aca town hall geneva - americansabroad.org · doubling the standard deduction providing tax relief...

TRANSCRIPT

Presented on May 17, 2017

Kenneth A. Freshman, CPA, JD, LLM

ACA Town Hall Geneva

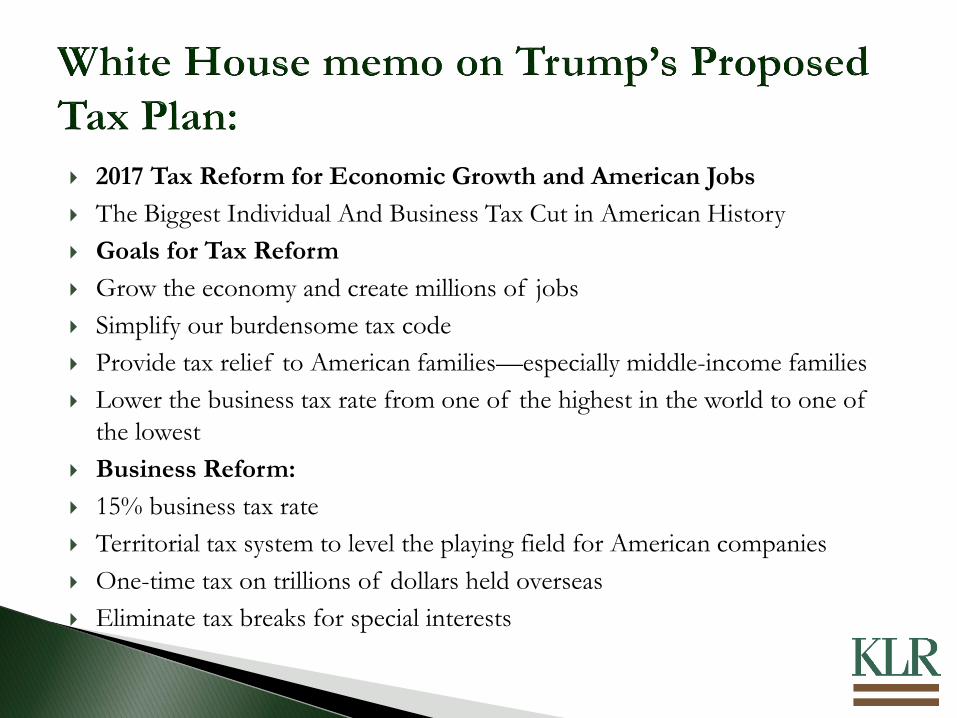

2017 Tax Reform for Economic Growth and American Jobs

The Biggest Individual And Business Tax Cut in American History

Goals for Tax Reform

Grow the economy and create millions of jobs

Simplify our burdensome tax code

Provide tax relief to American families—especially middle-income families

Lower the business tax rate from one of the highest in the world to one of

the lowest

Business Reform:

15% business tax rate

Territorial tax system to level the playing field for American companies

One-time tax on trillions of dollars held overseas

Eliminate tax breaks for special interests

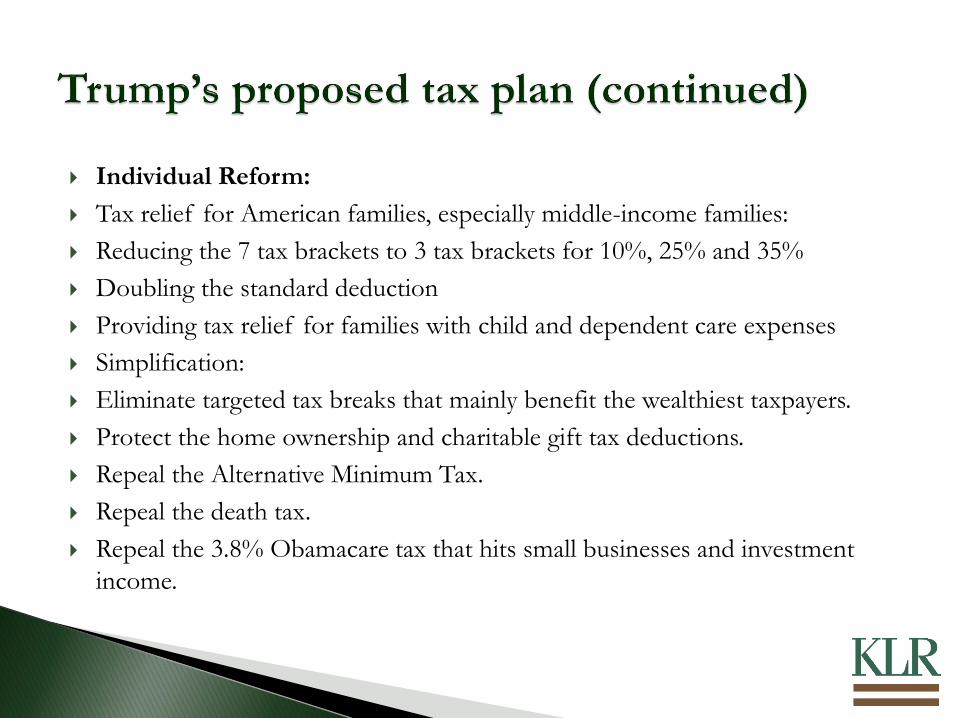

Individual Reform:

Tax relief for American families, especially middle-income families:

Reducing the 7 tax brackets to 3 tax brackets for 10%, 25% and 35%

Doubling the standard deduction

Providing tax relief for families with child and dependent care expenses

Simplification:

Eliminate targeted tax breaks that mainly benefit the wealthiest taxpayers.

Protect the home ownership and charitable gift tax deductions.

Repeal the Alternative Minimum Tax.

Repeal the death tax.

Repeal the 3.8% Obamacare tax that hits small businesses and investment

income.

Reporting for foreign equivalent Possible Tax consequences

Bank / Brokerage Account

FBAR 8938

Retirement account FBAR, 8938, 3520, 8621 Additional income for employer contributions, investment income, possible characterization as trust

Business ownership 5471, 8865, 8858, 926 Current recognition of undistributed income undercontrolled foreign corporation rules

Mutual Fund / ETF 8621 Acceleration of income recognition, less favorable tax rates, interest charge

Trust 3520, 3520-A Penalty tax on accumulated distribution

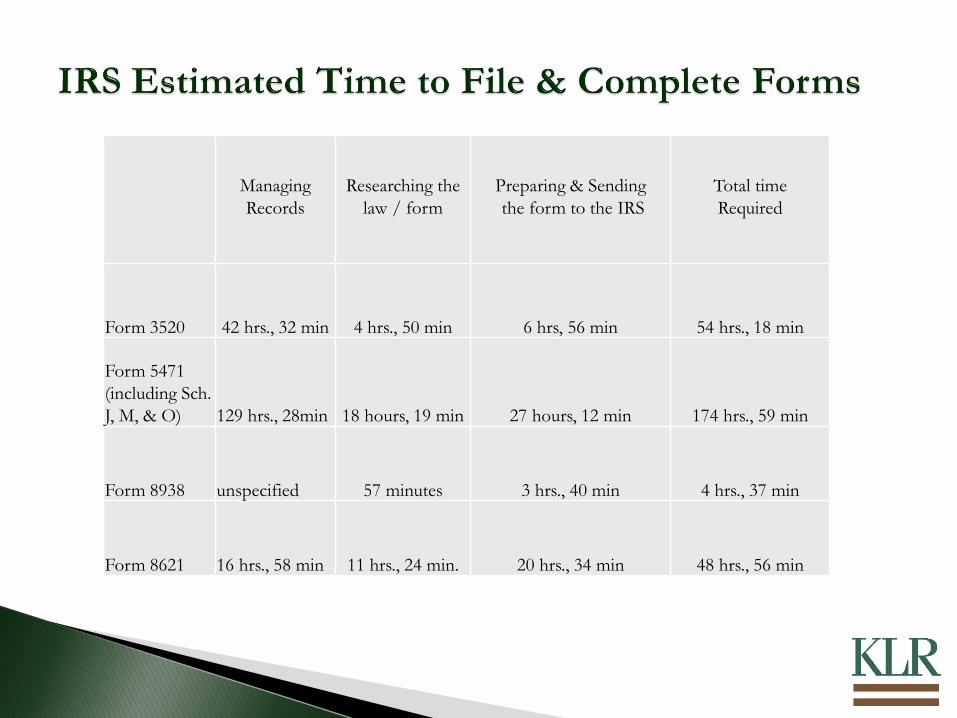

Managing

Records

Researching the

law / form

Preparing & Sending

the form to the IRS

Total time

Required

Form 3520 42 hrs., 32 min 4 hrs., 50 min 6 hrs, 56 min 54 hrs., 18 min

Form 5471

(including Sch.

J, M, & O) 129 hrs., 28min 18 hours, 19 min 27 hours, 12 min 174 hrs., 59 min

Form 8938 unspecified 57 minutes 3 hrs., 40 min 4 hrs., 37 min

Form 8621 16 hrs., 58 min 11 hrs., 24 min. 20 hrs., 34 min 48 hrs., 56 min

If you are a U.S. citizen or a resident alien of the U.S.

and you live abroad, you are taxed on your worldwide

income. However, you may qualify to exclude from

income up to an amount of your foreign earnings that

is adjusted annually for inflation.

Exclusion allowed is the smaller of the foreign earned

income or annual maximum limit of $102,100 (2017)

To avoid double taxation the taxpayer may use the

Foreign Earned Income Exclusion, Foreign Tax Credit,

or an Income Tax Treaty

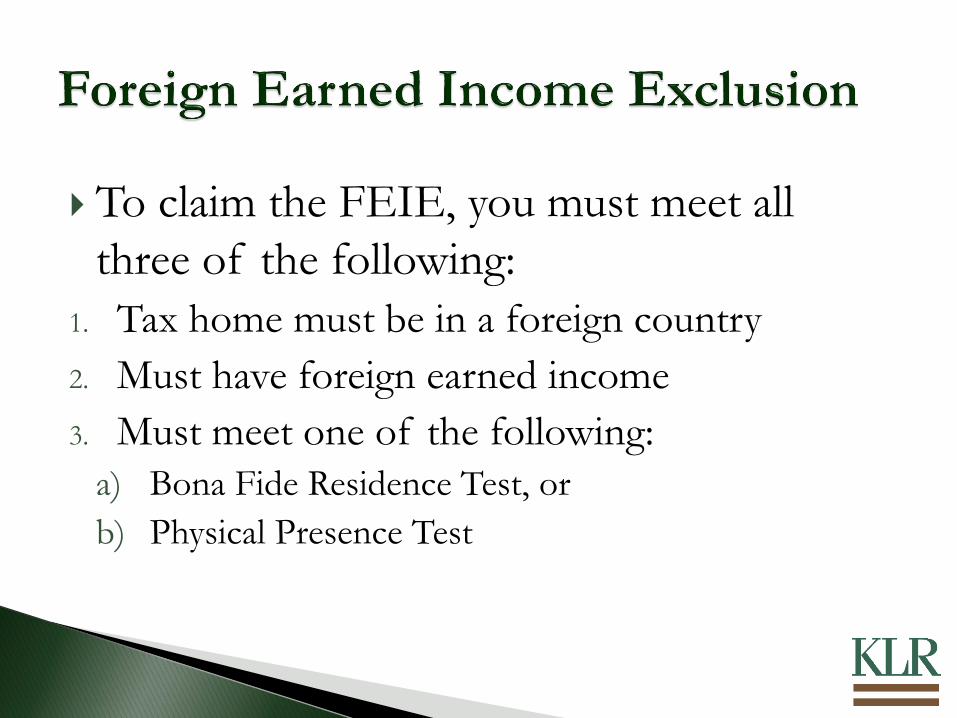

To claim the FEIE, you must meet all

three of the following:

1. Tax home must be in a foreign country

2. Must have foreign earned income

3. Must meet one of the following:

a) Bona Fide Residence Test, or

b) Physical Presence Test

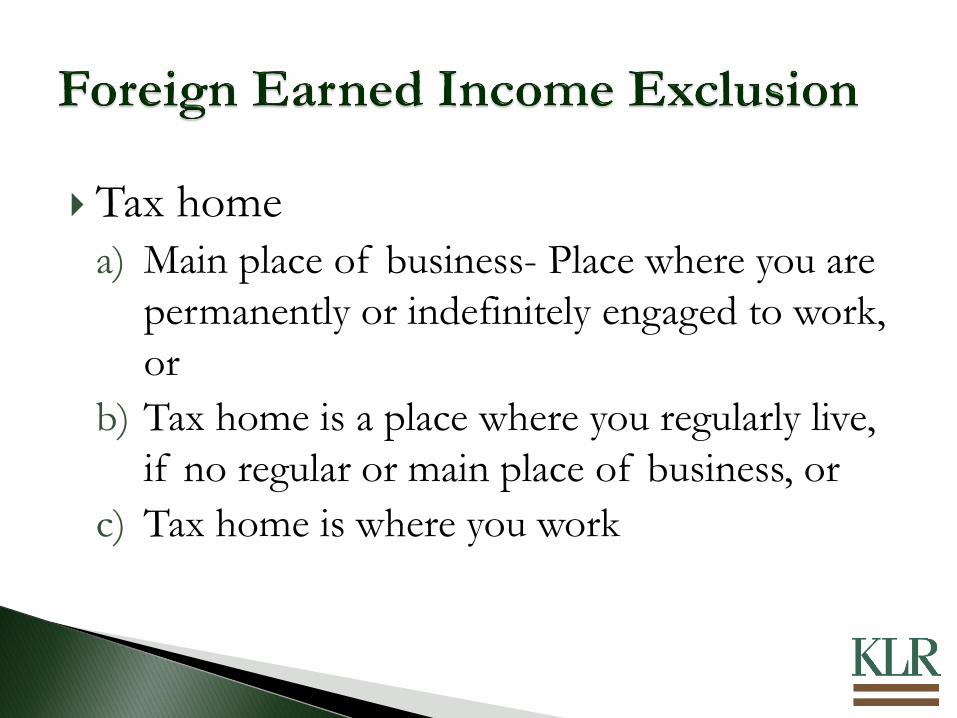

Tax home

a) Main place of business- Place where you are

permanently or indefinitely engaged to work,

or

b) Tax home is a place where you regularly live,

if no regular or main place of business, or

c) Tax home is where you work

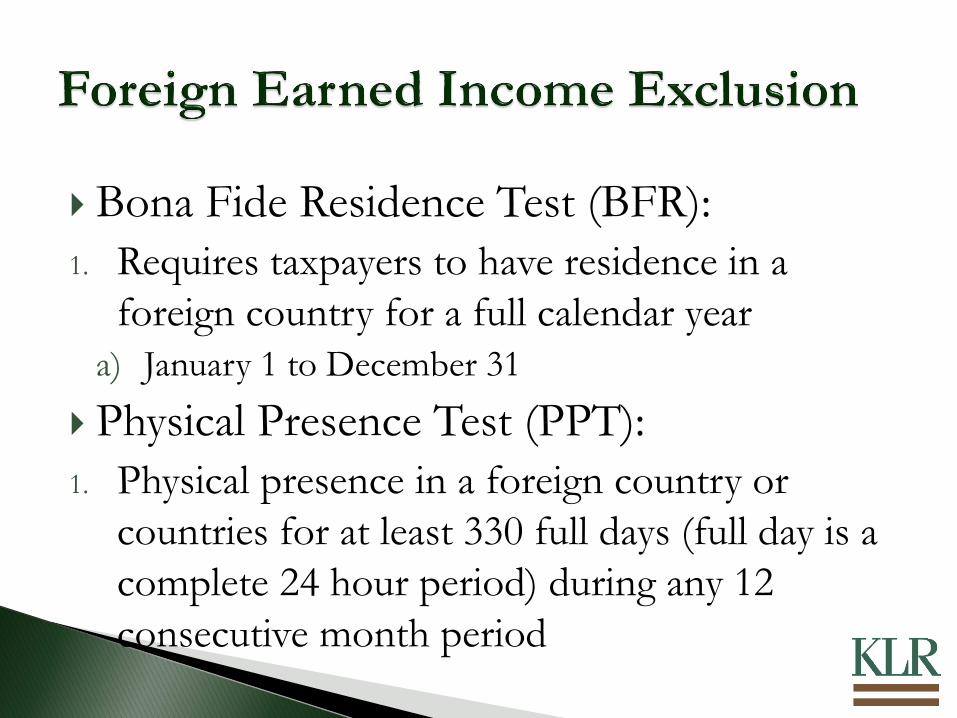

Bona Fide Residence Test (BFR):

1. Requires taxpayers to have residence in a

foreign country for a full calendar year

a) January 1 to December 31

Physical Presence Test (PPT):

1. Physical presence in a foreign country or

countries for at least 330 full days (full day is a

complete 24 hour period) during any 12

consecutive month period

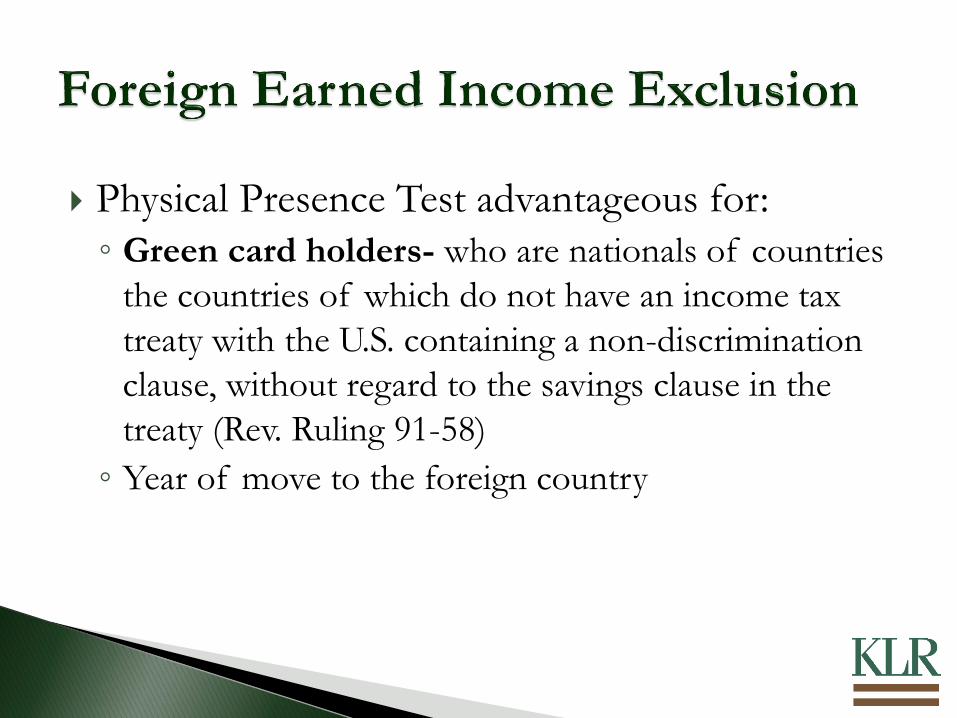

Physical Presence Test advantageous for:

◦ Green card holders- who are nationals of countries

the countries of which do not have an income tax

treaty with the U.S. containing a non-discrimination

clause, without regard to the savings clause in the

treaty (Rev. Ruling 91-58)

◦ Year of move to the foreign country

Computing the exclusion

1. Prorate the number of qualifying days

a) Example (Foreign – 280 days in calendar year)

b) 280/365 * $102,100 = $78,323

Voluntary and claimed on Form 2555

Once elected it applies to all future tax years

unless revoked◦ If revoked, it cannot be claimed for at least 5 years without

IRS approval.

Housing exclusion may be claimed for housing

expenses

Amount is limited to the smaller of the actual

expenses or the maximum allowed for the location

less the base housing amount of $16,336 (2017). Base

amount is 16% of the maximum FEIE amount.

The housing deduction applies only to self-

employment income.

Can be used in conjunction with the FEIE or alone

The taxpayer can exclude the housing cost

amounts of only one foreign residence

◦ An exception applies when a second residence is

maintained because living conditions where the

taxpayer resides are dangerous, unhealthful, or at war.

Housing costs need to be reasonable expenses

paid or incurred during the taxable year for

housing in a foreign country.

Allowed housing expenses:

◦ Rent

◦ Utilities (other than telephone)

◦ Rental fees

◦ Furniture rental

◦ Residential parking

◦ Real and personal property insurance

◦ Repairs

Relieves the taxpayer from the burden of double taxation

when their foreign sourced income is taxed by both the

U.S. and the foreign country.

Limitations

◦ The FTC can only reduce U.S. taxes on foreign source income; it

cannot reduce U.S. taxes on U.S. source income.

◦ The FTC is not available for foreign taxes paid on income

excluded under the foreign earned income exclusion or the

foreign housing exclusion

Claimed on Form 1116

Dollar-for dollar tax credit, deducted from U.S.

tax liability

Allows for a 1-year carryback and a 10-year

carryover of the unused foreign taxes.

Taxpayer has a choice between taking the

foreign taxes as a credit or as an itemized

deduction

Four tests to qualify:

1. The tax must be imposed on the taxpayer

2. The taxpayer must have paid or accrued the tax

3. The tax must be the legal and actual foreign tax

liability

4. The tax must be an income tax or a tax in lieu of

income. It cannot be an excise tax, sales tax, VAT,

capital or net worth tax.

What?

◦ The tax must be imposed on the taxpayer

◦ Tax is attributable to property held for the production of

income

How?

◦ ONLY deductible under Schedule A in the “Taxes You Paid,

Other taxes” section in the year in which it is paid or accrued.

Creditable taxes are separated into categories or “baskets” like: ◦ General Limitation (wages)◦ Passive (interest, dividends, capital gains and loss,

rental income or loss)

Taxpayers may claim the foreign tax credit by

using one of two accounting methods:

◦ As the tax is paid ("the paid method"), or

◦ As the tax is accrued ("the accrued method")

These elections are binding for all baskets

Only foreign taxes paid during year qualify

for credit

Converted to US dollars using exchange

rate on payment date

Can change from paid to accrued method

but only ONCE

The taxpayer claims a foreign tax credit for the total

foreign tax liability for the year, even though the foreign

tax may be paid in a different year. Accrue when all

events have taken place that fix amount of tax and

liability to pay it (i.e. fixed and determinable)

Cannot switch to paid method in the future

Converted to US dollars using average exchange rate

during the period of accrual

Accrue taxes on US return in the year in which the

taxes of the foreign country accrue

Foreign tax credit allowed is the lesser of:

◦ Foreign tax paid or accrued less amount allocable to

excluded income

◦ Amount of U.S. tax on foreign source taxable

income

Apportion US tax liability between US source

income and foreign source net income

◦ Limitation = Foreign Source Taxable Income /

Worldwide Taxable Income * US Tax

Prevents using foreign tax as a credit against tax

on US source income

Provides relief by reclassifying U.S. source

income that is taxed in both the foreign country

and the U.S. as foreign source income

Allows a greater foreign tax credit

Only available if “relief from double taxation”

article exists in treaty

Publication 514 has a list of the countries for

which treaty resourcing is allowed

Ten years to file claim for refunds of US tax for foreign taxes paid or accrued not claimed in prior years

Ten year period begins the day after the regular due date for filing the return

Applies to:◦ math errors in foreign tax calculation

◦ unreported amounts in prior years

◦ other changes in size of credit

Purpose: to reduce or eliminate double taxation

between countries.

U.S. has income tax treaties with more than 60

countries

Individuals must be a tax resident of the other

country to qualify for the treaty benefit

Treaty tie-breaker rules exist for determining

residency

Must attach a fully completed Form 8833 with

U.S. tax return

◦ Failure to report required information on Form 8833

may result in a $1,000 penalty for each failure.

Each treaty has different guidelines

IRS Publication 901, U.S. Tax Treaties for

guidance

Standard Dependent Service Clause

◦ Only taxable in resident country if

Present in other country 183 days or less; and

Paid by or on behalf of nonresident employer; and

Remuneration is not borne by a permanent

establishment or fixed base of the employer in

other country

◦ Specific treaties – 12 month period U.S. taxpayer or a

rolling 12 month period

Define tax residents for treaty application

◦ Tie breaker clause

Modify source of income to eliminate

withholding or can apply a reduced rate of

withholding to certain income (1042-S)

Residency – Treaty “Tie Breaker” Rules

◦ Standard tie breakers, if resident of both countries

(in order):

Permanent home

Center of vital interests (closest personal and

economic relations)

Habitual abode

Citizenship

Unless disclosure is specifically waived, Form

8833 must be filed

Disclosure may still be required on Form

1040NR, page 5

Generally, a U.S. return is technically required in

any case

◦ Exception, only not effectively connected income and

proper withholding and proper reporting on Form

1042S by payer

The definition of a Passive Foreign Investment Company

is a:

◦ Income test- Non-US Corporation that has 75% or

more of its gross income from Passive income, or

◦ Asset test- 50% or more of the average fair market

value of its assets produce passive income (cash is

considered a passive asset)

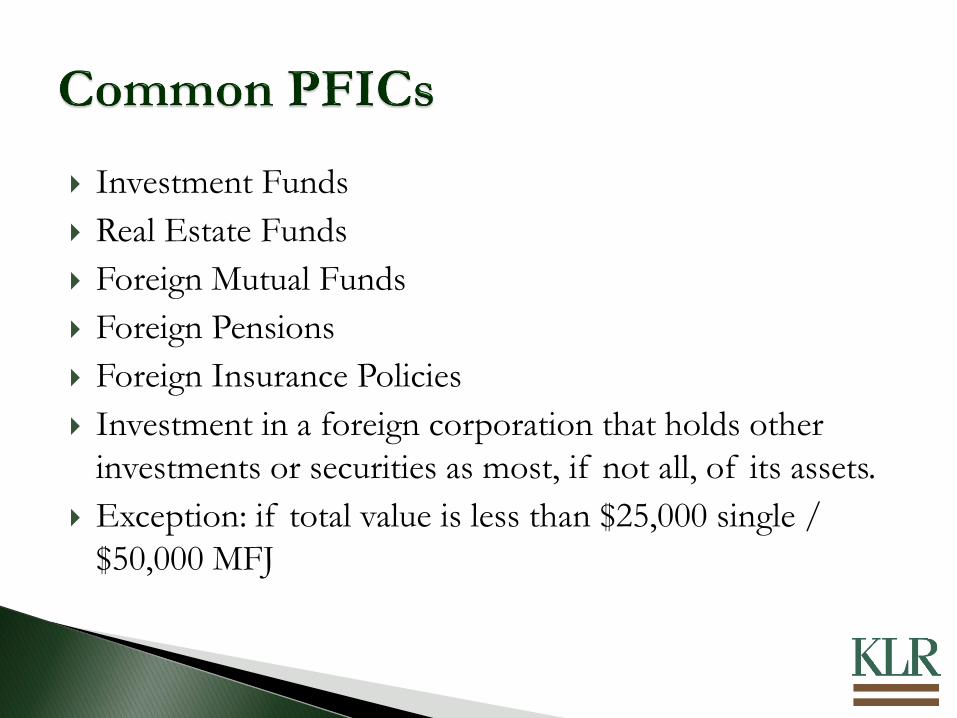

Investment Funds

Real Estate Funds

Foreign Mutual Funds

Foreign Pensions

Foreign Insurance Policies

Investment in a foreign corporation that holds other

investments or securities as most, if not all, of its assets.

Exception: if total value is less than $25,000 single /

$50,000 MFJ

• Mark-to-Market Election• Must be made only in first year, or if approved by the IRS during OVDI

• All gain is taxed as ordinary income

• Any losses can be taken up to any unreversed inclusions, but after that

are lost

• Qualified Electing Fund Election• Must be made only in the first year and by the original US investor(s)

• Any income is treated as ordinary income and any capital gains treated

as long-term capital gains

• 1291 Fund• Default if neither the MTM or QEF election was made in the first year

• If this is the initial year of investment in a PFIC a

MTM election should be made, as it is the easiest to

track year to year

• Each year you must take into income any gain on the

appreciation of the PFIC’s value or gain from any sales

made during the year.

• A loss can be taken in a year only up to the amount of

any prior year(s) included income

• Sometimes a “QEF” election is made by the US

shareholder(s) of the PFIC in the first year.

• QEF election allows the PFIC to be treated the

same as a US mutual fund, where capital gains

are recognized (this is not the case for MTM nor

1291 Fund)

• This requires an annual statement made by the

PFIC and sent to the US investors so that the

items of income and capital gains can be

recognized each year by that US investor

PFIC Elections: QEF

• A common problem with QEF is when Hedge

Funds provide some PFICs that have made

QEF elections and some that have not made

QEF elections.

• Depending on the information provided by such

Hedge Fund, one may need to separately state

the individual investments. This could lead even

further to more cumbersome reporting.

PFIC Elections: QEF

• If no MTM or QEF election was made in the initial year

then this is the default treatment of the PFIC

• Any actual distributions made in the taxable year must be

calculated over the course of the actual days the units were

held by the taxpayer

• The gain is calculated for the current year as well as all prior

years and the highest ordinary income rate of tax for each

year is applied as well as interest charges applied.

• Any losses are not recognized

PFIC: 1291 Fund

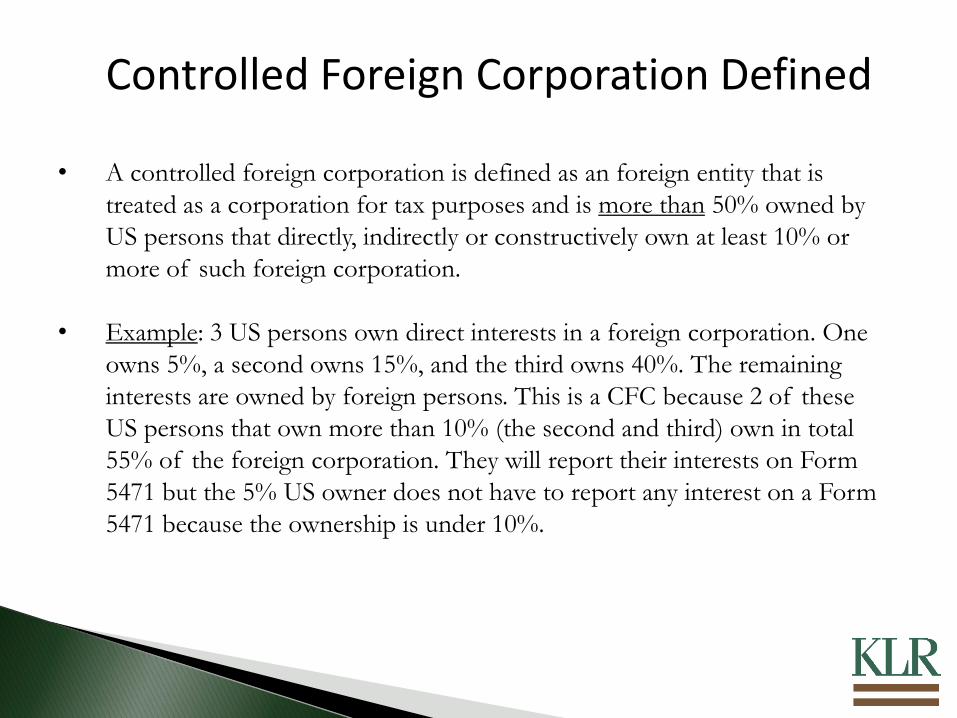

• A controlled foreign corporation is defined as an foreign entity that is

treated as a corporation for tax purposes and is more than 50% owned by

US persons that directly, indirectly or constructively own at least 10% or

more of such foreign corporation.

• Example: 3 US persons own direct interests in a foreign corporation. One

owns 5%, a second owns 15%, and the third owns 40%. The remaining

interests are owned by foreign persons. This is a CFC because 2 of these

US persons that own more than 10% (the second and third) own in total

55% of the foreign corporation. They will report their interests on Form

5471 but the 5% US owner does not have to report any interest on a Form

5471 because the ownership is under 10%.

Controlled Foreign Corporation Defined

• If a US person is an owner of a foreign corporation that meets the

definition of a PFIC, and it does not meet the definition of a CFC, then the

PFIC rules apply.

• “Once a PFIC, Always a PFIC” – If later there are enough US investors that

could qualify the foreign corporation as a CFC, unfortunately once the

PFIC “taint” is on the corporation the PFIC rules will always apply. You

cannot treat the company as a CFC with the new investor. The investor

must also be aware of this prior PFIC treatment before investing.

• However CFC does trump PFIC in initial year of formation/acquisition. If

this is the first year any US investors are purchasing or forming the foreign

corporation, if it meets the CFC rules in this initial year it can (and should)

be treated as a CFC in the first year to avoid PFIC treatment. (But if

subsequent years it fails to be a CFC, then the PFIC rules will come in and

trump any further CFC treatment.)

PFIC vs. CFC

• Subpart F income is the most easily missed component of preparing Form

5471 for CFCs.

• There are various forms of Subpart F income (§952(a)):

• Insurance Income (§953)

• Foreign Based Company Income (§954)

• Various other types of income that relate to the international boycott

(under §999), illegal payments (under §162(c)); and income under

§901(j) (denial of foreign tax credit with respect to certain countries)

CFC and Subpart F

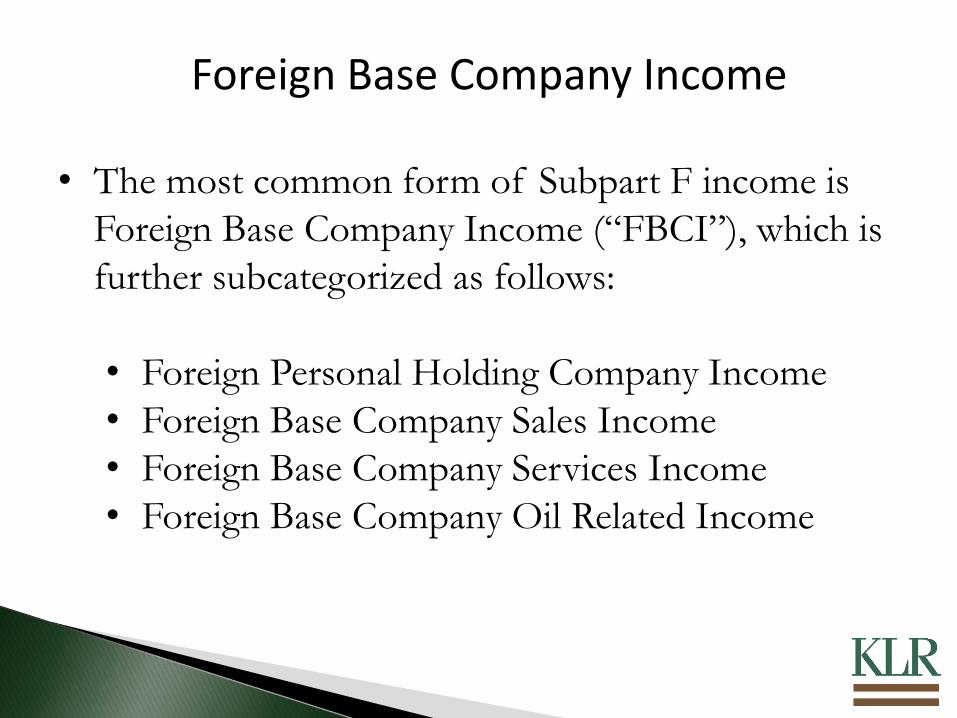

• The most common form of Subpart F income is

Foreign Base Company Income (“FBCI”), which is

further subcategorized as follows:

• Foreign Personal Holding Company Income

• Foreign Base Company Sales Income

• Foreign Base Company Services Income

• Foreign Base Company Oil Related Income

Foreign Base Company Income

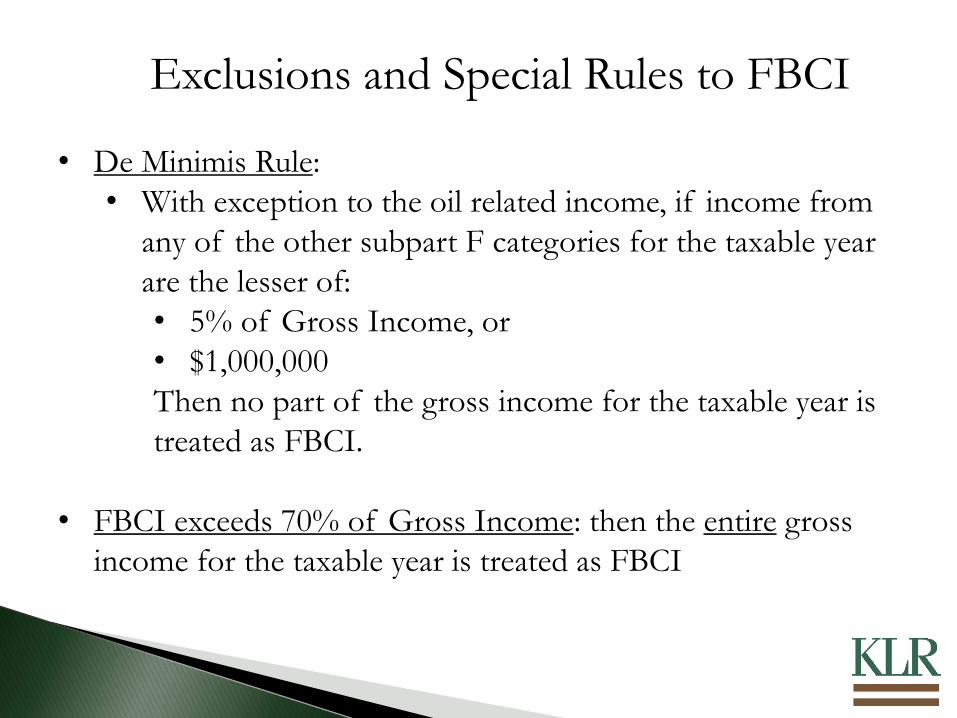

• De Minimis Rule:

• With exception to the oil related income, if income from

any of the other subpart F categories for the taxable year

are the lesser of:

• 5% of Gross Income, or

• $1,000,000

Then no part of the gross income for the taxable year is

treated as FBCI.

• FBCI exceeds 70% of Gross Income: then the entire gross

income for the taxable year is treated as FBCI

Exclusions and Special Rules to FBCI

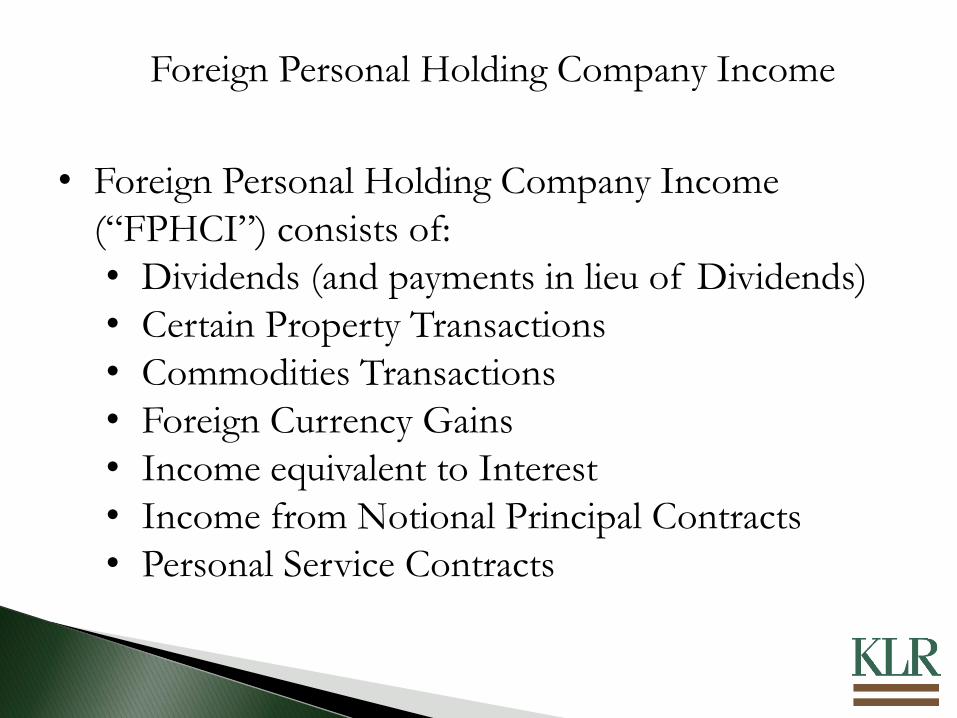

• Foreign Personal Holding Company Income

(“FPHCI”) consists of:

• Dividends (and payments in lieu of Dividends)

• Certain Property Transactions

• Commodities Transactions

• Foreign Currency Gains

• Income equivalent to Interest

• Income from Notional Principal Contracts

• Personal Service Contracts

Foreign Personal Holding Company Income

• Rents and Royalties derived from an active

business dealing in rents or royalties

• Certain Export Financing

• Exception for Dealers (in contracts/

securities)

Exceptions to FPHCI

It is very important to properly categorize the filer reporting the Form 5471:

• Category 2 Filers: Use this only if the financial statements list the filer as

an officer or director of a corporation and:• In the taxable year the filer has acquired (in one or more transactions) stock

which meets the 10% vote or value of the corporation, or

• Acquired an additional 10% or more vote or value o the outstanding stock in

the corporation

• Category 3 Filers: Use this in the taxable year that the filer either:

• Becomes a U.S. person during the year and meets the 10% or more

stock ownership requirement (vote or value) – Most missed area

• Acquires 10% or more of the vote or value in the corporation

• Acquires an additional 10% or more of the vote or value

• Disposes of 10% or more of the vote or value

Category Reporting

• Category 4 Filers: filer who had control (more than 50% direct, indirect

or constructive ownership) for an uninterrupted period of at least 30 days

during the annual accounting period of the foreign corporation.

• Category 5 Filers: filer who owns stock in a CFC for an uninterrupted

period of 30 days or more during any tax year of the foreign corporation

and who owned that stock on the last day of that year.

Biggest misses for in disclosing the category of filer are:• Don’t recognize a Category 3 filer (Usually when a non-resident becomes a resident

one forgets to ask if they may own foreign corporations.)

• Don’t prepare a Cat 3 Statement if in fact they identify the Cat 3 filer (This is always

a requirement.)

• Don’t recognize the filer meets Cat 4 or 5 through familial relationships

(Constructive ownership missed.)

Category Reporting cont.

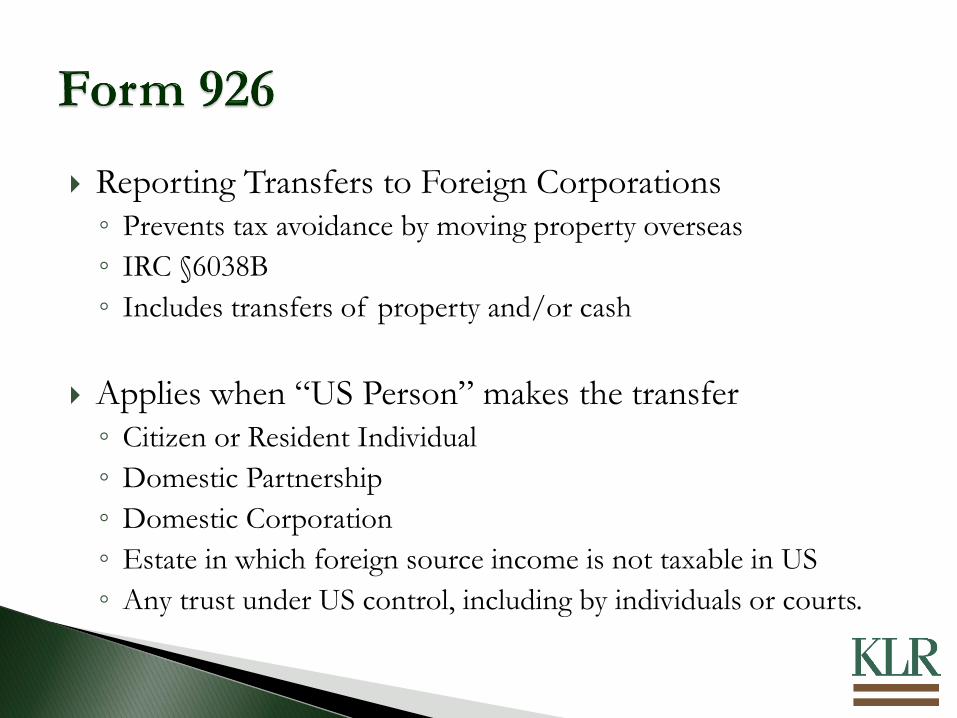

Reporting Transfers to Foreign Corporations

◦ Prevents tax avoidance by moving property overseas

◦ IRC §6038B

◦ Includes transfers of property and/or cash

Applies when “US Person” makes the transfer

◦ Citizen or Resident Individual

◦ Domestic Partnership

◦ Domestic Corporation

◦ Estate in which foreign source income is not taxable in US

◦ Any trust under US control, including by individuals or courts.

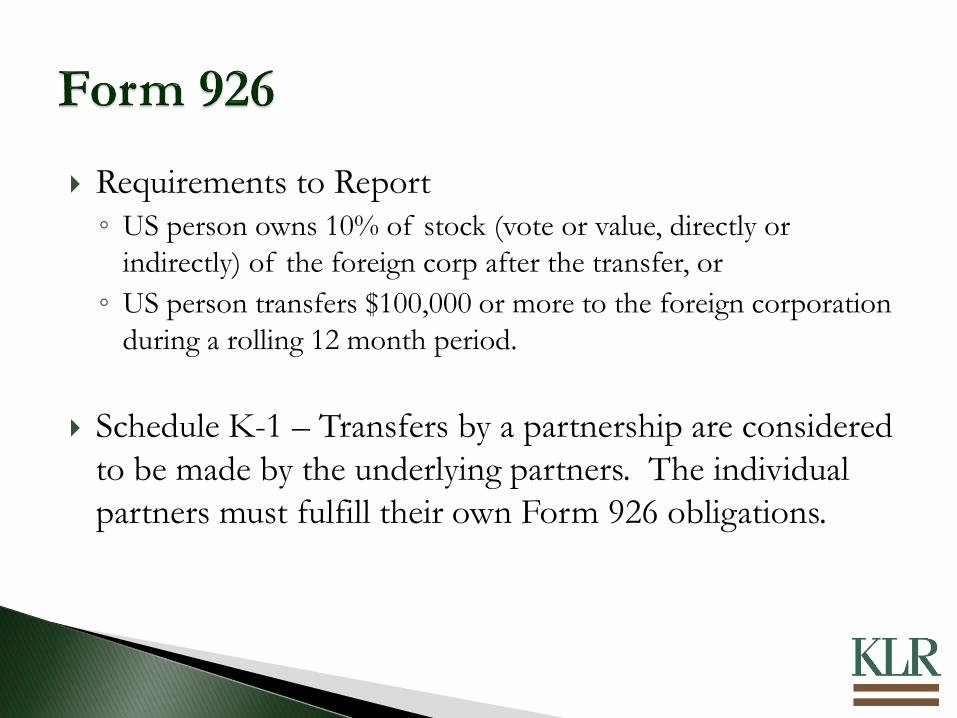

Requirements to Report

◦ US person owns 10% of stock (vote or value, directly or

indirectly) of the foreign corp after the transfer, or

◦ US person transfers $100,000 or more to the foreign corporation

during a rolling 12 month period.

Schedule K-1 – Transfers by a partnership are considered

to be made by the underlying partners. The individual

partners must fulfill their own Form 926 obligations.

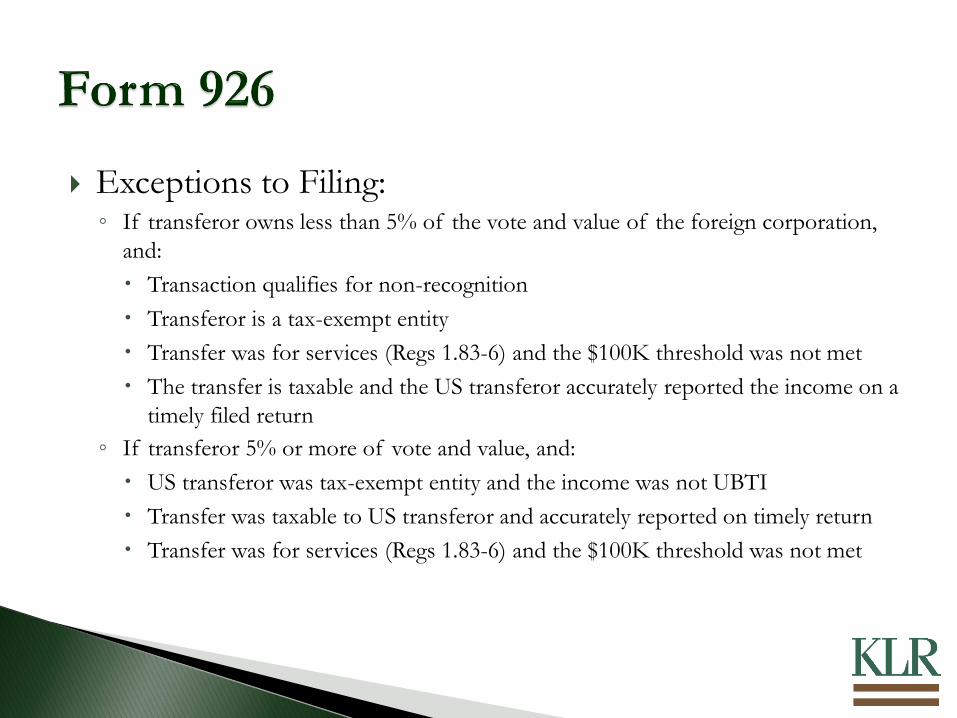

Exceptions to Filing:◦ If transferor owns less than 5% of the vote and value of the foreign corporation,

and:

Transaction qualifies for non-recognition

Transferor is a tax-exempt entity

Transfer was for services (Regs 1.83-6) and the $100K threshold was not met

The transfer is taxable and the US transferor accurately reported the income on a

timely filed return

◦ If transferor 5% or more of vote and value, and:

US transferor was tax-exempt entity and the income was not UBTI

Transfer was taxable to US transferor and accurately reported on timely return

Transfer was for services (Regs 1.83-6) and the $100K threshold was not met

Penalties for Non-Compliance under §1.6038B1(f)(1)

◦ 10% of the FMV of the property at the time of transfer, up to

$100,000, unless failure was due to intentional disregard

◦ Penalty may be abated if proof of reasonable cause can be

provided.

◦ Non-recognition treatment of an otherwise non-recognition

transfer may be revoked if the Form 926 is not properly included

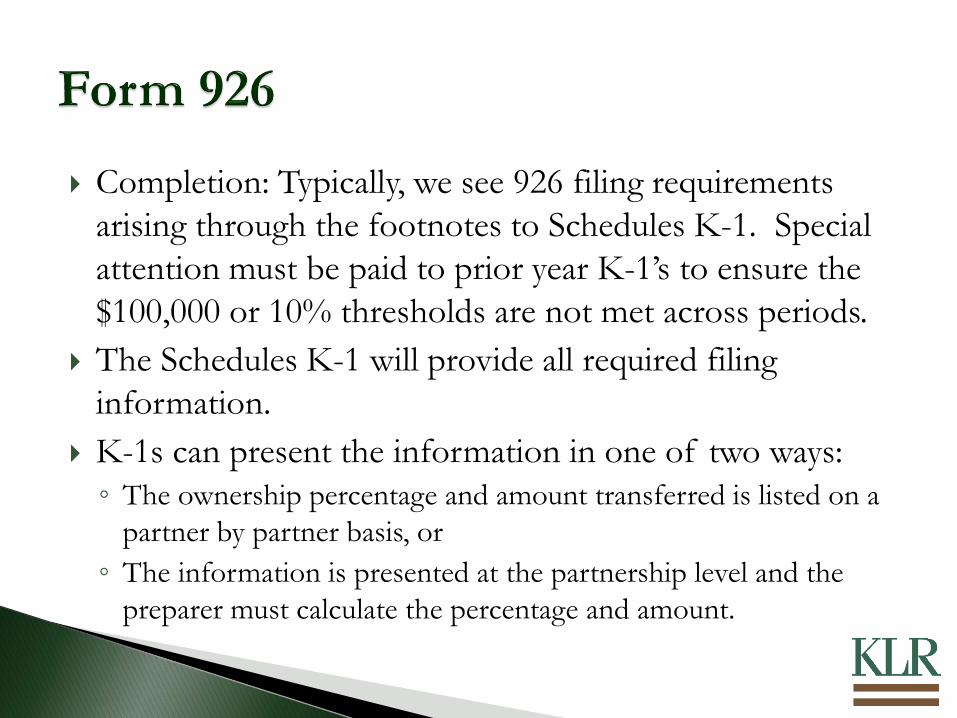

Completion: Typically, we see 926 filing requirements

arising through the footnotes to Schedules K-1. Special

attention must be paid to prior year K-1’s to ensure the

$100,000 or 10% thresholds are not met across periods.

The Schedules K-1 will provide all required filing

information.

K-1s can present the information in one of two ways:

◦ The ownership percentage and amount transferred is listed on a

partner by partner basis, or

◦ The information is presented at the partnership level and the

preparer must calculate the percentage and amount.

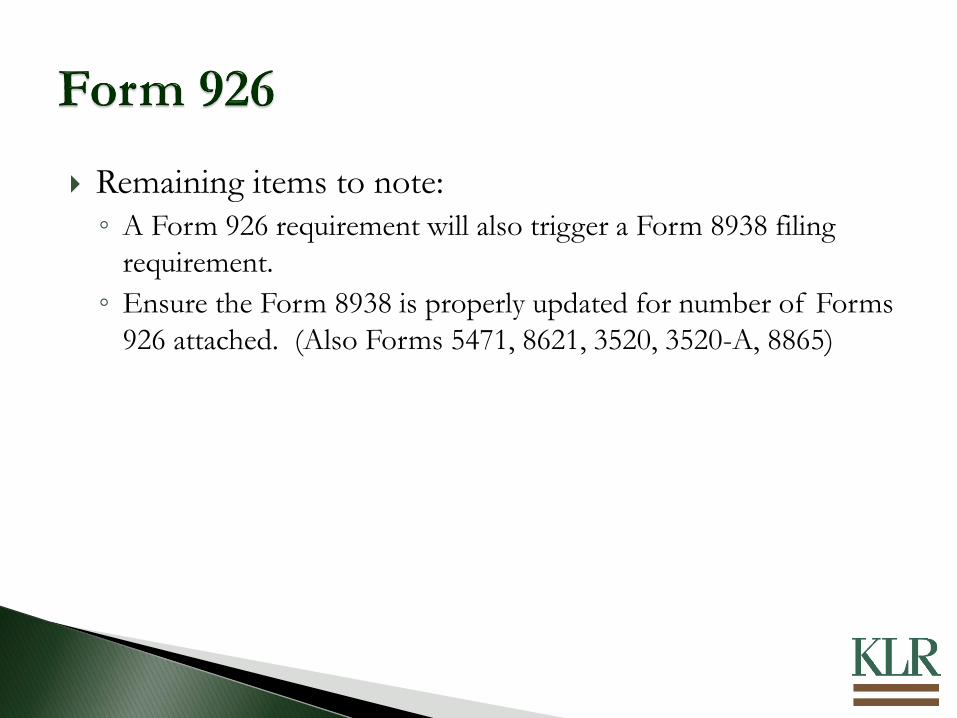

Remaining items to note:

◦ A Form 926 requirement will also trigger a Form 8938 filing

requirement.

◦ Ensure the Form 8938 is properly updated for number of Forms

926 attached. (Also Forms 5471, 8621, 3520, 3520-A, 8865)

Information Return of US Persons with respect to

Foreign Disregarded Entities – at lease 10% owned

directly, indirectly, or constructively.

Filed for each foreign disregarded entity (FDE) – by

default definition as a branch or check-the-box branch◦ An entity created or organized in a foreign jurisdiction and that is disregarded as separate from

its owner for US income tax purposes (§301.7701-2, 3)

◦ What is the IRS looking for in this filing?

Schedule C – US GAAP income statement in foreign currency and USD

Schedule C-1 – §987 Gain or Loss Information

Schedule F – Balance Sheet

Schedule G – Other information

Schedule H – Current E&P or taxable income

Section 987

◦ §987 gain/loss information is reported on Schedule C-1 as part

of 8858 filing. It requires an ultimate parent to recognize

currency gains/losses on branch remittances from a QBU with a

different functional currency:

We are talking about the recognition of historical FX

gain/loss upon the distribution of money.

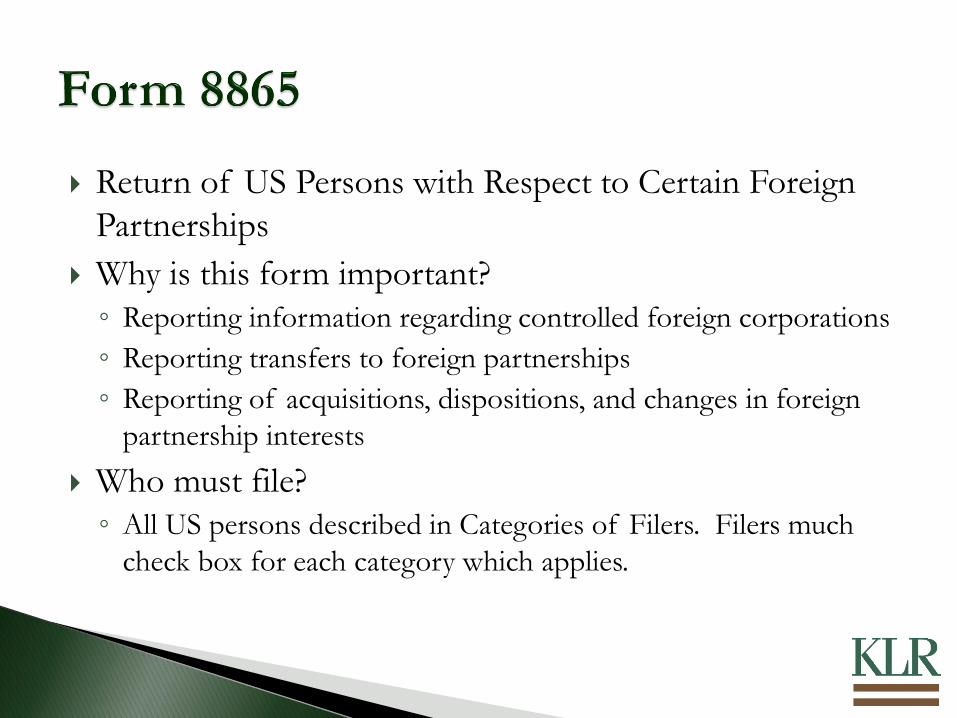

Return of US Persons with Respect to Certain Foreign

Partnerships

Why is this form important?

◦ Reporting information regarding controlled foreign corporations

◦ Reporting transfers to foreign partnerships

◦ Reporting of acquisitions, dispositions, and changes in foreign

partnership interests

Who must file?

◦ All US persons described in Categories of Filers. Filers much

check box for each category which applies.

Exceptions to Filing:

◦ Multiple Category 1 Filers

◦ Constructive Owners

◦ Members of an Affiliated Group

◦ Exception for Certain Trusts

◦ Exception for Certain Category 4 Filers

Non-Compliance:

◦ A $10,000 penalty applies for failure to file when due and in the manner

prescribed

◦ $10,000 for failure to file the delinquent returns within 90 days of the IRS

Notice, plus $10,000 penalty for each 30-day period during which the

failure continues, up to a maximum $50,000.

◦ 10% or more reduction of the foreign tax credits under §§901, 902, & 960

◦ Penalty equal to 10% of the FMV of the property at the time of

contribution subject to a $100,000 limit unless the failure was intentional

disregard. (Transferor recognizes gain as if the contributed property was

sold for FMV.)

◦ Penalties imposed under §6662(j) if the IRS finds a failure for

underpayment attributable to undisclosed foreign financial assets.

Annual Return to Report Transactions With Foreign

Trusts and Receipt of Certain Foreign Gifts

Requirements for Filing:

◦ Contribution of property to a foreign trust

◦ Treated as an owner of the foreign trust

◦ Receives a distribution from the foreign trust

Due date is same day as the Form 1040

Filed in Ogden, not with the Form 1040

Exceptions to Filing:

◦ Transfers to foreign trusts described in §§402(b), 404(a)(4), or

404A

◦ Most FMV transfers by a US person to the foreign trust

◦ Transfers, or distributions from foreign trusts, for which an IRS

determination letter of tax-exemption under §501(c)(3)

◦ Transfers to Canadian retirement plans (RRSP, RRIF)

◦ Distributions from foreign trusts treated as compensation for

services

Annual Information Return of Foreign Trust With A US

Owner

Trustee of a foreign trust must file Form 3520-A if the

trust has a US owner

US owner is responsible for making sure form is filed

Due date is same day as the Form 1040

Filed in Ogden, not with the Form 1040

Failure to File results in a maximum penalty of $10,000

Will be treated as the same capital gains as if the property

sold was in the US.

Be sure to calculate gain on the transaction in the

functional currency before converting to USD.

Research will be needed to determine taxability in the

country of sale to determine FTC implications.

If the property was your main home, you can still qualify

for the gain exclusion under §121.

Foreign Exchange Gain or Loss:

◦ Be wary of the payoff of an outstanding mortgage in a foreign

currency. A difference in the exchange rates would result in a FX

gain or loss. These gains/losses are considered personal in

nature.

◦ Personal losses are not deductible.

◦ Personal gains (short term) are taxed at graduated rates

◦ Personal gains (long term) would get the preferential cap gains

treatment.

Generally, unfunded deferred compensation

arrangements are not subject to US tax until distribution

Funded domestic deferred comp arrangements that do

not satisfy the qualified plan requirements are subject to

tax under §402(b)

Amounts contributed to, or accrued under, foreign

pension plans and funded deferred comp arrangements

that are subject to US tax are also taxed under §402(b)

Plans that qualify under §401(a)

◦ Contributions are excluded from income

◦ Earnings of the plan are not taxed to the employee

◦ Distributions are taxed as an annuity under §72

◦ Foreign plans are qualified if they meet all conditions

There are thirty-seven conditions to be met under §401(a)

◦ Foreign plans are almost never qualified

Pertains to “employees’ trust”

◦ Funds are delivered to trustee or plan manager by employer or

employee

◦ The plan manager/trustee is subject to fiduciary duties

Does not qualify under qualifications of §401(a)

Will apply to almost all foreign plans

Accounts will be treated like normal bank accounts

◦ No tax deferrals, but no trust reporting requirements

◦ Will be subject to US tax when received by NRA in the US, even if

attributable to services performed outside the US

Both employee and employer contributions are included

in income when the rights in the plan vest

There is no foreign earned income exclusion permitted

for these funds (not treated as earned income)

For purposes of FTC: US tax applies in year the interest

vests

◦ FTC will apply in the year of distribution

◦ This may cause timing issues if distribution doesn’t happen

within a year of contribution (only one year carryback)

Depending upon the treatment of the plan, there may be

reporting requirements for Form 3520.

The plan may be considered to be a foreign trust

Determining ownership of a foreign trust is under IRC

§§672-679

Employees would be taxed on the earnings of the

§402(b) plan attributable to employee contributions, but

not on earnings attributable to employer contributions

Amounts actually distributed or made available to be

distributed are considered income and taxable

The distribution is taxed as if a distribution from an

annuity under §72

This treatment exempts previously taxed amounts

Each distribution is allocated between previously taxed

amounts and untaxed earnings

Still no FEIE treatment; not considered earned

Same FTC issues as noted prior

Possible 3520 filing requirements

These materials are not intended to be written advice under IRS

Circular 230. They are of a general nature and should not be used as a

substitute for consultation with an appropriate US tax advisor in

specific situations. Additionally tax rules frequently change as the laws

are modified or re-interpreted.

KLR through its Global Tax Services group provides tax preparation and

planning services for individuals and entities subject to U.S. taxation and

information reporting requirements. Failure to deal properly with the myriad of

international issues related to U.S. taxation can result not only in the improper

computation of U.S. tax liabilities, but also in the imposition of onerous

penalties for the failure to disclose foreign related assets and transactions.

KLR’s tax services include but are not limited to the following:

Individual federal and state income

tax returns for inbound and

expatriate taxpayers

Foreign bank reports

Expatriation analysis and filings

Tax Equalization computations

Foreign related withholding forms

Treaty certification requests

Preparation of prior year returns

for the IRS voluntary disclosure

programs

Disclosure of interests in foreign

entities

KLR is an active member of the Leading Edge Global Alliance (LEA Global,)

the 2nd largest international professional association of independently-owned

accounting, financial and business advisory firms.

LEA Global enables KLR to access the resources of multibillion dollar global

professional services organization, providing additional industry expertise,

professional training and education, and peer-to-peer networking opportunities

nationally and globally, around the corner and around the world.