 2/8/2022 Netherlands

1/17/2012 First Republic Bank Baa3/BBB 6.700 200 Perpetual Perpetual US 1/11/2012 Rabobank Nederland Aa2/AA- 3.375 2,500 5YR FXD 1/19/2017 Netherlands 7/20/2011 Rabobank Nederland Aa2/AA- 3mL+20bp 360 2YR FRN 7/25/2013 Netherlands

7/5/2011 Svenska Handelsbanken AB Aa3/AA- 3.125 1,250 5YR FXD 7/12/2016 Sweden 5/24/2011 BNP Paribas SA A2/A+ 3.250 100 4YR FXD 3/11/2015 France

4/20/211 BNP Paribas SA A2/A+ 3.250 150 4YR FXD 3/11/2015 France 4/14/2011 Rabobank Nederland Aa2/AA- 3mL+35bp 350 3YR FRN 4/14/2014 Netherlands

4/6/2011 BNP Paribas (New York) A2/A+ 5.000 1,000 10YR FXD 1/15/2021 France 3/22/2011 UBS AG (Stamford) A2/A 3mL+40bp 300 2YR FRN 9/25/2012 Switzerland 2/17/2011 BNP Paribas SA A2/A+ 3.250 100 4YR FXD 3/11/2015 France 1/25/2011 UBS AG (Stamford) A2/A 2.250 1,000 3YR FXD 1/28/2014 Switzerland 1/25/2011 UBS AG (Stamford) A2/A 3mL+100bp 750 3YR FRN 1/28/2014 Switzerland 1/12/2011 BNP Paribas (New York) A2/A+ 5.000 2,000 10YR FXD 1/15/2021 France

1/4/2011 Rabobank Nederland Aa2/AA- 1.850 1,250 3YR FXD 1/10/2014 Netherlands 1/4/2011 Rabobank Nederland Aa2/AA- 4.500 1,500 10YR FXD 1/11/2021 Netherlands

55

Specific Offering Types

56

Foreign bank issuances of covered bonds

• Foreign banks issuing into the U.S. market have been relying on their domestic covered bond framework and have been using cover pool assets that are foreign (not in the U.S.).

• Issuances into the U.S. have been structured as program issuances (or syndicated takedowns) conducted on an exempt basis, that means that the foreign issuer is relying on exemptions from the U.S. securities laws requiring registration of public offerings of securities.

• To date, only one issuer (RBC) has registered a covered bond with the SEC. It is expected that other foreign issuers will follow suit.

• As a result, offerings have been targeted at U.S. institutional investors and generally conducted in reliance on Rule 144A.

57

Foreign bank issuances of capital securities

• A number of jurisdictions within Europe have provided guidance to their financial institutions relating to the type of instruments eligible for Tier 1 or Tier 2 treatment, including contingent capital.

• Issuances into the U.S. of contingent capital securities have been structured as 144A or 3(a)(2) offerings into the U.S.

• U.S. investors have demonstrated interest in contingent capital instruments, as well as in Tier 2 instruments.

58

Issuances of structured securities

• Many foreign banks establish issuance programs (either relying on Rule 144A or 3(a)(2)) that permit them to access U.S. investors to offer structured products

• Structured products may include equity-linked, index-linked, interest rate-linked, commodity-linked or currency-linked notes

• Some foreign banks also issue “Yankee CDs” (or certificates of deposit) from their U.S. branches; Yankee CDs may (or may not) be subject to FDIC insurance

59

Registered Offerings: Non-U.S. Issuers Offer

Securities as “Foreign Private Issuers”

60

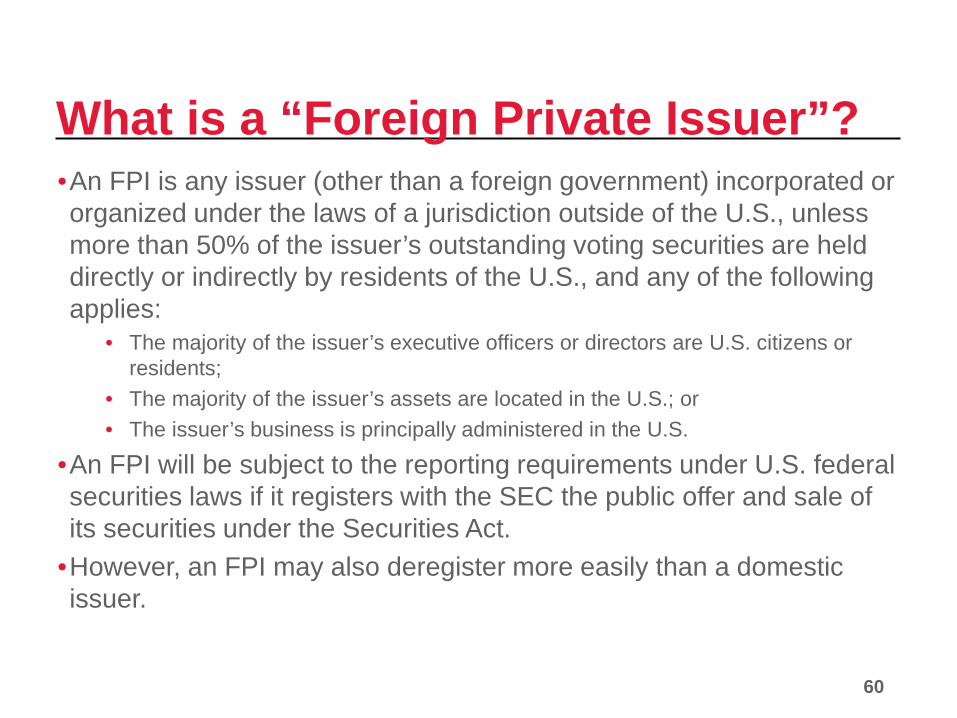

What is a “Foreign Private Issuer”? •An FPI is any issuer (other than a foreign government) incorporated or organized under the laws of a jurisdiction outside of the U.S., unless more than 50% of the issuer’s outstanding voting securities are held directly or indirectly by residents of the U.S., and any of the following applies:

• The majority of the issuer’s executive officers or directors are U.S. citizens or residents;

• The majority of the issuer’s assets are located in the U.S.; or • The issuer’s business is principally administered in the U.S.

•An FPI will be subject to the reporting requirements under U.S. federal securities laws if it registers with the SEC the public offer and sale of its securities under the Securities Act.

•However, an FPI may also deregister more easily than a domestic issuer.

61

Benefits available to FPIs • An FPI may exit (or deregister) the U.S. reporting regime more

easily than a U.S. issuer. • Quarterly reports: An FPI is not required to file quarterly reports –

submits its non-U.S. reports under cover of Form 6-K. • Proxies: An FPI is not required to file proxy statements. • Ownership reporting: No Section 16 (“short-swing” profits) reporting. • Governance: An FPI may choose to rely on certain home-country

practices. • XBRL: Temporary XBRL relief was previously granted to FPIs. • Internal controls: Annual internal control reporting • Executive compensation: As an FPI, certain of the more onerous

executive compensation disclosure requirements are not applicable • IFRS without GAAP reconciliation • 12g3-2(b) exemption

62

Registration Process

63

Which registration form should be used? • Once an FPI has been subject to the U.S. reporting requirements for

at least 12 calendar months, it may use Form F-3 to offer securities publicly in the United States.

• Form F-3 is a short-form registration statement (analogous to Form S-3 for U.S. domestic issuers) and may be used by an FPI if the FPI meets both the form’s registrant requirements and the applicable transaction requirements.

• Form F-3 permits an FPI to disclose minimal information in the prospectus included in the Form F-3 by incorporating by reference the more extensive disclosures already filed with the SEC under the Exchange Act, primarily in the FPI’s most recent Annual Report on Form 20-F and its Forms 6-K.

• Form F-3’s filed by WKSI’s are automatically effective, without SEC review. • Shelf registration statements on Form F-3 are typically not reviewed.

64

What is a WKSI? • A “well-known seasoned issuer” (“WKSI”) is an issuer that has at least $700 million of common equity held by non-affiliates or (b) issued $1 billion of non-convertible securities during the past three years.

• Can be a U.S. issuer or a non-U.S. issuer. • Can be a subsidiary of a company that is a WKSI. • Subject to certain disqualifications.

65

Automatic Shelf Registration Statements • Automatic, immediate effectiveness, without SEC review • Registration of unspecified amounts of specified classes of securities • Presumption of proper form

• Process and consequences of notification by Staff if SEC objects to use of form • Impacts form of underwriting agreement, opinions and other offering documents.

• Omission of information from base prospectus • Identification of primary or secondary offering • Description of securities • Names of selling security holders • Plan of distribution

• Mechanics for including omitted information • Limited requirements for post-effective amendments

• Pay-as-you-go registration fees as an option • Unique to automatic shelf registrations • “In whole or in part” • Practical application in MTN programs and other special situations

66

Ongoing Reporting

Obligations and Governance

67

Ongoing reporting obligations • An FPI that has registered securities under Section 12(b) or 12(g) of

the Exchange Act or is required to file under Section 15(d) of the Exchange Act (because it has recently completed a registered offering) is obligated to file the following Exchange Act reports with the SEC: • Annual Report on Form 20-F • Reports on Form 6-K

68

Annual Report on Form 20-F • The information required to be disclosed in an Annual Report on

Form 20-F includes, but is not limited to, the following: • Operating results; • Liquidity and capital resources; • Trend information; • Off-balance sheet arrangements; • Consolidated financial statements and other financial information; • Significant business changes; • Selected financial data; • Risk factors; • History and development of the FPI; • Business overview; and • Organizational structure.

69

Reports on Form 6-K • An FPI must also “furnish” reports on Form 6-K to the SEC from time

to time. • Generally, a Form 6-K contains information that is material to an

investment decision in the securities of an FPI. • May include press releases, securityholder reports and other materials that an

FPI publishes in its home-country in accordance with home-market law or custom, as well as any other information that the FPI may want to make publicly available.

• Reports on Form 6-K generally take the place of Quarterly Reports on Form 10-Q (which include financial reports) and Current Reports on Form 8-K (which include disclosure on material events) that U.S. domestic issuers are required to file.

• For many of the larger FPIs, the Forms 6-K that are filed with the SEC generally include similar types of information and are filed with the same frequency as Forms 10-Q and 8-K that are filed by U.S. domestic issuers.

• The disclosures are prepared in accordance with “home country” practice.

70

Sarbanes-Oxley requirements • Section 302 of Sarbanes-Oxley requires certifications by an FPI’s

CEO/CFO regarding the effectiveness of the FPI’s disclosure controls and procedures, the completeness and accuracy of the FPI’s reports filed under Section 13(a) and 15(d) of the Securities Act, and any deficiencies in, and material changes to, the FPI’s internal control over financial reporting.

• Section 302 reporting begins once the FPI is an SEC registrant. • These certifications must be included in the FPI’s Form 20-F. • Other reports filed or furnished by the FPI, such as reports on Form 6-K, are not

subject to the certification requirements.

• Section 404 of Sarbanes-Oxley requires an annual report by both management and external auditors regarding the effectiveness of the company’s internal controls over financial reporting.

• Section 404 reporting begins with the second annual filing with the SEC. • FPIs that are “non-accelerated” filers do not have to provide the auditor’s

attestation.

71

• “Disclosure controls and procedures” are controls and other procedures designed to ensure that the information required to be disclosed in the reports filed under the Exchange Act, on a timely basis, is recorded, processed, summarized and reported.

• Disclosure controls and procedures include, but are not limited to, controls and procedures designed to ensure that information required to be disclosed by a company in its Exchange Act reports is appropriately accumulated and communicated to the company’s management, including its principal executive and financial officers, to allow timely decisions regarding required disclosure.

• Important to have an “up the chain” process of reporting from lower managers to CEO and CFO.

Disclosure controls and procedures

72

Liability Concerns

73

Securities liability – Rule 144A and Section 3(a)(2) • Neither Rule 144A offerings or securities offerings of, or guaranteed

by, a bank under Section 3(a)(2) are subject to the civil liability provisions under Section 11 and Section 12(a)(2) of the Securities Act.

• Rule 144A offerings and offerings under Section 3(a)(2) are subject to Section 10(b) of the Exchange Act and the anti-fraud provisions of Rule 10b-5 of the Exchange Act.

• Impact on offering documents, and use of offering circulars to convey material information and risk factors.

74

Liability under the Exchange Act •Rule 10b-5 applies to registered and exempt offerings. •Rule 10b-5 of the Exchange Act prohibits:

• The use of any device, scheme, or artifice to defraud; • The making of any untrue statement of a material fact or the omission of a material

fact necessary to make the statements made not misleading; or • The engaging in any act, practice, or course of business that would operate to

deceive any person in connection with the purchase or sale of any securities.

•To bring a successful cause of action under Rule 10b-5, the plaintiff must prove:

• That there was a misrepresentation or failure to disclose a material fact, • That was made in connection with plaintiffs’ purchase or sale of a security, • That defendants acted with “scienter,” or the intent or knowledge of the violation, • That plaintiffs “relied” on defendants’ misrepresentation or omission, and • That such misrepresentation or omission caused plaintiffs’ damages.

75

Section 11 liability – registered offerings • Directors and officers of an FPI who sign a registration statement

filed in connection with a securities offering are subject to the liability provisions of Section 11 of the Securities Act.

• Section 11 of the Securities Act creates civil liability for misstatements or omissions in a registration statement at the time it became effective.

• Any person that acquired a security registered under a registration statement, and did not have knowledge of the misstatement or omission at the time of the acquisition of the security, can bring suit against:

• Every person who signed the registration statement, including the FPI; • Every director of the FPI at the time of the filing of the registration statement,

whether or not such director signed the registration statement; and • Experts who consent to such status, but only with respect to those sections of

the registration statement (e.g., auditors).

76

Section 12 liability – registered offerings • Section 12 of the Securities Act assigns liability to any person who

offers or sells a security in violation of Section 5 of the Securities Act (pursuant to Section 12(a)(1)), or by means of a prospectus or oral communication that includes a misstatement or omission of material fact (pursuant to Section 12(a)(2)).

• Plaintiffs bringing a claim under Section 12 are afforded rescissory relief, if they still have ownership of the securities, or damages, if they no longer own the security.

• No action under Section 12(a)(1) may be brought more than three years after the bona fide public offering of a security, or, in the case of Section 12(a)(2), more than three years after the actual sale of a security.