academy of professional accounting (apa) · revision: types of audit report unmodified report...

TRANSCRIPT

Professional Accounting Education

Provided by Academy of Professional Accounting (APA)

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台

ACCA F8 习题详解 Audit and Assurance (AA)

审计与鉴证业务 第21讲

ACCA Lecturer: Andy Qu

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 2

1

2

MCQ Bank: Audit Report (1)

Contents of Class 21

Case: Palm and Ash Trading (June 2015)

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 3

Revision: Types of audit Report

Unmodified Report

Modified Report but unmodified opinion

Emphasis of Matter Paragraph

Modified Report and Opinion

Nature Material but not

pervasive Material and pervasive

F/S are materially misstated

Qualified Opinion (Disagreement)

Adverse Opinion

Auditor unable to obtain sufficient audit evidence

Qualified Opinion (Limitation on scope)

Disclaimer of Opinion

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 4

MCQ: Audit Report (1)

Which of the following is not included in an unmodified

auditor's report?

A Management's responsibility for the financial statements

B Auditors' responsibilities

C Audit opinion

D Deficiencies of internal controls

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 5

MCQ: Audit Report (1)

D

The basic elements of the auditor's report are title,

addressee, introductory paragraph, management's

responsibility for financial statements, auditor's

responsibility, opinion paragraph, other reporting

responsibilities, auditor's signature, date of the report and

auditor's address.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 6

MCQ: Audit Report (1)

The auditor of Q Co has completed the audit and has

concluded that sufficient appropriate evidence has been

obtained, which confirms that the financial statements are

not materially misstated.

Which form of audit opinion will the auditor issue?

A Adverse opinion

B Qualified opinion

C Unmodified opinion

D A disclaimer of opinion

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 7

MCQ: Audit Report (1)

C

An unmodified opinion is expressed when the auditor

concludes that the financial statements are prepared, in

all material respects, in accordance with the applicable

financial reporting framework.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 8

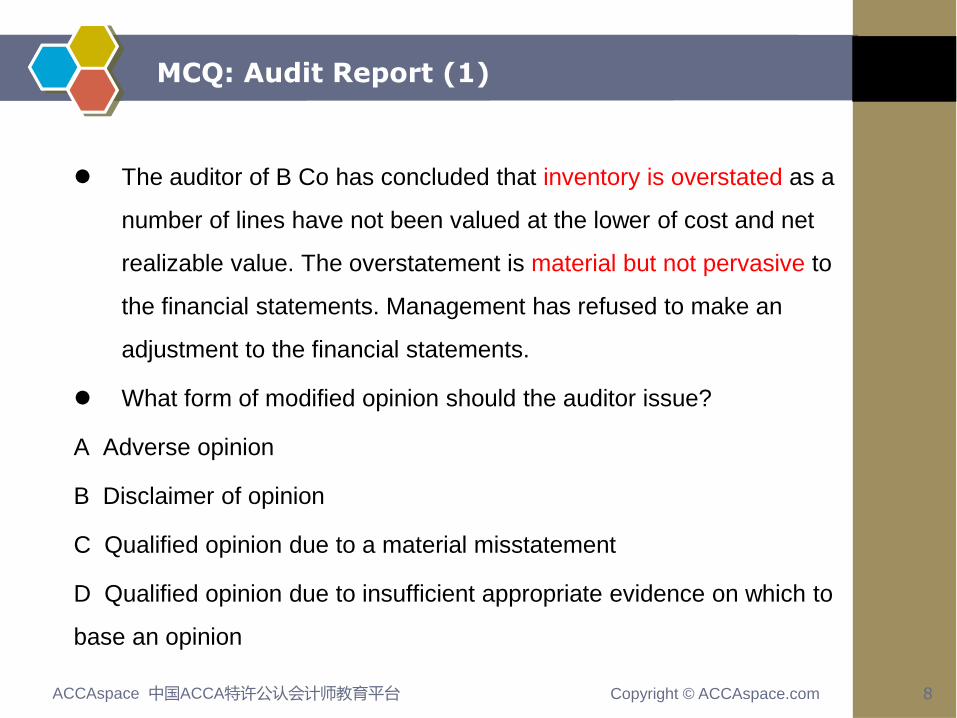

MCQ: Audit Report (1)

The auditor of B Co has concluded that inventory is overstated as a

number of lines have not been valued at the lower of cost and net

realizable value. The overstatement is material but not pervasive to

the financial statements. Management has refused to make an

adjustment to the financial statements.

What form of modified opinion should the auditor issue?

A Adverse opinion

B Disclaimer of opinion

C Qualified opinion due to a material misstatement

D Qualified opinion due to insufficient appropriate evidence on which to

base an opinion

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 9

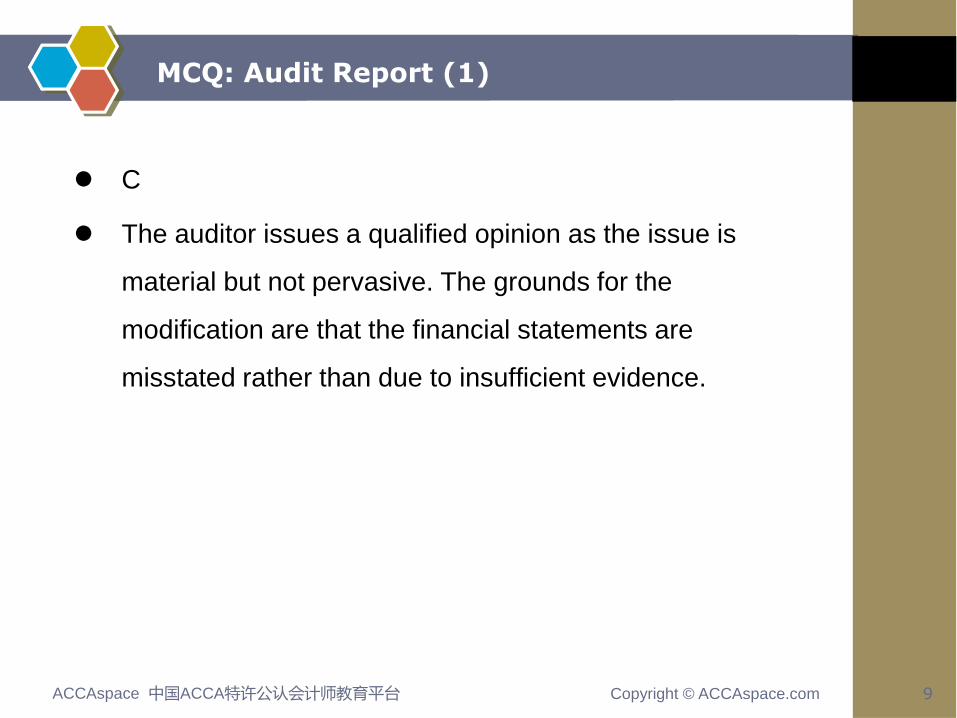

MCQ: Audit Report (1)

C

The auditor issues a qualified opinion as the issue is

material but not pervasive. The grounds for the

modification are that the financial statements are

misstated rather than due to insufficient evidence.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 10

MCQ: Audit Report (1)

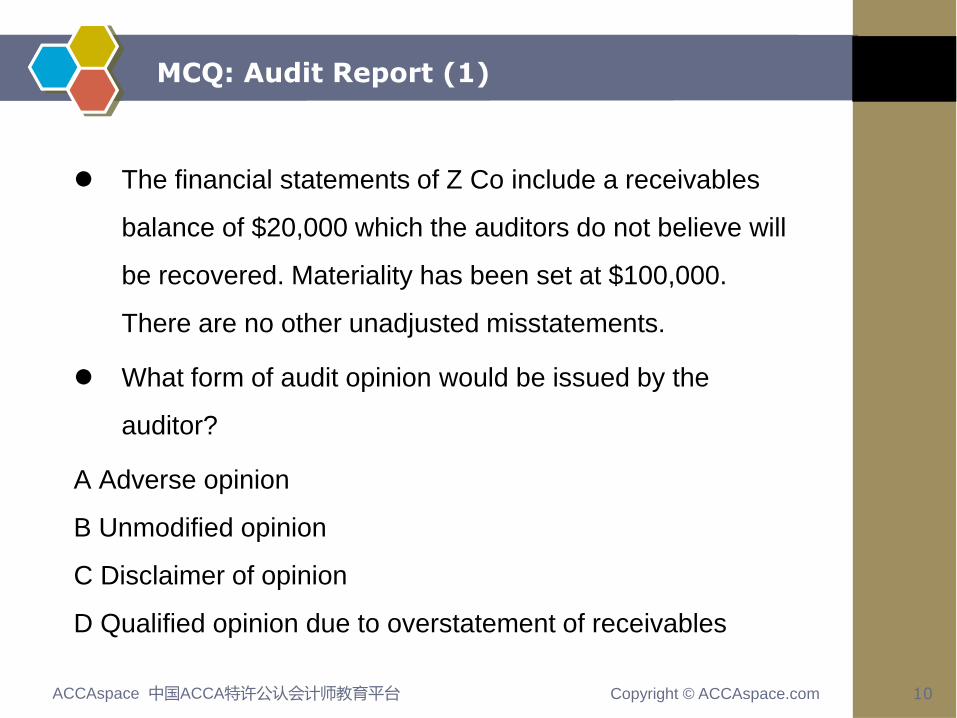

The financial statements of Z Co include a receivables

balance of $20,000 which the auditors do not believe will

be recovered. Materiality has been set at $100,000.

There are no other unadjusted misstatements.

What form of audit opinion would be issued by the

auditor?

A Adverse opinion

B Unmodified opinion

C Disclaimer of opinion

D Qualified opinion due to overstatement of receivables

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 11

MCQ: Audit Report (1)

B

Although the receivables balance is overstated, the

amount involved is not material.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 12

Case: June 2015

You are the audit manager of Chestnut & Co and are reviewing the key

issues identified in the files of two audit clients.

Palm Industries Co (Palm)

Palm’s year end was 31 March 2015 and the draft financial statements

show revenue of $28·2 million, receivables of $5·6 million and profit before

tax of $4·8 million. The fieldwork stage for this audit has been completed.

A customer of Palm owed an amount of $350,000 at the year end. Testing

of receivables in April highlighted that no amounts had been paid to Palm

from this customer as they were disputing the quality of certain goods

received from Palm. The finance director is confident the issue will be

resolved and no allowance for receivables was made with regards to this

balance.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 13

Case: June 2015

Ash Trading Co (Ash)

Ash is a new client of Chestnut & Co, its year end was 31 January 2015

and the firm was only appointed auditors in February 2015, as the

previous auditors were suddenly unable to undertake the audit. The

fieldwork stage for this audit is currently ongoing.

The inventory count at Ash’s warehouse was undertaken on 31 January

2015 and was overseen by the company’s internal audit department.

Neither Chestnut & Co nor the previous auditors attended the count.

Detailed inventory records were maintained but it was not possible to

undertake another full inventory count subsequent to the year end. The

draft financial statements show a profit before tax of $2·4 million,

revenue of $10·1 million and inventory of $510,000.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 14

Case: June 2015

Required:

For each of the two issues:

(i) Discuss the issue, including an assessment of

whether it is material;

(ii) Recommend ONE procedure the audit team

should undertake to try to resolve the issue; and

(iii) Describe the impact on the audit report if the

issue remains UNRESOLVED.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 15

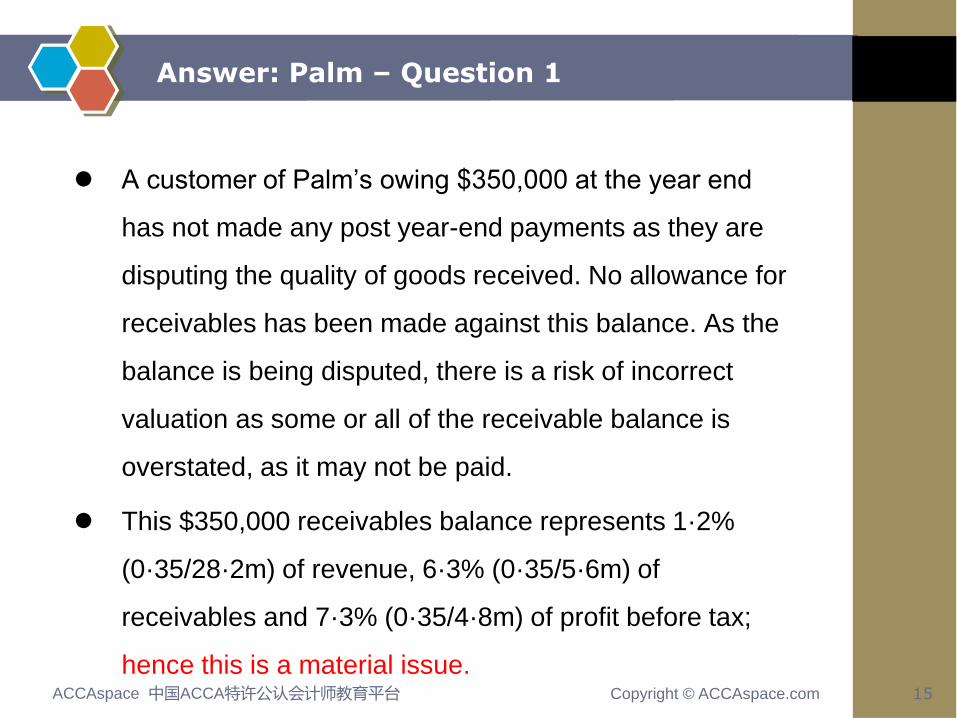

Answer: Palm – Question 1

A customer of Palm’s owing $350,000 at the year end

has not made any post year-end payments as they are

disputing the quality of goods received. No allowance for

receivables has been made against this balance. As the

balance is being disputed, there is a risk of incorrect

valuation as some or all of the receivable balance is

overstated, as it may not be paid.

This $350,000 receivables balance represents 1·2%

(0·35/28·2m) of revenue, 6·3% (0·35/5·6m) of

receivables and 7·3% (0·35/4·8m) of profit before tax;

hence this is a material issue.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 16

Answer: Palm – Question 2

A procedure to adopt includes:

– Review whether any payments have subsequently been

made by this customer since the audit fieldwork was

completed.

– Discuss with management whether the issue of quality of

goods sold to the customer has been resolved, or whether it

is still in dispute.

– Review the latest customer correspondence with regards

to an assessment of the likelihood of the customer making

payment.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 17

Answer: Palm – Question 3

If management refuses to provide against this receivable,

the audit report will need to be modified. As receivables

are overstated and the error is material but not pervasive

a qualified opinion would be necessary.

A basis for qualified opinion paragraph would be needed

and would include an explanation of the material

misstatement in relation to the valuation of receivables

and the effect on the financial statements. The opinion

paragraph would be qualified ‘except for’.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 18

Answer: Ash Trading – Question 1

Ash Trading Co (Ash)

Chestnut & Co was only appointed as auditors

subsequent to Ash’s year end and hence did not attend

the year-end inventory count. Therefore, they have not

been able to gather sufficient and appropriate audit

evidence with regards to the completeness and existence

of inventory.

Inventory is a material amount as it represents 21·3%

(0·51/2·4m) of profit before tax and 5% (0·51/10·1m) of

revenue; hence this is a material issue.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 19

Answer: Ash Trading – Question 2

A procedure to adopt includes:

– Review the internal audit reports of the inventory count to

identify the level of adjustments to the records to assess the

reasonableness of relying on the inventory records.

– Undertake a sample check of inventory in the warehouse

and compare to the inventory records and then from inventory

records to the warehouse, to assess the reasonableness of

the inventory records maintained by Ash.

Copyright © ACCAspace.com ACCAspace 中国ACCA特许公认会计师教育平台 20

Answer: Ash Trading – Question 3

The auditors will need to modify the audit report as they

are unable to obtain sufficient appropriate evidence in

relation to inventory which is a material but not pervasive

balance. Therefore a qualified opinion will be required.

A basis for qualified opinion paragraph will be required to

explain the limitation in relation to the lack of evidence

over inventory. The opinion paragraph will be qualified

‘except for’.

Professional Accounting Education

Provided by Academy of Professional Accounting (APA)