acca p2 clmn december 2012 exam current issues presenter – tom clendon 1

TRANSCRIPT

ACCA P2 CLMN December 2012 exam

Current issues

Presenter – Tom Clendon1

Format – 15 minutes & 3 hours

• Section A - No choice - 50 marks • 35 marks group numbers• 25 marks of Para 1 = sub 1, Para 2 = sub 2• 10 marks accounting adjustment (FI)• Must lay out your answer• Comprehensive income statement or s of fp or

cash flow• 15 marks = ethics OPPIC & accounting issue

2

Section B

• 2 from 3• Make the choice in the reading time• Q2 / Q3 – accounting standards• Depth & application• Financial instruments• Q4 Current issues

3

Management Commentary

• Practice statement issued December 2010• Objective is to assist management to provide

a useful management commentary• Not mandatory• A context to supplement & interpret• Past present & future• Words rather than numbers!• Audit review not audited

4

Principles of the MC

• Provide management’s perspective• Objectives & strategies• Forward orientated• Relevant & faithful• Clear & straight forward• Focussed on material issues

5

Elements of the MC

• Nature of the business• Management’s objectives & strategies• Significant - resources, risks, relationships• Results• KPIs

6

IFRS13 Fair Value Measurement

Why ?• USA joint project • single source• Does not extend use• Does not apply to leases or share based

payments• FV can apply on initial measurement,

recurring basis, on a non-recurring basis

7

FVM - definition

“The price that could be received to sell an asset (or paid to transfer a liability) in an orderly transaction between market participants at the measurement date.”

i.e. market based approachHighest and bestPre – transaction costs ignore (not a feature of the asset)

8

FVM – hierarchy of inputs

• Level 1 – observable in an active markete.g. listed coy shares – FVTP&L / PF Assets• Level 2 – observable in an inactive market or

for similar itemse.g. property• Level 3 – unobservable inputse.g. deferred consideration / PV FCF Liabilities

9

FVM

• Financial assets have to be initially measured at FV, one is bought for $100 cash when it has a FV of $150.

• Possible ? Yes – RPT or bargain• Accounting is … gain of $50

10

FVM

• Acquired, with the intention to trade, a $100m zero coupon bond at par that is redeemable at a premium of $21m in two years time, effective rate of interest being 10%. At year one end interest rates are now 5%.

• Show the accounting

11

FVM

• At end of year one• FV of the asset = 115• CV of the asset = 110• Difference to i/s = 5 gain

12

IFRS10 Consolidated Financial Statements

Why?• USA joint project • to prevent “off balance sheet finance” i.e. the

non consolidation of highly geared controlled entities

• Principles based approach to control• Power over the investee; exposure, or rights, to

variable returns, the ability to use its power to affect the amount of the returns

13

Is there control ?

• Consider the size of the holding and the dispersion of holdings

• 48% investment?• Options? (potential voting rights)• Contract?

14

Leases

• IAS17 requires a classification between finance & operating

• Based on a judgment as to whether substantially all risks & rewards pass

• Finance = asset, liability, depreciation & finance cost

• Operating = operating cost

15

Problem with IAS17

• Similar items are dealt with differently• Results in an all or nothing approach• Classification is subjective• Creates opportunity for creative accounting• Lessees can account for long term leases

being as operating – off balance sheet finance• Conflict with the framework – liability &

faithful representation (complete)

16

Solution

• Create a single model – cease the classification process – treat all leases the same

• Adhere to the framework approach – assets & liabilities – recognition criteria

• In future recognise all obligations created by leases – liabilities on balance sheet

17

Consider

• Lessee, asset life of ten years, cash price $100,000, two year lease, rentals in arrears $10,000 per annum, interest rates 10%

• ? Accounting per IAS17 • ? Accounting per proposals

18

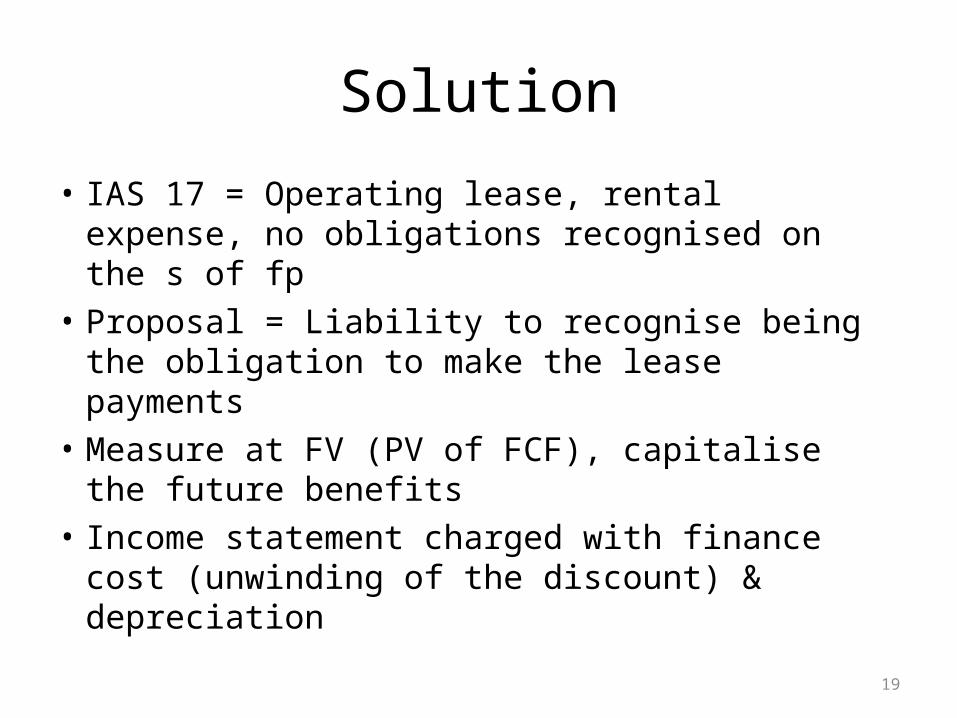

Solution

• IAS 17 = Operating lease, rental expense, no obligations recognised on the s of fp

• Proposal = Liability to recognise being the obligation to make the lease payments

• Measure at FV (PV of FCF), capitalise the future benefits

• Income statement charged with finance cost (unwinding of the discount) & depreciation

19

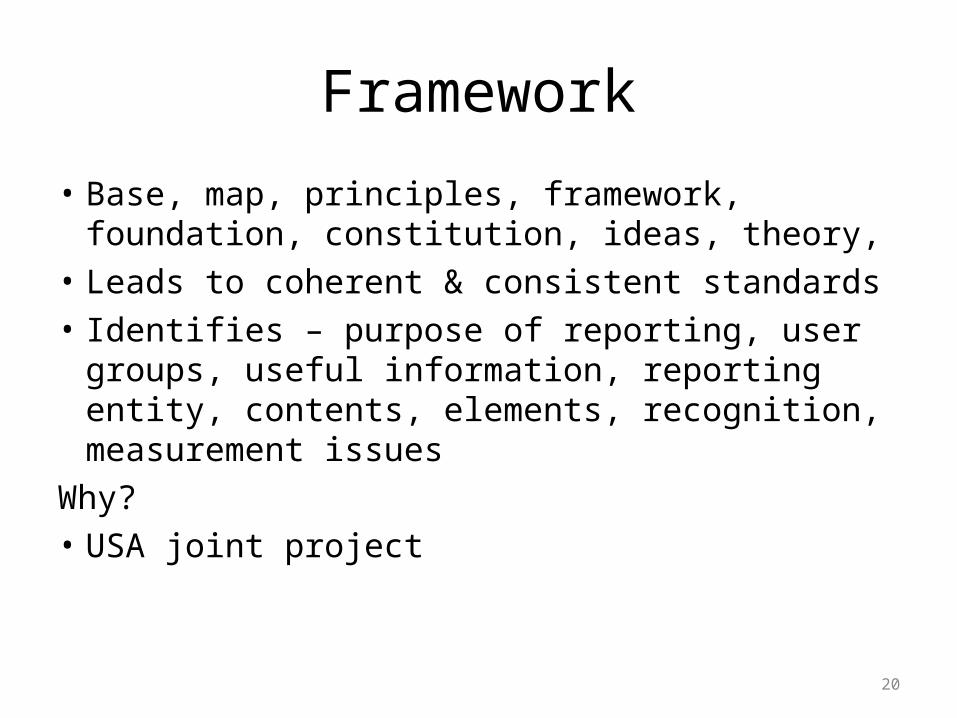

Framework

• Base, map, principles, framework, foundation, constitution, ideas, theory,

• Leads to coherent & consistent standards• Identifies – purpose of reporting, user groups,

useful information, reporting entity, contents, elements, recognition, measurement issues

Why?• USA joint project

20

What’s new?

• Useful information has two fundamental characteristics

Relevant• Capable of making a difference• Predictive / confirmatory

21

What’s new

• Useful information has two fundamental characteristics

Faithful representation• Complete• Neutral• Free from error• Reliable / substance over form / objective

22

What’s new

• Useful information has four enhancing characteristics

1.Comparability 2.Verifiability3.Timeliness4.Understandability

23