acca p2 int-uk interim assessment - questions 2014

DESCRIPTION

2014TRANSCRIPT

Date sent to marker

Date received from marker

Date returned to student

Student's overall mark

INTERIM ASSESSMENT SCRIPT SUBMISSION FORM Script marking is only available to Classroom, Live Online and Distance Learning students enrolled on appropriate Kaplan courses.

Name: …………….…………………………………………..………………..…..……….….…

Address: …………………………………………………………………………………..….......

………………………………………………………..……………………………………..…......... ………………………………………………………............……………………..................

Kaplan Student Number: …………………………………………………………….....…

Your email address:

ACCA – Paper P2 Corporate Reporting

2014 Interim Assessment

Instructions

• Please complete your personal details above. • All scripts should ideally be submitted to your Kaplan centre for marking via email to help speed up the marking

process. Please scan this form and your answer script in a single PDF and email it to your Kaplan centre. • Alternatively you may post your script to us. If so, please use the correct Royal Mail tariff (large letter). • Classroom students may submit scripts to their local centre in person. You will be provided with the dated receipt below which you should retain as proof of submission.

Note: If you are a sponsored student, your result will form part of the report to your employer.

Office use

Centre

Date received

Marker’s initials

Receipt – only issued if script submitted by classroom student in person to Kaplan centre:

--------------------------------------------------------------------------------------------------------------------------------------

Name: ....................................................................... Received by: ............................................................ Script: ....................................................................... Date: ......................................................................

Marking Report

Notice to Markers

1 When commenting about the script performance, please ensure on individual questions and on overall assessment your comments cover areas of examination technique including:

• Time management

• Handwriting • Presentation and layout

• Use of English

• Points clearly and concisely made

• Relevance of answers to question

• Coverage and depth of answer

• Accuracy of calculations

• Calculations cross-referenced to workings

• All parts of the requirement attempted

• Length of answers equates to marks available

• Read the question carefully

2 For each question, please provide suitable constructive comments

Question Number

General Comments Exam Technique Comments

ACCA INTERIM ASSESSMENT

Corporate Reporting 2014

Time allowed

Reading time: 15 minutes

Writing time: 3 hours

This paper is divided into two sections

Section A This question is compulsory and MUST be answered

Section B Answer BOTH questions

Do not open this paper until instructed by the supervisor This question paper must not be removed from the examination hall

Kaplan Publishing/Kaplan Financial

Pape

r P2

(IN

T &

UK)

ACCA P2 ( INT & UK): CORPORATE REPORTING

2 KAPLAN PUBLISHING

© Kaplan Financial Limited, 2014

The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited and all other Kaplan group companies expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, and consequential or otherwise arising in relation to the use of such materials.

All rights reserved. No part of this examination may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without prior permission from Kaplan Publishing.

INTERIM ASSESSMENT: QUESTIONS

KAPLAN PUBLISHING 3

SECTION A

This question is compulsory and MUST be answered

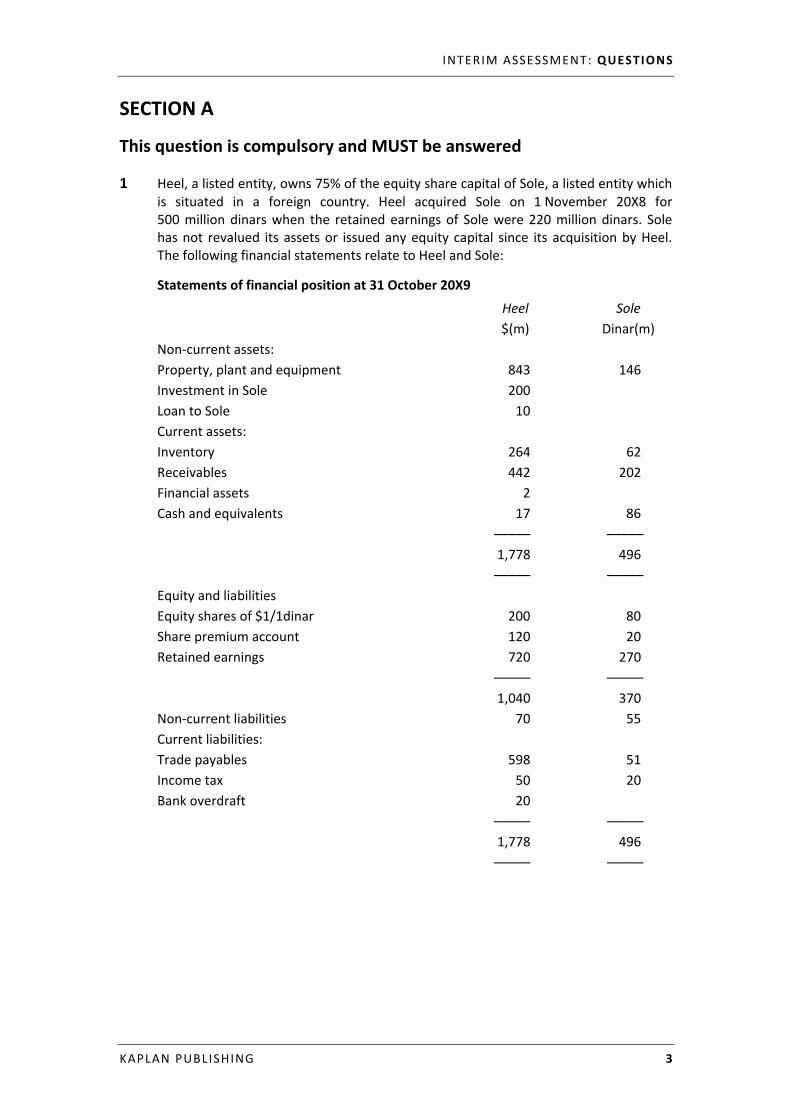

1 Heel, a listed entity, owns 75% of the equity share capital of Sole, a listed entity which is situated in a foreign country. Heel acquired Sole on 1 November 20X8 for 500 million dinars when the retained earnings of Sole were 220 million dinars. Sole has not revalued its assets or issued any equity capital since its acquisition by Heel. The following financial statements relate to Heel and Sole:

Statements of financial position at 31 October 20X9

Heel Sole $(m) Dinar(m) Non-current assets: Property, plant and equipment 843 146 Investment in Sole 200 Loan to Sole 10 Current assets: Inventory 264 62 Receivables 442 202 Financial assets 2 Cash and equivalents 17 86 ––––– ––––– 1,778 496 ––––– ––––– Equity and liabilities Equity shares of $1/1dinar 200 80 Share premium account 120 20 Retained earnings 720 270 ––––– ––––– 1,040 370 Non-current liabilities 70 55 Current liabilities: Trade payables 598 51 Income tax 50 20 Bank overdraft 20 ––––– ––––– 1,778 496 ––––– –––––

ACCA P2 ( INT & UK): CORPORATE REPORTING

4 KAPLAN PUBLISHING

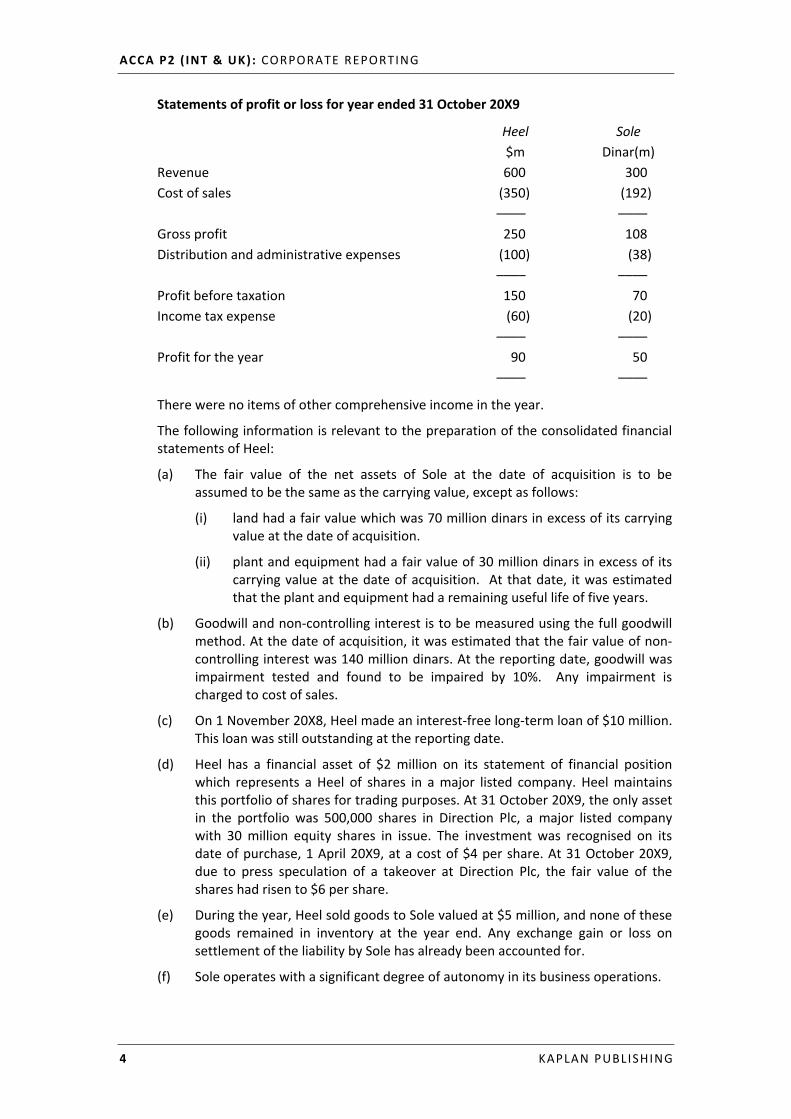

Statements of profit or loss for year ended 31 October 20X9

Heel Sole $m Dinar(m) Revenue 600 300 Cost of sales (350) (192) –––– –––– Gross profit 250 108 Distribution and administrative expenses (100) (38) –––– –––– Profit before taxation 150 70 Income tax expense (60) (20) –––– –––– Profit for the year 90 50 –––– ––––

There were no items of other comprehensive income in the year.

The following information is relevant to the preparation of the consolidated financial statements of Heel:

(a) The fair value of the net assets of Sole at the date of acquisition is to be assumed to be the same as the carrying value, except as follows:

(i) land had a fair value which was 70 million dinars in excess of its carrying value at the date of acquisition.

(ii) plant and equipment had a fair value of 30 million dinars in excess of its carrying value at the date of acquisition. At that date, it was estimated that the plant and equipment had a remaining useful life of five years.

(b) Goodwill and non-controlling interest is to be measured using the full goodwill method. At the date of acquisition, it was estimated that the fair value of non-controlling interest was 140 million dinars. At the reporting date, goodwill was impairment tested and found to be impaired by 10%. Any impairment is charged to cost of sales.

(c) On 1 November 20X8, Heel made an interest-free long-term loan of $10 million. This loan was still outstanding at the reporting date.

(d) Heel has a financial asset of $2 million on its statement of financial position which represents a Heel of shares in a major listed company. Heel maintains this portfolio of shares for trading purposes. At 31 October 20X9, the only asset in the portfolio was 500,000 shares in Direction Plc, a major listed company with 30 million equity shares in issue. The investment was recognised on its date of purchase, 1 April 20X9, at a cost of $4 per share. At 31 October 20X9, due to press speculation of a takeover at Direction Plc, the fair value of the shares had risen to $6 per share.

(e) During the year, Heel sold goods to Sole valued at $5 million, and none of these goods remained in inventory at the year end. Any exchange gain or loss on settlement of the liability by Sole has already been accounted for.

(f) Sole operates with a significant degree of autonomy in its business operations.

INTERIM ASSESSMENT: QUESTIONS

KAPLAN PUBLISHING 5

(g) The following exchange rates are relevant to the financial statements:

Dinars to $31 October/1 November 20X8 2.5 31 October 20X9 2.0 Average rate for year to 31 October 20X9 2.3

Required:

(a) Prepare a consolidated statement of profit or loss and other comprehensive income for the Heel Group for the year ended 31 October 20X9, together with a consolidated statement of financial position at that date in accordance with International Financial Reporting Standards. (35 marks)

(b) (i) Explain the accounting treatment in the group accounts when the parent buys additional shares in a subsidiary. (3 marks)

(ii) Explain the accounting treatment in the group accounts when the parent sells shares in a subsidiary without losing control. (3 marks)

(iii) Explain the accounting treatment in the group accounts in the event that the sale of shares in a subsidiary during the year does result in a loss of control and is regarded as a discontinued operation. (3 marks)

(c) Explain the legal and ethical considerations of incorrectly accounting for the sale or purchase of shares in a subsidiary in the group accounts. (6 marks)

(Total: 50 marks)

ACCA P2 ( INT & UK): CORPORATE REPORTING

6 KAPLAN PUBLISHING

SECTION B

Answer BOTH questions

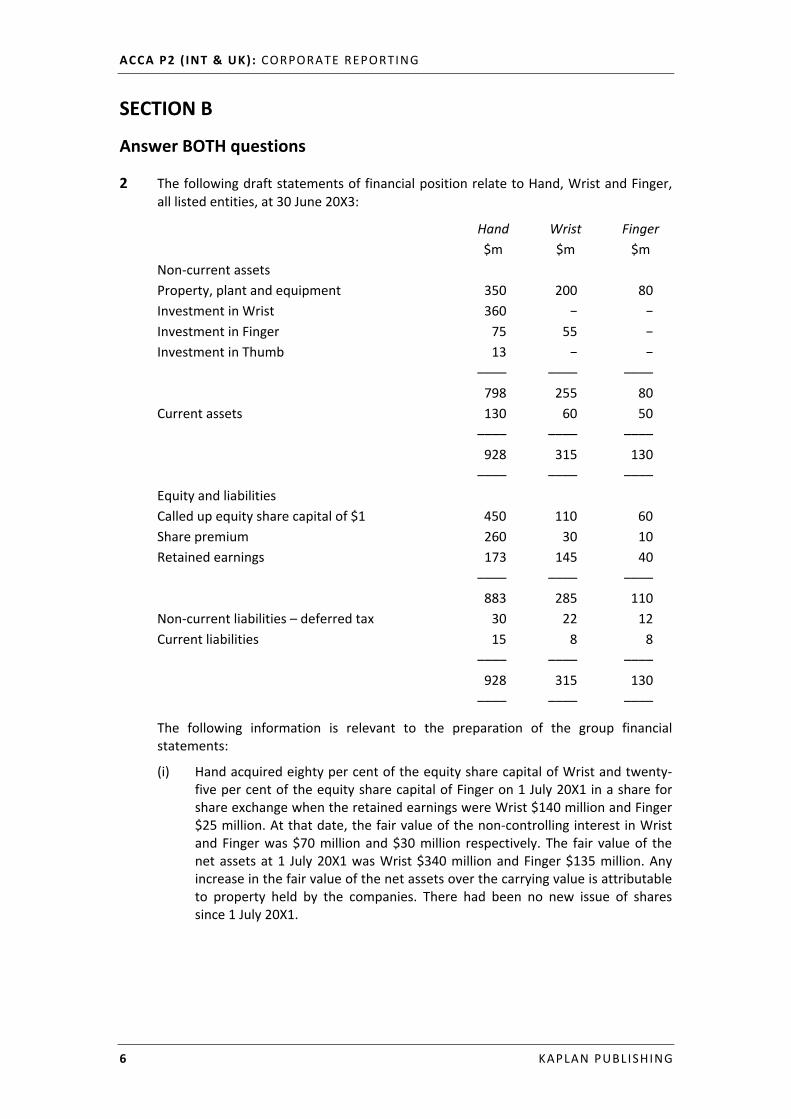

2 The following draft statements of financial position relate to Hand, Wrist and Finger, all listed entities, at 30 June 20X3:

Hand Wrist Finger $m $m $m

Non-current assets Property, plant and equipment 350 200 80 Investment in Wrist 360 − − Investment in Finger 75 55 − Investment in Thumb 13 − − –––– –––– –––– 798 255 80 Current assets 130 60 50 –––– –––– –––– 928 315 130 –––– –––– –––– Equity and liabilities Called up equity share capital of $1 450 110 60 Share premium 260 30 10 Retained earnings 173 145 40 –––– –––– –––– 883 285 110 Non-current liabilities – deferred tax 30 22 12 Current liabilities 15 8 8 –––– –––– –––– 928 315 130 –––– –––– ––––

The following information is relevant to the preparation of the group financial statements:

(i) Hand acquired eighty per cent of the equity share capital of Wrist and twenty-five per cent of the equity share capital of Finger on 1 July 20X1 in a share for share exchange when the retained earnings were Wrist $140 million and Finger $25 million. At that date, the fair value of the non-controlling interest in Wrist and Finger was $70 million and $30 million respectively. The fair value of the net assets at 1 July 20X1 was Wrist $340 million and Finger $135 million. Any increase in the fair value of the net assets over the carrying value is attributable to property held by the companies. There had been no new issue of shares since 1 July 20X1.

INTERIM ASSESSMENT: QUESTIONS

KAPLAN PUBLISHING 7

(ii) Wrist had acquired a sixty-five per cent interest in Finger five years earlier for a consideration of $55 million when the retained earnings of Finger were $13 million. The fair value of the net assets of Finger at that date was $90 million with the increase in fair value attributable to property held by the companies. Property is depreciated within the group at five per cent per annum.

(iii) Hand purchased a thirty-five per cent interest in Thumb, an incorporated entity on 1 July 20X2. The only asset of Thumb is a portfolio of investments which is held for trading purposes. The stake in Thumb was purchased for cash for $13 million. The carrying value of the net assets of Thumb on 1 July 20X2 was $20 million and their fair value was $22 million. On 30 June 20X3, the fair value of the net assets was $28 million. Hand exercises significant influence over Thumb. Thumb values the portfolio on a ‘mark to market’ basis.

(iv) Wrist has included a brand name in its property, plant and equipment at a cost of $10 million. The brand earnings can be separately identified and could be sold separately from the rest of the business. The fair value of the brand at 30 June 20X3 was $6 million. The fair value of the brand at the time of Wrist’s acquisition by Hand was $10 million.

(v) The policy of Hand is to measure goodwill using the full goodwill method. At the date of acquisition, the fair value of the non-controlling interest in Wrist and Finger (both direct and indirect) was $70 million and $30 million respectively.

(vi) During the year to 30 June 20X3, Finger supplied goods to Hand at a sales value of $20 million at a mark-up of twenty-five per cent. At the reporting date, eighty per cent of the goods remained in inventory. Hand had an amount due to Finger of $3 million at the reporting date.

Required:

Prepare the consolidated statement of financial position of the Hand Group at 30 June 20X3 in accordance with International Financial Reporting Standards. (25 marks)

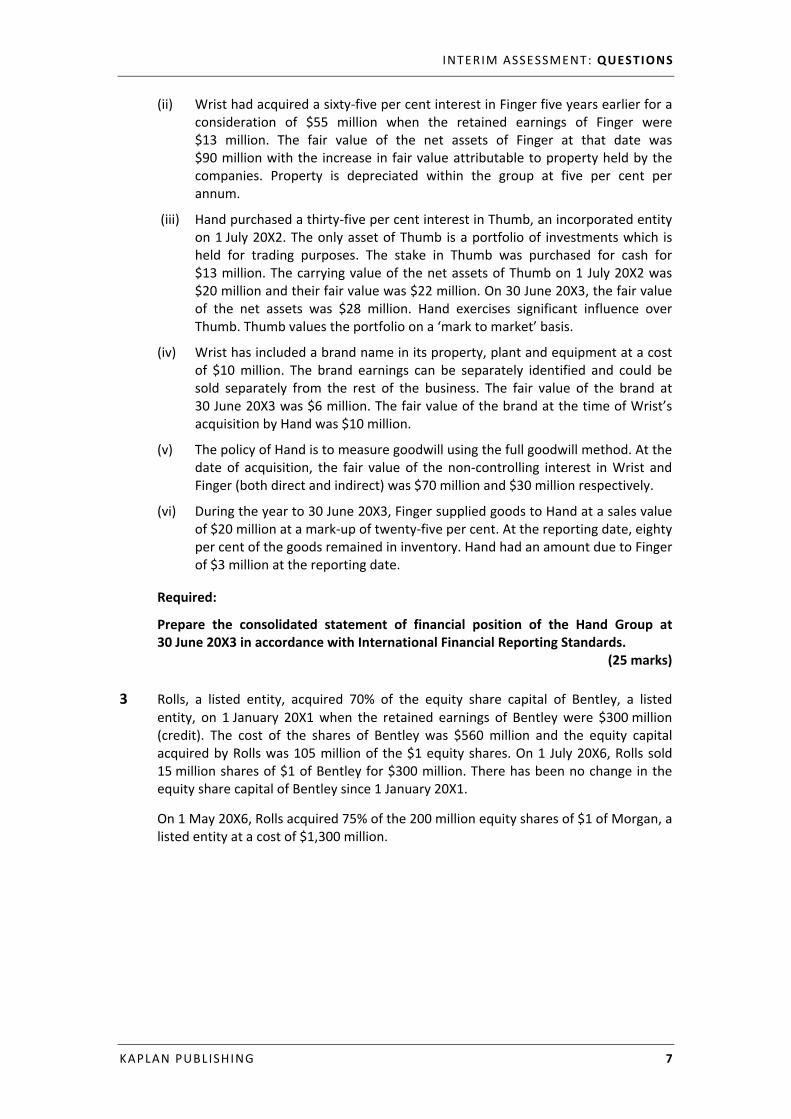

3 Rolls, a listed entity, acquired 70% of the equity share capital of Bentley, a listed entity, on 1 January 20X1 when the retained earnings of Bentley were $300 million (credit). The cost of the shares of Bentley was $560 million and the equity capital acquired by Rolls was 105 million of the $1 equity shares. On 1 July 20X6, Rolls sold 15 million shares of $1 of Bentley for $300 million. There has been no change in the equity share capital of Bentley since 1 January 20X1.

On 1 May 20X6, Rolls acquired 75% of the 200 million equity shares of $1 of Morgan, a listed entity at a cost of $1,300 million.

ACCA P2 ( INT & UK): CORPORATE REPORTING

8 KAPLAN PUBLISHING

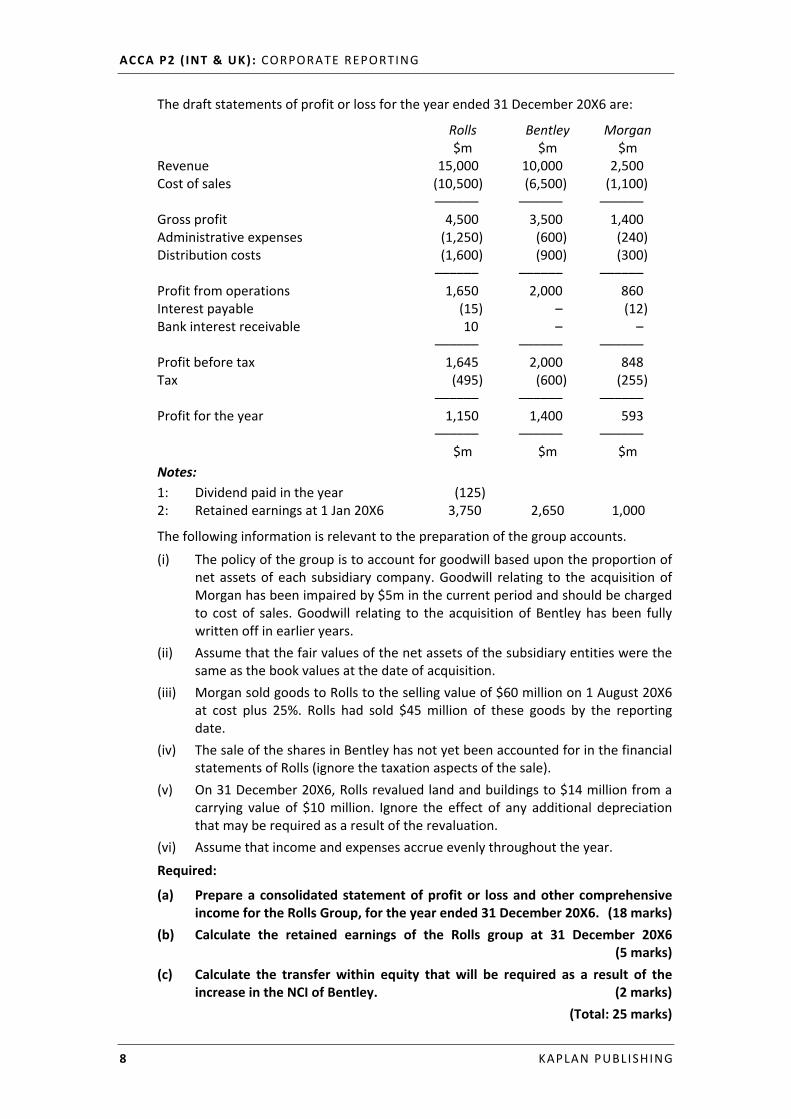

The draft statements of profit or loss for the year ended 31 December 20X6 are:

Rolls Bentley Morgan $m $m $m

Revenue 15,000 10,000 2,500 Cost of sales (10,500) (6,500) (1,100) –––––– –––––– –––––– Gross profit 4,500 3,500 1,400 Administrative expenses (1,250) (600) (240) Distribution costs (1,600) (900) (300) –––––– –––––– –––––– Profit from operations 1,650 2,000 860 Interest payable (15) – (12) Bank interest receivable 10 – – –––––– –––––– –––––– Profit before tax 1,645 2,000 848 Tax (495) (600) (255) –––––– –––––– –––––– Profit for the year 1,150 1,400 593 –––––– –––––– ––––––

$m $m $m Notes: 1: Dividend paid in the year (125) 2: Retained earnings at 1 Jan 20X6 3,750 2,650 1,000

The following information is relevant to the preparation of the group accounts.

(i) The policy of the group is to account for goodwill based upon the proportion of net assets of each subsidiary company. Goodwill relating to the acquisition of Morgan has been impaired by $5m in the current period and should be charged to cost of sales. Goodwill relating to the acquisition of Bentley has been fully written off in earlier years.

(ii) Assume that the fair values of the net assets of the subsidiary entities were the same as the book values at the date of acquisition.

(iii) Morgan sold goods to Rolls to the selling value of $60 million on 1 August 20X6 at cost plus 25%. Rolls had sold $45 million of these goods by the reporting date.

(iv) The sale of the shares in Bentley has not yet been accounted for in the financial statements of Rolls (ignore the taxation aspects of the sale).

(v) On 31 December 20X6, Rolls revalued land and buildings to $14 million from a carrying value of $10 million. Ignore the effect of any additional depreciation that may be required as a result of the revaluation.

(vi) Assume that income and expenses accrue evenly throughout the year.

Required:

(a) Prepare a consolidated statement of profit or loss and other comprehensive income for the Rolls Group, for the year ended 31 December 20X6. (18 marks)

(b) Calculate the retained earnings of the Rolls group at 31 December 20X6 (5 marks)

(c) Calculate the transfer within equity that will be required as a result of the increase in the NCI of Bentley. (2 marks)

(Total: 25 marks)