about pruprotect

TRANSCRIPT

Introducing PruProtectProtection that goes further

PRUPM11013 UBD XX Sept 2013

FOR ADVISERS

2

Sections

1. Who is PruProtect

2. Trends impacting protection

3. Facts, stats and quotes

4. Personal products

5. Business products

6. Vitality and Vitality Plus

7. Growing your business

Who is PruProtect

4

Make people healthier and enhance and protect their lives

Who is PruProtect

5

• PruProtect is a joint venture between Prudential and leading South African insurer, Discovery

• By combining Prudential’s trusted reputation and Discovery’s history of creative insurance solutions, we’ve developed a new type of Serious Illness Cover

• PruProtect builds on the success of PruHealth in the PMI market

About PruProtect

6

Combined strengths

Financial strength AA

Highly respected brand

Approx 7 million customers in the UK

Prudential Assurance Company has a Standard & Poor's rating of AA, March 2013

Protection and wellness is our core business

7

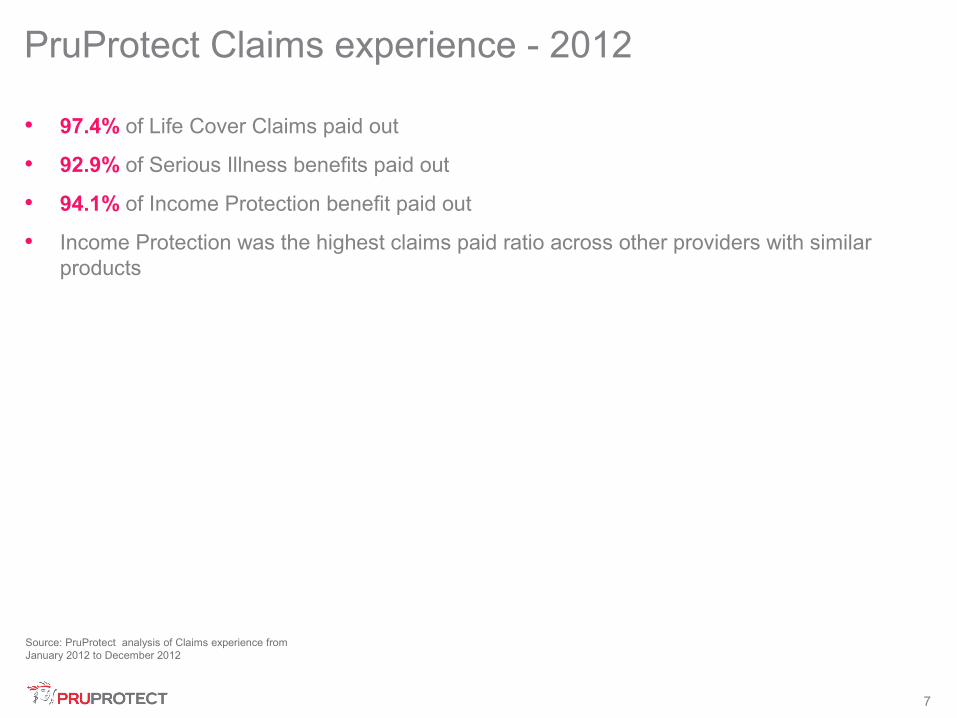

• 97.4% of Life Cover Claims paid out

• 92.9% of Serious Illness benefits paid out

• 94.1% of Income Protection benefit paid out

• Income Protection was the highest claims paid ratio across other providers with similar products

PruProtect Claims experience - 2012

Source: PruProtect analysis of Claims experience from January 2012 to December 2012

8

99% claims paid vs declined claims

• More than £19m were paid out in Serious Illness benefits

• Over £60m Life Cover benefits were paid out

• More than £104m has been paid out to claimants or their estates

• The Global Education Protector currently covers the education costs of 3,378 children under Group Risk

Discovery Life’s 2012 claims experience

Source: Discovery Life Claims experience from January 2012 to December 2012

9

Discovery Life’s 2012 claims experience

Why 1% of received claims were invalid

60% Non-disclosure

24% Policy terms or conditions not met

10% Misrepresentation99% paid

Source: Discovery Life Claims experience from January 2012 to December 2012

See our claims sales aid for more details

6% Suicide within two years

10

Discovery growth: scale and relevanceDiscovery Group membership growth

2001Discovery Life

1997 VitalityDiscovery

2010Standard Life acquisition

2010Discovery Invest

PruProtectThe Vitality Group

2004PruHealth

June 93Discover Health

Launch

Mem

ber

s

2013

Source: Discovery (2013)

2012 Over 6 million

members worldwid

e

11

Continued Growth in the In-force Portfolio – No. of Policies

PruProtect Growth in In-force number of policies

10.3% IFA Market share

12

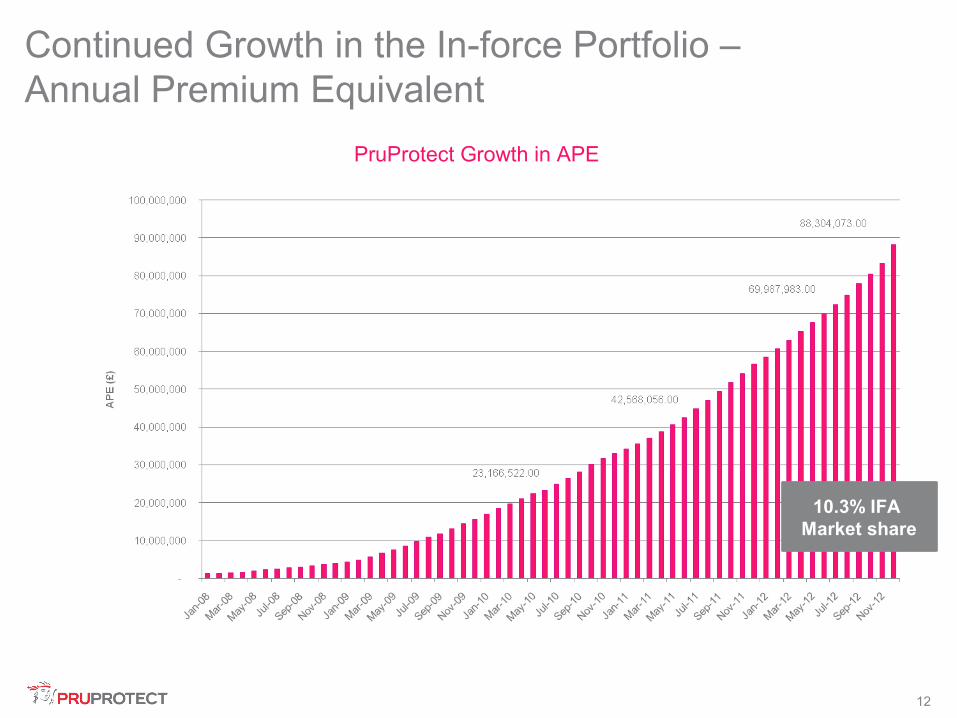

Continued Growth in the In-force Portfolio – Annual Premium Equivalent

PruProtect Growth in APE

10.3% IFA Market share

13

PruProtect’s model – continuing to push the boundaries

Value of benefits

Dynamic pricing

Upfront efficiency

Narrow once-off Broad definitions, multiple claims

Current market

Wellness underpin

14

Our product evolution

15

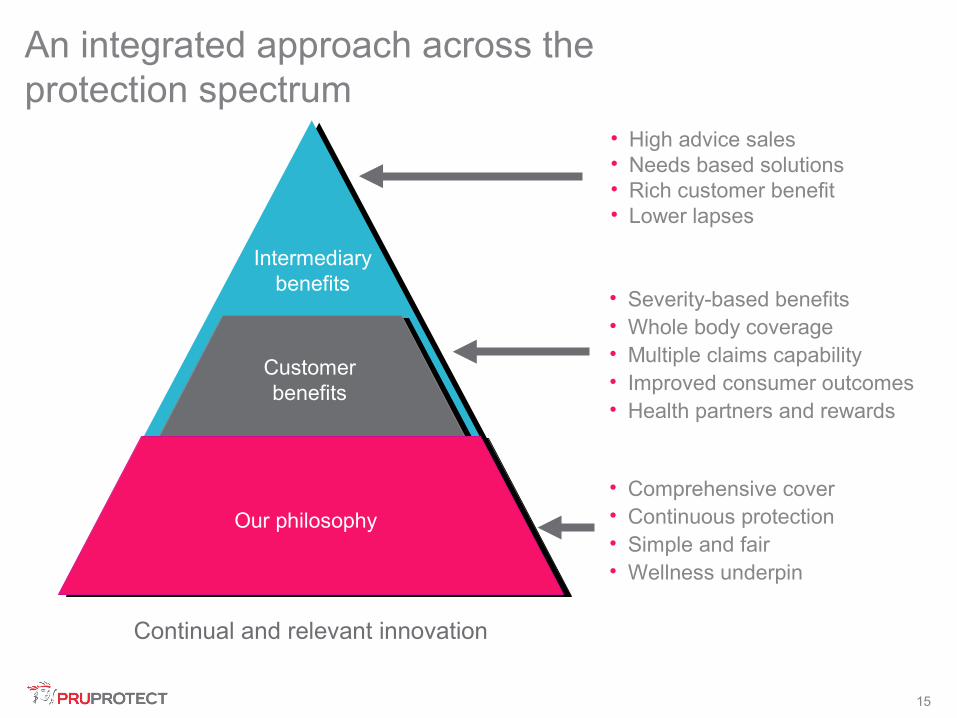

An integrated approach across the protection spectrum

• High advice sales• Needs based solutions• Rich customer benefit• Lower lapses

• Severity-based benefits• Whole body coverage• Multiple claims capability• Improved consumer outcomes• Health partners and rewards

• Comprehensive cover• Continuous protection• Simple and fair• Wellness underpin

Intermediary benefits

Customer benefits

Our philosophy

Continual and relevant innovation

16

We offer a range of premium options to suit your clients’ financial situation

• Have a look at our more affordable Essentials Plan

• Vitality Optimiser – combining all the rewards of Vitality with an upfront discount on our award winning cover

• Your clients can even earn reductions on their premiums by engaging in our Vitality programme

Pricing

Our financial strength and stability

18

• The Prudential Health Holdings Limited group of companies was set up as a joint venture between Prudential Assurance Company and Discovery (a South African insurer).

• The joint venture comprises two businesses (1) a health business PruHealth, and (2) a protection business, PruProtect.

• Originally this was a 50% / 50% joint venture.

• In August 2010, Discovery purchased Standard Life Healthcare for £138m and placed this into the joint venture. At the same time the shareholding changed to Discovery 75% and Prudential 25%.

Group history

19

• The PHHL Group has two health companies, PHIL, which underwrites the ex-Standard Life Healthcare entity, and PHL, which underwrites the original JV PruHealth business.

• PruProtect business is underwritten by PAC.

• PHSL is the services company that employs all staff and holds all contractual arrangements and provides the distribution and administration services for both PruHealth and PruProtect.

Legal entity structure

KeyNote: All entities in the structure, other than Discovery, are UK registered.

Discovery Discovery Holdings LimitedPrudential Prudential PlcDOHL Discovery Offshore Holdings LimitedPAC Prudential Assurance Company LimitedPHHL Prudential Health Holdings LimitedPHIL Prudential Health Insurance Limited (formerly Standard Life Healthcare Ltd)PHL Prudential Health LimitedPHSL Prudential Health Services Limited

Discovery (SA)

Prudential

PACDOHL

PHHL

PHIL

PHL

PHSL

100% 100%

75%25%

100% 100%

100%

20

Group and shareholder performancePrudential and Discovery display both scale and success in their markets overtime.

Prudential Assurance Company (year to 31 December 2012)• Net Assets: £4,740m• Turnover: £14,116m• Profit/(Loss): £376m

Discovery Group (year to 30 June 2013)• Net Assets: £914m (15.22 Rand/GBP closing rate)• Turnover: £1,778m (13.98 Rand/GBP average rate)• Profit/ (Loss): £152m (13.98 Rand/GBP average rate)

Prudential Health Holdings Group (12 months to 30 June 2013)• Net Assets: £207m• Turnover: £339m• Loss before tax: £(11.0m) (stated after one off expense)

21

• PruProtect business is written through Prudential Assurance Company Limited (PAC) in the Prudential Group. As a result, it benefits from the scale, diversity and solvency of PAC.

• The major rating agencies have given the following ratings to PAC:

Financial strength ratings*

Correct as of May 2013

22

• PruProtect’s Life and Serious Illness Cover products are reinsured by Hannover Life Re UK. They have an AA- (very Strong) financial strength rating from S&P and an A+ (Superior) from A.M. Best.

• Gen Re reinsures PruProtect’s Income Protect products. Gen Re is a subsidiary of the Berkshire Hathaway Group and has been rated as AA+ by S&P.

• Swiss Re reinsures the PruProtect over 50s products. Swiss Re is rated AA- by S&P.

• All three of our reinsurance providers are in the world’s top five largest reinsurance groups.

• From outset and on a continuing basis, our providers have participated in our business on financing and quota share bases.

• This approach allows PruProtect to enhance its in-house risk expertise with continuing insight from some of the world’s leading risk professionals.

• Our arrangements also demonstrate the confidence that these market-leading insurance organisations continue to hold in PruProtect’s products and pricing structures.

Reinsurance

23

In addition to the financial strength illustrated by PruProtect, there are two further ways in which customers interests are safeguarded.

The Financial Conduct Authority (FCA)

•The FCA requires insurance companies to complete an Individual Capital Assessment (ICA) every year. The ICA is a worst case scenario test of extreme events which produces a capital reserve figure. PruProtect is required to hold assets/reserves that amount to this figure i.e. to provide an additional margin of protection against significant adverse events

The Financial Service Compensation Scheme (FSCS)

•The FSCS is the compensation fund of last resort for customers of authorised financial services firms. In the event that an insurer becomes insolvent or ceases trading FSCS can pay compensation to the customers of the insolvent insurer.

•Insurance companies are required to pay into the FSCS for purposes of compensating customers in extreme circumstances, who have suffered financial loss following a company going insolvent. All insurance companies pay into this scheme and it would cover up to 90% of a customer's claim amount.

Further financial assurance

24

Awards and recognition

2007-2013 2008 - 2013

2009 - 2013

Peter Chadborn, principle at IFA CBK, said: PruProtect has continued to innovate and challenge old thinking in the market. The industry needs such companies who are not afraid of breaking the mould in order to introduce new ideas.

If you’d like to know more, please speak to your Business Consultant or take a look at pruprotect.co.uk/adviser

Thank you