abrantes 2013 reluctant investor v1f

TRANSCRIPT

The Reluctant Investor and European Project Financing

in Transition

Mariana Abrantes de Sousa

PPP LusofoniaLisboa 18-Jun-2013

Efficient financial intermediationis key to competitiveness

Traditionally bank-centered, European financial intermediation is likely to become influenced by investorsavings and direct investment decisions

• Although the real Govt bong “risk-free” rate has been trending downwards towards zero

• And the BASEL-based illusion of “risk-free” Governmentbonds was dashed by the Eurozone debt crisis

• Retail savers continue reluctant to take on risk to earn higher returns

=> Professional investors have an important role to play in selecting and investing in projects offering good risk/return

Source: Hirst, http://ftalphaville.ft.com/2014/06/13/1876272/guest-post-no-you-cant-have-your-risk-free-returns-back/

Good financial intermediation adds valueInvestment <> Savings

• Agregation of investable savings

• Guarantee of deposits

• Tenor transformation, short term depositsinto long term loans

• Risk diversification

• Project /client selection

• Appraisal and due diligence

• Deal structuring, arranging

• Project risk underwriting– Construction risk

– Revenue risk , volume, price

– Operating performance risk

– Financial risk

• Pricing risk correctly

• Project monitoring, control

4http://ppplusofonia.blogspot.com

Casserly: Facing up to the risksRisk management typology

Type of credit risk portfolio Risk underwriting approach

Small, granular, homogeneous , numerous SCORING and other statistical tools

- Housing, consumer loans- SMEs

- Standardised loan contracts, securiy and pricing

- Monitoring by exception

Large, straightforward, homogeneous Rating, internal or external (outsourcingcredit analysis)

- Large corporates - Simplified contracts, lower pricing, lowmonitoring

Large, complex, unique, heterogeneous Credit analysts in-house, backstopped by experienced credit committee

- Project finance, LBO, structured finance - Intensive due diligence and monitoring- Tailored contracts, higher pricing- Seniority, protection and control

5

Captial markets potentialWhere the money is now

• Regulated (risk averse) investors

– Insurers

– Pension funds, USD 28 trillion

(19 in the US)

• Sovereign wealth funds

• Hedge funds and vulture funds

• Venture capitalists

• Specialist infrastructure funds

• … the ECB recycling to banks

6

Only the specialistinfrastructure funds havereal hands-oninvestment/lendingcapacity to arrange/structure dealsand to and to evaluate, price andassume/underwrite trafficrisk, that is to add value

by INTERMEDIATING between savers andinvestors

Dealing with project risks in PPPs

• Study it, quantify it, under multiplescenaries

• Reduce it, for example– Modular investments– Proven technology

• Mitigate it, at a cost, for example– Redudant systems– Corridor approach, add synergies– Anchor clients

• Transfer it, at a price, addingcounterparty risk

• Diversify it, portfolio approach• Price it (the residual RISK)• Survive it (capital, resilience, recoveries)

Allocate risk to theparty best able to Support it, price it,

and absorb it

Expressed preferences of Pension Funds as investors in PF bonds…

• Inflation linked debt to hedge inflation-indexed pension liabilities • Brownfield assets in operational phase, generating cash flow, no construction

risk• Good intrinsic value of project, value proposition in natural monopolies, well

regulated • Good risk –adjusted returns or very stable returns (bond proxies) • Long tenors • Liquid secondary markets, negotiable • Government guarantees • No renegotiations

• Mostly passive / indirect investors in infrastructure (only 2% of assets as direct investments )

• Most are lacking the know-how for hands-on envolvement in project finance

• Most prefer to rely on due diligence and monitoring expertise of “controllingcreditors”

8

Project revenue mechanismsand external support

Examples of Credit Enhancements• Standby liquidity facilities, stand by equity• Minimum revenue guarantees from Govt Concedent• Maturity payment guarantees from Govt Concedent• Contingent, stand-by mezzanine debt• Local government loan guarantees• Partial Risk Guarantees, ex from MIGA • Viability gap (investment) subsidies• Output based / smart (operating) subsidies and

results-based financing• …

Project risks versus counterparty risks From distress project to distressed sovereign

• Each project contract which transfers certain project risks (ex. insurance ) risk to another counterparty adds the performance and credit risk of that counterparty (ex. AIG)

• Multiple external credit enhancements can make a marginally feasible project appear more bankable

• Multiple and overlapping project contracts can complicate credit workout renegotiations in distressed project situations

• Excessive demands for external support is a warning to rethink a project

• Moving from user tariffs to availability payments, or to minimumrevenues guarantees, creditors may avoid project risks, but cannot avoidthe Concedent’s sovereign credit risk

Mariana ABRANTES de Sousa 1010

Excessive risk aversion leads to risk naiveté and economic distortions

• The general trend of "de-risking" institutional portfolios is seen in the reduction of pension fund assets allocated to global equities from about 60% in 2001-2006 to 47% in 2012

• Many institutional investors have increased "alternative assets" (including infrastructure)

• The impact of new rules on bank solvency and solvency of insurers reduces the supply of long-term bank credit

• Accounting for impairment and risk-based regulation may increase risk aversion and pro-cyclicality of credit supply

=> Recommendations

• Avoid inconsistencies (eg conflicts between the of long-term investment needs and regulation based on risk aversion)

• Clarify fiduciary duties to investors in connection with investments "green" and sustainable

• Develop new instruments for long-term investment (eg obligations of projects and specialized funds)

• Increase the role and risk absorption capacity of official development banks, especially in "segments" of difficult market

Fonte : Adapted from G. Inderst , Private Infrastructure Finance and Investment in Europe, Working Papers BEI 2013/ 02

The hands-on role of “controlling creditor”or fronting bank

• Project Finance is“secured cash flowlending”, which requires– Security, perfected

charges over the project– Protection in a robust

cash flow– Control and monitoring

of collateral andborrower performance and decision making

• Meaningful creditor oversightof complex contractual arrangements

• Aplication of incentives andcontrols

• Timely approval of drawdownrequests, waivers, consents, amendments

• Handling project stresses andcoordinating inter-creditordecision making

• Dealing with conflicts of interest between senior andsubordinated creditors

12

Conclusions• Rigorous project (traffic) due diligence is essential for

efficiency of financial intermediation and economicresource allocation; avoid due diligence “light”

• Greatest innovation needed: PPP creditors must beable to assess, assume and price, and then absorb, project (traffic) risks, in order to contribute to goodproject selection and continuing project management

• Creditors and investors must staff-up for hands-onlong term lending and prepare to take some theinevitable losses with adequate capital

http://ppplusofonia.blogspot.com 13

Annexes

Domestic savings become more important

AgênciaCurto Prazo

Notação

Longo Prazo(LP)

Notação

Outlook(LP)

ÚltimaAlteração

de Rating (LP)

ÚltimaAvaliação deRating (LP)

DBRSR-2

(middle)BBB (low) Estável

30-jan-2012Downgrade(BBB p/ BBB

(low)

26-mai-2014OutlookEstável

Fitch Ratings B BB+ Positivo24-nov-2011Downgrade

(BBB- p/ BB+)

11-abr-2014Confirmado

OutlookPositivo

Moody's Not Prime Ba2 Positivo09-mai-2014

Upgrade( Ba3 p/ Ba2)

09-mai-2014OutlookPositivo

Standard & Poor's

B BB Estável13-jan-2012Downgrade(BBB- p/ BB)

09-mai-2014OutlookEstável

NOTA: Alterações de Outlook não são consideradas alterações de notação de rating. http://www.igcp.pt/gca/?id=54, retrieved 16-Jun-2014

Sorereign credit rating – Republica Portuguesa

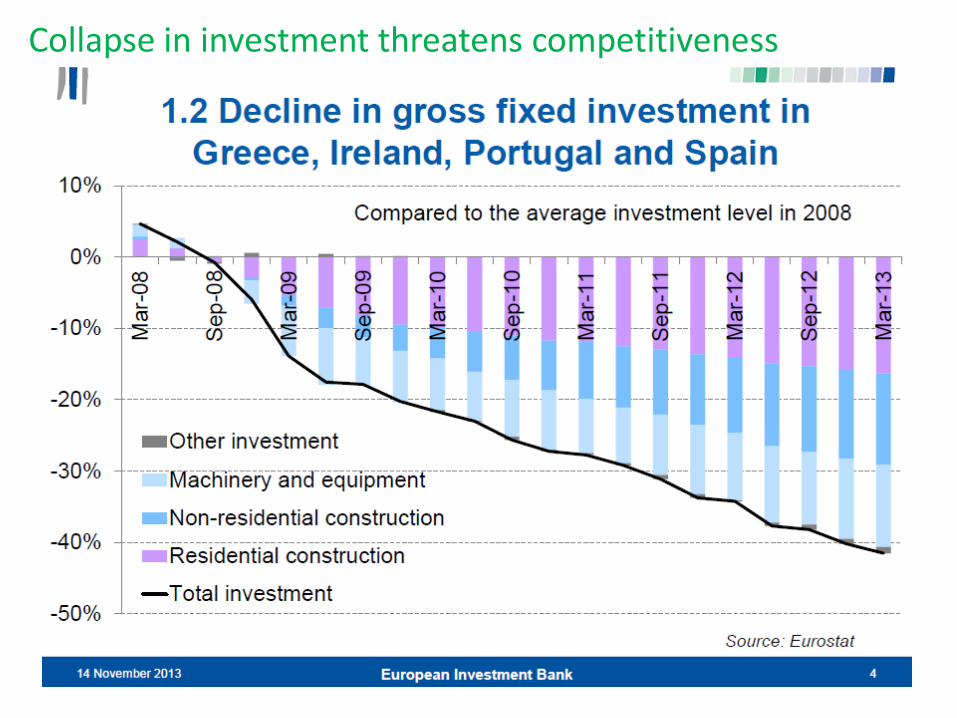

Collapse in investment threatens competitiveness

Severe colapse in deficit countries