about this new manual - mastercard · about this new manual ... and describes the objectives of the...

TRANSCRIPT

Information about this New Manual

New Manual This SecureCode Merchant Implementation Guide, dated September 2005, is an entirely new manual.

Contents This manual contains excerpts from the SecureCode Member Enrollment and Implementation Guide, and describes the objectives of the SecureCode Electronic Commerce Program, enablement requirements and options for participating members, roles, responsibilities, and obligations of program participants, and the implementation and testing procedures, with specific focus on the SecureCode issuer platforms based on the SPA algorithm.

Please refer to “Using this Manual” for a complete list of the contents of this manual.

Billing MasterCard will bill principal members for this document in printed format. Please refer to the MasterCard Consolidated Billing System Manual for billing-related information.

Questions? If you have questions about this manual, please contact the Customer Operations Services team or your regional help desk. Please refer to “Using this Manual” for more contact information.

MasterCard is Listening…

Please take a moment to provide us with your feedback about the material and usefulness of the SecureCode Merchant Implementation Guide using the following e-mail address:

We continually strive to improve our publications. Your input will help us accomplish our goal of providing you with the information you need.

SecureCode Merchant Implementation Guide September 2005

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 Publication Code: SMI

Copyright The information contained in this manual is proprietary and confidential to MasterCard International Incorporated (MasterCard) and its members.

This material may not be duplicated, published, or disclosed, in whole or in part, without the prior written permission of MasterCard.

Legal Notice This document contains the proprietary and confidential

information of MasterCard International Incorporated (“MasterCard”). Such information may not be used for any unauthorized purpose and may not be published or disclosed to third parties, in whole or part, without the express written permission of MasterCard. You acknowledge and agree that between you and MasterCard this document and all portions thereof, including, but not limited to, any copyright, trade secret and other intellectual property rights relating thereto, are and at all times shall remain the sole property of MasterCard and that title and full ownership rights in the information contained herein and all portions thereof are reserved to and at all times shall remain with MasterCard. You agree to safeguard the confidentiality of the information contained herein using the same standard you employ to safeguard your own confidential information of like kind, but in no event less than a commercially reasonable standard of care. If you do not agree with the foregoing conditions, you are required to return this document immediately to MasterCard.

Trademarks Trademark notices and symbols used in this manual reflect the

registration status of MasterCard trademarks in the United States. Please consult with the Customer Operations Services team or the MasterCard Law Department for the registration status of particular product, program, or service names outside the United States.

All third-party product and service names are trademarks or registered trademarks of their respective owners.

Media This document is available:

• On MasterCard OnLine®

• On the MasterCard Electronic Library (CD-ROM)

MasterCard International Incorporated 2200 MasterCard Boulevard O’Fallon MO 63368-7263 USA

1-636-722-6100

www.mastercard.com

Sep 2005

Table of Contents

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 i

Using this Guide

Purpose...................................................................................................................1

Audience.................................................................................................................1

Overview ................................................................................................................1

Excerpted Text .......................................................................................................3

Language Use .........................................................................................................3

Times Expressed.....................................................................................................3

Revisions.................................................................................................................4

Support ...................................................................................................................4 Regional Representative...................................................................................5

Section 1 Overview

MasterCard and Electronic Commerce ...............................................................1-1

Maestro and Electronic Commerce.....................................................................1-1

The Opportunity to Grow Your Online Business with the MasterCard SecureCode Program...........................................................................................1-2

MasterCard SecureCode Platform Components .................................................1-3 What is UCAF?...............................................................................................1-3 What is an AAV?............................................................................................1-5 What is a Merchant Plug-In? .........................................................................1-5

Section 2 MasterCard SecureCode 3-D Secure Solution Overview

Overview .............................................................................................................2-1

Components ........................................................................................................2-2 Issuer Domain ...............................................................................................2-2 Acquirer Domain...........................................................................................2-3

Table of Contents

© 2005 MasterCard International Incorporated

ii September 2005 • SecureCode Merchant Implementation Guide

Interoperability Domain................................................................................2-3

Messages ..............................................................................................................2-5 Card Range Request/Response.....................................................................2-5 Verification Request/Response .....................................................................2-5 Payer Authentication Request/Response......................................................2-5 Payer Authentication Transaction Request/Response .................................2-6

Cardholder Enrollment........................................................................................2-7 Cardholder Enrollment Process ....................................................................2-7 Sample Cardholder Enrollment Flow ...........................................................2-8

Cardholder Authentication ................................................................................2-13 Sample Cardholder Authentication Process ...............................................2-13 Sample Cardholder Authentication Flow ...................................................2-15

Section 3 Merchants

Overview .............................................................................................................3-3

Infrastructure .......................................................................................................3-4 Establishment of SecureCode Operating Environment ...............................3-4 Authorization System Enhancements ...........................................................3-4 Maestro Considerations.................................................................................3-6

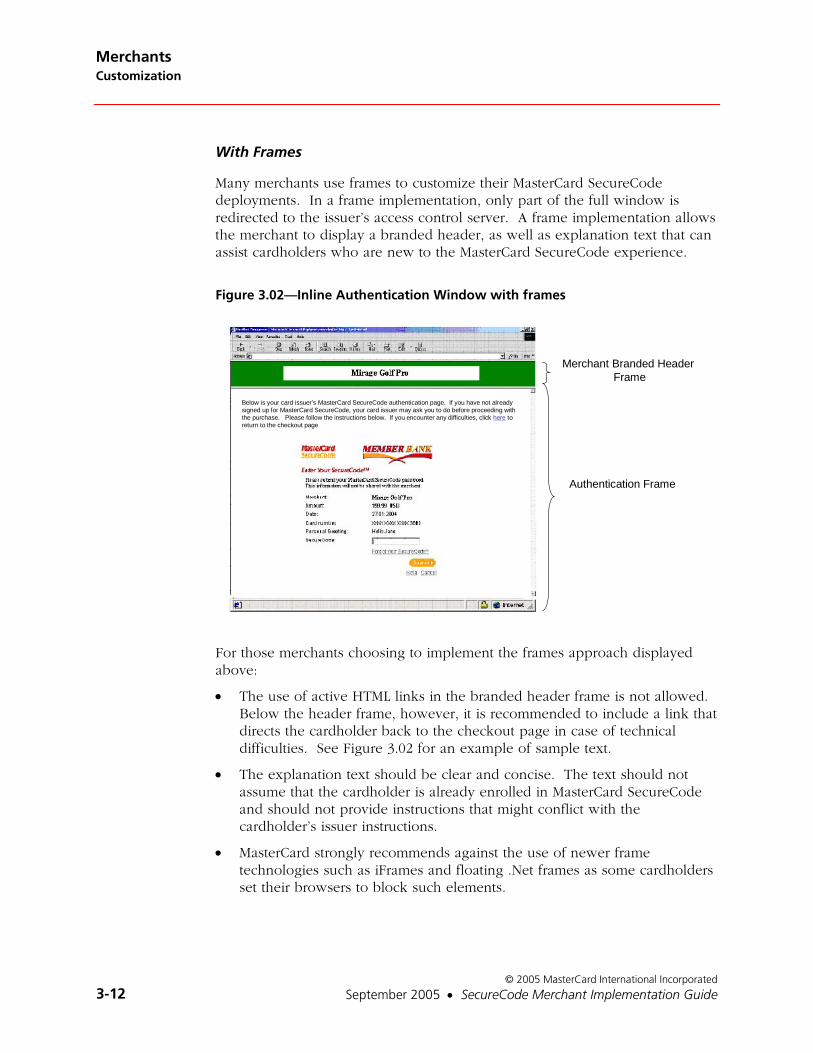

Customization ......................................................................................................3-8 Program Identifier Usage Guidelines ...........................................................3-8 Integrated Support for Merchant Plug-In Processing ..................................3-8 Consumer Message on Payment Page .......................................................3-10 Creation of Cardholder Authentication Window .......................................3-10 TERMURL field ............................................................................................3-13 Replay Detection.........................................................................................3-14 Merchant Server Plug-In Configuration......................................................3-14

Operational........................................................................................................3-17 Loading of MasterCard Root Certificates ....................................................3-17 Loading of MasterCard SSL Client Certificate.............................................3-17 MPI Log Monitoring ....................................................................................3-17 MPI Authentication Request/Response Archival........................................3-17

Accountholder Authentication Value (AAV) Processing..................................3-18

Table of Contents

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 iii

Identification of SPA AAV format in PARes ...............................................3-18 Validation of Payer Authentication Response (PARes) signature .............3-18

Global Infrastructure Testing Requirements.....................................................3-19

MasterCard SecureCode Participating Merchant Listings .................................3-19

Merchant Processing Matrix ..............................................................................3-20

Appendix A Merchant Customer Service Guide

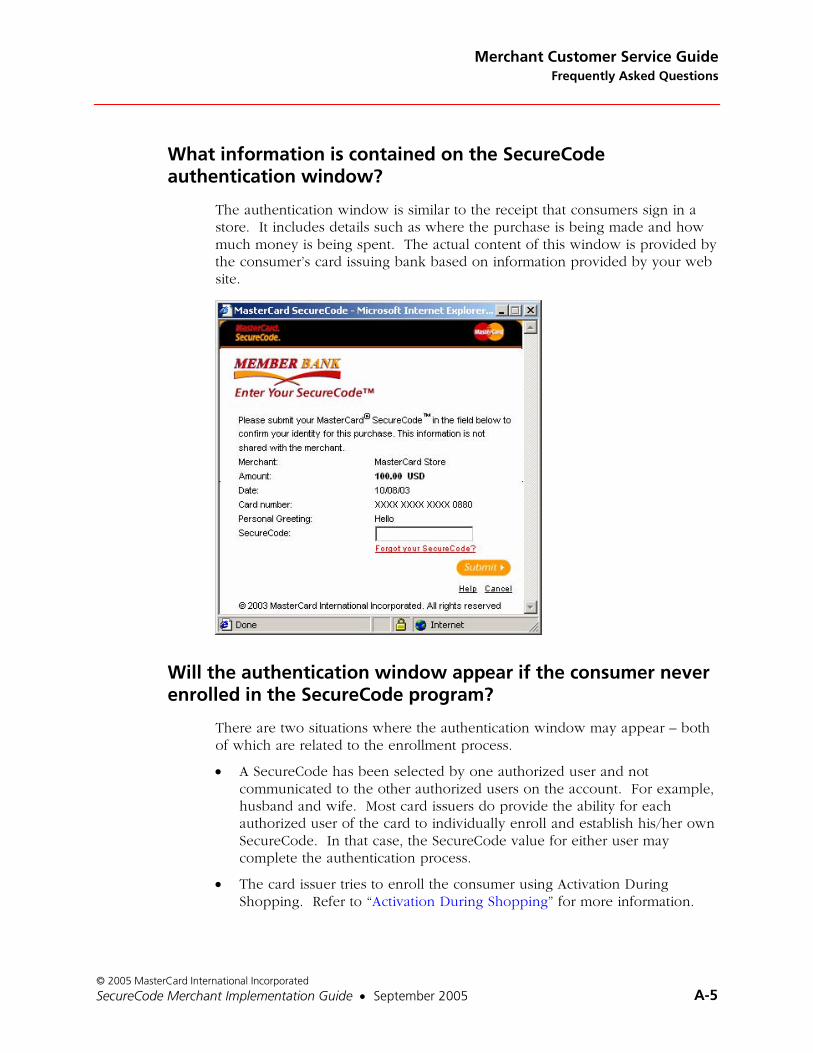

Overview ............................................................................................................ A-1 Audience....................................................................................................... A-1 Purpose......................................................................................................... A-1

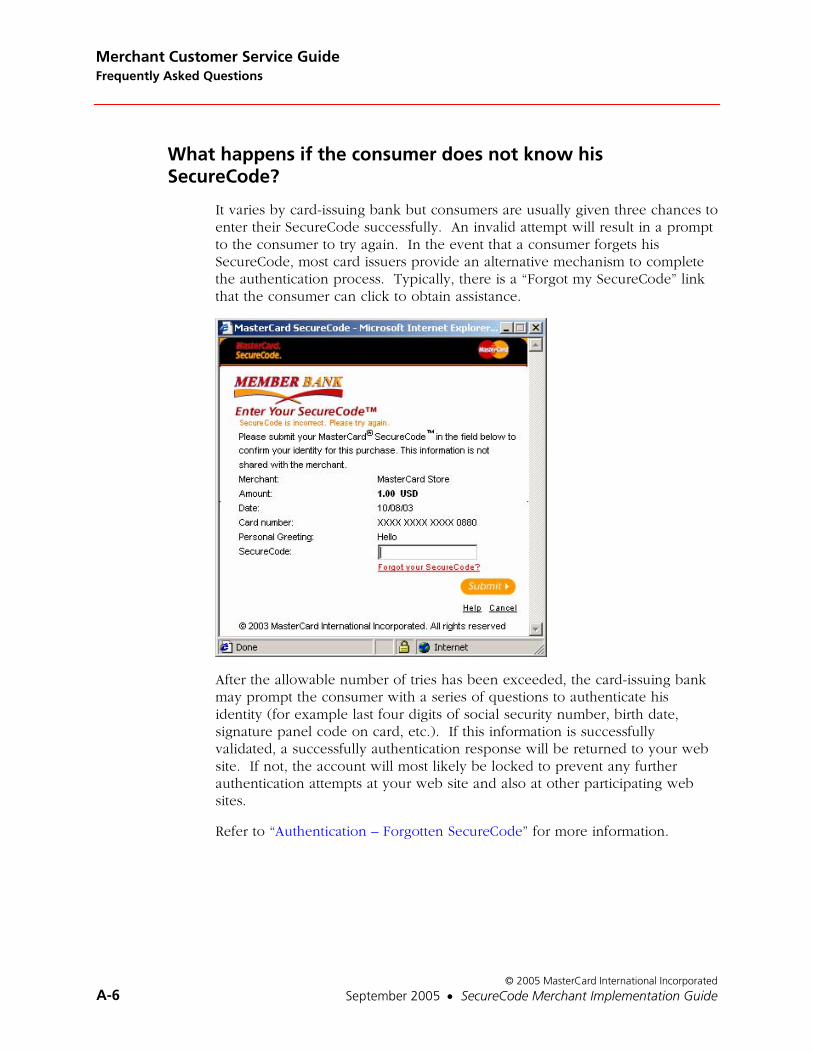

Frequently Asked Questions.............................................................................. A-2 What is MasterCard® SecureCode™? .......................................................... A-2 What is a SecureCode?................................................................................. A-2 What is the format of a SecureCode? .......................................................... A-2 Why is our web site supporting SecureCode? ............................................ A-2 How does our web site support SecureCode?............................................ A-2 What is a Personal Greeting? ....................................................................... A-3 What is the difference between authentication and authorization?........... A-3 How does MasterCard SecureCode work? .................................................. A-3 What is the difference between a pop-up and an inline authentication window? ............................................................................... A-4 How does our web site know if a card is protected by MasterCard SecureCode? ................................................................................................. A-4 Who knows the consumer’s SecureCode? .................................................. A-4 What are the consumer’s system requirements for MasterCard SecureCode? ................................................................................................. A-5 How does a consumer enroll in the SecureCode program?....................... A-5 What information is contained on the SecureCode authentication window?........................................................................................................ A-5 Will the authentication window appear if the consumer never enrolled in the SecureCode program?......................................................... A-6 What happens if the consumer does not know his SecureCode?.............. A-6 What is pop-up killer software and what happens if it is installed on the consumer’s PC?................................................................................. A-7 What happens if authentication fails?.......................................................... A-8

Table of Contents

© 2005 MasterCard International Incorporated

iv September 2005 • SecureCode Merchant Implementation Guide

What happens if the consumer does not choose to enroll or does not enter his SecureCode? ........................................................................... A-8 What happens if the consumer clicks the “x” in the top right corner of the authentication window? .................................................................... A-9

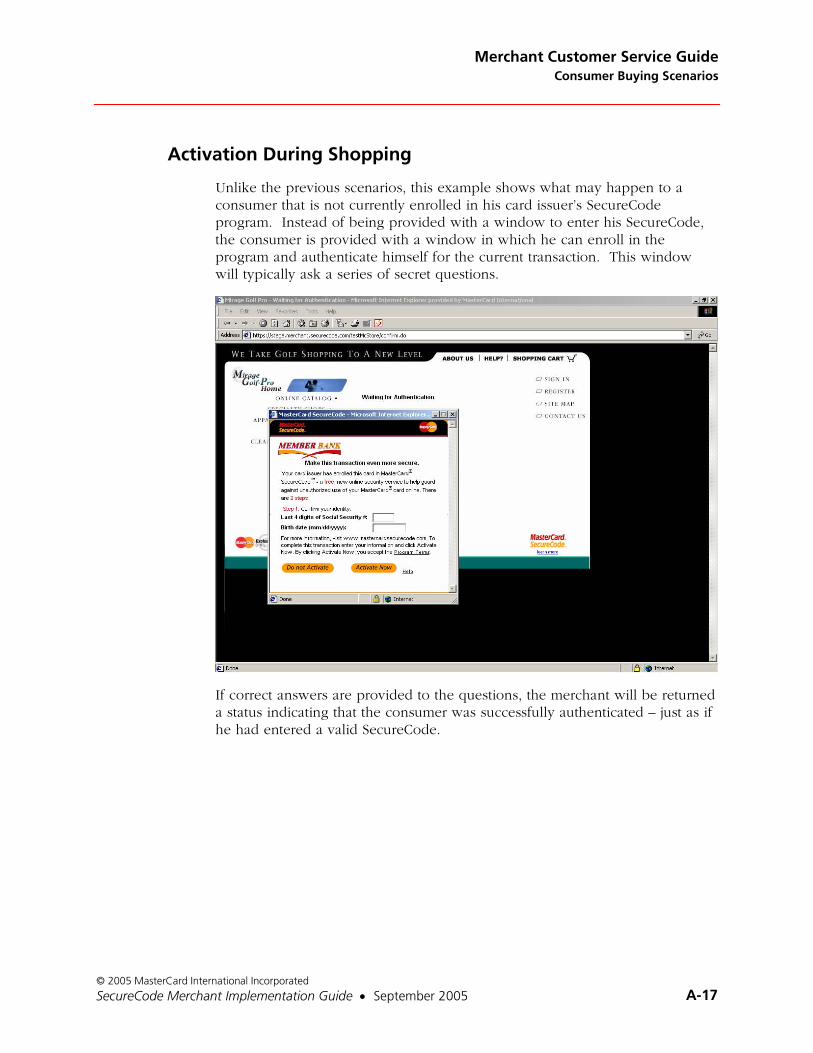

Cardholder Enrollment..................................................................................... A-10 Traditional Cardholder Enrollment............................................................ A-10 Activation During Shopping ...................................................................... A-10

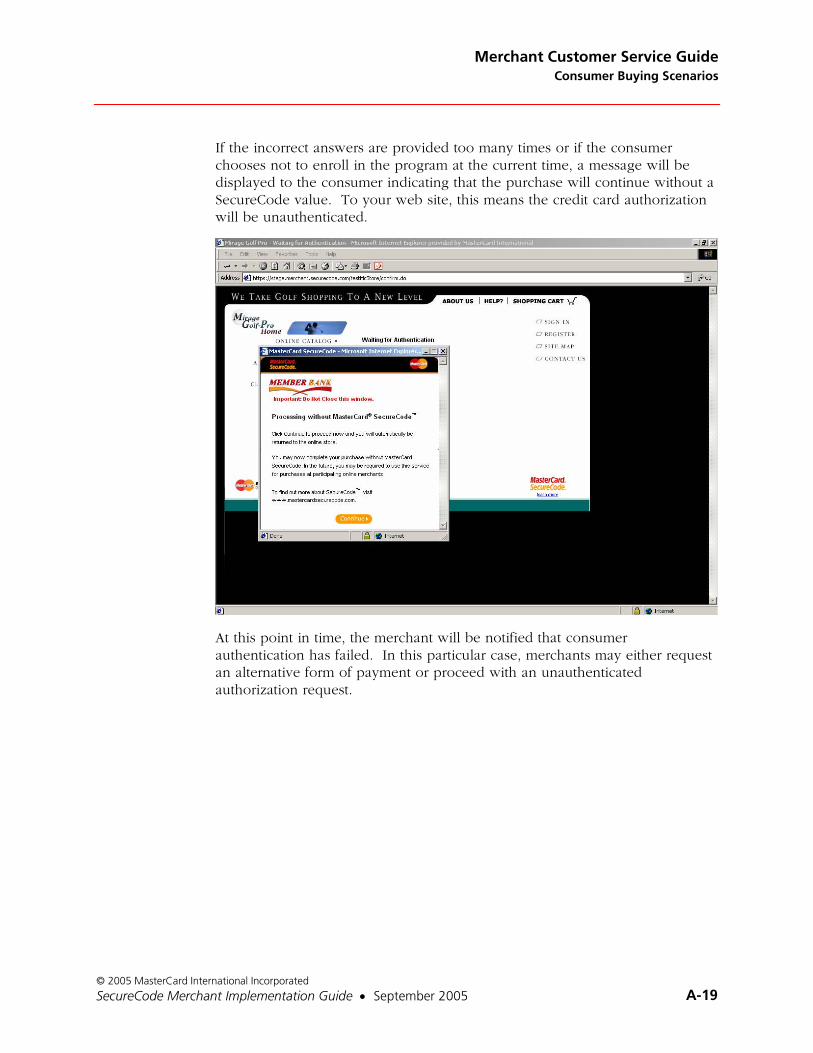

Consumer Buying Scenarios ............................................................................ A-12 Authentication - Successful........................................................................ A-13 Authentication – Forgotten SecureCode ................................................... A-14 Authentication – Failed .............................................................................. A-16 Authentication – Account Locked ............................................................. A-18 Authentication – “X’ing” Out The Window............................................... A-19 Activation During Shopping ...................................................................... A-22 Activation During Shopping – Opt Out of Enrollment ............................ A-25

Appendix B MasterCard SecureCode SPA Algorithm Specification

Overview ............................................................................................................ B-1

Accountholder Authentication Value Layout .................................................... B-2

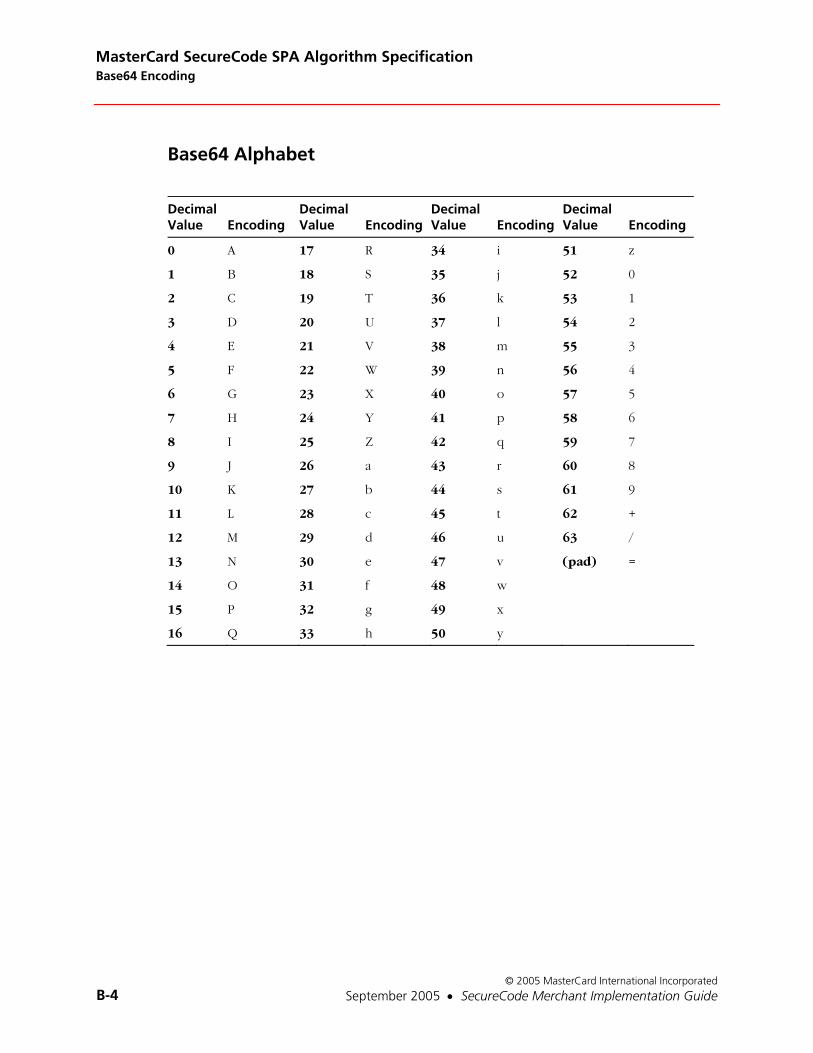

Base64 Encoding ................................................................................................ B-3 Introduction.................................................................................................. B-3 Examples ...................................................................................................... B-3 Base64 Alphabet........................................................................................... B-6

Appendix C Contact Information

Contact Information ........................................................................................... C-1

Appendix D MasterCard SecureCode Program Identifier Usage Guidelines

General Standards of Use ..................................................................................D-1 Authorized Use.............................................................................................D-1

Table of Contents

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 v

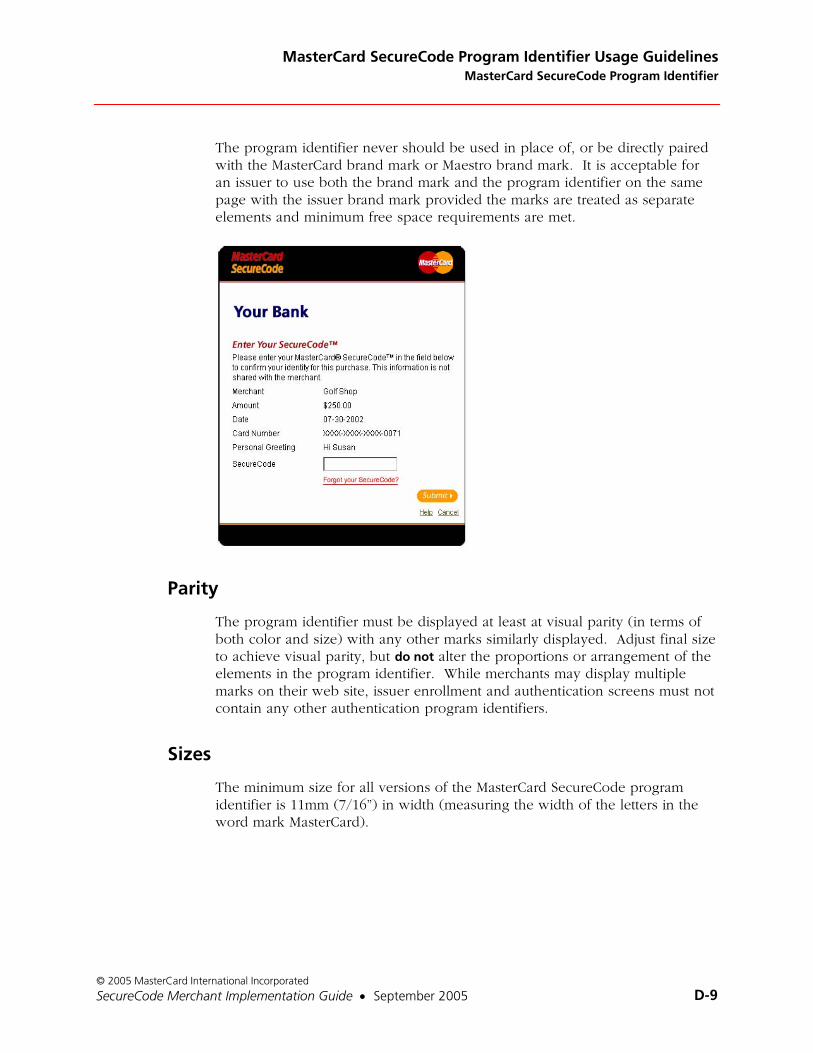

MasterCard SecureCode Word Mark..................................................................D-1

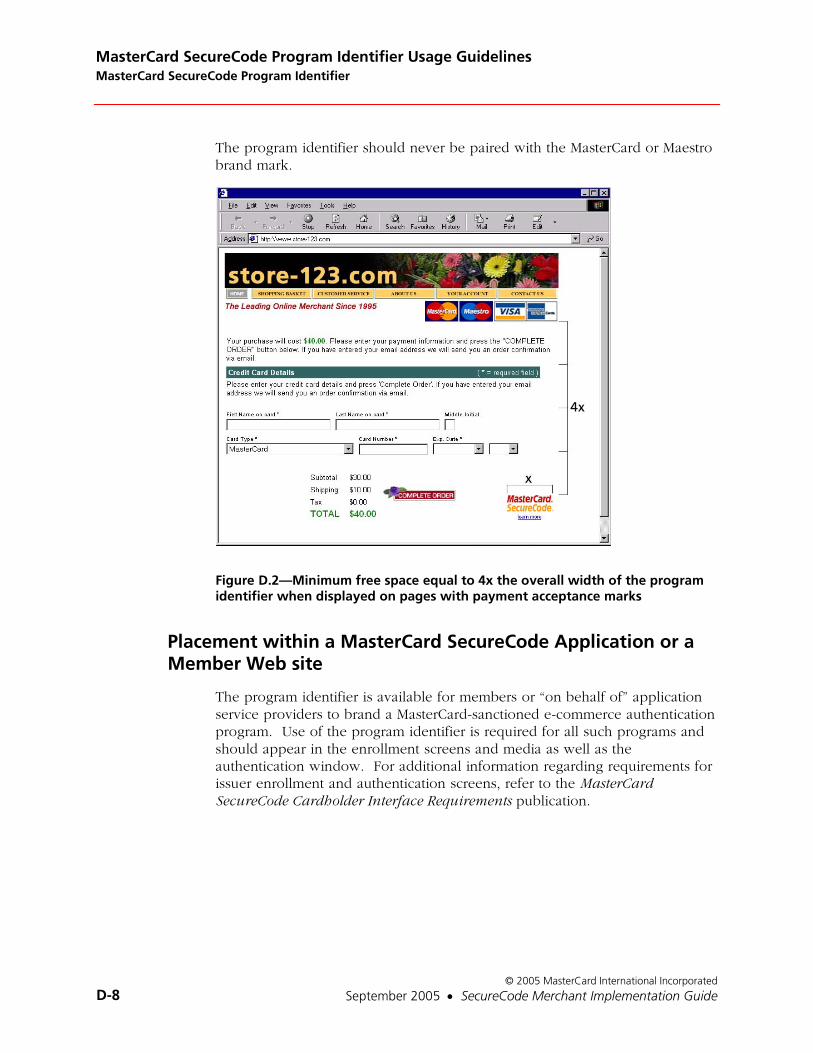

MasterCard SecureCode Program Identifier ......................................................D-2 Approved Versions.......................................................................................D-2 Placement on a Merchant Website..............................................................D-6 Placement within a MasterCard SecureCode Application or a Member Website ..........................................................................................D-8 Parity.............................................................................................................D-9 Sizes ..............................................................................................................D-9

Authorized Artwork..........................................................................................D-10

For More Information.......................................................................................D-10

Appendix E Maestro Considerations

Account in Good Standing..................................................................................E-1

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 i

Using this Guide This chapter contains information that helps you understand and use this document.

Purpose...................................................................................................................1

Audience.................................................................................................................1

Overview ................................................................................................................1

Excerpted Text .......................................................................................................2

Language Use .........................................................................................................2

Times Expressed.....................................................................................................3

Revisions.................................................................................................................3

Support ...................................................................................................................4 Regional Representative...................................................................................4

Using this GuidePurpose

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 1

Purpose The SecureCode Merchant Implementation Guide describes the following:

• Objectives of the MasterCard SecureCode Electronic Commerce Program

• MasterCard and Maestro offering, benefits, and enablement requirements and options for participating members

• Roles, responsibilities, and obligations of both MasterCard and program participants

• Implementation and testing procedures, with specific focus on the MasterCard SecureCode issuer platforms based on the SPA algorithm.

Audience This manual is intended for use by MasterCard and Maestro members who are considering participating in the MasterCard SecureCode Electronic Commerce Program.

Overview The following table provides an overview of this manual:

Chapter Description

Table of Contents A list of the manual’s chapters and subsections. Each entry references a chapter and page number.

Using this Guide A description of the manual’s purpose and its contents.

1 Overview Provides a general overview of the MasterCard SecureCode Electronic Commerce program.

2 MasterCard SecureCode 3-D Secure Solution Overview

Provides a general overview of MasterCard’s implementation of 3-D Secure for MasterCard® cards and Maestro® cards, including cardholder enrollment and payer authentication.

3 Merchants Provides a general overview of the various activities and requirements associated with building and maintaining the merchant components required to support MasterCard SecureCode.

A Merchant Customer Service Guide

Overview of the MasterCard SecureCode service, along with an understanding of the consumer experience, in order to provide assistance to customers when needed

Using this Guide Excerpted Text

© 2005 MasterCard International Incorporated

2 September 2005 • SecureCode Merchant Implementation Guide

Chapter Description

B MasterCard SecureCode SPA Algorithm Specification

Layout of the Accountholder Authentication Value (AAV) to be used by issuers participating in MasterCard SecureCode, as well as an overview of Base64 encoding

C Contact Information MasterCard contact information

D MasterCard SecureCode Program Identifier Usage Guidelines

Contains guidelines, which are intended for all use of the MasterCard SecureCode word mark and/or the MasterCard SecureCode program identifier

E Maestro Considerations

Contains detailed information regarding Maestro specific processing issues associated with MasterCard SecureCode

Excerpted Text At times, this document may include text excerpted from another document. A note before the repeated text always identifies the source document. In such cases, we included the repeated text solely for the reader’s convenience. The original text in the source document always takes legal precedence.

Language Use The spelling of English words in this manual follows the convention used for U.S. English as defined in Merriam-Webster’s Collegiate Dictionary. MasterCard is incorporated in the United States and publishes in the United States. Therefore, this publication uses U.S. English spelling and grammar rules.

An exception to the above spelling rule concerns the spelling of proper nouns. In this case, we use the local English spelling.

Using this GuideTimes Expressed

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 3

Times Expressed MasterCard is a global company with locations in many time zones. The MasterCard operations and business centers are in the United States. The operations center is in St. Louis, Missouri, and the business center is in Purchase, New York.

For operational purposes, MasterCard refers to time frames in this manual as either “St. Louis time” or “New York time.” Coordinated Universal Time (UTC) is the basis for measuring time throughout the world. You can use the following table to convert any time used in this manual into the correct time in another zone:

St. Louis,

Missouri USA

Central Time

Purchase, New York USA

Eastern Time UTC

Standard time

(last Sunday in October to the first Sunday in April a)

9:00 10:00 15:00

Daylight saving time

(first Sunday in April to last Sunday in October)

9:00 10:00 14:00

a For Central European Time, last Sunday in October to last Sunday in March.

Revisions MasterCard periodically will issue revisions to this document as we implement enhancements and changes, or as corrections are required.

With each revision, we include a Summary of Changes describing how the text changed. Revision markers (vertical lines in the right margin) indicate where the text changed. The date of the revision appears in the footer of each page.

Occasionally, we may publish revisions or additions to this document in a Global Operations Bulletin or other bulletin. Revisions announced in another publication, such as a bulletin, are effective as of the date indicated in that publication, regardless of when the changes are published in this manual.

Using this Guide Support

© 2005 MasterCard International Incorporated

4 September 2005 • SecureCode Merchant Implementation Guide

Support Please address your questions to the Customer Operations Services team as follows:

Phone: 1-800-999-0363 or 1-636-722-6176 1-636-722-6292 (Spanish Language support)

Fax: 1-636-722-7192

E-mail: Canada, Caribbean, and U.S. [email protected] Asia/Pacific [email protected] Europe [email protected] South Asia/Middle East/Africa [email protected] Latin America (Spanish

Language support) [email protected]

Address: MasterCard International Incorporated Customer Operations Services 2200 MasterCard Boulevard O’Fallon MO 63368-7263 USA

Telex: 434800 answerback: 434800 ITAC UI

Regional Representative

The regional representatives work out of the regional offices. Their role is to serve as intermediaries between the members and other departments in MasterCard. Members can inquire and receive responses in their own language and during their office’s hours of operation.

To find out the location of the regional office serving your area, call the Customer Operations Services team at:

Phone: 1-800-999-0363 or 1-636-722-6176

1-636-722-6292 (Spanish Language support)

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 1-i

1 Overview This section provides a general overview of the MasterCard SecureCode Electronic Commerce program.

MasterCard and Electronic Commerce ...............................................................1-1

Maestro and Electronic Commerce.....................................................................1-1

The Opportunity to Grow Your Online Business with the MasterCard SecureCode Program...........................................................................................1-2

MasterCard SecureCode Platform Components .................................................1-3 What is UCAF?...............................................................................................1-3

UCAF Structure........................................................................................1-3 What is an AAV?............................................................................................1-5 What is a Merchant Plug-In? .........................................................................1-5

OverviewMasterCard and Electronic Commerce

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 1-1

MasterCard and Electronic Commerce Electronic commerce transactions account for an increasing share of MasterCard and member gross dollar volume, currently estimated at more than 8%. The number of remote transactions is increasing at a rate of 30% to 35% per year. For this reason, it is important to position electronic commerce and mobile commerce channels to increase gross dollar volume profitability by using security and authentication solutions that authenticate cardholders, thereby reducing chargebacks and expenses associated with disputed transactions.

From a risk perspective, the current MasterCard electronic and mobile transaction environment closely resembles traditional mail order/telephone order (MO/TO) transactions. The remote nature of these transactions increases risk, resulting in more cardholder disputes, and associated chargebacks.

These factors increase costs to MasterCard members for managing disputes and chargebacks. Approximately 60% of all chargebacks for electronic commerce transactions are associated with reason code 4837 – No Cardholder Authorization or reason code 4863 Cardholder Not Recognized, where the consumer denies responsibility for the transaction and the acquirer lacks evidence of the cardholder’s authentication or the consumer does not recognize the transaction.

Proving that the cardholder conducted and authorized the transaction in a virtual, non-face-to-face environment of electronic and mobile commerce has been extremely difficult. The MasterCard SecureCode program is designed to provide the infrastructure for an issuer security solution that reduces problems associated with disputed charges that impact all parties in a transaction – the issuer, the acquirer, the cardholder and the merchant.

Maestro and Electronic Commerce Low credit card penetration in many countries has led to inefficient payment forms like cash on delivery, check, and domestic transfer/ACH. MasterCard SecureCode will allow Maestro® cards to be used for Internet purchases in a safe and secure environment. Currently there are over 560 million Maestro® cards and MasterCard SecureCode will allow Maestro to be the first fully authenticated global online debit brand accepted on the Internet. Unless otherwise stated by domestic country rules, all Maestro Internet transactions will be guaranteed.

Sep 2005

Sep 2005

Overview The Opportunity to Grow Your Online Business with the MasterCard SecureCode Program

© 2005 MasterCard International Incorporated

1-2 September 2005 • SecureCode Merchant Implementation Guide

The Opportunity to Grow Your Online Business with the MasterCard SecureCode Program

MasterCard SecureCode offers flexible, robust and easy to implement solutions for cardholder authentication. Recognizing that one size does not fit all, MasterCard places a premium on flexibility, enabling issuers to choose from a broad array of security solutions for authenticating their cardholders including both password and smart card-based approaches.

Based on the MasterCard implementation of 3-D Secure, MasterCard and Maestro issuers may use issuer assigned or cardholder selected passwords to authenticate their cardholders. Issuers may also choose to utilize the Chip Authentication Protocol (CAP), which provides for the creation of a one-time use cardholder authentication password, similar to what the cardholder experiences in a face-to-face environment using chip and pin. This program provides a seamless integration of both EMV and 3-D Secure technologies that result in stronger authentication than traditional static password solutions.

MasterCard SecureCode is the MasterCard consumer-and-merchant-facing name for all existing and new MasterCard cardholder authentication solutions. While these solutions may each appear quite different on the surface, these various approaches converge around UCAF and share a number of common features. Hence the common program name – MasterCard SecureCode.

In every case, for example, two things occur:

1. The MasterCard® or Maestro® cardholder is authenticated using a secure private code unique to them (MasterCard SecureCode). With both password and Chip Authentication Program implementations of MasterCard SecureCode, an authentication box appears on the order confirmation page and prompts the cardholder for their SecureCode. In a password-based implementation, the cardholder enters the SecureCode previously registered with the issuer. With the Chip Authentication Program, the cardholder inserts her/her smart card into a card reader and enters the challenge and his/her PIN. Then, the chip generates a value that the cardholder places into the issuer authentication window as the SecureCode.

2. The authentication data is transported from party to party via the MasterCard UCAF mechanism.

Sep 2005

Sep 2005

OverviewMasterCard SecureCode Platform Components

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 1-3

MasterCard SecureCode Platform Components The MasterCard SecureCode Platform is comprised of a number of layered components. Each of the components, as described below, provides for specific authorization and authentication functionality during the processing of a MasterCard SecureCode transaction. When combined, the platform provides a mechanism for online merchants to receive a similar global payment guarantee to one that brick-and-mortar retailers enjoy with physical point-of-sale transactions.

What is UCAF?

UCAF Structure

UCAF (Universal Cardholder Authentication Field) is a standard, globally interoperable method of collecting cardholder authentication data at the point of interaction across all channels, including the Internet and mobile devices.

Within the MasterCard authorization networks (for example Banknet, MDS, RSC, EPSnet), UCAF is a universal, multi-purpose data transport infrastructure that is used to communicate authentication information among cardholder, issuer, merchant and acquirer communities. It is a variable length, 32-position field with a flexible data structure that can be tailored to support the needs of a variety of issuer security and authentication approaches.

Overview MasterCard SecureCode Platform Components

© 2005 MasterCard International Incorporated

1-4 September 2005 • SecureCode Merchant Implementation Guide

The generic structure of UCAF is illustrated below:

Con

trol B

yte

Application-Specific Data

1 BinaryByte

Max 23 Binary Bytes

Max 32 characters (after Base64 encoding)

The control byte contains a value that is specific to each security application. MasterCard is responsible for assigning and managing UCAF control byte values and the structure of UCAF application specific data. Other solutions, which utilize UCAF for authentication collection and transport, will be assigned its own control byte value and the structure of the application-specific data will be tailored to support the specifics of the security protocol.

The current SecureCode control byte definitions include:

Usage Base64 Encoded

Value Hexadecimal

Value

3-D Secure SPA AAV for first and subsequent transactions

J x’8C’

3-D Secure SPA AAV for attempts H x’86’

In most UCAF implementations, the application specific data is defined as binary data with a maximum length of 24 binary bytes – including the control byte. However, there are some restrictions in the various MasterCard authorization networks regarding the passing of binary data in the authorization messages. As a result, all UCAF data generated by SPA algorithm-based MasterCard SecureCode implementations must be base64 encoded at some point prior to being included in the authorization message. The purpose of this encoding is to produce a character representation of the associated binary data. This results in a character representation that is approximately 33% larger than the binary equivalent. For this reason, the UCAF field is defined with a maximum length of 32 positions. For additional information on base64 encoding, refer to appendix A, “MasterCard SecureCode SPA AAV.”

OverviewMasterCard SecureCode Platform Components

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 1-5

What is an AAV?

The Accountholder Authentication Value (AAV) is a MasterCard SecureCode specific token that uses the UCAF field for transport within MasterCard authorization messages. It is generated by the issuer and presented to the merchant for placement in the authorization request upon successful authentication of the cardholder.

In the case of a chargeback or other potential dispute processing, the AAV will be used to identify the processing parameters associated with the transaction. Among other things, the field values will identify:

• The issuer ACS that created the AAV.

• The sequence number that can be used to positively identify the transaction within the universe of transactions for that location.

• The secret key used to create the Message Authentication Code (MAC), which is a cryptographic method that will not only ensure AAV data integrity but also bind the entire AAV structure to a specific PAN.

UCAF is the mechanism that is used to transmit the AAV from the merchant to issuer for authentication purposes during the authorization process.

What is a Merchant Plug-In?

As part of the MasterCard SecureCode infrastructure requirements, all merchant end-points must implement application software capable of processing 3-D Secure messages. An end-point is described as any merchant or merchant processor platform, which directly connects to the MasterCard SecureCode infrastructure.

A merchant plug-in is a software application that is developed and tested to be compliant with the 3-D Secure protocol and interoperable with the MasterCard SecureCode infrastructure. The plug-in application is typically provided by a technology vendor and integrated with the merchant’s commerce server. It serves as the controlling application for the processing of 3-D Secure messages.

Sep 2005

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-i

2 MasterCard SecureCode 3-D Secure Solution Overview This chapter provides a general overview of the MasterCard implementation of 3-D Secure for MasterCard® cards and Maestro® cards, including cardholder enrollment and payer authentication.

Overview .............................................................................................................2-1

Components ........................................................................................................2-2 Issuer Domain ...............................................................................................2-2

Cardholder Browser and Related Cardholder Software ........................2-2 Enrollment Server ...................................................................................2-2 Access Control Server .............................................................................2-2 AAV Validation Server/Process ..............................................................2-2

Acquirer Domain...........................................................................................2-3 Merchant Plug-In.....................................................................................2-3 Signature Validation Server ....................................................................2-3

Interoperability Domain................................................................................2-3 Directory Server ......................................................................................2-3 Certificate Authority ................................................................................2-4 Transaction History Server .....................................................................2-4 Attempts Server .......................................................................................2-4

Messages ..............................................................................................................2-5 Card Range Request/Response.....................................................................2-5 Verification Request/Response .....................................................................2-5 Payer Authentication Request/Response......................................................2-5 Payer Authentication Transaction Request/Response .................................2-6

Cardholder Enrollment........................................................................................2-7 Cardholder Enrollment Process ....................................................................2-7 Sample Cardholder Enrollment Flow ...........................................................2-8

Welcome .................................................................................................2-8 Enter Your Card Number........................................................................2-9 Terms & Conditions and Privacy Policy ................................................2-9 Validate Your Identity...........................................................................2-10 Validate Your Identity...........................................................................2-10 Create Your SecureCode ......................................................................2-11

MasterCard SecureCode 3-D Secure Solution Overview

© 2005 MasterCard International Incorporated

2-ii September 2005 • SecureCode Merchant Implementation Guide

Congratulations .....................................................................................2-12

Cardholder Authentication ................................................................................2-13 Sample Cardholder Authentication Process ...............................................2-13 Sample Cardholder Authentication Flow ...................................................2-15

Enter Payment Information ..................................................................2-15 Confirm and Submit Order...................................................................2-15 Enter Your SecureCode ........................................................................2-16 Purchase Completed.............................................................................2-16

MasterCard SecureCode 3-D Secure Solution OverviewOverview

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-1

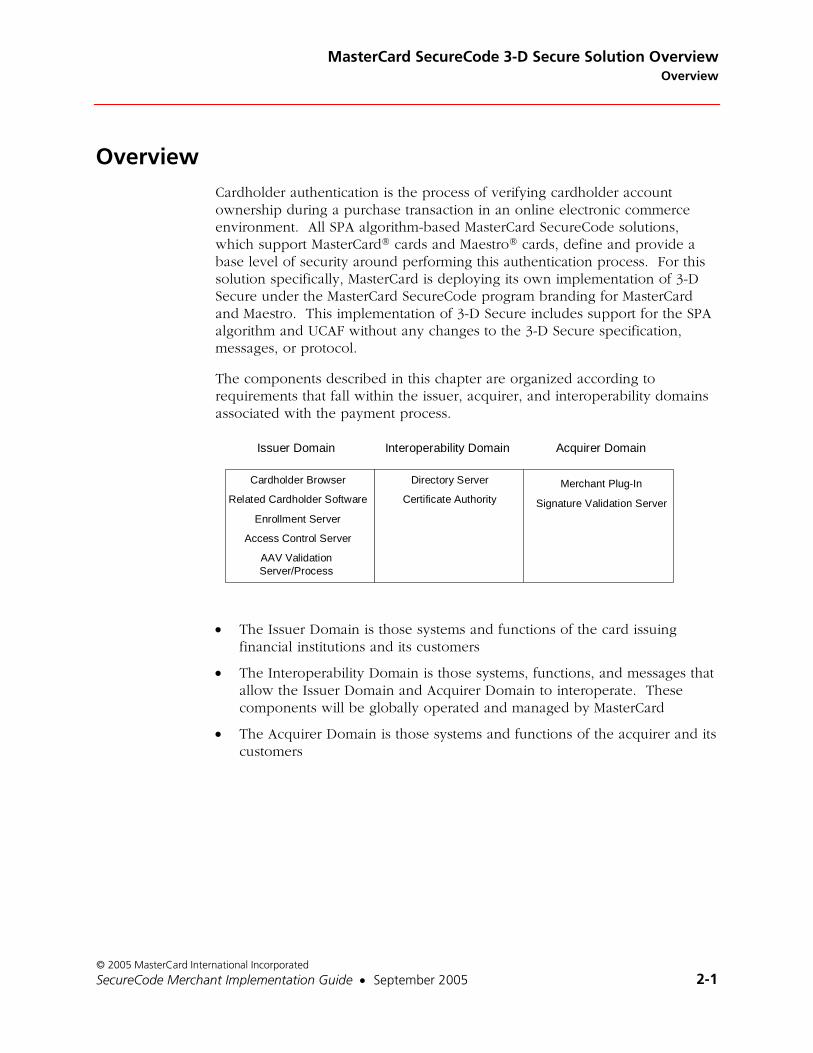

Overview Cardholder authentication is the process of verifying cardholder account ownership during a purchase transaction in an online electronic commerce environment. All SPA algorithm-based MasterCard SecureCode solutions, which support MasterCard® cards and Maestro® cards, define and provide a base level of security around performing this authentication process. For this solution specifically, MasterCard is deploying its own implementation of 3-D Secure under the MasterCard SecureCode program branding for MasterCard and Maestro. This implementation of 3-D Secure includes support for the SPA algorithm and UCAF without any changes to the 3-D Secure specification, messages, or protocol.

The components described in this chapter are organized according to requirements that fall within the issuer, acquirer, and interoperability domains associated with the payment process.

Cardholder Browser

Related Cardholder Software

Enrollment Server

Access Control Server

AAV Validation Server/Process

Directory Server

Certificate AuthorityMerchant Plug-In

Signature Validation Server

Issuer Domain Interoperability Domain Acquirer Domain

• The Issuer Domain is those systems and functions of the card issuing financial institutions and its customers

• The Interoperability Domain is those systems, functions, and messages that allow the Issuer Domain and Acquirer Domain to interoperate. These components will be globally operated and managed by MasterCard

• The Acquirer Domain is those systems and functions of the acquirer and its customers

MasterCard SecureCode 3-D Secure Solution Overview Components

© 2005 MasterCard International Incorporated

2-2 September 2005 • SecureCode Merchant Implementation Guide

Components

Issuer Domain

Cardholder Browser and Related Cardholder Software

The Cardholder browser acts as a conduit to transport messages between the Merchant Server Plug-In (in the Acquirer Domain) and the Access Control Server (in the Issuer Domain). Optional cardholder software to support implementations such as chip cards may also be included.

Both the browser and related software are considered to be off-the-shelf components that do not require any specific modification to support 3-D Secure.

Enrollment Server

The purpose of the enrollment server is to facilitate the process of cardholder enrollment for an issuer’s implementation of 3-D Secure under the MasterCard SecureCode program. The server will be used to perform initial cardholder authentication, as well as administrative activities such as SecureCode resets and viewing 3-D Secure payment history. In some cases, the enrollment server and the access control server may be packaged together.

Access Control Server

The access control server serves two basic, yet vital, functions during the course of a MasterCard SecureCode online purchase. First, it will verify whether a given account number is enrolled in the MasterCard SecureCode program. Secondly, it will facilitate the actual cardholder authentication process.

AAV Validation Server/Process

This server or process will be used to perform validation of the cardholder authentication data received by the issuer’s authorization system in the authorization messages.

Sep 2005

MasterCard SecureCode 3-D Secure Solution OverviewComponents

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-3

Acquirer Domain

Merchant Plug-In

The merchant server plug-in creates and processes payer authentication messages and then returns control to the merchant software for further authorization processing. The plug-in is invoked after the cardholder finalizes the purchase request, which includes selecting the account number to be used, and submitting the order but prior to obtaining authorization for the purchase.

Signature Validation Server

The signature validation server is used to validate the digital signature on purchase requests that have been successfully authenticated by the issuer. This server may be integrated with the merchant plug-in or may be a separately installed component.

Interoperability Domain

Directory Server

The MasterCard SecureCode global directory server provides centralized decision-making capabilities to merchants enrolled in the MasterCard SecureCode program. Based on the account number contained in the merchant enrollment verification request message, the directory will first determine whether the account number is part of a participating MasterCard or Maestro issuer’s card range. It will then direct eligible requests to the appropriate issuer’s access control server for further processing.

All implementations of this issuer platform must use the MasterCard SecureCode global directory server for processing MasterCard® card and Maestro® card transactions.

MasterCard SecureCode 3-D Secure Solution Overview Components

© 2005 MasterCard International Incorporated

2-4 September 2005 • SecureCode Merchant Implementation Guide

Certificate Authority

The MasterCard Certificate Authority is used to generate and distribute all private hierarchy end-entity and subordinate certificates, as required, to the various components and subordinate certificate authorities across all three domains. These certificates include:

• MasterCard Root certificate (used for both MasterCard and Maestro)

• SSL Server and Client certificates issued under the MasterCard hierarchy

• Issuer Digital Signing certificates issued under the MasterCard hierarchy

Additionally, SSL certificates based on a public root hierarchy are required. These certificates are not issued by the MasterCard Certificate Authority and must be obtained from another commercially available certificate-issuing provider.

Transaction History Server

The MasterCard SecureCode infrastructure does not support this component server.

Attempts Server

The MasterCard SecureCode infrastructure does not support this component server.

Sep 2005

MasterCard SecureCode 3-D Secure Solution OverviewMessages

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-5

Messages

Card Range Request/Response

Message Pair: CRReq/CRRes

For performance reasons, the Merchant Server Plug-In has the capability to cache the card ranges contained in the Directory, which indicate issuer participation in 3-D Secure. The Card Range Request/Response messages are used by the Merchant Server Plug-In as a way to request updates to the cache from the Directory.

Verification Request/Response

Message Pair: VEReq/VERes

The first step in the payer authentication process is to validate that the cardholder account number is part of an issuer’s card range, which is participating in 3-D Secure. The Verification Request/Response messages are sent from the Merchant Server Plug-In to the Directory to check card range eligibility. If the specified account number is contained within a SecureCode eligible card range, this message is then sent from the Directory to the Access Control Server to check if the specific account number is enrolled and active to participate in 3-D Secure.

For those merchants that cache the contents of the MasterCard SecureCode directory server, this message is not used if the cache indicates that the issuer is not enrolled in 3-D Secure. If the cache does indicate that the issuer is enrolled, or if no cache is being maintained, this message must be formatted and processed as described.

Payer Authentication Request/Response

Message Pair: PAReq/PARes

Once it has been determined that a cardholder is enrolled to participate in 3-D Secure, the actual process of payer authentication is performed for each online purchase. The Payer Authentication Request/Response messages are sent from the Merchant Server Plug-In to the Access Control Server to perform the actual authentication. It is at this point in the process where the cardholder will be presented with an authentication window and asked to enter his SecureCode.

Sep 2005

MasterCard SecureCode 3-D Secure Solution Overview Messages

© 2005 MasterCard International Incorporated

2-6 September 2005 • SecureCode Merchant Implementation Guide

The Access Control Server will perform authentication and, if successful, generate an Accountholder Authentication Value (AAV). This information, if received by the merchant, must be sent to the acquirer and forwarded to the issuer as part of the authorization request.

Payer Authentication Transaction Request/Response

Message Pair: PATransReq/PATransRes

Following authentication, it may be desirable to centralize storage of authentication requests for later dispute processing. The Payer Authentication Transaction Request/Response messages provide a record of this authentication activity sent from the ACS to the History Server.

The MasterCard SecureCode global infrastructure does not support these messages.

MasterCard SecureCode 3-D Secure Solution OverviewCardholder Enrollment

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-7

Cardholder Enrollment

Cardholder Enrollment Process

Enrollment is the process whereby authorized MasterCard and Maestro branded cardholders will activate their cards for a specific issuer’s MasterCard SecureCode program. Part of the planning process for building a 3-D Secure infrastructure will involve determining exactly how this process will work.

The major component associated with enrollment is the enrollment server. It is responsible for driving the process under which:

• The cardholder validates that his account number is designated as eligible to participate in MasterCard SecureCode by the card issuing financial institution.

• The cardholder is authenticated by the card issuing financial institution through the validation of secret questions, independently determined by each issuer participating in the program.

• The cardholder sets up and defines his SecureCode

• The cardholder performs functions such as profile administration (including SecureCode and e-mail changes) and review of recent purchases.

Enrollment Server

Issuer or 3rd PartyValidation

Acct Holder

File

Internet1

2

3

4

In a typical example:

1. The cardholder visits an issuer enrollment site. This may be accessible, for example, from the issuer’s web site or home banking system.

MasterCard SecureCode 3-D Secure Solution Overview Cardholder Enrollment

© 2005 MasterCard International Incorporated

2-8 September 2005 • SecureCode Merchant Implementation Guide

2. The cardholder is asked to provide issuer identified enrollment data. During this phase of the process, the cardholder will be asked a series of secret questions to prove his identity to the issuer.

3. The enrollment data, or answers to the secret questions, is validated by the issuer.

4. If the appropriate answers are provided, the cardholder is considered to be authenticated and is allowed to establish his SecureCode to be associated with the specified account number. The SecureCode is stored by the issuer for later use during online purchases at participating merchants.

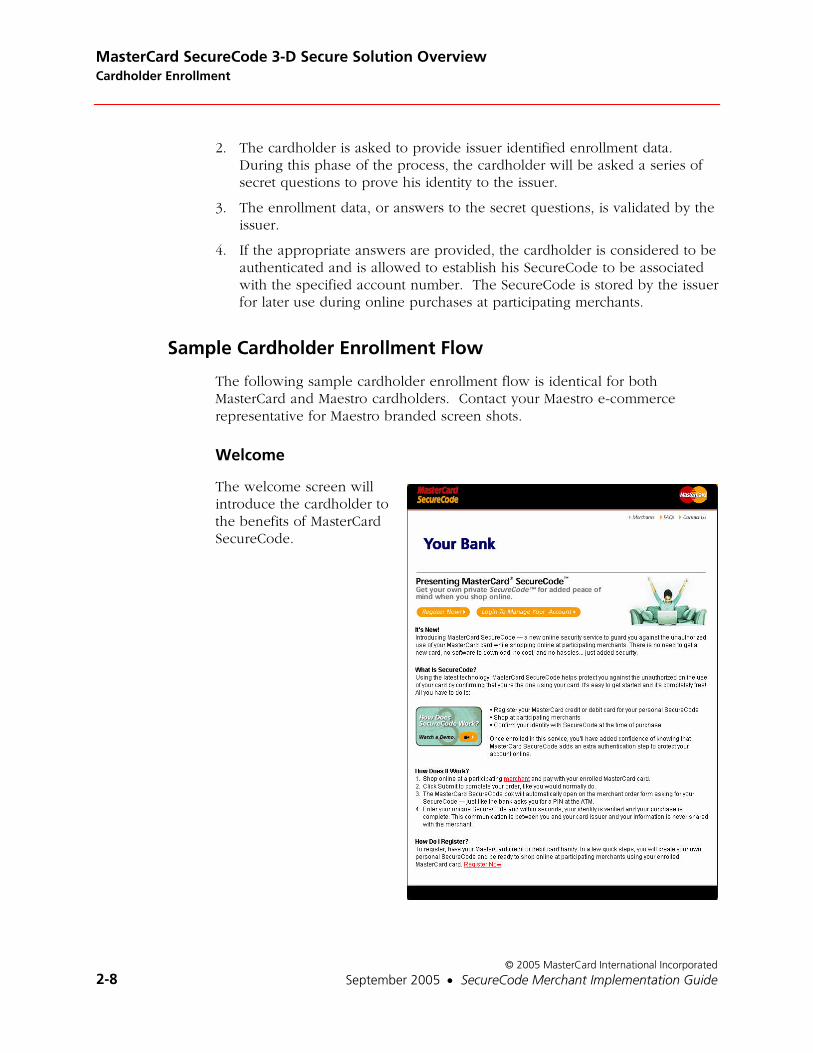

Sample Cardholder Enrollment Flow

The following sample cardholder enrollment flow is identical for both MasterCard and Maestro cardholders. Contact your Maestro e-commerce representative for Maestro branded screen shots.

Welcome

The welcome screen will introduce the cardholder to the benefits of MasterCard SecureCode.

MasterCard SecureCode 3-D Secure Solution OverviewCardholder Enrollment

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-9

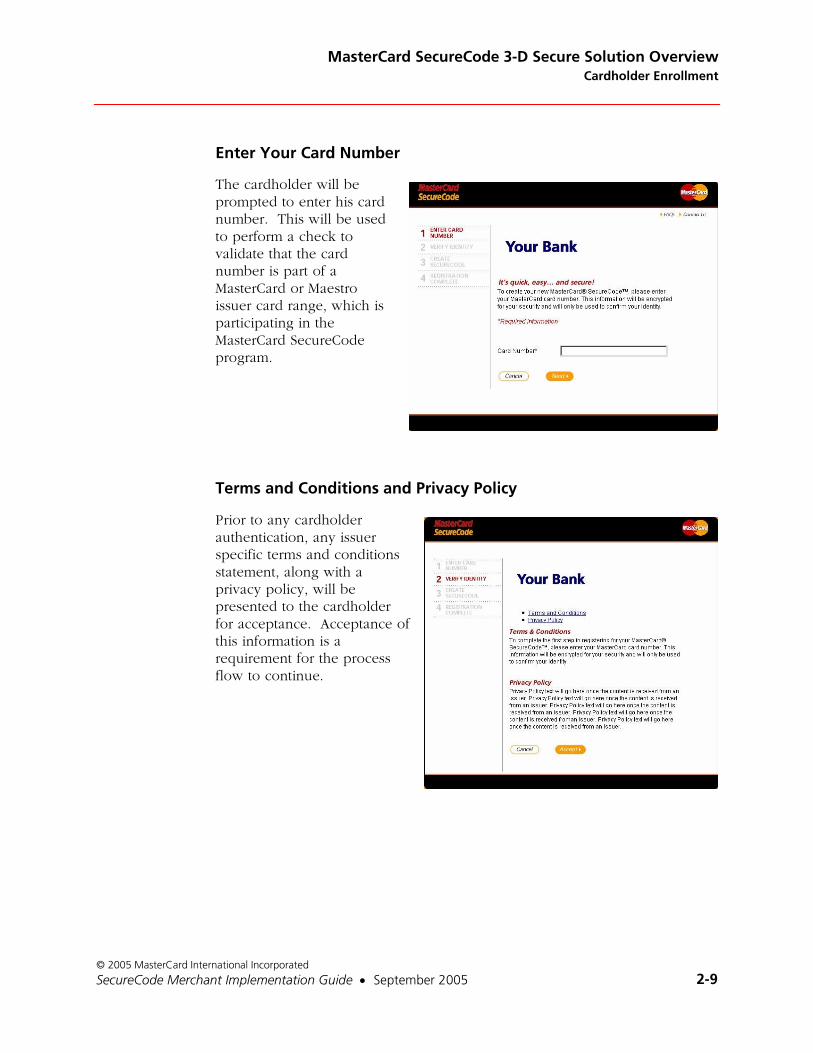

Enter Your Card Number

The cardholder will be prompted to enter his card number. This will be used to perform a check to validate that the card number is part of a MasterCard or Maestro issuer card range, which is participating in the MasterCard SecureCode program.

Terms and Conditions and Privacy Policy

Prior to any cardholder authentication, any issuer specific terms and conditions statement, along with a privacy policy, will be presented to the cardholder for acceptance. Acceptance of this information is a requirement for the process flow to continue.

MasterCard SecureCode 3-D Secure Solution Overview Cardholder Enrollment

© 2005 MasterCard International Incorporated

2-10 September 2005 • SecureCode Merchant Implementation Guide

Validate Your Identity

This is the first of two displays that may be used to collect cardholder authentication data. The “Name on Card” field allows for MasterCard SecureCode registration of multiple individuals using the same account number (for example husband and wife).

Only the name and expiration date fields are required. All additional fields are customizable as determined by the issuer.

Validate Your Identity

This screen is the second of two, which may be used to collect cardholder authentication data. All questions on this screen are customizable as determined by the issuer.

MasterCard SecureCode 3-D Secure Solution OverviewCardholder Enrollment

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-11

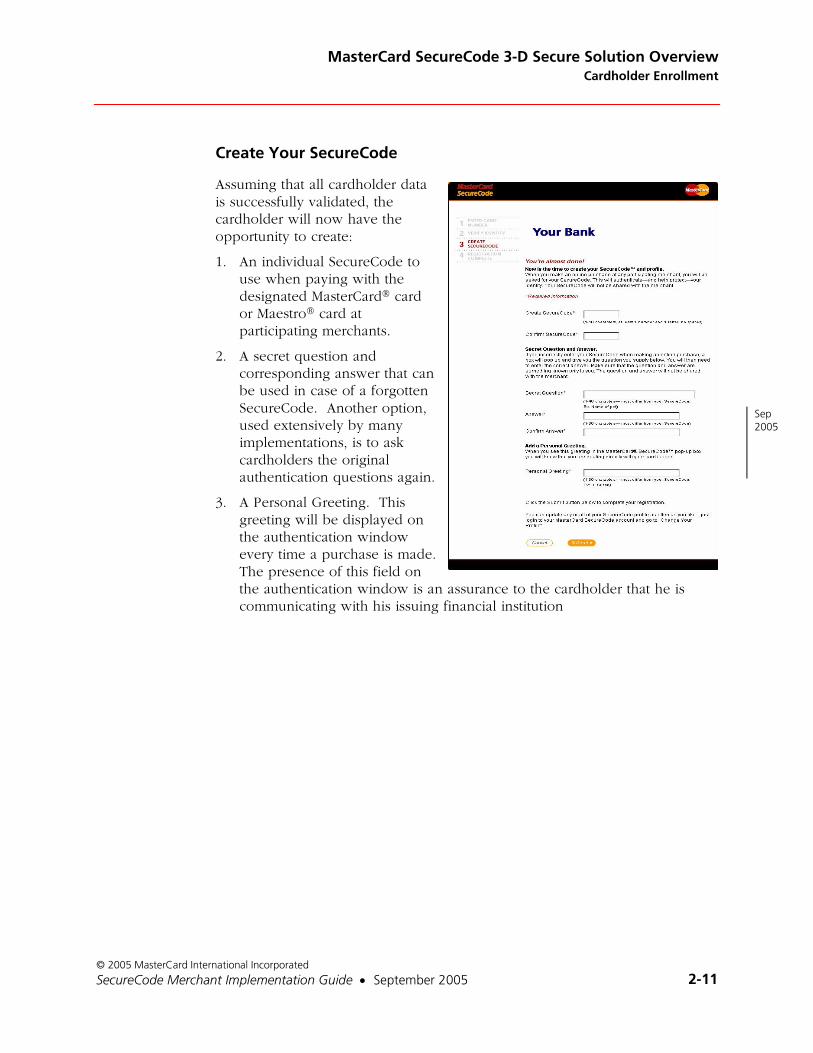

Create Your SecureCode

Assuming that all cardholder data is successfully validated, the cardholder will now have the opportunity to create:

1. An individual SecureCode to use when paying with the designated MasterCard® card or Maestro® card at participating merchants.

2. A secret question and corresponding answer that can be used in case of a forgotten SecureCode. Another option, used extensively by many implementations, is to ask cardholders the original authentication questions again.

3. A Personal Greeting. This greeting will be displayed on the authentication window every time a purchase is made. The presence of this field on the authentication window is an assurance to the cardholder that he is communicating with his issuing financial institution

Sep 2005

MasterCard SecureCode 3-D Secure Solution Overview Cardholder Enrollment

© 2005 MasterCard International Incorporated

2-12 September 2005 • SecureCode Merchant Implementation Guide

Congratulations

The cardholder is now ready to start shopping!

MasterCard SecureCode 3-D Secure Solution OverviewCardholder Authentication

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-13

Cardholder Authentication

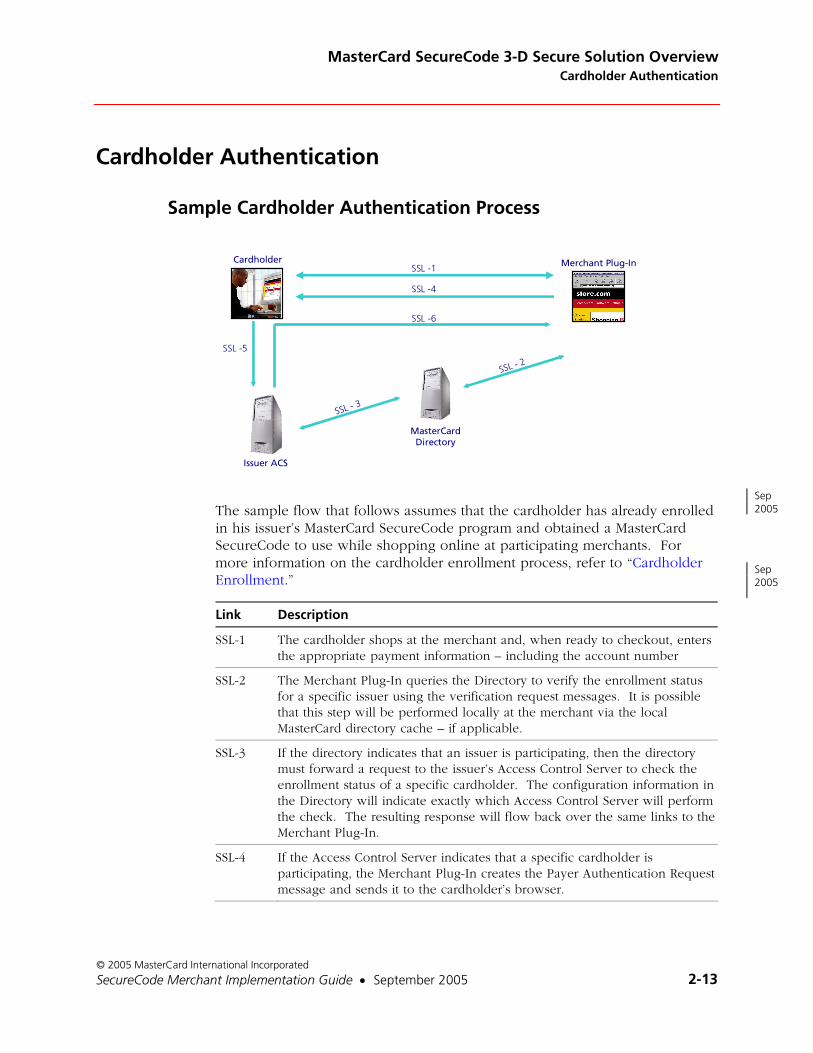

Sample Cardholder Authentication Process

Cardholder Merchant Plug-In

SSL - 2

MasterCardDirectory

SSL -1

Issuer ACS

SSL -6

SSL -4

SSL -5

SSL - 3

The sample flow that follows assumes that the cardholder has already enrolled in his issuer’s MasterCard SecureCode program and obtained a MasterCard SecureCode to use while shopping online at participating merchants. For more information on the cardholder enrollment process, refer to “Cardholder Enrollment.”

Link Description

SSL-1 The cardholder shops at the merchant and, when ready to checkout, enters the appropriate payment information – including the account number

SSL-2 The Merchant Plug-In queries the Directory to verify the enrollment status for a specific issuer using the verification request messages. It is possible that this step will be performed locally at the merchant via the local MasterCard directory cache – if applicable.

SSL-3 If the directory indicates that an issuer is participating, then the directory must forward a request to the issuer’s Access Control Server to check the enrollment status of a specific cardholder. The configuration information in the Directory will indicate exactly which Access Control Server will perform the check. The resulting response will flow back over the same links to the Merchant Plug-In.

SSL-4 If the Access Control Server indicates that a specific cardholder is participating, the Merchant Plug-In creates the Payer Authentication Request message and sends it to the cardholder’s browser.

Sep 2005

Sep 2005

MasterCard SecureCode 3-D Secure Solution Overview Cardholder Authentication

© 2005 MasterCard International Incorporated

2-14 September 2005 • SecureCode Merchant Implementation Guide

Link Description

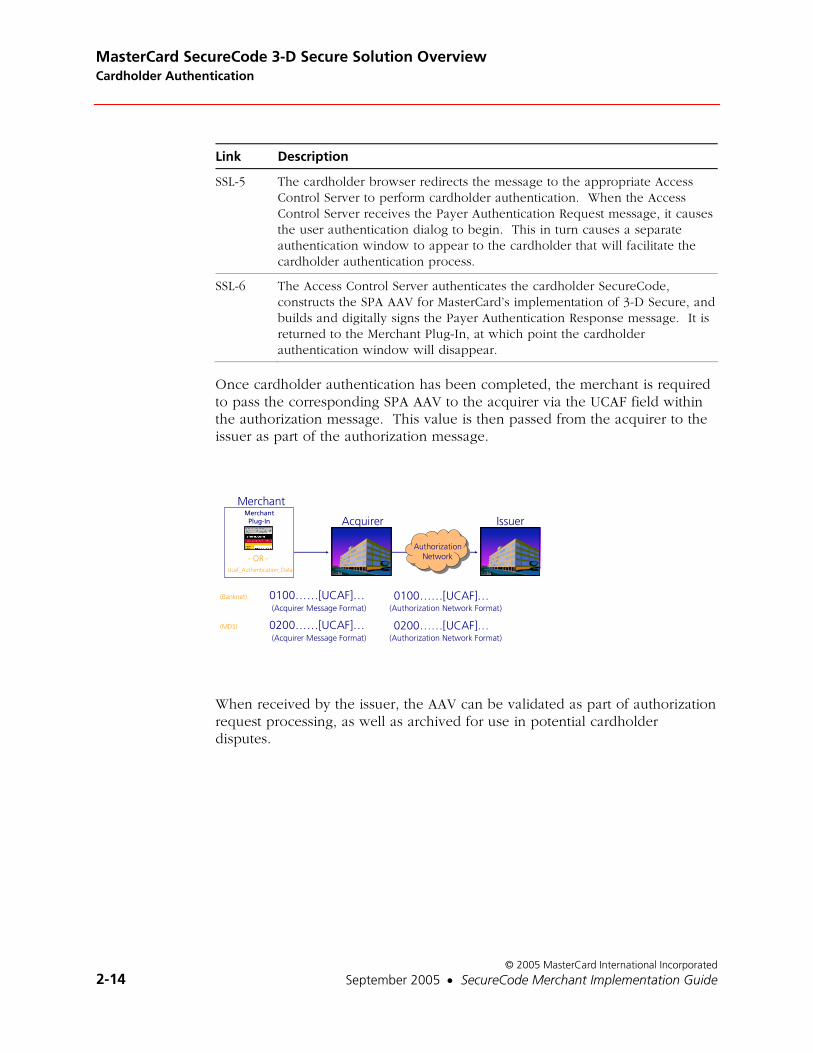

SSL-5 The cardholder browser redirects the message to the appropriate Access Control Server to perform cardholder authentication. When the Access Control Server receives the Payer Authentication Request message, it causes the user authentication dialog to begin. This in turn causes a separate authentication window to appear to the cardholder that will facilitate the cardholder authentication process.

SSL-6 The Access Control Server authenticates the cardholder SecureCode, constructs the SPA AAV for MasterCard’s implementation of 3-D Secure, and builds and digitally signs the Payer Authentication Response message. It is returned to the Merchant Plug-In, at which point the cardholder authentication window will disappear.

Once cardholder authentication has been completed, the merchant is required to pass the corresponding SPA AAV to the acquirer via the UCAF field within the authorization message. This value is then passed from the acquirer to the issuer as part of the authorization message.

Merchant Plug-In

Merchant

Acquirer Issuer

Authorization Network

0100……[UCAF]…(Acquirer Message Format)

0100……[UCAF]…(Authorization Network Format)

Ucaf_Authentication_Data

- OR -

0200……[UCAF]…(Acquirer Message Format)

0200……[UCAF]…(Authorization Network Format)

(Banknet)

(MDS)

When received by the issuer, the AAV can be validated as part of authorization request processing, as well as archived for use in potential cardholder disputes.

MasterCard SecureCode 3-D Secure Solution OverviewCardholder Authentication

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 2-15

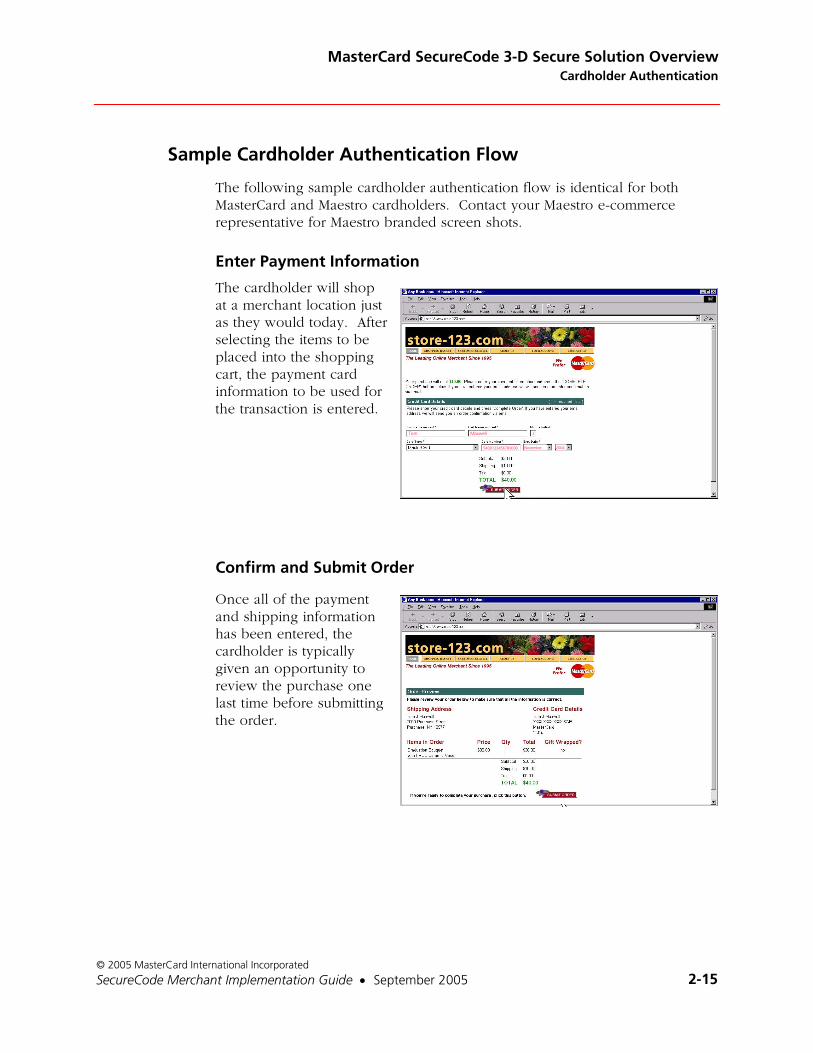

Sample Cardholder Authentication Flow

The following sample cardholder authentication flow is identical for both MasterCard and Maestro cardholders. Contact your Maestro e-commerce representative for Maestro branded screen shots.

Enter Payment Information

The cardholder will shop at a merchant location just as they would today. After selecting the items to be placed into the shopping cart, the payment card information to be used for the transaction is entered.

Confirm and Submit Order

Once all of the payment and shipping information has been entered, the cardholder is typically given an opportunity to review the purchase one last time before submitting the order.

Tom JMaxwell

5400123456789000 November 2004

MasterCard SecureCode 3-D Secure Solution Overview Cardholder Authentication

© 2005 MasterCard International Incorporated

2-16 September 2005 • SecureCode Merchant Implementation Guide

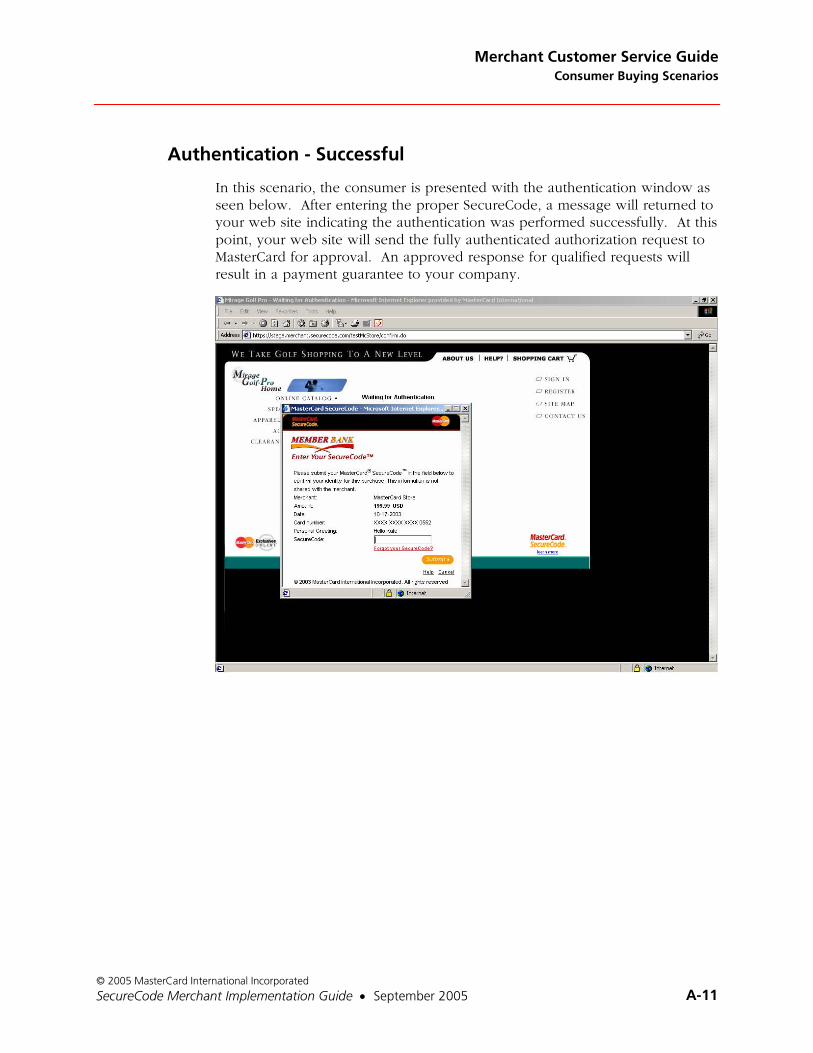

Enter Your SecureCode

Upon submitting the final order, the cardholder will be presented with an authentication window from their MasterCard® card or Maestro® card-issuing bank. At this point, the cardholder will enter his SecureCode value to perform authentication processing.

Purchase Completed

After validation of the cardholder SecureCode by the issuing bank, the authentication window will disappear and the authorization of the payment card will complete as usual.

* * * * * *

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 3-i

3 Merchants This chapter provides a general overview of the various activities and requirements associated with building and maintaining the merchant components required to support MasterCard SecureCode.

Overview .............................................................................................................3-3

Infrastructure .......................................................................................................3-4 Establishment of SecureCode Operating Environment ...............................3-4 Authorization System Enhancements ...........................................................3-4

Passing the AAV in the Authorization Message.....................................3-4 AAV Usage ..............................................................................................3-5 Passing the ECI in the Authorization Message ......................................3-5 Recurring Payments ................................................................................3-6

Maestro Considerations.................................................................................3-6 Account Number Length Requirements.................................................3-6 Authorization Request Timeframes ........................................................3-7 Account in Good Standing .....................................................................3-7

Customization ......................................................................................................3-8 Program Identifier Usage Guidelines ...........................................................3-8 Integrated Support for Merchant Plug-In Processing ..................................3-8 Consumer Message on Payment Page .......................................................3-10 Creation of Cardholder Authentication Window .......................................3-10

Pop-Up Authentication Windows ........................................................3-10 Inline Windows.....................................................................................3-11

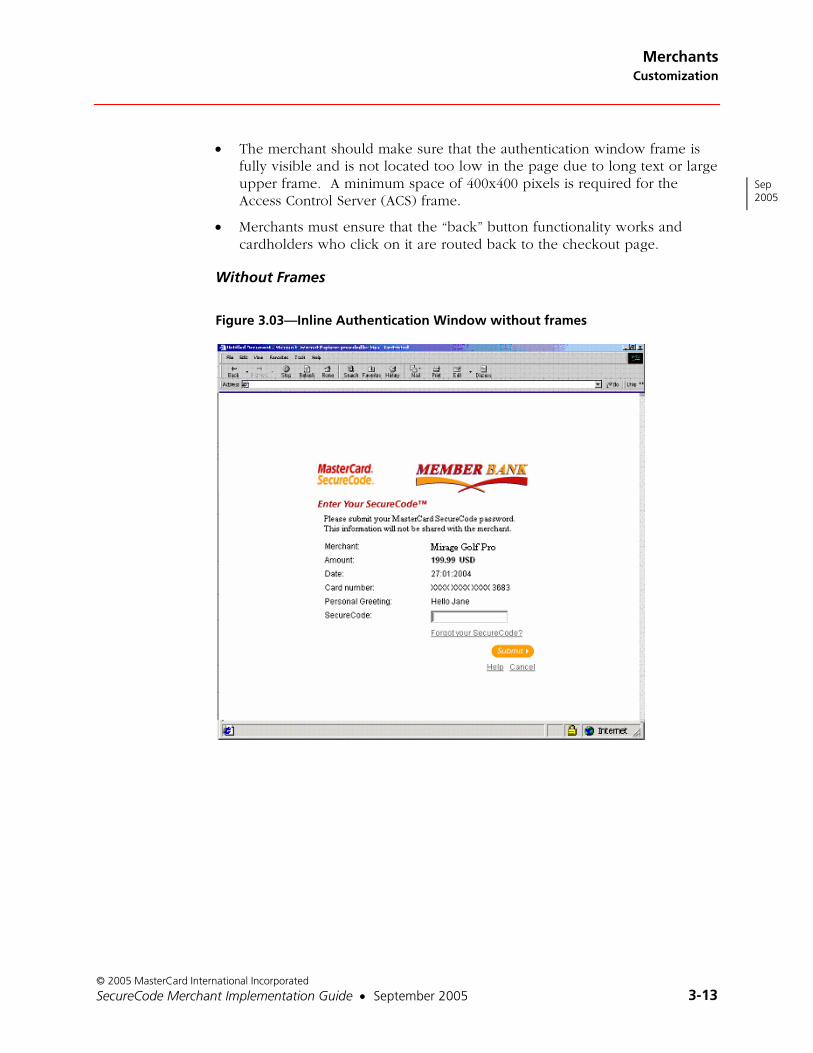

With Frames....................................................................................3-12 Without Frames...............................................................................3-13

TERMURL Field ...........................................................................................3-14 Replay Detection.........................................................................................3-14 Merchant Server Plug-In Configuration......................................................3-14

Initialization of MasterCard Directory URL ..........................................3-14 Initialization of MPI Processing Timers................................................3-14

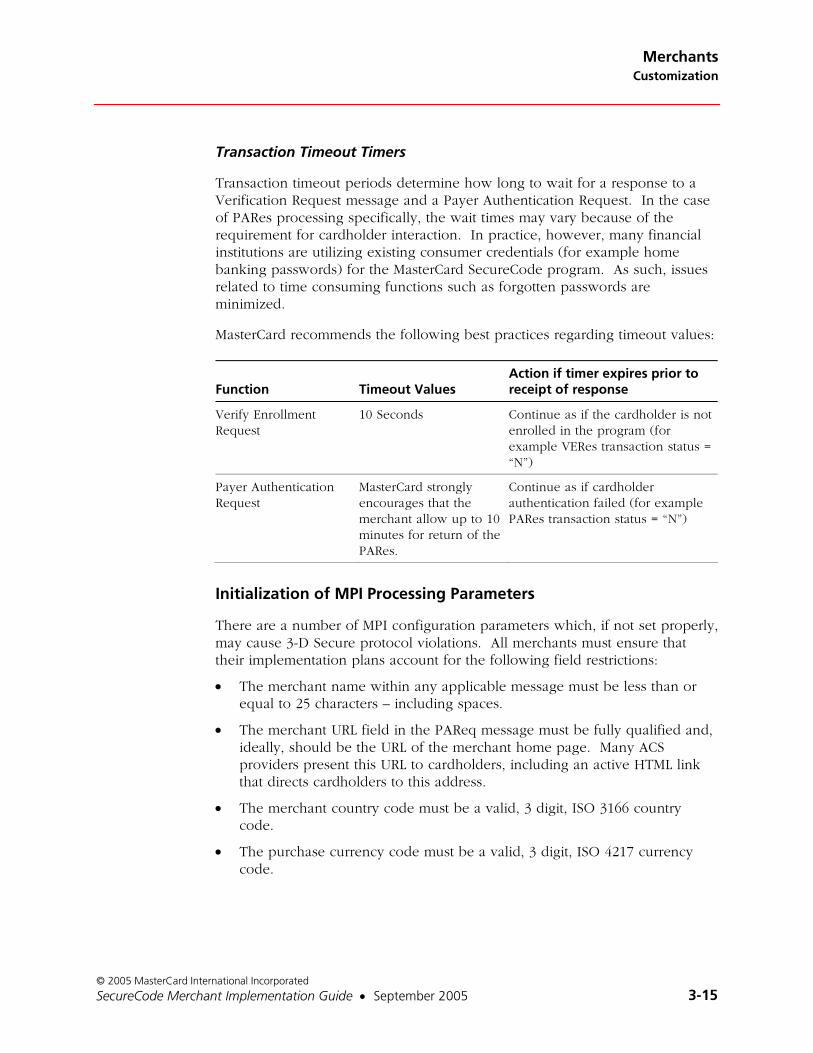

Cache Expiration Timers ................................................................3-14 Transaction Timeout Timers ..........................................................3-15

Initialization of MPI Processing Parameters.........................................3-15 TERMURL ..............................................................................................3-16 “Zero” or Empty Parameters.................................................................3-16

Merchants Overview

© 2005 MasterCard International Incorporated

3-ii September 2005 • SecureCode Merchant Implementation Guide

Operational........................................................................................................3-17 Loading of MasterCard Root Certificates ....................................................3-17 Loading of MasterCard SSL Client Certificate.............................................3-17 MPI Log Monitoring ....................................................................................3-17 MPI Authentication Request/Response Archival........................................3-17

Accountholder Authentication Value (AAV) Processing..................................3-18 Identification of SPA AAV Format in PARes ..............................................3-18 Validation of Payer Authentication Response (PARes) Signature .............3-18

Global Infrastructure Testing Requirements.....................................................3-19

MasterCard SecureCode Participating Merchant Listings .................................3-19

MasterCard Site Data Protection Program ........................................................3-19

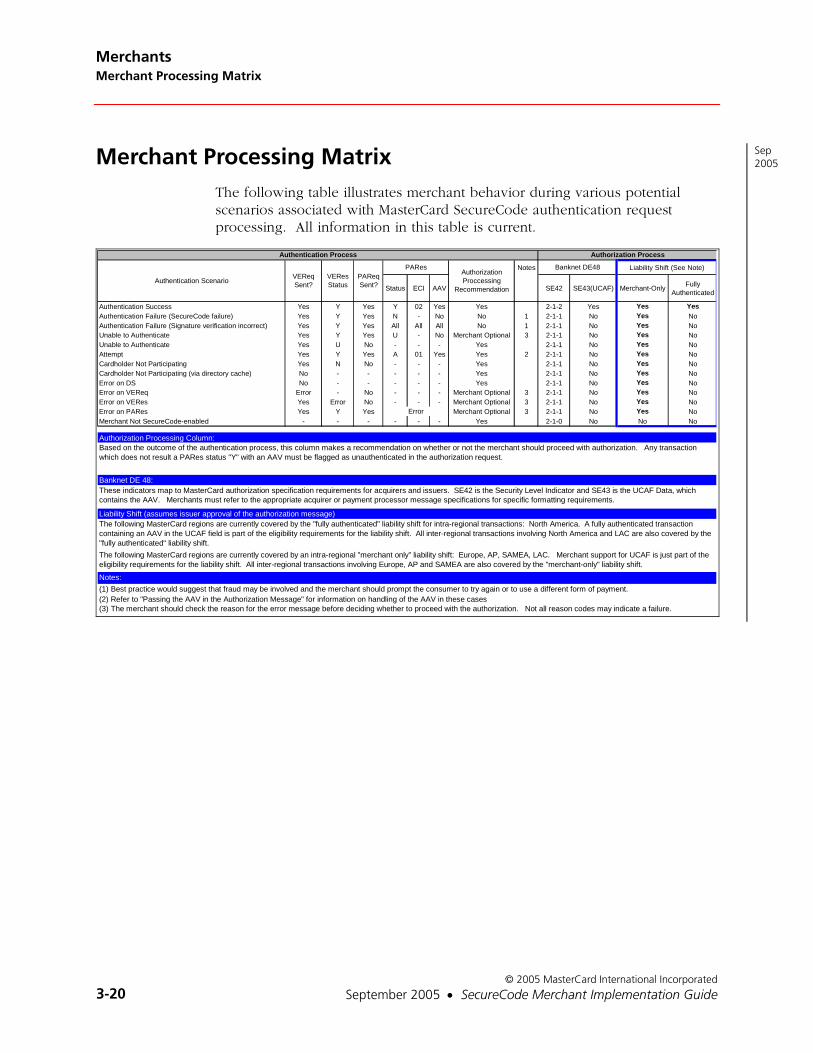

Merchant Processing Matrix ..............................................................................3-20

MerchantsOverview

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 3-3

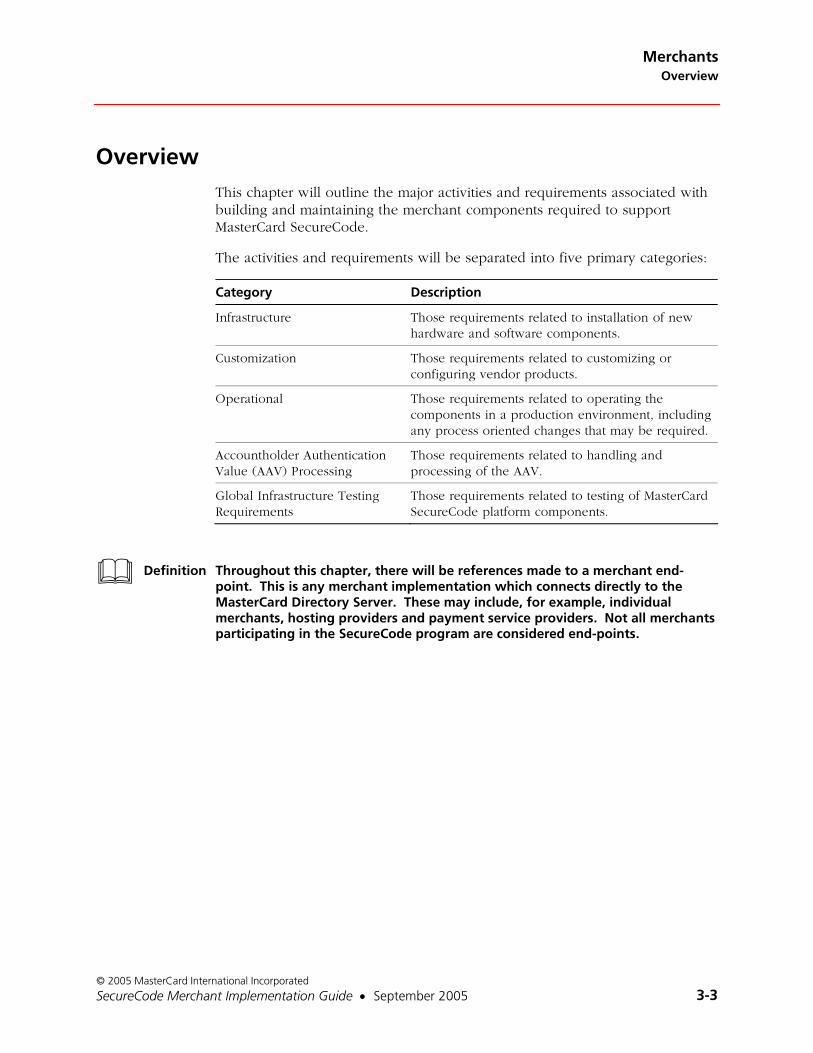

Overview This chapter will outline the major activities and requirements associated with building and maintaining the merchant components required to support MasterCard SecureCode.

The activities and requirements will be separated into five primary categories:

Category Description

Infrastructure Those requirements related to installation of new hardware and software components.

Customization Those requirements related to customizing or configuring vendor products.

Operational Those requirements related to operating the components in a production environment, including any process oriented changes that may be required.

Accountholder Authentication Value (AAV) Processing

Those requirements related to handling and processing of the AAV.

Global Infrastructure Testing Requirements

Those requirements related to testing of MasterCard SecureCode platform components.

Definition Throughout this chapter, there will be references made to a merchant end-point. This is any merchant implementation which connects directly to the MasterCard Directory Server. These may include, for example, individual merchants, hosting providers and payment service providers. Not all merchants participating in the SecureCode program are considered end-points.

Merchants Infrastructure

© 2005 MasterCard International Incorporated

3-4 September 2005 • SecureCode Merchant Implementation Guide

Infrastructure

Establishment of SecureCode Operating Environment

All merchants participating in the MasterCard SecureCode program are required to install or have access to a 3-D Secure v1.0.2 or higher compliant Merchant Server Plug-In. A current list of MasterCard SecureCode compliant vendors can be found at http://www.mastercardmerchant.com/securecode/vendors.html.

Authorization System Enhancements

Passing the AAV in the Authorization Message

MasterCard requires that the SPA AAV returned to the merchant in the Payer Authentication Response (PARes) message be included in all electronic commerce transactions in which cardholder authentication has been performed successfully. Currently this is defined as being when the merchant plug-in detects a value of “Y” in the transaction status field of the PARes message.

Note MasterCard currently utilizes a transaction status of “A” only when the cardholder opts out of enrollment during activation during shopping. For authorizations covered by the merchant-only liability shift, these transactions still meet the liability shift qualifying criteria when authorized by the issuer.

Merchants must ensure that they follow the message formatting requirements of their acquirer when generating UCAF related authorization requests. There are two potential issues to consider:

1. MasterCard requires that the SPA AAV contained in the authorization from the acquirer to the issuer be base64 encoded. Passing this data in binary format is not an option. Merchant plug-in software typically provides the SPA AAV returned in the PARes message already in this format. While some acquirers allow merchants to simply pass the base64 encoded SPA AAV through in the authorization, others have varying requirements. Depending on the specific merchant system and acquirer message formats, it may be necessary for the SPA AAV to be converted between ASCII and EBCDIC encoding prior to it being sent to the acquirer. Any such conversion must only be performed on the SPA AAV after it has been base64 encoded. Any attempt to modify the binary representation of the SPA AAV will result in corruption of the data and the inability of the issuer to perform cardholder authentication verification processing.

Sep 2005

MerchantsInfrastructure

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 3-5

For additional information on base64 encoding, refer to “Accountholder Authentication Value Layout” in appendix B.

2. While an authentication status of “A” is a valid PARes status response and will contain a SPA AAV, it is not considered to be a successful cardholder authentication. MasterCard requires that acquirers ensure that only unauthenticated authorization requests result from authentications with this particular status. This is similar to what would happen in the case of a status of “N” in the VERes message. In these cases, MasterCard requires that the SPA AAV provided with the PARes message be excluded from the authorization message. In some cases, the merchant will be required to exclude this from the authorization message sent to their acquirer. In other cases, the acquirer may require that the merchant send the SPA AAV and then exclude it prior to sending the authorization message to MasterCard.

If there are any questions, merchants should consult with their acquirers for more detailed information.

AAV Usage

The AAV contained within a single authorization request must match the AAV value returned by the issuer for a single associated authentication request. Reuse of an AAV across multiple authorization request messages is only permitted if these authorization requests are part of the same transaction information document (TID), for example; split shipment processing. In all cases, the total transaction amount of the authorization message(s) must not exceed the associated transaction amount contained in the authentication request.

Passing the ECI in the Authorization Message

An electronic commerce indicator (ECI) flag will be present in a PARes message when the status field contains a value of “Y” or “A.” The 3-D Secure protocol defines that this ECI field be determined by each brand. As a result, MasterCard has adopted values that may be different from other participating payment brands.

Most, if not all, acquirers and payment processors have defined the ECI as a required field in their authorization request message formats. Each merchant must ensure that the MasterCard ECI value is properly translated to a valid value as defined in the appropriate acquirer or payment processor authorization message format. Failure to perform the appropriate translation may affect the ability to obtain authorizations successfully.

Sep 2005

Sep 2005

Merchants Infrastructure

© 2005 MasterCard International Incorporated

3-6 September 2005 • SecureCode Merchant Implementation Guide

MasterCard has currently defined two ECI values. The table below indicates the relationship between these values and the status field in the PARes message. Any questions on translating MasterCard defined values for authorization should be directed to your acquirer or payment processor.

PARes Status Field Description

MasterCard ECI Value

Y Cardholder was successfully authenticated 02

A Authentication could not be completed but a proof of authentication attempt was provided. The presence of the AAV from this response in a corresponding authorization message does not constitute a fully authenticated transaction and does not qualify for chargeback protection under the global liability shift as outlined in Section 1.

See “Passing the AAV in the Authorization Message” for more information

01

N Cardholder authentication failed Absent

U Authentication could not be completed due to technical or other problems

Absent

Recurring Payments

Only the initial authorization request for a recurring payment may contain UCAF data. Merchants must not provide UCAF data in any subsequent recurring payment authorizations as these are not considered electronic commerce transactions by MasterCard and are not eligible for participation in the MasterCard SecureCode program.

Maestro cards are not eligible to be used for recurring payments.

Maestro Considerations

The following requirements and activities are specific to merchant support of Maestro® cards as part of the MasterCard SecureCode program. Contact your acquirer for a complete set of Maestro e-commerce acceptance requirements.

Account Number Length Requirements

Maestro merchants must support cardholder account numbers that are from 13 to 19 digits in length.

Sep 2005

Sep 2005

Sep 2005

Sep 2005

Sep 2005

MerchantsInfrastructure

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 3-7

Authorization Request Timeframes

In the case of split shipment, Maestro merchants are required to notify the cardholder if original price is exceeded or the total completion of the order has taken more than 30 days from the time the cardholder placed the order. If the actual amount of the transaction is higher than the original authorization, then a new authorization for the additional amount if required. Maestro recommends that merchants’ advise cardholders at the time of check out that additional delivery fees may result in the case of a split shipment.

Account in Good Standing

Merchants should support the Account in Good Standing Transaction. Refer to “Maestro Considerations” for more information.

Sep 2005

Merchants Customization

© 2005 MasterCard International Incorporated

3-8 September 2005 • SecureCode Merchant Implementation Guide

Customization

Program Identifier Usage Guidelines

Merchants are required to adhere to the applicable usage guidelines as outlined in “MasterCard SecureCode Program Identifier Usage Guidelines.” Proof of adherence must be provided to MasterCard as a condition of successful completion of SecureCode functional testing. MasterCard highly recommends that all screen shots be provided for review as soon as possible in case changes are required.

A copy of the MasterCard SecureCode logo artwork, as well as any updates to the program identifier usage guidelines, is available for download at http://www.mastercardmerchant.com/securecode/artwork.html.

Integrated Support for Merchant Plug-In Processing

The following sample diagram depicts a sample, high level, flow of a transaction through a merchant’s e-commerce site that has integrated support for MasterCard SecureCode.

Sep 2005

MerchantsCustomization

© 2005 MasterCard International Incorporated

SecureCode Merchant Implementation Guide • September 2005 3-9

Figure 3.01—Sample Integrated MasterCard SecureCode Solution

Consumer shops andselects items for

purchaseMerchant prompts cardholder for

payment information

Merchant displays orderconfirmation and the cardholder

clicks the submit button

Merchant displaysreceipt page

Merchant submitsauthenticated

authorization requestwith UCAF data in

the UCAF transportfield.

Merchant submits anunauthenticated

authorization request

MerchantPlug-In checks

if card is incached card

range

Merchant Plug-Ingenerates VEReq tosee if cardholder is

enrolled in the program

ReceivedVERes=Y

within timeoutvalue?

Merchant Plug-Ingenerates PAReq

message to performcardholder

authentication

CardholderAuthentication

Failed?

Yes

No

PARes=YECI=02

PARes=AECI=01 Interrogate

AuthenticationResponse

No

PARes=U Interrogatereason code. Is it

acceptable tocontinue?

No

Yes

Unless otherwiseindicated, this is therecommendeddefault choice

PAReqReceived

within timeoutvalue?

No

PAReqSignatureValidation

Successful?

Yes

Yes

Yes

No

Yes

No

At the completion of the authentication process, the merchant should create an authorization message, which contains the appropriate UCAF related data fields. The associated merchant acquirer or processor will provide message specifications detailing UCAF related data fields within their authorization, clearing and settlement records.

Sep 2005

This diagram indicates merchant best practices regarding SecureCode processing.

Any transaction that does not result in a PARes status “Y” with an AAV and a successful signature validation, must be flagged as unauthenticated if the authorization request process continues.

Merchants Customization

© 2005 MasterCard International Incorporated

3-10 September 2005 • SecureCode Merchant Implementation Guide

Consumer Message on Payment Page

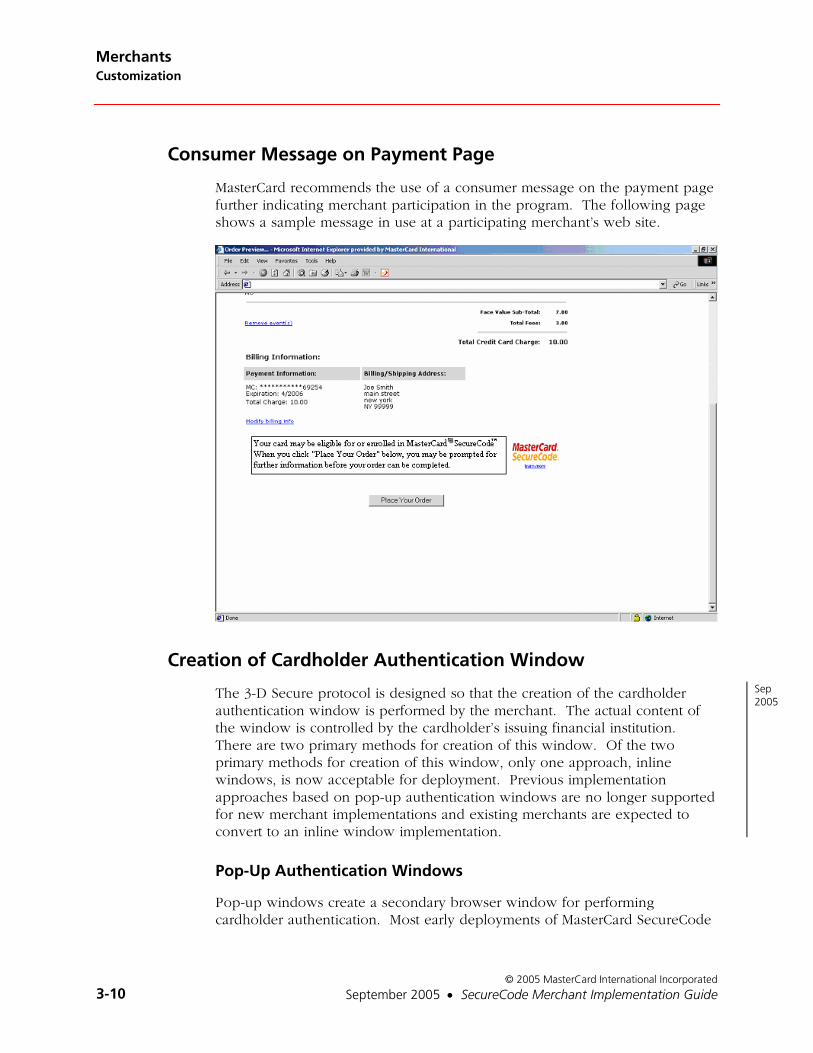

MasterCard recommends the use of a consumer message on the payment page further indicating merchant participation in the program. The following page shows a sample message in use at a participating merchant’s web site.

Creation of Cardholder Authentication Window